Firm Heterogeneities, Multi-Dimensional Proximities, and Systematic Dynamics of M&A Partnering: Evidences from Transitional China

Abstract

:1. Introduction

2. Literature Review and Conceptual Framework

2.1. Literature Review: Motives and Determinants of Corporate M&As

2.1.1. Corporate Heterogeneities of M&A Activities

2.1.2. Multi-Dimensional Proximities and M&A Partnering

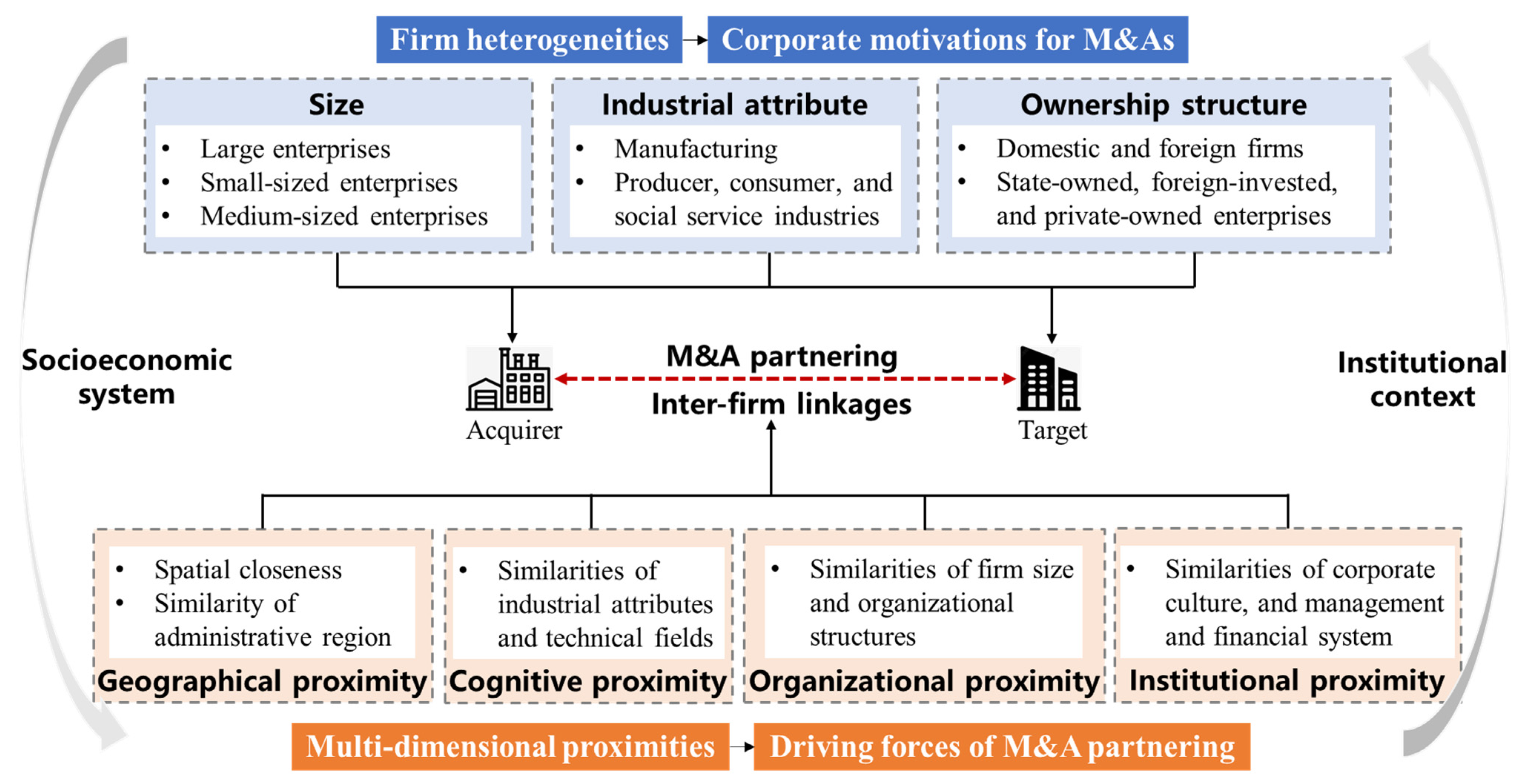

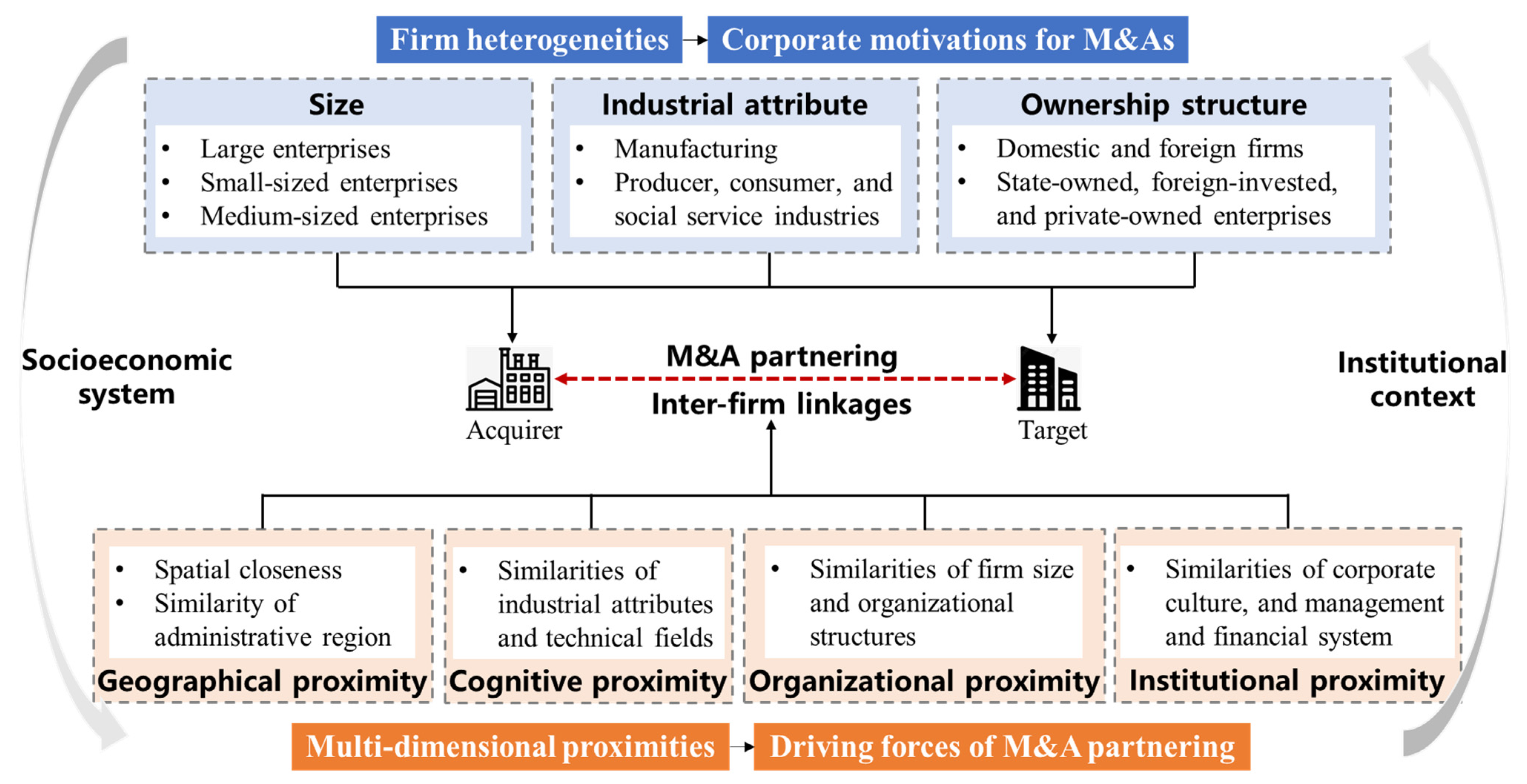

2.2. Conceptual Framework: Partnership Dynamics of M&As in the Chinese Context

3. Study Area and Data Description

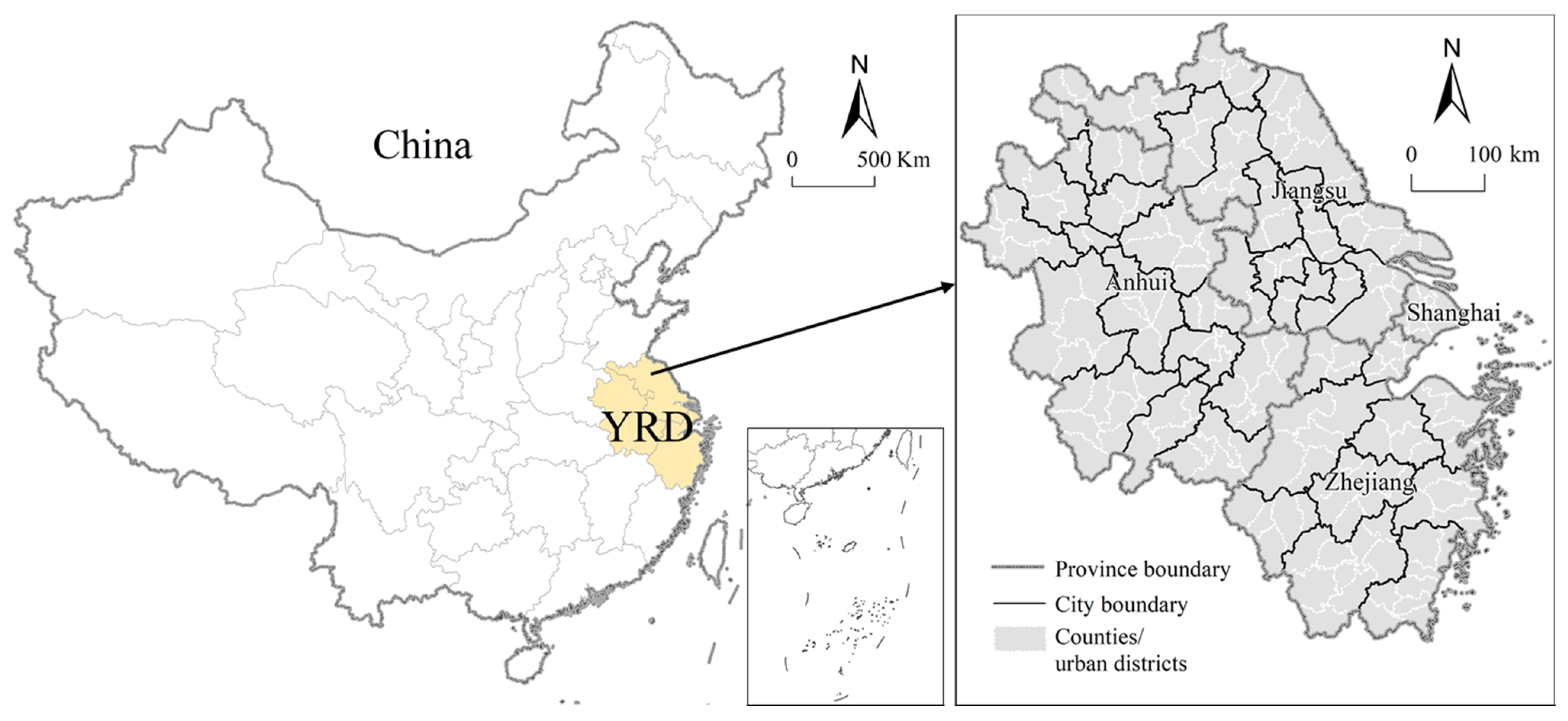

3.1. The Yangtze River Delta (YRD): An Emerging Global-City Region

3.2. Data Source and Processing

4. Model Setting and Variable Specification

5. Empirical Results

5.1. Overall Effects of Proximities on China’s Domestic M&A Partnering

5.1.1. Effects of Geographical Proximity

5.1.2. Effects of Cognitive Proximity

5.1.3. Effects of Organizational Proximity

5.1.4. Effects of Institutional Proximity

5.2. Acquiring Preferences of Corporations Differentiated by Attributes

5.2.1. Acquiring Preferences of Corporations with Different Industrial Attributes

5.2.2. Acquiring Preferences of Corporations with Different Ownership Structures

5.2.3. Acquiring Preferences of Corporations with Different Sizes

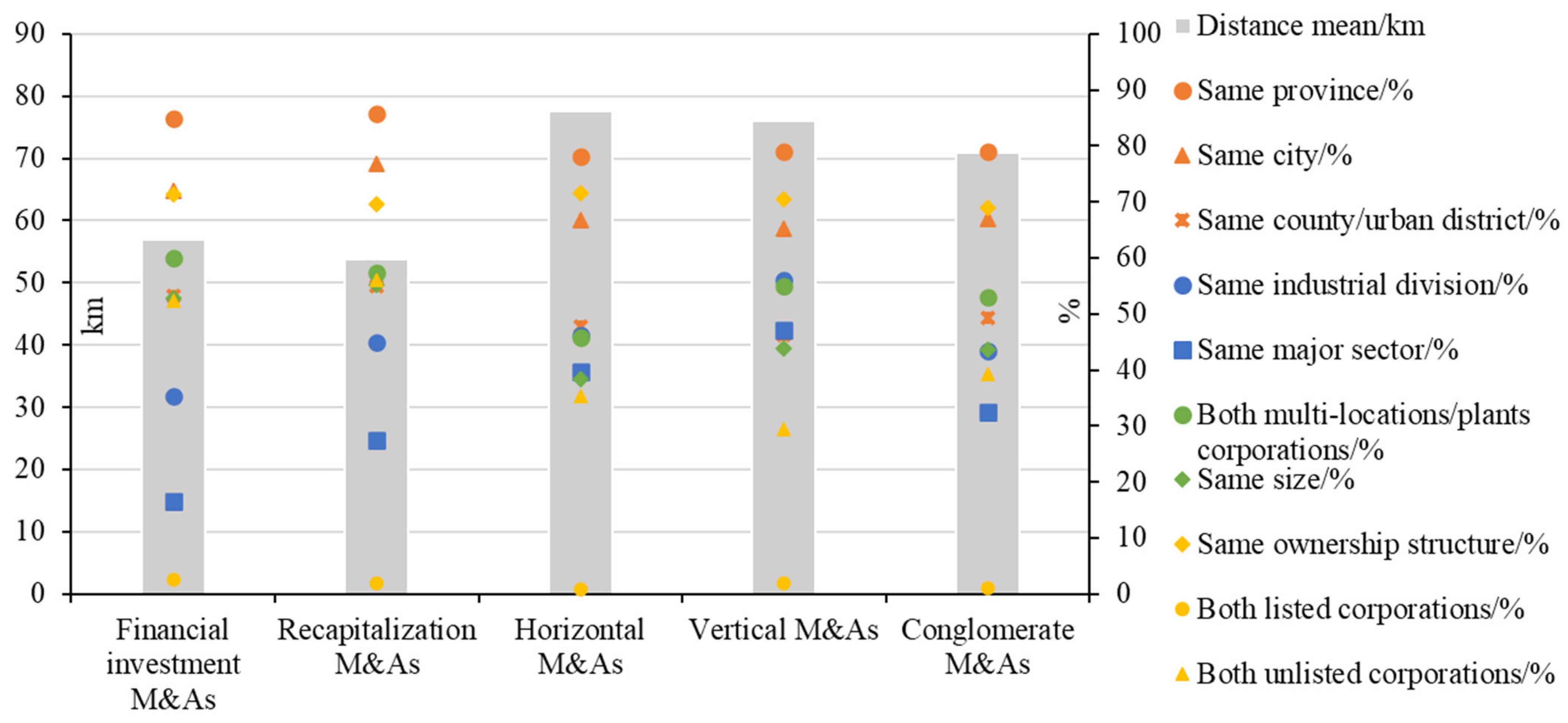

5.3. Multi-Dimensional Proximities and M&A Partnering Differentiated by Types

5.3.1. Geographical Proximity and Different Types of M&A Partnering

5.3.2. Cognitive Proximity and Different Types of M&A Partnering

5.3.3. Organizational Proximity and Different Types of M&A Partnering

5.3.4. Institutional Proximity and Different Types of M&A Partnering

6. Discussion: Proximity Dynamics of M&A Partnering in the Chinese Context

7. Conclusions

Funding

Institutional Review Board Statement

Informed Consent Statement

Data Availability Statement

Conflicts of Interest

References

- Dicken, P.; Malmberg, A. Firms in territories: A relational perspective. Econ. Geogr. 2001, 77, 345–363. [Google Scholar] [CrossRef]

- Alcácer, J.; Cantwell, J.; Piscitello, L. Internationalization in the information age: A new era for places, firms, and international business networks? J. Int. Bus. Stud. 2016, 47, 499–512. [Google Scholar] [CrossRef]

- Sigler, T.; Martinus, K.; Loginova, J. Socio-spatial relations observed in the global city network of firms. PLoS ONE 2021, 16, e0255461. [Google Scholar] [CrossRef] [PubMed]

- Isaksen, A.; Jakobsen, S.E.; Njøs, R.; Normann, R. Regional industrial restructuring resulting from individual and system agency. Innov. Eur. J. Soc. Sci. Res. 2019, 32, 48–65. [Google Scholar] [CrossRef]

- MacKinnon, D. Beyond strategic coupling: Reassessing the firm-region nexus in global production networks. J. Econ. Geogr. 2012, 12, 227–245. [Google Scholar] [CrossRef]

- Seddighi, H.R.; Mathew, S. Innovation and regional development via the firm’s core competence: Some recent evidence from North East England. J. Innov. Knowl. 2020, 5, 219–227. [Google Scholar] [CrossRef]

- Hirshleifer, J. Investment Decision under Uncertainty: Choice—Theoretic approaches. Q. J. Econ. 1965, 79, 509–536. [Google Scholar] [CrossRef]

- Chapman, K. Cross-border mergers/acquisitions: A review and research agenda. J. Econ. Geogr. 2003, 3, 309–334. [Google Scholar] [CrossRef]

- Wang, J.; Wei, Y.D.; Lin, B. Functional division and location choices of Chinese outward FDI: The case of ICT firms. Environ. Plan. A Econ. Space 2021, 53, 937–957. [Google Scholar] [CrossRef]

- Knight, E.; Kumar, V.; Wójcik, D.; O’Neill, P. The competitive advantage of regions: Economic geography and strategic management intersections. Reg. Stud. 2020, 54, 591–595. [Google Scholar] [CrossRef]

- Brenes, E.R.; Ciravegna, L.; Woodside, A.G. Constructing useful models of firms’ heterogeneities in implemented strategies and performance outcomes. Ind. Mark. Manag. 2017, 62, 17–35. [Google Scholar] [CrossRef]

- Myles Shaver, J.; Flyer, F. Agglomeration economies, firm heterogeneity, and foreign direct investment in the United States. Strateg. Manag. J. 2000, 20, 1175–1193. [Google Scholar] [CrossRef]

- Seth, A.; Song, K.P.; Pettit, R. Synergy, managerialism or hubris? An empirical examination of motives for foreign acquisitions of US firms. J. Int. Bus. Stud. 2000, 31, 387–405. [Google Scholar] [CrossRef]

- Harré, M.S.; Eremenko, A.; Glavatskiy, K.; Hopmere, M.; Pinheiro, L.; Watson, S.; Crawford, L. Complexity Economics in a Time of Crisis: Heterogeneous Agents, Interconnections, and Contagion. Systems 2021, 9, 73. [Google Scholar] [CrossRef]

- Görg, H. Analysing foreign market entry—The choice between greenfield investment and acquisitions. Econ. Tech. Pap. 2000, 27, 165–181. [Google Scholar] [CrossRef] [Green Version]

- Raff, H.; Ryan, M.; Stähler, F. The choice of market entry mode: Greenfield investment, M&A and joint venture. Int. Rev. Econ. Financ. 2009, 18, 3–10. [Google Scholar]

- Harms, P.; Méon, P.G. Good and useless FDI: The growth effects of greenfield investment and mergers and acquisitions. Rev. Int. Econ. 2018, 26, 37–59. [Google Scholar] [CrossRef]

- Hansen, U.E.; Fold, N.; Hansen, T. Upgrading to lead firm position via international acquisition: Learning from the global biomass power plant industry. J. Econ. Geogr. 2016, 16, 131–153. [Google Scholar] [CrossRef]

- Moretti, F.; Biancardi, D. Inbound open innovation and firm performance. J. Innov. Knowl. 2020, 5, 1–19. [Google Scholar] [CrossRef]

- Chapman, K.; Edmond, H. Mergers/acquisitions and restructuring in the EU chemical industry: Patterns and implications. Reg. Stud. 2000, 34, 753–767. [Google Scholar] [CrossRef]

- Boschma, R.; Hartog, M. Merger and Acquisition Activity as Driver of Spatial Clustering: The Spatial Evolution of the Dutch Banking Industry, 1850–1993. Econ. Geogr. 2014, 90, 247–266. [Google Scholar] [CrossRef] [Green Version]

- Leigh, R.; North, D.J. Regional aspects of acquisition activity in British manufacturing industry. Reg. Stud. 1978, 12, 227–245. [Google Scholar] [CrossRef]

- Green, M.B. Mergers and acquisitions. In The International Encyclopedia of Geography; Richardson, D., Castree, N., Goodchild, M.F., Kobayashi, A., Liu, W., Marston, R.A., Eds.; John Wiley & Sons: New York, NY, USA, 2018. [Google Scholar]

- Rao, N.V.; Reddy, K. The impact of the global financial crisis on cross-border mergers and acquisitions: A continental and industry analysis. Eurasian Bus. Rev. 2015, 5, 309–341. [Google Scholar] [CrossRef]

- Gunessee, S.; Hu, S. Chinese cross-border mergers and acquisitions in the developing world: Is Africa unique? Thunderbird Int. Bus. Rev. 2021, 63, 27–41. [Google Scholar] [CrossRef]

- Ellwanger, N.; Boschma, R. Who Acquires Whom? The Role of Geographical Proximity and Industrial Relatedness in Dutch Domestic M&As between 2002 and 2008. Tijdschr. Econ. Soc. Geogr. 2015, 106, 608–624. [Google Scholar]

- Schildt, H.A.; Laamanen, T. Who buys whom: Information environments and organizational boundary spanning through acquisitions. Strateg. Organ. 2006, 4, 111–133. [Google Scholar] [CrossRef]

- Böckerman, P.; Lehto, E. Geography of Domestic Mergers and Acquisitions (M&As): Evidence from Matched Firm-level Data. Reg. Stud. 2006, 40, 847–860. [Google Scholar]

- Zademach, H.-M.; Rodríguez-Pose, A. Cross-Border M&As and the Changing Economic Geography of Europe. Eur. Plan. Stud. 2009, 17, 765–789. [Google Scholar]

- Di Guardo, M.C.; Marrocu, E.; Paci, R. The Concurrent Impact of Cultural, Political, and Spatial Distances on International Mergers and Acquisitions. World Econ. 2016, 39, 824–858. [Google Scholar] [CrossRef]

- Boschma, R.; Marrocu, E.; Paci, R. Symmetric and asymmetric effects of proximities. The case of M&A deals in Italy. J. Econ. Geogr. 2016, 16, 505–535. [Google Scholar]

- Kvĕtoň, V.; Bĕlohradský, A.; Blažek, J. The variegated role of proximities in acquisitions by domestic and international companies in different phases of economic cycles. Pap. Regi. Sci. 2020, 99, 583–602. [Google Scholar] [CrossRef]

- Green, M.B.; Cromley, R.G. The horizontal merger: Its motives and spatial employment impacts. Econ. Geogr. 1982, 58, 358–370. [Google Scholar] [CrossRef]

- Rozen-Bakher, Z. Comparison of merger and acquisition (M&A) success in horizontal, vertical and conglomerate M&As: Industry sector vs. services sector. Serv. Ind. J. 2018, 38, 492–518. [Google Scholar]

- Duysters, G.; Cloodt, M.; Schoenmakers, W.; Jacob, J. Internationalisation efforts of Chinese and Indian companies: An empirical perspective. Tijdschr. Econ. Soc. Geogr. 2015, 106, 169–186. [Google Scholar] [CrossRef]

- Lebedev, S.; Peng, M.W.; Xie, E.; Stevens, C.E. Mergers and acquisitions in and out of emerging economies. J. World Bus. 2015, 50, 651–662. [Google Scholar] [CrossRef]

- Buckley, P.J.; Yu, P.; Liu, Q.; Munjal, S.; Tao, P. The institutional influence on the location strategies of multinational enterprises from emerging economies: Evidence from China’s cross-border mergers and acquisitions. Manag. Organ. Rev. 2016, 12, 425–448. [Google Scholar] [CrossRef] [Green Version]

- Bruhn, N.C.P.; Calegário, C.L.L.; de Melo Carvalho, F.; Campos, R.S.; dos Santos, A.C. Mergers and acquisitions in Brazilian industry: A study of spillover effects. Int. J. Product. Perform. Manag. 2017, 66, 51–77. [Google Scholar] [CrossRef]

- Zheng, Y.; Yan, D.; Ren, B. Institutional distance, firm heterogeneities, and FDI location choice of EMNEs. Nankai Bus. Rev. Int. 2016, 7, 192–215. [Google Scholar] [CrossRef]

- Hossain, M.S. Merger & Acquisitions (M&As) as an important strategic vehicle in business: Thematic areas, research avenues & possible suggestions. J. Econ. Bus. 2021, 116, 106004. [Google Scholar]

- Ascani, A. The takeover selection decisions of multinational enterprises: Empirical evidence from European target firms. J. Econ. Geogr. 2018, 18, 1227–1252. [Google Scholar] [CrossRef]

- Kim, S.J. Networks, scale, and transnational corporations: The case of the South Korean seed industry. Econ. Geogr. 2006, 82, 317–338. [Google Scholar] [CrossRef]

- Clark, G.L. Costs and prices, corporate competitive strategies and regions. Environ. Plan. A 1993, 25, 5–26. [Google Scholar] [CrossRef]

- Hussinger, K. On the importance of technological relatedness: SMEs versus large acquisition targets. Technovation 2010, 30, 57–64. [Google Scholar] [CrossRef]

- Rodríguez-Pose, A.; Zademach, H.M. Industry dynamics in the German merger and acquisitions market. Tijdschr. Econ. Soc. Geogr. 2006, 97, 296–313. [Google Scholar] [CrossRef] [Green Version]

- Mariotti, S.; Piscitello, L.; Elia, S. Local externalities and ownership choices in foreign acquisitions by multinational enterprises. Econ. Geogr. 2014, 90, 187–211. [Google Scholar] [CrossRef]

- Barattieri, A.; Borchert, I.; Mattoo, A. Cross-border mergers and acquisitions in services: The role of policy and industrial structure. Can. J. Econ. 2016, 49, 1470–1501. [Google Scholar] [CrossRef] [Green Version]

- Weitzel, U.; McCarthy, K.J. Theory and evidence on mergers and acquisitions by small and medium enterprises. Int. J. Entrep. Innov. Manag. 2011, 14, 248–275. [Google Scholar] [CrossRef] [Green Version]

- Balland, P.; Boschma, R.; Frenken, K. Proximity and Innovation: From Statics to Dynamics. Reg. Stud. 2015, 49, 907–920. [Google Scholar] [CrossRef]

- Caragliu, A.; Nijkamp, P. Space and knowledge spillovers in European regions: The impact of different forms of proximity on spatial knowledge diffusion. J. Econ. Geogr. 2016, 16, 749–774. [Google Scholar] [CrossRef]

- Boschma, R. Proximity and Innovation: A Critical Assessment. Reg. Stud. 2005, 39, 61–74. [Google Scholar] [CrossRef]

- Chakrabarti, A.; Mitchell, W. The persistent effect of geographic distance in acquisition target selection. Organ. Sci. 2013, 24, 1805–1826. [Google Scholar] [CrossRef] [Green Version]

- Wu, J.; Wei, Y.D.; Chen, W. Spatial proximity, localized assets, and the changing geography of domestic mergers and acquisitions in transitional China. Growth Chang. 2020, 51, 954–976. [Google Scholar] [CrossRef]

- PwC 2021. China M&A 2020 Review and 2021 Outlook. Available online: https://www.pwccn.com/en/services/deals-m-and-a/publications/ma-2020-review-and-2021-outlook.html (accessed on 1 October 2021).

- Wei, G. Ownership structure, corporate governance and company performance in China. Asia Pac. Bus. Rev. 2007, 13, 519–545. [Google Scholar] [CrossRef]

- Li, L.; McMurray, A.; Sy, M.; Xue, J. Corporate ownership, efficiency and performance under state capitalism: Evidence from China. J. Policy Model. 2018, 40, 747–766. [Google Scholar] [CrossRef]

- Wei, Y.H.D. Network linkages and local embeddedness of foreign ventures in China: The case of Suzhou municipality. Reg. Stud. 2015, 49, 287–299. [Google Scholar] [CrossRef]

- Wei, Y.D. Decentralization, marketization, and globalization: The triple processes underlying regional development in China. Asian Geogr. 2001, 20, 7–23. [Google Scholar] [CrossRef]

- Wei, Y.D.; Bi, X.; Wang, M.; Ning, Y. Globalization, economic restructuring, and locational trajectories of software firms in shanghai. Prof. Geogr. 2016, 68, 211–226. [Google Scholar] [CrossRef]

- He, C.; Pan, F.; Chen, T. Research progress of industrial geography in China. J. Geogr. Sci. 2016, 26, 1057–1066. [Google Scholar] [CrossRef]

- Fan, G.; Ma, G.; Wang, X. Institutional reform and economic growth of China: 40-year progress toward marketization. Acta Oecon. 2019, 69, 7–20. [Google Scholar] [CrossRef]

- Chen, W.; Yenneti, K.; Wei, Y.D.; Yuan, F.; Wu, J.; Gao, J. Polycentricity in the Yangtze River Delta Urban Agglomeration (YRDUA): More cohesion or more disparities? Sustainability 2019, 11, 3106. [Google Scholar] [CrossRef] [Green Version]

- Ye, C.; Zhu, J.; Li, S.; Yang, S.; Chen, M. Assessment and analysis of regional economic collaborative development within an urban agglomeration: Yangtze River Delta as a case study. Habitat Int. 2019, 83, 20–29. [Google Scholar] [CrossRef]

- Wu, J.; Wei, Y.; Li, Q.; Yuan, F. Economic transition and changing location of manufacturing industry in china: A study of the yangtze river delta. Sustainability 2018, 10, 2624. [Google Scholar] [CrossRef] [Green Version]

{kind=link}

{kind=link}

{kind=link}

| Category | Description | Abbreviation | |

|---|---|---|---|

| Geographical proximity | Spatial distance | Spatial distance (km) calculated by ArcGIS between the acquirer and the target | LnDistance |

| Same province | Dummy variable, 1 when the acquirer and the target are co-located in the same province | Intra_P | |

| Same city | Dummy variable, 1 when the acquirer and the target are co-located in the same city | Intra_C | |

| Same county/urban district | Dummy variable, 1 when the acquirer and the target are co-located in the same county or urban district | Intra_D | |

| Cognitive proximity | Same industrial division | Dummy variable, 1 when the highest degree of industrial and technical relatedness is at industrial division | Inra_I |

| Same major sector | Dummy variable, 1 when the highest degree of industrial and technical relatedness is at major sector | Intra_G | |

| Organizational proximity | Same locational pattern | Dummy variable, 1 when both the acquirer and the target have at least one outside investment event | Multi_L |

| Same size | Dummy variable, 1 when the acquirer and the target are grouped in the same size measured by registered capital | Same_S | |

| Institutional proximity | Same ownership structure | Dummy variable, 1 when the acquirer and the target are featured by the same ownership structure (i.e., SOEs, POEs, and FIEs) | Same_Ins |

| Same listed status | Dummy variable, 1 when both the acquirer and the target are listed corporations | List | |

| Dummy variable, 1 when both the acquirer and the target are unlisted firms | Nonlist | ||

| Category | M&A Partnerings | M&A Non-Partnerings | |

|---|---|---|---|

| Geographical proximity | Distance mean | 69.83 km | 187.43 km |

| Same province | 80.34% | 29.34% | |

| Same city | 68.00% | 14.78% | |

| Same county/urban district | 49.01% | 5.44% | |

| Cognitive proximity | Same industrial division | 48.88% | 32.70% |

| Same major sector | 37.16% | 17.85% | |

| Organizational proximity | Same locational pattern | 56.04% | 57.28% |

| Same size | 46.39% | 41.79% | |

| Institutional proximity | Same ownership structure | 70.26% | 69.99% |

| Both listed | 1.77% | 3.78% | |

| Both unlisted | 38.08% | 43.91% | |

| Number of M&A deals | 5543 | 1,890,104 | |

| Variables | 1996–2016 | 1996–2000 | 2001–2005 | 2006–2010 | 2011–2016 |

|---|---|---|---|---|---|

| LnDistance | −0.855 *** | −0.559 *** | −0.812 *** | −0.903 *** | −0.886 *** |

| Intra_P | (1.128 ***) | (1.492 ***) | (1.411 ***) | (1.440 ***) | (0.978 ***) |

| Intra_C | (0.731 ***) | (1.648 ***) | (0.629 ***) | (0.750 ***) | (0.786 ***) |

| Intra_D | (1.496 ***) | (0.631 ***) | (1.435 ***) | (1.441 ***) | (1.597 ***) |

| Inra_I | 0.601 *** | 0.620 *** | 0.594 *** | 0.794 *** | 0.518 *** |

| Intra_G | (0.981 ***) | (0.694***) | (0.972 ***) | (1.126 ***) | (0.934 ***) |

| Multi_L | −0.077 ** | 0.079 | −0.194 * | −0.128 * | −0.101 ** |

| Same_S | 0.100 *** | 0.001 | 0.139 | 0.144 * | 0.094 ** |

| Same_Ins | 0.401 *** | 0.579 *** | 0.352 *** | 0.382 *** | 0.357 *** |

| List | −1.515 *** | −1.124 ** | −1.247 *** | −1.564 *** | −1.400 *** |

| Nonlist | −0.546 *** | −0.231 | −0.306 *** | −0.471 *** | −0.626 *** |

| _cons | 1.627 *** (−3.131 ***) | −0.106 (−3.043 ***) | 1.324 (−3.399 ***) | 1.643 *** (−3.504 ***) | 1.945 *** (−2.963 ***) |

| No. of partnerings | 5543 | 124 | 696 | 1413 | 3310 |

| No. of non-partnerings | 27,715 | 620 | 3480 | 7065 | 16,550 |

| -Log likelihood | 11,137.1 (11,050.5) | 289.5 (299.7) | 1395.1 (1367.5) | 2661.6 (2658.4) | 6730.7 (6658.4) |

| LR chi2 | 7700.7 *** (7874.0 ***) | 91.5 *** (71.0 ***) | 978.3 *** (1033.6 ***) | 2316.5 *** (2322.9 ***) | 4434.8 *** (4579.6 ***) |

| Pseudo R2 | 0.257 (0.263) | 0.137 (0.106) | 0.260 (0.274) | 0.303 (0.304) | 0.248 (0.256) |

| 1996–2000 | 2001–2005 | 2006–2010 | 2011–2016 | |

|---|---|---|---|---|

| Distance mean | 45.69 km | 53.37 km | 56.30 km | 79.99 km |

| Same province | 86.29% | 85.26% | 85.22% | 76.92% |

| Same city | 83.06% | 76.39% | 74.47% | 62.84% |

| Same county/urban district | 44.35% | 52.65% | 52.48% | 46.89% |

| Same industrial division | 43.55% | 45.06% | 53.89% | 47.70% |

| Same major sector | 30.65% | 34.48% | 42.50% | 35.65% |

| Acquirer services, target manufacturing | 25.00% | 17.60% | 13.65% | 11.45% |

| Acquirer manufacturing, target producer services | 0.81% | 4.43% | 5.30% | 14.83% |

| Acquirer manufacturing, target consumer and social services | 8.06% | 8.15% | 5.59% | 6.10% |

| Both multi-locations/plants corporations | 6.45% | 63.38% | 56.58% | 56.07% |

| Same size | 36.29% | 48.78% | 51.49% | 44.05% |

| Acquirer large-sized, target medium-sized | 37.90% | 29.61% | 30.13% | 36.65% |

| Acquirer large-sized, target small-sized | 15.32% | 9.01% | 8.13% | 10.15% |

| Acquirer SMEs, target large-sized | 0.00% | 7.87% | 6.08% | 4.56% |

| Same ownership structure | 54.84% | 64.23% | 62.80% | 75.26% |

| Both listed corporations | 6.45% | 2.58% | 1.70% | 1.45% |

| Acquirer listed, target unlisted | 50.81% | 38.20% | 44.48% | 59.61% |

| Manufacturing | Producer Services | Consumer and Social Services | SOEs | POEs | FIEs | Large-Sized | Medium-Sized | Small-Sized | |

|---|---|---|---|---|---|---|---|---|---|

| Distance mean | 83.27 km | 61.08 km | 57.73 km | 32.64 km | 69.26 km | 75.59 km | 72.61 km | 55.37 km | 57.87 km |

| Same province | 78.74% | 80.52% | 82.90% | 94.69% | 80.35% | 77.22% | 79.62% | 83.96% | 84.36% |

| Same city | 62.86% | 71.60% | 71.62% | 87.55% | 66.78% | 67.41% | 66.79% | 74.26% | 73.74% |

| Same county/urban district | 48.50% | 49.61% | 50.76% | 61.22% | 50.63% | 43.34% | 48.18% | 53.64% | 51.40% |

| Same industrial division | 51.78% | 47.11% | 50.04% | 40.41% | 49.10% | 54.44% | 48.66% | 50.67% | 47.49% |

| Same major sector | 51.78% | 23.24% | 36.79% | 25.51% | 37.10% | 46.26% | 37.71% | 35.98% | 27.93% |

| Acquirer services, target manufacturing | — | 25.89% | 16.83% | 22.86% | 14.49% | 8.06% | 11.88% | 19.14% | 18.99% |

| Acquirer manufacturing, target producer services | 28.44% | — | — | 3.27% | 9.88% | 11.80% | 12.27% | 2.96% | 5.03% |

| Acquirer manufacturing, target consumer and social services | 16.55% | — | — | 3.27% | 5.46% | 9.23% | 6.95% | 3.10% | 2.23% |

| Both multi-locations/plants corporations | 51.78% | 63.40% | 50.94% | 64.29% | 55.29% | 52.80% | 56.82% | 50.94% | 57.54% |

| Same size | 42.08% | 49.81% | 45.93% | 66.73% | 44.29% | 45.91% | 47.51% | 45.28% | 22.35% |

| Acquirer large-sized, target medium-sized | 41.80% | 27.77% | 32.59% | 23.47% | 30.41% | 37.50% | 40.96% | — | — |

| Acquirer large-sized, target small-sized | 11.27% | 8.39% | 8.50% | 4.90% | 8.84% | 10.86% | 11.53% | — | — |

| Acquirer SMEs, target large-sized | 2.47% | 7.47% | 7.07% | 2.65% | 8.76% | 3.50% | — | 32.61% | 27.37% |

| Same ownership structure | 70.66% | 67.89% | 74.49% | 9.80% | 88.43% | 18.22% | 68.37% | 79.38% | 81.56% |

| Both listed corporations | 1.95% | 1.45% | 1.43% | 0.41% | 0.62% | 3.04% | 2.12% | 0.00% | 0.00% |

| Both unlisted corporations | 21.49% | 51.83% | 45.57% | 58.16% | 52.75% | 23.95% | 27.52% | 90.97% | 91.62% |

| Acquirer listed, target unlisted | 74.18% | 33.08% | 47.72% | 14.69% | 38.29% | 71.14% | 63.22% | 1.35% | 0.00% |

| Acquirer unlisted, target listed | 2.38% | 13.65% | 5.28% | 26.73% | 8.34% | 1.87% | 7.14% | 7.68% | 8.38% |

| Variables | Financial Investment M&As | Recapitalization M&As | Horizontal M&As | Vertical M&As | Conglomerate M&As |

|---|---|---|---|---|---|

| LnDistance | −0.858 *** | −0.988 *** | −0.868 *** | −0.849 *** | −0.829 *** |

| Intra_P | (1.571 ***) | (1.272 ***) | (1.060 ***) | (1.116 ***) | (1.114 ***) |

| Intra_C | (0.278) | (1.099 ***) | (0.807 ***) | (0.716 ***) | (0.583 ***) |

| Intra_D | (1.630 ***) | (1.464 ***) | (1.416 ***) | (1.399 ***) | (1.563 ***) |

| Inra_I | 0.085 | 0.402 *** | 0.519 *** | 0.864 *** | 0.462 *** |

| Intra_G | (0.092) | (0.619 ***) | (1.118 ***) | (1.359 ***) | (0.857 ***) |

| Multi_L | −0.036 | −0.084 | −0.390 ** | −0.158 *** | −0.025 |

| Same_S | 0.402 *** | 0.544 *** | −0.075 | 0.045 | −0.094 |

| Same_Ins | 0.613 *** | 0.513 *** | 0.321 * | 0.342 *** | 0.340 *** |

| List | −0.494 | −1.051 *** | −1.964 ** | −1.588 *** | −1.917 *** |

| Nonlist | 0.147 | 0.323 *** | −0.848 *** | −1.009 *** | −0.529 *** |

| _cons | 1.109 *** (−3.122 ***) | 1.446 *** (−3.369 ***) | 2.205 *** (−3.117 ***) | 1.763 *** (−3.215 ***) | 1.681 *** (−3.028 ***) |

| No. of partnerings | 465 | 792 | 247 | 2522 | 1311 |

| No. of non-partnerings | 2325 | 3960 | 1235 | 12,610 | 6555 |

| -Log likelihood | 952.4 (945.9) | 1458.4 (1469.2) | 502.3 (492.6) | 4959.4 (4970.1) | 2686.6 (2678.5) |

| LR chi2 | 625.6 *** (638.6 ***) | 1367.2 *** (1345.5 ***) | 331.0 *** (350.2) | 3716.9 *** (3695.6 ***) | 1718.7 *** (1734.8 ***) |

| Pseudo R2 | 0.247 (0.252) | 0.319 (0.314) | 0.249 (0.262) | 0.273 (0.271) | 0.242 (0.245) |

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2022 by the author. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Wu, J. Firm Heterogeneities, Multi-Dimensional Proximities, and Systematic Dynamics of M&A Partnering: Evidences from Transitional China. Systems 2022, 10, 32. https://doi.org/10.3390/systems10020032

Wu J. Firm Heterogeneities, Multi-Dimensional Proximities, and Systematic Dynamics of M&A Partnering: Evidences from Transitional China. Systems. 2022; 10(2):32. https://doi.org/10.3390/systems10020032

Chicago/Turabian StyleWu, Jiawei. 2022. "Firm Heterogeneities, Multi-Dimensional Proximities, and Systematic Dynamics of M&A Partnering: Evidences from Transitional China" Systems 10, no. 2: 32. https://doi.org/10.3390/systems10020032

APA StyleWu, J. (2022). Firm Heterogeneities, Multi-Dimensional Proximities, and Systematic Dynamics of M&A Partnering: Evidences from Transitional China. Systems, 10(2), 32. https://doi.org/10.3390/systems10020032