2.1. Evolution of Pension Funds in Ghana

Pensions in Ghana started as far back as the colonial era to cater for those who worked in the colonial administration and mine workers (

Kpessa-Whyte 2011). It was a non-contributory scheme that was exclusive and available to only urban dwellers, mostly the Europeans and a few Africans, to reward and encourage loyalty. In 1950, the first pension scheme, the Pension Ordinance No. 42 (Cap 30) and Superannuation schemes were introduced to cater for the retirement benefit of Ghanaian public workers, such as teachers, university lecturers, doctors, and nurses; however, a clear majority of Ghanaians were unable to benefit from this scheme (

Ashidam 2011). The Social Security Act (No. 279) was passed in 1965 to cover all private and public-sector workers who were not covered under the previous scheme. It was a provident fund, providing benefits for old age, invalidity and survivor benefit. This scheme was revoked, and the Social Security and National Insurance Act (SSNIT) was established under NRCD 127. In 1991, the Social Security Act was enacted, and the scheme was turned into a defined contribution scheme (

Donkor-Hyiaman et al. 2019). However, some workers such as the Armed Forces, Police and Prison Service were exempted from joining the scheme. Ghana operates three pension benefits: Old Age Benefit, Invalidity Benefit, and Death Survivor Payment. To qualify for the old age benefit under the new scheme, a worker must have worked for a minimum of 240 months and be at least 60 years of age, while those in the mines and other extractive industries have a mandatory retirement age of 58. Workers who have been injured at work may qualify for payment under the invalidity benefit section of the social security system (

Mensah 2013). If a worker dies before the required retirement age, their benefits are calculated as the present value of all contributions and paid as a lump sum to the surviving spouse or dependents; this is known as the death survivor payment. Funding of the schemes is based on contributions made by the employer and the employee on behalf of the employee. The employer contributes 12.5% of the employee’s salary, while the employee contributes 5% of their salary, totalling 17.5%. These contributions are invested, and when the employee reaches retirement age, becomes permanently incapacitated or dies before retirement, the total contributions and returns on the investment are paid as a lump sum to the employee or their dependents (

Kpessa-Whyte 2011).

Over the years, concerns have been raised about SSNIT not paying enough benefits to retirees and failing to include informal sector workers, who constitute about 80% of the workforce in the scheme; this led to a reform in July 2004. This led to the drafting and passing of the National Pensions Act 2008 to provide universal pensions to all Ghanaian workers (

Kpessa-Whyte 2011). The Act is divided into four parts; the first discusses having a regulatory body. The second part deals with the provision of the schemes, the third part deals with the management of the schemes, and finally, the general provisions of the Act are contained in the fourth part. Under the new scheme, 18.5% of a worker’s monthly salary will be paid towards their pension, which is distributed between the first and second tiers. The first two tiers are mandatory, and the third tier is voluntary. The first tier, which makes up 13.5% of an employee’s monthly salary, goes to SSNIT, and it is mandatory for both public and private sector workers. Still, self-employed individuals have the option of joining or not. Out of the 13.5%, 2.5% goes to the NHIS, and 5% of an employee’s monthly salary is allocated to the second tier, which is managed privately by approved pension fund managers. The aim is to give pensioners lump sum benefits compared to what is presently available under the SSNIT. The third tier is a voluntary provident fund and personal pension scheme, which provides tax benefit incentives for workers who opt for this scheme and the first two (

Dorfman 2015). It could be managed personally or by approved pension fund managers. The previous pension schemes in Ghana were relatively exclusive and did not cover 80% of Ghana’s working population. The introduction of the Authority and the third tier is an effort to address the issues concerning the old pensions system, which by design excluded those in the informal sector and did not provide avenues for the citizenry to arrange their pensions in addition to the state pension. In this case, pension fund managers (firms) oversee the pensions of citizens who want to attain better pension outcomes during retirement. All pension fund managers in Ghana are required registered to register individually as limited liability firms under the Companies Act, 2019 and seek additional certifications of operation from National Pensions Regulatory Authority (

NPRA 2022). There are no limitations on the forms on registrations, but it must be prescribed by the NPRA and the Companies Act, 2019 (

Kpessa-Whyte and Tsekpo 2020). There are no legal restrictions on where investments can be made, as far as it is a legitimate investment venture (

Kpessa-Whyte 2011).

2.2. Corporate Governance of Pension Funds

Corporate governance has been explained as a mechanism by which operational managers of entities are made to act in the interest of the owners of the entities and other stakeholders (

Aboagye and Otieku 2010). The authors alluded that the organisations with good corporate governance structures report better performance, implying that when managers take keen interest in putting the right structures in place, the firm performs well. The

OECD (

2004) also explains corporate governance as “a set of relationships between a company’s management, its board, its shareholders, and other stakeholders. Corporate governance provides the structure through which the company’s objectives are set, and the means of attaining those objectives and monitoring performance are determined” (

Alda 2021). Corporate governance includes relations between owners and top management, and these relations make it possible for agents to be accountable to shareholders (

Kowalewski 2016). Corporate governance concerns rules and regulations that organisations apply and follow to achieve visions and missions translated into stated objectives for boards of directors and managers of resources. Sound corporate governance encourages the efficient use of resources and accountability for managers’ stewardship of those resources (

Ioannou and Serafeim 2012). Institutions that practice good corporate governance are more likely to achieve institutional objectives and goals (

Agyemang and Castellini 2015).

Kumari and Pattanayak (

2017) recommended that shareholders tie the remuneration of board members to their performance and that organisations develop an annual mechanism to check management cum board activities.

Kowalewski (

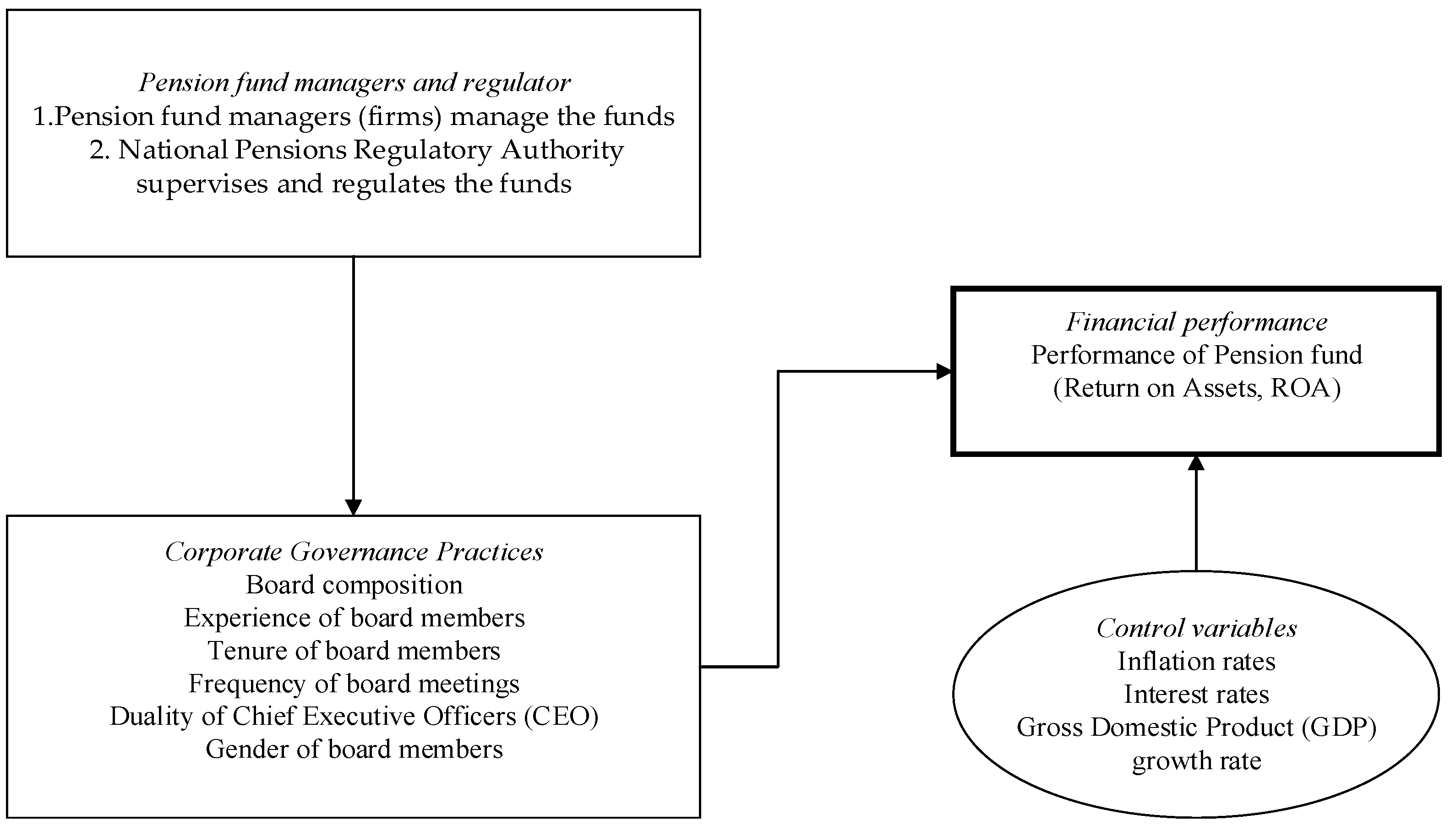

2016) advocates the need for a firm (well-informed) board to drive an organisation’s vision with a good sense of judgment in management and performance. Researchers have professed the need for strong corporate governance mechanisms in all aspects of an institution’s life to ensure the diligence and integrity of these entities’ operations. Good corporate governance is now a prime concern to owners and other stakeholders of institutions. These concerns extend to the general welfare of society. Good stewardship and sustained accountability are expected from firms by society. In pension fund management settings, two sets of factors affect corporate entity’s effectiveness. The first is the internal corporate governance factors relating to pension fund management. This involves effective interactions between internal systems relating to pension funds. The second factor is the external corporate governance factors concerning the regulatory and legal framework under which the pension funds operate. The first node in

Figure 1 exhibits the managers of pension funds with the regulators from the National Pensions and Regulatory Authority (NPRA), which is a body that supervises pension fund management in Ghana. The National Pension Act 2008 (Act 766) established the National Pensions Regulatory Authority (NPRA) as the sole supervisor (regulator) of pension fund activities in Ghana (

Donkor-Hyiaman et al. 2019). The NPRA monitors the operations of all pensions in the country by demanding regular reports from the pension fund managers (

Anku-Tsede 2019). The regulatory body also updates the pension managers of new regulatory requirements. It oversees the registration and dissolution of pension fund managers (firms) by invoking various legal codes of the country. The NPRA trains fund managers and monitors the progress of pension funds by reviewing annual reports. The NPRA assigns supervisors to each of the pension funds, and internally, there is a specific manager within the pension fund firms to meet the requirements of the NPRA (

NPRA 2022).

The second node represents the components of corporate governance practices on pension funds. The third node shows macroeconomic variables that reduce the biases in the observed variables of corporate governance practices towards the performance of pension funds. These three nodes relate to pension funds’ finance performance, which is represented by the return on assets in the fourth node.

2.3. Theories and Hypothesis Development

Scholars have discussed the concept of corporate governance and ownership of assets in various stages of human development.

Goldsmith (

1995) referenced Adam Smith, 1776, who argues that most wealth managers cannot be expected to watch over it with the same zeal as the owners. This breeds the concept of conflict of interest amongst owners and managers of their firms. It brings in agency theory. Agency theory postulates that an agent or agency (board of directors) is hired by one or more person(s), called the principal(s) (shareholders), under a contract and is compensated by the principal to achieve desired outcomes for the principal (

Ellis and Johnson 1993;

Fama 1980). Owners of institutions give away decision-making rights to agents, hoping that the agents will act in their best interest and respect the fiduciary duty that promotes utmost good faith (

Eisenhardt 1989).

Arrow (

1985) designed two models of asymmetrical information, explaining agency theory through the hidden action model and the hidden information model. In the hidden action model, the principal does not observe the agent’s actions but only observes the outcome of the actions. The hidden information model shows a principal who observes the agent’s actions but does not know the vital information needed to perform those actions (

Buallay et al. 2017). Information asymmetry arises when the principal does not have all the information when analysing the agent’s performance. Adverse selection occurs when the principal selects the wrong agent for the task ahead. In addition, agents can underperform on their promises to obtain maximum compensation; this is a moral hazard (

Darko et al. 2016;

Ellis and Johnson 1993;

Fama and Jensen 1983). The moral hazard is higher when the agent has the more specialised knowledge to perform a task but fails. Thus, it may be impossible for the principal to ensure that the agent always acts in their best interests. However, there are three ways in which this challenge can be minimised, namely:

Board independence (to supervise management).

Market for corporate control (mischievous managers are controlled by an active merger and acquisition market programme).

Agent equity ownership—ensuring that agents are part owners of the organisation they manage.

The above-listed methods come at a cost to the principal (

Hill and Jones 1992;

Jensen and Meckling 1976). Some sources of agency cost are recruitment, adverse selection, specifying principal preferences, establishing incentives, moral hazard, stealing, side deals, monitoring and policing, bonding and insurance (

Sami et al. 2011;

Shapiro 2005). Sometimes, the costs incurred in regulating and controlling agents may not be worth the benefits of improved agent behaviour (

Mitnick 2015;

Wiersema and Bantel 1992). Studies have criticised the agency theory, saying it has been overly simple with its assumptions and does not reflect real-world activities. The usage of agency theory in academia has received its criticisms. For instance,

Kato et al. (

2017) argued that agency problems are not immune to only one firm but many firms.

Vafeas and Vlittis (

2016) have claimed that agency theory does not address any apparent organisational problems that cannot be generalised. Agents acting on their parochial interest can derail firm profitability, leading to shareholder losses.

Another theory that supports corporate governance and pension funds is the stakeholder theory. The theory assumes organisational management within a firm comes with multiple constituents made up of owners, employees, suppliers, local communities, creditors and other stakeholders (

Donkor-Hyiaman et al. 2019;

Jackson 2005;

Korac-Kakabadse et al. 2001).

Jones and Wicks (

1999) argued that stakeholder theory suggests that the extent to which managers attend to stakeholder interests largely depends upon the managers’ values and moral guidelines. Good morals and values translate to their behaviour.

Bonnafous-Boucher (

2005) suggested that the demographic characteristics of top managers and stakeholders lead to firms’ different strategic decisions. Therefore, top management characteristics do have an impact on the firm performance. Inferring from

Aguilera and Crespi-Cladera’s (

2016) study, it could be hypothesised that limited studies on board characteristics such as board composition could be limited. It is important to understand the impact of board composition on firm performance. A firm’s board of directors is usually based on institutional requirements of both host and home countries (

Morgan and Kristensen 2006). Hypothetically, corporate governance and the performance of pension funds have been framed as follows:

H1: Board composition positively affects pension fund performance.

H2: The experience of the board members positively influences pension fund performance.

H3: Frequency of board meetings positively influences pension fund performance.

H4: Tenure of the board members positively influences pension fund performance.

Concerning studies on performance, corporate governance structures have significantly impacted the firm’s performance (

Soana 2011;

Jo et al. 2014). A significant component of corporate governance is the board of directors, of which the CEO is a member. An element of corporate board structure is the separation of the board chairman from the firm’s CEO in terms of roles. CEO duality suggests that the board chairman also acts as the CEO (

Samaha et al. 2012). This will lead to a conflict of interests.

Lattemann et al. (

2009) argue that to deal with CEO duality, there should be clear policy and practical measures to separate their roles, leading to higher levels of corporate transparency and performance. In contrast, authors such as

Giannarakis (

2014),

Phan and Hegde (

2012) have posited that CEO duality affects disclosures and organisational practices, negatively affecting the firm’s performance. It was hypothesised as the following:

H5: CEO duality is negatively associated with pension fund performance.

A review of studies also suggests that the gender composition of the board has been usually associated with the firm’s financial performance (

Sami et al. 2011).

Vafeas and Vlittis (

2019) mentioned that independent female directors, compared to their male counterparts, might take organisational practice issues seriously due to their stronger moral orientations and reputational reasons.

Rupp et al. (

2006) argued that an increasing number of women on the boards would have positive impacts on the firm’s performance. Thus:

H6: Diversity of the board is positively associated with pension fund performance

,

,

{kind=link}

{kind=link}

{kind=link}