Predicting Operating Income via a Generalized Operating-Leverage Model

Abstract

1. Introduction

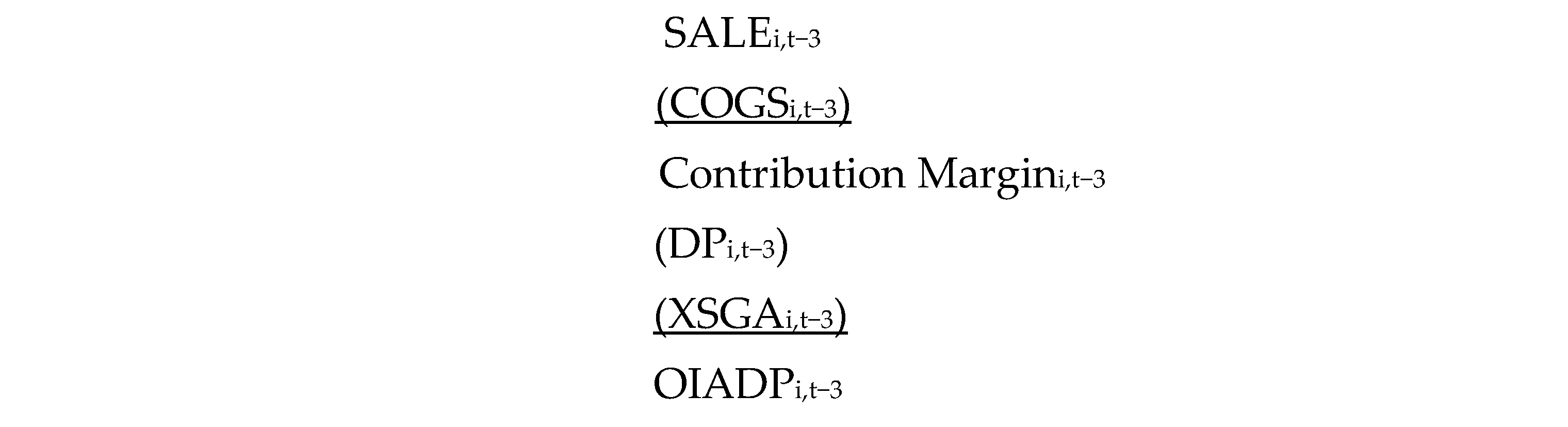

where Contribution Margin = Total Sales Revenue − Total Variable Costs

2. Literature Review

- By using Casey et al. (2016) finding that the Compustat SALE − COGS − DP − XSGA equates to the Compustat OIADP;

- By predicting the OIADP operating income as opposed to the Return on Equity (ROE);

- By specifying the Compustat depreciation and amortization (DP) and selling, general, and administrative costs (XSGA) as sticky costs following Shust and Weiss (2014) and Chen et al. (2019);

- By employing the COGS as a proxy for the total variable costs following Chen et al. (2019);

- By predicting the future COGS by using the estimated future SALE-to-COGS ratio.

3. Methodology

3.1. Data

3.2. Methodology for Predicting Quarterly OIADP

3.3. Restating Operating Leverage for Constant SALE/COGS Ratio for Quarters

(operating leveragei,t * percent change in sales from period t to period t + n)

(1 + (CHG_QTR_SALEi,t+1 * BASE_QTR_OLi,t−3)) * OIADPi,t−3

(((average of SALE for periods t − 2 through t) − SALEi,t−3)/SALEi,t−3)

(1 + (((average of SALE-to-COGS for periods t − 2 through t) −

SALE_to_COGSi,t−3)/SALE_to_COGSi,t−3)) * SALE_to_COGSi,t−3

(SALEi,t−3 − (SALEi,t−3/EST_QTR_SALE_to_COGSi,t+1))/(SALEi,t−3 −

(SALEi,t−3/(EST_QTR_SALE_to_COGSi,t+1/COGSi,t+1)) − DPi,t−3 − XSGAi,t−3)

(1 + (CHG_QTR_SALEi,t+1 * RESTATED_QTR_OLi,t−3)) *

(SALEi,t−3 − (SALEi,t−3/EST_QTR_SALE_to_COGSi,t+1) − DPi,t−3 − XSGAi,t−3)

RESTATED_QTR_OL_WITH_STICKY_DP_AND_XSGAi,t−3 =

(SALEi,t−3 − SALEi,t−3/EST_QTR_SALE_to_COGSi,t+1)/

(SALEi,t−3 − SALEi,t−3/EST_QTR_SALE_to_COGSi,t+1 − DPi,t−3 − XSGAi,t−3 −

(CHG_QTR_SALEi,t+1 * 0.484 * DPi,t−3) − (CHG_QTR_SALEi,t+1 * 0.377 * XSGAi,t−3))

RESTATED_QTR_ OL_WITH_STICKY_DP_AND_XSGAi,t−3 =

(SALEi,t−3 − SALEi,t−3/EST_QTR_SALE_to_COGSi,t+1)/

(SALEi,t−3 − SALEi,t−3/EST_QTR_SALE_to_COGSi,t+1 − DPi,t−3 − XSGAi,t−3 −

(CHG_QTR_SALEi,t+1 * 0.205 * DPi,t−3) − (CHG_QTR_SALEi,t+1 * 0.235 * XSGAi,t−3))

RESTATED_QTR_OL_WITH_STICKY_DP_AND_XSGAi,t−3)) *

(SALEi,t−3 − (SALEi,t−3/EST_QTR_SALE_to_COGSi,t+1) − DPi,t−3 − XSGAi,t−3 −

(CHG_QTR_SALEi,t+1 * 0.484 * DPi,t−3) − (CHG_QTR_SALEi,t+1 * 0.377 * XSGAi,t−3))

FULL_MODEL_ESTIMATED_QTR_OIADPi,t+1 = (1 + (CHG_QTR_SALEi,t+1 *

RESTATED_QTR _OL_WITH_STICKY_DP_AND_XSGAi,t−3)) *

(SALEi,t−3 − (SALEi,t−3/EST_QTR_SALE_to_COGSi,t+1) − DPi,t−3 − XSGAi,t−3 −

(CHG_QTR_SALEi,t+1 * 0.205 * DPi,t−3) − (CHG_SALEi,t+1 * 0.235 * XSGAi,t−3))

(1 + (((average of SALE-to-COGS for quarters t − 2 through t) −

[SALEi,t−3/COGSi,t−3])/[SALEi,t−3/COGSi,t−3])) * [SALEi,t−3/COGSi,t−3]

(ESTIMATED_QTR_OIADPi,t+1 − OIADPi,t−1)/ATi,t−1

Absolute Value ((OIADPi,t+1 − ESTIMATED_QTR_OIADPi,t+1)/OIADPi,t+1)

3.4. Methodology for Predicting Annual OIADP

(1 + (CHG_1YR_SALEi,t+1 * BASE_1YR_OLi,t)) * OIADPi,t

(SALEi,t − ((SALEi,t + SALEi,t−1)/2))/((SALEi,t + SALEi,t−1)/2)

(SALEi,t − (SALEi,t/EST_1YR_SALE_to_COGSi,t+1))/

(SALEi,t − (SALEi,t/EST_1YR_SALE_to_COGSi,t+1) − DPi,t − XSGAi,t)

where EST_1YR_SALE_to_COGSi,t+1 =

((SALEi,t/COGSi,t) + (SALEi,t−1/COGSi,t−1))/2

(1 + (CHG_1YR_SALEi,t+1 * RESTATED_1YR_OLi,t)) *

(SALEi,t − (SALEi,t/EST_1YR_SALE_to_COGSi,t+1) − DPi,t − XSGAi,t)

RESTATED_1YR_OL_WITH_STICKY_DP_AND_XSGAi,t =

(SALEi,t − SALEi,t/EST_1YR_SALE_to_COGSi,t+1)/

(SALEi,t − SALEi,t/EST_1YR_SALE_to_COGSi,t+1 − DPi,t − XSGAi,t −

(CHG_1YR_SALE * 0.647 * DPi,t) − (CHG_1YR_SALE * 0.440 * XSGAi,t))

RESTATED_1YR_OL_WITH_STICKY_DP_AND_XSGAi,t =

(SALEi,t − SALEi,t/EST_1YR_SALE_to_COGSi,t+1)/

(SALEi,t − SALEi,t/EST_1YR_SALE_to_COGSi,t+1 − DPi,t − XSGAi,t −

(CHG_1YR_SALE * 0.393 * DPi,t) − (CHG_1YR_SALE * 0.309 * XSGAi,t))

ESTIMATED_1YR_OIADPi,t+1 =

(1 + (CHG_1YR_SALE * RESTATED_1YR_OL_WITH_STICKY_DP_AND_XSGAi,t)) *

(SALEi,t − (SALEi,t/EST_1YR_SALE_to_COGSi,t+1) − DPi,t − XSGAi,t −

(CHG_1YR_SALE * 0.647* DPi,t) − (CHG_1YR_SALE * 0.440 * XSGAi,t))

ESTIMATED_1YR_OIADPi,t+1 =

(1 + (CHG_1YR_SALE * RESTATED_1YR_OL_WITH_STICKY_DP_AND_XSGAi,t)) *

(SALEi,t − (SALEi,t/EST_1YR_SALE_to_COGSi,t+1) − DPi,t − XSGAi,t −

(CHG_1YR_SALEi,t+1 * 0.393 * DPi,t) − (CHG_1YR_SALEi,t+1 * 0.309 * XSGAi,t))

3.5. Testing the Veracity of the Generalized Operating-Leverage Model

(SALEi,t − (SALEi,t/(SALEi,t+1/COGSi,t+1)))/

(SALEi,t − (SALEi,t/(SALEi,t+1/COGSi,t+1)) − DPi,t+1 − XSGAi,t+1)

(1 + (((SALEi,t+1 − SALEi,t)/SALEi,t) * RESTATED_OL)) *

(SALEi,t − (SALEi,t/(SALEi,t+1/COGSi,t+1)) − DPi,t+1 − XSGAi,t+1)

(NEXT_YR_OPERATING_INCOMEi,t+1 − OIADPi,t)/ATi,t−1

3.6. Consideration of Dow Jones Industrial Average (DJIA) Firms

4. Results and Discussion

4.1. Results for Estimating Next-Quarter OIADP

4.2. Results for Estimating Next-Year Annual OIADP

4.3. Results for Estimating Three-Year-Ahead OIADP

4.4. Results for Estimating Next-Quarter OIADP within Industry Context

5. Conclusions, Summary, and Future Research

Author Contributions

Funding

Data Availability Statement

Conflicts of Interest

Appendix A

operating incomet) = future period t + n operating income

(St − Vt − Ft) + {[(St+n − St)/St] * [(St − Vt)]}

St − Vt − Ft + St+n − St − St+n*Vt/St + St*Vt/St

− Vt − Ft + St+n − St+n*Vt/St + St*Vt/St =

− Vt − (Ft) + St+n − St+n*(Vt/St) + St* (Vt/St) =

− Vt − Ft+n + St+n − Vt+n + Vt =

St+n − Vt+n − Ft+n

Appendix B

- Applying ABJ Methodology to Compute Sticky Factors for XSGA and DP Quarterly

+ β2 * Decrease_Dummyi,t * log [SALEi,t/SALEi,t−1)] + εi,t

{kind=link}

| Regression Specification Models based on ABJ: log [COGSi,t/COGSi,t−3] = β0 + β1 log[SALEi,t/SALEi,t−3] + β2 * Decrease_Dummyi,t−3 to t * log [SALEi,t/SALEi,t−3)] + εi,t log [DPi,t/DPi,t−1] = β0 + β1 log[SALEi,t/SALEi,t−1−3] + β2 * Decrease_Dummyi,t−3 to t * log [SALEi,t/SALEi,t−3)] + εi,t log [XSGAi,t/XSGAi,t−1] = β0 + β1 log [SALEi,t/SALEi,t−1] + β2 * Decrease_Dummyi,t * log [SALEi,t/SALEi,t−1)] + εi,t | |||||||

| Coefficient Estimates (t-statistics) | |||||||

| Dependent Variable | N | Adj. R-Square | % Increase in Dependent Variable for 1% increase in Sales (β1) | SALE Change Decrease Dummy (β2) | % Decrease in Dependent Variable for 1% Decrease in Sales (β1 + β2) | β1 p-value (t value) | β2 p-value (t value) |

| COGS | 241,043 | 0.445 | 0.879 | −0.162 | 0.717 | 0.000 296.380 | 0.001 −36.064 |

| DP | 241,043 | 0.105 | 0.484 | −0.279 | 0.205 | 0.000 139.327 | 0.000 −52.839 |

| XSGA | 241,043 | 0.150 | 0.377 | −0.142 | 0.235 | 0.000 154.402 | 0.000 −38.349 |

Appendix C

- Applying ABJ Methodology to Compute Sticky Factors for XSGA and DP Annually

| Regression Specification Models based on ABJ: log [COGSi,t/COGSi,t−1] = β0 + β1 log[SALEi,t/SALEi,t−1] + β2 * Decrease_Dummyi,t * log [SALEi,t/SALEi,t−1)] + εi,t log [DPi,t/DPi,t−1] = β0 + β1 log[SALEi,t/SALEi,t−1] + β2 * Decrease_Dummyi,t * log [SALEi,t/SALEi,t−1)] + εi,t log [XSGAi,t/XSGAi,t−1] = β0 + β1 log [SALEi,t/SALEi,t−1] + β2 * Decrease_Dummyi,t * log [SALEi,t/SALEi,t−1)] + εi,t | |||||||

| Coefficient Estimates (t-statistics) | |||||||

| Dependent Variable | N | Adj. R-square | % Increase in Dependent Variable for 1% Increase in Sales (β1) | SALE Change * Decrease Dummy (β2) | % Decrease in Dependent Variable for 1% Decrease in Sales (β1 + β2) | β1 p-value (t value) | β2 p-value (t value) |

| COGS | 188,808 | 0.589 | 0.880 | −0.046 | 0.834 | 0.000 404.713 | 0.001 −11.050 |

| DP | 188,808 | 0.267 | 0.647 | −0.254 | 0.393 | 0.000 227.362 | 0.000 −46.695 |

| XSGA | 188,808 | 0.310 | 0.440 | −0.131 | 0.309 | 0.000 245.616 | 0.000 −38.125 |

| 1 | Bostwick et al. (2016) found that S&P subtracts (DP − AM) from the cogs to derive the COGS when entities disclose and quantify the allocation of amortization (AM) but not depreciation. |

| 2 | For all observations, we require OIADP − (SALE − COGS − DP − XSGA) < 0.001 and SALE, COGS, DP, and XSGA values > 0. |

| 3 |

References

- Abarbanell, Jeffrey, and Brian Bushee. 1997. Fundamental analysis, future earnings, and stock prices. Journal of Accounting Research 35: 1–24. [Google Scholar] [CrossRef]

- Anderson, Mark, Rajiv Banker, and Surya Janakiraman. 2003. Are selling, general, and administrative costs ‘sticky’? Journal of Accounting Research 41: 47–63. [Google Scholar] [CrossRef]

- Banker, Rajiv, and Dmitri Byzalov. 2014. Asymmetric cost behavior. Journal of Management Accounting Research 26: 43–79. [Google Scholar] [CrossRef]

- Banker, Rajiv, and Lei Chen. 2006. Predicting earnings using a model based on cost variability and cost stickiness. The Accounting Review 81: 285–307. [Google Scholar] [CrossRef]

- Banker, Rajiv, Dmitri Byzalov, Shunlan Fang, and Yi Liang. 2018. Cost management research. Journal of Management Accounting Research 30: 187–209. [Google Scholar] [CrossRef]

- Bernstein, Leopold. 1988. Financial Statement Analysis. Homewood: Irwin. [Google Scholar]

- Bostwick, Eric, Sherwood Lambert, and Joseph Donelan. 2016. A wrench in the COGS: An analysis of the differences between cost of goods sold as reported in Compustat and in the financial statements. Accounting Horizons 30: 177–93. [Google Scholar] [CrossRef]

- Casey, Ryan, Feng Gao, Michael Kirschenheiter, Siyi Li, and Shailendra Pandit. 2016. Do Compustat financial statement data articulate? Journal of Financial Reporting 1: 37–59. [Google Scholar] [CrossRef]

- Chang, Tom, Samuel Hartzmark, David Solomon, and Eugene Soltes. 2017. Being surprised by the unsurprising: Earnings seasonality and stock returns. Review of Financial Studies 30: 281–323. [Google Scholar] [CrossRef]

- Chen, Huafeng, Marcin Kacperczyk, and Hernán Ortiz-Molina. 2011. Firm-specific attributes and the cross-section of momentum. Journal of Financial and Quantitative Analysis 46: 25–58. [Google Scholar] [CrossRef]

- Chen, James. 2023. Blue Chip Meaning and Examples. Investopedia. Available online: https://www.investopedia.com/terms/b/bluechip.asp (accessed on 23 December 2023).

- Chen, Zhiyao, Jarrad Harford, and Avraham Kamara. 2019. Operating Leverage, Profitability, and Capital Structure. Journal of Financial and Quantitative Analysis 54: 369–92. [Google Scholar] [CrossRef]

- Ciftci, Mustafa, and Taisier Zoubi. 2019. The magnitude of sales change and asymmetric cost behavior. Journal of Management Accounting Research 31: 65–81. [Google Scholar] [CrossRef]

- Ciftci, Mustafa, Raj Mashruwala, and Dan Weiss. 2016. Implications of cost behavior for analysts’ earnings forecasts. Journal of Management Accounting Research 28: 57–80. [Google Scholar] [CrossRef]

- Donangelo, Andrés. 2014. Labor mobility: Implications for asset pricing. Journal of Finance 69: 1321–46. [Google Scholar] [CrossRef]

- Du, Kai, Steven Huddart, and Xin Daniel Jiang. 2023. Lost in standardization: Effects of financial statement database discrepancies on inference. Journal of Accounting and Economics 76: 101573. [Google Scholar] [CrossRef]

- Fairfield, Patricia, Richard Sweeney, and Teri Yohn. 1996. Accounting Classification and the Predictive Content of Earnings. The Accounting Review 71: 337–55. [Google Scholar]

- Grau, Alfredo, and Araceli Reig. 2021. Operating leverage and profitability of SMEs: Agri-food industry in Europe. Small Business Economics 57: 221–42. [Google Scholar] [CrossRef]

- Griffin, Paul. 1977. The time-series behavior of quarterly earnings: Preliminary evidence. Journal of Accounting Research 15: 71–83. [Google Scholar]

- Gulen, Huseyin, Yuhang Xing, and Lu Zhang. 2011. Value versus growth: Time-varying expected stock returns. Financial Management 40: 381–407. [Google Scholar] [CrossRef]

- Hayn, Carla. 1995. The information content of losses. Journal of Accounting and Economics 20: 125–53. [Google Scholar]

- Hilton, Ronald, and David Platt. 2023. Managerial Accounting: Creating Value in a Dynamic Business Environment, 13th ed. New York: McGraw Hill. [Google Scholar]

- Jones, Charles, and Robert Utzenberger. 1969. Is earnings seasonality reflected in stock prices? Financial Analysts Journal 25: 57–59. [Google Scholar] [CrossRef]

- Kanoujiya, Jagjeevan, Pooja Jain, Souvik Banerjee, Rameesha Kalra, Shailesh Rastogi, and Venkata Bhimavarapu. 2023. Impact of Leverage on Valuation of Non-Financial Firms in India under Profitability’s Moderating Effect: Evidence in Scenarios Applying Quantile Regression. Journal of Risk and Financial Management 16: 366. [Google Scholar] [CrossRef]

- Lev, Baruch. 1974. On the association between operating leverage and risk. Journal of Financial and Quantitative Analysis 9: 627–41. [Google Scholar] [CrossRef]

- Lev, Baruch, and Robert Thiagarajan. 1993. Fundamental information analysis. Journal of Accounting Research 31: 190–215. [Google Scholar] [CrossRef]

- Lipe, Robert. 1986. The information contained in the components of earnings. Journal of Accounting Research 24: 37–64. [Google Scholar] [CrossRef]

- Mandelker, Gershon, and Ghon Rhee. 1984. The impact of the degrees of operating and financial leverage on systematic risk of common stock. Journal of Financial and Quantitative Analysis 19: 45–57. [Google Scholar] [CrossRef]

- Novy-Marx, Robert. 2011. Operating leverage. Review of Finance 15: 103–34. [Google Scholar] [CrossRef]

- Restuti, Mitha Dwi, Lindawati Gani, Elvia Shauki, and Lianny Leo. 2022. Does Managerial Ability Lead to Different Cost Stickiness Behavior? Evidence from ASEAN Countries. International Journal of Financial Studies 10: 48. [Google Scholar] [CrossRef]

- Rouxelin, Florent, Wan Wongsunwai, and Nir Yehuda. 2018. Aggregate cost stickiness in GAAP financial statements and future unemployment rate. The Accounting Review 93: 299–325. [Google Scholar] [CrossRef]

- Sagi, Jacob, and Mark Seasholes. 2007. Firm-specific attributes and the cross-section of momentum. Journal of Financial Economics 84: 389–434. [Google Scholar] [CrossRef]

- Shust, Efrat, and Dan Weiss. 2014. Discussion of asymmetric cost behavior-sticky costs: Expenses versus cash flows. Journal of Management Accounting Research 26: 81–90. [Google Scholar] [CrossRef]

- Simintzi, Elena, Vikrant Vig, and Paolo Volpin. 2015. Labor protection and leverage. Review of Financial Studies 28: 561–91. [Google Scholar] [CrossRef]

- Sloan, Richard. 1996. Do stock prices fully reflect information in accruals and cash flows about future earnings? The Accounting Review 71: 289–316. [Google Scholar]

- Welch, Paul. 1984. A generalized distributed lag model for predicting quarterly earnings. Journal of Accounting Research 22: 744–57. [Google Scholar] [CrossRef]

- Zhou, Hui, Worapree Ole Maneesoonthorn, and Xiangjin Bruce Chen. 2021. The predictive ability of quarterly financial statements. International Journal of Financial Studies 9: 50. [Google Scholar] [CrossRef]

| Strata of Abs. ERRORS | Count of Company-Years | Percent of Total Company-Years | Cumulative Percent of Company-Years | Percentile of Company-Years | Ordered Obs. | Percentile of Abs. ERRORs |

|---|---|---|---|---|---|---|

| 0–5% | 25,531 | 10.59% | 10.59% | 1st Percentile: | 2411 | 0.46% |

| 5–10% | 23,020 | 9.55% | 20.14% | 5th Percentile: | 12,055 | 2.29% |

| 10–15% | 19,239 | 7.98% | 28.12% | 10th Percentile: | 24,111 | 4.71% |

| 15–20% | 15,962 | 6.62% | 34.74% | 25th Percentile: | 60,276 | 12.97% |

| 20–25% | 13,663 | 5.67% | 40.40% | Median: | 120,553 | 35.61% |

| 25–50% | 45,670 | 18.94% | 59.35% | 75th Percentile: | 180,829 | 93.24% |

| 50–100% | 41,436 | 17.19% | 76.53% | 90th Percentile: | 216,995 | 245.35% |

| >100% | 56,585 | 23.47% | 100.00% | 95th Percentile: | 229,050 | 499.47% |

| Total: | 241,106 | 100.00% | 100.00% | 99th Percentile: | 238,694 | 2498.45% |

| Linear Regression Results | ||||||

| N | Adj. R-square | Coeff. | t-value | p-value | ||

| 241,105 | 0.106 | 0.523 | 169.009 | 0.000 | ||

| Model | Linear Regression Results | Median Abs. Value Error | ||||

|---|---|---|---|---|---|---|

| N | Adj. R-Square | Coeff. | t-Value | p-Value | ||

| BASE MODEL: No adjustment for constant SALE-to-COGS or sticky DP or XSGA (6). | 241,106 | 0.015 | 0.121 | 61.415 | 0.000 | 40.40% |

| INTERMEDIATE MODEL: restated SALE-to-COGS but no adjustment for sticky DP or XSGA (9). | 241,106 | 0.099 | 0.378 | 162.314 | 0.000 | 38.70% |

| FULL MODEL: adjustment for SALE-to-COGS and adjusting for sticky DP and XSGA, as shown in Table 1 (11). | 241,106 | 0.106 | 0.523 | 169.009 | 0.000 | 35.61% |

| Strata of Abs. Value Errors | Count of Company-Years | Percent of Total Company-Years | Cumulative Percent of Company-Years | Percentile of Company-Years | Ordered Obs. | Percentile of Abs. Value Errors |

|---|---|---|---|---|---|---|

| 0–5% | 22,456 | 14.19% | 14.19% | 1st Percentile: | 1582 | 0.33% |

| 5–10% | 19,889 | 12.57% | 26.76% | 5th Percentile: | 7912 | 1.70% |

| 10–15% | 16,322 | 10.31% | 37.08% | 10th Percentile: | 15,824 | 3.46% |

| 15–20% | 13,136 | 8.30% | 45.38% | 25th Percentile: | 39,559 | 9.23% |

| 20–25% | 10,729 | 6.78% | 52.16% | Median: | 79,119 | 23.28% |

| 25–50% | 32,233 | 20.37% | 72.53% | 75th Percentile: | 118,678 | 55.27% |

| 50–100% | 21,288 | 13.45% | 85.98% | 90th Percentile: | 142,413 | 143.86% |

| >100% | 22,185 | 14.02% | 100.00% | 95th Percentile: | 150,325 | 295.20% |

| Total: | 158,238 | 100.00% | 100.00% | 99th Percentile: | 156,655 | 1527.25% |

| Linear Regression Results | ||||||

| N | Adj. R-square | Coeff. | t-value | p-value | ||

| 158,237 | 0.147 | 0.453 | 165.018 | 0.000 | ||

| Strata of Abs. Value Errors | Count of Company-Years | Percent of Total Company-Years | Cumulative Percent of Company-Years | Percentile of Company-Years | Ordered Obs. | Percentile of Abs. Value Errors |

|---|---|---|---|---|---|---|

| 0–5% | 380 | 20.42% | 20.42% | 1st Percentile: | 19 | 0.24% |

| 5–10% | 341 | 18.32% | 38.74% | 5th Percentile: | 93 | 1.32% |

| 10–15% | 276 | 14.83% | 53.57% | 10th Percentile: | 186 | 2.46% |

| 15–20% | 184 | 9.89% | 63.46% | 25th Percentile: | 465 | 6.15% |

| 20–25% | 145 | 7.79% | 71.25% | Median: | 930 | 13.84% |

| 25–50% | 319 | 17.14% | 88.39% | 75th Percentile: | 1395 | 27.60% |

| 50–100% | 107 | 5.75% | 94.14% | 90th Percentile: | 1674 | 55.22% |

| >100% | 109 | 5.86% | 100.00% | 95th Percentile: | 1767 | 110.55% |

| Total: | 1861 | 100.00% | 100.00% | 99th Percentile: | 1841 | 686.40% |

| Linear Regression Results | ||||||

| N | Adj. R-square | Beta | t-value | p-value | ||

| 1860 | 0.338 | 0.750 | 165.018 | 0.000 | ||

| Strata of Abs. Value Errors | Count of Company-Years | Percent of Total Company-Years | Cumulative Percent of Company-Years | Percentile of Company-Years | Ordered Obs. | Percentile of Abs. Value Errors |

|---|---|---|---|---|---|---|

| 0–5% | 19,400 | 10.28% | 10.28% | 1st Percentile: | 1888 | 0.48% |

| 5–10% | 17,613 | 9.33% | 19.61% | 5th Percentile: | 9439 | 2.45% |

| 10–15% | 15,155 | 8.03% | 27.63% | 10th Percentile: | 18,878 | 4.87% |

| 15–20% | 12,899 | 6.83% | 34.47% | 25th Percentile: | 47,194 | 13.24% |

| 20–25% | 10,770 | 5.71% | 40.17% | Median: | 94,389 | 36.15% |

| 25–50% | 34,904 | 18.49% | 58.66% | 75th Percentile: | 141,583 | 97.33% |

| 50–100% | 32,026 | 16.97% | 75.63% | 90th Percentile: | 169,899 | 264.52% |

| >100% | 46,010 | 24.37% | 100.00% | 95th Percentile: | 179,338 | 536.49% |

| Total: | 188,777 | 100.00% | 100.00% | 99th Percentile: | 186,889 | 2760.82% |

| Linear Regression Results | ||||||

| N | Adj. R-square | Beta | t-value | p-value | ||

| 188,776 | 0.064 | 0.259 | 113.678 | 0.000 | ||

| Strata of Abs. ERRORS | Count of Firm-Years | Percent of Total Firm-Years | Cumulative Percent of Firm-Years | Percentile of Firm-Years | Ordered Obs. | Percentiles of Abs. Values of Estimate Errors |

|---|---|---|---|---|---|---|

| 0–5% | 211 | 24.25% | 24.25% | 1st Percentile: | 9 | 0.30% |

| 5–10% | 199 | 22.87% | 47.13% | 5th Percentile: | 44 | 1.05% |

| 10–15% | 112 | 12.87% | 60.00% | 10th Percentile: | 87 | 1.88% |

| 15–20% | 71 | 8.16% | 68.16% | 25th Percentile: | 218 | 5.20% |

| 20–25% | 54 | 6.21% | 74.37% | Median: | 435 | 11.00% |

| 25–50% | 119 | 13.68% | 88.05% | 75th Percentile: | 653 | 26.09% |

| 50–100% | 55 | 6.32% | 94.37% | 90th Percentile: | 783 | 58.06% |

| >100% | 49 | 5.63% | 100.00% | 95th Percentile: | 827 | 112.23% |

| Total: | 870 | 100.00% | 100.00% | 99th Percentile: | 861 | 475.18% |

| Linear Regression Results | ||||||

| N | Adj. R-square | Beta | t-value | p-value | ||

| 869 | 0.354 | 0.936 | 21.846 | <0.001 | ||

| Strata of Abs. Errors | Count of Firm-Years | Percent of Total Firm-Years | Cumulative Percent of Firm-Years | Percentile of Firm-Years | Ordered Obs. | Percentile of Abs. Values of Estimate Errors |

|---|---|---|---|---|---|---|

| 0–5% | 4821 | 4.26% | 10.40% | 1st Percentile: | 1131 | 1.18% |

| 5–10% | 4750 | 4.20% | 21.93% | 5th Percentile: | 5656 | 5.85% |

| 10–15% | 4629 | 4.09% | 29.82% | 10th Percentile: | 11,313 | 11.88% |

| 15–20% | 4446 | 3.93% | 36.59% | 25th Percentile: | 28,282 | 31.64% |

| 20–25% | 4276 | 3.78% | 43.86% | Median: | 56,564 | 84.92% |

| 25–50% | 17758 | 15.70% | 66.17% | 75th Percentile: | 84,846 | 323.61% |

| 50–100% | 19555 | 17.29% | 83.21% | 90th Percentile: | 101,815 | 1133.40% |

| >100% | 52893 | 46.76% | 100.00% | 95th Percentile: | 107,472 | 2721.74% |

| Total: | 113128 | 100.00% | 100.00% | 99th Percentile: | 111,997 | 11201800.00% |

| Linear Regression Results | ||||||

| N | Adj. R-square | Beta | t-value | p-value | ||

| 11,3127 | 0.017 | 0.068 | 44.867 | 0.001 | ||

| SIC 1-Digit Code | Adj. R-Square | N | Beta | t-Value | p-Value |

|---|---|---|---|---|---|

| SIC 1 | 0.189 | 23,964 | 0.766 | 74.857 | <0.000 |

| SIC 2 | 0.121 | 45,264 | 0.577 | 78.762 | <0.000 |

| SIC 3 | 0.123 | 70,319 | 0.613 | 99.135 | <0.000 |

| SIC 4 | 0.116 | 31,756 | 0.484 | 64.536 | <0.000 |

| SIC 5 | 0.058 | 24,620 | 0.271 | 39.007 | <0.000 |

| SIC 6 | 0.155 | 69,199 | 0.596 | 112.75 | <0.000 |

| SIC 7 | 0.067 | 40,437 | 0.444 | 54.043 | <0.000 |

| SIC 8 | 0.107 | 11,182 | 0.54 | 36.586 | <0.000 |

| SIC 9 | 0.087 | 1299 | 0.542 | 11.168 | <0.000 |

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2024 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Lambert, S.L.; Krieger, K.; Mauck, N. Predicting Operating Income via a Generalized Operating-Leverage Model. Int. J. Financial Stud. 2024, 12, 11. https://doi.org/10.3390/ijfs12010011

Lambert SL, Krieger K, Mauck N. Predicting Operating Income via a Generalized Operating-Leverage Model. International Journal of Financial Studies. 2024; 12(1):11. https://doi.org/10.3390/ijfs12010011

Chicago/Turabian StyleLambert, Sherwood Lane, Kevin Krieger, and Nathan Mauck. 2024. "Predicting Operating Income via a Generalized Operating-Leverage Model" International Journal of Financial Studies 12, no. 1: 11. https://doi.org/10.3390/ijfs12010011

APA StyleLambert, S. L., Krieger, K., & Mauck, N. (2024). Predicting Operating Income via a Generalized Operating-Leverage Model. International Journal of Financial Studies, 12(1), 11. https://doi.org/10.3390/ijfs12010011