Volatility Connectedness of Chinese Financial Institutions: Evidence from a Frequency Dynamics Perspective

Abstract

:1. Introduction

2. Methodology

2.1. Diebold–Yilmaz Time-Domain Connectedness

2.2. Baruník–Křehlík Frequency-Domain Connectedness

2.3. Graphical Display of Network

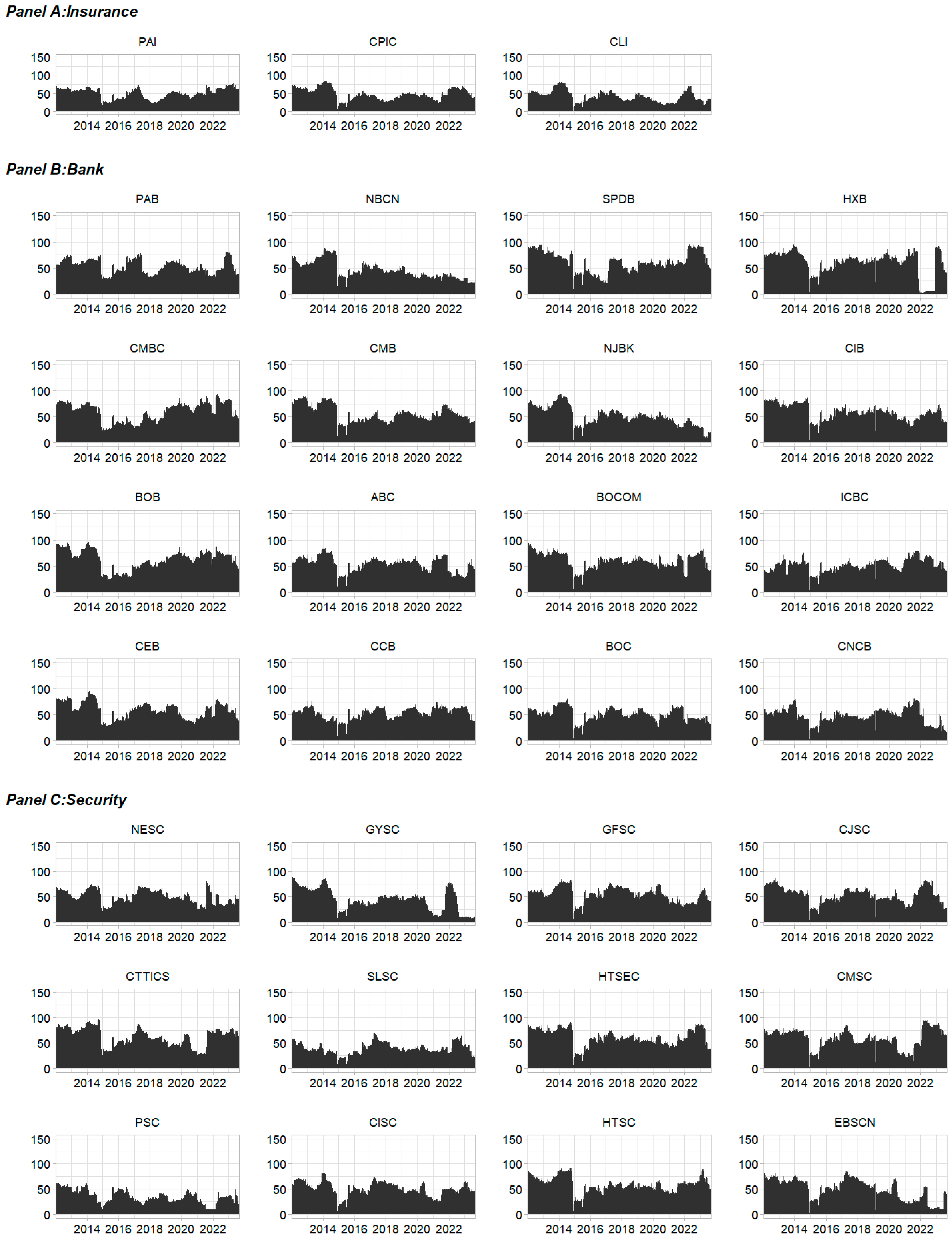

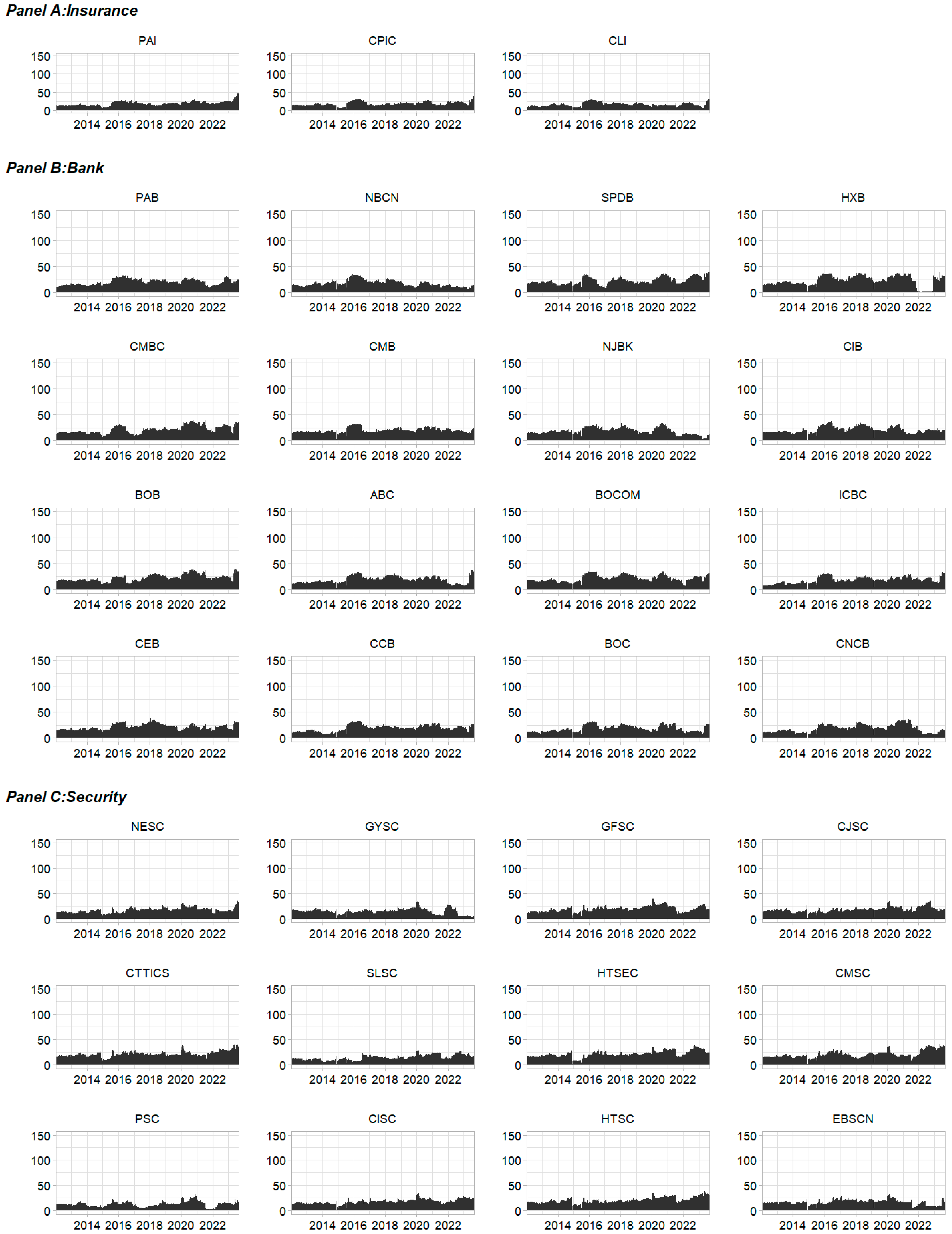

3. Data

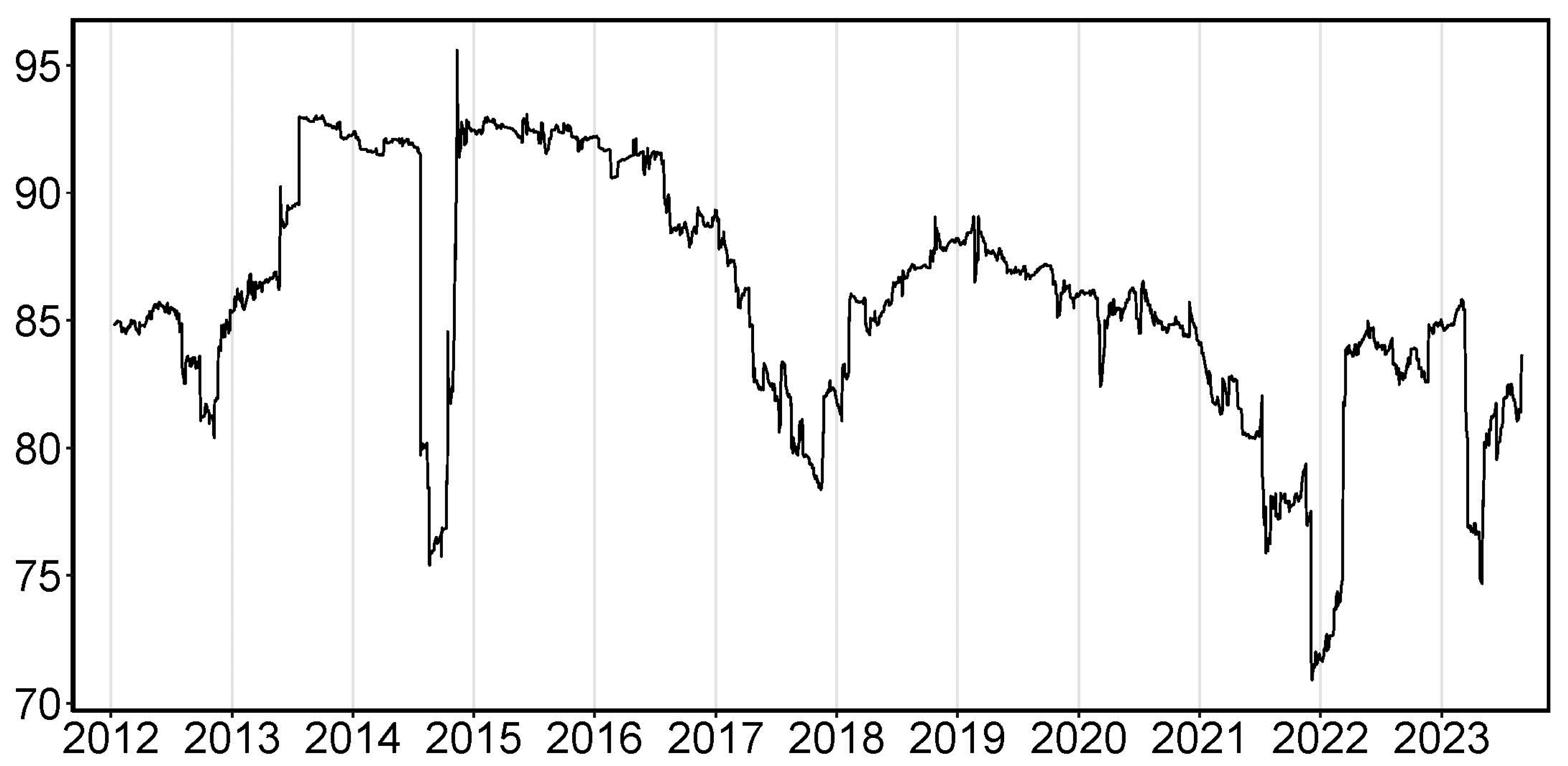

4. Empirical results

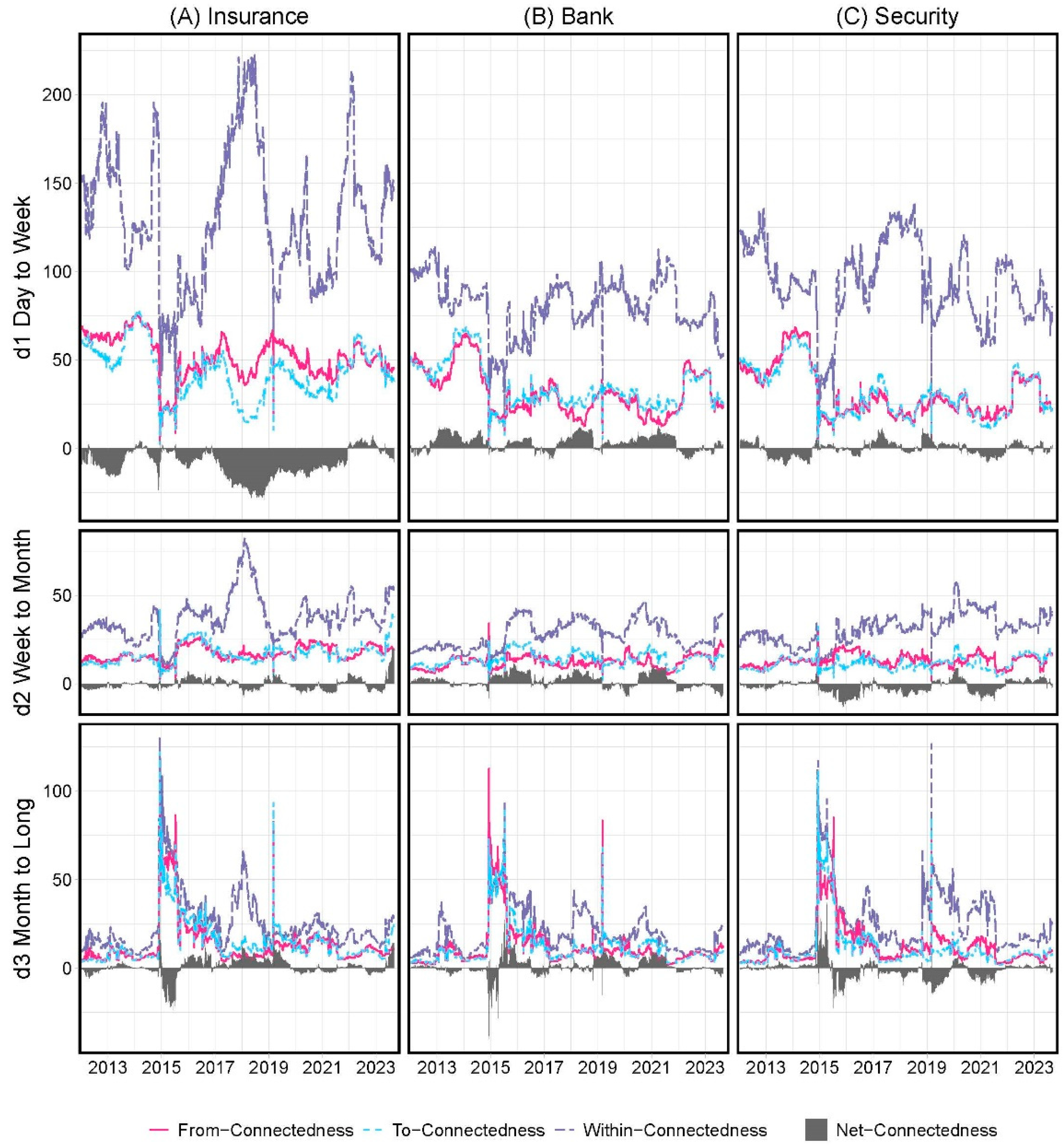

4.1. Dynamic Analysis

4.1.1. Total Frequency Connectedness

4.1.2. Sector Directional Frequency Connectedness

4.1.3. Institution Directional Frequency Connectedness

4.2. Network Estimation Results

4.2.1. Full-Sample Networks

4.2.2. Network Structure on Some Critical Dates

5. Conclusions and Discussion

Author Contributions

Funding

Data Availability Statement

Conflicts of Interest

Appendix A. Short-Term and Medium-Term Directional Connectedness of 31 Chinese Financial Institutions

| 1 | The choice of a forecast horizon of 100 days was based on Baruník and Křehlík’s (2018) original paper, although the connectedness approach developed by these authors was not affected by the selected forecast horizon. |

References

- Xu, Q.; Zhang, Y.; Zhang, Z. Tail-risk spillovers in cryptocurrency markets. Financ. Res. Lett. 2021, 38, 101453. [Google Scholar] [CrossRef]

- Mader, P.; Mertens, D.; Van Der Zwan, N. Financialization: An introduction. In The Routledge International Handbook of Financialization; Routledge: Oxfordshire, UK, 2020; pp. 1–16. [Google Scholar]

- Gofman, M. Efficiency and stability of a financial architecture with too-interconnected-to-fail institutions. J. Financ. Econ. 2017, 124, 113–146. [Google Scholar] [CrossRef]

- Barucca, P.; Bardoscia, M.; Caccioli, F.; D’Errico, M.; Visentin, G.; Caldarelli, G.; Battiston, S. Network valuation in financial systems. Math. Financ. 2020, 30, 1181–1204. [Google Scholar] [CrossRef]

- Duarte, F.; Eisenbach, T.M. Fire-sale spillovers and systemic risk. J. Financ. 2021, 76, 1251–1294. [Google Scholar] [CrossRef]

- Fang, L.; Sun, B.; Li, H.; Yu, H. Systemic risk network of Chinese financial institutions. Emerg. Mark. Rev. 2018, 35, 190–206. [Google Scholar] [CrossRef]

- Li, J.; Yao, Y.; Li, J.; Zhu, X. Network-based estimation of systematic and idiosyncratic contagion: The case of Chinese financial institutions. Emerg. Mark. Rev. 2019, 40, 100624. [Google Scholar] [CrossRef]

- Alessandri, P.; Masciantonio, S.; Zaghini, A. Tracking Banks’ Systemic Importance Before and After the Crisis. Int. Financ. 2015, 18, 157–186. [Google Scholar] [CrossRef]

- Diebold, F.X.; Yilmaz, K. Measuring financial asset return and volatility spillovers, with application to global equity markets. Econ. J. 2009, 119, 158–171. [Google Scholar] [CrossRef]

- Bahloul, S.; Khemakhem, I. Dynamic return and volatility connectedness between commodities and Islamic stock market indices. Resour. Policy 2021, 71, 101993. [Google Scholar] [CrossRef]

- Youssef, M.; Mokni, K.; Ajmi, A.N. Dynamic connectedness between stock markets in the presence of the COVID-19 pandemic: Does economic policy uncertainty matter? Financ. Innov. 2021, 7, 13. [Google Scholar] [CrossRef]

- Umar, Z.; Jareño, F.; Escribano, A. Agricultural commodity markets and oil prices: An analysis of the dynamic return and volatility connectedness. Resour. Policy 2021, 73, 102147. [Google Scholar] [CrossRef]

- Gong, X.; Xu, J. Geopolitical risk and dynamic connectedness between commodity markets. Energy Econ. 2022, 110, 106028. [Google Scholar] [CrossRef]

- Chen, R.; Iqbal, N.; Irfan, M.; Shahzad, F.; Fareed, Z. Does financial stress wreak havoc on banking, insurance, oil, and gold markets? New empirics from the extended joint connectedness of TVP-VAR model. Resour. Policy 2022, 77, 102718. [Google Scholar] [CrossRef]

- Arfaoui, N.; Yousaf, I.; Jareño, F. Return and volatility connectedness between gold and energy markets: Evidence from the pre-and post-COVID vaccination phases. Econ. Anal. Policy 2023, 77, 617–634. [Google Scholar] [CrossRef]

- Bostanci, G.; Yilmaz, K. How connected is the global sovereign credit risk network? J. Bank. Financ. 2020, 113, 105761. [Google Scholar] [CrossRef]

- Yang, L.; Hamori, S. Modeling the global sovereign credit network under climate change. Int. Rev. Financ. Anal. 2023, 87, 102618. [Google Scholar] [CrossRef]

- Hung, N.T.; Nguyen, L.T.M.; Vo, X.V. Exchange rate volatility connectedness during COVID-19 outbreak: DECO-GARCH and Transfer Entropy approaches. J. Int. Financ. Mark. Inst. Money 2022, 81, 101628. [Google Scholar] [CrossRef]

- Huynh, T.L.D.; Nasir, M.A.; Nguyen, D.K. Spillovers and connectedness in foreign exchange markets: The role of trade policy uncertainty. Q. Rev. Econ. Financ. 2020, 87, 191–199. [Google Scholar] [CrossRef]

- Wen, T.; Wang, G.J. Volatility connectedness in global foreign exchange markets. J. Multinatl. Financ. Manag. 2020, 54, 100617. [Google Scholar] [CrossRef]

- Koutmos, D. Return and volatility spillovers among cryptocurrencies. Econ. Lett. 2018, 173, 122–127. [Google Scholar] [CrossRef]

- Hasan, M.; Naeem, M.A.; Arif, M.; Yarovaya, L. Higher moment connectedness in cryptocurrency market. J. Behav. Exp. Financ. 2021, 32, 100562. [Google Scholar] [CrossRef]

- Li, Z.; Mo, B.; Nie, H. Time and frequency dynamic connectedness between cryptocurrencies and financial assets in China. Int. Rev. Econ. Financ. 2023, 86, 46–57. [Google Scholar] [CrossRef]

- Mensi, W.; Al Rababa’a, A.R.; Vo, X.V.; Kang, S.H. Asymmetric spillover and network connectedness between crude oil, gold, and Chinese sector stock markets. Energy Econ. 2021, 98, 105262. [Google Scholar] [CrossRef]

- Dai, Z.; Zhu, H.; Zhang, X. Dynamic spillover effects and portfolio strategies between crude oil, gold and Chinese stock markets related to new energy vehicle. Energy Econ. 2022, 109, 105959. [Google Scholar] [CrossRef]

- Härdle, W.K.; Wang, W.; Yu, L. TENET: Tail-Event driven NETwork risk. J. Econom. 2016, 192, 499–513. [Google Scholar] [CrossRef]

- Wang, G.J.; Jiang, Z.Q.; Lin, M.; Xie, C.; Stanley, H.E. Interconnectedness and systemic risk of China’s financial institutions. Emerg. Mark. Rev. 2018, 35, 1–18. [Google Scholar] [CrossRef]

- Wang, G.J.; Xie, C.; Zhao, L.; Jiang, Z.Q. Volatility connectedness in the Chinese banking system: Do state-owned commercial banks contribute more? J. Int. Financ. Mark. Inst. Money 2018, 57, 205–230. [Google Scholar] [CrossRef]

- Diebold, F.X.; Yilmaz, K. On the network topology of variance decompositions: Measuring the connectedness of financial firms. J. Econom. 2014, 182, 119–134. [Google Scholar] [CrossRef]

- Liang, Q.; Lu, Y.; Li, Z. Business connectedness or market risk? Evidence from financial institutions in China. China Econ. Rev. 2020, 62, 101503. [Google Scholar] [CrossRef]

- Baruník, J.; Křehlík, T. Measuring the Frequency Dynamics of Financial Connectedness and Systemic Risk. J. Financ. Econom. 2018, 16, 271–296. [Google Scholar] [CrossRef]

- Bissoondoyal-Bheenick, E.; Do, H.; Hu, X.; Zhong, A. Learning from SARS: Return and volatility connectedness in COVID-19. Financ. Res. Lett. 2021, 41, 101796. [Google Scholar] [CrossRef]

- Elnahass, M.; Trinh, V.Q.; Li, T. Global banking stability in the shadow of Covid-19 outbreak. J. Int. Financ. Mark. Inst. Money 2021, 72, 101322. [Google Scholar] [CrossRef]

- Wang, Y.; Zhang, D.; Wang, X.; Fu, Q. How does COVID-19 affect China’s insurance market? Emerg. Mark. Financ. Trade 2020, 56, 2350–2362. [Google Scholar] [CrossRef]

- Sun, Y.; Wu, M.; Zeng, X.; Peng, Z. The impact of COVID-19 on the Chinese stock market: Sentimental or substantial? Financ. Res. Lett. 2021, 38, 101838. [Google Scholar] [CrossRef] [PubMed]

- Cheng, T.; Liu, J.; Yao, W.; Zhao, A.B. The impact of COVID-19 pandemic on the volatility connectedness network of global stock market. Pac. Basin Financ. J. 2022, 71, 101678. [Google Scholar] [CrossRef]

- Umar, Z.; Jareño, F.; Escribano, A. Dynamic return and volatility connectedness for dominant agricultural commodity markets during the COVID-19 pandemic era. Appl. Econ. 2022, 54, 1030–1054. [Google Scholar] [CrossRef]

- Umar, Z.; Jareño, F.; de la O González, M. The impact of COVID-19-related media coverage on the return and volatility connectedness of cryptocurrencies and fiat currencies. Technol. Forecast. Soc. Chang. 2021, 172, 121025. [Google Scholar] [CrossRef]

- Hamouda, F. What can we learn about repurchase programmes and systemic risk? Evidence from US banks during financial turmoil. J. Risk Manag. Financ. Inst. 2023, 16, 34–51. [Google Scholar]

- Diebold, F.X.; Yilmaz, K. Trans-Atlantic equity volatility connectedness: US and European financial institutions, 2004–2014. J. Financ. Econom. 2015, 14, 81–127. [Google Scholar]

- Shahzad, U.; Ferraz, D.; Nguyen, H.H.; Cui, L. Investigating the spill overs and connectedness between financial globalization, high-tech industries and environmental footprints: Fresh evidence in context of China. Technol. Forecast. Soc. Change 2022, 174, 121205. [Google Scholar] [CrossRef]

- Jiang, J.; Piljak, V.; Tiwari, A.K.; Äijö, J. Frequency volatility connectedness across different industries in China. Financ. Res. Lett. 2019, 101376. [Google Scholar] [CrossRef]

- Tiwari, A.K.; Cunado, J.; Gupta, R.; Wohar, M.E. Volatility spillovers across global asset classes: Evidence from time and frequency domains. Q. Rev. Econ. Financ. 2018, 70, 194–202. [Google Scholar] [CrossRef]

- Wang, X.; Wang, Y. Volatility spillovers between crude oil and Chinese sectoral equity markets: Evidence from a frequency dynamics perspective. Energy Econ. 2019, 80, 995–1009. [Google Scholar] [CrossRef]

- Diebold, F.X.; Yilmaz, K. Better to give than to receive: Predictive directional measurement of volatility spillovers. Int. J. Forecast. 2012, 28, 57–66. [Google Scholar] [CrossRef]

- Baruńik, J.; Kočenda, E.; Vácha, L.S. Volatility spillovers across petroleum markets. Energy J. 2015, 36, 309–329. [Google Scholar] [CrossRef]

- Adekoya, O.B.; Oliyide, J.A.; Noman, A. The volatility connectedness of the EU carbon market with commodity and financial markets in time-and frequency-domain: The role of the US economic policy uncertainty. Resour. Policy 2021, 74, 102252. [Google Scholar] [CrossRef]

- Barigozzi, M.; Brownlees, C. Nets: Network estimation for time series. J. Appl. Econom. 2019, 34, 347–364. [Google Scholar] [CrossRef]

- Jiang, S.; Li, Y.; Lu, Q.; Wang, S.; Wei, Y. Volatility communicator or receiver? Investigating volatility spillover mechanisms among Bitcoin and other financial markets. Res. Int. Bus. Financ. 2022, 59, 101543. [Google Scholar] [CrossRef]

- Koop, G.; Pesaran, M.H.; Potter, S.M. Impulse response analysis in nonlinear multivariate models. J. Econom. 1996, 74, 119–147. [Google Scholar] [CrossRef]

- Pesaran, H.H.; Shin, Y. Generalized impulse response analysis in linear multivariate models. Econ. Lett. 1998, 58, 17–29. [Google Scholar] [CrossRef]

- Stiassny, A. A spectral decomposition for structural VAR models. Empir. Econ. 1996, 21, 535–555. [Google Scholar] [CrossRef]

- Nicholson, W.B.; Matteson, D.S.; Bien, J. VARX-L: Structured regularization for large vector autoregressions with exogenous variables. Int. J. Forecast. 2017, 33, 627–651. [Google Scholar] [CrossRef]

- Simon, N.; Friedman, J.; Hastie, T.; Tibshirani, R. A sparse-group lasso. J. Comput. Graph. Stat. 2013, 22, 231–245. [Google Scholar] [CrossRef]

- Dew-Becker, I.; Giglio, S. Asset pricing in the frequency domain: Theory and empirics. Rev. Financ. Stud. 2016, 29, 2029–2068. [Google Scholar] [CrossRef]

- Demirer, M.; Diebold, F.X.; Liu, L.; Yilmaz, K. Estimating global bank network connectedness. J. Appl. Econom. 2018, 33, 1–15. [Google Scholar] [CrossRef]

- Jacomy, M.; Venturini, T.; Heymann, S.; Bastian, M. ForceAtlas2, a continuous graph layout algorithm for handy network visualization designed for the Gephi software. PLoS ONE 2014, 9, e98679. [Google Scholar] [CrossRef]

- Garman, M.B.; Klass, M.J. On the Estimation of Security Price Volatilities from Historical Data. J. Bus. 1980, 53, 67–78. [Google Scholar] [CrossRef]

- Shah, A.A.; Paul, M.; Bhanja, N.; Dar, A.B. Dynamics of connectedness across crude oil, precious metals and exchange rate: Evidence from time and frequency domains. Resour. Policy 2021, 73, 102154. [Google Scholar] [CrossRef]

- Wang, Y.; Zhang, Z.; Li, X.; Chen, X.; Wei, Y. Dynamic return connectedness across global commodity futures markets: Evidence from time and frequency domains. Phys. A Stat. Mech. Its Appl. 2020, 542, 123464. [Google Scholar] [CrossRef]

- Ouyang, Z.; Zhou, X.; Xie, N. Time-varying connectedness measurement of Chinese financial institutions: New evidence from the frequency domain perspective. Syst. Eng. Theory Pract. 2022, 42, 2087–2101. [Google Scholar] [CrossRef]

- Foglia, M.; Addi, A.; Angelini, E. The Eurozone banking sector in the time of COVID-19: Measuring volatility connectedness. Glob. Financ. J. 2022, 51, 100677. [Google Scholar] [CrossRef]

- Chen, Y.P.; Chen, Y.L.; Chiang, S.H.; Mo, W.S. Determinants of connectedness in financial institutions: Evidence from Taiwan. Emerg. Mark. Rev. 2023, 55, 100951. [Google Scholar] [CrossRef]

- Costa, A.; Matos, P.; da Silva, C. Sectoral connectedness: New evidence from US stock market during COVID-19 pandemics. Financ. Res. Lett. 2022, 45, 102124. [Google Scholar] [CrossRef] [PubMed]

- Fan, X.; Wang, Y.; Wang, D. Network connectedness and China’s systemic financial risk contagion—An analysis based on big data. Pac. Basin Financ. J. 2021, 68, 101322. [Google Scholar] [CrossRef]

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| Ticker Code | Financial Institution | Abbr. | Mean | Std. Dev. | Skewness | Kurtosis | ADF |

|---|---|---|---|---|---|---|---|

| Panel A: Insurance | |||||||

| 601318.SS | Ping An Insurance | PAI | 0.0007 | 0.0009 | 6.26 | 77.92 | −32.093 *** |

| 601601.SS | China Pacific Insurance | CPIC | 0.0009 | 0.0010 | 3.84 | 27.47 | −30.876 *** |

| 601628.SS | China Life Insurance | CLI | 0.0009 | 0.0012 | 4.494 | 33.34 | −26.268 *** |

| Panel B: Banks | |||||||

| 000001.SZ | Ping An Bank | PAB | 0.0008 | 0.0010 | 4.396 | 38.06 | −29.637 *** |

| 002142.SZ | Bank of Ningbo | NBCB | 0.0009 | 0.0012 | 5.318 | 58.05 | −29.107 *** |

| 600000.SS | Shanghai Pudong Development Bank | SPDB | 0.0005 | 0.0008 | 4.126 | 28.63 | −28.839 *** |

| 600015.SS | Hua Xia Bank | HXB | 0.0006 | 0.0009 | 5.258 | 50.37 | −26.748 *** |

| 600016.SS | China Minsheng Banking | CMBC | 0.0006 | 0.0010 | 5.216 | 45.88 | −26.147 *** |

| 600036.SS | China Merchants Bank | CMB | 0.0007 | 0.0009 | 6.173 | 69.85 | −27.399 *** |

| 601009.SS | Bank of Nanjing | NJBK | 0.0007 | 0.0011 | 5.239 | 48.79 | −27.117 *** |

| 601166.SS | Industrial Bank | CIB | 0.0006 | 0.0009 | 4.146 | 28.56 | −29.045 *** |

| 601169.SS | Bank of Beijing | BOB | 0.0005 | 0.0009 | 4.844 | 39.34 | −26.741 *** |

| 601288.SS | Agricultural Bank of China Limited | ABC | 0.0004 | 0.0007 | 5.547 | 47.02 | −27.599 *** |

| 601328.SS | Bank of Communications | BOCOM | 0.0005 | 0.0009 | 6.084 | 56.98 | −23.255 *** |

| 601398.SS | Industrial and Commercial Bank of China | ICBC | 0.0004 | 0.0007 | 7.051 | 81.36 | −26.930 *** |

| 601818.SS | China Everbright Bank | CEB | 0.0006 | 0.0010 | 6.783 | 81.79 | −26.274 *** |

| 601939.SS | China Construction Bank Corporation | CCB | 0.0005 | 0.0008 | 6.423 | 71.23 | −25.285 *** |

| 601988.SS | Bank of China Limited | BOC | 0.0004 | 0.0009 | 7.442 | 80.89 | −24.330 *** |

| 601998.SS | China CITIC Bank Corporation Limited | CNCB | 0.0007 | 0.0012 | 4.49 | 32.83 | −26.976 *** |

| Panel C: Securities | |||||||

| 000686.SZ | Northeast Securities | NESC | 0.0011 | 0.0015 | 3.669 | 26.61 | −29.014 *** |

| 000728.SZ | Guoyuan Securities | GYSC | 0.0011 | 0.0016 | 4.179 | 32.13 | −27.186 *** |

| 000776.SZ | GF Securities | GFSC | 0.0010 | 0.0014 | 4.615 | 44.75 | −28.925 *** |

| 000783.SZ | Changjiang Securities | CJSC | 0.0010 | 0.0015 | 4.829 | 44.68 | −28.038 *** |

| 600030.SS | CITIC Securities | CITICS | 0.0009 | 0.0013 | 4.42 | 37.03 | −28.984 *** |

| 600109.SS | Sinolink Securities | SLSC | 0.0013 | 0.0017 | 3.992 | 32.11 | −29.332 *** |

| 600837.SS | Haitong Securities | HTSEC | 0.0009 | 0.0012 | 3.666 | 24.51 | −30.530 *** |

| 600999.SS | China Merchants Securities | CMSC | 0.0010 | 0.0014 | 4.636 | 41.99 | −26.952 *** |

| 601099.SS | The Pacific Securities | PSC | 0.0012 | 0.0016 | 3.737 | 26.29 | −28.644 *** |

| 601377.SS | Industrial Securities | CISC | 0.0011 | 0.0015 | 4.272 | 37.63 | −30.085 *** |

| 601688.SS | Huatai Securities | HTSC | 0.0010 | 0.0014 | 4.281 | 35.98 | −27.371 *** |

| 601788.SS | Everbright Securities | EBSCN | 0.0011 | 0.0015 | 4.251 | 35.39 | −27.821 *** |

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2023 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Li, Y.; Ni, Y.; Zheng, H.; Zhou, L. Volatility Connectedness of Chinese Financial Institutions: Evidence from a Frequency Dynamics Perspective. Systems 2023, 11, 502. https://doi.org/10.3390/systems11100502

Li Y, Ni Y, Zheng H, Zhou L. Volatility Connectedness of Chinese Financial Institutions: Evidence from a Frequency Dynamics Perspective. Systems. 2023; 11(10):502. https://doi.org/10.3390/systems11100502

Chicago/Turabian StyleLi, Yishi, Yongpin Ni, Hanxing Zheng, and Linyi Zhou. 2023. "Volatility Connectedness of Chinese Financial Institutions: Evidence from a Frequency Dynamics Perspective" Systems 11, no. 10: 502. https://doi.org/10.3390/systems11100502

APA StyleLi, Y., Ni, Y., Zheng, H., & Zhou, L. (2023). Volatility Connectedness of Chinese Financial Institutions: Evidence from a Frequency Dynamics Perspective. Systems, 11(10), 502. https://doi.org/10.3390/systems11100502