Asymptotic Dependence Modelling of the BRICS Stock Markets

Abstract

:1. Introduction

1.1. Market Linkages and Extremal Dependence

1.1.1. Stock Markets Linkages

1.1.2. Extremal Dependence

1.2. Reviews of Studies on BRICS

1.3. Contributions and Research Highlights

- The 90th percentile is a more suitable choice in preference to the higher variance 95th and 99th percentiles;

- The pair of Brazilian IBOV and Chinese SHCOMP markets, which have a fairly strong dependence under the CMEV modelling, produced a nearly weak dependence under the point process;

- Bivariate point process results showed that the model best describes all the 10 paired markets is the Husler–Reiss, with the lowest AIC value in each pair;

- The entire findings were consistent with the results obtained from the CMEV modelling;

- The only likely exception to the consistency was between the pair of Brazilian IBOV and Chinese SHCOMP markets, which has a fairly strong dependence under the CMEV modelling but produced a nearly weak dependence under the point process;

- Weak extremal (asymptotic) dependence between each of the 7 (out of 10) paired markets from extremal dependence modelling outcomes gives beneficial risk reduction and high investment returns through international portfolio diversifications;

- A fairly good investment opportunity derivable from international portfolio diversifications can also be expected because the extremal dependence between the markets in these market pairs is “fairly strong” as compared to the “weak asymptotic” dependence.

2. Materials and Methods

2.1. Conditional Multivariate Extreme Value Modelling

2.1.1. Marginal Transformation

2.1.2. Regression Model Structure

2.1.3. Laplace Margins

2.1.4. Threshold Selection

2.1.5. Extreme Value Mixture Models

Bulk Model-Based Tail Fraction Approach

Parameterised Tail Fraction Approach

2.1.6. Estimation of Parameters

2.2. Multivariate Point Processes

2.2.1. Overview

2.2.2. Bivariate Point Process Model

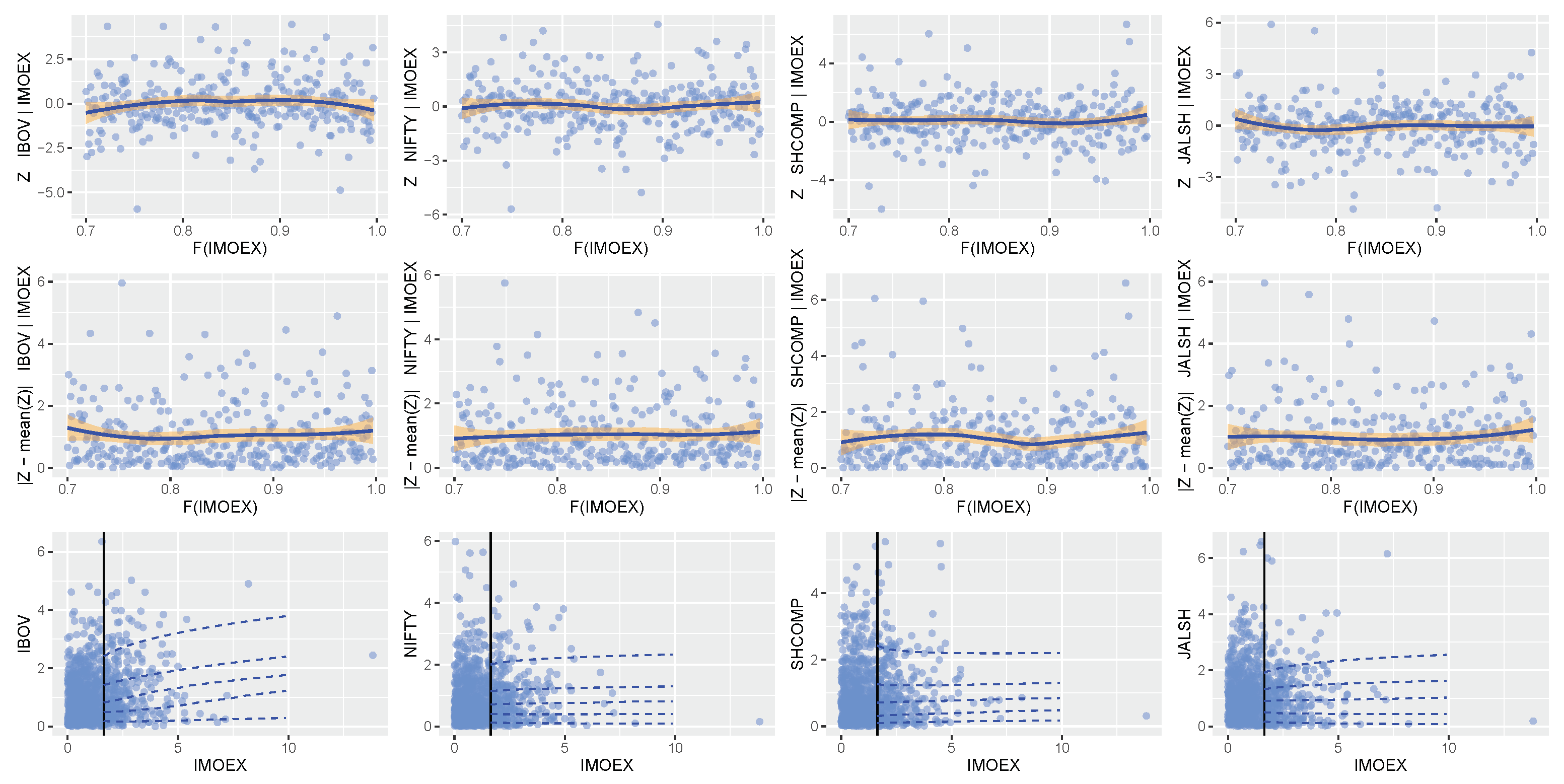

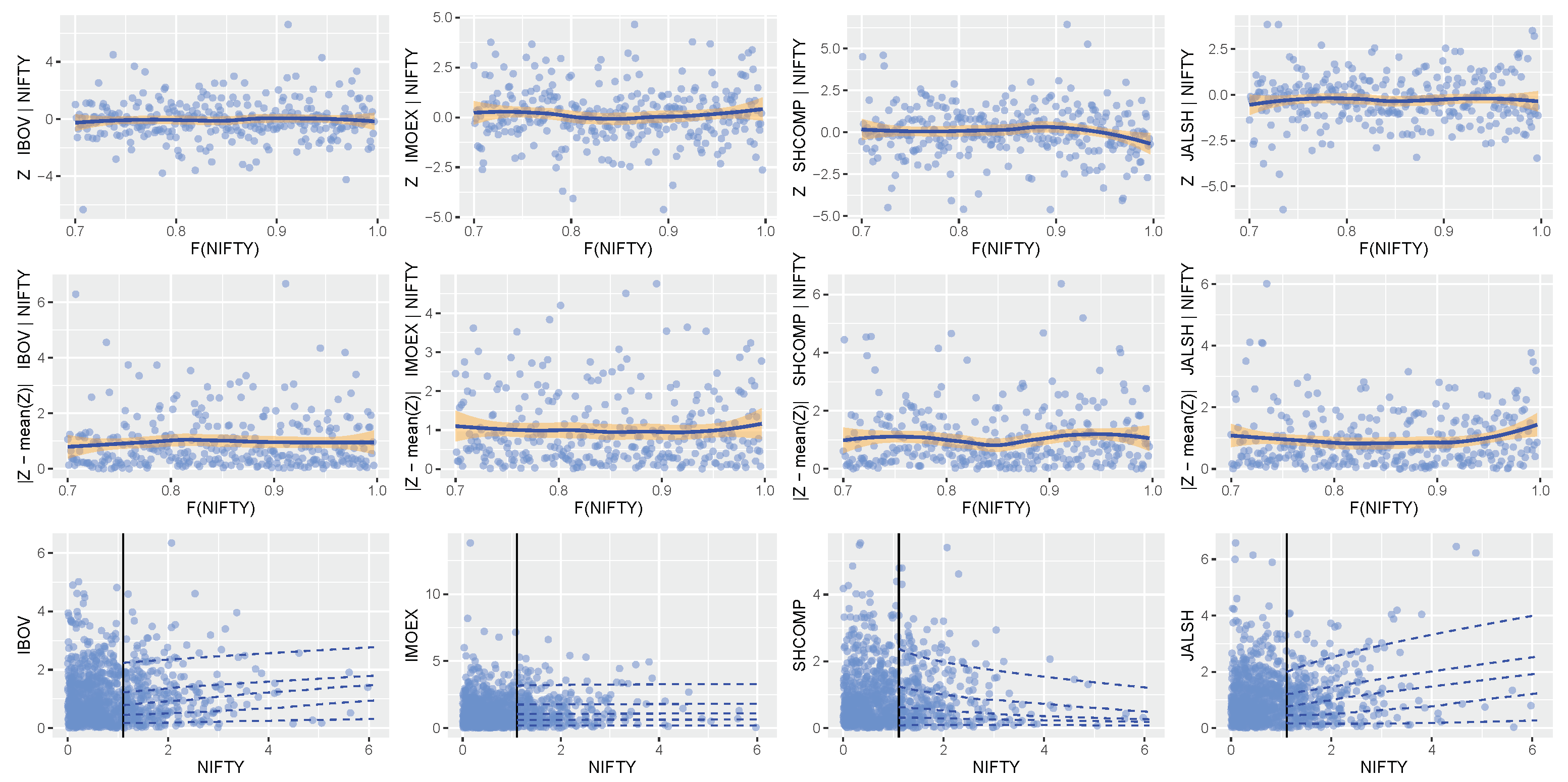

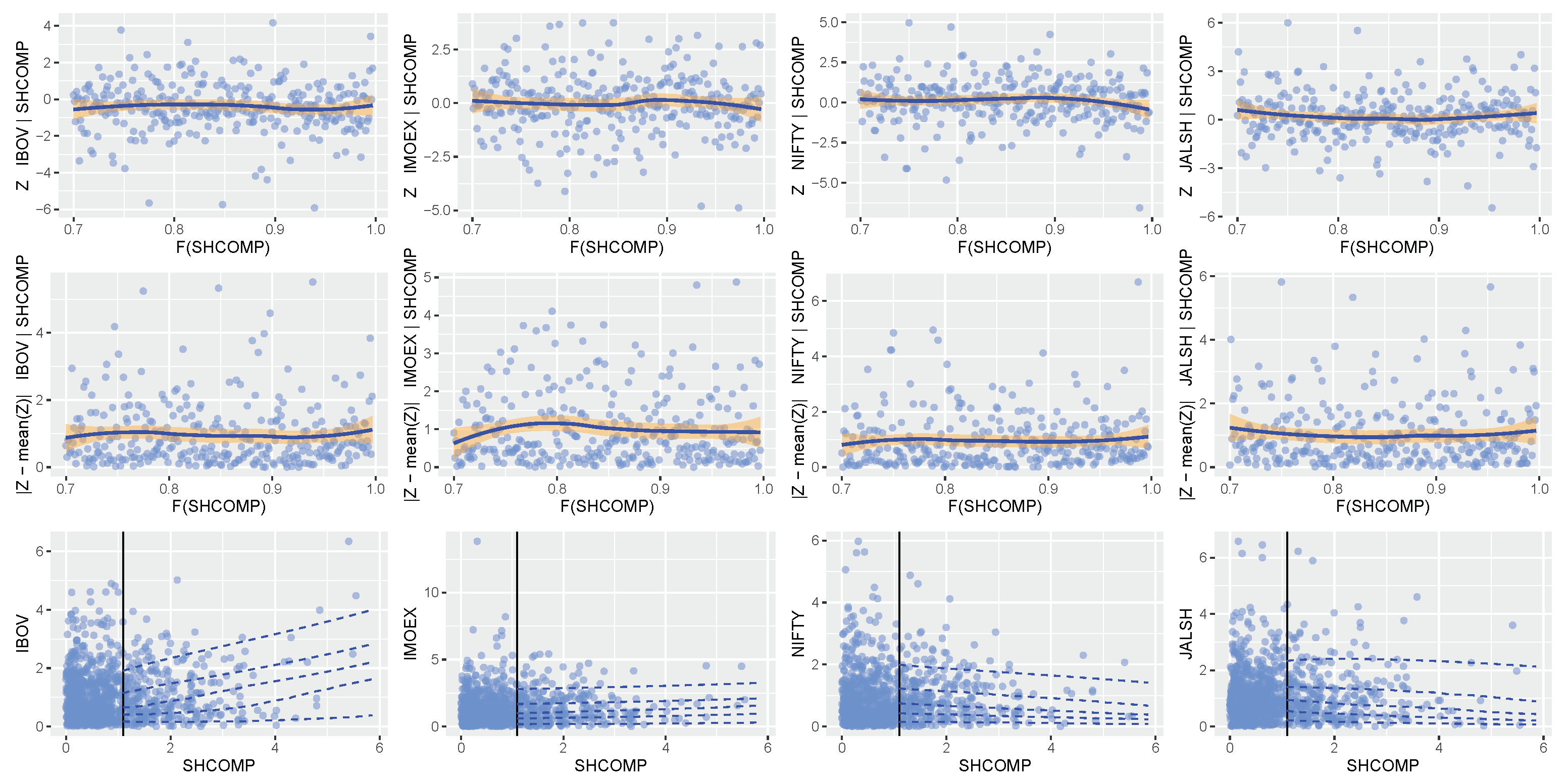

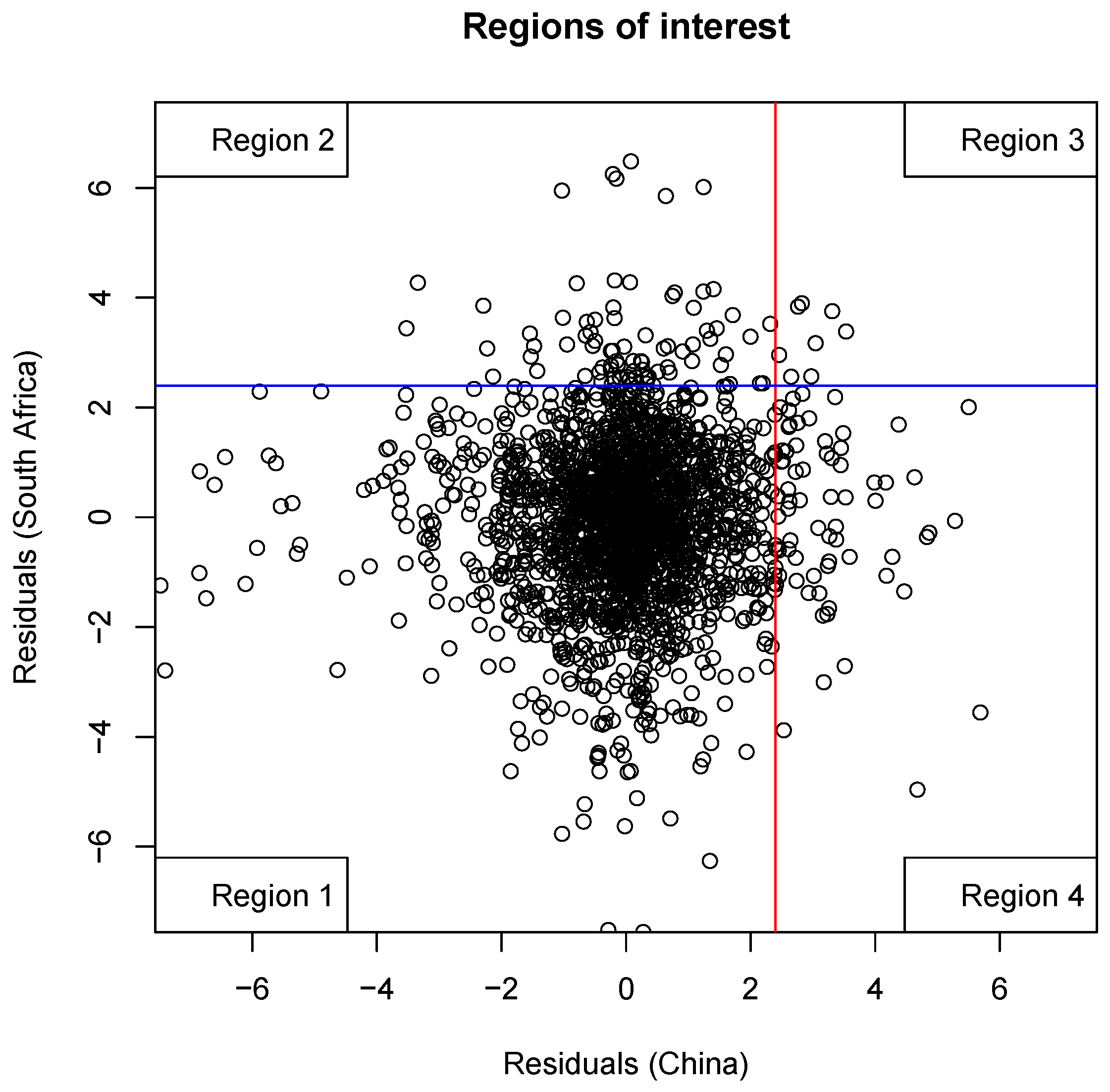

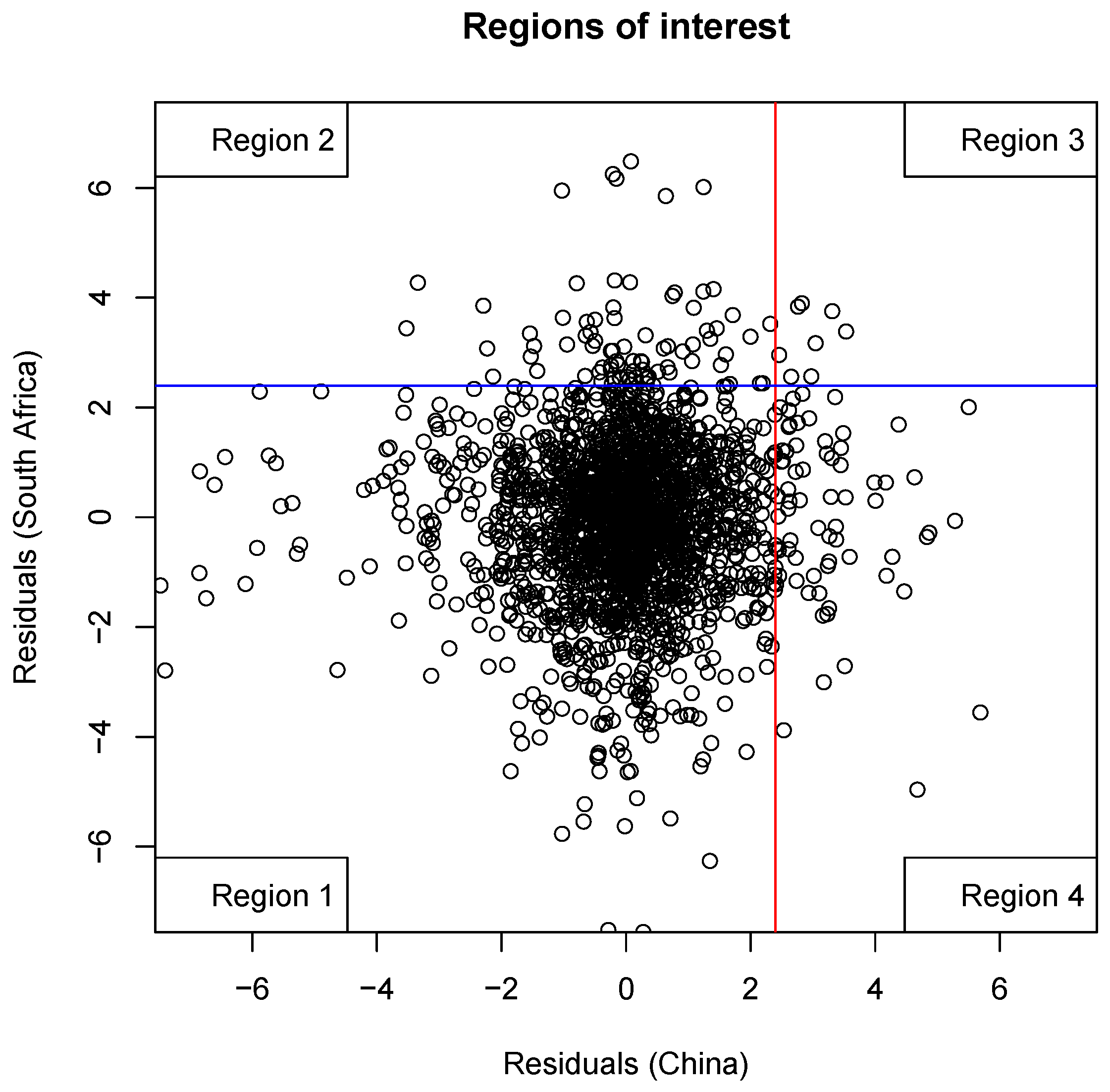

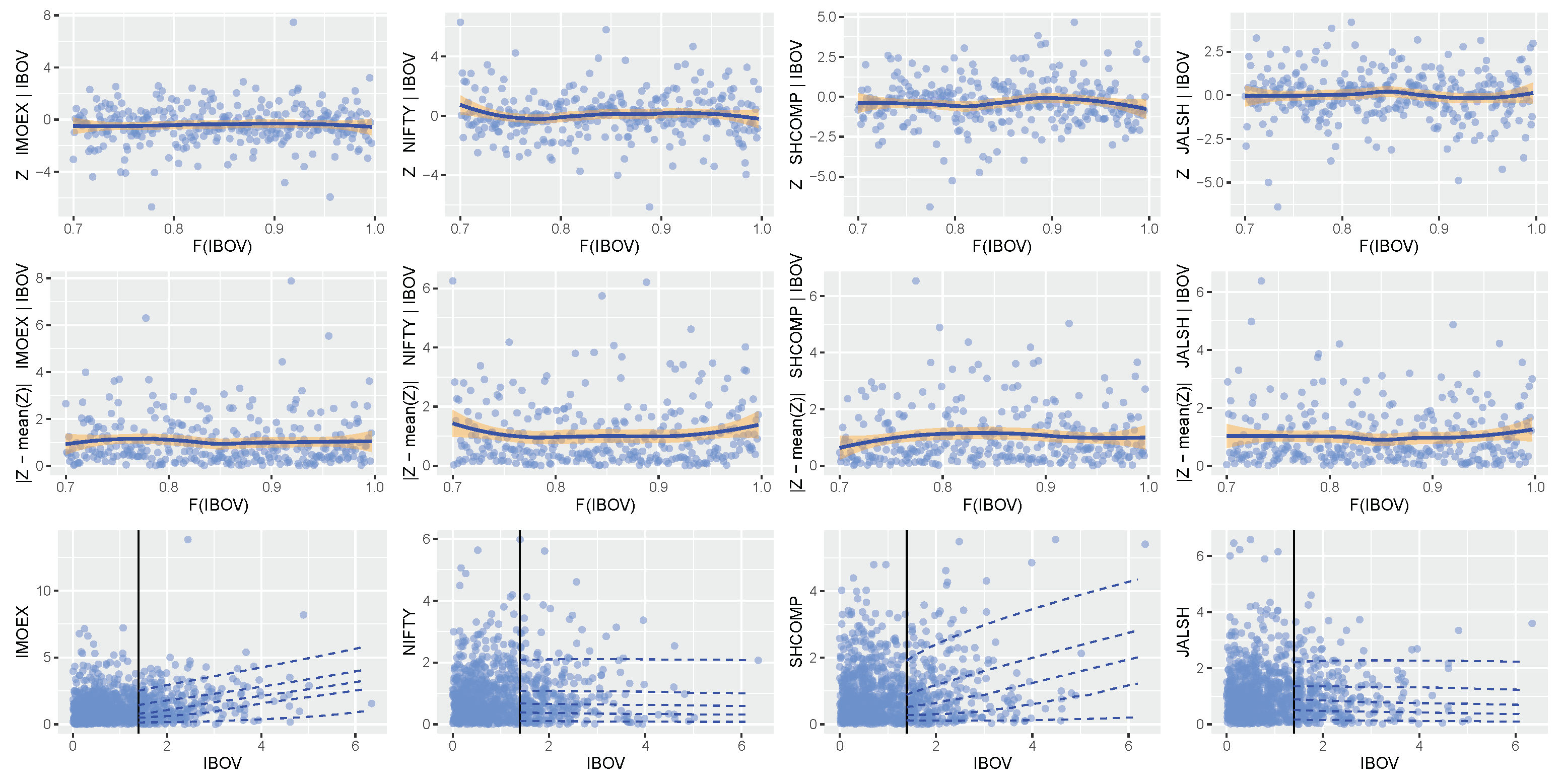

2.3. Diagnostics: Model Checking

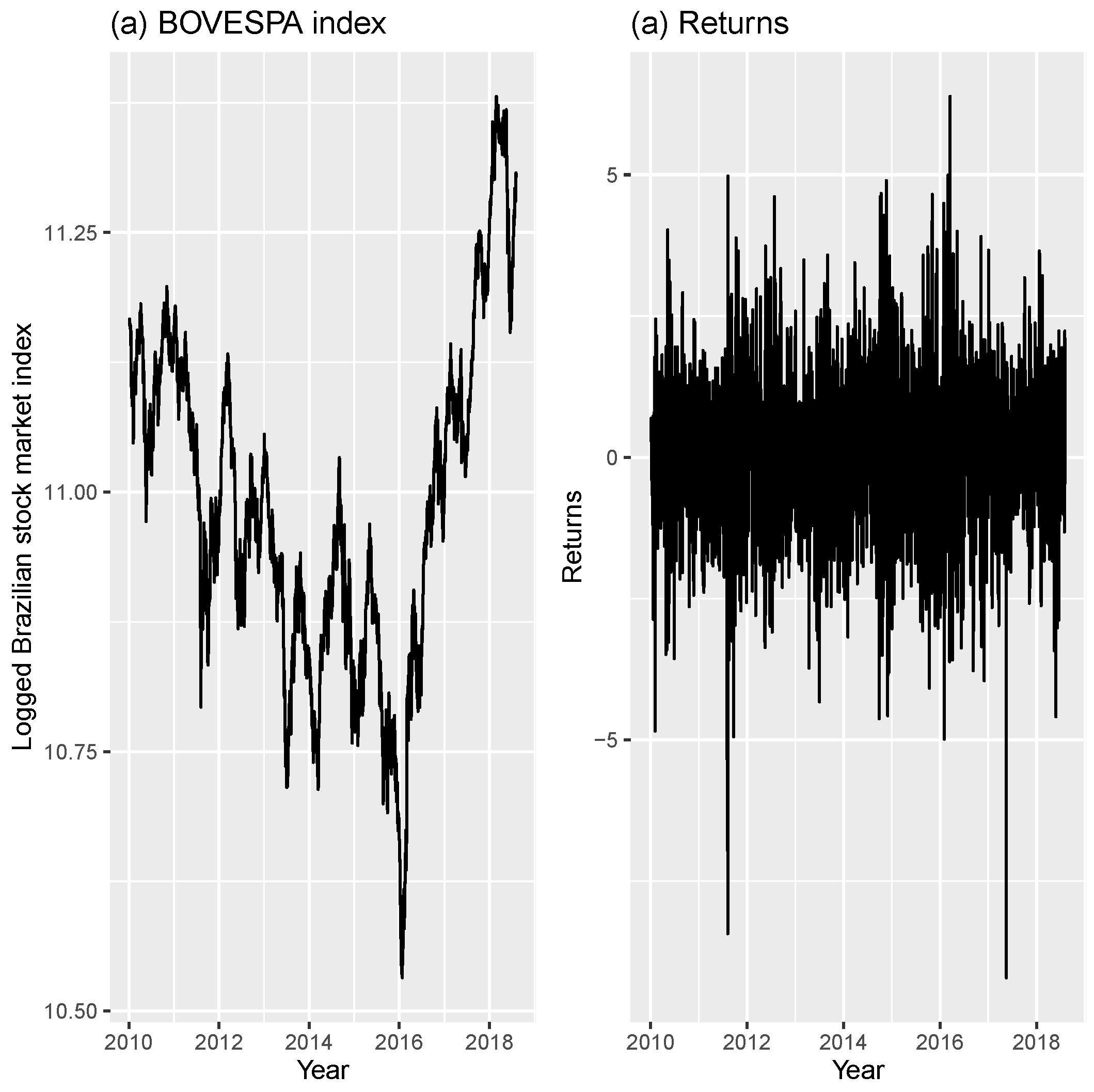

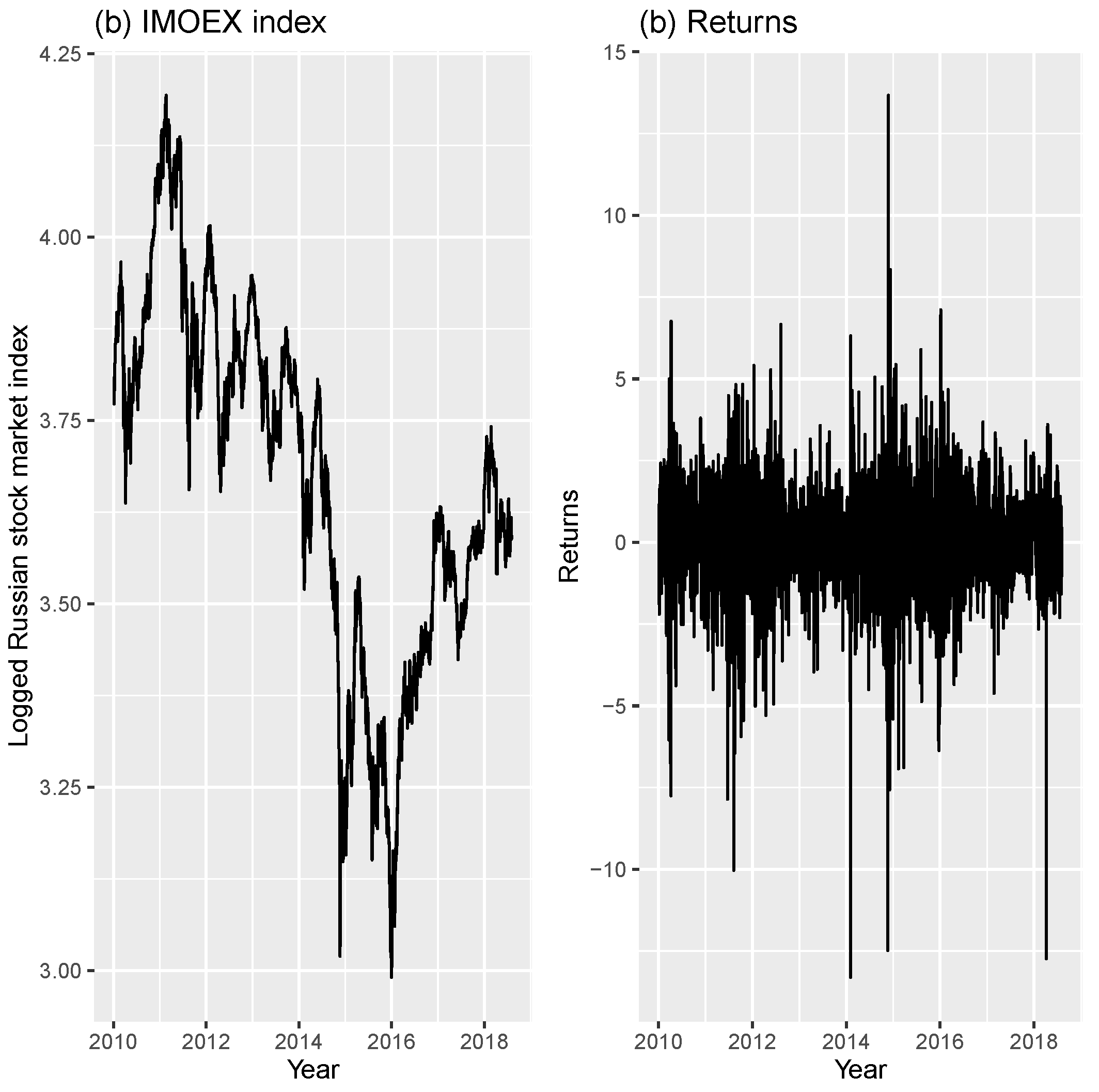

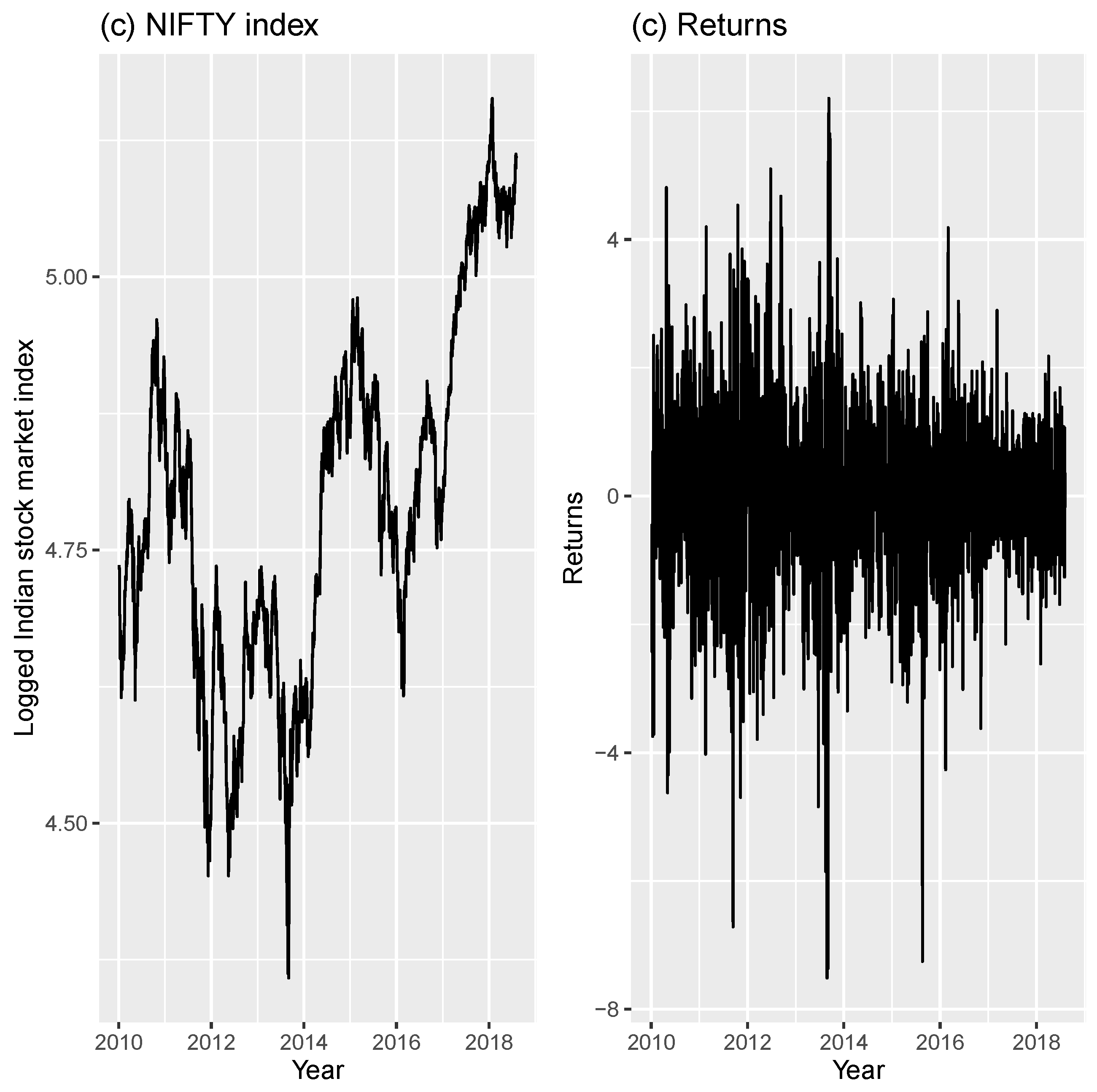

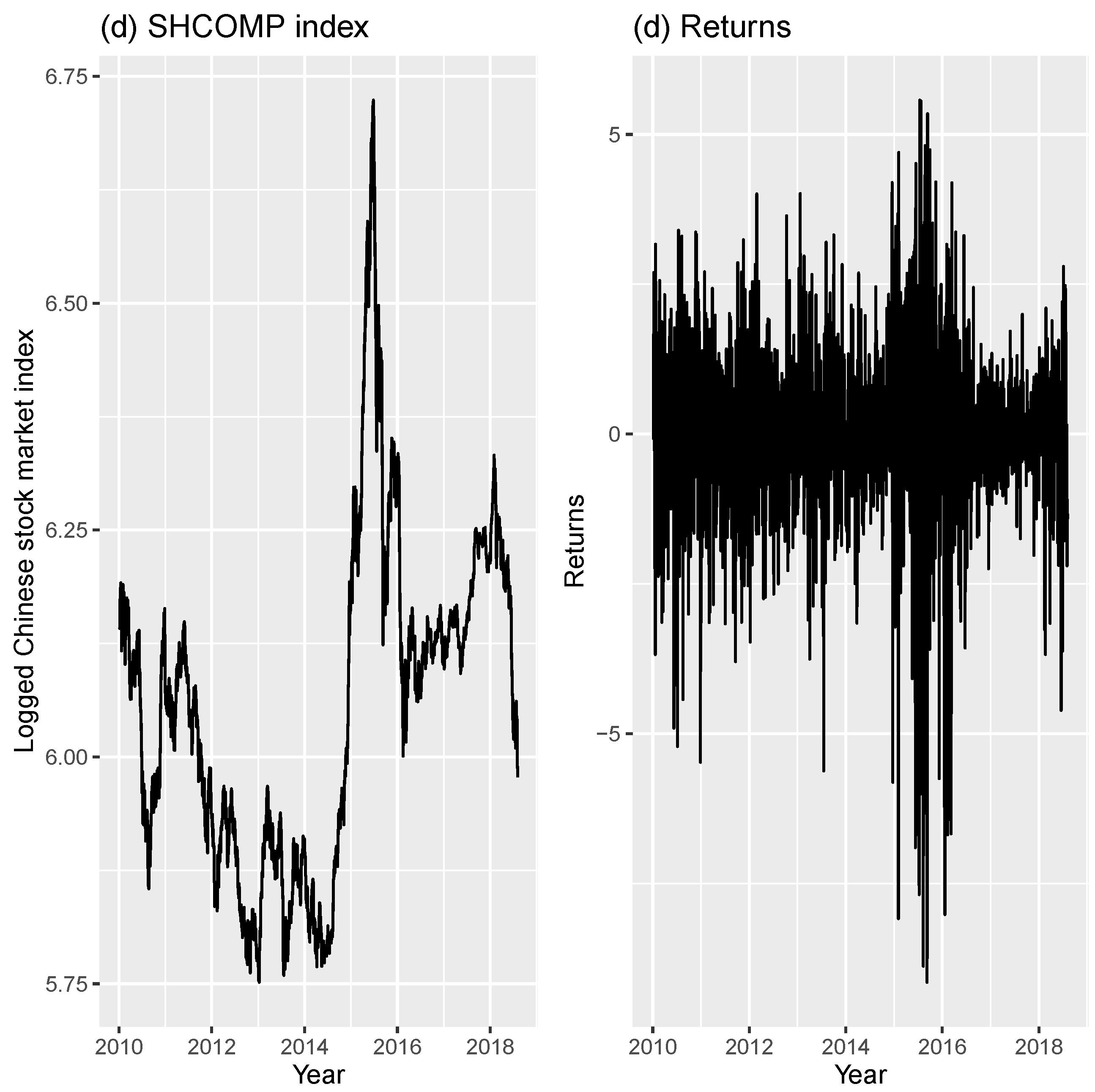

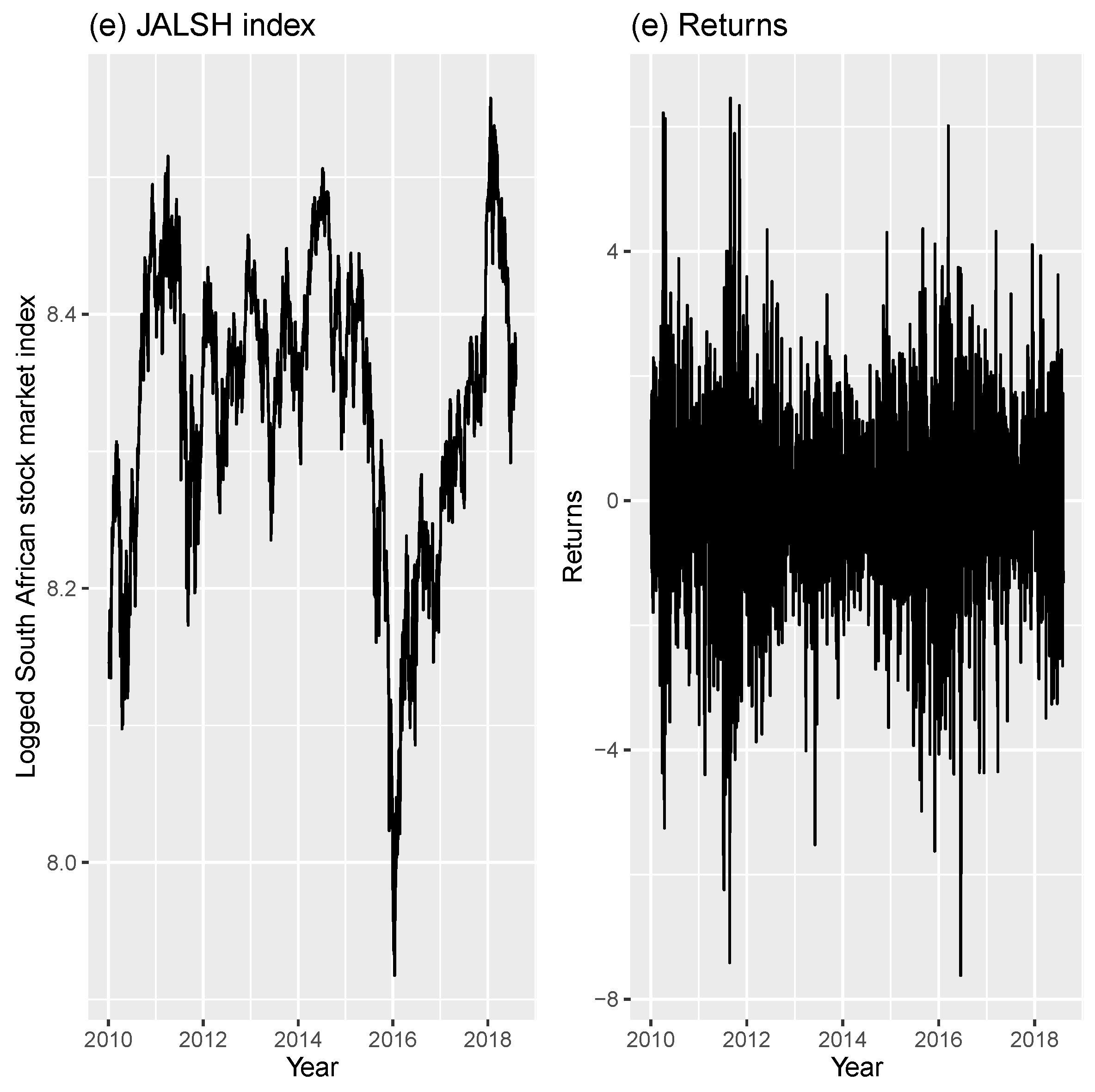

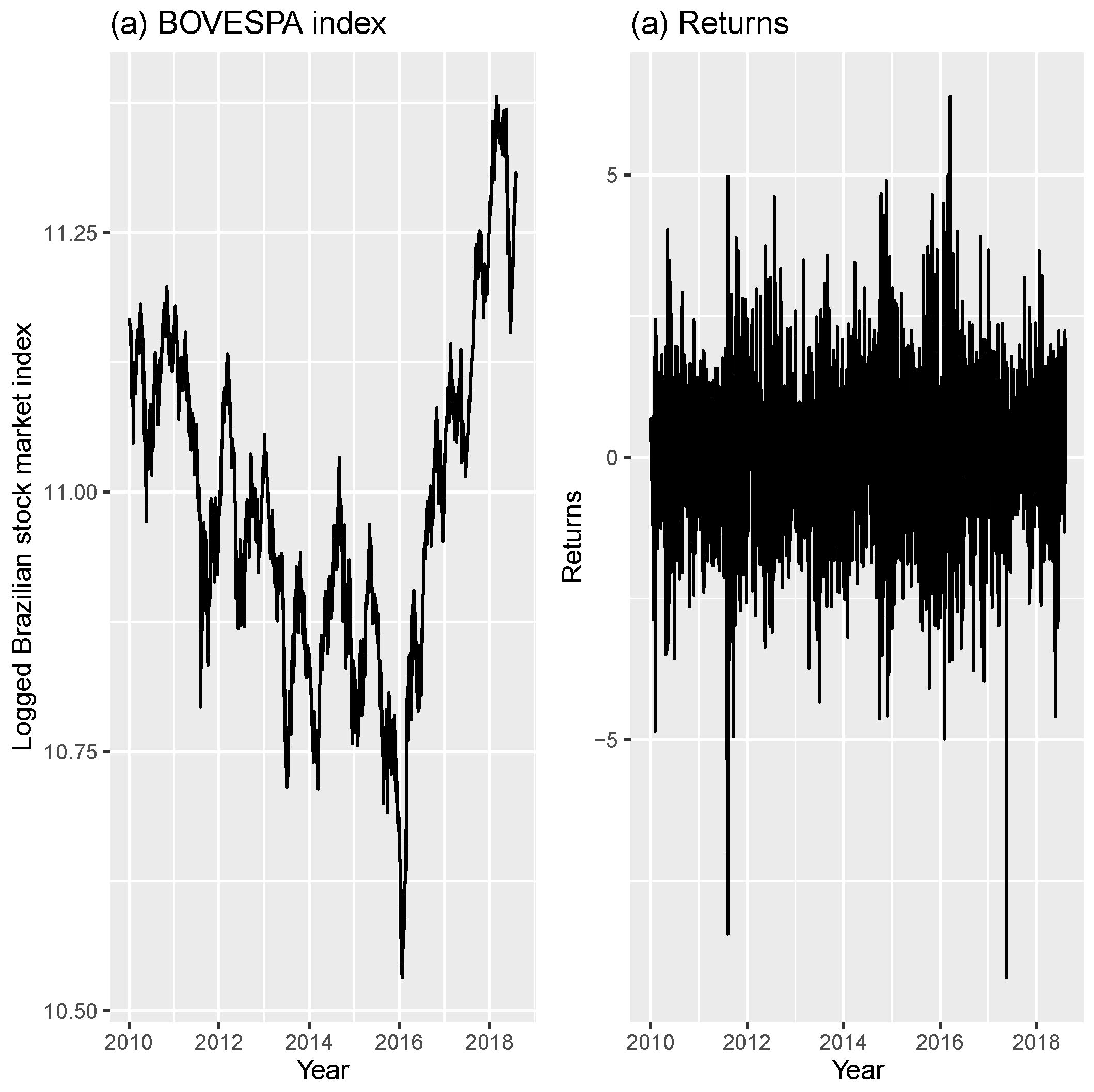

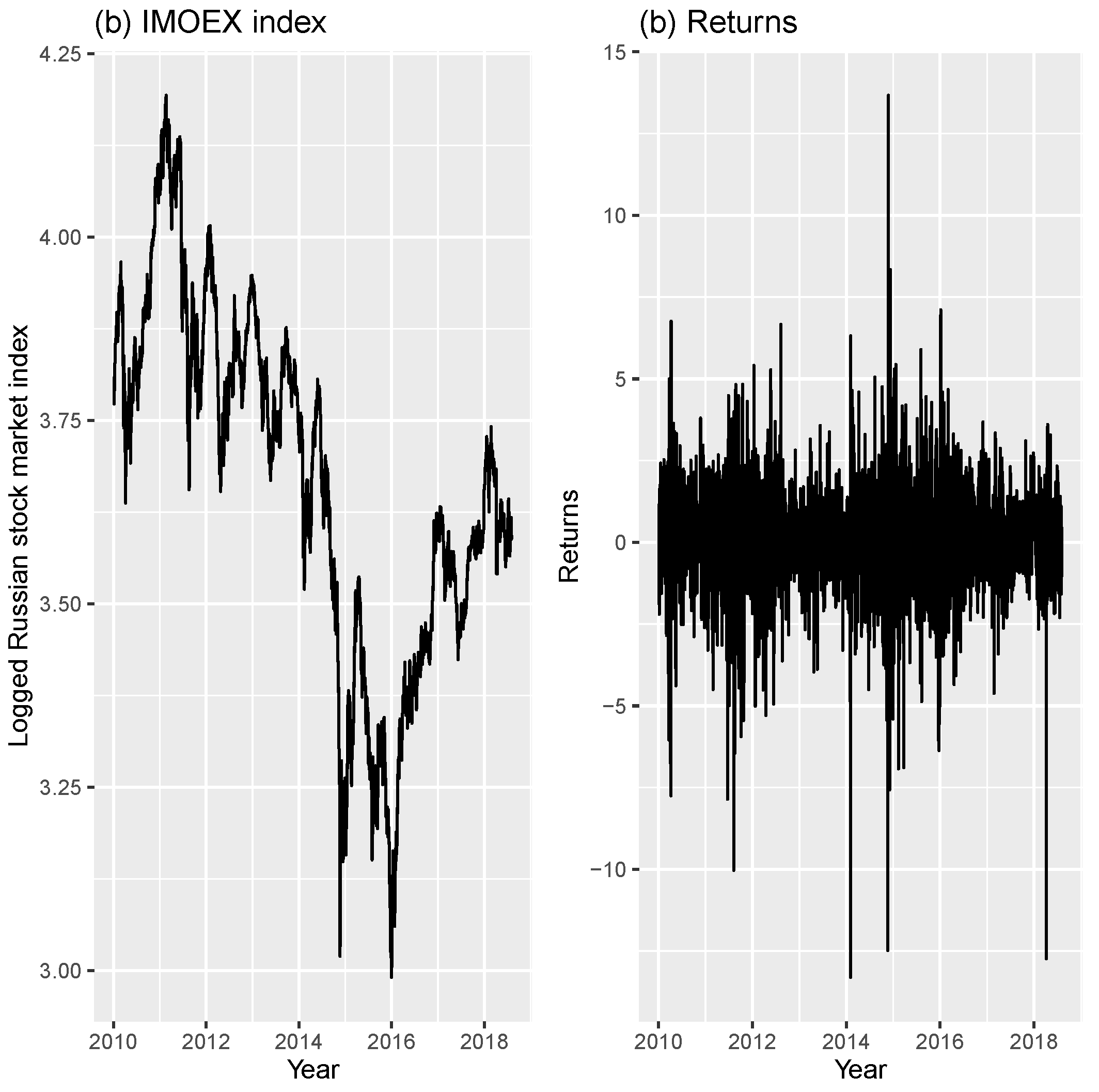

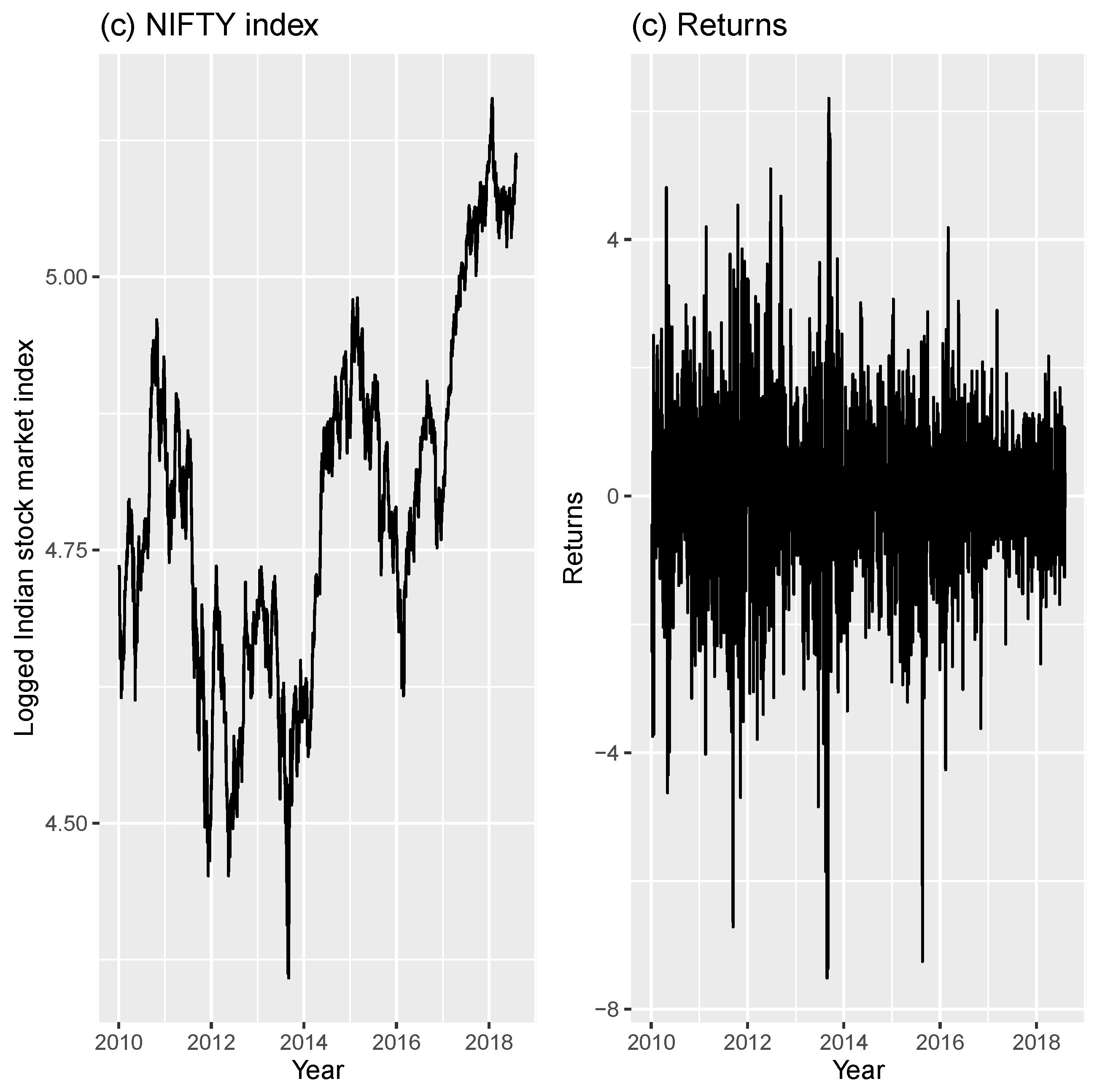

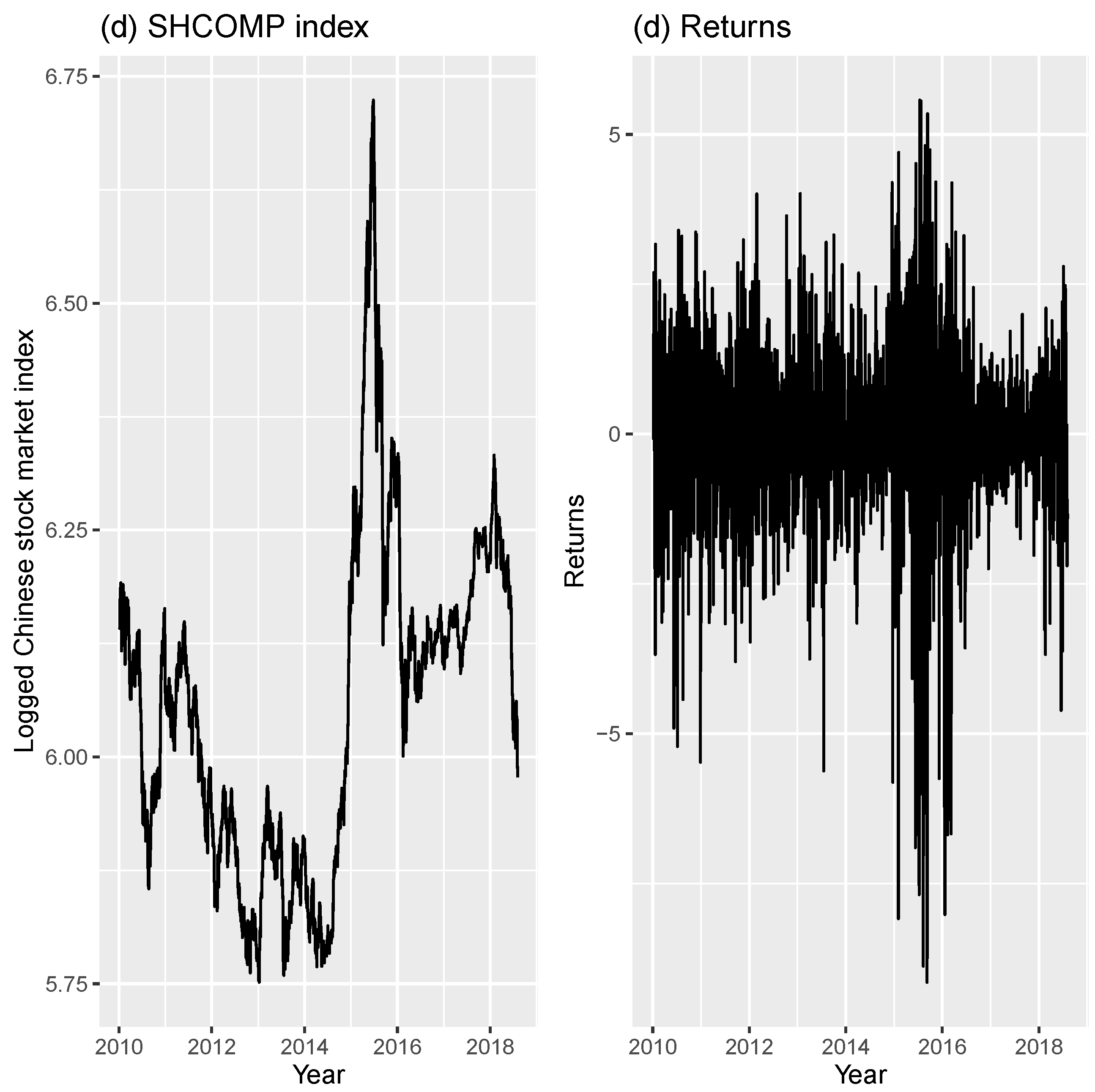

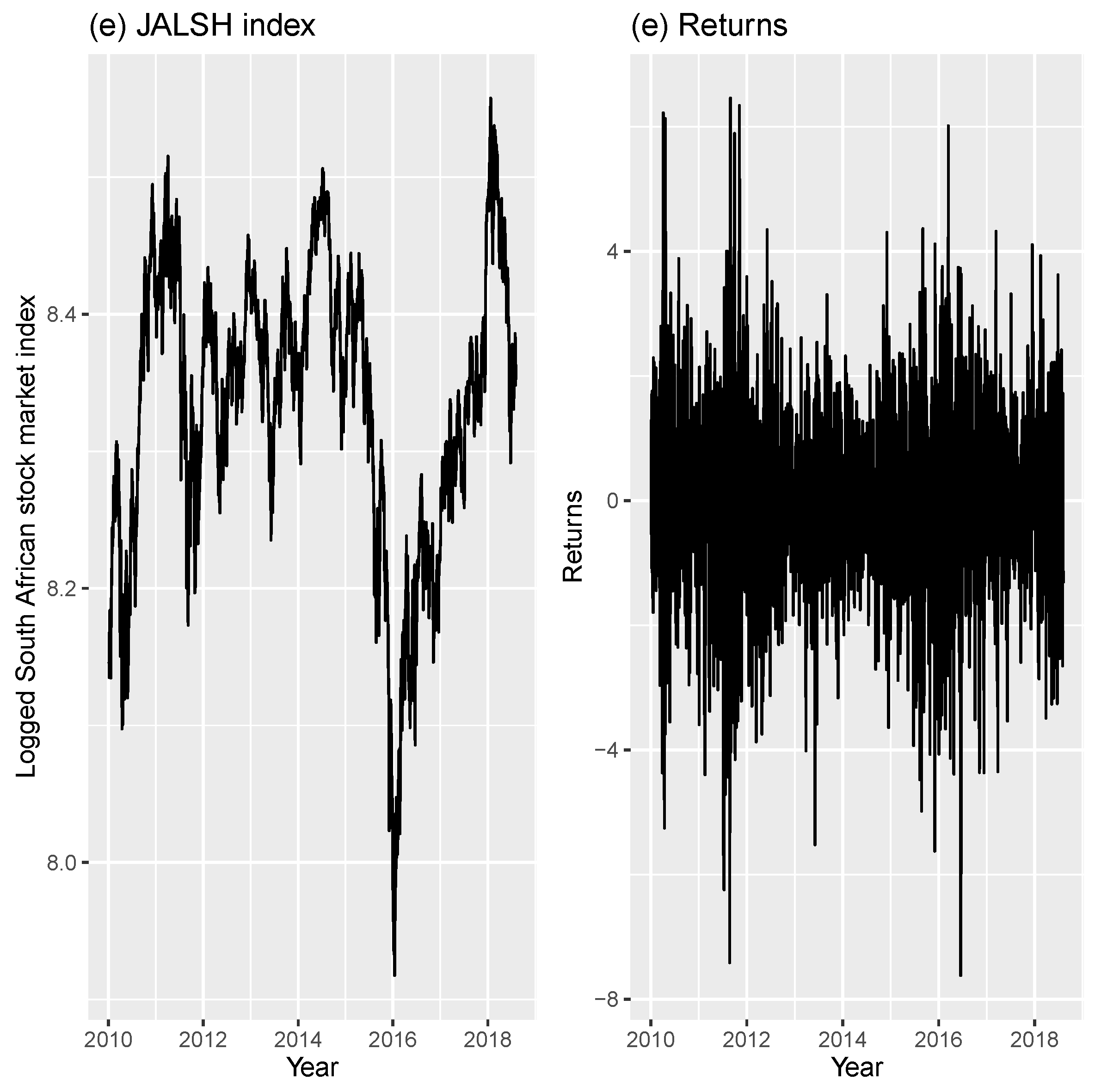

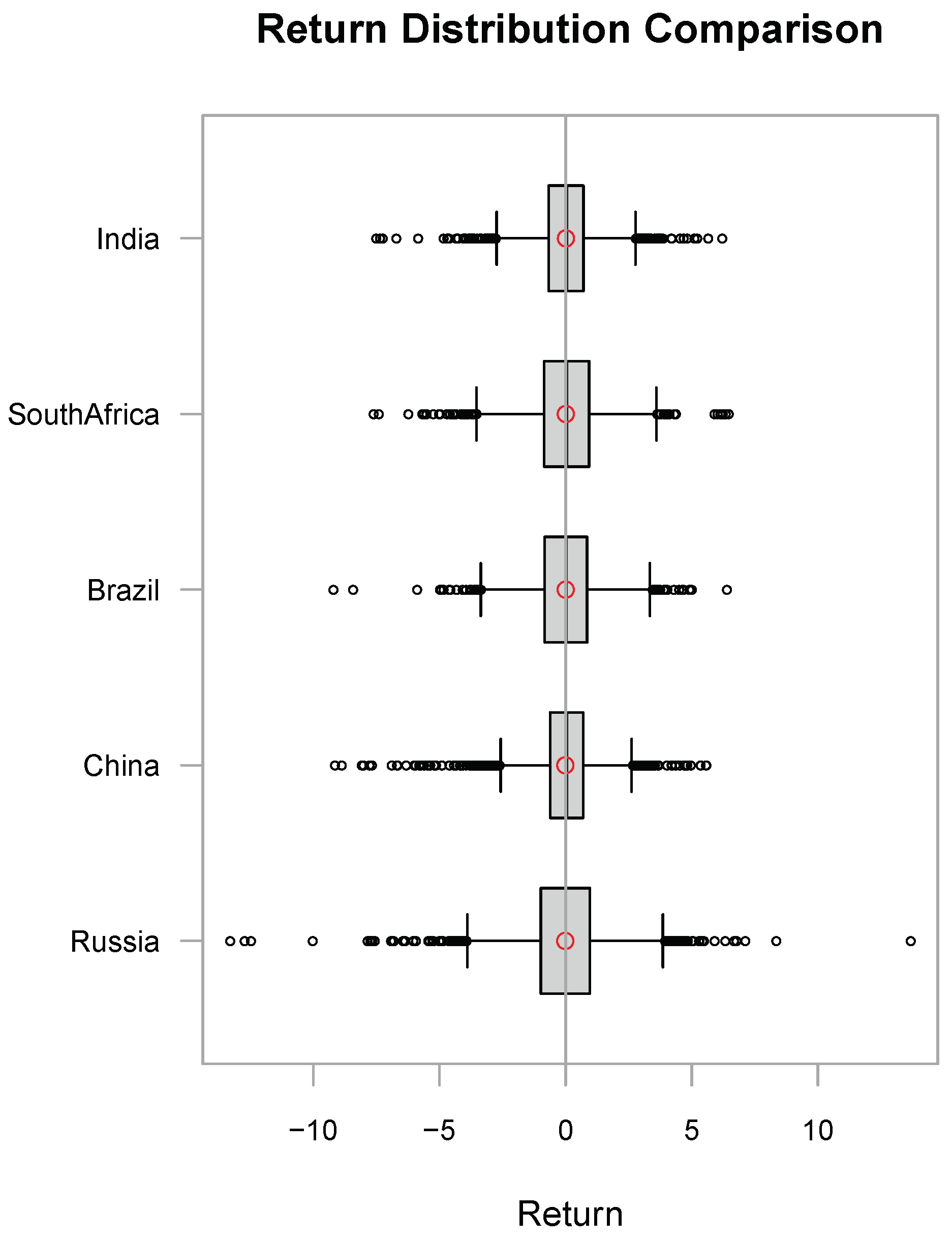

2.4. Data Description

3. Results

3.1. Multivariate Extreme Value Modelling

3.2. Conditional Multivariate Extreme Value Model

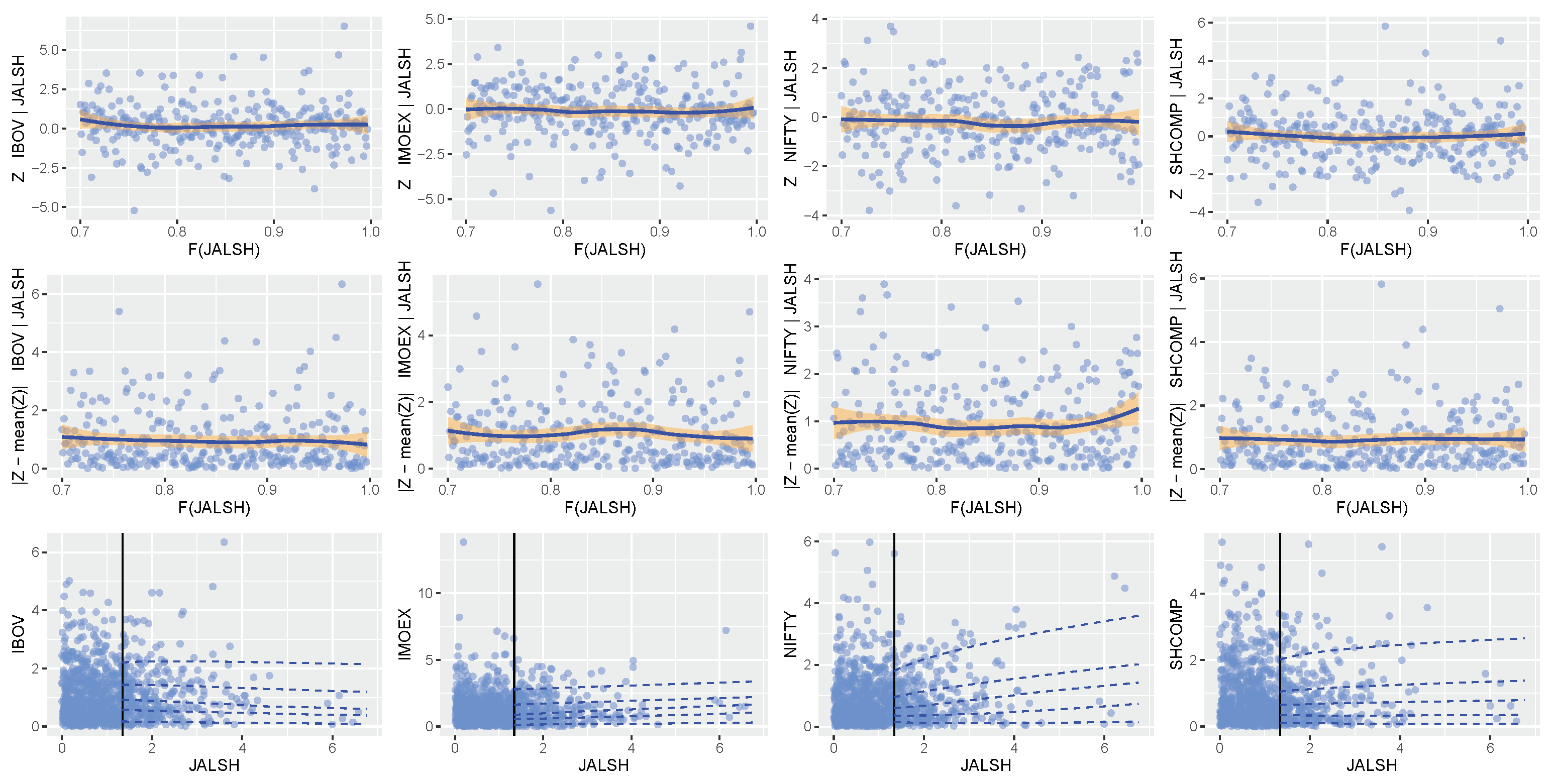

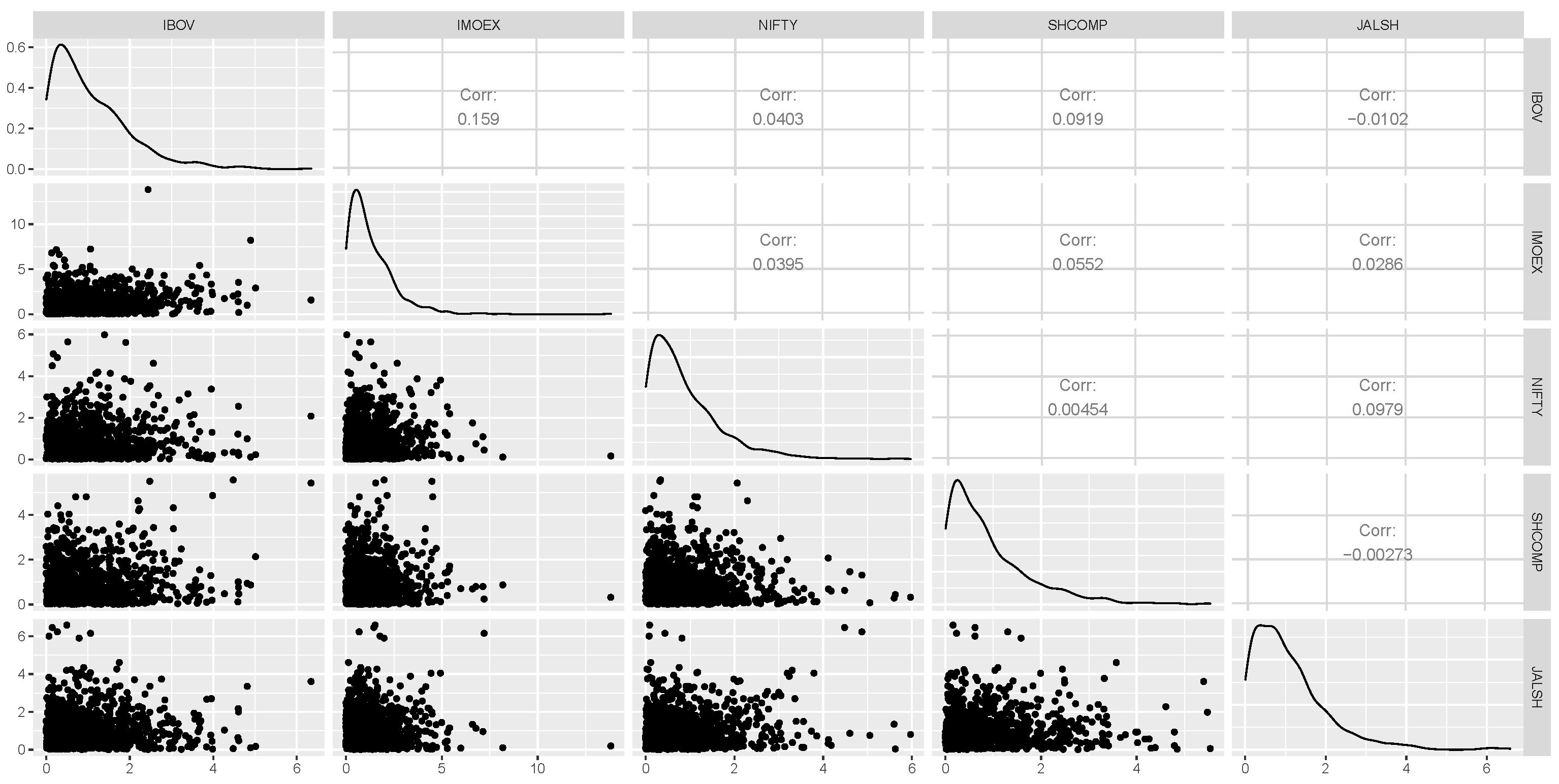

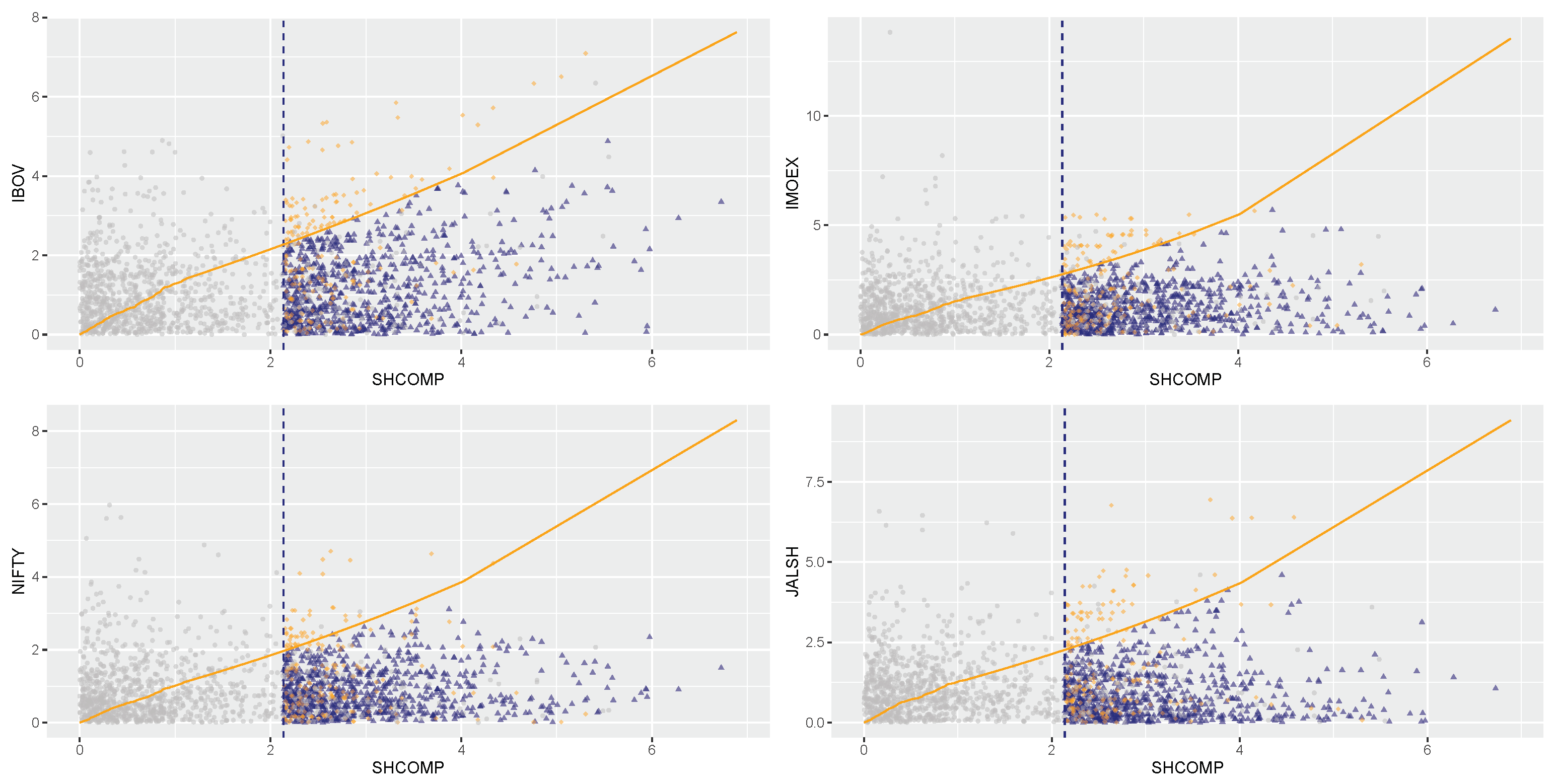

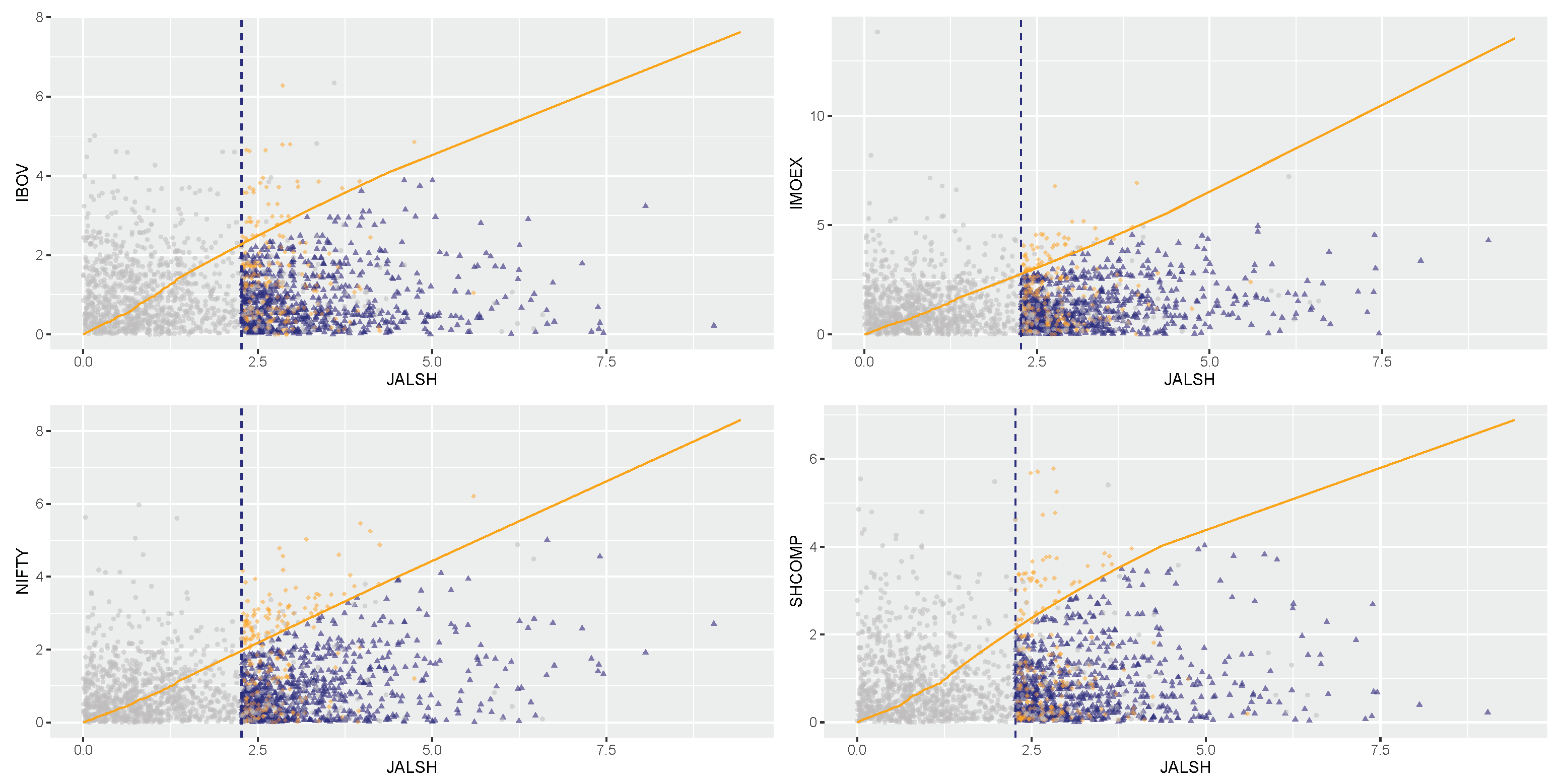

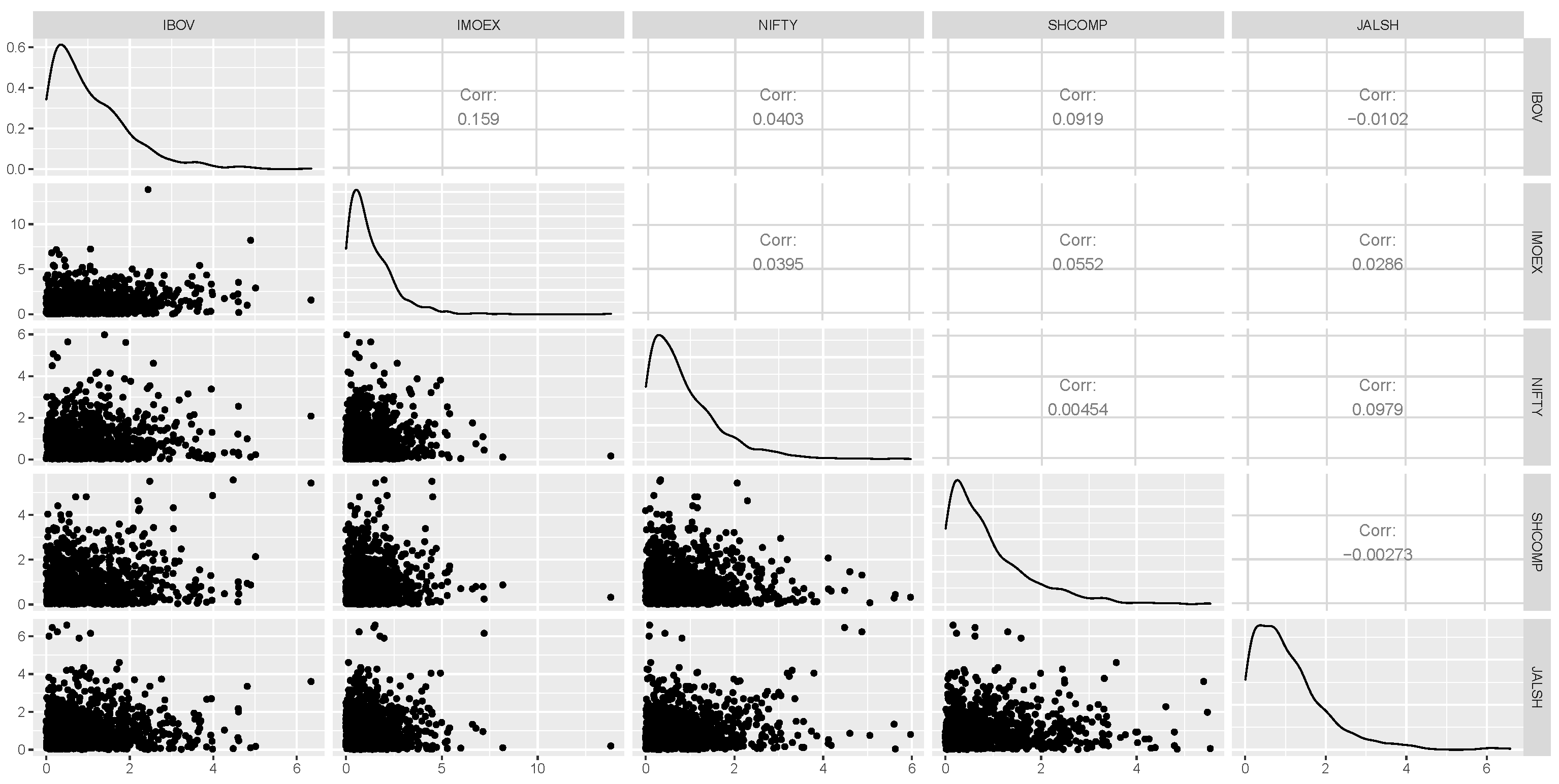

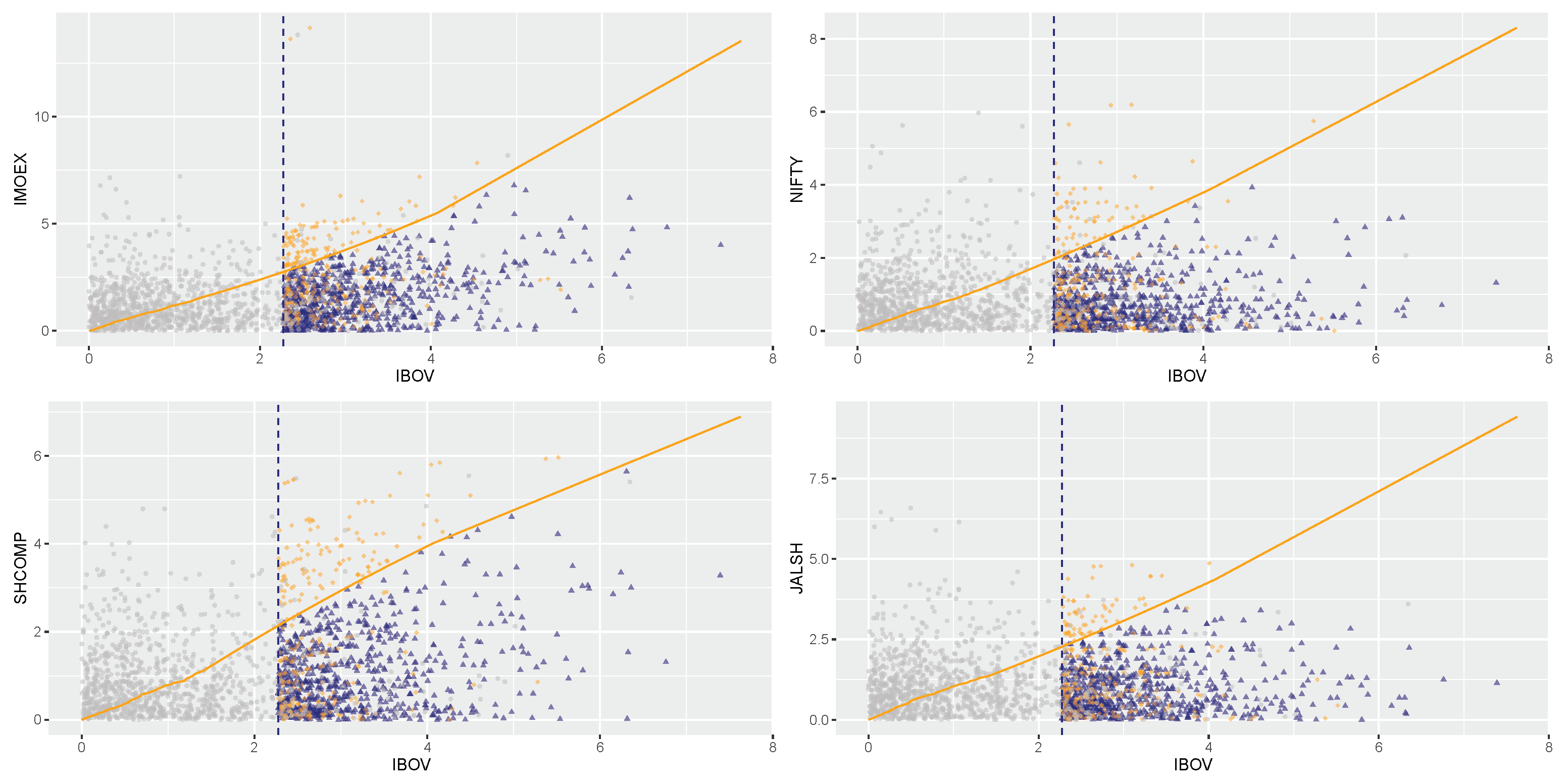

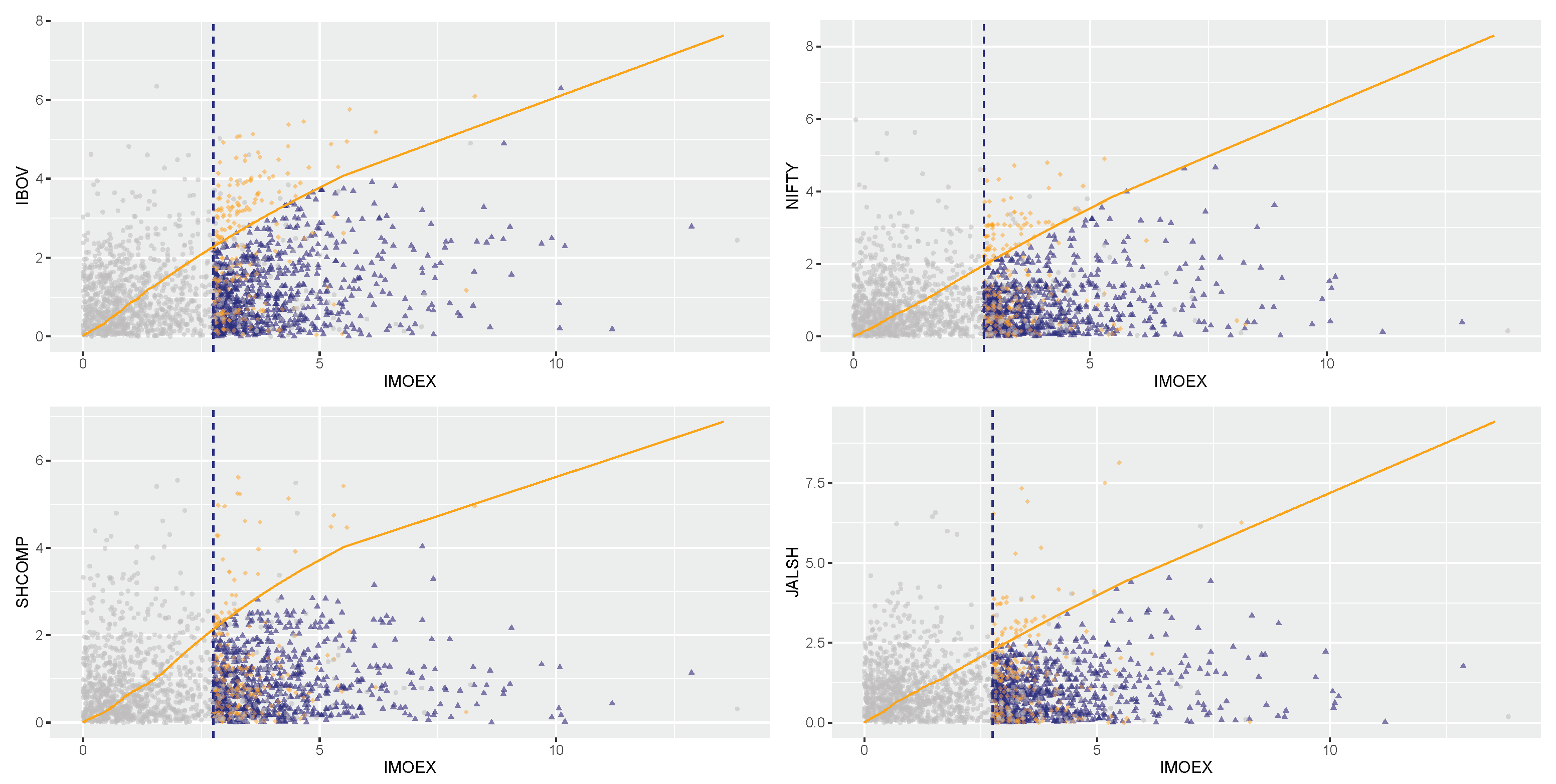

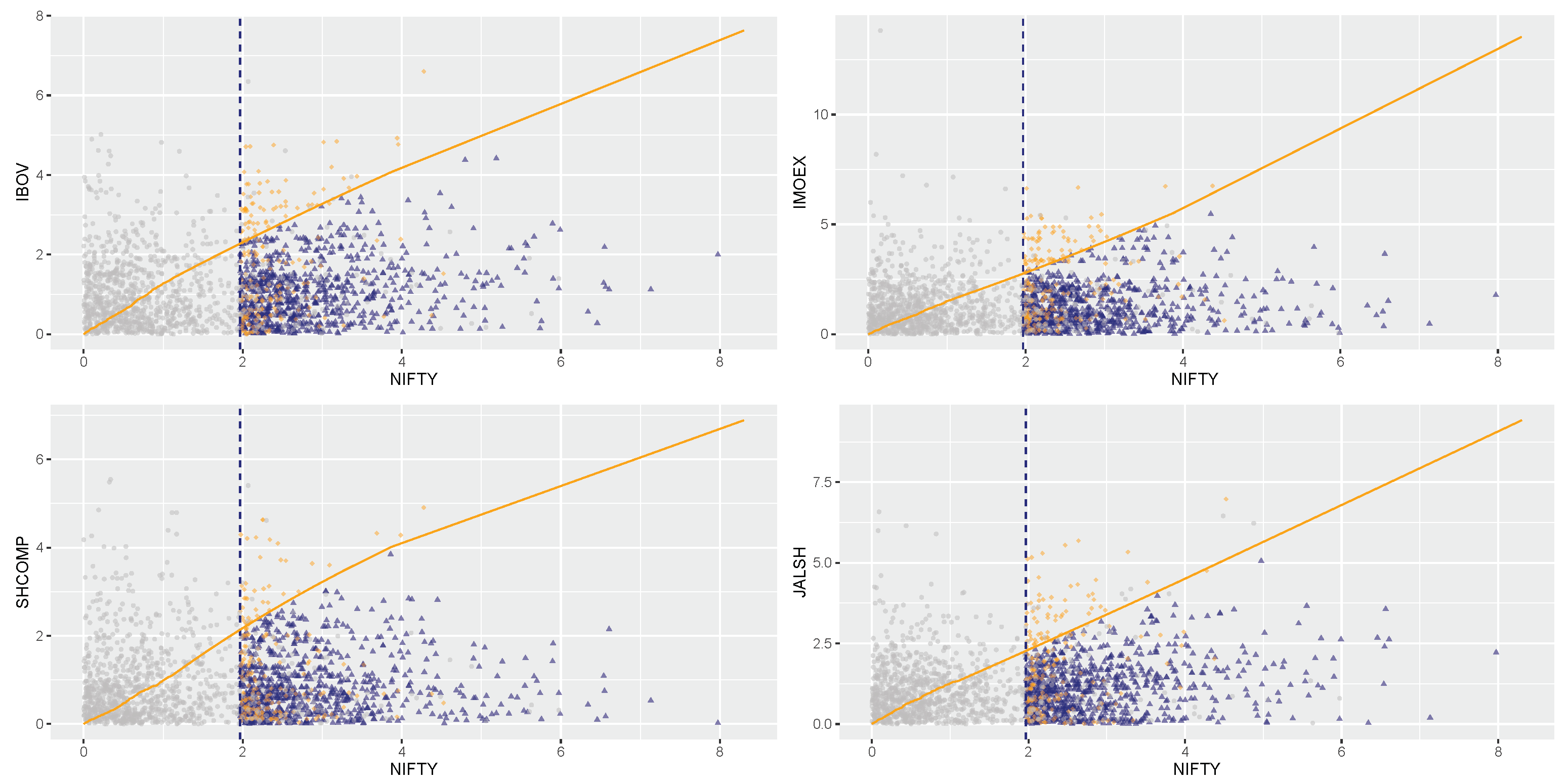

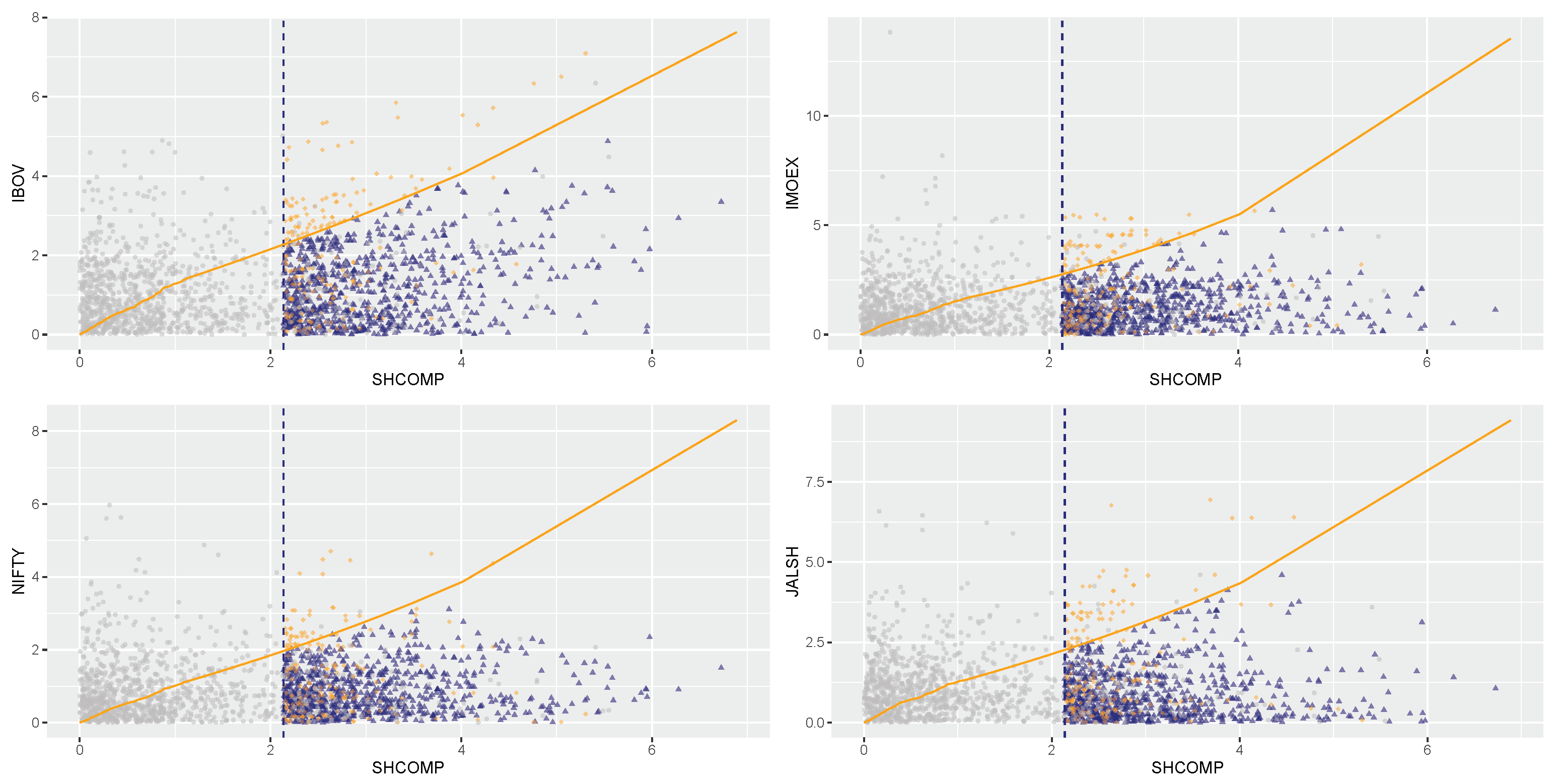

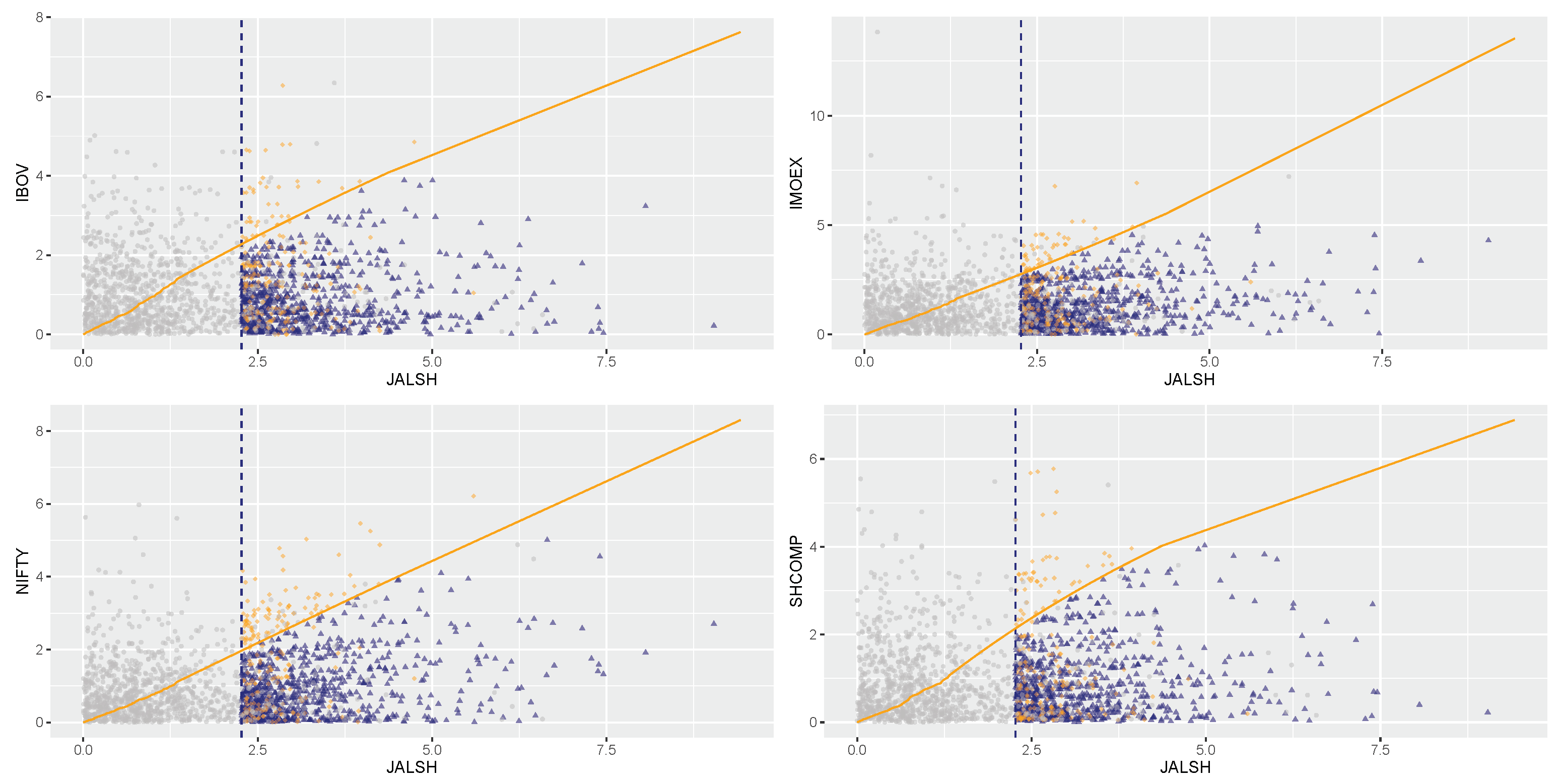

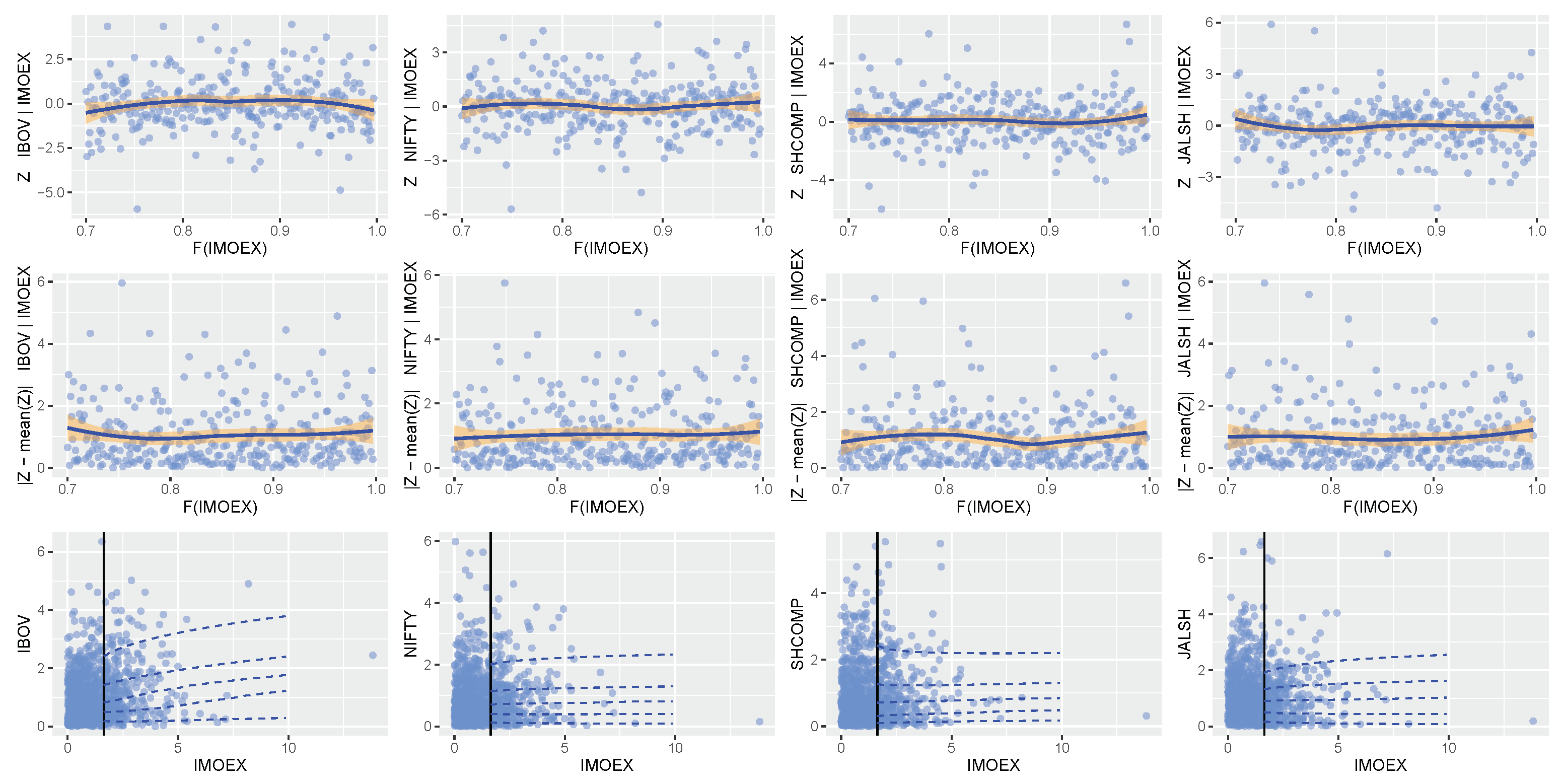

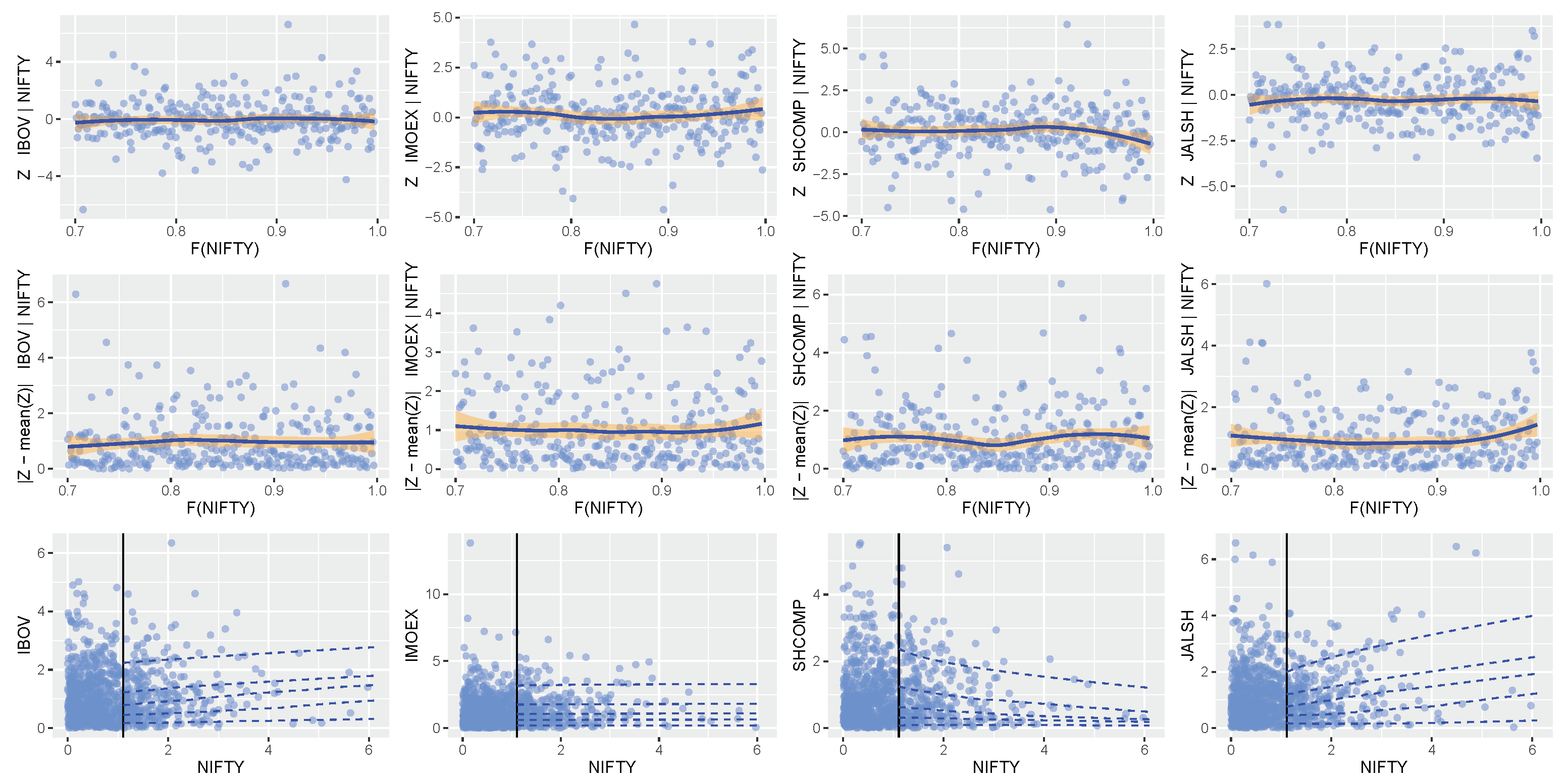

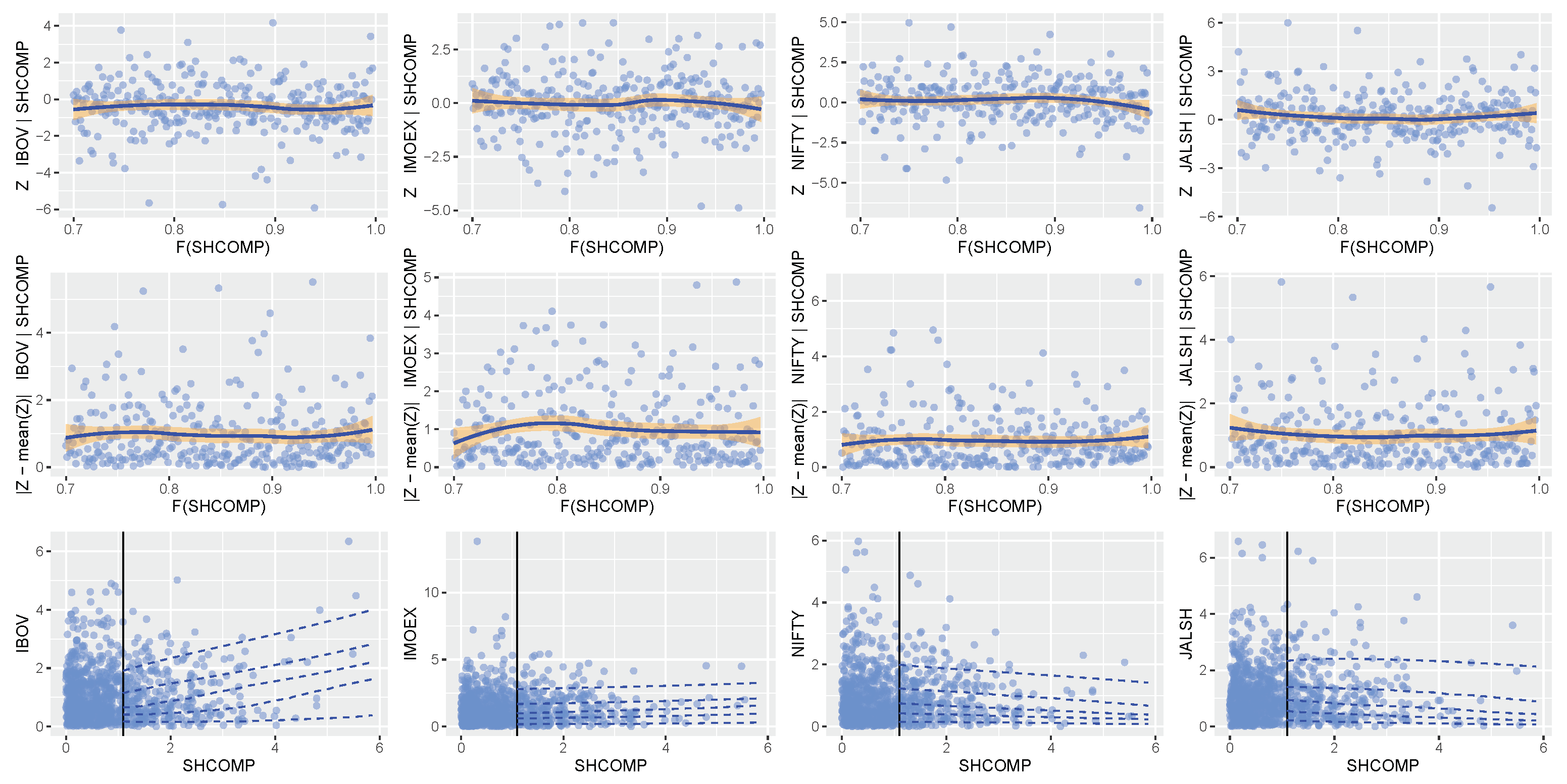

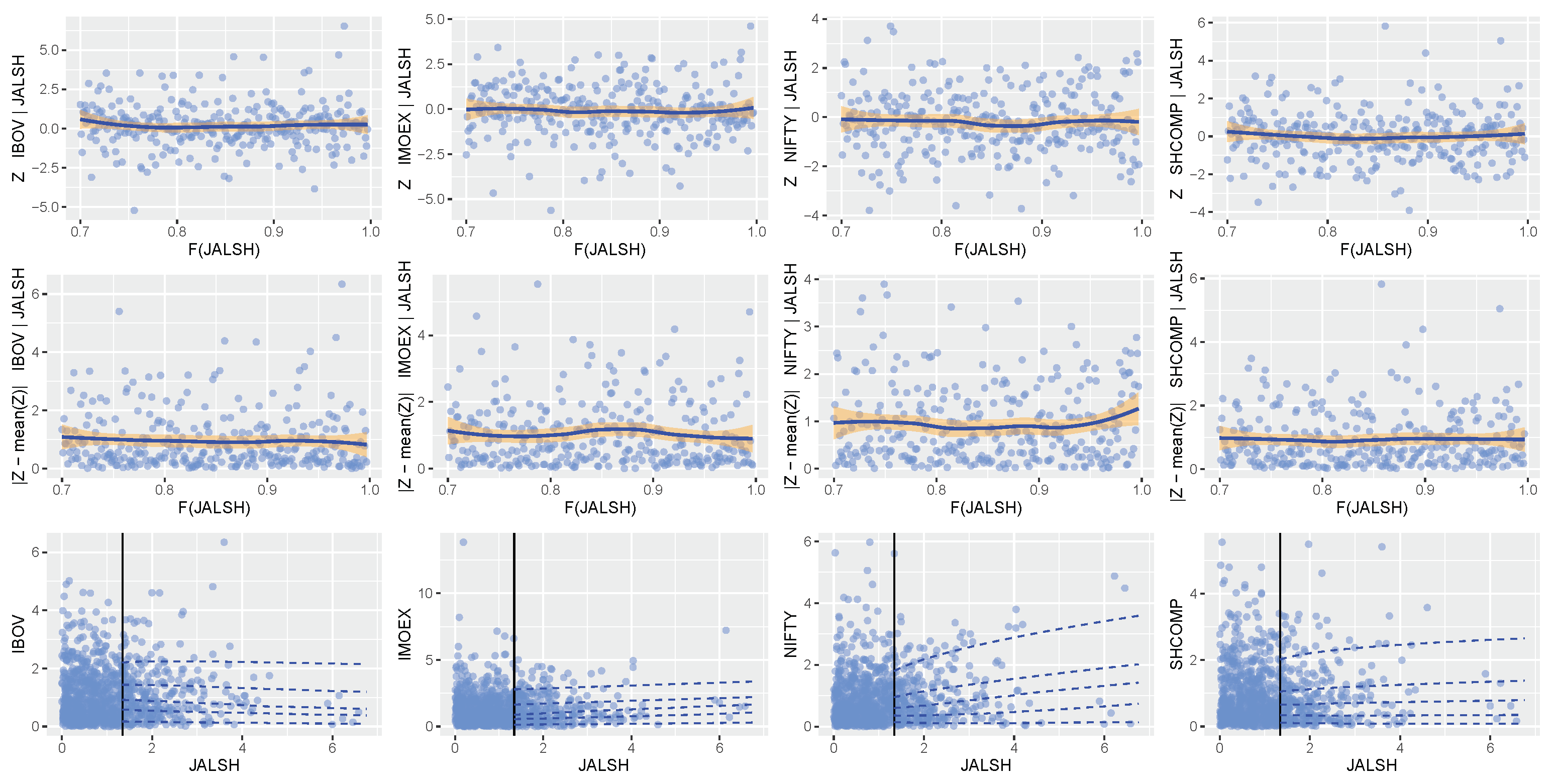

3.2.1. Multivariate Exploratory Plots

3.2.2. CMEV Model Fitting and Diagnostics

3.2.3. Dependence Modelling and Model Diagnostics

3.2.4. Extremal Dependence Results of the CMEV Model

- Conditioning on Brazilian IBOV market: From the table, it is clearly shown that the Russian IMOEX and Chinese SHCOMP markets have fairly strong positive extremal dependence on large values of the Brazilian IBOV market, with the Russian IMOEX market having stronger dependence than the Chinese SHCOMP market on the Brazilian IBOV market. The Indian NIFTY and South African JALSH markets, on the other hand, have a very weak negative extremal dependence on the conditioning the Brazilian IBOV market;

- Conditioning on Russian IMOEX market: The Brazilian IBOV, Indian NIFTY, Chinese SHCOMP and South African JALSH markets have a relatively weak positive extremal dependence on the Russian IMOEX market, with the strongest of this weak dependence being between the Russian IMOEX and Brazilian IBOV markets;

- Conditioning on Indian NIFTY market: Here, it is observed that the Brazilian IBOV and Russian IMOEX markets have varying levels of weak positive extremal dependencies on the Indian NIFTY market, while the asymptotic dependence between the Indian NIFTY and South African JALSH markets are moderately strong. The Chinese SHCOMP market, however has a weak negative dependence on the Indian NIFTY market;

- Conditioning on Chinese SHCOMP market: The values of this dependence parameter shows that the Brazilian IBOV is the most (fairly) strongly positively dependent on large values of the Chinese SHCOMP market, while the Russian IMOEX, Indian NIFTY, and South African JALSH markets have only weak extremal dependence on the Chinese SHCOMP market. More specifically, the Indian NIFTY and South African JALSH markets have weak negative levels of dependence while the Russian IMOEX market has a weak positive dependence on the Chinese SHCOMP market;

- Conditioning on South African JALSH market: The values of the dependence parameter estimates show that the Russian IMOEX, Indian NIFTY, and Chinese SHCOMP markets all have different weak positive extremal dependencies on the South African JALSH market. The strongest of these is between the South African JALSH and Indian NIFTY markets. The Brazilian IBOV market has a weak negative extremal dependence on the South African JALSH market.

3.2.5. Prediction under the CMEV Model

3.3. Bivariate Point Process Modelling

Point Process and CMEV Models Compared

4. Discussion

5. Conclusions

Author Contributions

Funding

Institutional Review Board Statement

Informed Consent Statement

Data Availability Statement

Acknowledgments

Conflicts of Interest

Abbreviations

| BRICS | Brazil, Russia, India, China, and South Africa |

| GARCH | Generalised Autoregressive Conditional Heteroscedasticity |

| CMEV | Conditional Multivariate Extreme Value |

| GAS | Generalised Autoregressive Score |

| GFC | Global Financial Crisis |

| EVT | Extreme Value Theory |

| GEVD | Generalised Extreme Value Distribution |

| GPD | Generalised Pareto Distribution |

| MLE | Maximum Likelihood Estimation |

Appendix A

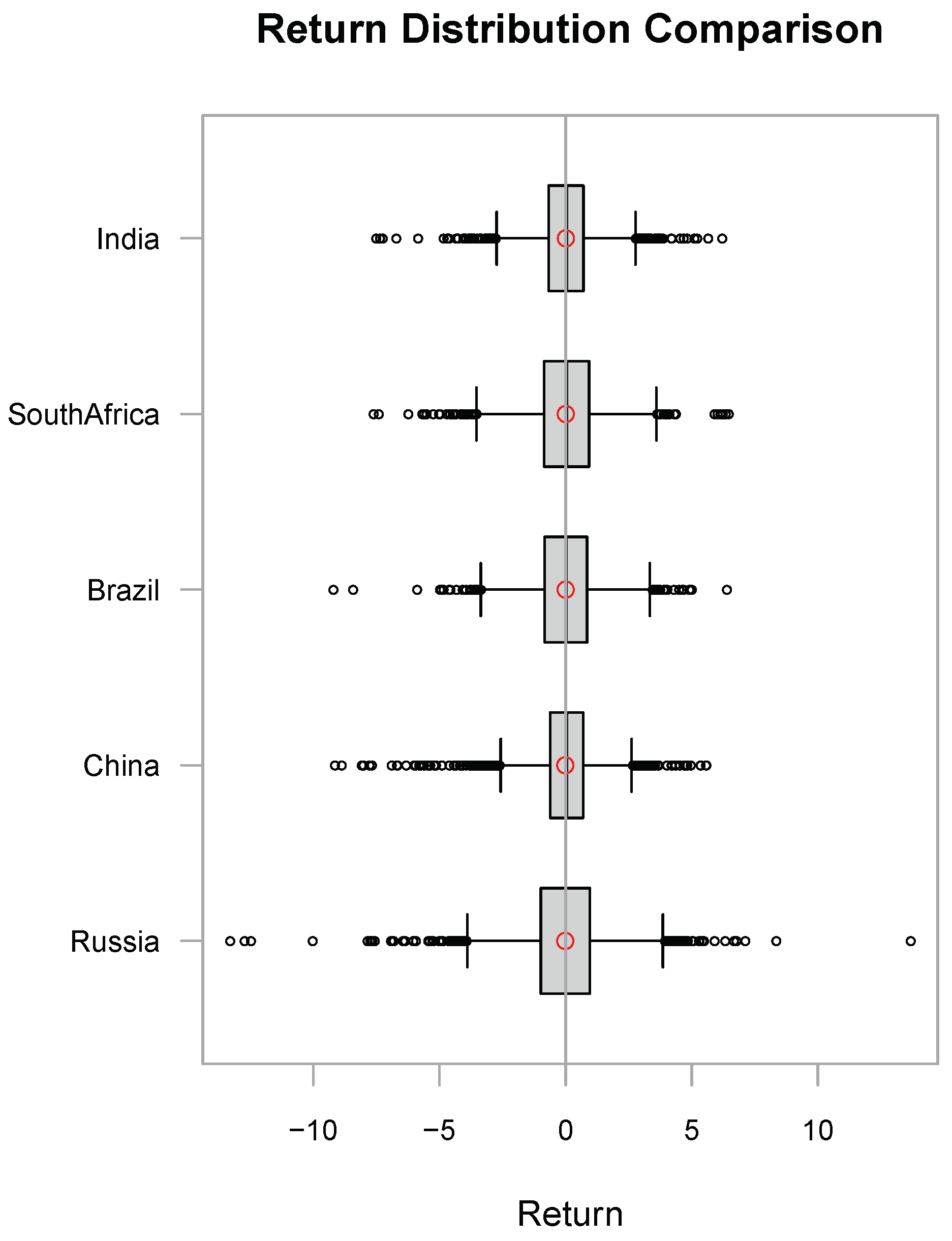

Appendix A.1. Box Plots of the Markets Returns Data

Appendix A.2. Dependence Model Diagnostics

References

- Afuecheta, Emmanuel, Utazi Chigozie, Ranganai Edmore, and Nnanatu Chibuzor. 2020. An Application of extreme value theory for measuring Financial Risk in BRICS Economies. Annals of Data Science 7: 1–40. [Google Scholar] [CrossRef]

- Alagidede, Paul. 2008. How Integrated Are Africa’s Stock Markets with the Rest of the World? Stirling: University of Stirling. [Google Scholar]

- Aloui, Riadh, Mohamed Safouane Ben Aissa, and Duc Khuong Nguyen. 2011. Global financial crisis, extreme interdependences, and contagion effects: The role of economic structure? Journal of Banking & Finance 35: 130–41. [Google Scholar] [CrossRef]

- Alqaralleh, Huthaifa, and Alessandra Canepa. 2021. Evidence of Stock Market Contagion during the COVID-19 Pandemic: A Wavelet-Copula-GARCH Approach. Journal of Risk and Financial Management 4: 329. [Google Scholar] [CrossRef]

- Babu, Manivannan, Cr Hariharan, and S. Srinivasan. 2015. Testing the co-movement of BRICS nations’ capital markets. IIMS Journal of Management Science 6: 213–22. [Google Scholar] [CrossRef]

- Bali, Turan G. 2000. Testing the empirical performance of stochastic volatility models of the short term interest rate. Journal of Financial and Quantitative Analysis 35: 191–215. [Google Scholar] [CrossRef]

- Bartram, Söhnke M., and Gunter Dufey. 2001. International portfolio investment: Theory, evidence, and institutional framework. Financial Markets, Institutions & Instruments 10: 85–155. [Google Scholar] [CrossRef]

- Bekaert, Geert, Campbell R. Harvey, and Angela Ng. 2005. Market integration and contagion. The Journal of Business 78: 39–70. [Google Scholar] [CrossRef] [Green Version]

- BenSaida, Ahmed, Sousse Boubaker, and Duc Khuong Nguyen. 2018. The shifting dependence dynamics between the G7 stock markets. Quantitative Finance 18: 801–12. [Google Scholar] [CrossRef]

- Bensalah, Younes. 2000. Steps in Applying Extreme Value Theory to Finance: A Review. Working Paper 2000-20. Ottawa: Bank of Canada, Available online: https://ideas.repec.org/p/bca/bocawp/00-20.html (accessed on 7 May 2022).

- Boubaker, Sabri, and Jamel Jouini. 2014. Linkages between emerging and developed equity markets: Empirical evidence in the PMG framework. North American Journal of Economics and Finance 29: 322–35. [Google Scholar] [CrossRef]

- Bouri, Elie, Rangan Gupta, Seyedmehdi Hosseini, and Chi Keung Marco Lau. 2018. Does global fear predict fear in BRICS stock markets? Evidence from a Bayesian Graphical Structural VAR model. Emerging Markets Review 34: 124–42. [Google Scholar] [CrossRef] [Green Version]

- Chan-Lau, Jorge A., Donald J. Mathieson, and James Y. Yao. 2004. Extreme contagion in equity markets. IMF Staff Papers 51: 386–408. Available online: https://www.jstor.org/stable/30035880 (accessed on 17 June 2020). [CrossRef]

- Chen, James. 2020. Brazil, Russia, India, China and South Africa (BRICS). Available online: https://www.investopedia.com/terms/b/brics.asp (accessed on 17 June 2020).

- Cheung, Yin-Wong, and Lilian K. Ng. 1990. The dynamics of S & P 500 index and S & P 500 futures intraday price volatilities. Review of Futures Markets 9: 458–86. [Google Scholar]

- Coles, Stuart. 2001. An Introduction to Statistical Modelling of Extreme Values. London: Springer. [Google Scholar]

- Coles, Stuart. G., and Jonathan. A. Tawn. 1991. Modelling extreme multivariate events. Journal of the Royal Statistical Society 53: 377–92. [Google Scholar] [CrossRef]

- Fazio, Giorgio. 2007. Extreme interdependence and extreme contagion between emerging markets. Journal of International Money and Finance 26: 1261–91. [Google Scholar] [CrossRef] [Green Version]

- Ferro, Christopher A. T., and Johan Segers. 2003. Inference for clusters of extreme values. Journal of the Royal Statistical Society, Series B (Statistical Methodology) 65: 545–56. [Google Scholar] [CrossRef]

- Fullana, Olga, Javier Ruiz, and David Toscano. 2021. Stock market bubbles and monetary policy effectiveness. The European Journal of Finance 27: 963–75. [Google Scholar] [CrossRef]

- Gaganis, Chrysovalantis, and Peter Molnár. 2021. Economic policies and their effects on financial market. The European Journal of Finance 27: 929–31. [Google Scholar] [CrossRef]

- Ghini, Ahmed El, and Youssef Saidi. 2017. Return and volatility spillovers in the Moroccan stock market during the financial crisis. Empirical Economics 52: 1481–504. [Google Scholar] [CrossRef] [Green Version]

- Gourieroux, Christian, and Joann Jasiak. 2001. Financial Econometrics. Princeton: Princeton University Press. [Google Scholar]

- Heffernan, Janet E., and Jonathan A. Tawn. 2004. A conditional approach for multivariate extreme values. Journal of the Royal Statistical Society Series B 56: 497–546. [Google Scholar] [CrossRef]

- Hong, Yongmiao, Yanhui Liu, and Shouyang Wang. 2009. Granger causality in risk and detection of extreme risk spillover between financial markets. Journal of Econometrics 150: 271–87. [Google Scholar] [CrossRef] [Green Version]

- Hong, Yongmiao. 2001. A test for volatility spillover with applications to exchange rates. Journal of Econometrics 103: 183–224. [Google Scholar] [CrossRef]

- Hu, Yang, and Carl Scarrott. 2018. Evmix: An R package for extreme value mixture modeling, threshold estimation and boundary corrected kernel density estimation. Journal of Statistical Software 84: 1–27. [Google Scholar] [CrossRef] [Green Version]

- Ijumba, Claire. 2013. Multivariate Analysis of the BRICS Financial Markets. Unpublished. Master’s thesis, University of KwaZulu-Natal, Durban, South Africa. Available online: http://hdl.handle.net/10413/11309 (accessed on 17 February 2021).

- Jawadi, Fredj, and Ricardo M. Sousa. 2013. Structural breaks and nonlinearity in US and UK public debts. Applied Economics Letters 20: 653–57. [Google Scholar] [CrossRef]

- Ji, Qiang, Bing-Yue Liu, Juncal Cunado, and Rangan Gupta. 2020a. Risk spillover between the US and the remaining G7 stock markets using time-varying copulas with Markov switching: Evidence from over a century of data. The North American Journal of Economics and Finance 51: 100846. [Google Scholar] [CrossRef] [Green Version]

- Ji, Qiang, Bing-Yue Liu, Wan-Li Zhao, and Ying Fan. 2020b. Modelling dynamic dependence and risk spillover between all oil price shocks and stock market returns in the BRICS. International Review of Financial Analysis 68: 101238. [Google Scholar] [CrossRef]

- Ji, Qiang, Elie Bouri, and David Roubaud. 2018. Dynamic network of implied volatility transmission among US equities, strategic commodities, and BRICS equities. International Review of Financial Analysis 57: 1–12. [Google Scholar] [CrossRef]

- Kuepper, Justin. 2019. International Diversification: Example Portfolios. The Balance. Available online: https://www.thebalance.com/internationaldiversication-example-portfolios-4148204 (accessed on 16 October 2021).

- Lee, Chien-Chiang, Mei-Ping Chen, and Erh-Yin Sun. 2017. Member states’ pact and industry co-movements in the BRICS markets. Applied Economics 49: 313–34. [Google Scholar] [CrossRef]

- MacDonald, Anna, Carl John Scarrott, Dominic Savio Lee, Brian A. Darlow, Marco Reale, and Glynn Russell. 2011. A flexible extreme value mixture model. Computational Statistics & Data Analysis 55: 2137–57. [Google Scholar] [CrossRef]

- Maghyereh, Aktham, and Basel Awartani. 2012. Return and volatility spillovers between Dubai financial market and Abu Dhabi Stock Exchange in the UAE. Applied Financial Economics 22: 837–48. [Google Scholar] [CrossRef]

- Mensi, Walid, Shawkat Hammoudeh, Seong-Min Yoon, and Duc Khuong Nguyen. 2016. Asymmetric linkages between BRICS stock returns and country risk ratings: Evidence from dynamic panel threshold models. Review of International Economics 24: 1–19. [Google Scholar] [CrossRef]

- Odit, M. P., K. Dookhan, and J. C. Marylin. 2011. The impact of risk management and portfolio diversification on the Mauritian banking sector. International Journal of Management & Information Systems 15: 117–128. [Google Scholar] [CrossRef]

- Reisen, Helmut. 2000. Pensions, Savings and Capital Flows from Ageing to Emerging Markets. Paris: OECD. [Google Scholar]

- Samuel, Richard A. 2018. Modelling Equity Risk and Extremal Dependence: A Survey of Four African Stock Markets. Master’s dissertation, University of Venda, Thohoyandou, South Africa. [Google Scholar]

- Scarrott, Carl, and Anna MacDonald. 2012. A review of extreme value threshold estimation and uncertainty quantification. Revstat Statistical Journal 10: 33–60. [Google Scholar] [CrossRef]

- Segal, Troy. 2021. Diversification. Investopedia. Available online: https://www.investopedia.com/terms/d/diversification.asp (accessed on 16 June 2021).

- Solnik, Bruno H. 1974. Why do not diversify internationally rather than domestically. Financial Analyst Journal 30: 48–54. [Google Scholar] [CrossRef]

- Southworth, Harry, Janet E. Heffernan, and Paul D. Metcalfe. 2020. Texmex: Statistical Modelling of Extreme Values. R Package Version 2.4.4. Available online: https://cran.r-project.org/web/packages/texmex/index.html (accessed on 7 May 2022).

- Stephenson, Alec. 2018. Functions for Extreme Value Distributions. R Package ‘evd’. Available online: https://cran.r-project.org/web/packages/evd/evd.pdf (accessed on 3 November 2021).

- Stulz Rene, M. 1981. A model of international asset pricing. Journal of Financial Economics 9: 383–406. [Google Scholar] [CrossRef]

- Tancredi, Andrea, Clive Anderson, and Anthony O’Hagan. 2006. Accounting for threshold uncertainty in extreme value estimation. Extremes 9: 87–106. [Google Scholar] [CrossRef]

- Warshaw, Evan. 2019. Extreme dependence and risk spillovers across north American equity markets. The North American Journal of Economics and Finance 47: 237–51. [Google Scholar] [CrossRef]

- Yang, Hu. 2013. Extreme value mixture modelling with simulation study and applications in finance and insurance. UC Research Repository 2013: 1–113. Available online: https://ir.canterbury.ac.nz/handle/10092/8538 (accessed on 28 September 2021).

- Yavas, Burhan F. 2007. Benefits of international portfolio diversification. Graziadio Business Report 10: 1–10. Available online: https://gbr.pepperdine.edu/2010/08/benefits-of-international-portfolio-diversification/ (accessed on 14 June 2021).

- Zonouzi, Jamaledin Mohseni S., Gholamreza Mansourfar, and Fateme Bagherzadeh Azar. 2014. Benefits of international portfolio diversification implication of the Middle Eastern oil-producing countries. International Journal of Islamic and Middle Eastern Finance and Management 7: 457–72. [Google Scholar] [CrossRef]

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| REF | Data | Models | Main Findings |

|---|---|---|---|

| Chan-Lau et al. (2004) | Stock returns of some emerging and some mature stock markets | Extremal dependence and correlation approaches | Results show that the measures of contagion are not highly correlated |

| Ji et al. (2020b) | Oil demand and stock returns of BRICS countries | Time-varying copula-GARCH CoVAR approach | The results show that there is a large risk spillover from some oil demand to the stock returns in all the BRICS countries |

| Samuel (2018) | Daily stock returns for South Africa, Egypt, Nigeria, and Kenya | Bivariate-threshold-excess model and point process approach | The markets displayed asymptotic independence or (very) weak asymptotic dependence and negative dependence |

| Ijumba (2013) | BRICS’s stock returns | Vector Autoregressive (VAR), univariate GARCH (1,1) and multivariate GARCH models | The Multivariate GARCH showed volatility persistence among BRICS stock markets |

| Afuecheta et al. (2020) | BRICS’s stock returns | Generalised extreme value distribution, the generalised logistic distribution, the generalised Pareto distribution, the Student’s t-one exponential parameter distribution and the Student’s t-two parameter Weibull distribution; Galambos, Hsler–Reiss, Gumbel, normal, and Student’s t | The results indicated that the GEVD gave the best fit to the tails of the returns distributions of the BRICS stock markets. Using the copulas in modelling the tail dependence, the Gumbel copula gave the best fit |

| Fullana et al. (2021) | Stock market returns and monetary policy | Structural vector autoregressive and regression models | Results suggest no significant monetary policy shocks on the stock market returns under certain circumstances |

| BenSaida et al. (2018) | G7 stock market indices | Regime-switching copula models | Results showed evidence of regime shifts in the dependence structure during crisis periods |

| Model | Independence | Dependence |

|---|---|---|

| Logistic | → 1 | → 0 |

| Negative logistic | → 0 | →∞ |

| Husler–Reiss | → 0 | →∞ |

| Bilogistic | = → 1 | = → 0 |

| Negative bilogistic | = → ∞ | = → 0 |

| Coles–Tawn (or Dirichlet) | = → 0 | = → ∞ |

| Dependence Parameters | IMOEX | NIFTY | SHCOMP | JALSH | |

|---|---|---|---|---|---|

| Conditioning on: IBOV | a | 0.3888 | −0.0194 | 0.3157 | −0.0408 |

| b | 0.1019 | 0.0257 | 0.2452 | 0.0633 | |

| Dependence Parameters | IBOV | NIFTY | SHCOMP | JALSH | |

| Conditioning on: IMOEX | a | 0.1655 | 0.0151 | 0.0314 | 0.0184 |

| b | 0.1386 | 0.0669 | −0.1024 | 0.1650 | |

| Conditioning on: NIFTY | a | 0.1116 | 0.0059 | −0.1110 | 0.2531 |

| b | 0.0066 | 0.0140 | −0.1518 | 0.2034 | |

| Dependence Parameters | IBOV | IMOEX | NIFTY | JALSH | |

| Conditioning on: SHCOMP | a | 0.3159 | 0.0717 | −0.0957 | −0.1235 |

| b | 0.2081 | −0.0055 | −0.0352 | 0.1015 | |

| Dependence Parameters | IBOV | IMOEX | NIFTY | SHCOMP | |

| Conditioning on: JALSH | a | −0.0606 | 0.1018 | 0.2011 | 0.0311 |

| b | 0.0642 | −0.0138 | 0.2315 | 0.1255 |

| Conditioning on IBOV | IMOEX | NIFTY | SHCOMP | JALSH |

| 0.510 | 0.305 | 0.454 | 0.302 | |

| Conditioning on IMOEX | IBOV | NIFTY | SHCOMP | JALSH |

| 0.433 | 0.346 | 0.358 | 0.351 | |

| Conditioning on NIFTY | IBOV | IMOEX | SHCOMP | JALSH |

| 0.323 | 0.363 | 0.315 | 0.402 | |

| Conditioning on SHCOMP | IBOV | IMOEX | NIFTY | JALSH |

| 0.425 | 0.347 | 0.342 | 0.278 | |

| Conditioning on JALSH | IBOV | IMOEX | NIFTY | SHCOMP |

| 0.280 | 0.337 | 0.408 | 0.318 |

| AIC | |||

| Logistic | 0.5994 (0.0117) | Nil | 3762.38 |

| Negative logistic | 0.9055 (0.0314) | Nil | 3711.77 |

| Husler–Reiss | 1.3413 (0.0345) | Nil | 3669.11 |

| Bilogistic | 0.5829 (0.0258) | 0.6155 (0.0247) | 3763.84 |

| Negative bilogistic | 1.1938 (0.1134) | 1.0210 (0.0978) | 3712.99 |

| ct (or Dirichlet) | 0.8195 (0.1010) | 1.0172 (0.1369) | 3718.47 |

| AIC | |||

| Logistic | 0.6066 (0.0114) | Nil | 3756.67 |

| Negative logistic | 0.8854 (0.0300) | Nil | 3701.53 |

| Husler–Reiss | 1.3174 (0.0330) | Nil | 3656.31 |

| Bilogistic | 0.6209 (0.0244) | 0.5909 (0.0267) | 3758.23 |

| Negative bilogistic | 1.0470 (0.1029) | 1.2140 (0.1141) | 3702.85 |

| ct (or Dirichlet) | 0.9829 (0.1364) | 0.7940 (0.0959) | 3710.40 |

| AIC | |||

| Logistic | 0.6086 (0.0114) | Nil | 3788.63 |

| Negative logistic | 0.8779 (0.0296) | Nil | 3733.10 |

| Husler–Reiss | 1.3100 (0.0326) | Nil | 3683.98 |

| Bilogistic | 0.6264 (0.0235) | 0.5901 (0.0250) | 3789.91 |

| Negative bilogistic | 1.0629 (0.0988) | 1.2186 (0.1111) | 3734.46 |

| ct (or Dirichlet) | 0.9515 (0.1229) | 0.7931 (0.0949) | 3742.99 |

| AIC | |||

| Logistic | 0.6132 (0.0114) | Nil | 3817.37 |

| Negative logistic | 0.8646 (0.0292) | Nil | 3761.19 |

| Husler–Reiss | 1.2906 (0.0321) | Nil | 3715.79 |

| Bilogistic | 0.6137 (0.0246) | 0.6125 (0.0254) | 3819.37 |

| Negative bilogistic | 1.1414 (0.1098) | 1.1707 (0.1096) | 3763.17 |

| ct (or Dirichlet) | 0.8591 (0.1121) | 0.8303 (0.1027) | 3772.86 |

| AIC | |||

| Logistic | 0.6073 (0.0116) | Nil | 3873.50 |

| Negative logistic | 0.8818 (0.0302) | Nil | 3821.21 |

| Husler–Reiss | 1.3110 (0.0332) | Nil | 3780.47 |

| Bilogistic | 0.6185 (0.0240) | 0.5955 (0.0254) | 3875.22 |

| Negative bilogistic | 1.0850 (0.1033) | 1.1839 (0.1100) | 3822.96 |

| ct (or Dirichlet) | 0.9256 (0.1208) | 0.8203 (0.0997) | 3830.56 |

| AIC | |||

| Logistic | 0.6072 (0.0116) | Nil | 3941.75 |

| Negative logistic | 0.8806 (0.0303) | Nil | 3887.51 |

| Husler–Reiss | 1.3145 (0.0334) | Nil | 3838.94 |

| Bilogistic | 0.6140 (0.0244) | 0.6003 (0.0252) | 3943.65 |

| Negative bilogistic | 1.1083 (0.1068) | 1.1628 (0.1106) | 3889.43 |

| ct (or Dirichlet) | 0.9066 (0.1206) | 0.8415 (0.1072) | 3897.57 |

| AIC | |||

| Logistic | 0.6126 (0.0114) | Nil | 3935.83 |

| Negative logistic | 0.8653 (0.0293) | Nil | 3883.64 |

| Husler–Reiss | 1.2908 (0.0321) | Nil | 3839.97 |

| Bilogistic | 0.6068 (0.0232) | 0.6184 (0.0231) | 3937.75 |

| Negative bilogistic | 1.1356 (0.1036) | 1.1759 (0.1065) | 3885.60 |

| ct (or Dirichlet) | 0.8727 (0.1101) | 0.8151 (0.0967) | 3894.70 |

| AIC | |||

| Logistic | 0.6063 (0.0117) | Nil | 3805.05 |

| Negative logistic | 0.8826 (0.0305) | Nil | 3758.71 |

| Husler–Reiss | 1.3070 (0.0332) | Nil | 3719.32 |

| Bilogistic | 0.6142 (0.0231) | 0.5980 (0.0245) | 3806.90 |

| Negative bilogistic | 1.1027 (0.1029) | 1.1632 (0.1055) | 3760.61 |

| ct (or Dirichlet) | 0.8996 (0.1146) | 0.8365 (0.1005) | 3767.56 |

| AIC | |||

| Logistic | 0.6040 (0.0115) | Nil | 3745.97 |

| Negative logistic | 0.8924 (0.0304) | Nil | 3699.66 |

| Husler–Reiss | 1.3200 (0.0332) | Nil | 3664.18 |

| Bilogistic | 0.6054 (0.0229) | 0.6026 (0.0229) | 3747.97 |

| Negative bilogistic | 1.1070 (0.0979) | 1.1343 (0.1005) | 3701.64 |

| ct (or Dirichlet) | 0.8946 (0.1064) | 0.8649 (0.1018) | 3707.80 |

| AIC | |||

| Logistic | 0.6149 (0.0114) | Nil | 3869.14 |

| Negative logistic | 0.8605 (0.0290) | Nil | 3810.94 |

| Husler–Reiss | 1.2883 (0.0320) | Nil | 3764.18 |

| Bilogistic | 0.6283 (0.0242) | 0.6006 (0.0260) | 3870.76 |

| Negative bilogistic | 1.1129 (0.1076) | 1.2121 (0.1143) | 3812.71 |

| ct (or Dirichlet) | 0.8926 (0.1183) | 0.7915 (0.0977) | 3823.01 |

| Brazilian IBOV and Indian NIFTY | Weak | Weak |

| Brazilian IBOV and S/African JALSH | Weak | Weak |

| Russian IMOEX and Indian NIFTY | Weak | Weak |

| Russian IMOEX and Chinese SHCOMP | Weak | Weak |

| Russian IMOEX and S/African JALSH | Weak | Weak |

| Indian NIFTY and Chinese SHCOMP | Weak | Weak |

| Chinese SHCOMP and S/African JALSH | Weak | Weak |

| Panel B | ||

| Brazilian IBOV and Russian IMOEX | Fairly strong | Fairly strong |

| Indian NIFTY and S/African JALSH | Fairly strong | Fairly strong |

| Panel C | ||

| Brazilian IBOV and Chinese SHCOMP | Fairly strong | Nearly weak |

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2022 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Sigauke, C.; Mukhodobwane, R.; Chagwiza, W.; Garira, W. Asymptotic Dependence Modelling of the BRICS Stock Markets. Int. J. Financial Stud. 2022, 10, 58. https://doi.org/10.3390/ijfs10030058

Sigauke C, Mukhodobwane R, Chagwiza W, Garira W. Asymptotic Dependence Modelling of the BRICS Stock Markets. International Journal of Financial Studies. 2022; 10(3):58. https://doi.org/10.3390/ijfs10030058

Chicago/Turabian StyleSigauke, Caston, Rosinah Mukhodobwane, Wilbert Chagwiza, and Winston Garira. 2022. "Asymptotic Dependence Modelling of the BRICS Stock Markets" International Journal of Financial Studies 10, no. 3: 58. https://doi.org/10.3390/ijfs10030058

APA StyleSigauke, C., Mukhodobwane, R., Chagwiza, W., & Garira, W. (2022). Asymptotic Dependence Modelling of the BRICS Stock Markets. International Journal of Financial Studies, 10(3), 58. https://doi.org/10.3390/ijfs10030058