Market Manipulation around Seasoned Equity Offerings: Evidence Prior to the Global Financial Crisis of 2007–2009

Abstract

:1. Introduction

2. Literature Review

3. The Model

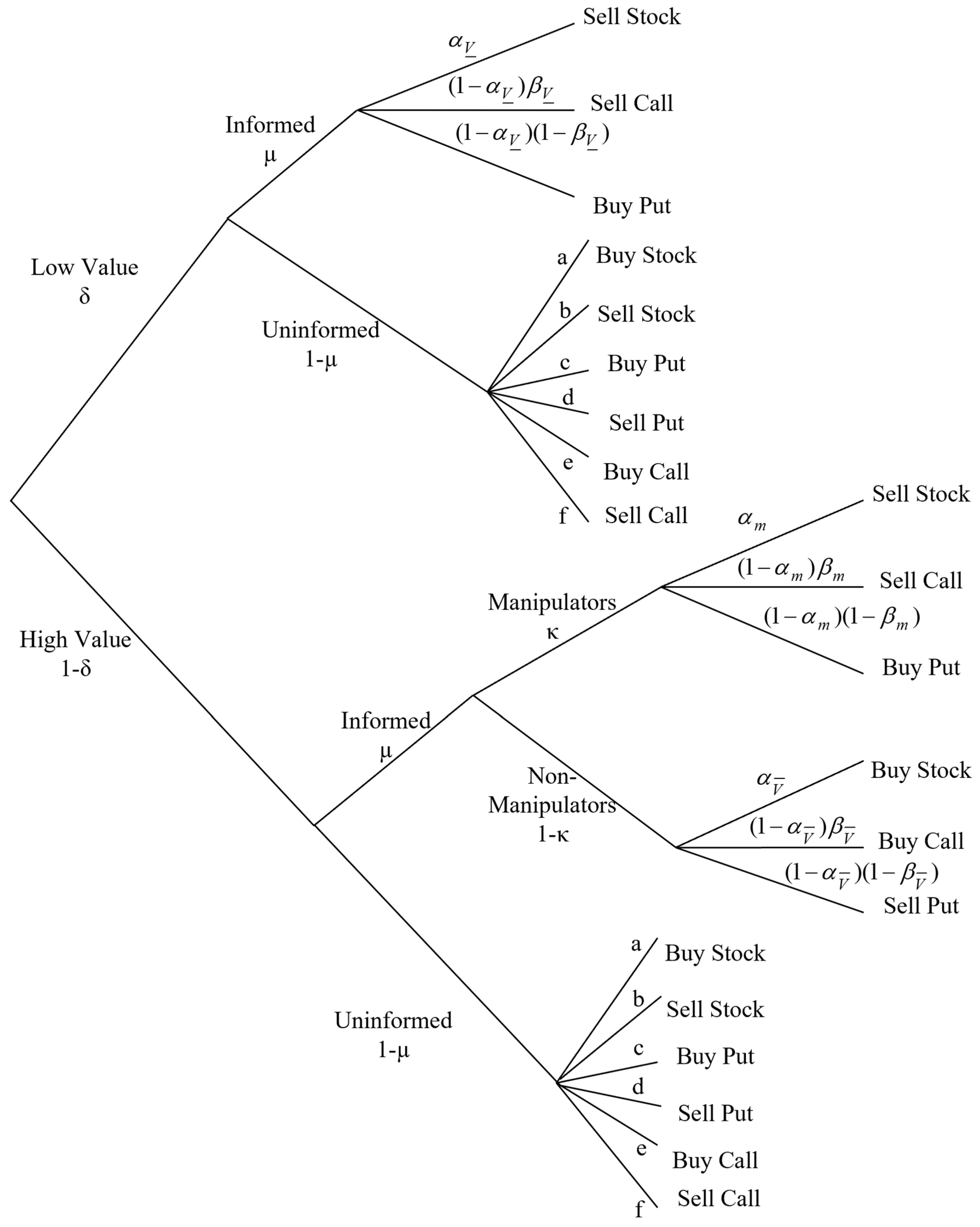

3.1. Market Participants

3.2. Market Transactions, Market Makers’ Rational Expectations, and Manipulators’ Trading Strategies

3.3. Equilibrium Prices in the Options and Equity Markets in the Presence of Manipulators

3.4. The Profits and Losses of Informed Traders

3.4.1. Profits of Informed Traders with Unfavorable Information

3.4.2. Profits of Non-Manipulative Informed Traders with Favorable Information

3.4.3. Losses of Manipulators in the Secondary Markets

3.5. The Trading Strategies of Different Types of Traders

3.5.1. Trading Strategies of Informed Traders

- (a)

- (b)

- (c)

- (d)

- (e)

3.5.2. The Trading Strategies of Uninformed Traders

3.6. Mechanism of Distorting Stock Prices and Rational Anticipation of the Market Makers

3.6.1. Manipulative Behavior in the Absence of Market Makers’ Anticipation

3.6.2. Manipulative Trading with the Presence of Market Makers’ Anticipation

3.7. Short Sales Constraints and SEO Pre-Offer Market

3.7.1. Short Sales Constraints and Bid–Ask Spreads in Each Market

3.7.2. Short Sales Constraints and Venues of Informed Trading

- (a)

- (b)

- (c)

- (d)

3.7.3. Short Sales Constraints and Manipulative Conduct

Short Sales Constraints and Cost of Manipulation

Short Sales Constraints and Market Makers’ Adjustments of Estimations

4. Data

5. Empirical Results

5.1. Volume, Open Interest, and Spread for Calls, Puts around SEO Pricing

5.2. Change in Put–Call Ratio Prior to SEO Pricing

5.3. Trading Activities upon Existence of Different Kinds of Information

5.4. Change in Open Interest and Change in Bid–Ask Spread

5.5. Change in Open Interest and 5-Day Pre-Offer CAR

5.6. Pre-Offer CAR and Post-Offer CAR

6. Conclusions

Author Contributions

Funding

Data Availability Statement

Conflicts of Interest

| 1 | Rule 10b-21 was replaced by Rule 105, Reg M, in 1997, which is essentially similar to Rule 10b-21, but limits the restrictions on short selling to five trading days before the SEO’s issue date. |

| 2 | To better understand the use of the event study approach in finance, readers are invited to refer to Boubaker et al. (2014, 2015), among others. |

| 3 | Compared with the pre-scheduled information event (earnings announcements, for example), takeover announcements may contain more superior private information due to the lack of analyst forecasts on takeovers. |

| 4 | The equilibrium condition can be obtained using Bayes’ theorem. We thank an anonymous referee for pointing this out. |

| 5 | http://www.deltaneutral.com/ (accessed on 19 June 2007). |

| 6 | In other words, endogeneity is a serious issue that may affect the results of the paper and should be interpreted with care. |

| 7 | The changes defined by Equations (23)–(25) are equivalent to continuously compounded percentage changes. For example, Equation (23) can be re-written as follows.

|

| 8 | Due to the existence of trading days with no or fewer calls or puts transactions, there are a lot of missing values or outliers in the data on the put–call ratio of the trading volume. This may bring bias to our results. |

| 9 | Cao et al. (2005) document that the average put–call ratio of the trading volume decreases by 22.8% in the pre-takeover-announcement period. In Amin and Lee’s (1997) study on options market around an earnings announcement, they report that during the three trading days before an announcement, the abnormal trading volume in the calls market is all significant at the 5% level, while only on day −2 is the abnormal puts volume significant at the 5% level. |

References

- Aggarwal, Rajesh K., and Guojun Wu. 2006. Stock Market Manipulations. The Journal of Business 79: 1915–53. [Google Scholar] [CrossRef]

- Amin, Kaushik I., and Charles MC Lee. 1997. Option Trading, Price Discovery, and Earnings News Dissemination. Contemporary Accounting Research 14: 153–92. [Google Scholar] [CrossRef]

- Boubaker, Sabri, Alexis Cellier, and Wael Rouatbi. 2014. The Sources of Shareholder Wealth Gains from Going Private Transactions: The Role of Controlling Shareholders. Journal of Banking and Finance 43: 226–46. [Google Scholar] [CrossRef]

- Boubaker, Sabri, Hisham Farag, and Duc Khuong Nguyen. 2015. Short-term Overreaction to Specific Events: Evidence from an Emerging Market. Research in International Business and Finance 35: 153–65. [Google Scholar] [CrossRef]

- Cao, Charles, Zhiwu Chen, and John M. Griffin. 2005. Informational Content of Option Volume Prior to Takeovers. The Journal of Business 78: 1073–109. [Google Scholar] [CrossRef] [Green Version]

- Chan, Kalok, Y. Peter Chung, and Wai-Ming Fong. 2002. The Information Role of Stock and Option Volume. Review of Financial Studies 15: 1049–75. [Google Scholar] [CrossRef]

- Corwin, Shane A. 2003. The Determinants of Underpricing for Seasoned Equity Offers. Journal of Finance 58: 2249–79. [Google Scholar] [CrossRef]

- Cumming, Douglas, Shan Ji, Rejo Peter, and Monika Tarsalewska. 2020. Market Manipulation and Innovation. Journal of Banking & Finance 120: 105957. [Google Scholar]

- Danielsen, Bartley R., and Sorin M. Sorescu. 2001. Why Do Option Introductions Depress Stock Prices? A Study of Diminishing Short Sale Constraints. Journal of Financial and Quantitative Analysis 36: 451–84. [Google Scholar] [CrossRef]

- Diamond, Douglas W., and Robert E. Verrecchia. 1987. Constraints on Short-Selling and Asset Price Adjustment to Private Information. Journal of Financial Economics 18: 277–311. [Google Scholar] [CrossRef]

- Easley, David, Maureen O’hara, and Pulle Subrahmanya Srinivas. 1998. Option Volume and Stock Prices: Evidence on Where Informed Traders Trade. Journal of Finance 63: 431–65. [Google Scholar] [CrossRef]

- Gerard, Bruno, and Vikram Nanda. 1993. Trading and Manipulation Around Seasoned Equity Offerings. The Journal of Finance 48: 213–45. [Google Scholar] [CrossRef]

- Griffin, John M., and Amin Shams. 2018. Manipulation in the VIX? The Review of Financial Studies 31: 1377–417. [Google Scholar] [CrossRef]

- Horst, Ulrich, and Felix Naujokat. 2011. On Derivatives with Illiquid Underlying and Market Manipulation. Quantitative Finance 11: 1051–66. [Google Scholar] [CrossRef]

- Jarrow, Robert A. 1994. Derivative Security Markets, Market Manipulation, and Option Pricing Theory. Journal of Financial and Quantitative Analysis 29: 241–61. [Google Scholar] [CrossRef]

- Jarrow, Robert, Scott Fung, and Shih-Chuan Tsai. 2018. An Empirical Investigation of Large Trader Market Manipulation in Derivatives Markets. Review of Derivatives Research 21: 331–74. [Google Scholar] [CrossRef]

- Kim, Kenneth A., and Hyun-Han Shin. 2004. The Puzzling Increase in the Underpricing of Seasoned Equity Offerings. Financial Review 39: 343–65. [Google Scholar] [CrossRef]

- Kumar, Praveen, and Duane J. Seppi. 1992. Futures Manipulation with Cash Settlement. Journal of Finance 47: 1485–502. [Google Scholar]

- Mayhew, Stewart, Atulya Sarin, and Kuldeep Shastri. 1995. The Allocation of Informed Trading Across Related Markets: An Analysis of the Impact of Changes in Equity-Option Margin Requirements. Journal of Finance 50: 1635–53. [Google Scholar] [CrossRef]

- Mei, Jianping, Guojun Wu, and Chunsheng Zhou. 2004. Behavior Based Manipulation: Theory and Prosecution Evidence. Available online: https://ssrn.com/abstract=457880 (accessed on 3 May 2022).

- Nyström, Kaj, and Mikko Parviainen. 2017. Tug-Of-War, Market Manipulation, and Option Pricing. Mathematical Finance 27: 279–312. [Google Scholar] [CrossRef] [Green Version]

- Ofek, Eli, Matthew Richardson, and Robert F. Whitelaw. 2004. Limited Arbitrage and Short Sales Restrictions: Evidence from the Options Markets. Journal of Financial Economics 74: 305–42. [Google Scholar] [CrossRef] [Green Version]

- Safieddine, Assem, and William J. Wilhelm. 1996. An Empirical Investigation of Short-Selling Activity Prior to Seasoned Equity Offerings. The Journal of Finance 51: 729–49. [Google Scholar] [CrossRef]

{kind=link}

| Increase | Decrease | |

| No change | No change | |

| Bid–ask spread in the stock market | Decrease | Increase |

| Decrease | Increase | |

| No change | No change | |

| Bid–ask spread in the call market | Increase | Decrease |

| No change | No change | |

| Increase | Decrease | |

| Bid–ask spread in the put market | Increase | Decrease |

| Panel A: Calls | ||||||||

| Day | Volume | Open Interest | Spread | Call/Stock (Volume) | ||||

| Level | Change | Level | Change | Level | Change | Level | Change | |

| −5 | 724.26 | 0.3778 *** | 23,340.38 | 0.0749 *** | 0.1643 | −0.0196 | 0.0334 | 0.1725 ** |

| (0.0000) | (0.0098) | (0.5064) | (0.0293) | |||||

| −4 | 747.78 | 0.2532 *** | 23,720.24 | 0.0574 * | 0.1634 | −0.0258 | 0.0305 | 0.0626 |

| (0.0026) | (0.0601) | (0.4186) | (0.4142) | |||||

| −3 | 585.76 | 0.3220 *** | 20,775.27 | 0.0564 * | 0.1633 | −0.0009 | 0.0294 | 0.0873 |

| (0.0001) | (0.0528) | (0.9783) | (0.2647) | |||||

| −2 | 795.01 | 0.4099 *** | 22,955.15 | 0.0458 | 0.1635 | −0.0158 | 0.0353 | 0.1460 * |

| (0.0000) | (0.1091) | (0.6217) | (0.0666) | |||||

| −1 | 1124.57 | 0.5335 *** | 22,397.54 | 0.0508 * | 0.1618 | −0.0025 | 0.0510 | −0.0143 |

| (0.0000) | (0.0813) | (0.9445) | (0.8592) | |||||

| 0 | 1532.21 | 1.2263 *** | 23,131.71 | 0.0794 *** | 0.1687 | 0.0298 | 0.0191 | −0.306 *** |

| (0.0000) | (0.0038) | (0.3998) | (0.0002) | |||||

| 1 | 1063.74 | 0.8102 *** | 23,507.88 | 0.1566 *** | 0.1712 | 0.0302 | 0.0228 | −0.0937 |

| (0.0000) | (0.0000) | (0.4108) | (0.2481) | |||||

| 2 | 915.78 | 0.4921 *** | 23,877.86 | 0.1945 *** | 0.1615 | 0.0022 | 0.0280 | 0.0071 |

| (0.0000) | (0.0000) | (0.9501) | (0.9293) | |||||

| 3 | 848.44 | 0.4220 *** | 23,110.39 | 0.2012 *** | 0.1724 | 0.0419 | 0.0277 | 0.0143 |

| (0.0000) | (0.0000) | (0.2804) | (0.8553) | |||||

| 4 | 576.92 | 0.3150 *** | 23,153.83 | 0.2075 *** | 0.1683 | 0.0261 | 0.0230 | −0.0416 |

| (0.0006) | (0.0000) | (0.4908) | (0.6047) | |||||

| 5 | 746.23 | 0.2779 *** | 23,187.22 | 0.2291 *** | 0.1756 | 0.0329 | 0.0297 | −0.0397 |

| (0.0051) | (0.0000) | (0.4220) | (0.6540) | |||||

| Panel B: Puts. | ||||||||

| Day | Volume | Open Interest | Spread | Put/Stock (Volume) | ||||

| Level | Change | Level | Change | Level | Change | Level | Change | |

| −5 | 470.23 | 0.2795 *** | 20,764.37 | 0.0868 ** | 0.2283 | −0.0116 | 0.0218 | 0.1690 ** |

| (0.0008) | (0.0129) | (0.7175) | (0.0262) | |||||

| −4 | 674.90 | 0.2887 *** | 21,142.41 | 0.0885 *** | 0.2321 | −0.0125 | 0.0244 | 0.1751 ** |

| (0.0020) | (0.0098) | (0.7185) | (0.0443) | |||||

| −3 | 686.08 | 0.4497 *** | 19,151.21 | 0.0866 ** | 0.2278 | −0.0204 | 0.0277 | 0.2829 *** |

| (0.0000) | (0.0141) | (0.5288) | (0.0007) | |||||

| −2 | 710.71 | 0.3569 *** | 20,631.73 | 0.0998 *** | 0.2267 | −0.0236 | 0.0290 | 0.1864 ** |

| (0.0001) | (0.0069) | (0.4819) | (0.0276) | |||||

| −1 | 717.73 | 0.3904 *** | 20,313.36 | 0.1140 *** | 0.2115 | −0.100 *** | 0.0223 | 0.0687 |

| (0.0001) | (0.0039) | (0.0058) | (0.4316) | |||||

| 0 | 1109.95 | 0.7084 *** | 21,153.74 | 0.1429 *** | 0.1979 | −0.120 *** | 0.0131 | −0.280 *** |

| (0.0000) | (0.0004) | (0.0016) | (0.0006) | |||||

| 1 | 884.60 | 0.4902 *** | 21,492.04 | 0.1616 *** | 0.1945 | −0.118 *** | 0.0143 | −0.1292 * |

| (0.0000) | (0.0001) | (0.0005) | (0.0915) | |||||

| 2 | 758.06 | 0.3671 *** | 21,637.50 | 0.1840 *** | 0.2075 | −0.0884 ** | 0.0183 | 0.0794 |

| (0.0000) | (0.0000) | (0.0125) | (0.2834) | |||||

| 3 | 448.59 | 0.3230 *** | 20,248.20 | 0.1686 *** | 0.2134 | −0.096 *** | 0.0195 | 0.0887 |

| (0.0003) | (0.0001) | (0.0038) | (0.2766) | |||||

| 4 | 412.00 | 0.2692 *** | 20,286.44 | 0.1919 *** | 0.2141 | −0.0752 ** | 0.0195 | 0.0764 |

| (0.0024) | (0.0000) | (0.0349) | (0.3478) | |||||

| 5 | 607.61 | 0.3063 *** | 20,418.72 | 0.2153 *** | 0.2196 | −0.0696 * | 0.0143 | 0.1232 * |

| (0.0001) | (0.0000) | (0.0587) | (0.0727) | |||||

| Change in Put-Call Ratio | ||||||

|---|---|---|---|---|---|---|

| Volume | Open Interest | Spread | ||||

| Day | Level | Change | Level | Change | Level | Change |

| −5 | 1.6066 | 7.5020 *** | 0.9031 | 0.0264 | 3.1868 | 0.0355 |

| (0.0046) | (0.4009) | (0.5487) | ||||

| −4 | 3.4564 | 20.1593 * | 1.1845 | 0.0463 | 3.1719 | 0.0466 |

| (0.0636) | (0.1607) | (0.4383) | ||||

| −3 | 3.4609 | 11.5715 *** | 0.9438 | 0.0456 | 3.0164 | −0.0105 |

| (0.0022) | (0.1574) | (0.8653) | ||||

| −2 | 6.1027 | 11.9327 ** | 0.9742 | 0.0674 ** | 2.7370 | 0.0031 |

| (0.0317) | (0.0493) | (0.9585) | ||||

| −1 | 2.1512 | 8.7328 *** | 0.9719 | 0.0794 ** | 2.7284 | −0.0879 |

| (0.0004) | (0.0224) | (0.1844) | ||||

| 0 | 0.9845 | 3.2992 *** | 0.9627 | 0.0783 ** | 2.7685 | −0.1310 * |

| (0.0000) | (0.0271) | (0.0567) | ||||

| 1 | 1.2386 | 4.3561 *** | 0.8055 | 0.0199 | 2.8055 | −0.1080 |

| (0.0000) | (0.5979) | (0.1097) | ||||

| 2 | 1.3723 | 6.1316 *** | 0.8709 | 0.0035 | 2.9589 | −0.0630 |

| (0.0001) | (0.9279) | (0.3517) | ||||

| 3 | 2.4612 | 11.3684 ** | 0.8575 | −0.0173 | 2.5806 | −0.1408 ** |

| (0.0408) | (0.6472) | (0.0368) | ||||

| 4 | 1.2953 | 6.4719 *** | 0.8706 | −0.0003 | 2.5458 | −0.1259 * |

| (0.0005) | (0.9934) | (0.0650) | ||||

| 5 | 1.3354 | 5.1705 *** | 0.8742 | 0.0033 | 2.7998 | −0.1025 |

| (0.0000) | (0.9339) | (0.1583) | ||||

| Panel A: Calls. | ||||||||

| Unfavorable Information (n = 123) | Favorable Information (n = 114) | |||||||

| ∆Volume | ∆OI | ∆Spread | ∆Call/Stock | ∆Volume | ∆OI | ∆Spread | ∆Call/Stock | |

| Day | (1) | (2) | (3) | (4) | (5) | (6) | (7) | (8) |

| −5 | 0.2119 * | 0.0407 | −0.0815 ** | 0.0050 | 0.5616 *** | 0.1126 *** | 0.0500 | 0.3580 *** |

| (0.0675) | (0.3097) | (0.0346) | (0.9637) | (0.0000) | (0.0076) | (0.2644) | (0.0015) | |

| −4 | 0.2360 ** | 0.0241 | −0.0855 ** | 0.0682 | 0.2713 ** | 0.0922 ** | 0.0361 | 0.0568 |

| (0.0403) | (0.5676) | (0.0406) | (0.5097) | (0.0285) | (0.0378) | (0.4541) | (0.6197) | |

| −3 | 0.2441 ** | 0.0463 | −0.0575 | 0.0085 | 0.4083 *** | 0.0675 | 0.0622 | 0.1746 |

| (0.0308) | (0.2425) | (0.1750) | (0.9363) | (0.0014) | (0.1180) | (0.2279) | (0.1329) | |

| −2 | 0.2810 ** | 0.0497 | −0.0816 * | 0.0404 | 0.5552 *** | 0.0413 | 0.0580 | 0.2650 ** |

| (0.0209) | (0.2063) | (0.0560) | (0.7079) | (0.0000) | (0.3228) | (0.2291) | (0.0249) | |

| −1 | 0.4367 *** | 0.0345 | −0.0628 | −0.0580 | 0.6387 *** | 0.0683 | 0.0623 | 0.0333 |

| (0.0006) | (0.3436) | (0.1576) | (0.5995) | (0.0000) | (0.1399) | (0.2681) | (0.7770) | |

| 0 | 1.1037 *** | 0.0551 | 0.0079 | −0.3889 *** | 1.3631 *** | 0.1062 ** | 0.0543 | −0.2141 ** |

| (0.0000) | (0.1283) | (0.8568) | (0.0016) | (0.0000) | (0.0111) | (0.3411) | (0.0437) | |

| 1 | 0.6980 *** | 0.1214 *** | 0.0005 | −0.1559 | 0.9323 *** | 0.1949 *** | 0.0618 | −0.0259 |

| (0.0000) | (0.0023) | (0.9918) | (0.1743) | (0.0000) | (0.0000) | (0.2778) | (0.8218) | |

| 2 | 0.4372 *** | 0.1396 *** | −0.0210 | 0.0251 | 0.5519 *** | 0.2538 *** | 0.0263 | −0.0125 |

| (0.0003) | (0.0010) | (0.6264) | (0.8245) | (0.0002) | (0.0000) | (0.6439) | (0.9125) | |

| 3 | 0.2810 *** | 0.1418 *** | 0.0415 | −0.0671 | 0.5740 *** | 0.2648 *** | 0.0423 | 0.1022 |

| (0.0077) | (0.0010) | (0.3792) | (0.5041) | (0.0002) | (0.0000) | (0.4986) | (0.4046) | |

| 4 | 0.2494 ** | 0.1431 *** | 0.0315 | −0.0798 | 0.3881 *** | 0.2789 *** | 0.0201 | 0.0010 |

| (0.0307) | (0.0012) | (0.4752) | (0.4657) | (0.0077) | (0.0000) | (0.7509) | (0.9935) | |

| 5 | 0.1355 | 0.1543 *** | 0.0612 | −0.1562 | 0.4384 *** | 0.3129 *** | 0.0017 | 0.0917 |

| (0.2792) | (0.0008) | (0.2028) | (0.1718) | (0.0053) | (0.0000) | (0.9803) | (0.5052) | |

| Panel B: Puts. | ||||||||

| Unfavorable Information (n = 123) | Favorable Information (n = 114) | |||||||

| ∆Volume | ∆OI | ∆Spread | ∆Put/Stock | ∆Volume | ∆OI | ∆Spread | ∆Put/Stock | |

| Day | (1) | (2) | (3) | (4) | (5) | (6) | (7) | (8) |

| −5 | 0.2376 ** | 0.0658 | 0.0413 | 0.1393 | 0.3263 *** | 0.1100 ** | −0.0696 | 0.2021 * |

| (0.0344) | (0.1944) | (0.3679) | (0.1705) | (0.0093) | (0.0217) | (0.1220) | (0.0781) | |

| −4 | 0.1951 | 0.0701 | 0.0518 | 0.1101 | 0.3872 *** | 0.1077 ** | −0.0798 * | 0.2436 ** |

| (0.1404) | (0.1647) | (0.3281) | (0.3752) | (0.0034) | (0.0205) | (0.0723) | (0.0468) | |

| −3 | 0.4752 *** | 0.0888 * | 0.0304 | 0.3093 *** | 0.4212 *** | 0.0841 * | −0.0765 * | 0.2534 ** |

| (0.0002) | (0.0812) | (0.5263) | (0.0063) | (0.0019) | (0.0849) | (0.0753) | (0.0397) | |

| −2 | 0.4842 *** | 0.0893 | 0.0309 | 0.3214 *** | 0.2134 * | 0.1115 ** | −0.0843 * | 0.0342 |

| (0.0004) | (0.1028) | (0.5135) | (0.0096) | (0.0937) | (0.0231) | (0.0777) | (0.7632) | |

| −1 | 0.3810 *** | 0.0907 | −0.0351 | 0.0759 | 0.4006 ** | 0.1392 *** | −0.1706 *** | 0.0608 |

| (0.0045) | (0.1386) | (0.4971) | (0.5343) | (0.0107) | (0.0045) | (0.0008) | (0.6288) | |

| 0 | 0.9087 *** | 0.1187 * | −0.0554 | −0.1358 | 0.4865 *** | 0.1696 *** | −0.1948 *** | −0.4404 *** |

| (0.0000) | (0.0516) | (0.2827) | (0.1959) | (0.0044) | (0.0012) | (0.0005) | (0.0004) | |

| 1 | 0.5701 *** | 0.1621 ** | −0.1090 ** | −0.0705 | 0.4026 *** | 0.1611 *** | −0.1288 ** | −0.1936 * |

| (0.0001) | (0.0110) | (0.0179) | (0.5176) | (0.0036) | (0.0029) | (0.0121) | (0.0724) | |

| 2 | 0.4322 *** | 0.1659 *** | −0.0952 ** | 0.1701 | 0.2956 ** | 0.2036 *** | −0.0807 | −0.0202 |

| (0.0003) | (0.0095) | (0.0358) | (0.1048) | (0.0163) | (0.0002) | (0.1454) | (0.8467) | |

| 3 | 0.3616 *** | 0.1367 ** | −0.1036 ** | 0.1273 | 0.2814 ** | 0.2028 *** | −0.0869 * | 0.0470 |

| (0.0082) | (0.0292) | (0.0179) | (0.3150) | (0.0143) | (0.0002) | (0.0828) | (0.6414) | |

| 4 | 0.2309 ** | 0.1701 ** | −0.1033 ** | 0.0333 | 0.3119 ** | 0.2161 *** | −0.0434 | 0.1244 |

| (0.0491) | (0.0100) | (0.0257) | (0.7702) | (0.0215) | (0.0002) | (0.4324) | (0.2859) | |

| 5 | 0.4247 *** | 0.1883 *** | −0.1323 *** | 0.2435 ** | 0.1716 | 0.2455 *** | 0.0023 | −0.0136 |

| (0.0001) | (0.0047) | (0.0039) | (0.0111) | (0.1186) | (0.0000) | (0.9694) | (0.8898) | |

| CAR[−5, −1] | ΔOI_call−1 | ΔSpread_call−1 | ΔOI_put−1 | Δspread_put−1 | |

|---|---|---|---|---|---|

| CAR[−5, −1] | 1.0000 | −0.0406 | −0.3890 *** | −0.1484 ** | 0.3043 *** |

| (0.5354) | (<0.0001) | (0.0229) | (<0.0001) | ||

| ΔOI_call−1 | −0.0406 | 1.0000 | 0.0308 | 0.4616 *** | 0.0035 |

| (0.5354) | (0.6454) | (<0.0001) | (0.9579) | ||

| Δspread_call−1 | −0.3890 *** | 0.0308 | 1.0000 | 0.1078 | −0.4646 *** |

| (<0.0001) | (0.6454) | (0.1061) | (<0.0001) | ||

| ΔOI_put−1 | −0.1484 ** | 0.4616 *** | 0.1078 | 1.0000 | −0.1745 *** |

| (0.0229) | (<0.0001) | (0.1061) | (0.0086) | ||

| Δspread_put−1 | 0.3043 *** | 0.0035 | −0.4646 *** | −0.1745 *** | 1.0000 |

| (<0.0001) | (0.9579) | (<0.0001) | (0.0086) |

| Panel A: CAR[−5, −1] for terciles of SEOs ranked by change in puts’ open interest. | ||||||||

| Five-day Pre-offer CAR | ||||||||

| Change in Puts Open Interests | n | Mean | Std Dev | Median | Minimum | Q1 | Q3 | Maximum |

| Tercile 1 (Low) | 78 | 0.6983 | 6.6865 | −0.3165 | −14.4529 | −2.3216 | 2.0730 | 25.4722 |

| Tercile 2 (Middle) | 79 | −2.1436 | 5.9128 | −1.3526 | −22.7571 | −4.7246 | 0.5481 | 10.3906 |

| Tercile 3 (High) | 78 | −2.9351 | 6.8017 | −2.2004 | −26.1788 | −4.5232 | 1.6416 | 9.2187 |

| Univariate Test across Categories for Pre-offer CAR | ||||||||

| Wilcoxon Test | Median Test | |||||||

| Chi-Square | p-value | Chi-Square | p-value | |||||

| 8.7098 | 0.0128 ** | 5.4174 | 0.0666 | |||||

| Panel B: CAR[−5, −1] for terciles of SEOs ranked by change in calls’ open interest. | ||||||||

| Five-day Pre-offer CAR | ||||||||

| Change in Calls Open Interests | n | Mean | Std Dev | Median | Minimum | Q1 | Q3 | Maximum |

| Tercile 1 (Low) | 78 | −1.0669 | 6.6177 | −1.4275 | −26.1788 | −3.3268 | 1.1694 | 25.4722 |

| Tercile 2 (Middle) | 79 | −1.5099 | 6.1611 | −1.1619 | −22.7571 | −4.1977 | 1.4566 | 18.0239 |

| Tercile 3 (High) | 78 | −1.8118 | 7.1597 | −1.0669 | −25.3441 | −4.2608 | 2.1410 | 13.1235 |

| Univariate Test across Categories for Pre-offer CAR | ||||||||

| Wilcoxon Test | Median Test | |||||||

| Chi-Square | p-value | Chi-Square | p-value | |||||

| 0.0199 | 0.9901 | 1.1790 | 0.5546 | |||||

| Panel A: Correlation between CAR[−5, −1] and CAR [0, 20] for terciles of SEOs ranked by change in puts’ open interest. | ||

| Change in Put/Call Ratio of Open Interest | n | Correlation (Pre-offer CAR, Post-offer CAR) |

| Tercile 1 | 78 | −0.0899 |

| (0.4338) | ||

| Tercile 2 | 79 | 0.1960 * |

| (0.0834) | ||

| Tercile 3 | 78 | −0.2595 ** |

| (0.0218) | ||

| Panel B: Correlation between CAR[−5, −1] and CAR [0, 20] for terciles of SEOs ranked by change in calls’ open interest. | ||

| Change in Put/Call Ratio of Open Interest | n | Correlation (Pre-offer CAR, Post-offer CAR) |

| Tercile 1 | 78 | −0.1254 |

| (0.2740) | ||

| Tercile 2 | 79 | 0.0715 |

| (0.5313) | ||

| Tercile 3 | 78 | −0.0760 |

| (0.5083) | ||

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2022 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Charoenwong, C.; Ding, D.K.; Wang, P. Market Manipulation around Seasoned Equity Offerings: Evidence Prior to the Global Financial Crisis of 2007–2009. Int. J. Financial Stud. 2022, 10, 33. https://doi.org/10.3390/ijfs10020033

Charoenwong C, Ding DK, Wang P. Market Manipulation around Seasoned Equity Offerings: Evidence Prior to the Global Financial Crisis of 2007–2009. International Journal of Financial Studies. 2022; 10(2):33. https://doi.org/10.3390/ijfs10020033

Chicago/Turabian StyleCharoenwong, Charlie, David K. Ding, and Ping Wang. 2022. "Market Manipulation around Seasoned Equity Offerings: Evidence Prior to the Global Financial Crisis of 2007–2009" International Journal of Financial Studies 10, no. 2: 33. https://doi.org/10.3390/ijfs10020033

APA StyleCharoenwong, C., Ding, D. K., & Wang, P. (2022). Market Manipulation around Seasoned Equity Offerings: Evidence Prior to the Global Financial Crisis of 2007–2009. International Journal of Financial Studies, 10(2), 33. https://doi.org/10.3390/ijfs10020033