Exploring Online Payment System Adoption Factors in the Age of COVID-19—Evidence from the Turkish Banking Industry

Abstract

:1. Introduction

2. Literature Review

2.1. Next-Generation Payment Instruments

2.2. Factors Affecting the Adoption of Online Payment Systems

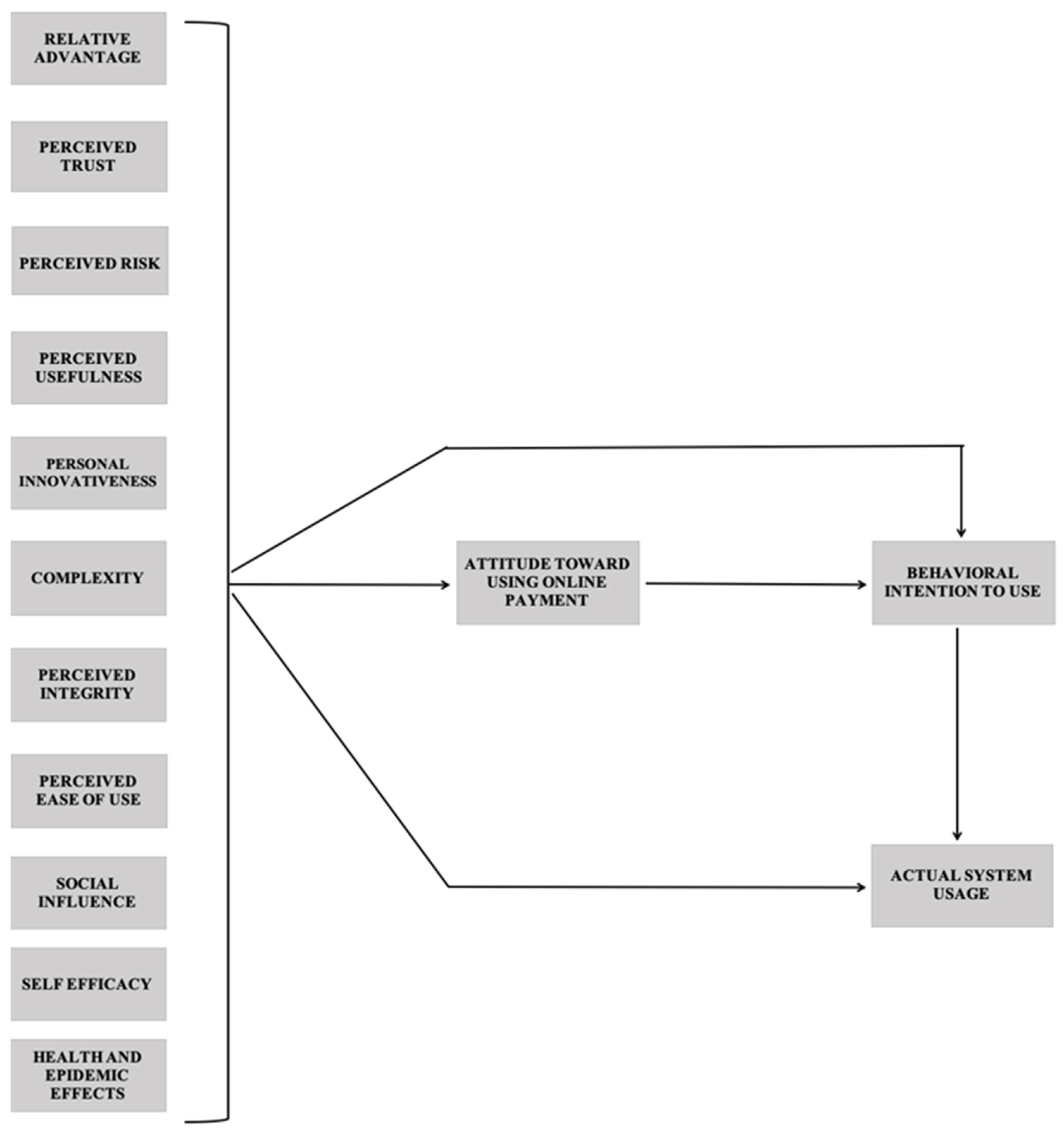

2.3. Theoretical Framework

3. Research Methodology

3.1. Measures and Data Collection

3.2. Descriptive Statistics

3.3. Analyses

3.3.1. Exploratory Factor Analysis

3.3.2. Regression Analysis

4. Results and Discussion

4.1. Exploratory Factor Analysis

4.2. Regression Analysis

4.3. Discussion

Limitations

5. Conclusions

Author Contributions

Funding

Institutional Review Board Statement

Informed Consent Statement

Data Availability Statement

Conflicts of Interest

Abbreviations

| CFA | Confirmatory Factor Analysis |

| CMPA | Compatibility |

| COMPE | Complexity |

| EFA | Exploratory Factor Analysis |

| EFT | Electronic Fund Transfer |

| E-TAM | Extended Technology Acceptance Model |

| FC | Facilitating Conditions |

| Fintech | Financial Technologies |

| HE | Health and Epidemic Effects |

| IDT | Innovation Diffusion Theory |

| NFC | Near Field Communication |

| PC | Perceived Cost |

| PCR | Perceived Credibility |

| PE | Perceived Enjoyment |

| PEU | Perceived Ease of Use |

| PI | Perceived Integrity |

| PIN | Perceived Innovativeness |

| PR | Perceived Risk |

| PT | Perceived Trust |

| PU | Perceived Usefulness |

| RA | Relative Advantage |

| QIC | Quality of Internet Connection |

| QR | Quick Response Code |

| SE | Self-Efficacy |

| SEM | Structural Equation Modeling |

| SI | Social Influence |

| TAM | Technology Acceptance Model |

| TRA | Theory of Reasoned Action |

| UB | Ubiquity |

| UTAUT | Unified Theory of Acceptance and Use of Technology |

Appendix A

{kind=link}

| FACTORS | ITEMS | SOURCE |

|---|---|---|

| 1. PERCEIVED EASE OF USE (PEU) | (PEU1) It is easy for me to make my payment transactions online. | Davis et al. (1989); Venkatesh and Davis (2000); Schierz et al. (2010); Lin (2011); Chuang et al. (2016) |

| (PEU2) The online payment process is clear and understandable. | ||

| (PEU3) I can easily perform my transactions such as shopping, public payments (invoices, taxes, etc.) online. | ||

| (PEU4) I find it easy to complete my payment transactions online. | ||

| (PEU5) I believe it is easy to adapt to paying online. | ||

| 2. PERCEIVED USEFULNESS (PU) | (PU1) Making my payment transactions online increases my productivity, efficiency and performance. | Davis (1989); Hanafizadeh et al. (2014); Schierz et al. (2010); Gu et al. (2009); Raleting and Nel (2011) |

| (PU2) I save a lot of time and effort by making my payments online. | ||

| (PU3) Making my payments online gives me more control over my payment transactions. | ||

| (PU4) Paying online is useful when processing my payment transactions. | ||

| (PU5) I find it very useful to make my payments online. | ||

| 3. PERCEIVED TRUST (PT) | (PT1) I am not worried about paying online, as I know my transactions will be safe and secure. | Gefen et al. (2003); Al-Somali et al. (2009); Hanafizadeh et al. (2014) |

| (PT2) While I make my payment transactions online, I feel safe when sending sensitive information requested for the transaction. | ||

| (PT3) Sites where I pay online will not disclose any information to a third party unless I give my permission. | ||

| (PT4) I believe that privacy is guaranteed for sites where I pay online. | ||

| (PT5) I trust my online payment transactions as if I made a physical payment. | ||

| 4. PERCEIVED RISK (PR) | (PR1) I think that making payments online is more risky than other traditional payment services. | Rogers (1983); Bauer et al. (2005); Raleting and Nel (2011) |

| (PR2) When paying online, the system I receive service may not perform well and may perform the payment incorrectly. | ||

| (PR3) Paying online is risky. | ||

| (PR4) I am afraid of the misuse of personal information when making payments online. | ||

| (PR5) I am afraid that I will lose my money while making any payment transactions online. | ||

| (PR6) I am afraid of making payments online because I think people will access my account and personal information. | ||

| 5. SOCIAL INFLUENCE (SI) | (SI1) Suggestions from friends/family members/mass media influence my decision to make payments online. | Venkatesh and Davis (2000); Venkatesh et al. (2003); Sivathanu (2018); Gu et al. (2009) |

| (SI2) Many people who have an important place in my life think that I need to make payments online. | ||

| (SI3) In general, when I use any new technology, I trust my own instincts more than anyone else’s advice. | ||

| (SI4) Most people around me make their payments online. | ||

| (SI5) Making my payments online improves my status in society. | ||

| 6. COMPATIBILITY (CMPA) | (CMPA1) Making payments online is suitable for my lifestyle. | Rogers (1983); Agarwal and Prasad (1998); Hanafizadeh et al. (2014); Schierz et al. (2010) |

| (CMPA2) Making my payments online is compatible with the way I manage my payment transactions. | ||

| (CMPA3) Adopting the internet card payment system to be able to make payments online fits my way of working. | ||

| 7. SELF EFFICACY (SE) | (SE1) I am sure that I will prefer to make payments online even if I have never made a transaction before. | Venkatesh and Davis (1996); Gu et al. (2009); Boonsiritomachai and Pitchayadejanant (2017) |

| (SE2) If there are directions in the system about how to make transactions, I can make my payments online. | ||

| (SE3) If I had seen someone else use it before trying it myself, I could have made my payments online. | ||

| 8. RELATIVE ADVANTAGE (RA) | (RA1) I can access and make my payment transactions over the internet anytime and anywhere. | Rogers (1983); Moore and Benbasat (1991); Lin (2011) |

| (RA2) Making my payment transactions online enables me to perform my daily work quickly. | ||

| (RA3) My adaptation to online card payment is useful for managing my payment transactions. | ||

| 9. PERCEIVED CREDIBILITY (PCR) | (PC1) Making my payment transactions online does not disclose my personal information. | Wang et al. (2003); Hanafizadeh et al. (2014) |

| (PC2) I can find it safe to pay by card on the internet while carrying out the process of my payment transactions. | ||

| (PC3) I can find the internet safe while requesting and receiving other information. | ||

| 10. HEALTH AND EPIDEMIC EFFECTS (HE) | (HE1) Despite the COVID-19 pandemic, I did not delay the card payment transactions I made online. | Acemoğlu and Johnson (2007) |

| (HE2) With the COVID-19 pandemic, I made all my possible payment transactions online. | ||

| (HE3) During the quarantine process caused by the COVID-19 pandemic, the number of my payment transactions (online shopping, invoices, etc.) increased compared to the online payment transactions I made in the normal period. | ||

| (HE4) The COVID-19 pandemic has changed my perception of my online payment transactions. | ||

| (HE5) Even after the COVID-19 pandemic is over, I will try to make my payments online. | ||

| 11. QUALITY OF INTERNET CONNECTION (QIC) | (QIC1) My access to the internet is easy. | Sathye (1999); Al-Somali et al. (2009); |

| (QIC2) The Internet enables me to handle my online financial transactions accurately. | ||

| (QIC3) Using the internet for handling online financial transactions is efficient. | ||

| (QIC4) The Internet guarantees that all transactions to the bank have been completed. | ||

| 12. PERCEIVED COST (PC) | (PC1) It would be very costly to use the internet for my payment transactions. | Sathye (1999); Hanafizadeh et al. (2014) |

| (PC2) I think that using the internet for my payment transactions will have a high cost of internet access. | ||

| (PC3) I have financial barriers (eg internet access cost) to use the internet for my payment transactions. | ||

| 13. PERCEIVED INTEGRITY (PI) | (PI1) I think the companies I pay for are honest. | Bhattacherjee (2000); Lin (2011) |

| (PI2) I think the companies I make payment transactions will with fulfill their commitments. | ||

| (PI3) I think the companies with which I make payment transactions give unbiased information about the transactions. | ||

| 14. PERCEIVED ENJOYMENT (PE) | (PE1) Making my payments online is fun. | Davis et al. (1992); Pikkarainen et al. (2004) |

| (PE2) Making my payments online is positive. | ||

| (PE3) Making my payments online is exciting. | ||

| (PE4) Making my payments online is wise. | ||

| 15. FACILITATING CONDITIONS (FC) | (FC1) I have the necessary resources to make my payment transactions online. | Taylor and Todd (1995); Burnett (2000); Yu (2012) |

| (FC2) I have the necessary knowledge to make my payment transactions online. | ||

| (FC3) Making my payment transactions online is compatible with my life. | ||

| (FC4) Help can be obtained when I have problems while making my payment transactions online. | ||

| 16. UBIQUITY (UB) | (UB1) I can make my payment transactions from anywhere on the internet. | Anderson and Narus (1990); Zhou (2012) |

| (UB2) I can make my payment transactions online whenever I want. | ||

| (UB3) If necessary, I can make my payment transactions online anytime, anywhere. | ||

| 17. COMPLEXITY (COMPE) | (COMPE1) Making payments online requires a lot of mental effort. | Rogers (1983); Taylor and Todd (1995) |

| (COMPE2) Making payments online requires technical skills. | ||

| (COMPE3) Making payments online can be frustrating. | ||

| 18. PERSONAL INNOVATIVENESS (PIN) | (PI1) My friends and neighbors often come to me for advice about new products and innovations. | Agarwal and Karahanna (2000); Sulaiman et al. (2007); Lee et al. (2007) |

| (PI2) I like to buy new and different things. | ||

| (PI3) I am usually among the first to try new products. | ||

| (PI4) I like to keep up with technological advances. | ||

| (PI5) It is very important to me to feel that I am a part of a group. | ||

| ATTITUDE (AT) | (AT1) I think it is a wise idea to make payments online. | Davis (1989); Schierz et al. (2010); Lin (2011) |

| (AT2) I am not satisfied with the traditional payment system. | ||

| (AT3) Using the internet while purchasing products and services and paying bills is a nice experience. | ||

| (AT4) I will encourage online card payments among my colleagues. | ||

| (AT5) Overall, my attitude towards online card payment is positive. | ||

| BEHAVIORAL INTENTION TO USE (BI) | (BI1) I am thinking of making all my payments over the internet. | Davis (1989); Venkatesh et al. (2003); Gefen et al. (2003); Schierz et al. (2010); Lin (2011) |

| (BI2) I am thinking of making payments online frequently. | ||

| (BI3) I believe that it is valuable for me to adopt online payment transactions with a card. |

| Component | Initial Eigenvalues | Extraction Sums of Squared Loadings | ||||

|---|---|---|---|---|---|---|

| Total | % of Variance | Cumulative % | Total | % of Variance | Cumulative % | |

| 1 | 21.316 | 29.606 | 29.606 | 21.316 | 29.606 | 29.606 |

| 2 | 5.440 | 7.556 | 37.162 | 5.440 | 7.556 | 37.162 |

| 3 | 4.735 | 6.576 | 43.738 | 4.735 | 6.576 | 43.738 |

| 4 | 2.571 | 3.571 | 47.309 | 2.571 | 3.571 | 47.309 |

| 5 | 2.177 | 3.024 | 50.333 | 2.177 | 3.024 | 50.333 |

| 6 | 1.923 | 2.671 | 53.004 | 1.923 | 2.671 | 53.004 |

| 7 | 1.797 | 2.497 | 55.501 | 1.797 | 2.497 | 55.501 |

| 8 | 1.641 | 2.279 | 57.780 | 1.641 | 2.279 | 57.780 |

| 9 | 1.555 | 2.160 | 59.939 | 1.555 | 2.160 | 59.939 |

| 10 | 1.434 | 1.991 | 61.931 | 1.434 | 1.991 | 61.931 |

| 11 | 1.312 | 1.822 | 63.753 | 1.312 | 1.822 | 63.753 |

| Extraction Method: Principal Component Analysis. | ||||||

| Factor 1 | Factor 2 | Factor 3 | Factor 4 | Factor 5 | Factor 6 | Factor 7 | Factor 8 | Factor 9 | Factor 10 | Factor 11 | |

|---|---|---|---|---|---|---|---|---|---|---|---|

| UB2 | 0.840 | ||||||||||

| UB3 | 0.816 | ||||||||||

| FC1 | 0.806 | ||||||||||

| UB1 | 0.779 | ||||||||||

| FC2 | 0.767 | ||||||||||

| FC3 | 0.742 | ||||||||||

| RA1 | 0.681 | ||||||||||

| QIC2 | 0.649 | ||||||||||

| HE5 | 0.648 | ||||||||||

| QIC3 | 0.639 | ||||||||||

| RA2 | 0.624 | ||||||||||

| CMPA3 | 0.616 | ||||||||||

| PE4 | 0.609 | ||||||||||

| CMPA2 | 0.602 | ||||||||||

| PE2 | 0.591 | ||||||||||

| FC4 | 0.590 | ||||||||||

| HE1 | 0.573 | ||||||||||

| CMPA1 | 0.569 | ||||||||||

| RA3 | 0.549 | ||||||||||

| QIC1 | 0.536 | ||||||||||

| HE2 | 0.516 | ||||||||||

| PT4 | 0.828 | ||||||||||

| PT3 | 0.823 | ||||||||||

| PT2 | 0.642 | ||||||||||

| PC1 | 0.633 | ||||||||||

| PT5 | 0.633 | ||||||||||

| PC2 | 0.558 | ||||||||||

| PC3 | 0.549 | ||||||||||

| PT1 | 0.515 | ||||||||||

| PR5 | 0.760 | ||||||||||

| PR3 | 0.738 | ||||||||||

| PR4 | 0.730 | ||||||||||

| PR6 | 0.721 | ||||||||||

| PR1 | 0.703 | ||||||||||

| PR2 | 0.688 | ||||||||||

| PU2 | 0.760 | ||||||||||

| PU1 | 0.721 | ||||||||||

| PU3 | 0.710 | ||||||||||

| PU5 | 0.699 | ||||||||||

| PU4 | 0.681 | ||||||||||

| PIN3 | 0.809 | ||||||||||

| PIN2 | 0.766 | ||||||||||

| PIN4 | 0.672 | ||||||||||

| PIN1 | 0.610 | ||||||||||

| COMPE1 | 0.828 | ||||||||||

| COMPE2 | 0.809 | ||||||||||

| COMPE3 | 0.612 | ||||||||||

| PC3 | 0.519 | ||||||||||

| PI2 | 0.697 | ||||||||||

| PI3 | 0.681 | ||||||||||

| PI1 | 0.650 | ||||||||||

| PEU1 | 0.742 | ||||||||||

| PEU3 | 0.609 | ||||||||||

| PEU4 | 0.538 | ||||||||||

| SI2 | 0.745 | ||||||||||

| SI1 | 0.550 | ||||||||||

| SI5 | 0.514 | ||||||||||

| SE2 | 0.710 | ||||||||||

| SE3 | 0.651 | ||||||||||

| HE4 | 0.794 | ||||||||||

| HE3 | 0.737 |

References

- Abdullah, Engku Mohamad Engku, Aisyah Abdul Rahman, and Ruzita Abdul Rahim. 2018. Adoption of financial technology (Fintech) in mutual fund/unit trust investment among Malaysians: Unified Theory of Acceptance and Use of Technology (UTAUT). International Journal of Engineering & Technology 7: 110–18. [Google Scholar]

- Aboelmaged, Mohamed, and Tarek R. Gebba. 2013. Mobile Banking Adoption: An Examination of Technology Acceptance Model and Theory of Planned Behavior. International Journal of Business Research and Development 2: 35–50. [Google Scholar] [CrossRef]

- Acemoğlu, Daron, and Simon Johnson. 2007. Disease and Development: The Effect of Life Expectancy on Economic Growth. Journal of Political Economy 115: 925–85. [Google Scholar] [CrossRef] [Green Version]

- Agarwal, Ritu, and Elena Karahanna. 2000. Time Flies When You’re Having Fun: Cognitive Absorption and Beliefs about Information Technology Usage. MIS Quarterly 24: 665–94. [Google Scholar] [CrossRef]

- Agarwal, Ritu, and Jayesh Prasad. 1998. A Conceptual and Operational Definition of Personal Innovativeness in the Domain of Information Technology. Information Systems Research 9: 204–15. [Google Scholar] [CrossRef]

- Ajzen, Icek. 2002. Perceived Behavioral Control, Self-Efficacy, Locus of Control, and the Theory of Planned Behavior. Journal of Applied Social Psychology 32: 665–83. [Google Scholar] [CrossRef]

- Ajzen, Icek, and Martin Fishbein. 1980. Understanding Attitudes and Predicting Social Behavior. Englewood Cliffs: Prentice-Hall. [Google Scholar]

- Akturan, Ulun, and Nuray Tezcan. 2012. Mobile Banking Adoption of the Youth Market, Perceptions and Intentions. Emerald Insight 30: 444–59. [Google Scholar]

- Aldás-Manzano, Joaquin, Carlos Lassala-Navarre, Carla Ruiz-Mafé, and Silvia Sanz-Blas. 2009. Key Drivers of Internet Banking Services Use. Online Information Review 33: 672–95. [Google Scholar] [CrossRef]

- Al-Somali, Sabah Abdullah, Roya Gholami, and Ben Clegg. 2009. An Investigation into the Acceptance of Online Banking in Saudi Arabia. Technovation 29: 130–41. [Google Scholar] [CrossRef]

- AlSoufi, Ali, and Hayat Ali. 2014. Customers’ perception of m-banking adoption in Kingdom of Bahrain: An empirical assessment of an extended TAM model. arXiv arXiv:1403.2828. [Google Scholar]

- Amin, Hanudin, Mohd Rizal Abdul Hamida, Suddin Ladaa, and Zuraidah Anis. 2008. The adoption of mobile banking in Malaysia: The case of Bank Islam Malaysia Berhad (BIMB). International Journal of Business and Society 9: 43. [Google Scholar]

- Anderson, James C., and James A. Narus. 1990. A Model of Distributor Firm and Manufacturer Firm Working Partnerships. Journal of Marketing 54: 42–58. [Google Scholar] [CrossRef]

- Bankole, Felix O., Omolola O. Bankole, and Irwin Brown. 2011. Mobile banking adoption in Nigeria. The Electronic Journal of Information Systems in Developing Countries 47: 1–23. [Google Scholar] [CrossRef]

- Bauer, Hans H., Tina Reichardt, Stuart J. Barnes, and Marcus M. Neumann. 2005. Driving Consumer Acceptance of Mobile Marketing: A Theoretical Framework and Empirical Study. Journal of Electronic Commerce Research 6: 181–91. [Google Scholar]

- Bhattacherjee, Anol. 2000. Acceptance of E-commerce Services: The Case of Electronic Brokerages. IEEE Transactions on System, Man, and Cybernetics—Part A: Systems and Humans 20: 411–20. [Google Scholar] [CrossRef] [Green Version]

- BKM. 2020. General Statistical Data for Selected Mounth. Available online: https://bkm.com.tr/en/secilen-aya-ait-istatistikler/ (accessed on 12 December 2021).

- Bommer, William H., Shailesh Rana, and Emil Milevoj. 2022. A meta-analysis of e-Wallet adoption using the UTAUT model. International Journal of Bank Marketing 40: 791–819. [Google Scholar] [CrossRef]

- Boonsiritomachai, Waranpong, and Krittipat Pitchayadejanant. 2017. Determinants Affecting Mobile Banking Adoption by Generation Y Based on the Unified Theory of Acceptance and Use of Technology Model Modified by the Technology Acceptance Model Concept. Kasetsart Journal of Social Sciences 40: 349–58. [Google Scholar] [CrossRef]

- Burnett, Rachel. 2000. Legal Aspects of E-commerce. Computing and Control Engineering Journal 11: 111–14. [Google Scholar] [CrossRef]

- Cao, Wen. 2016. FinTech Acceptance Research in Finland–Case Company Plastc. Unpublished Master’s thesis, Aalto University School of Business, Espoo, Finland. [Google Scholar]

- Chitungo, Shallone K., and Simon Munongo. 2013. Extending the technology acceptance model to mobile banking adoption in rural Zimbabwe. Journal of Business Administration and Education 3: 51–79. [Google Scholar]

- Chuang, Li-Min, Chun-Chu Liu, and Hsiao-Kuang Kao. 2016. The Adoption of Fintech Service: TAM perspective. International Journal of Management and Administrative Sciences 3: 1–15. [Google Scholar]

- Crabbe, Margaret, Craig Standing, Susan Standing, and Heikki Karjaluoto. 2009. An Adoption Model for Mobile Banking in Ghana. International Journal of Mobile Communications 7: 515–43. [Google Scholar] [CrossRef]

- Cunha, Paulo Rupino, Paulo Melo, and Helder Sebastião. 2021. From Bitcoin to Central Bank Digital Currencies: Making Sense of the Digital Money Revolution. Future Internet 13: 165. [Google Scholar] [CrossRef]

- Davis, Fred D. 1989. Perceived Usefulness, Perceived Ease of Use and User Acceptance of Information Technology. MIS Quarterly 13: 318–39. [Google Scholar] [CrossRef] [Green Version]

- Davis, Fred D., Richard P. Bagozzi, and Paul R. Warshaw. 1989. User Acceptance of Computer Technology: A Comparison of Two Theoretical Models. Management Science 35: 982–1003. [Google Scholar] [CrossRef] [Green Version]

- Davis, Fred D., Richard P. Bagozzi, and Paul R. Warshaw. 1992. Extrinsic and Intrinsic Motivation to Use Computers in the Workplace. Journal of Applied Social Psychology 22: 1111–32. [Google Scholar] [CrossRef]

- Dmour, Al Ahilyya, Hani Al Dmour, Ran Al-Barghuthi, and Ran Al-Dmour. 2021. Factors Influencing the Adoption of E-Payment During Pandemic Outbreak (COVID-19): Empirical Evidence. In The Effect of Coronavirus Disease (COVID-19) on Business Intelligence. Cham: Springer, pp. 133–54. [Google Scholar]

- Du, Wenyu, Dorothy E. Leidner, Shan L. Pan, and Wenchi Ying. 2018. Affordances, Experimentation and Actualization of FinTech: A Blockchain Implementation Study. Journal of Strategic Information Systems 28: 50–65. [Google Scholar] [CrossRef]

- Fabris, Nikola. 2019. Cashless society–the future of money or a utopia? Journal of Central Banking Theory and Practice 8: 53–66. [Google Scholar] [CrossRef] [Green Version]

- Fishbein, Martin, and Icek Ajzen. 1975. Beliefs, Attitude, Intention and Behaviour: An Introduction to Theory and Research. Reading: Addison-Wesley. [Google Scholar]

- Gefen, David, Elena Karahanna, and Detmar W. Straub. 2003. Trust and TAM in Online Shopping: An Integrated Model. MIS Quarterly 27: 51–90. [Google Scholar] [CrossRef]

- George, Joey F. 2002. Influences on the Intent to Make Internet Purchases. Internet Research 12: 165–80. [Google Scholar] [CrossRef]

- Ghosh, Gourab. 2021. Adoption of digital payment system by consumer: A review of literature. International Journal of Creative Research Thoughts 9: 412–18. [Google Scholar]

- Gu, Ja-Chul, Sang-Chul Lee, and Yung-Ho Suh. 2009. Determinants of Behavioral Intention to Mobile Banking. Expert Systems with Applications 36: 11605–16. [Google Scholar] [CrossRef]

- Guriting, Petrus, and Nelson Oly Ndubisi. 2006. Borneo Online Banking: Evaluating Customer Perceptions and Behavioral Intention. Management Research News 29: 6–15. [Google Scholar] [CrossRef]

- Hair, Joseph F., William C. Black, Barry J. Babin, Rolph E. Anderson, and Ronald L. Tatham. 2006. Multivariate Data Analysis, 6th ed. Upper Saddle River: Pearson Prentice Hall. [Google Scholar]

- Hanafizadeh, Payam, Mehdi Behboudi, Amir Abedini Koshksaray, and Marziyeh Jalilvand Shirkhani Tabar. 2014. Mobile-banking adoption by Iranian bank clients. Telematics and Informatics 31: 62–78. [Google Scholar] [CrossRef]

- Higgins, James. 2005. Introduction to Multiple Regression (Chp4). The Radical Statistician. Available online: https://www.academia.edu/33271787/Chapter_4_Introduction_to_Multiple_Regression (accessed on 7 March 2021).

- Husni, Emir, N. Kuspriyanto, Noor Basjaruddin, Tito Waluyo Purboyo, Sugeng Purwantoro, and Huda Ubaya. 2011. Efficient tag-to-tag near field communication (NFC) protocol for secure mobile payment. Paper presented at 2011 2nd International Conference on Instrumentation, Communications, Information Technology, and Biomedical Engineering, Bandung, Indonesia, November 8–9. [Google Scholar]

- Interactive Advertising Bureau. 2016. A Global Perspective of Mobile Commerce. Available online: https://www.iab.com/wp-content/uploads/2016/09/2016-IAB-Global-Mobile-Commerce-Report-FINAL-092216.pdf (accessed on 5 February 2022).

- Jiang, Yun, Hassan Ahmad, Asad Hassan Butt, Muhammad Nouman Shafique, and Sher Muhammad. 2021. QR digital payment system adoption by retailers: The moderating role of COVID-19 knowledge. Information Resources Management Journal (IRMJ) 34: 41–63. [Google Scholar] [CrossRef]

- J.P. Morgan. 2020. 2020 E-Commerce Payments Trends Report: Turkey. Available online: https://www.jpmorgan.com/merchant-services/insights/reports/turkey-2020 (accessed on 15 June 2021).

- Kalkan, Pınar. 2021. Analysis of The Effects of Pandemic Economy on Internet Shopping. Journals of Social, Humanities and Administrative Sciences 4: 740–58. [Google Scholar]

- Kapoor, Kawaljeet Kaur, Yogesh K. Dwivedi, and Michael D. Williams. 2014. Rogers’ innovation adoption attributes: A systematic review and synthesis of existing research. Information Systems Management 31: 74–91. [Google Scholar] [CrossRef] [Green Version]

- Kazi, Abdul Kabeer, and Mohammad Adeel Mannan. 2013. Factors affecting adoption of mobile banking in Pakistan. International Journal of Research in Business and Social Science (2147–4478) 2: 54–61. [Google Scholar] [CrossRef]

- Khan, Burhan Ul Islam, Rashidah F. Olanrewaju, Asifa Mehraj Baba, Adil Ahmad Langoo, and Shahul Assad. 2017. A Compendious Study of Online Payment Systems: Past Developments, Present Impact, and Future Considerations. International Journal of Advanced Computer Science and Applications 8: 256–71. [Google Scholar]

- Khraim, Hamza Salim, Younes Ellyan Al Shoubaki, and Aymen Salim Khraim. 2011. Factors Affecting Jordanian Consumers’ Adoption of Mobile Banking Services. International Journal of Business and Social Science 2: 96–105. [Google Scholar]

- Kim, Kyung Kyu, and Bipin Prabhakar. 2004. Initial Trust and the Adoption of B2C e-Commerce: The Case of Internet Banking. Database for Advances in Information System 35: 50–64. [Google Scholar] [CrossRef]

- Kim, Yonghee, Jeongil Choi, Young-Ju Park, and Jiyoung Yeon. 2016. The Adoption of Mobile Payment Services for “Fintech”. International Journal of Applied Engineering Research 11: 1058–61. [Google Scholar]

- Kleijnen, Mirella, Martin Wetzels, and Ko De Ruyter. 2004. Consumer Acceptance of Wireless Finance. Journal of Financial Services Marketing 8: 206–17. [Google Scholar] [CrossRef]

- Kumar, Aswin. 2019. Digital Payment and Its Effects in Indian Business. Iconic Research and Engineering Journals 2: 4–7. [Google Scholar]

- Kumar, Dileep, and Yeonseung Ryu. 2009. A Brief Introduction of Biometrics and Fingerprint Payment Technology. International Journal of Advanced Science and Technology 4: 25–38. [Google Scholar]

- Kurnia, Sherah, Benjamin Lim, and Heejin Lee. 2007. Exploring the Reasons for a Failure of Electronic Payment Systems: A Case Study of an Australian Company. Journal of Research and Practice in Information Technology 39: 231–43. [Google Scholar]

- Lederer, Albert L., Donna J. Maupin, Mark P. Sena, and Youlong Zhuang. 2000. The Technology Acceptance Model and the World Wide Web. Decision Support System 29: 269–82. [Google Scholar] [CrossRef]

- Lee, Hae Young, Hailin Qu, and Yoo Shin Kim. 2007. A Study of the Impact of Personal Innovativeness on Online Travel Shopping Behavior-A Case Study of Korean Travelers. Tourism Management 28: 886–97. [Google Scholar] [CrossRef]

- Levitin, Adam J. 2017. Pandora’s Digital Box: The Promise and Perils of Digital Wallets. Penn Law Journals 166: 305. [Google Scholar] [CrossRef] [Green Version]

- Lin, Hsiu-Fen. 2011. An empirical investigation of mobile banking adoption: The effect of innovation attributes and knowledge-based trust. International Journal of Information Management 31: 252–60. [Google Scholar] [CrossRef]

- Luarn, Pin, and Hsin-Hui Lin. 2005. Toward an Understanding of the Behavioral Intention to Use Mobile Banking. Computers in Human Behavior 21: 873–91. [Google Scholar] [CrossRef]

- Magnier-Watanabe, Remy. 2014. An Institutional Perspective of Mobile Payment Adoption: The Case of Japan. Paper presented at 47th Hawaii International Conference on System Science, Waikoloa, HI, USA, January 6–9. [Google Scholar]

- Mallat, Niina. 2007. Exploring Consumer Adoption of Mobile Payments—A Qualitative Study. Journal of Strategic Information Systems 16: 413–32. [Google Scholar] [CrossRef]

- Meharia, Priyanka. 2012. Assurance on The Reliability of Mobile Payment System and Its Effects on Its’ Use: An Empirical Examination. Accounting and Management Information Systems 11: 97–111. [Google Scholar]

- Moon, Ji-Won, and Young-Gul Kim. 2001. Extending the TAM for a World Wide Web Context. Information & Management 38: 217–30. [Google Scholar]

- Moore, Gary C., and Izak Benbasat. 1991. Development of an Instrument to Measure the Perceptions of Adoption in Information Technology Innovation. Information Systems Research 2: 192–222. [Google Scholar] [CrossRef] [Green Version]

- Náñez Alonso, Sergio Luis, Javier Jorge-Vazquez, and Ricardo Francisco Reier Forradellas. 2021. Central banks digital currency: Detection of optimal countries for the implementation of a CBDC and the implication for payment industry open innovation. Journal of Open Innovation: Technology, Market, and Complexity 7: 72. [Google Scholar] [CrossRef]

- Náñez Alonso, Sergio Luis, Miguel Ángel Echarte Fernández, David Sanz Bas, and Jarosław Kaczmarek. 2020. Reasons fostering or discouraging the implementation of central bank-backed digital currency: A review. Economies 8: 41. [Google Scholar] [CrossRef]

- Nysveen, Herbjørn, Per E. Pedersen, and Helge Thorbjørnsen. 2005. Intentions to Use Mobile Services: Antecedents and Cross-Service Comparisons. Journal of the Academy of Marketing Science 33: 330–46. [Google Scholar] [CrossRef]

- Omodero, Cordelia Onyinyechi. 2021. Fintech Innovation in the Financial Sector: Influence of E-Money Products on a Growing Economy. Studia Universitatis Vasile Goldiş, Arad-Seria Ştiinţe Economice 31: 40–53. [Google Scholar] [CrossRef]

- Ozturkoglu, Omer, Ebru E. Saygılı, and Yucel Ozturkoglu. 2016. A manufacturing-oriented model for evaluating the satisfaction of workers–Evidence from Turkey. International Journal of Industrial Ergonomics 54: 73–82. [Google Scholar] [CrossRef]

- Pazvant, Ece. 2017. Evaluation of the Intention of Using Products with Internet of Things within the Context of Technology Acceptence. Master’s thesis, Duzce University, Duzce, Turkey. [Google Scholar]

- Pikkarainen, Teo, Kari Pikkarainen, Heikki Karjaluoto, and Seppo Pahnila. 2004. Consumer Acceptance of Online Banking: An Extension of the Technology Acceptance Model. Internet Research 14: 224–35. [Google Scholar] [CrossRef] [Green Version]

- Püschel, Júlio, José Afonso Mazzon, and José Mauro C. Hernandez. 2010. Mobile Banking: Proposition of an Integrated Adoption Intention Framework. International Journal of Bank Marketing 28: 389–409. [Google Scholar] [CrossRef] [Green Version]

- Raleting, T., and Jacques Nel. 2011. Determinants of low-income non-users’ attitude towards WIG mobile phone banking: Evidence from South Africa. African Journal of Business Management 5: 212–23. [Google Scholar]

- Riquelme, Hernan E., and Rosa E. Rios. 2010. The Moderating Effect of Gender in the Adoption of Mobile Banking. International Journal of Bank Marketing 28: 328–41. [Google Scholar] [CrossRef]

- Rogers, E. M. 1983. Diffusion of Innovations, 3rd ed. New York: Free Press. [Google Scholar]

- Rogers, E. M. 1995. Diffusion of Innovations, 4th ed. New York: Free Press. [Google Scholar]

- Safeena, Rahmath, Hema Date, Abdullah Kammani, and Nisar Hundewale. 2012. Technology Adoption and Indian Consumers: Study on Mobile Banking. International Journal of Computer Theory and Engineering 4: 1020–24. [Google Scholar] [CrossRef] [Green Version]

- Sahi, Alaa Mahdi, Haliyana Khalid, and Alhamzah Fadhil Abbas. 2021. Digital Payment Adoption: A Review (2015–2020). Journal of Management Information & Decision Sciences 24: 1–9. [Google Scholar]

- Sathye, Milind. 1999. Adoption of Internet Banking by Australian Consumers: An Empirical Investigation. International Journal of Bank Marketing 17: 324–34. [Google Scholar] [CrossRef]

- Saygili, Ebru E., and Tuncay Ercan. 2021. An Overview of International Fintech Instruments Using Innovation Diffusion Theory Adoption Strategies. Innovative Strategies for Implementing FinTech in Banking 3: 46–66. [Google Scholar]

- Schierz, Paul Gerhardt, Oliver Schilke, and Bernd W. Wirtz. 2010. Understanding Consumer Acceptance of Mobile Payment Services: An Empirical Analysis. Electronic Commerce Research and Applications 9: 209–16. [Google Scholar] [CrossRef]

- Shaikh, Aijaz A., and Heikki Karjaluoto. 2015. Mobile Banking Adoption: A Literature Review. Telematics and Informatics 32: 129–42. [Google Scholar] [CrossRef] [Green Version]

- Sheng, Min, Lu Wang, and Yinjun Yu. 2011. An Emprical Model of Individual Mobile Banking Acceptance in China. Paper presented at International Conference on Computational and Information Sciences, Chengdu, China, October 21–23; pp. 434–37. [Google Scholar]

- Sivathanu, Brijesh. 2018. Adoption of digital payment systems in the era of demonetization in India: An empirical study. Journal of Science and Technology Policy Management 10: 143–71. [Google Scholar] [CrossRef]

- Soon, Tan Jin. 2008. QR Code. Synthesis Journal 2008: 59–78. [Google Scholar]

- Statista. 2021. E-Commerce Report 2021. Available online: https://www.statista.com/outlook/dmo/ecommerce/turkey (accessed on 21 February 2022).

- Sulaiman, Ainin, Noor Ismawati Jaafar, and Suhana Mohezar. 2007. An Overview of Mobile Banking Adoption Among the Urban Community. International Journal Mobile Communications 5: 157–68. [Google Scholar] [CrossRef]

- Sumanjeet, Singh. 2009. Emergence of Payment Systems in the Age of Electronic Commerce: The State of Art. Global Journal of International Business Research 2: 17–36. [Google Scholar]

- Tarhini, Ali, Kate Hone, and Xiaohui Liu. 2015. A Cross-Cultural Examination of the Impact of Social, Organisational and Individual Factors on Educational Technology Acceptance between British and Lebanese University Students. British Journal of Educational Technology 46: 739–55. [Google Scholar] [CrossRef] [Green Version]

- Taylor, Shirley, and Peter A. Todd. 1995. A Test of Competing Models. Information Systems Research 6: 144–76. [Google Scholar] [CrossRef]

- Teo, Thompson S. H., Vivien K. G. Lim, and Raye Y. C. Lai. 1999. Intrinsic and Extrinsic Motivation in Internet Usage. Omega International Journal of Management Science 27: 25–37. [Google Scholar] [CrossRef]

- Tobbin, Peter, and J. K. Kuwornu. 2012. Adoption of Mobile Money Transfer Technology: Structural Equation Modeling Approach. European Journal of Business and Management 3: 58–77. [Google Scholar]

- Venkatesh, Viswanath. 2000. Determinants of Perceived Ease of Use: Integrating Control, Intrinsic Motivation, and Emotion into the Technology Acceptance Model. Information Systems Research 11: 342–65. [Google Scholar] [CrossRef] [Green Version]

- Venkatesh, Viswanath, and Fred D. Davis. 1996. A model of the antecedents of perceived ease of use: Development and test. Decision Sciences 27: 451–81. [Google Scholar] [CrossRef]

- Venkatesh, Viswanath, and Fred D. Davis. 2000. A Theoretical Extension of The Technology Acceptance Model: Four Longitudinal Field Studies. Management Science 46: 186–204. [Google Scholar] [CrossRef] [Green Version]

- Venkatesh, Viswanath, and Xiaojun Zhang. 2010. Unified Theory of Acceptance and Use of Technology: US vs. China. Journal of Global Information Technology Management 13: 5–27. [Google Scholar] [CrossRef]

- Venkatesh, Viswanath, Michael G. Morris, Gordon B. Davis, and Fred D. Davis. 2003. User Acceptance of Information Technology: Toward A Unified View. Management Information Systems Research Center, University of Minnesota 27: 425–78. [Google Scholar] [CrossRef] [Green Version]

- Wang, Yi-Shun, Yu-Min Wang, Hsin-Hui Lin, and Tzung-I Tang. 2003. Determinant of User Acceptance of Internet Banking: An Empirical Study. International Journal of Service Industry Management 14: 501–20. [Google Scholar] [CrossRef]

- We Are Social. 2022. Digital 2022: Another Year of Bumper Growth. Available online: https://wearesocial.com/uk/blog/2022/01/digital-2022-another-year-of-bumper-growth-2/ (accessed on 3 May 2022).

- Wessels, Lisa, and Judy Drennan. 2010. An Investigation of Consumer Acceptance of M-Banking. Faculty of Business, Queensland University of Technology, Brisbane, Australia 28: 547–68. [Google Scholar] [CrossRef]

- Yan, Hong, and Zhonghua Yang. 2015. Examining Mobile Payment User Adoption from the Perspective of Trust. International Journal of u- and Virtual e- Service Science and Technology 8: 117–30. [Google Scholar]

- Yu, Chian-Son. 2012. Factors Affecting Individuals to Adopt Mobile Banking: Empirical Evidence from the UTAUT Model. Journal of Electronic Commerce Research 13: 104–21. [Google Scholar]

- Zheng, Juan, and Shan Li. 2020. What Drives Students’ Intention to Use Tablet Computers: An Extended Technology Acceptance Model. International Journal of Educational Research 102: 101612. [Google Scholar] [CrossRef]

- Zhou, Tao. 2012. Examining Mobile Banking User Adoption from the Perspectives of Trust and Flow Experience. Information Technology Management 13: 27–37. [Google Scholar] [CrossRef]

| Instrument | Definition | Advantages |

|---|---|---|

| Near Field Communication (NFC) | A wireless application that enables close-range communication between electronic devices as an extension of radio frequency identification technology. The devices are brought closer together via NFC technology, and the transaction takes place at a 10 cm range and without contact (Husni et al. 2011). | It provides easy and secure communication between two electronic devices. During the NFC payment process, any NFC-enabled account must be chosen and the phone read by the contactless POS equipment. |

| Quick Response Code (QR) | A new generation two-dimensional barcode type, designed for usage in the Japanese automotive industry. The QR code can contain any type of data, including text, a website address, or a video link. (Soon 2008). | The QR Code reader software can quickly and easily read a QR Code from a mobile phone and open the corresponding product or service page. It simplifies the payment process and enables payment across a broad network of access points by being produced via channels such as POS, ATM and a web page. |

| Digital Wallet | A software program that is used to store and transmit payment authorization data for one or more credit or deposit accounts (Levitin 2017). By uploading the payment account information to the digital wallet, the consumer can use the wallet as a payment device. | The user contacts the bank via a digital wallet and is granted the authority to approve the transaction. The bank is responsible for implementing the required security measures to ensure a smooth transaction procedure. |

| Biometric Payment | Payments made by consumers using a unique feature such as their fingerprint, eye, or voice to validate their identification during payment transactions. | With the use of digital payments, concerns about the confidentiality and security of consumer payment transactions arose, and consumers requested that transactions be terminated with two-factor verification, which involves performing a personal verification in addition to the transaction password (Kumar and Ryu 2009). |

| Blockchain | Blockchain technology was created as distributed ledgers for bitcoin (Du et al. 2018). Blockchain technology is being used in the financial sector for the following purposes: payment transactions, transfer transactions, purchase-sale platforms, authorization, digital identity management, and document management. | The absence of authority and intermediary systems cuts costs while also speeding up transaction activities. The use of several points of control operations reduces the likelihood of system fraud (Saygili and Ercan 2021). |

| Factor | Definition | Previous Studies |

|---|---|---|

| Perceived Ease of Use (PEU) TAM | The degree to which one believes it would be simple to use a specific system is referred to as perceived ease of use. Consumers are more inclined to adopt an application that is simpler to use than another (Davis 1989). | (Davis et al. 1989; Venkatesh 2000; Venkatesh and Davis 2000; Safeena et al. 2012; Hanafizadeh et al. 2014; Chuang et al. 2016; Kim et al. 2016; Tobbin and Kuwornu 2012). |

| Perceived Usefulness (PU) TAM | The degree to which an individual believes that utilizing a particular system will improve his or her job performance (Davis 1989). Perceived usefulness refers to the opportunities provided by mobile banking and whether it is advantageous to conduct financial transactions using a mobile phone (Aldás-Manzano et al. 2009). | (Davis 1989; Guriting and Ndubisi 2006; Riquelme and Rios 2010; Amin et al. 2008; Aldás-Manzano et al. 2009; Kazi and Mannan 2013; AlSoufi and Ali 2014; Hanafizadeh et al. 2014). |

| Perceived Trust (PT) E-TAM | PT is the anticipation that when one chooses to trust others, they will not behave opportunistically by taking advantage of the situation (Gefen et al. 2003). Trust reduces fraud, uncertainty, and potential threats, hence minimizing these worries and promoting e-commerce and e-payment transactions. | (Kurnia et al. 2007; Kim and Prabhakar 2004; Hanafizadeh et al. 2014; Mallat 2007; Tobbin and Kuwornu 2012) |

| Perceived Risk (PR) E-TAM | PR is a belief in the potential uncertainty of customers’ mobile money transactions (Tobbin and Kuwornu 2012). | (Akturan and Tezcan 2012; Tobbin and Kuwornu 2012; Hanafizadeh et al. 2014). |

| Self-Efficacy (SE) E-TAM | An individual’s assessment of his or her ability to use digital payment. It is a metric to assess one’s capacity to use digital payments. | (Luarn and Lin 2005; Gu et al. 2009). |

| Social Influence (SI) UTAUT | Customers’, friends’, family members’ and other consumers’ perceptions of technology use can be defined as social influence. (Venkatesh et al. 2003). | (Venkatesh et al. 2003; Venkatesh and Zhang 2010; Tarhini et al. 2015; Sivathanu 2018). |

| Perceived Credibility (PCR) E-TAM | PC is the degree to which an individual feels that using mobile banking will create no security or privacy risks (Wang et al. 2003). | (Luarn and Lin 2005; Hanafizadeh et al. 2014). |

| Compatibility (CMPA) IDT | The degree to which an innovation is judged to be consistent with present values, prior experience and potential customers’ demands (Rogers 1995). Kleijnen et al. (2004) defined CMPA in the context of mobile banking as the degree to which a product or service is compatible with the consumer’s lifestyle and current needs. | (Rogers 1995; Kleijnen et al. 2004; Wessels and Drennan 2010; Khraim et al. 2011; Sheng et al. 2011; Hanafizadeh et al. 2014; Lin 2011). |

| Relative Advantage (RA) IDT | RA is the extent to which an innovation is judged to be superior to the idea it replaces. Although economic advantage can be measured, social-prestige elements, convenience and satisfaction are frequently key components. What matters is whether an individual views the invention as beneficial (Rogers 1995). | (Rogers 1995; Taylor and Todd 1995; Püschel et al. 2010; Lin 2011). |

| Health and Epidemic Effects (HE) | The pandemic impacts of e-commerce and e-payments where physical contact is avoided. Long-term quarantines, prohibitions, and limits are imposed due to health and epidemic issues affect mobile payments. | (Acemoğlu and Johnson 2007; Dmour et al. 2021; Jiang et al. 2021). |

| Complexity (COMPE) IDT | Complexity is the degree to which an innovation is thought to be difficult to utilize (Rogers 1983). Taylor and Todd (1995) describe it as the degree to which an innovation is perceived to be relatively difficult to comprehend and use. | (Rogers 1983; Taylor and Todd 1995; Khraim et al. 2011). |

| Quality of Internet Connection (QIC) E-TAM | The quality of the internet connection allows users to complete their transactions quickly and easily. | (Sathye 1999; Al-Somali et al. 2009). |

| Ubiquity (UB) E-TAM | Ubiquity is defined as users’ ability to access mobile banking from anywhere at any time using mobile terminals and networks (Zhou 2012). This enables users to trade from any location. However, it will necessitate additional resources and effort on the part of service providers. | (Zhou 2012; Yan and Yang 2015). |

| Perceived Enjoyment (PE) E-TAM | Perceived enjoyment is the degree to which technology use is regarded as a pleasurable activity in the absence of other factors. | (Nysveen et al. 2005; Teo et al. 1999). |

| Personal Innovativeness (PIN) E-TAM | Personal innovativeness is defined as a willingness to experiment with new technology (Agarwal and Karahanna 2000). | (Agarwal and Karahanna 2000; Zhou 2012). |

| Perceived Integrity (PI) E-TAM | The commitment to principles in the mutually occurring process is referred to as perceived integrity. This component includes the concept of honesty, which instills trust in those who are trusted and increases compliance by minimizing uncertainty (Bhattacherjee 2000). | (Bhattacherjee 2000; Lin 2011) |

| Facilitating Conditions (FC) UTAUT | Facilitating conditions indicate that users have access to the resources required to engage in any behavior (Taylor and Todd 1995). | (Taylor and Todd 1995; Raleting and Nel 2011; Crabbe et al. 2009; Sivathanu 2018). |

| Perceived Cost (PC) E-TAM | Cost is defined by Luarn and Lin (2005) as the degree to which “a person believes that using m-banking will cost money”. | (Sathye 1999; Kleijnen et al. 2004; Luarn and Lin 2005). |

| Authors–Theory | Aim (To Identify the Determinants of) | Sample (No. of Participants/Country) | Methodology | Independent Variables | Findings |

|---|---|---|---|---|---|

| Raleting and Nel (2011) E-TAM; UTAUT | Attitude towards mobile phone banking | 465/South Africa | Confirmatory factor analysis (CFA) | PU, PEU, SE, FC, PR, PC | PEU and PU influence attitude |

| Bankole et al. (2011) UTAUT | Mobile banking adoption | 231/Nigeria | Regression Analysis | PT, Utility Expectancy, Effort Expectancy (EE), Utility Expectancy, Social Factors, Power Distance, Convenience and Cost | Utility Expectancy, effort expectancy and power distance have an impact on BI |

| Sheng et al. (2011) TAM and IDT | Acceptance of individual mobile banking | 278/China | Exploratory Factor Analysis (EFA) and Regression Analysis | PU, PEU, CMPA, Triability, PR | PU, PEU, CMPA and PR influence BI |

| Tobbin and Kuwornu (2012) E-TAM and IDT | Acceptance of mobile money transfer | 298/Ghana | Structural equation modeling (SEM) | PU, PEU, PT, PR, RA, Triability, Transactional Cost, Perceived Privacy | PEU, PU, PR and PT affect BI |

| Hanafizadeh et al. (2014) E-TAM | Mobile banking adoption by bank clients | 361/Iran | SEM | PU, PEU, need for personal interaction, PR, PC, CMPA, PT, PCR, | All of the independent variables affect behavioral intention |

| Cao (2016) TAM, UTAUT, Motivational Model and Adoption of Risky Technologies | Acceptance of all-in-one payment method | 117/Finland | EFA, CFA, SEM | PEU, PU, PE, PIN, SI, Need for Minimalism, Price Value, Security Concerns, Perceived Information | PU, Price Value, SI, PIN, Security Concerns, PE, Perceived Information affect BI |

| Abdullah et al. (2018) UTAUT | Adoption of fintech in mutual fund/unit trust investment | 203/Malaysia | EFA and Regression Analysis | SI, Performance Expectancy, EE, FC, Perceived Credibility | Performance Expectancy, EE and SI have an impact on BI |

| Gender | % | Education of Participants | % | Current Job Participants | % |

|---|---|---|---|---|---|

| Male | 42.7 | High school | 4.9 | Public Sector | 24.8 |

| Female | 57.3 | University | 65.4 | Private Sector | 36.6 |

| Graduate school | 29.7 | Self Employed | 7.8 | ||

| Student | 27.4 | ||||

| Retired | 3.5 | ||||

| Age of Participants | % | Income of Participants | % | Frequency of Card Payments of Participants | % |

| 18–25 years | 30.5 | 0–3.000 TL | 29.6 | Less than once a week | 37.1 |

| 26–35 years | 16.7 | 3.001–6.000 TL | 18.8 | At least once a week | 27.2 |

| 36–45 years | 42.4 | 6.001–9.000 TL | 15.7 | 2–3 times a week | 18.5 |

| 46–55 years | 6.9 | 9.001–12.000 TL | 11.3 | 4–5 times a week | 7.3 |

| 56–65 years | 3.5 | 12.001–15.000 TL | 7.5 | More than 5 per week | 9.6 |

| 15.000 TL and above | 17.1 | More than 5 per month | 0.3 |

| Kaiser–Meyer–Olkin Measure of Sampling Adequacy. | 0.911 | |

| Approx. Chi-Square | 17,136.359 | |

| Bartlett’s Test of Sphericity | df | 2556 |

| Sig. | 0.000 | |

| Factors | Items | Item Description | Cronbach Alpha Value (α) |

|---|---|---|---|

| 1. Relative advantage (RA) | CMPA1 | Customer lifestyle | 0.959 |

| CMPA2 | Payment management | ||

| CMPA3 | Way of working | ||

| RA1 | Access facility | ||

| RA2 | Fast transactions | ||

| RA3 | Benefit of adoption | ||

| HEI1 | Delay of transactions | ||

| HEI2 | Current customer transactions | ||

| HEI5 | Continuity of customer transactions | ||

| QIC1 | Access to the internet | ||

| QIC2 | Benefits of internet access | ||

| QIC3 | Efficiency of internet access | ||

| PE2 | Feeling positive | ||

| PE4 | To feel wise | ||

| FC1 | Have the necessary resources | ||

| FC2 | Have the necessary information | ||

| FC3 | Compatible with lifestyle | ||

| FC4 | Ease of access to help | ||

| UB1 | Transactions from anywhere | ||

| UB2 | Transactions whenever the customer wants | ||

| UB3 | Transactions online anytime, anywhere. | ||

| 2. Perceived trust (PT) | PT1 | Transaction security | 0.906 |

| PT2 | Information security | ||

| PT3 | Information privacy | ||

| PT4 | Trust privacy | ||

| PT5 | Feeling of trust | ||

| PCR1 | Believe in personal information’s privacy | ||

| PCR2 | Believe in the transaction processes | ||

| PCR3 | Believe in the confidentiality of information sharing | ||

| 3. Perceived risk (PR) | PR1 | Transaction risk | 0.878 |

| PR2 | System risk | ||

| PR3 | Payment risk | ||

| PR4 | Security risk | ||

| PR5 | Financial risk | ||

| PR6 | Security risk | ||

| 4. Perceived usefulness (PU) | PU1 | Productivity, efficiency and performance increase | |

| PU2 | Saving of time and labor saving | 0.867 | |

| PU3 | Gain control over transactions | ||

| PU4 | Usefulness of transactions | ||

| PU5 | Useful transactions | ||

| 5. Personal innovativeness (PI) | PIN1 | Giving advice about new products and innovations | 0.785 |

| PIN2 | Buying new and different things | ||

| PIN3 | Testing new products | ||

| PIN4 | Keeping up with technological advances | ||

| 6. Complexity (COMPE) | PC3 | Financial barriers | 0.755 |

| COMPE1 | Customers’ mental effort | ||

| COMPE2 | Customers’ technical skills | ||

| COMPE3 | Frustration of online payments | ||

| 7. Perceived integrity (PI) | PI1 | Honesty | 0.887 |

| PI2 | Fulfilling commitment | ||

| PI3 | Unbiased information about the transactions | ||

| 8. Perceived ease of use (PEU) | PEU1 | Easy payments | 0.786 |

| PEU3 | Easy to perform | ||

| PEU4 | Easy to complete | ||

| 9. Social influence (SI) | SI1 | Suggestions from friends/family members/mass media | 0.503 |

| SI2 | Many people who have an important place in my life | ||

| SI5 | Status in society | ||

| 10. Self-efficacy (SE) | SE2 | Directions in the system | 0.515 |

| SE3 | Tried by someone else | ||

| 11. Health and epidemic effects (HE) | HE3 | Increasing of payment transactions | 0.584 |

| HE4 | Perception of my online payment transactions. |

| Least Squares Estimations | ||||

|---|---|---|---|---|

| Dependent Variable: ATTITUDE | Dependent Variable: BI | |||

| Model A1 | Model A2 | Model B1 | Model B2 | |

| Constant | −0.046389 | −0.041862 | −0.093456 | −0.060632 |

| (0.2958) | (0.3367) | (0.0716) | (0.1662) | |

| RA | 0.632394 *** | 0.633335 *** | 0.563767 *** | 0.210851 *** |

| (0.0000) | (0.0000) | (0.0000) | (0.0021) | |

| PT | 0.21437 *** | 0.212892 *** | 0.165903 *** | 0.044416 |

| (0.0000) | (0.0000) | (0.0000) | (0.2493) | |

| PR | −0.103106 *** | −0.106335 *** | −0.095877 *** | −0.034668 |

| (0.0052) | (0.0032) | (0.0073) | (0.3057) | |

| PU | 0.276212 *** | 0.276271 *** | 0.279803 *** | 0.128394 *** |

| (0.0000) | (0.0000) | (0.0000) | (0.0086) | |

| PI | 0.259707 *** | 0.259304 *** | 0.318178 *** | 0.170387 *** |

| (0.0000) | (0.0000) | (0.0000) | (0.0000) | |

| COMPE | −0.03926 | −0.058463 * | −0.040417 | |

| (0.3023) | (0.1009) | (0.2254) | ||

| PI | 0.163167 *** | 0.162509 *** | 0.186166 *** | 0.097349 *** |

| (0.0000) | (0.0000) | (0.0000) | (0.0101) | |

| PEU | 0.064403 * | 0.064669 * | 0.104433 *** | 0.068636 ** |

| (0.0634) | (0.0591) | (0.0013) | (0.0221) | |

| SI | 0.163175 *** | 0.16486 *** | 0.188692 *** | 0.09493 ** |

| (0.0000) | (0.0000) | (0.0000) | (0.0272) | |

| SE | 0.222056 *** | 0.222435 *** | 0.20402 *** | 0.0801 * |

| (0.0000) | (0.0000) | (0.0000) | (0.0614) | |

| HE | 0.074867 ** | 0.073289 * | 0.06818 * | 0.022918 |

| (0.0484) | (0.0524) | (0.0737) | (0.5385) | |

| D_MALE1 | 0.15345 | 0.137926 | 0.169284 * | 0.074832 |

| (0.0369) | (0.0493) | (0.0547) | (0.3385) | |

| ATTITUDE | 0.558413 *** | |||

| (0.0000) | ||||

| N. of Obs. | 288 | 288 | 289 | 286 |

| R-squared | 0.716997 | 0.715593 | 0.619945 | 0.701073 |

| Adjusted R-squared | 0.704648 | 0.704258 | 0.603421 | 0.686786 |

| F-statistic | 58.06017 | 63.13088 | 37.51758 | 49.07074 |

| Prob(F-statistic) | 0 | 0 | 0 | 0 |

| Ordered Logit Estimations | |||

|---|---|---|---|

| Dependent Variable: ACTUALUSAGE | |||

| Model C1 | Model C2 | Model C3 | |

| BI | 0.049328 | 0.576741 | |

| (0.7618) | (0.0000) | ||

| RA | 0.4073 *** | 0.42729 *** | |

| (0.0110) | (0.0018) | ||

| PR | −0.321918 *** | −0.32925 *** | |

| (0.0110) | (0.0086) | ||

| PU | 0.417511 *** | 0.43161 *** | |

| (0.0034) | (0.0012) | ||

| PI | 0.320476 ** | 0.34175 *** | |

| (0.0182) | (0.0064) | ||

| COMPE | −0.233469 * | −0.2457 ** | |

| (0.0519) | (0.0397) | ||

| PI | 0.227614 * | 0.24048 ** | |

| (0.0608) | (0.0423) | ||

| PEU | 0.435921 *** | 0.44627 *** | |

| (0.0036) | (0.0027) | ||

| HE | 0.238215 ** | 0.23238 ** | |

| (0.0388) | (0.0426) | ||

| AGE | −0.654177 *** | −0.65566 *** | −0.540183 *** |

| (0.0000) | (0.0000) | (0.0000) | |

| INCOME | 0.38169 *** | 0.38345 *** | 0.401535 *** |

| (0.0000) | (0.0000) | (0.0000) | |

| PRIEMP | 0.519441 ** | 0.53488 ** | 0.41621 * |

| (0.0464) | (0.0391) | (0.0784) | |

| SELFEMP | 1.703099 *** | 1.73085 *** | 1.421923 *** |

| (0.0001) | (0.0001) | (0.0003) | |

| N. of Obs. | 289 | 291 | 327 |

| Pseudo R-squared | 0.126206 | 0.1264 | 0.090298 |

| LR statistic | 104.6538 | 105.383 | 85.80175 |

| Prob(LR statistic) | 0 | 0 | 0 |

| Dependent Variables | ||||||

|---|---|---|---|---|---|---|

| Independent Variables | Attitude (Models A1, A2) | Behavioral Intention (Model B1) | Behavioral Intention (Model B2) | Actual Usage (Model C1) | Actual Usage (Model C2) | Actual Usage (Model C3) |

| Relative advantage (RA) | (+) | (+) | (+) | (+) | (+) | |

| Perceived trust (PT) | (+) | (+) | ||||

| Perceived risk (PR) | (−) | (−) | (−) | (−) | ||

| Perceived usefulness (PU) | (+) | (+) | (+) | (+) | (+) | |

| Personal innovativeness (PI) | (+) | (+) | (+) | (+) | (+) | |

| Complexity (COMPE) | (−) | (−) | ||||

| Perceived integrity (PI) | (+) | (+) | (+) | (+) | (+) | |

| Perceived ease of use (PEU) | (+) | (+) | (+) | (+) | (+) | |

| Social influence (SI) | (+) | (+) | (+) | |||

| Self-efficacy (SE) | (+) | (+) | (+) | |||

| Health and epidemic effects (HE) | (+) | (+) | (+) | (+) | ||

| Gender—male | (+) | (+) | ||||

| Income | (+) | (+) | (+) | |||

| Age | (−) | (−) | (−) | |||

| Private sector employment | (+) | (+) | (+) | |||

| Self-employment | (+) | (+) | (+) | |||

| Attitude | (+) | |||||

| Behavioral intention | (+) | |||||

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2022 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Coskun, M.; Saygili, E.; Karahan, M.O. Exploring Online Payment System Adoption Factors in the Age of COVID-19—Evidence from the Turkish Banking Industry. Int. J. Financial Stud. 2022, 10, 39. https://doi.org/10.3390/ijfs10020039

Coskun M, Saygili E, Karahan MO. Exploring Online Payment System Adoption Factors in the Age of COVID-19—Evidence from the Turkish Banking Industry. International Journal of Financial Studies. 2022; 10(2):39. https://doi.org/10.3390/ijfs10020039

Chicago/Turabian StyleCoskun, Melih, Ebru Saygili, and Mehmet Oguz Karahan. 2022. "Exploring Online Payment System Adoption Factors in the Age of COVID-19—Evidence from the Turkish Banking Industry" International Journal of Financial Studies 10, no. 2: 39. https://doi.org/10.3390/ijfs10020039

APA StyleCoskun, M., Saygili, E., & Karahan, M. O. (2022). Exploring Online Payment System Adoption Factors in the Age of COVID-19—Evidence from the Turkish Banking Industry. International Journal of Financial Studies, 10(2), 39. https://doi.org/10.3390/ijfs10020039