Management Accounting Practices in the Hospitality Industry: The Portuguese Background

Abstract

1. Introduction

- What practices are identified in MA research applied to the Portuguese hospitality industry?

- What is the global productivity in MA research applied to the Portuguese hospitality industry, and what are the most prominent topics?

- What is the position of Portuguese research in MA applied to the hospitality industry compared to research worldwide?

2. Materials and Methods

2.1. Methods Used

- To identify the most used practices in MA research applied to the Portuguese hospitality industry.

- To assess productivity and to determine the most prominent topics in MA research applied to the Portuguese hospitality industry.

- To compare the evolution of Portuguese research on MA applied to the hospitality industry and its positioning in relation to the global level.

2.2. Data Collection and Organization Procedures

2.3. Data Analysis Techniques and Procedures

3. Results and Discussion

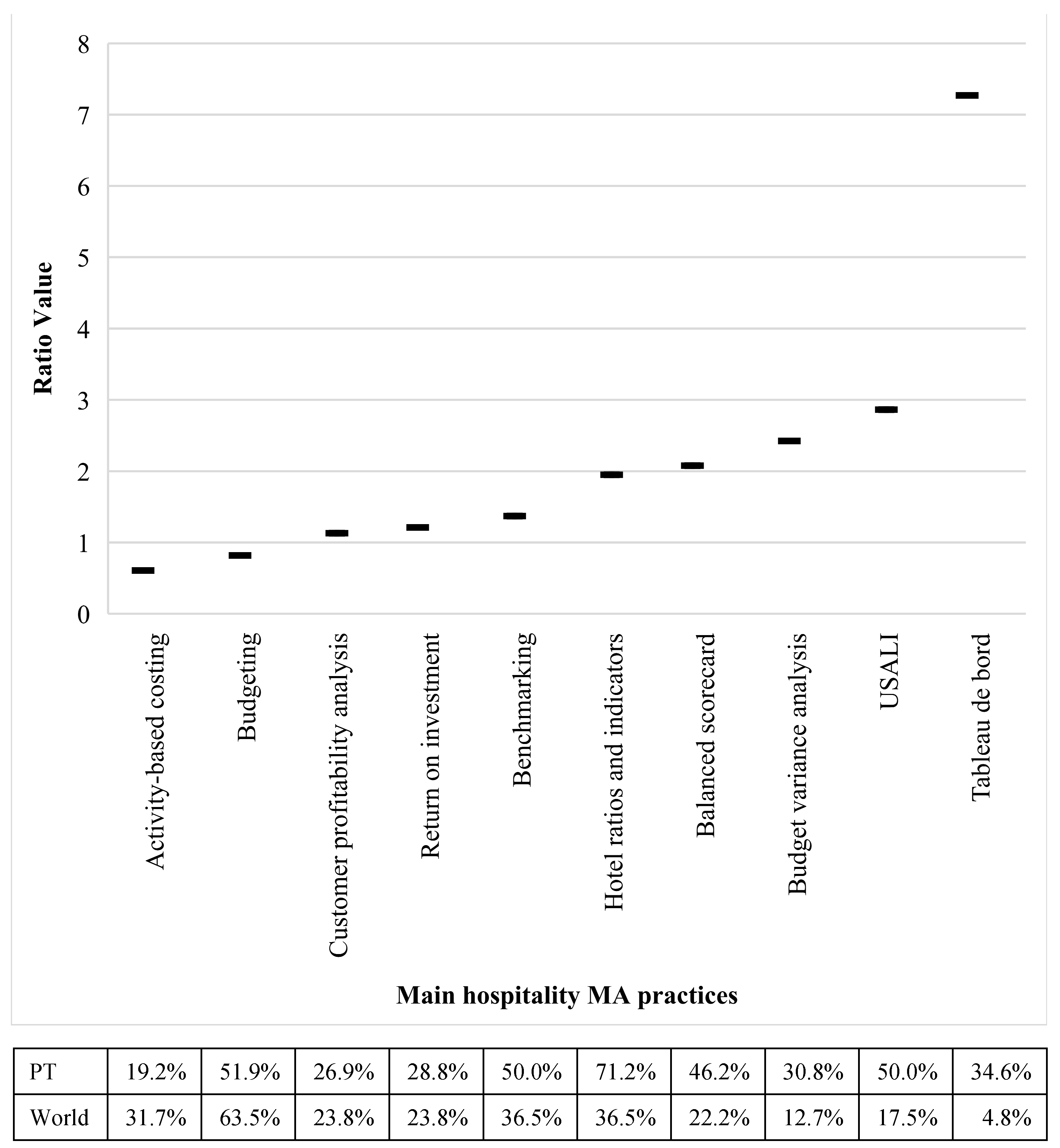

3.1. Most Used Practices in MA Research

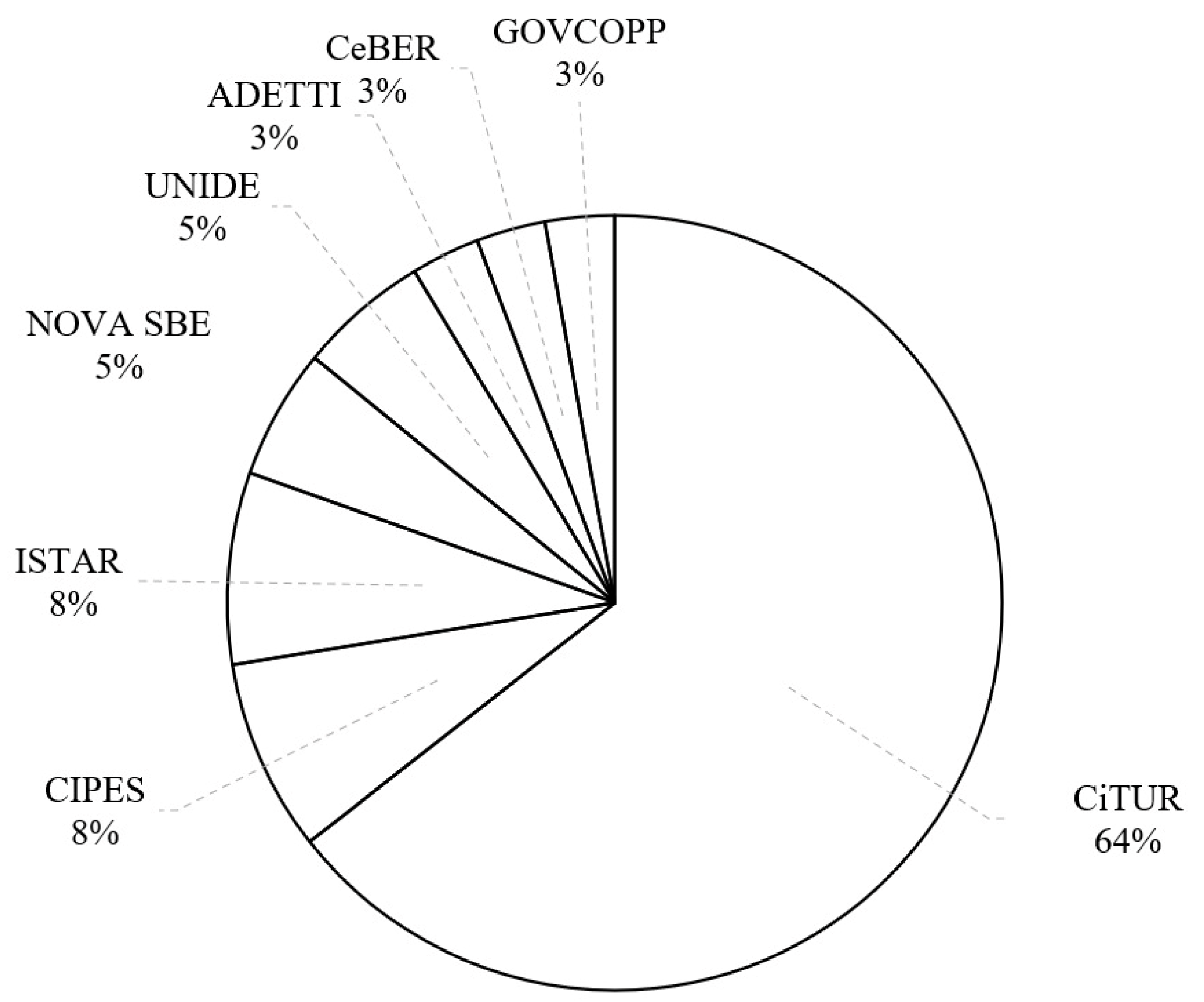

3.2. Productivity and the Most Prominent Topics

3.3. Comparing Portuguese Hospitality MA Research with the Global Level

4. Conclusions

4.1. The Most Used Practices in MA Research Applied to the Portuguese Hospitality Industry

4.2. The Productivity in MA Research Applied to the Portuguese Hospitality Industry

4.3. The Most Prominent Topics in MA Research Applied to the Portuguese Hospitality Industry

4.4. Comparison of the Evolution of the Portuguese Hospitality MA Research and ITS Positioning in Relation to the Global Level

4.5. Contributions, Implications, and Future Research

Author Contributions

Funding

Data Availability Statement

Conflicts of Interest

Appendix A. Studies of the Sample

| No. | Authors | No. | Authors |

| 1 | Lima Santos, L.; Gomes, C.; Arroteia, N.; Coelho, J.; Silva, P. | 27 | Paiva, I. S.; Reis, P.; Lourenço, I. |

| 2 | Lima Santos, L.; Gomes, C.; Arroteia, N. | 28 | Faria, A. R.; Ferreira, L.; Trigueiros, D. |

| 3 | Lima Santos, L.; Gomes, C.; Arroteia, N. | 29 | Faria, A. R.; Ferreira, L.; Trigueiros, D. |

| 4 | Lima Santos, L.; Gomes, C.; Arroteia, N. | 30 | Malheiros, C.; Gomes, C.; Lima Santos, L.; Cardoso, P. |

| 5 | Faria, A.; Trigueiros, D.; Ferreira, L. | 31 | Gomes, C.; Lima Santos, L.; Malheiros, C.; Cardoso, P. |

| 6 | Cruz, I.; Scapens, R.; Major, M. | 32 | Lima Santos, L.; Malheiros, C.; Gomes, C.; |

| 7 | Nunes, C.; Machado, M. | 33 | Faria, A. R.; Ferreira, L.; Trigueiros, D. |

| 8 | Nunes, C.; Machado, M. | 34 | Faria, A. R.; Ferreira, L.; Trigueiros, D. |

| 9 | Gomes, C.; Arroteia, N.; Lima Santos, L. | 35 | Lima Santos, L.; Gomes, C.; Malheiros, C. |

| 10 | Lamelas, J.; Filipe, J. | 36 | Silva, C.; Lima Santos, L.; Gomes, C.; Malheiros, C. |

| 11 | Nunes, R.; Machado, M. | 37 | Tourita, Í.; Gomes, C.; Malheiros, C.; Lima Santos, L. |

| 12 | Lima Santos, L.; Gomes, C.; Arroteia, N.; Almeida, P. | 38 | Rolim, M.; Malheiros, C.; Gomes, C.; Lima Santos, L. |

| 13 | Gomes, C.; Lima Santos, L.; Arroteia, N. | 39 | Pãozinho, R.; Lima Santos, L.; Gomes, C.; Malheiros, C. |

| 14 | Arroteia, N.; Lima Santos, L.; Gomes, C. | 40 | Ribeiro, M.; Vasconcelos, M.; Rocha, F. |

| 15 | Lima Santos, L.; Gomes, C.; Arroteia, N.; Almeida, P. | 41 | Campos, F.; Gomes, C.; Lima Santos, L. |

| 16 | Brito, A. | 42 | Carrera, C.; Gomes, C.; Lima Santos, L. |

| 17 | Quesado, P.; Guzmán, B.; Rodrigues, L. | 43 | Metreveli, M.; Lima Santos, L.; Gomes, C.; Mendes, A. |

| 18 | Nunes, C.; Machado, M. | 44 | Lima Santos, L.; Malheiros, C.; Gomes, C.; Guerra, T. |

| 19 | Faria, A. R.; Trigueiros, D.; Ferreira, L. | 45 | Pedroso, E.; Gomes, Carlos |

| 20 | Faria, A. R.; Trigueiros, D.; Ferreira, L. | 46 | Machado, M.; Nunes, C. |

| 21 | Gomes, C.; Lima Santos, L.; Arroteia, N. | 47 | Nunes, C.; Machado, M. |

| 22 | Borges, S.; Gustavo, N. | 48 | Costa, R.; Mota, J. |

| 23 | Correia, Henrique; Lima Santos, L.; Gomes, C.; Ribeiro Ferreira, R. | 49 | Lima Santos, L.; Gomes, C.; Lisboa, I. |

| 24 | Casqueira, N.; Gomes, C.; Lima Santos, L.; Malheiros, C.; Ribeiro Ferreira, R. | 50 | Lima Santos, L.; Gomes, C.; Malheiros, C. |

| 25 | Vieira Alves, D.; Lima Santos, L.; Malheiros, C. | 51 | Nunes, C.; Machado, M. |

| 26 | Sousa Paiva, I.; Lourenço, I. | 52 | Machado, M.; Nunes, C. |

References

- Agapito, Dora. 2020. The senses in tourism design: A bibliometric review. Annals of Tourism Research 83: 102934. [Google Scholar] [CrossRef]

- Aladwan, Mohammad, Omar Alsinglawi, and Omar Alhawatmeh. 2018. The applicability of target costing in jordanian hotels industry. Academy of Accounting and Financial Studies Journal 22: 1–13. Available online: https://www.researchgate.net/publication/328722978 (accessed on 30 April 2022).

- Almeida, Giovana, and Lucília Cardoso. 2022. Discussions between Place Branding and Territorial Brand in Regional Development—A Classification Model Proposal for a Territorial Brand. Sustainability 14: 6669. [Google Scholar] [CrossRef]

- Alves, Diana, Cátia Malheiros, and Conceição Gomes. 2019. Spa Metrics for Performance Evaluation. Tourism and Hospitality International Journal 13: 12–36. [Google Scholar]

- Bassotto, Leandro, Marcos Lopes, Mozar Brito, and Gideon Benedicto. 2021. Productive efficiency and risks for dairy farms: An integrative review. Revista de Economia e Sociologia Rural 60: 1–20. [Google Scholar] [CrossRef]

- Bastos, Bernardo Pereira. 2022. Contribution of hotels’ revenue management for supply chain sustainability. Journal of Revenue and Pricing Management. in press. [Google Scholar] [CrossRef]

- Borges, António, João Macedo, António Moreira, and Helena Isidro. 1998. Financial Accounting Practices, 1st ed. Lisbon: Áreas Editora. [Google Scholar]

- Brito, Aida. 2014. Applicability of Management Accounting Systems by Accommodation Units. In Innovation, Management and Education in Tourism and Hospitality, 1st ed. Edited by Gonçalo Fernandes, Anabela Sardo, José Martins and António Melo. Guarda: Polytechnic Institute of Guarda. Available online: http://hdl.handle.net/10314/2349 (accessed on 20 April 2022).

- Bufrem, Leilah, and Yara Prates. 2005. Recorded scientific knowledge and information measuring practices. Information Science 34: 9–25. [Google Scholar] [CrossRef]

- Campos, Filipa, Conceição Gomes, and Luís Lima Santos. 2020. Comparative Analysis of USALI, USAR and USFRS. Tourism and Hospitality International Journal 14: 91–113. [Google Scholar]

- Campos, Filipa, Luís Lima Santos, Conceição Gomes, and Lucília Cardoso. 2022. Management Accounting Practices in the Hospitality Industry: A Systematic Review and Critical Approach. Tourism and Hospitality 3: 243–64. [Google Scholar] [CrossRef]

- Cardoso, Lucília, Arthur Araújo, Luís Lima Santos, Zélia Breda, Carlos Costa, and Roland Schegg. 2021. Country performance analysis of swiss tourism, leisure and hospitality management research. Sustainability 13: 2378. [Google Scholar] [CrossRef]

- Cardoso, Lucília, Meng-Mei Chen, Arthur Araújo, Giovana Almeida, Francisco Dias, and Luiz Moutinho. 2022. Accessing Neuromarketing Scientific Performance: Research Gaps and Emerging Topics. Behavioral Sciences 12: 55. [Google Scholar] [CrossRef]

- Cardoso, Lucília, Rui Silva, Giovana Almeida, and Luís Lima Santos. 2020. A bibliometric model to analyze country research performance: Scival topic prominence approach in tourism, leisure and hospitality. Sustainability 12: 9897. [Google Scholar] [CrossRef]

- Carrera, Carla, Conceição Gomes, and Luís Lima Santos. 2020. Avaliação das empresas hoteleiras em função do VAL. Tourism and Hospitality International Journal 15: 12–39. [Google Scholar]

- Casqueira, Nuno, Conceição Gomes, Luís Lima Santos, Cátia Malheiros, and Raúl Ferreira. 2016. Performance evaluation of small independent hotels through management accounting indicators and ratios. Paper presented at the A Pathway for the New Generation of Tourism Research: Proceedings of the 2nd EATSA Conference, Peniche, Portugal, July 28–29. [Google Scholar]

- Chen, Jianan, Yoon Koh, and Seoki Lee. 2011. Does the market care about RevPAR? A case study of five large U.S. lodging chains. Journal of Hospitality and Tourism Research 35: 258–73. [Google Scholar] [CrossRef]

- Correia, Henrique, Luís Lima Santos, Conceição Gomes, and Raúl Ferreira. 2016. USALI Adapted to the Small Independent Hotels. Paper presented at the A Pathway for the New Generation of Tourism Research: Proceedings of the 2nd EATSA Conference, Peniche, Portugal, July 28–29. [Google Scholar]

- Costa, Rui, and Jorge Mota. 2021. Earnings management in hospitality firms: Evidence from Portugal. Tourism 69: 578–94. [Google Scholar] [CrossRef]

- Faria, Ana Rita, Duarte Trigueiros, and Leonor Ferreira. 2012. Costing and Management Control Practices in the Algarve Hotel Sector. Tourism & Management Studies 8: 100–7. Available online: https://search.ebscohost.com/login.aspx?direct=true&db=edssci&AN=edssci.S2182.84582012000100011& (accessed on 5 March 2022).

- Faria, Ana Rita, Duarte Trigueiros, and Leonor Ferreira. 2015. Budgeting practices in the hotel sector the case of the Algarve. Paper presented at the VI Postgraduate Conference ESGHT–Management, Hospitality & Tourism, Faro, Portugal, July 10. [Google Scholar]

- Faria, Ana Rita, Leonor Ferreira, and Duarte Trigueiros. 2017. Performance Measurement in Hotels: The Case of the Algarve (Portugal). XIX Seminário Luso-Espanhol (SLE) de Economia Empresarial. Available online: https://www.researchgate.net/publication/321167961_Performance_measurement_in_hotels_the_case_of_the_Algarve (accessed on 26 November 2021).

- Faria, Ana Rita, Leonor Ferreira, and Duarte Trigueiros. 2018a. Analyzing customer profitability in hotels using activity-based costing. Tourism & Management Studies 14: 65–74. [Google Scholar] [CrossRef]

- Faria, Ana Rita, Leonor Ferreira, and Duarte Trigueiros. 2018b. Budgeting in Algarve hotels: Alignment with international practice. Dos Algarves: A Multidisciplinary e-Journal 34: 3–25. [Google Scholar] [CrossRef]

- Foris, Diana, Alina Tecau, Madalina Hartescu, and Tiberiu Foris. 2019. Relevance of the features regarding the performance of booking websites. Tourism Economics 26: 1021–41. [Google Scholar] [CrossRef]

- Gietaneh, Wodaje, Atsede Alle, Muluneh Alene, Moges Agazhe Assemie, Muluye Molla Simieneh, and Molla Yigzaw Birhanu. 2022. Quality disparity in terms of clients’ satisfaction with selected exempted health care services provided in Ethiopia: Meta-analysis. Health Policy OPEN 3: 100068. [Google Scholar] [CrossRef]

- Gil, António. 2008. Métodos e Técnicas de Pesquisa Social, 6th ed. São Paulo: Atlas S.A. [Google Scholar] [CrossRef]

- Gomes, Conceição, Luís Lima Santos, and Nuno Arroteia. 2015. The adoption of USALI in hotel companies in Portugal. Paper presented at XV CICA, Coimbra, Portugal, June 11–12. [Google Scholar]

- Gomes, Conceição, Nuno Arroteia, and Luís Lima Santos. 2011. Management accounting in Portuguese hotel enterprises: The influence of organizational and cultural factors. Paper presented at GBATA Conference “Fulfilling the Worldwide Sustainability Challenge: Strategies, Innovations, and Perspectives for Forward Momentum in Turbulent Times”, Istanbul, Turkey, July 12–16. [Google Scholar]

- Gonçalves, Miguel. 2010. Subsidies for the prehistory of the first accounting teaching establishment in Portugal. Review of Business and Legal Sciences 17: 175–99. [Google Scholar] [CrossRef]

- Górska-Warsewicz, Hanna, and Olena Kulykovets. 2020. Hotel brand loyalty: A systematic literature review. Sustainability 12: 4810. [Google Scholar] [CrossRef]

- Govella, Nicodem, Deodatus Maliti, Amos Mlwale, John Masallu, Nosrat Mirzai, Paul Johnson, Heather Ferguson, and Gerry Killeen. 2016. An improved mosquito electrocuting trap that safely reproduces epidemiologically relevant metrics of mosquito human-feeding behaviours as determined by human landing catch. Malaria Journal 15: 1–17. [Google Scholar] [CrossRef] [PubMed]

- HANYC. 2014. Uniform System of Accounts for the Lodging Industry, 11th ed. New York: Hotel Association of New York City, Inc. [Google Scholar]

- Hochrein, Simon, and Christoph Glock. 2012. Systematic literature reviews in purchasing and supply management research: A tertiary study. International Journal of Integrated Supply Management 7: 215–45. [Google Scholar] [CrossRef]

- Huang, Mu Hsuan, Chi Shiou Lin, and Dar Zen Chen. 2011. Counting methods, country rank changes, and counting inflation in the assessment of national research productivity and impact. Journal of the American Society for Information Science and Technology 62: 2427–36. [Google Scholar] [CrossRef]

- Iloranta, Riina. 2022. Luxury tourism—A review of the literature. European Journal of Tourism Research 30: 3007. [Google Scholar] [CrossRef]

- Jones, Tracy. 2008. Improving hotel budgetary practice—A positive theory model. International Journal of Hospitality Management 27: 529–40. [Google Scholar] [CrossRef]

- Korstanje, Maximiliano. 2021. The decline of book reviews in tourism discipline. Journal of Tourism, Heritage and Services Marketing 7: 76–78. [Google Scholar] [CrossRef]

- Koseoglu, Mehmet Ali, Roya Rahimi, Fevzi Okumus, and Jingyan Liu. 2016. Bibliometric studies in tourism. Annals of Tourism Research 61: 180–98. [Google Scholar] [CrossRef]

- Leong, Lai Ying, Teck Soon Hew, Garry Wei Han Tan, Keng Boon Ooi, and Voon Hsien Lee. 2021. Tourism research progress—A bibliometric analysis of tourism review publications. Tourism Review 76: 1–26. [Google Scholar] [CrossRef]

- Lima Santos, Luís, Cátia Malheiros, and Conceição Gomes. 2018. Do Stars Matter? A Comparison of Operating Ratios and Indicators Among Hotels. Paper presented at the X International Tourism Congress, Quito, Equador, November 13–15. [Google Scholar]

- Lima Santos, Luís, Conceição Gomes, Ana Rita Faria, Rogério Lunkes, Cátia Malheiros, Fabricia Silva da Rosa, and Catarina Nunes. 2016. Contabilidade de Gestão Hoteleira, 1st ed. Cacém: ATF Edições Técnicas. [Google Scholar]

- Lima Santos, Luís, Conceição Gomes, and Cátia Malheiros. 2019. Achieving a Competitive Management in Micro and Small Independent Hotels. In Multilevel Approach to Competitiveness in the Global Tourism Industry. Edited by Sérgio Teixeira and João Ferreira. Berlin: ResearchGate, pp. 229–55. [Google Scholar] [CrossRef]

- Lima Santos, Luís, Conceição Gomes, and Nuno Arroteia. 2010. As técnicas de contabilidade de gestão nas unidades hoteleiras portuguesas. Paper presented at the IV International Tourism Congress, Peniche, Portugal, November 24–25. [Google Scholar]

- Lima Santos, Luís, Conceição Gomes, and Nuno Arroteia. 2012. Management accounting practices in the Portuguese lodging industry. Journal of Modern Accounting and Auditing 8: 1–14. [Google Scholar]

- Lima Santos, Luís, Cátia Malheiros, Conceição Gomes, and Tânia Guerra. 2020a. TRevPAR as hotels performance evaluation indicator and influencing factors in Portugal. EATSJ-Euro-Asia Tourism Studies Journal 1: 93–105. [Google Scholar]

- Lima Santos, Luís, Conceição Gomes, Nuno Arroteia, and Paulo Almeida. 2014. The perception of management accounting in the Portuguese lodging industry. Paper presented at Managing in an Interconnected World: Pioneering Business and Technology Excellence, Baku, Azerbeijan, July 8–12. [Google Scholar]

- Lima Santos, Luís, Conceição Gomes, Cátia Malheiros, and Ana Lucas. 2021. Impact Factors on Portuguese Hotels’ Liquidity. Journal of Risk and Financial Management 14: 144. [Google Scholar] [CrossRef]

- Lima Santos, Luís, Lucília Cardoso, Noelia Araújo-Vila, and Jose Fraiz-Brea. 2020b. Sustainability perceptions in tourism and hospitality: A mixed-method bibliometric approach. Sustainability 12: 8852. [Google Scholar] [CrossRef]

- Lima Santos, Luís, Rui Silva, Lucília Cardoso, and Cidália Oliveira. 2022. Accounting and business management research: Tracking 50 years of country performance Accounting and business management research: Tracking 50 years of country performance. Academy of Accounting and Financial Studies Journal 26: 1–22. [Google Scholar]

- Lucas, Ana, Vera Pinto, and Paulo Gomes. 2022. Financial Accounting in the Hospitality and Restaurant Industry, 1st ed. Cacém: Lidel. [Google Scholar]

- Lunkes, Rogério, Daiane Bortoluzzi, Marcielle Anzilago, and Fabricia Rosa. 2020. Influence of online hotel reviews on the fit between strategy and use of management control systems: A study among small- and medium-sized hotels in Brazil. Journal of Applied Accounting Research 21: 615–34. [Google Scholar] [CrossRef]

- Machado, Maria, and Catarina Nunes. 2020. Performance evaluation methods in the services sector: Empirical study in hotels. International Journal of Services and Operations Management 37: 220–40. [Google Scholar] [CrossRef]

- Machado, Maria, and Catarina Nunes. 2021. Tableau de Bord and Balanced Scorecard: Knowledge dissemination in the hotel industry. International Journal of Productivity and Quality Management. Forthcoming. [Google Scholar] [CrossRef]

- Machado, Maria, and Miguel Silva. 2021. Knowledge and utilisation of the uniform system of accounts for the lodging industry: Evidence from Portugal. International Journal of Procurement Management 14: 400–412. [Google Scholar] [CrossRef]

- Malheiros, Cátia, Conceição Gomes, Luís Lima Santos, and Paula Cardoso. 2017. Are the independent hotels identified with USALI? Paper presented at the GBATA Conference 19th, Vienna, Austria, July 11–15. [Google Scholar]

- Metreveli, Marina, Luís Lima Santos, Conceição Gomes, and Alexandra Sofia Mendes. 2020. COVID-19 and its impact on hotel business. Paper presented at the XII International Tourism Congress, Gramado, Brazil, October 27–29. [Google Scholar]

- Mia, Lokman, and Anoop Patiar. 2002. The interactive effect of superior-subordinate relationship and budget participation on managerial performance in the hotel industry: An exploratory study. Journal of Hospitality and Tourism Research 26: 235–57. [Google Scholar] [CrossRef]

- Mkwizu, Kezia. 2021. Re-defining Domestic Tourism in the New Normal: A literature Review. Paper presented at the 3rd Africa-Asia Dialogue Network (AADN) International Conference on Advances in Business Management and Electronic Commerce Research, Ganzhou, China, November 26–28. [Google Scholar]

- Molinos, Diego, Daniel Mesquita, and Debora Hoff. 2016. ZipfTool: A bibliometric tool to aid theoretical research. Revista de Informática Teórica e Aplicada 23: 293–317. [Google Scholar] [CrossRef][Green Version]

- Nunes, Catarina, and Maria Machado. 2011. Mudança nos sistemas de controlo de gestão: Factores potenciadores e inibidores em hotéis de cinco estrelas. Paper presented at International Conference on Tourism & Management Studies, Faro, Portugal, October 26–29. [Google Scholar]

- Nunes, Catarina, and Maria Machado. 2012. Financial Assessment of Performance in the Hotel Industry. European Journal of Tourism, Hospitality and Recreation 3: 97–109. Available online: www.ejthr.com (accessed on 5 December 2021).

- Nunes, Catarina Rosa, and Maria João Cardoso Vieira Machado. 2020. Benchmarking in the hotel industry: The use of USALI. International Journal of Process Management and Benchmarking 10: 382–96. [Google Scholar] [CrossRef]

- Paul, Otlet. 1986. The book and measurement: Bibliometrics. In Bibliometrics: Theory and Practice, 9th ed. Edited by Edson Nery Fonseca. São Paulo: Cultrix, pp. 20–34. [Google Scholar]

- Paiva, Inna, and Isabel Lourenço. 2016. Determinants of earnings management in the hotel industry: An international perspective. Corporate Ownership and Control 14: 449–57. [Google Scholar] [CrossRef][Green Version]

- Paiva, Inna, Paulo Reis, and Isabel Lourenço. 2016. Research in hospitality management and accounting: A research synthesis and analysis of current literature and future challenges. Problems and Perspectives in Management 14: 83–91. [Google Scholar] [CrossRef][Green Version]

- Palmer, Alfonso, Albert Sesé, and Juan Jose Montaño. 2005. Tourism and statistics. Bibliometric study 1998-2002. Annals of Tourism Research 32: 167–78. [Google Scholar] [CrossRef]

- Paul, Justin, and Alex Criado. 2020. The art of writing literature review: What do we know and what do we need to know? International Business Review 29: 101717. [Google Scholar] [CrossRef]

- Pavlatos, Odysseas, and Ioannis Paggios. 2007. Cost accounting in Greek hotel enterprises: An empirical approach. Tourismos 2: 39–59. [Google Scholar]

- Pavlatos, Odysseas, and Ioannis Paggios. 2009. Management accounting practices in the Greek hospitality industry. Managerial Auditing Journal 24: 81–98. [Google Scholar] [CrossRef]

- Pedroso, Elsa, and Carlos Gomes. 2020. The effectiveness of management accounting systems in SMEs: A multidimensional measurement approach. Journal of Applied Accounting Research 21: 497–515. [Google Scholar] [CrossRef]

- Rolim, Maria, Cátia Malheiros, Conceição Gomes, and Luís Lima Santos. 2019. Determinante do TRevPAR: Uma análise dis hotéis entre 2010–2017. Paper presented at the XI International Tourism Congress, Madeira, Portugal, November 5–7; pp. 244–53. [Google Scholar]

- Souza, Paula, and Rogério Lunkes. 2015. Budgeting practices: A study on Brazilian hotel companies. Revista Brasileira de Pesquisa Em Turismo 9: 380–99. [Google Scholar] [CrossRef]

- Tourita, Íris, Conceição Gomes, Cátia Malheiros, and Luís Lima Santos. 2019. Accounting for dissimilarities in hospitality costs among Portuguese Regions. Paper presented at the XI International Tourism Congress, Madeira, Portugal, November 5–7; pp. 189–201. [Google Scholar]

- Urquidi-Martin, Ana, and Vicente Ripoll Feliu. 2013. The choice of management accounting techniques in the hotel sector: The role of contextual factors. Journal of Management Research 5: 65–82. [Google Scholar] [CrossRef]

- Uyar, Ali, and Necdet Bilgin. 2011. Budgeting practices in the Turkish hospitality industry: An exploratory survey in the Antalya region. International Journal of Hospitality Management 30: 398–408. [Google Scholar] [CrossRef]

- Zupic, Ivan, and Tomaž Čater. 2014. Bibliometric methods in management and organization. Organizational Research Methods 18: 429–72. [Google Scholar] [CrossRef]

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| Abstracts | Number of words before Zipf’s 1st law–stop words extraction |

| 52 | 9337 |

| Abstracts | Number of words after Zipf’s 1st law–stop words extraction |

| 52 | 5572 |

| Rank. | V. Name: | AF | RF | Rank. | V. Name | AF | RF |

|---|---|---|---|---|---|---|---|

| 1 | hotels | 119 | 0.021 | 22 | sector | 26 | 0.005 |

| 2 | hotel | 118 | 0.021 | 23 | operating | 23 | 0.004 |

| 3 | management | 108 | 0.019 | 24 | lodging | 20 | 0.004 |

| 4 | accounting | 77 | 0.014 | 24 | MA | 20 | 0.004 |

| 5 | used | 55 | 0.009 | 24 | most | 20 | 0.004 |

| 6 | USALI | 50 | 0.009 | 24 | systems | 20 | 0.004 |

| 7 | financial | 49 | 0.009 | 24 | through | 20 | 0.004 |

| 7 | study | 49 | 0.009 | 25 | accounts | 19 | 0.003 |

| 8 | industry | 46 | 0.008 | 25 | independent | 19 | 0.003 |

| 9 | performance | 45 | 0.008 | 25 | influence | 19 | 0.003 |

| 10 | Portuguese | 44 | 0.008 | 25 | main | 19 | 0.003 |

| 11 | indicators | 42 | 0.008 | 25 | one | 19 | 0.003 |

| 12 | techniques | 41 | 0.007 | 25 | paper | 19 | 0.003 |

| 13 | information | 39 | 0.007 | 25 | small | 19 | 0.003 |

| 14 | Portugal | 37 | 0.007 | 25 | tourism | 19 | 0.003 |

| 15 | between | 35 | 0.006 | 25 | uniform | 19 | 0.003 |

| 16 | ratios | 33 | 0.006 | 26 | knowledge | 18 | 0.003 |

| 17 | hospitality | 32 | 0.006 | 27 | adoption | 17 | 0.003 |

| 17 | system | 32 | 0.006 | 27 | characteristics | 17 | 0.003 |

| 18 | analysis | 31 | 0.006 | 27 | importance | 17 | 0.003 |

| 18 | managers | 31 | 0.006 | 27 | obtained | 17 | 0.003 |

| 19 | research | 30 | 0.005 | 27 | structure | 17 | 0.003 |

| 20 | results | 28 | 0.005 | 27 | studies | 17 | 0.003 |

| 21 | data | 27 | 0.005 | 27 | there | 17 | 0.003 |

| 22 | companies | 26 | 0.005 | 27 | whether | 17 | 0.003 |

| Hospitality MA Practices | Portuguese Ranking | World Ranking According to Campos et al. (2022) |

|---|---|---|

| Hotel ratios and indicators | 1st | 2nd |

| Budgeting | 2nd | 1st |

| USALI | 3rd | 6th |

| Benchmarking | 3rd | 2nd |

| Balanced scorecard | 4th | 5th |

| Tableau de bord | 5th | 13th |

| Budget variance analysis | 6th | 9th |

| Return on investment | 7th | 4th |

| Customer profitability analysis | 8th | 4th |

| Activity-based costing | 8th | 3rd |

| Strategic planning | 9th | 8th |

| Product profitability | 9th | 12th |

| Product life cycle costing | 9th | 9th |

| Kaizen costing | 10th | 15th |

| Target costing | 10th | 14th |

| Product costing | 10th | 7th |

| Economic value added | 10th | 13th |

| Break-even point | 10th | 10th |

| Activity-based budget | 10th | 13th |

| Revenue management | 11th | 11th |

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2022 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Campos, F.; Gomes, C.; Cardoso, L.; Lima Santos, L. Management Accounting Practices in the Hospitality Industry: The Portuguese Background. Int. J. Financial Stud. 2022, 10, 88. https://doi.org/10.3390/ijfs10040088

Campos F, Gomes C, Cardoso L, Lima Santos L. Management Accounting Practices in the Hospitality Industry: The Portuguese Background. International Journal of Financial Studies. 2022; 10(4):88. https://doi.org/10.3390/ijfs10040088

Chicago/Turabian StyleCampos, Filipa, Conceição Gomes, Lucília Cardoso, and Luís Lima Santos. 2022. "Management Accounting Practices in the Hospitality Industry: The Portuguese Background" International Journal of Financial Studies 10, no. 4: 88. https://doi.org/10.3390/ijfs10040088

APA StyleCampos, F., Gomes, C., Cardoso, L., & Lima Santos, L. (2022). Management Accounting Practices in the Hospitality Industry: The Portuguese Background. International Journal of Financial Studies, 10(4), 88. https://doi.org/10.3390/ijfs10040088