Deregulating the Volume Limit on Share Repurchases

Abstract

1. Introduction

2. Literature Background

3. Materials and Methods

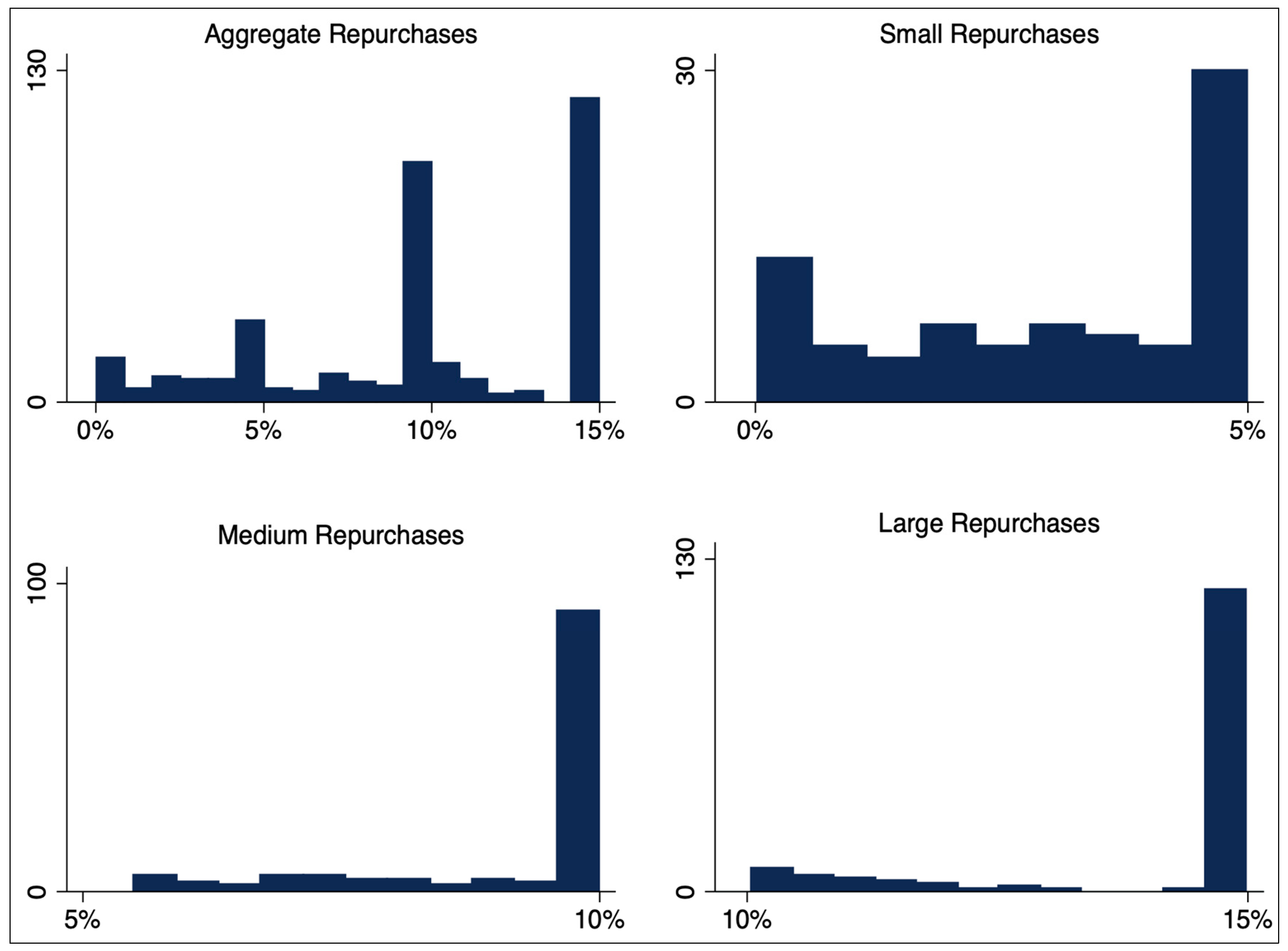

3.1. Repurchase Sample

3.2. Independent Variables

4. Research Objectives and Methodology

4.1. Increasing the Volume Limit

- H10 = Determinants of share repurchases are not dependent on payout size.

- H11 = Determinants of share repurchases are dependent on payout size.

- H20 = Determinants of share repurchases will change if the volume cap is increased.

- H21 = Determinants of share repurchases will not change if the volume cap is increased.In order to empirically test these hypotheses, we undertake a two-stage testing.

4.1.1. Stage I: Computing the Baseline Determinants

4.1.2. Stage II: Predicting the Impact of Liberalization

4.2. Robustness Testing

5. Results

5.1. Univariate Analysis

5.2. Mann–Whitney Rank Sum Testing

5.3. Determinants of Repurchase Size—Stage I

5.4. Increasing the Volume Cap—Stage II

5.5. Robustness Testing

6. Conclusions

Author Contributions

Funding

Informed Consent Statement

Data Availability Statement

Conflicts of Interest

Appendix A

{kind=link}

| Leverage | Firm Size | Cashflow | Dividend | M/B Ratio | EPS | Independence | Tax Ratio | |

|---|---|---|---|---|---|---|---|---|

| Leverage | 1.000 | |||||||

| Firm Size | 0.494 | 1.000 | ||||||

| Cashflow | −0.024 | −0.049 | 1.000 | |||||

| Dividend | 0.070 | 0.098 | 0.070 | 1.000 | ||||

| M/B Ratio | 0.005 | 0.102 | 0.092 | 0.014 | 1.000 | |||

| EPS | −0.137 | −0.145 | −0.564 | −0.370 | −0.016 | 1.000 | ||

| Independence | −0.252 | 0.111 | 0.232 | −0.087 | −0.005 | 0.269 | 1.000 | |

| Tax Ratio | 0.021 | 0.139 | −0.155 | −0.009 | 0.001 | 0.094 | 0.220 | 1.000 |

| Highest + ve | 0.494 | |||||||

| Lowest + ve | 0.001 | |||||||

| Highest − ve | −0.564 | |||||||

| Lowest − ve | −0.005 |

| 1 | We considered the use of Panel Regressions, but since our dataset is an unbalanced panel and encompasses a specific yearly frequency payout, the sample size is not sufficient enough to pursue panel data regressions. |

| 2 | A Pearson’s correlation matrix of the independent variables is provided in the Appendix A. The findings reveal that the correlation coefficients range between −0.564 and 0.494. |

References

- Andreou, Panayiotis C., Ilan Cooper, Ignacio Garcia de Olalla Lopez, and Christodoulos Louca. 2018. Managerial overconfidence and the buyback anomaly. Journal of Empirical Finance 49: 142–56. [Google Scholar] [CrossRef]

- Andriosopoulos, Dimitirs, and Mezaine Lasfer. 2015. The market valuation of share repurchases in Europe. Journal of Banking and Finance 55: 327–39. [Google Scholar] [CrossRef]

- Andriosopoulos, Dimitris, Kostas Andriosopoulos, and Hafiz Hoque. 2013. Information disclosure, CEO overconfidence, and share buyback completion rates. Journal of Banking and Finance 37: 5486–99. [Google Scholar] [CrossRef]

- Baker, H. Kent, Gary E. Powell, and E. Theodore Veit. 2003. Why companies use open-market repurchases: A managerial perspective. Quarterly Review of Economics and Finance 43: 483–504. [Google Scholar] [CrossRef]

- Banerjee, Suman, Mark Humphery-Jenner, and Vikram Nanda. 2018. Does CEO bias escalate repurchase activity? Journal of Banking and Finance 93: 105–26. [Google Scholar] [CrossRef]

- Ben-Rephael, Azi, Jacob Oded, and Avi Wohl. 2014. Do firms buy their stock at bargain prices? Evidence from actual stock repurchase disclosures. Review of Finance 18: 1299–340. [Google Scholar] [CrossRef]

- Billet, Matthew T., and Hui Xue. 2007. The takeover deterrent effect of open market share repurchases. Journal of Finance 62: 1827–50. [Google Scholar] [CrossRef]

- Bonaime, Alice A., Kristine W. Hankins, and Bradford D. Jordan. 2016. The cost of financial flexibility: Evidence from share repurchases. Journal of Corporate Finance 38: 345–62. [Google Scholar] [CrossRef]

- Brav, Alon, John R. Graham, Campbell R. Harvey, and Roni Michaely. 2005. Payout policy in the 21st century. Journal of Financial Economics 77: 483–527. [Google Scholar] [CrossRef]

- Bryan, Bob. 2016. US Companies Have Spent $2 Trillion Doing Something that Has Absolutely No Impact on Their Businesses. Available online: https://www.businessinsider.in/us-companies-have-spent-2-trillion-doing-something-that-has-absolutely-no-impact-on-their-business/articleshow/52769948.cms (accessed on 13 September 2023).

- Burns, Natasha, Brian C. McTier, and Kristina Minnick. 2015. Equity-incentive compensation and payout policy in Europe. Journal of Corporate Finance 30: 85–97. [Google Scholar] [CrossRef]

- Caton, Gary L., Jeremy Goh, Yen Teik Lee, and Scott C. Linn. 2016. Governance and post-repurchase performance. Journal of Corporate Finance 39: 155–73. [Google Scholar] [CrossRef]

- Cesari, Amedeo De, and Neslihan Ozkan. 2015. Executive incentives and payout policy: Empirical evidence from Europe. Journal of Banking and Finance 55: 70–91. [Google Scholar] [CrossRef]

- Chen, Ni-Yun, and Chi-Chun Liu. 2021. The effect of repurchase regulations on actual share reacquisitions and cost of debt. North America Journal of Economics and Finance 55: 101298. [Google Scholar] [CrossRef]

- Cline, Brandon N., and Claudia R. Williamson. 2016. Trust and the regulation of corporate self-dealing. Journal of Corporate Finance 41: 572–90. [Google Scholar] [CrossRef]

- De Cesari, Amedeo, Nicoletta Marinelli, and Rohit Sonika. 2024. The timing of stock repurchases: Do well-connected CEOs help or harm? Journal of Banking and Finance. Forthcoming. [Google Scholar] [CrossRef]

- Denis, David J., and Igor Osobov. 2008. Why do firms pay dividends? International evidence on the determinants of dividend policy. Journal of Financial Economics 89: 62–82. [Google Scholar] [CrossRef]

- Department for Business, Energy and Industrial Strategy. 2018. Government to Research Whether Companies Buy Back Their Own Shares to Inflate Executive Pay. Available online: https://www.gov.uk/government/news/government-to-research-whether-companies-buy-back-their-own-shares-to-inflate-executive-pay (accessed on 13 September 2023).

- Dhanani, Alpa. 2016. Corporate share repurchases in the UK: Perception and practices of corporate managers an investors. Journal of Applied Accounting Research 17: 331–55. [Google Scholar] [CrossRef]

- Dhanani, Alpa, and Roydon Roberts. 2009. Corporate Share Repurchases: The Perceptions and Practices of UK Financial Managers and Corporate Investors. Edinburgh: Institute of Chartered Accountants of Scotland. [Google Scholar]

- Dittmar, Amy K. 2000. Why do firms repurchase stock? Journal of Business 73: 331–55. [Google Scholar] [CrossRef]

- Dittmar, Amy K., and Laura Casares Field. 2015. Can managers time the market? Evidence using repurchase price data. Journal of Financial Economics 115: 261–82. [Google Scholar] [CrossRef]

- D’Mello, Ranjan, and Pervin K. Shroff. 2000. Equity undervaluation and decisions related to repurchase tender offers: An empirical investigation. Journal of Finance 60: 2399–421. [Google Scholar] [CrossRef]

- Edmans, Alex. 2016. Performance-based pay for executives still works. Harvard Business Review. Available online: https://hbr.org/2016/02/performance-based-pay-for-executives-still-works (accessed on 13 September 2023).

- Edmans, Alex. 2017. The case for stock buybacks. Harvard Business Review. Available online: https://hbr.org/2017/09/the-case-for-stock-buybacks (accessed on 1 September 2023).

- Evgeniou, Theodoros, and Theo Vermaelen. 2017. Share buybacks and gender diversity. Journal of Corporate Finance 45: 669–86. [Google Scholar] [CrossRef]

- Evgeniou, Theodoros, Enric Junque de Fortuny, Nick Nassuphis, and Theo Vermaelen. 2018. Volatility and the buyback anomaly. Journal of Corporate Finance 49: 32–53. [Google Scholar] [CrossRef]

- EY. 2023. Challenging 2022 in London Stock Markets as Proceeds Fall by 90%. Available online: https://www.ey.com/en_uk/news/2023/01/challenging-2022-for-london-stock-markets-as-proceeds-fall-by-90 (accessed on 13 September 2023).

- Farrell, Kathleen A., Jin Yu, and Yi Zhang. 2013. What are the characteristics of firms that engage in earnings per share management through share repurchases? Corporate Governance: An International Review 21: 344–50. [Google Scholar] [CrossRef]

- FCA. 2023. FCA proposes to simplify rules to help encourage companies to list in the UK. Available online: https://www.fca.org.uk/news/press-releases/fca-proposes-simplify-rules-help-encourage-companies-list-uk (accessed on 13 September 2023).

- Fenn, George W., and Nellie Liang. 2001. Corporate payout policy and managerial stock incentives. Journal of Financial Economics 60: 45–72. [Google Scholar] [CrossRef]

- Franks, Julian, Colin Mayer, and Luc Renneboog. 2001. Who disciplines management in poorly performing companies? Journal of Financial Intermediation 10: 209–48. [Google Scholar] [CrossRef]

- Fried, Jesse M. 2014. Insider trading via the corporation. University of Pennsylvania Law Review 162: 801–39. [Google Scholar] [CrossRef]

- Geiler, Philipp, and Luc Renneboog. 2015. Taxes, earnings payout and payout channel choice. Journal of International Financial Markets Institutions and Money 37: 178–203. [Google Scholar] [CrossRef]

- Goodacre, Harry. 2023. The Increasing Popularity of Share Buybacks Outside the US. Available online: https://www.schroders.com/en-gb/uk/intermediary/insights/the-increasing-popularity-of-share-buybacks-outside-the-us (accessed on 13 September 2023).

- Guay, Wayne, and Jarrad Harford. 2000. The cash-flow permanence and information content of dividend increases versus repurchase. Journal of Financial Economics 57: 385–415. [Google Scholar] [CrossRef]

- Ikenberry, David, Josef Lakonishok, and Theo Vermaelen. 1995. Market underreaction to open market share repurchases. Journal of Financial Economics 39: 181–208. [Google Scholar] [CrossRef]

- Jacob, Marcus, and Martin Jacob. 2013. Taxation, dividends, and share repurchase: Taking evidence global. Journal of Financial and Quantitative Analysis 48: 1241–69. [Google Scholar] [CrossRef]

- Jensen, Michael C. 1986. Agency costs of free cash flow, corporate finance, and takeovers. American Economic Review 76: 323–29. [Google Scholar]

- Jiang, Zhan, Kenneth A. Kim, Erik Lie, and Sean Yang. 2013. Share repurchases, catering and dividend substitution. Journal of Corporate Finance 21: 36–50. [Google Scholar] [CrossRef]

- Ji, Philip Inyeob. 2016. Is corporate payout taxation a long run phenomenon? Evidence from international data. North American Journal of Economics and Finance 36: 84–100. [Google Scholar] [CrossRef]

- John, Kose, Anzhela Knyazeva, and Diana Knyazeva. 2015. Governance and Payout Precommitment. Journal of Corporate Finance 33: 101–17. [Google Scholar] [CrossRef]

- Korkeamaki, Timo, Eva Lilijeblom, and Daniel Pasternack. 2010. Tax reform and payout policy: Do shareholder clienteles or payout policy adjust? Journal of Corporate Finance 16: 572–87. [Google Scholar] [CrossRef]

- Lee, Bong Soo, and Jungwan Suh. 2011. Cash holdings and share repurchases: International evidence. Journal of Corporate Finance 17: 1306–29. [Google Scholar] [CrossRef]

- Lee, Chun I., Demissew Diro Ejara, and Kimberly C. Gleason. 2010. An empirical analysis of European stock repurchases. Journal of Multinational Financial Management 20: 114–25. [Google Scholar] [CrossRef]

- Leng, Fei, and Gregory Noronha. 2013. Information and long-term stock performance following open-market share repurchases. The Financial Review 48: 461–87. [Google Scholar] [CrossRef]

- Lilienfeld-Toal, Ulf Von, and Stefan Ruenzi. 2014. CEO ownership, stock market performance and managerial discretion. Journal of Finance 69: 1013–50. [Google Scholar] [CrossRef]

- Lin, Ji-Chai, Clifford P. Stephens, and YiLin Wu. 2014. Limited attention, share repurchases, and takeover risk. Journal of Banking and Finance 2014: 283–301. [Google Scholar] [CrossRef]

- Lin, Tsui-Jung, Yi-Pei Chen, and Han-Fang Tsai. 2017. The relationship among information asymmetry, dividend policy and ownership structure. Finance Research Letters 20: 1–12. [Google Scholar] [CrossRef]

- Muirhead, Calum. 2023. Three City Brokers Warn that Weak Activity in the Markets has Hit their Business. Available online: https://www.thisismoney.co.uk/money/markets/article-11934167/Brokers-battering-downturn-hits-activity (accessed on 13 September 2023).

- O’Dwyer, Michael. 2024. UK Announced Biggest Overhaul of Listing Regime in Decades. Available online: https://www.ft.com/content/a990dfd6-ef99-40ca-b382-276f9f811d00 (accessed on 21 August 2024).

- Oswald, Dennis, and Steven Young. 2004. What role taxes and regulation? A second look at open market share buyback activity in the UK. Journal of Business, Finance and Accounting 31: 257–92. [Google Scholar] [CrossRef]

- Ota, Koji, Hironori Kawase, and David Lau. 2019. Does reputation matter? Evidence from share repurchases. Journal of Corporate Finance 58: 287–306. [Google Scholar] [CrossRef]

- Ozkan, Neslihan. 2007. Do corporate governance mechanisms influence CEO compensation? An empirical investigation of UK Companies. Journal of Multinational Financial Management 17: 349–64. [Google Scholar] [CrossRef]

- Padgett, Carol, and Zhiqi Wang. 2007. Short-Term Returns of UK Share Buyback Activity. Reading: University of Reading, pp. 1–30. Available online: https://core.ac.uk/download/pdf/6565339.pdf (accessed on 13 July 2024).

- PwC. 2019. Share repurchases, executive pay and Investment. BEIS Research Paper 2019/911. Available online: https://www.pwc.co.uk/economic-services/documents/share-repurchases-executive-pay-investment.pdf (accessed on 14 September 2023).

- Rau, P. Raghavendra, and Theo Vermaelen. 2002. Regulation, taxes and share repurchases in the United Kingdom. Journal of Business 75: 245–82. [Google Scholar] [CrossRef]

- Renneboog, Luc, and Grzegorz Trojanowski. 2011. Patterns in payout policy and payout channel choice. Journal of Banking and Finance 35: 1477–90. [Google Scholar] [CrossRef]

- SEC. 2023. Share Repurchase Disclosure Modernization. Available online: https://www.sec.gov/corpfin/secg-share-repurchase-disclosure-modernization (accessed on 14 September 2023).

- Sonika, Rohit, Nicholas F. Carline, and Mark B. Shackleton. 2014. The option and decision to repurchase stock. Financial Management 43: 833–55. [Google Scholar] [CrossRef]

- Wang, Chuan-San, Norman Strong, Samuel Tung, and Steve Lin. 2009. Share repurchases, the clustering problem, and the free cash flow hypothesis. Financial Management 38: 487–505. [Google Scholar] [CrossRef]

- Wang, Zigan, Qie Ellie Yin, and Luping Yu. 2024. Do share repurchases facilitate movement toward target capital structure? International evidence. Journal of Empirical Finance 77: 101498. [Google Scholar] [CrossRef]

- Willems, Michiel. 2021. Cash Holdings: UK Corporates’ £109bn Warchest Increasingly a Rival to Private Equity in M&A. Available online: https://www.cityam.com/cash-holdings-uk-corporates-109bn-warchest-increasingly-a-rival-to-private-equity-in-ma/ (accessed on 13 September 2023).

- Yook, Ken C. 2010. Long run stock-performance following stock repurchases. Quarterly Review of Economics and Finance 50: 323–31. [Google Scholar] [CrossRef]

| Repurchases | N (%) | Mean | Min | 5th % | Median | 95th % | Max |

|---|---|---|---|---|---|---|---|

| Aggregate | 360 (100) | 0.098 | 0.001 | 0.012 | 0.100 | 0.149 | 0.149 |

| Small | 82 (23) | 0.030 | 0.001 | 0.001 | 0.032 | 0.050 | 0.050 |

| Medium | 128 (36) | 0.092 | 0.055 | 0.060 | 0.100 | 0.100 | 0.100 |

| Large | 150 (41) | 0.141 | 0.100 | 0.103 | 0.149 | 0.149 | 0.149 |

| Variable | Description | Expected Influence |

|---|---|---|

| Leverage | The ratio of the total value of assets to the total value of liabilities | Negative |

| Firm Size | The natural logarithm of the £ mn total value of assets | Positive |

| Cashflow | The ratio of the operating profit before depreciation and taxation to the total value of assets | Positive |

| Dividend | The proportion of net profit distributed as ordinary dividends | Positive |

| M/B Ratio | The ratio of the firm’s market value to its book value | Negative |

| EPS | A binary variable, which takes the value ‘1’ if the annual earnings are negative | Positive |

| Independence | The proportion of board members that are independent directors | Positive |

| Tax Ratio | The ratio of the effective higher dividend tax rate to the higher capital gains tax rate | Positive |

| Panel I: Preference-Pts Allotment | |||

| Positive Preference (+) | Points (pts) | Negative Preference (−) | Points (pts) |

| (+) 1st | 6 | Equivalent Ratio | 0 |

| (+) 2nd | 5 | (−) 1st | −1 |

| (+) 3rd | 4 | (−) 2nd | −2 |

| (+) 4th | 3 | (−) 3rd | −3 |

| (+) 5th | 2 | (−) 4th | −4 |

| (+) 6th | 1 | (−) 5th | −5 |

| Equivalent Ratio | 0 | (−) 6th | −6 |

| Panel II: List of Pts Multiple Factors | |||

| Repurchase Subset | Pts Multiple Factor | ||

| Small Repurchases | 0.23 | ||

| Medium Repurchases | 0.36 | ||

| Large Repurchases | 0.41 | ||

| N (%) | Mean | Min | 5th % | Median | 95th % | Max | |

|---|---|---|---|---|---|---|---|

| Leverage | |||||||

| All | 360 (100) | 0.402 | 0.002 | 0.037 | 0.396 | 0.883 | 1.052 |

| Small | 82 (23) | 0.389 | 0.005 | 0.037 | 0.373 | 0.840 | 0.959 |

| Medium | 128 (36) | 0.453 | 0.023 | 0.108 | 0.421 | 0.950 | 0.956 |

| Large | 150 (41) | 0.365 | 0.002 | 0.023 | 0.343 | 0.907 | 1.052 |

| Firm Size | |||||||

| All | 360 (100) | 12.945 | 4.057 | 9.091 | 12.813 | 17.260 | 19.520 |

| Small | 82 (23) | 12.784 | 7.530 | 8.974 | 12.895 | 17.237 | 18.661 |

| Medium | 128 (36) | 13.486 | 8.143 | 9.565 | 13.613 | 17.241 | 19.520 |

| Large | 150 (41) | 12.570 | 4.057 | 9.067 | 12.313 | 17.278 | 19.273 |

| Cashflow | |||||||

| All | 360 (100) | 0.105 | −1.281 | −0.119 | 0.100 | 0.348 | 0.976 |

| Small | 82 (23) | 0.131 | −0.427 | 0.009 | 0.107 | 0.415 | 0.976 |

| Medium | 128 (36) | 0.113 | −1.281 | −0.015 | 0.113 | 0.316 | 0.580 |

| Large | 150 (41) | 0.085 | −0.806 | −0.154 | 0.072 | 0.349 | 0.585 |

| Dividend | |||||||

| All | 360 (100) | 0.416 | −6.979 | −0.177 | 0.355 | 1.373 | 9.112 |

| Small | 82 (23) | 0.569 | 0.000 | 0.000 | 0.412 | 1.77 | 3.847 |

| Medium | 128 (36) | 0.389 | −2.537 | −0.015 | 0.383 | 0.906 | 2.571 |

| Large | 150 (41) | 0.356 | −6.979 | −0.419 | 0.293 | 1.455 | 9.112 |

| M/B Ratio | |||||||

| All | 360 (100) | 2.248 | −112.243 | 0.378 | 1.571 | 8.090 | 27.327 |

| Small | 82 (23) | 3.660 | 0.115 | 0.527 | 1.795 | 15.234 | 27.327 |

| Medium | 128 (36) | 2.566 | 0.125 | 0.432 | 1.981 | 8.044 | 19.765 |

| Large | 150 (41) | 1.204 | −112.243 | 0.153 | 1.316 | 5.440 | 18.544 |

| EPS | |||||||

| All | 360 (100) | 0.125 | 0.000 | 0.000 | 0.000 | 1.000 | 1.000 |

| Small | 82 (23) | 0.036 | 0.000 | 0.000 | 0.000 | 0.000 | 1.000 |

| Medium | 128 (36) | 0.078 | 0.000 | 0.000 | 0.000 | 1.000 | 1.000 |

| Large | 150 (41) | 0.213 | 0.000 | 0.000 | 0.000 | 1.000 | 1.000 |

| Independence | |||||||

| All | 360 (100) | 0.551 | 0.054 | 0.245 | 0.500 | 1.000 | 1.000 |

| Small | 82 (23) | 0.539 | 0.054 | 0.200 | 0.483 | 1.000 | 1.000 |

| Medium | 128 (36) | 0.501 | 0.200 | 0.277 | 0.500 | 0.800 | 1.000 |

| Large | 150 (41) | 0.599 | 0.166 | 0.285 | 0.545 | 1.000 | 1.000 |

| Tax Ratio | |||||||

| All | 360 (100) | 0.702 | 0.375 | 0.375 | 0.625 | 1.092 | 1.700 |

| Small | 82 (23) | 0.665 | 0.375 | 0.375 | 0.625 | 1.092 | 1.700 |

| Medium | 128 (36) | 0.712 | 0.375 | 0.375 | 0.625 | 1.092 | 1.700 |

| Large | 150 (41) | 0.713 | 0.375 | 0.375 | 0.625 | 1.700 | 1.700 |

| Small Repurchases vs. Medium Repurchases | Small Repurchases vs. Large Repurchases | Medium Repurchases vs. Large Repurchases | |

|---|---|---|---|

| Leverage | −2.111 ** (0.034) | 0.919 (0.358) | 3.344 *** (0.001) |

| Firm Size | −1.844 * (0.065) | 0.473 (0.636) | 2.859 *** (0.004) |

| Cashflow | −0.175 (0.861) | 2.218 ** (0.026) | 2.596 *** (0.009) |

| Dividend | 1.441 (0.149) | 4.035 *** (0.001) | 3.091 *** (0.002) |

| M/B Ratio | −0.239 (0.811) | 2.376 ** (0.017) | 3.398 *** (0.001) |

| EPS | −1.216 (0.224) | −3.588 *** (0.001) | −3.132 *** (0.001) |

| Independence | 0.324 (0.745) | −1.875 * (0.060) | −2.911 *** (0.003) |

| Small Repurchases | Medium Repurchases | Large Repurchases | |

|---|---|---|---|

| Leverage | 0.031 ** (2.29) | 0.011 (0.75) | −0.004 (−0.37) |

| Firm Size | 0.0001 (0.13) | −0.0001 (−0.08) | −0.001 (−1.09) |

| Cashflow | 0.037 ** (2.00) | 0.041 ** (1.97) | 0.021 (1.16) |

| Dividend | −0.001 (−0.39) | −0.0001 (−0.04) | 0.003 (1.23) |

| M/B Ratio | −0.003 *** (−4.35) | −0.003 *** (−3.57) | −0.0008 ** (−2.27) |

| EPS | 0.045 *** (3.04) | 0.050 *** (3.75) | 0.034 *** (3.37) |

| Independence | −0.002 (−0.19) | 0.011 (0.82) | 0.035 *** (2.75) |

| Tax Ratio | 0.009 (0.89) | 0.011 (0.98) | −0.009 (−0.89) |

| Constant | 0.057 *** (3.84) | 0.077 *** (4.47) | 0.095 *** (5.80) |

| McFadden R2 | −0.360 | −2.434 | −0.172 |

| LR Chi2 | 32.21 | 36.27 | 38.13 |

| Prob > Chi2 | 0.000 | 0.000 | 0.000 |

| Left Censored | 0 | 82 | 210 |

| Uncensored | 82 | 128 | 150 |

| Right Censored | 278 | 150 | 0 |

| Total Obs. | 360 | 360 | 360 |

| Posited Liberalized Volume Cap | ||||||

| Panel I: Small Repurchases | ||||||

| 17.50% | 20% | 22.50% | 25% | 27.50% | 30% | |

| Leverage | 0.019 * (1.82) | 0.029 ** (2.04) | 0.031 ** (1.96) | 0.031 * (1.94) | 0.031 * (1.94) | 0.031 * (1.94) |

| Firm Size | 0.0001 (0.13) | 0.0001 (0.13) | 0.0001 (0.13) | 0.0001 (0.13) | 0.0001 (0.13) | 0.0001 (0.13) |

| Cashflow | 0.024 * (1.81) | 0.036 * (1.86) | 0.038 * (1.77) | 0.038 * (1.76) | 0.038 * (1.75) | 0.038 * (1.75) |

| Dividend | −0.0007 (−0.39) | −0.001 (−0.39) | −0.001 (−0.39) | −0.001 (−0.39) | −0.001 (−0.39) | −0.001 (−0.39) |

| M/B Ratio | −0.001 ** (−2.36) | −0.002 *** (−3.08) | −0.003 *** (−2.86) | −0.003 *** (−2.81) | −0.003 *** (−2.80) | −0.003 *** (−2.80) |

| EPS | 0.028 *** (2.75) | 0.043 *** (2.65) | 0.045 *** (2.38) | 0.046 ** (2.33) | 0.046 ** (2.32) | 0.046 ** (2.32) |

| Independence | −0.001 (−0.19) | −0.002 (−0.19) | −0.002 (−0.19) | −0.002 (−0.19) | −0.002 (−0.19) | −0.002 (−0.19) |

| Tax Ratio | 0.005 (0.84) | 0.008 (0.87) | 0.009 (0.86) | 0.009 (0.86) | 0.009 (0.86) | 0.009 (0.86) |

| Panel II: Medium Repurchases | ||||||

| Leverage | 0.033 (0.75) | 0.049 (0.75) | 0.056 (0.75) | 0.059 (0.75) | 0.059 (0.75) | 0.060 (0.75) |

| Firm Size | −0.0003 (−0.08) | −0.0004 (−0.08) | −0.0005 (−0.08) | −0.0005 (−0.08) | −0.0005 (−0.08) | −0.0005 (−0.08) |

| Cashflow | 0.118 * (1.89) | 0.175 ** (1.98) | 0.201 ** (1.99) | 0.211 ** (1.98) | 0.214 ** (1.97) | 0.215 ** (1.97) |

| Dividend | −0.0003 (−0.04) | −0.0006 (−0.04) | −0.0007 (−0.04) | −0.0007 (−0.04) | −0.0007 (−0.04) | −0.0007 (−0.04) |

| M/B Ratio | −0.010 *** (−3.23) | −0.014 *** (−3.64) | −0.016 *** (−3.70) | −0.017 *** (−3.68) | −0.018 *** (−3.66) | −0.018 *** (−3.66) |

| EPS | 0.144 *** (3.21) | 0.212 *** (3.77) | 0.243 *** (3.83) | 0.256 *** (3.77) | 0.259 *** (3.73) | 0.260 *** (3.71) |

| Independence | 0.033 (0.82) | 0.049 (0.82) | 0.057 (0.82) | 0.059 (0.82) | 0.060 (0.82) | 0.061 (0.82) |

| Tax Ratio | 0.032 (0.97) | 0.047 (0.98) | 0.054 (0.98) | 0.057 (0.98) | 0.058 (0.98) | 0.058 (0.98) |

| Panel III: Large Repurchases | ||||||

| Leverage | −0.031 (−0.37) | −0.037 (−0.37) | −0.039 (−0.37) | −0.040 (−0.37) | −0.040 (−0.37) | −0.040 (−0.37) |

| Firm Size | −0.009 (−1.10) | −0.010 (−1.10) | −0.011 (−1.10) | −0.011 (−1.10) | −0.011 (−1.10) | −0.011 (−1.10) |

| Cashflow | 0.142 (1.16) | 0.169 (1.16) | 0.178 (1.16) | 0.182 (1.16) | 0.182 (1.16) | 0.182 (1.16) |

| Dividend | 0.021 (1.24) | 0.025 (1.24) | 0.027 (1.24) | 0.027 (1.24) | 0.027 (1.24) | 0.027 (1.24) |

| M/B Ratio | −0.005 ** (−2.26) | −0.006 ** (−2.29) | −0.006 ** (−2.30) | −0.006 ** (−2.30) | −0.006 ** (−2.29) | −0.006 ** (−2.29) |

| EPS | 0.232 *** (3.45) | 0.276 *** (3.48) | 0.292 *** (3.48) | 0.297 *** (3.47) | 0.298 *** (3.47) | 0.298 *** (3.47) |

| Independence | 0.237 *** (2.81) | 0.283 *** (2.82) | 0.299 *** (2.81) | 0.304 *** (2.82) | 0.305 *** (2.82) | 0.306 *** (2.82) |

| Tax Ratio | −0.060 (−0.89) | −0.071 (−0.89) | −0.075 (−0.89) | −0.076 (−0.89) | −0.077 (−0.89) | −0.077 (−0.89) |

| Panel I: Small Repurchases | |||||||||

| M/B Ratio/EPS | M/B Ratio/Leverage | M/B Ratio/Cashflow | |||||||

| Baseline Ratio: 6.70% | Baseline Ratio: 9.70% | Baseline Ratio: 8.10% | |||||||

| Ratio | Pref | Pts | Ratio | Pref | Pts | Ratio | Pref | Pts | |

| 17.50% | 3.57% | (−) 4th | −4 | 5.26% | (−) 3rd | −3 | 4.17% | (−) 3rd | −3 |

| 20% | 4.65% | (−) 3rd | −3 | 6.90% | (−) 2nd | −2 | 5.56% | (−) 2nd | −2 |

| 22.50% | 6.67% | 1st | 0 | 9.68% | 1st | 0 | 7.89% | (−) 1st | −1 |

| 25% | 6.52% | (−) 2nd | −2 | 9.68% | 1st | 0 | 7.89% | (−) 1st | −1 |

| 27.50% | 6.52% | (−) 2nd | −2 | 9.68% | 1st | 0 | 7.89% | (−) 1st | −1 |

| 30% | 6.52% | (−) 2nd | −2 | 9.68% | 1st | 0 | 7.89% | (−) 1st | −1 |

| Leverage/EPS | Leverage/Cashflow | Cashflow/EPS | |||||||

| Baseline Ratio: 68.90% | Baseline Ratio: 83.80% | Baseline Ratio: 82.20% | |||||||

| Ratio | Pref | Pts | Ratio | Pref | Pts | Ratio | Pref | Pts | |

| 17.50% | 67.86% | (+) 3rd | 4 | 79.17% | (+) 1st | 6 | 85.71% | (+) 1st | 6 |

| 20% | 67.44% | (+) 2nd | 5 | 80.56% | (+) 2nd | 5 | 83.72% | (+) 2nd | 5 |

| 22.50% | 68.89% | 4th | 0 | 81.58% | (+) 3rd | 4 | 84.44% | (+) 3rd | 4 |

| 25% | 67.39% | (+) 1st | 6 | 81.58% | (+) 3rd | 4 | 82.61% | (+) 3rd | 4 |

| 27.50% | 67.39% | (+) 1st | 6 | 81.58% | (+) 3rd | 4 | 82.61% | (+) 3rd | 4 |

| 30% | 67.39% | (+) 1st | 6 | 81.58% | (+) 3rd | 4 | 82.61% | (+) 3rd | 4 |

| Panel II: Medium Repurchases | |||||||||

| M/B Ratio/EPS | M/B Ratio/Cashflow | Cashflow/EPS | |||||||

| Baseline Ratio: 6.00% | Baseline Ratio: 7.30% | Baseline Ratio: 82.00% | |||||||

| Ratio | Pref | Pts | Ratio | Pref | Pts | Ratio | Pref | Pts | |

| 17.50% | 6.94% | (+) 2nd | 5 | 8.47% | (+) 1st | 6 | 81.94% | (+) 6th | 0 |

| 20% | 6.60% | (+) 5th | 2 | 8.00% | (+) 5th | 2 | 82.55% | (+) 4th | 3 |

| 22.50% | 6.58% | (+) 6th | 1 | 7.96% | (+) 6th | 1 | 82.72% | (+) 1st | 6 |

| 25% | 6.64% | (+) 4th | 3 | 8.06% | (+) 4th | 3 | 82.42% | (+) 5th | 2 |

| 27.50% | 6.95% | (+) 1st | 6 | 8.41% | (+) 2nd | 5 | 82.63% | (+) 3rd | 4 |

| 30% | 6.92% | (+) 3rd | 4 | 8.37% | (+) 3rd | 4 | 82.69% | (+) 2nd | 5 |

| Panel III: Large Repurchases | |||||||||

| M/B Ratio/EPS | M/B Ratio/Independence | EPS/Independence | |||||||

| Baseline Ratio: 2.40% | Baseline Ratio: 2.30% | Baseline Ratio: 97.10% | |||||||

| Ratio | Pref | Pts | Ratio | Pref | Pts | Ratio | Pref | Pts | |

| 17.50% | 2.16% | (−) 2nd | −2 | 2.11% | (−) 2nd | −2 | 97.89% | (−) 5th | −5 |

| 20% | 2.17% | (−) 1st | −1 | 2.12% | (−) 1st | −1 | 97.53% | (−) 2nd | −2 |

| 22.50% | 2.05% | (−) 3rd | −3 | 2.01% | (−) 3rd | −3 | 97.66% | (−) 3rd | −3 |

| 25% | 2.02% | (−) 4th | −4 | 1.97% | (−) 4th | −4 | 97.70% | (−) 4th | −4 |

| 27.50% | 2.01% | (−) 5th | −5 | 1.97% | (−) 4th | −4 | 97.70% | (−) 4th | −4 |

| 30% | 2.01% | (−) 5th | −5 | 1.96% | (−) 5th | −5 | 97.39% | (−) 1st | −1 |

| Small Repurchases | Medium Repurchases | Large Repurchases | Total Weighted | Ranking | ||||

|---|---|---|---|---|---|---|---|---|

| Raw Pts | Weighted Pts | Raw Pts | Weighted Pts | Raw Pts | Weighted Pts | Pts | ||

| 17.50% | 6.00 | 1.38 | 11 | 3.96 | −9.00 | −3.69 | 1.65 | 4th |

| 20% | 8.00 | 1.84 | 7 | 2.52 | −4.00 | −1.64 | 2.72 | 1st |

| 22.50% | 7.00 | 1.61 | 8 | 2.88 | −9.00 | −3.69 | 0.80 | 5th |

| 25% | 11.00 | 2.53 | 8 | 2.88 | −12.00 | −4.92 | 0.49 | 6th |

| 27.50% | 11.00 | 2.53 | 15 | 5.40 | −13.00 | −5.33 | 2.60 | 3rd |

| 30% | 11.00 | 2.53 | 13 | 4.68 | −11.00 | −4.51 | 2.70 | 2nd |

| Panel I: Coefficients | ||||||||||||

| I | II | III | IV | V | VI | VII | VIII | IX | X | XI | XII | |

| M/B Ratio | −0.043 *** (−3.19) | −0.050 *** (−3.38) | −0.045 *** (−3.22) | −0.043 *** (−3.16) | −0.055 *** (−3.53) | −0.055 *** (−3.53) | −0.055 *** (−3.53) | −0.055 *** (−3.54) | −0.055 *** (−3.53) | −0.055 *** (−3.54) | −0.055 *** (−3.53) | −0.055 *** (−3.53) |

| EPS | 0.644 *** (4.27) | 0.858 *** (5.06) | 0.654 *** (4.35) | 0.620 *** (3.93) | 0.885 *** (4.94) | 0.881 *** (4.84) | 0.924 *** (4.73) | 0.885 *** (4.93) | 0.919 *** (4.63) | 0.881 *** (4.83) | 0.923 *** (4.72) | 0.919 *** (4.63) |

| Cashflow | 0.645 ** (2.26) | 0.774 *** (2.63) | 0.771 *** (2.61) | 0.803 *** (2.69) | 0.772 *** (2.58) | 0.800 *** (2.67) | 0.769 *** (2.57) | 0.801 *** (2.64) | 0.798 *** (2.63) | |||

| Leverage | 0.093 (0.48) | 0.241 (1.19) | 0.261 (1.08) | 0.239 (1.19) | 0.242 (1.21) | 0.261 (1.08) | 0.261 (1.08) | 0.241 (1.20) | 0.261 (1.08) | |||

| Independence | 0.140 (0.60) | 0.249 (1.08) | 0.260 (1.07) | 0.249 (1.08) | 0.253 (1.06) | 0.261 (1.07) | 0.263 (1.06) | 0.253 (1.06) | 0.262 (1.06) | |||

| Firm Size | −0.003 (−0.16) | −0.003 (−0.17) | −0.003 (−0.15) | −0.003 (−0.16) | ||||||||

| Dividend | 0.027 (0.51) | 0.027 (0.51) | 0.027 (0.51) | 0.027 (0.51) | ||||||||

| Tax Ratio | −0.015 (−0.10) | −0.013 (−0.09) | −0.015 (−0.10) | −0.012 (−0.08) | ||||||||

| Constant | 0.455 *** (7.64) | 0.381 *** (5.76) | 0.421 *** (4.31) | 0.380 *** (2.89) | 0.145 (0.88) | 0.176 (0.70) | 0.126 (0.75) | 0.154 (0.82) | 0.159 (0.63) | 0.182 (0.70) | 0.135 (0.71) | 0.164 (0.63) |

| McFadden R2 | 0.030 | 0.034 | 0.030 | 0.030 | 0.036 | 0.036 | 0.036 | 0.036 | 0.036 | 0.036 | 0.036 | 0.036 |

| WALD Chi2 | 37.67 | 40.04 | 38.40 | 39.21 | 44.22 | 44.52 | 44.23 | 44.22 | 44.49 | 44.51 | 44.22 | 44.48 |

| Prob > Chi2 | 0.000 | 0.000 | 0.000 | 0.000 | 0.000 | 0.000 | 0.000 | 0.000 | 0.000 | 0.000 | 0.000 | 0.000 |

| Total Obs. | 360 | 360 | 360 | 360 | 360 | 360 | 360 | 360 | 360 | 360 | 360 | 360 |

| Panel II: Marginal Effects | ||||||||||||

| I | II | III | IV | V | VI | VII | VIII | IX | X | XI | XII | |

| M/B Ratio | −0.015 *** (−3.24) | −0.017 *** (−3.43) | −0.016 *** (−3.25) | −0.015 *** (−3.20) | −0.019 *** (−3.59) | −0.019 *** (−3.59) | −0.019 *** (−3.58) | −0.019 *** (−3.59) | −0.019 *** (−3.58) | −0.019 *** (−3.59) | −0.019 *** (−3.59) | −0.019 *** (−3.59) |

| EPS | 0.228 *** (4.36) | 0.303 *** (5.18) | 0.232 *** (4.43) | 0.220 *** (3.98) | 0.312 *** (5.01) | 0.310 *** (4.90) | 0.325 *** (4.80) | 0.312 *** (5.00) | 0.324 *** (4.71) | 0.310 *** (4.90) | 0.325 *** (4.80) | 0.324 *** (4.70) |

| Cashflow | 0.228 ** (2.27) | 0.273 *** (2.64) | 0.272 *** (2.63) | 0.283 *** (2.71) | 0.272 *** (2.59) | 0.282 *** (2.69) | 0.271 *** (2.58) | 0.282 *** (2.66) | 0.281 *** (2.64) | |||

| Leverage | 0.033 (0.47) | 0.085 (1.19) | 0.092 (1.08) | 0.084 (1.18) | 0.085 (1.21) | 0.092 (1.07) | 0.092 (1.08) | 0.085 (1.20) | 0.092 (1.08) | |||

| Independence | 0.049 (0.60) | 0.088 (1.08) | 0.091 (1.07) | 0.088 (1.08) | 0.089 (1.06) | 0.092 (1.08) | 0.092 (1.06) | 0.089 (1.06) | 0.092 (1.06) | |||

| Firm Size | −0.001 (−0.16) | −0.001 (−0.17) | −0.001 (−0.15) | −0.001 (−0.16) | ||||||||

| Dividend | 0.009 (0.51) | 0.009 (0.51) | 0.009 (0.51) | 0.009 (0.51) | ||||||||

| Tax Ratio | −0.005 (−0.10) | −0.004 (−0.09) | −0.005 (−0.10) | −0.004 (−0.08) | ||||||||

| Panel I: Coefficients | ||||||||||||

| I | II | III | IV | V | VI | VII | VIII | IX | X | XI | XII | |

| M/B Ratio | −0.064 *** (−3.34) | −0.071 *** (−3.59) | −0.064 *** (−3.23) | −0.063 *** (−3.28) | −0.074 *** (−3.59) | −0.075 *** (−3.61) | −0.074 *** (−3.60) | −0.074 *** (−3.60) | −0.075 *** (−3.61) | −0.075 *** (−3.62) | −0.075 *** (−3.60) | −0.075 *** (−3.62) |

| EPS | 0.842 *** (4.16) | 1.051 *** (4.24) | 0.842 *** (4.13) | 0.780 *** (3.76) | 1.036 *** (4.06) | 1.013 *** (3.93) | 1.071 *** (3.89) | 1.043 *** (4.07) | 1.047 *** (3.77) | 1.017 *** (3.94) | 1.077 *** (3.90) | 1.052 *** (3.78) |

| Cashflow | 0.636 (1.50) | 0.777 * (1.77) | 0.763 * (1.74) | 0.803 * (1.80) | 0.812 * (1.84) | 0.789 * (1.77) | 0.800 * (1.81) | 0.839 * (1.87) | 0.827 * (1.84) | |||

| Leverage | −0.010 (−0.04) | 0.169 (0.62) | 0.288 (0.88) | 0.168 (0.62) | 0.154 (0.56) | 0.287 (0.88) | 0.287 (0.88) | 0.154 (0.56) | 0.286 (0.88) | |||

| Independence | 0.394 (1.42) | 0.487 * (1.70) | 0.549 * (1.82) | 0.487 * (1.70) | 0.445 (1.53) | 0.549 * (1.82) | 0.511 * (1.68) | 0.446 (1.53) | 0.512 * (1.68) | |||

| Firm Size | −0.019 (−0.67) | −0.019 (−0.67) | −0.022 (−0.76) | −0.022 (−0.76) | ||||||||

| Dividend | 0.023 (0.33) | 0.023 (0.33) | 0.024 (0.34) | 0.024 (0.34) | ||||||||

| Tax Ratio | 0.179 (0.74) | 0.199 (0.82) | 0.179 (0.74) | 0.199 (0.82) | ||||||||

| McFadden R2 | 0.043 | 0.046 | 0.043 | 0.046 | 0.050 | 0.051 | 0.050 | 0.051 | 0.051 | 0.052 | 0.051 | 0.052 |

| LR Chi2 | 33.72 | 35.98 | 33.72 | 35.74 | 38.94 | 39.39 | 39.05 | 39.49 | 39.50 | 40.07 | 39.61 | 40.18 |

| Prob > Chi2 | 0.000 | 0.000 | 0.000 | 0.000 | 0.000 | 0.000 | 0.000 | 0.000 | 0.000 | 0.000 | 0.000 | 0.000 |

| Total Obs. | 360 | 360 | 360 | 360 | 360 | 360 | 360 | 360 | 360 | 360 | 360 | 360 |

| Panel II: Marginal Effects | ||||||||||||

| I | II | III | IV | V | VI | VII | VIII | IX | X | XI | XII | |

| M/B Ratio | ||||||||||||

| 1st Tercile | 0.018 *** (3.44) | 0.020 *** (3.70) | 0.018 *** (3.31) | 0.018 *** (3.37) | 0.021 *** (3.69) | 0.021 *** (3.70) | 0.021 *** (3.69) | 0.021 *** (3.69) | 0.021 *** (3.71) | 0.021 *** (3.71) | 0.021 *** (3.70) | 0.021 *** (3.72) |

| 2nd Tercile | 0.005 *** (2.57) | 0.005 *** (2.69) | 0.005 ** (3.52) | 0.005 ** (2.55) | 0.005 *** (2.71) | 0.005 *** (2.72) | 0.005 *** (2.71) | 0.005 *** (2.71) | 0.005 *** (2.72) | 0.005 *** (2.72) | 0.005 *** (2.71) | 0.005 *** (2.72) |

| 3rd Tercile | −0.023 *** (−3.42) | −0.026 *** (−3.70) | −0.023 *** (−3.30) | −0.023 *** (−3.35) | −0.027 *** (−3.70) | −0.027 *** (−3.72) | −0.027 *** (−3.71) | −0.027 *** (−3.71) | −0.027 *** (−3.73) | −0.027 *** (−3.73) | −0.027 *** (−3.71) | −0.027 *** (−3.73) |

| EPS | ||||||||||||

| 1st Tercile | −0.241 *** (−4.12) | −0.300 *** (−4.20) | −0.240 *** (−4.09) | −0.222 *** (−3.72) | −0.294 *** (−4.01) | −0.287 ** (−3.88) | −0.304 *** (−3.85) | −0.296 *** (−4.03) | −0.297 *** (−3.74) | −0.288 *** (−3.89) | −0.305 *** (−3.87) | −0.029 *** (−3.75) |

| 2nd Tercile | −0.067 *** (−3.51) | −0.083 *** (−3.50) | −0.067 *** (−3.50) | −0.062 *** (−3.27) | −0.081 *** (−3.40) | −0.079 *** (−3.34) | −0.083 *** (−3.28) | −0.081 *** (−3.41) | −0.081 *** (−3.22) | −0.079 *** (−3.35) | −0.084 *** (−3.29) | −0.082 *** (−3.23) |

| 3rd Tercile | 0.309 *** (4.47) | 0.383 *** (4.56) | 0.308 *** (4.44) | 0.284 *** (3.98) | 0.375 *** (4.33) | 0.367 *** (4.18) | 0.388 *** (4.12) | 0.377 *** (4.36) | 0.379 *** (3.99) | 0.368 *** (4.19) | 0.390 *** (4.15) | 0.380 *** (4.00) |

| Cashflow | ||||||||||||

| 1st Tercile | −0.181 (−1.50) | −0.220 * (−1.77) | −0.216 * (−1.74) | −0.228 * (−1.80) | −0.230 * (−1.84) | −0.224 * (−1.77) | −0.227 * (−1.81) | −0.238 * (−1.87) | −0.234 * (−1.84) | |||

| 2nd Tercile | −0.050 (−1.45) | −0.060 * (−1.69) | −0.059 * (−1.66) | −0.062 * (−1.71) | −0.063 * (−1.75) | −0.061 * (−1.68) | −0.062 * (−1.72) | −0.065 * (−1.77) | −0.064 * (−1.74) | |||

| 3rd Tercile | 0.232 (1.51) | 0.281 * (1.79) | 0.276 * (1.76) | 0.291 * (1.82) | 0.294 * (1.86) | 0.285 * (1.79) | 0.289 * (1.83) | 0.303 * (1.89) | 0.299 * (1.86) | |||

| Leverage | ||||||||||||

| 1st Tercile | 0.003 (0.04) | −0.048 (−0.62) | −0.081 (−0.88) | −0.047 (−0.62) | −0.043 (−0.56) | −0.081 (−0.88) | −0.081 (−0.88) | −0.043 (−0.56) | −0.081 (−0.88) | |||

| 2nd Tercile | 0.0008 (0.04) | −0.013 (−0.62) | −0.022 (−0.87) | −0.013 (−0.61) | −0.012 (−0.56) | −0.022 (−0.87) | −0.022 (−0.87) | −0.012 (−0.56) | −0.022 (−0.87) | |||

| 3rd Tercile | −0.003 (−0.04) | 0.061 (0.62) | 0.104 (0.89) | 0.061 (0.62) | 0.056 (0.56) | 0.103 (0.88) | 0.104 (0.88) | 0.055 (0.56) | 0.103 (0.88) | |||

| Independence | ||||||||||||

| 1st Tercile | −0.112 (−1.42) | −0.148 * (−1.70) | −0.156 * (−1.83) | −0.148 * (−1.70) | −0.125 (−1.53) | −0.156 * (−1.83) | −0.145 * (−1.68) | −0.126 (−1.53) | −0.145 * (−1.68) | |||

| 2nd Tercile | −0.031 (−1.37) | −0.048 (−1.62) | −0.042 * (−1.72) | −0.381 (−1.62) | −0.034 (−1.47) | −0.043 * (−1.72) | −0.039 (−1.60) | −0.034 (−1.47) | −0.040 (−1.60) | |||

| 3rd Tercile | 0.143 (1.43) | 0.176 * (1.72) | 0.199 * (1.85) | 0.176 * (1.72) | 0.161 (1.54) | 0.199 * (1.85) | 0.185 * (1.70) | 0.161 (1.54) | 0.185 * (1.70) | |||

| Firm Size | ||||||||||||

| 1st Tercile | 0.005 (0.67) | 0.005 (0.67) | 0.006 (0.76) | 0.006 (0.76) | ||||||||

| 2nd Tercile | 0.001 (0.67) | 0.001 (0.66) | 0.001 (0.75) | 0.001 (0.74) | ||||||||

| 3rd Tercile | −0.007 (−0.67) | −0.007 (−0.67) | −0.007 (−0.76) | −0.007 (−0.76) | ||||||||

| Dividend | ||||||||||||

| 1st Tercile | −0.006 (−0.33) | −0.006 (−0.33) | −0.006 (−0.34) | −0.006 (−0.34) | ||||||||

| 2nd Tercile | −0.001 (−0.33) | −0.001 (−0.33) | −0.001 (−0.34) | −0.001 (−0.33) | ||||||||

| 3rd Tercile | 0.008 (0.33) | 0.008 (0.33) | 0.008 (0.34) | 0.008 (0.34) | ||||||||

| Tax Ratio | ||||||||||||

| 1st Tercile | −0.050 (−0.74) | −0.056 (−0.82) | −0.051 (−0.74) | −0.056 (−0.82) | ||||||||

| 2nd Tercile | −0.013 (−0.73) | −0.015 (−0.81) | −0.014 (−0.74) | −0.015 (−0.81) | ||||||||

| 3rd Tercile | 0.064 (0.74) | 0.072 (0.82) | 0.065 (0.74) | 0.072 (0.82) | ||||||||

| I | II | III | IV | V | VI | VII | VIII | IX | X | XI | XII | |

|---|---|---|---|---|---|---|---|---|---|---|---|---|

| M/B Ratio | −0.001 *** (−2.77) | −0.001 *** (−2.90) | −0.001 *** (−2.77) | −0.001 *** (−2.77) | −0.001 *** (−2.90) | −0.001 (−2.89) | −0.001 *** (−2.91) | −0.001 *** (−2.90) | −0.001 *** (−2.90) | −0.001 *** (−2.88) | −0.001 *** (−2.91) | −0.001 *** (−2.89) |

| EPS | 0.030 *** (4.35) | 0.037 *** (4.35) | 0.030 *** (4.27) | 0.029 *** (3.98) | 0.035 *** (4.10) | 0.036 (4.04) | 0.037 *** (3.97) | 0.035 *** (4.09) | 0.038 *** (3.92) | 0.036 *** (4.03) | 0.037 *** (3.96) | 0.038 *** (3.92) |

| Cashflow | 0.021 (1.34) | 0.022 (1.43) | 0.023 (1.43) | 0.024 (1.49) | 0.022 (1.41) | 0.024 (1.49) | 0.022 (1.41) | 0.024 (1.48) | 0.024 (1.48) | |||

| Leverage | −0.002 (−0.27) | 0.001 (0.12) | 0.001 (0.04) | 0.001 (0.12) | 0.001 (0.12) | 0.001 (0.05) | 0.001 (0.04) | 0.001 (0.13) | 0.001 (0.05) | |||

| Independence | 0.008 (0.77) | 0.009 (0.92) | 0.009 (0.83) | 0.009 (0.92) | 0.010 (0.91) | 0.009 (0.84) | 0.009 (0.83) | 0.010 (0.91) | 0.009 (0.84) | |||

| Firm Size | 0.001 (0.12) | 0.001 (0.11) | 0.001 (0.13) | 0.001 (0.11) | ||||||||

| Dividend | 0.001 (9.60) | 0.001 (0.51) | 0.001 (0.51) | 0.001 (0.51) | ||||||||

| Tax Ratio | −0.001 (−0.06) | −0.001 (−0.07) | −0.001 (−0.06) | −0.001 (−0.07) | ||||||||

| Constant | 0.097 *** (37.27) | 0.094 *** (27.67) | 0.098 *** (20.71) | 0.092 *** (15.22) | 0.088 *** (9.93) | 0.087 *** (6.35) | 0.087 *** (9.60) | 0.088 *** (8.65) | 0.086 *** (6.24) | 0.087 *** (6.09) | 0.087 *** (8.41) | 0.086 *** (5.99) |

| Adj R2 | 0.065 | 0.067 | 0.062 | 0.064 | 0.064 | 0.061 | 0.062 | 0.061 | 0.059 | 0.059 | 0.059 | 0.057 |

| Mean VIF | 1.00 | 1.32 | 1.01 | 1.05 | 1.27 | 1.42 | 1.31 | 1.25 | 1.43 | 1.38 | 1.29 | 1.40 |

| Total Obs. | 360 | 360 | 360 | 360 | 360 | 360 | 360 | 360 | 360 | 360 | 360 | 360 |

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2024 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Sodhi, A.; Stojanovic, A. Deregulating the Volume Limit on Share Repurchases. Int. J. Financial Stud. 2024, 12, 89. https://doi.org/10.3390/ijfs12030089

Sodhi A, Stojanovic A. Deregulating the Volume Limit on Share Repurchases. International Journal of Financial Studies. 2024; 12(3):89. https://doi.org/10.3390/ijfs12030089

Chicago/Turabian StyleSodhi, Adhiraj, and Aleksandar Stojanovic. 2024. "Deregulating the Volume Limit on Share Repurchases" International Journal of Financial Studies 12, no. 3: 89. https://doi.org/10.3390/ijfs12030089

APA StyleSodhi, A., & Stojanovic, A. (2024). Deregulating the Volume Limit on Share Repurchases. International Journal of Financial Studies, 12(3), 89. https://doi.org/10.3390/ijfs12030089