Towards a Dynamic Equilibrium-Seeking Model of a Closed Economy

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Abstract

1. Introduction

Antecedents

2. A Dynamic Equilibrium-Seeking Model

2.1. Conventions and Notation

. “Exogenous converters” are represented mathematically by capital letters and italics, while all “endogenous converters” are represented by a lowercase italicised font. Converters are used to provide clarity to the modelling process by explicitly showing how flows are calculated. Subscripts are used in equations to indicate the dimensionality of a variable. For example, the stock Industryaccountj denotes an accumulation of financial resources held by each industry j. A full list of stocks, flows and converters applied in the DES model is provided in the Supplementary Material.

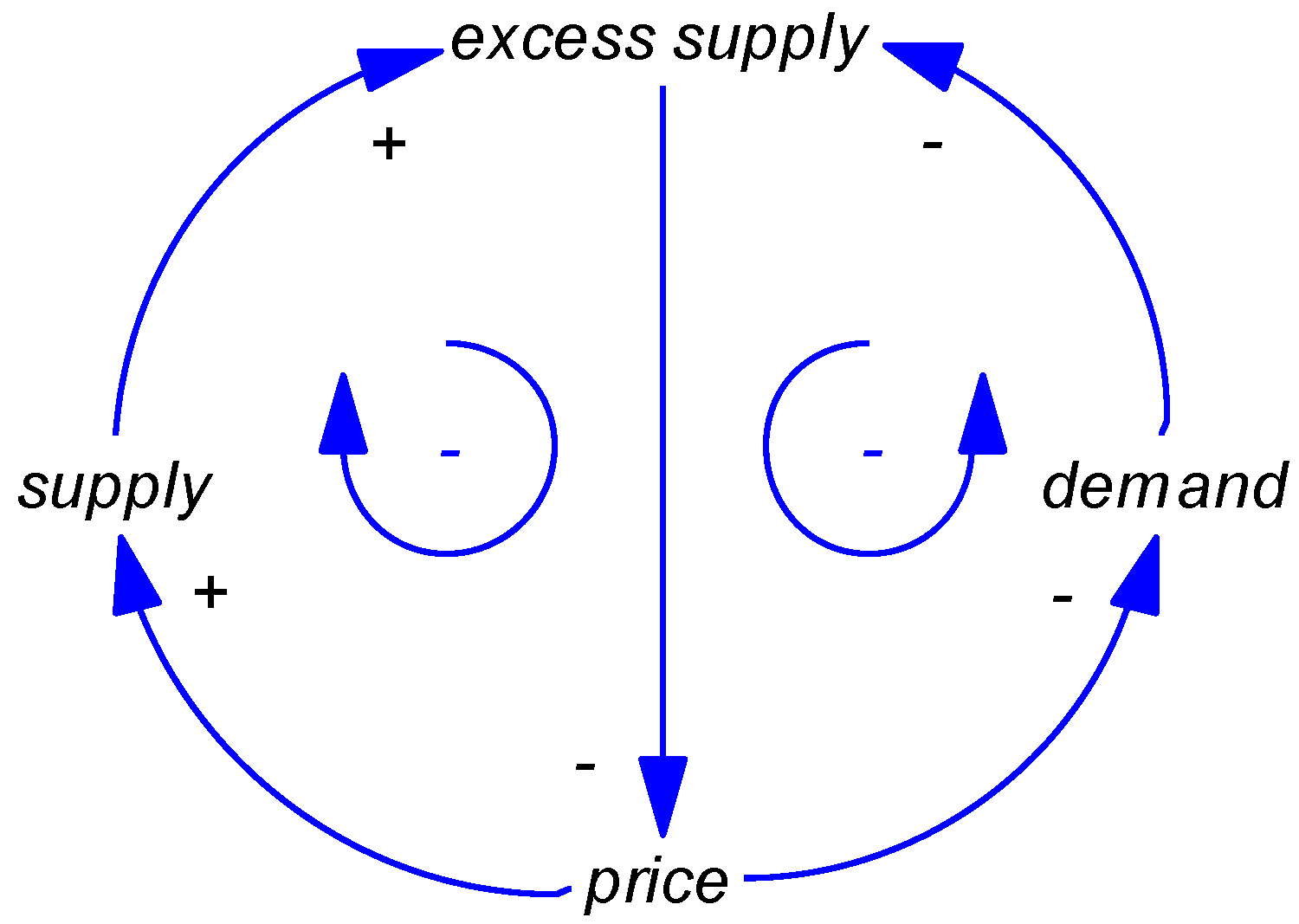

. “Exogenous converters” are represented mathematically by capital letters and italics, while all “endogenous converters” are represented by a lowercase italicised font. Converters are used to provide clarity to the modelling process by explicitly showing how flows are calculated. Subscripts are used in equations to indicate the dimensionality of a variable. For example, the stock Industryaccountj denotes an accumulation of financial resources held by each industry j. A full list of stocks, flows and converters applied in the DES model is provided in the Supplementary Material.2.2. Representing Supply, Demand and Price in a System Dynamics Model

2.3. The Dynamic Equilibrium-Seeking Model with Constant Factors (DES CF)

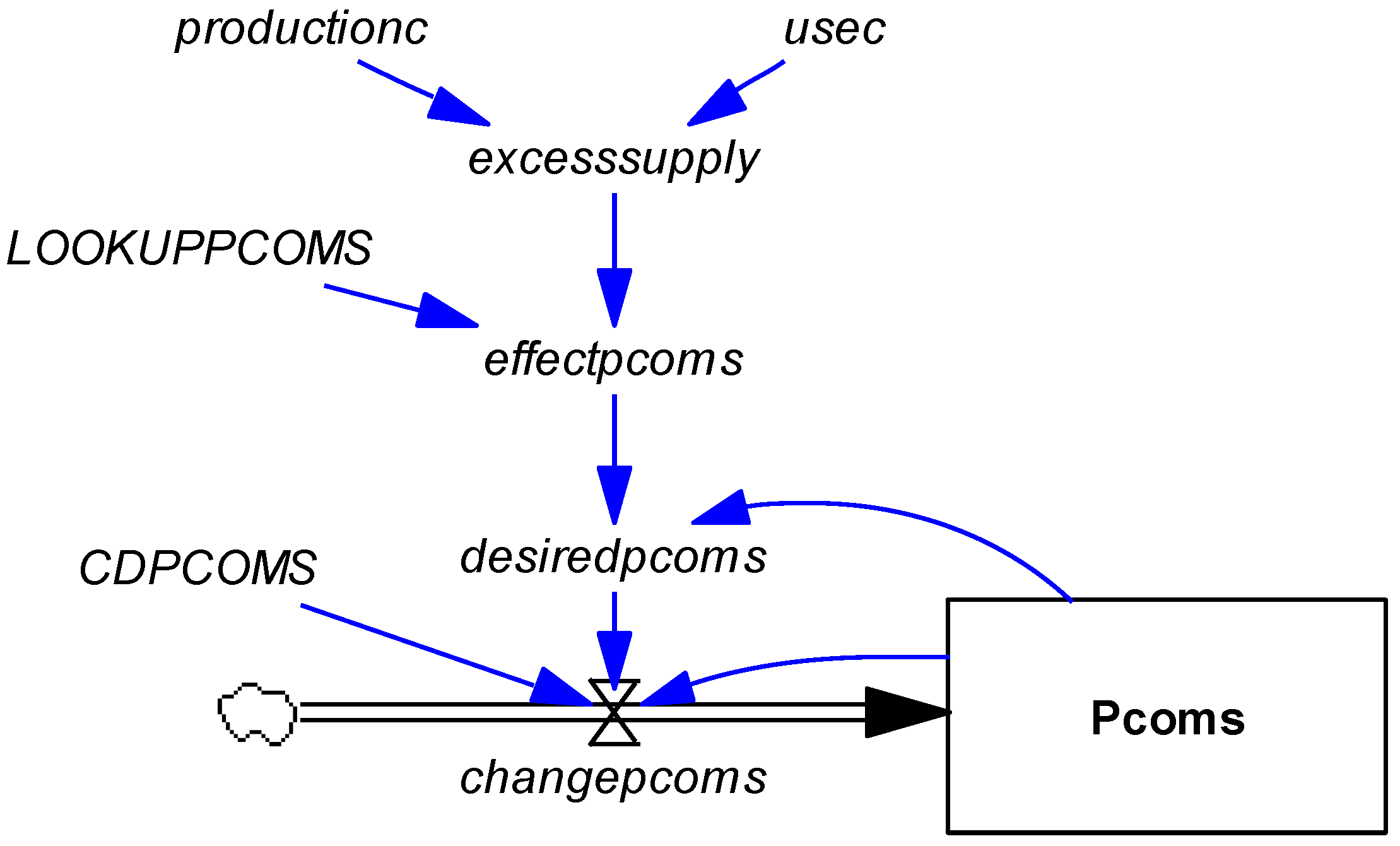

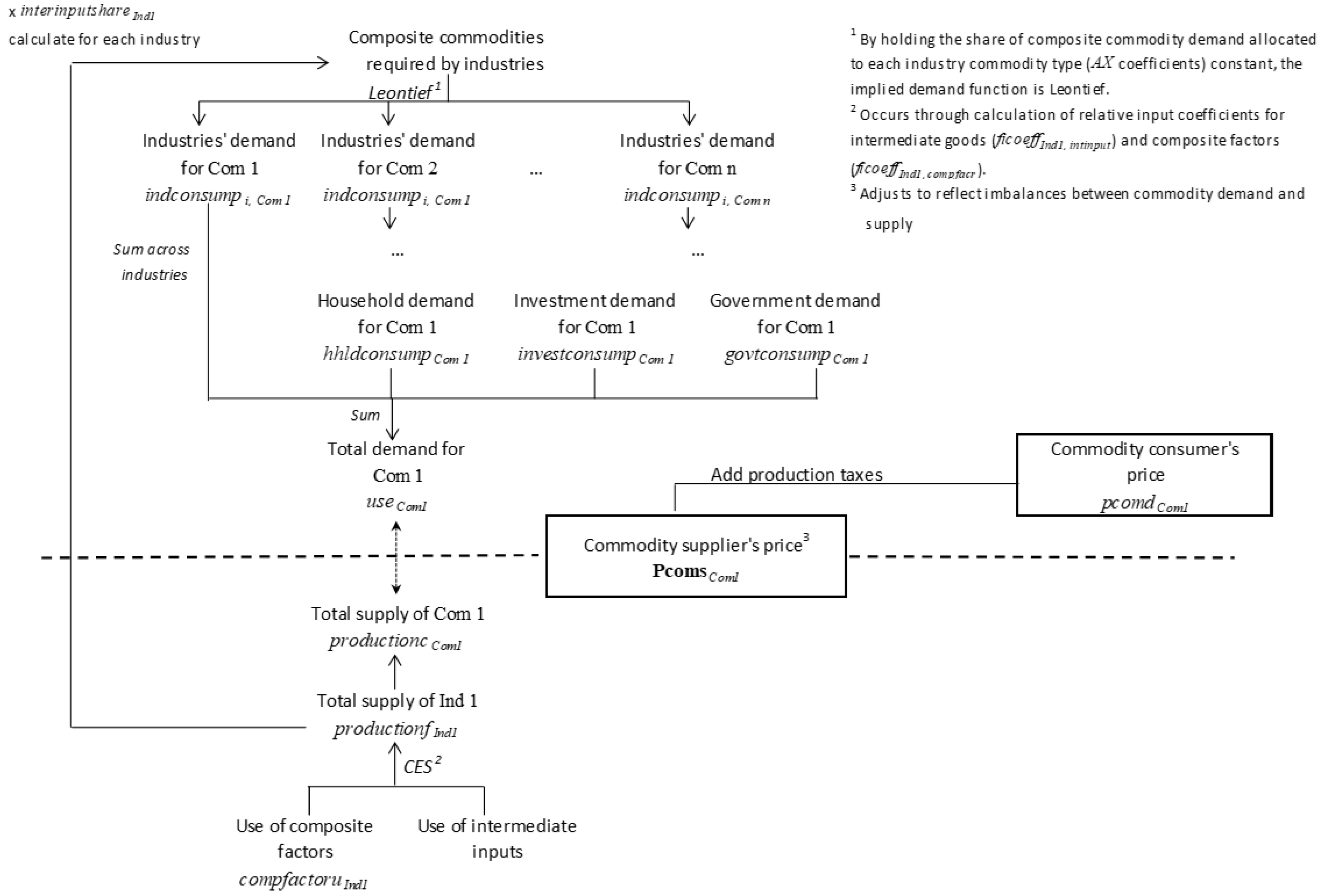

2.3.1. Commodities Module

2.3.2. Industries Module

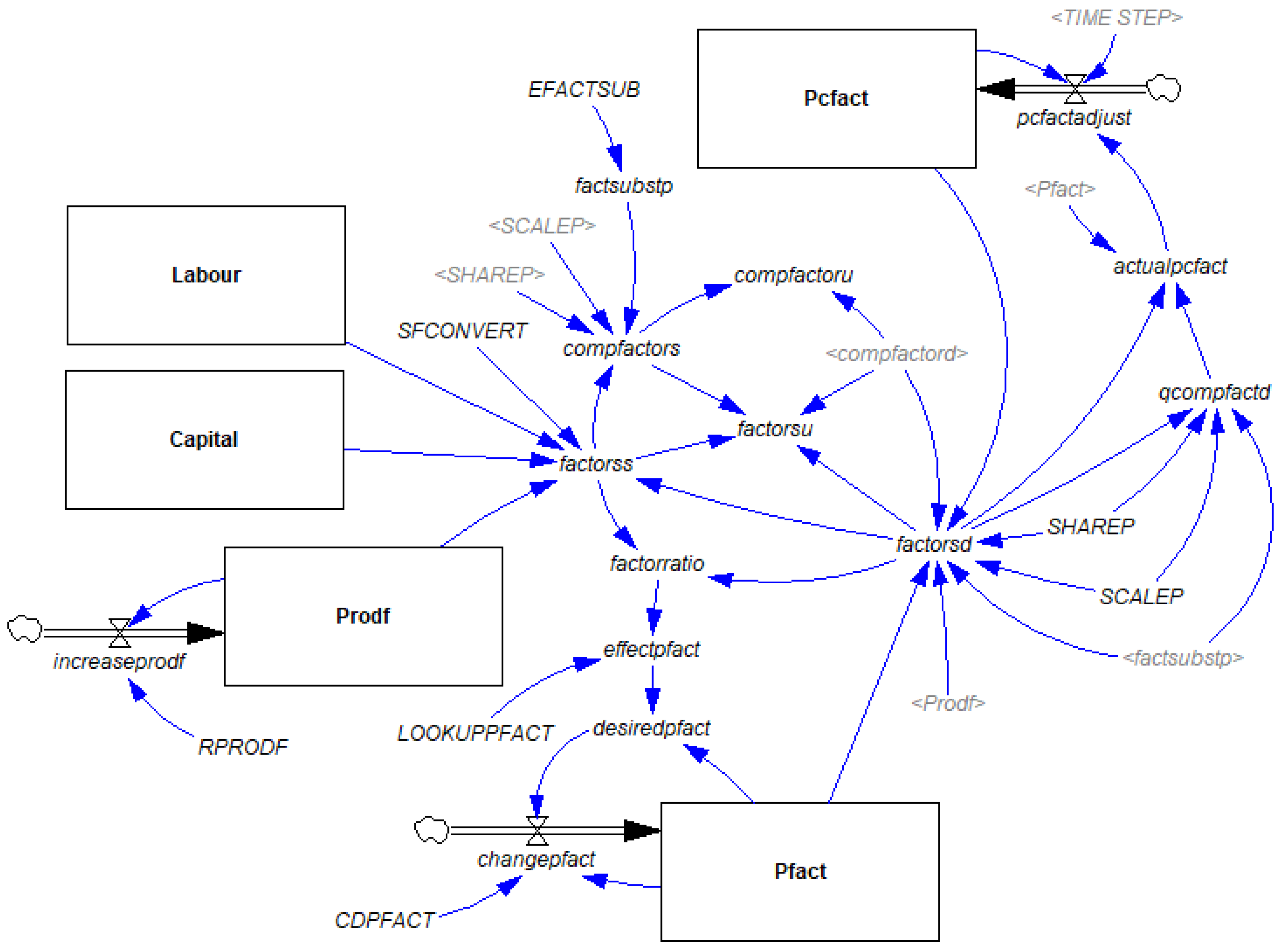

2.3.3. Factors Module

2.3.4. Government Module

2.3.5. Investment and Savings Module

2.3.6. Households Module

2.4. The Dynamic Equilibrium-Seeking Model with Factor Growth (DES FG)

2.4.1. Labour Module

2.4.2. Capital Module

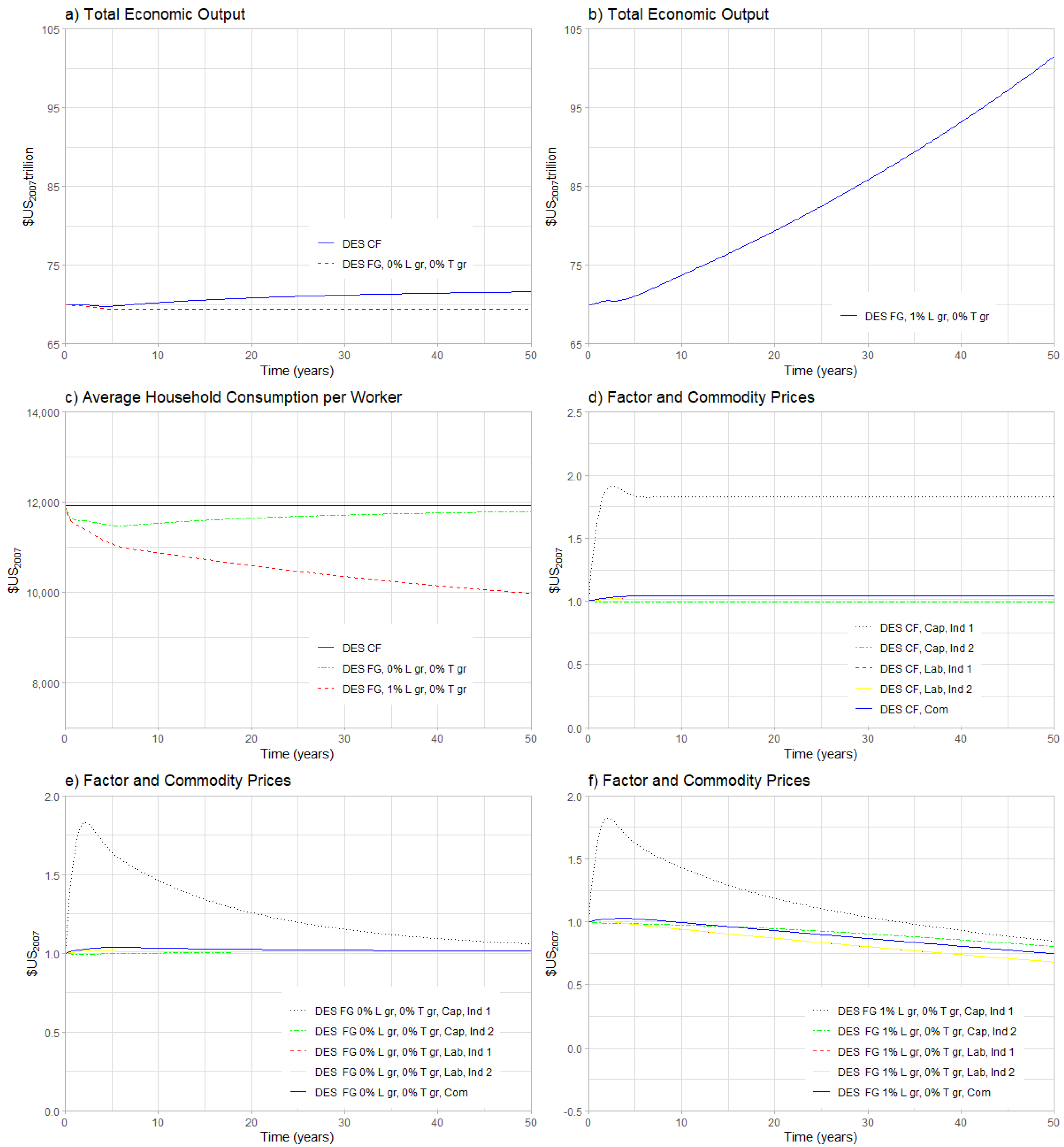

3. Results

3.1. Results without Exogenous Shock

3.2. Results with Exogenous Shock

4. Discussion

5. Conclusions

Supplementary Materials

Author Contributions

Funding

Acknowledgments

Conflicts of Interest

References

- Begg, D.; Fischer, S.; Dornbusch, R. Economics, 6th ed.; McGraw-Hill: New York, NY, USA, 2000. [Google Scholar]

- Samuelson, P.A.; Nordhaus, W.D. Economics, 19th ed.; Irwin/McGraw-Hill: New York, NY, USA, 2010. [Google Scholar]

- Dixon, P.B.; Jorgenson, D.W. Handbook of Computable General Equilibrium Modeling; Elsevier: Amsterdam, The Netherlands, 2013; Volume 1A. [Google Scholar]

- Dixon, P.B.; Jorgenson, D.W. Handbook of Computable General Equilibrium Modeling; Elsevier: Oxford, UK, 2013; Volume 1B. [Google Scholar]

- Hosoe, N.; Gasawa, K.; Hashimoto, H. Textbook of Computable General Equilibrium Modelling: Programming and Simulations; Lagrave Macmillan: Hampshire, UK, 2010. [Google Scholar]

- Lofgren, H.; Harris, R.L.; Sherman, R. A Standard Computable General Equilibrium Model in GAMS. Microcomputers in Policy Research 5; International Food Policy Research Institute: Washington, DC, USA, 2002. [Google Scholar]

- Quesnay, F. Le Tableau Économique. Edited and translated to English by M. Kuczynski and R. L. Meek. 1972; Macmillan: London, UK, 1758. [Google Scholar]

- Walras, L. Elements in Pure Economics, Original Work Published, 1874th ed.; Richard D. Irwin: Homewood, IL, USA, 1954. [Google Scholar]

- Leontief, W. The Structure of the American Economy (1919–1929); Harvard University Press: Cambridge, UK, 1941. [Google Scholar]

- Debreu, G. Theory of Value; Yale University Press: New Haven, CT, USA, 1959. [Google Scholar]

- Arrow, K.J.; Debreu, G. Existence of an equilibrium for a competitive economy. Econometrica 1954, 22, 265–290. [Google Scholar]

- Arrow, K.J. An extension of the basic theorems of classical welfare economics. In Proceedings of the Second Berkeley Symposium on Mathematical Statistics and Probability; University of California Press: Berkeley, CA, USA, 1951. [Google Scholar]

- Debreu, G. The coefficient of resource utilization. Econometrica 1951, 19, 273–292. [Google Scholar]

- Johansen, L. A Multi-Sector Study of Economic Growth; North-Holland: Amsterdam, The Netherlands, 1960. [Google Scholar]

- Harberger, A.C. The incidence of the corporate income tax. J. Political Econ. 1962, 70, 215–240. [Google Scholar]

- Scarf, H. The approximation of fixed points of a continuous mapping. Siam J. Appl. Math. 1967, 15, 1328–1343. [Google Scholar]

- Scarf, H.; Hansen, T. The Computation of Economic Equilibria; Yale University Press: New Haven, CT, USA, 1973. [Google Scholar]

- Aminu, A. A recursive dynamic computable general equilibrium analysis of value-added tax policy options for Nigeria. Econ. Struct. 2019, 8, 22. [Google Scholar]

- Gesualdo, M.; Giesecke, J.A.; Tran, N.H.; Felici, F. Building a computable general equilibrium tax model for Italy. Appl. Econ. 2019, 51–56, 6009–6020. [Google Scholar]

- Bye, B.; Strøm, B.; Åvitsland, T. Welfare effects of VAT reforms: A general equilibrium analysis. Int. Tax Public Financ. 2012, 19, 368–392. [Google Scholar]

- Shoven, J.B.; Whalley, J. Applied General Equilibrium; Cambridge University Press: Cambridge, UK, 1992. [Google Scholar]

- Shoven, J.B.; Whalley, J. Applied general-equilibrium models of taxation and international trade: An introduction and survey. J. Econ. Lit. 1984, 22, 1007–1051. [Google Scholar]

- Ginsburgh, V.; Keyser, M. The Structure of Applied General Equilibrium Models; MIT Press: Cambridge, MA, USA, 1997. [Google Scholar]

- Bekkers, E.; Antimiani, A.; Carrico, C.; Flaig, D.; Fontagne, L.; Foure, J.; Francois, J.; Itakura, K.; Kutilina-Dimitrova, Z.; Powers, W.; et al. Modelling Trade and Other Economic Interactions between Countries in Baseline Projections. J. Glob. Econ. Anal. 2020, 5, 273–345. [Google Scholar]

- Francois, J.; Martin, W. Computational General Equilibrium Modelling of International Trade. In Palgrave Handbook of International Trade; Palgrave Macmillan: London, UK, 2013. [Google Scholar]

- Partridge, M.D.; Rickman, D.S. Computable general equilibrium (CGE) modeling for regional economic development analysis. Reg. Stud. 2010, 21, 205–248. [Google Scholar]

- Partridge, M.D.; Rickman, D.S. Regional computable general equilibrium modeling: A survey and critical appraisal. Int. Reg. Sci. Rev. 1998, 86, 741–765. [Google Scholar] [CrossRef]

- Knowling, M.; White, J.T.; McDonald, G.W.; Kim, J.H.; Moore, C.R.; Hemmings, B. Disentangling environmental and economic contributions to hydro-economic model output uncertainty: An example in the context of land-use change impact assessment. Environ. Model. Softw. 2020, 127, 104653. [Google Scholar] [CrossRef]

- Fujimori, S.; Iizumi, T.; Hasegawa, T.; Takakura, J.; Takahashi, K.; Hijioka, Y. Macroeconomic Impacts of Climate Change Driven by Changes in Crop Yields. Sustainability 2018, 10, 3674. [Google Scholar] [CrossRef]

- Ren, X.; Weitzel, M.; O’Neill, B.C.; Lawrence, P.; Meiyappan, P.; Levis, S.; Balistreri, E.J.; Dalton, M. Avoided economic impacts of climate change on agriculture: Integrating a land surface model (CLM) with a global economic model (iPETS). Clim. Chang. 2016, 146, 517–531. [Google Scholar] [CrossRef]

- Bergman, L. CGE Modeling of Environmental Policy and Resource Management. In Handbook of Environmental Economics: Economy and International Environmental Issues; North-Holland: Amsterdam, The Netherlands, 2005; Volume 3, pp. 1274–1305. [Google Scholar]

- Shibusawa, H. A dynamic spatial CGE approach to assess economic effects of a large earthquake in China. Prog. Disaster Sci. 2020, 6, 100081. [Google Scholar] [CrossRef]

- Botzen, W.J.; Deschenes, O.; Sanders, M. The Economic Impacts of Natural Disasters: A Review of Models and Empirical Studies. Rev. Environ. Econ. Policy 2019, 13, 167–188. [Google Scholar] [CrossRef]

- McDonald, G.W.; Cronin, S.J.; Kim, J.H.; Smith, N.J.; Murray, C.A.; Procter, J.N. Computable general equilibrium modelling of economic impacts from volcanic event scenarios at regional and national scale, Mt. Taranaki, New Zealand. Bull. Volcanol. 2017, 78, 87. [Google Scholar] [CrossRef]

- Rose, A. Macroeconomic consequences of terrorist attacks: Estimation for the analysis of policies and rules. In Benefit-Cost Analyses for Security Policies: Does Increased Safety Have to Reduce Efficiency? Edward Elgar Publishing Limited: Cheltenham, UK, 2015; pp. 172–200. [Google Scholar]

- Miernyk, W.H. The Elements of Input-Output Analysis; Regional Research Institute, West Virginia University: Morgantown, WV, USA, 2020. [Google Scholar]

- Miller, R.E.; Blair, P.D. Input-Output Analysis: Foundations and Extensions; Cambridge University Press: New York, NY, USA, 2009. [Google Scholar]

- Raa, T.T. The Economics of Input-Output Analysis; The Edinburgh Building; Cambridge University Press: Cambridge, UK, 2006. [Google Scholar]

- Zodrow, G.R.; Diamond, J.W. Dynamic Overlapping Generations Computable General Equilibrium Models and the Analysis of Tax Policy: The Diamond-Zodrow Model. In Handbook of Development Economics; North-Holland: Amsterdam, The Netherlands, 2013; Volume 2, pp. 743–809. [Google Scholar]

- Bala, B.K.; Arshad, F.M.; Noh, K.M. System Dynamics: Modelling and Simulation; Springer: Singapore, 2017. [Google Scholar]

- Sterman, J.D. Business Dynamics: Systems Thinking and Modeling for a Complex World; McGraw-Hill Higher Education: Boston, MA, USA, 2000. [Google Scholar]

- Forrester, J.W. World Dynamics; Wright Allen Press: Cambridge, MA, USA, 1971. [Google Scholar]

- Forrester, J.W. Urban Dynamics; MIT Press: Cambridge, MA, USA, 1969. [Google Scholar]

- Forrester, J.W. Industrial Dynamics; MIT Press: Cambridge, MA, USA; John Wiley and Sons, Inc.: Hoboken, NJ, USA, 1961. [Google Scholar]

- Ravelojaona, P. On constant elasticity of substitution–Constant elasticity of transformation Directional Distance Functions. Eur. J. Oper. Res. 2019, 272, 780–791. [Google Scholar] [CrossRef]

- Van der Mensbrugghe, D.; Peters, J.C. Volume preserving CES and CET formulations. In Proceedings of the 19th Annual Conference on Global Economic Analysis, Washington, DC, USA, 15–17 June 2016. [Google Scholar]

- Sen, A. Neo-classical and neo-Keynesian theories of distribution. Econ. Rec. 1963, 39, 46–53. [Google Scholar]

- Popescu, C.R.; Popescu, G.N. An Exploratory Study Based on a Questionnaire Concerning Green and Sustainable Finance, Corporate Social Responsibility, and Performance: Evidence from the Romanian Business Environment. J. Risk Financ. Manag. 2019, 12, 162. [Google Scholar]

- Nemeth, G.; Szabo, L.; Ciscar, J.H. Estimation of Armington elasticities in a CGE economy-energy-environment model for Europe. Econ. Model. 2011, 28, 1993–1999. [Google Scholar] [CrossRef]

- Armington, P. A Theory of Demand for Products Distinguished by Place of Production. IMF Staff Pap. 1969, 16, 159–178. [Google Scholar]

- Neild, R. The future of economics: The case for an evolutionary approach. Econ. Labour Relat. Rev. 2017, 28, 164–172. [Google Scholar] [CrossRef]

- Dossi, G.; Nelson, R.R. An introduction to evolutionary theories in economics. J. Evol. Econ. 1994, 4, 153–172. [Google Scholar] [CrossRef]

| 1 |

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2020 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).

Share and Cite

McDonald, N.J.; McDonald, G.W. Towards a Dynamic Equilibrium-Seeking Model of a Closed Economy. Systems 2020, 8, 42. https://doi.org/10.3390/systems8040042

McDonald NJ, McDonald GW. Towards a Dynamic Equilibrium-Seeking Model of a Closed Economy. Systems. 2020; 8(4):42. https://doi.org/10.3390/systems8040042

Chicago/Turabian StyleMcDonald, Nicola J., and Garry W. McDonald. 2020. "Towards a Dynamic Equilibrium-Seeking Model of a Closed Economy" Systems 8, no. 4: 42. https://doi.org/10.3390/systems8040042

APA StyleMcDonald, N. J., & McDonald, G. W. (2020). Towards a Dynamic Equilibrium-Seeking Model of a Closed Economy. Systems, 8(4), 42. https://doi.org/10.3390/systems8040042