An ALE Meta-Analysis on Investment Decision-Making

Abstract

1. Introduction

2. Methods

2.1. Eligibility Criteria

2.2. Information Sources and Search

2.3. Data Collection Process

2.4. Meta-Analysis of Brain Activation Coordinates

2.5. Visualization

3. Results

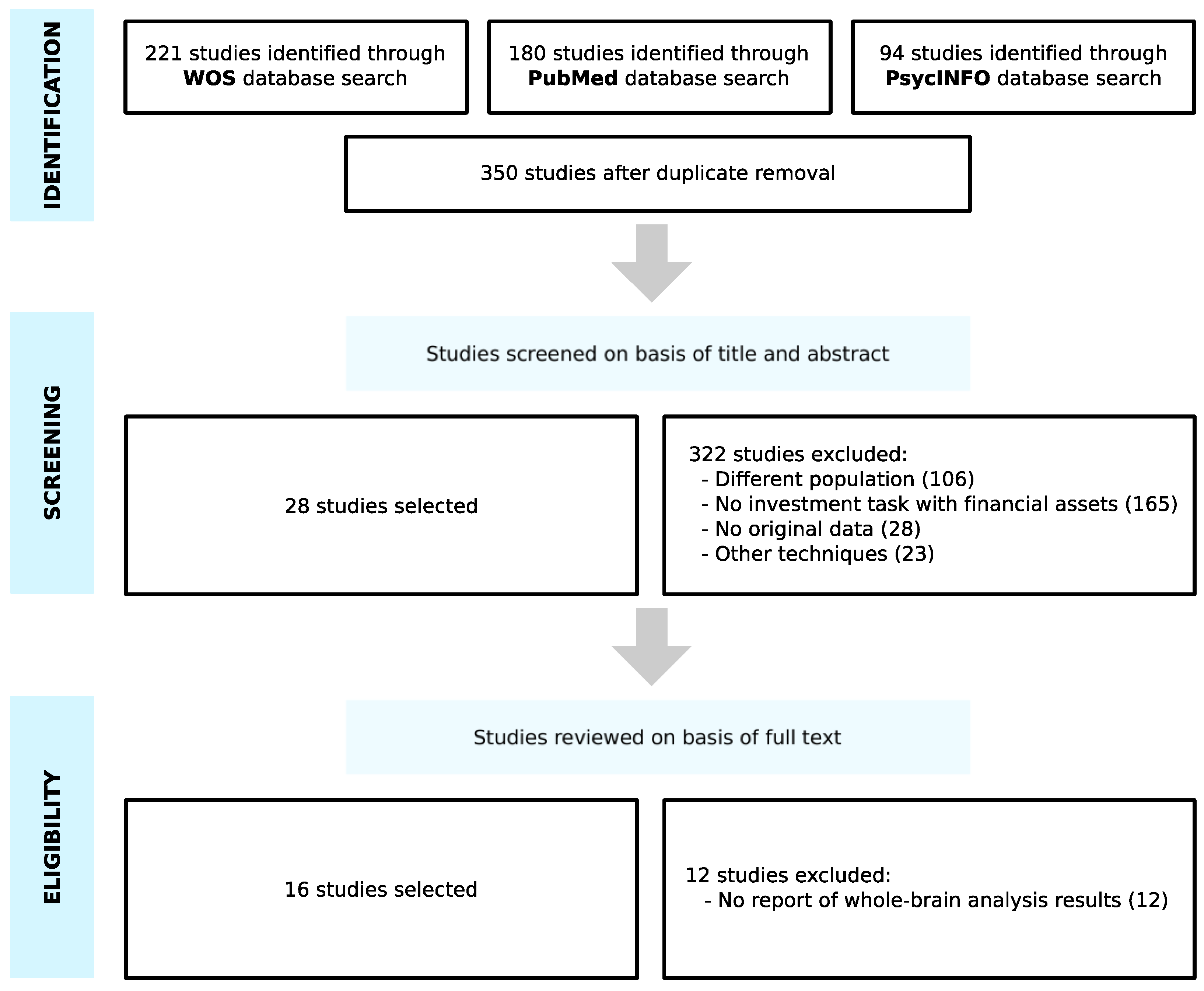

3.1. Study Selection

3.2. Study Characteristics

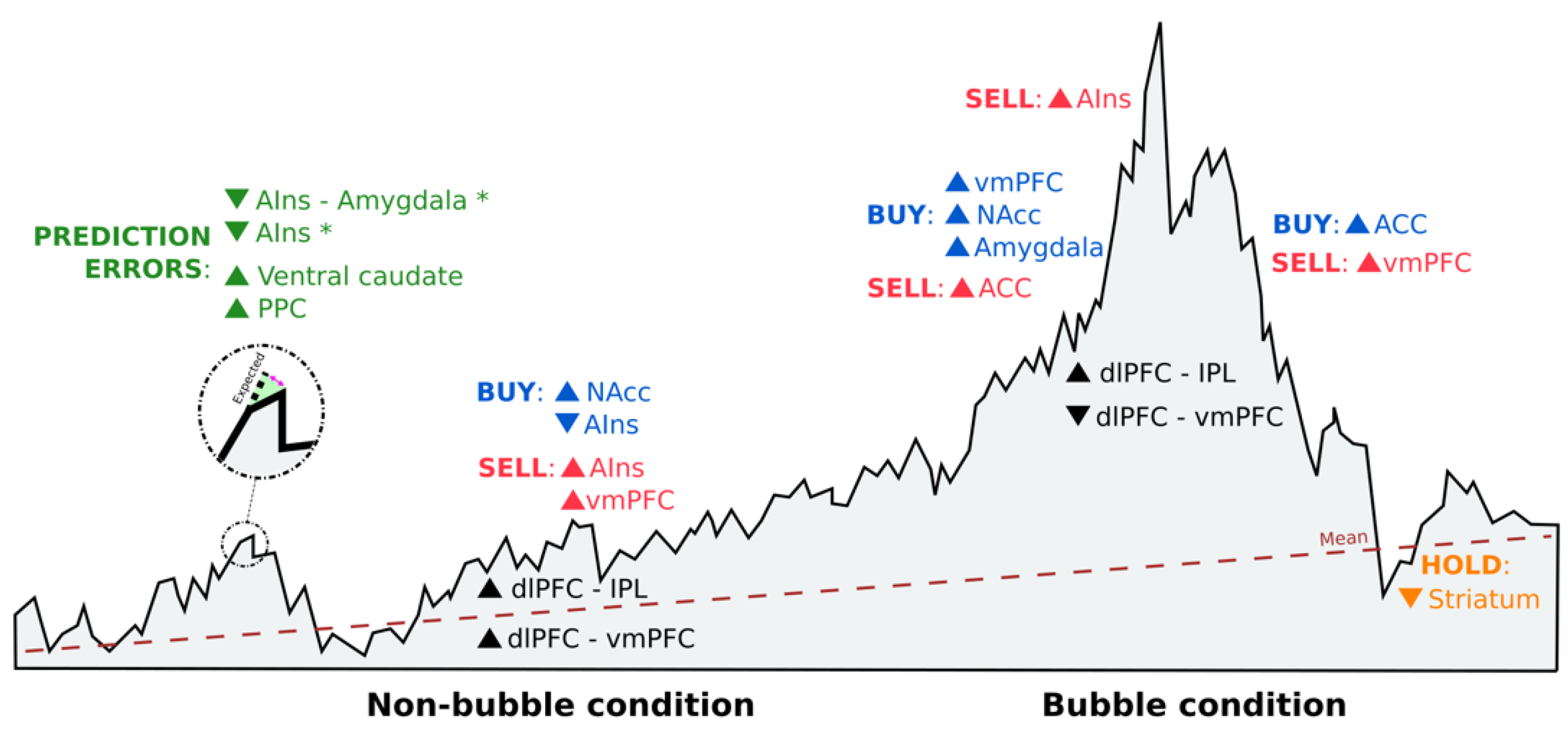

3.3. Study Results

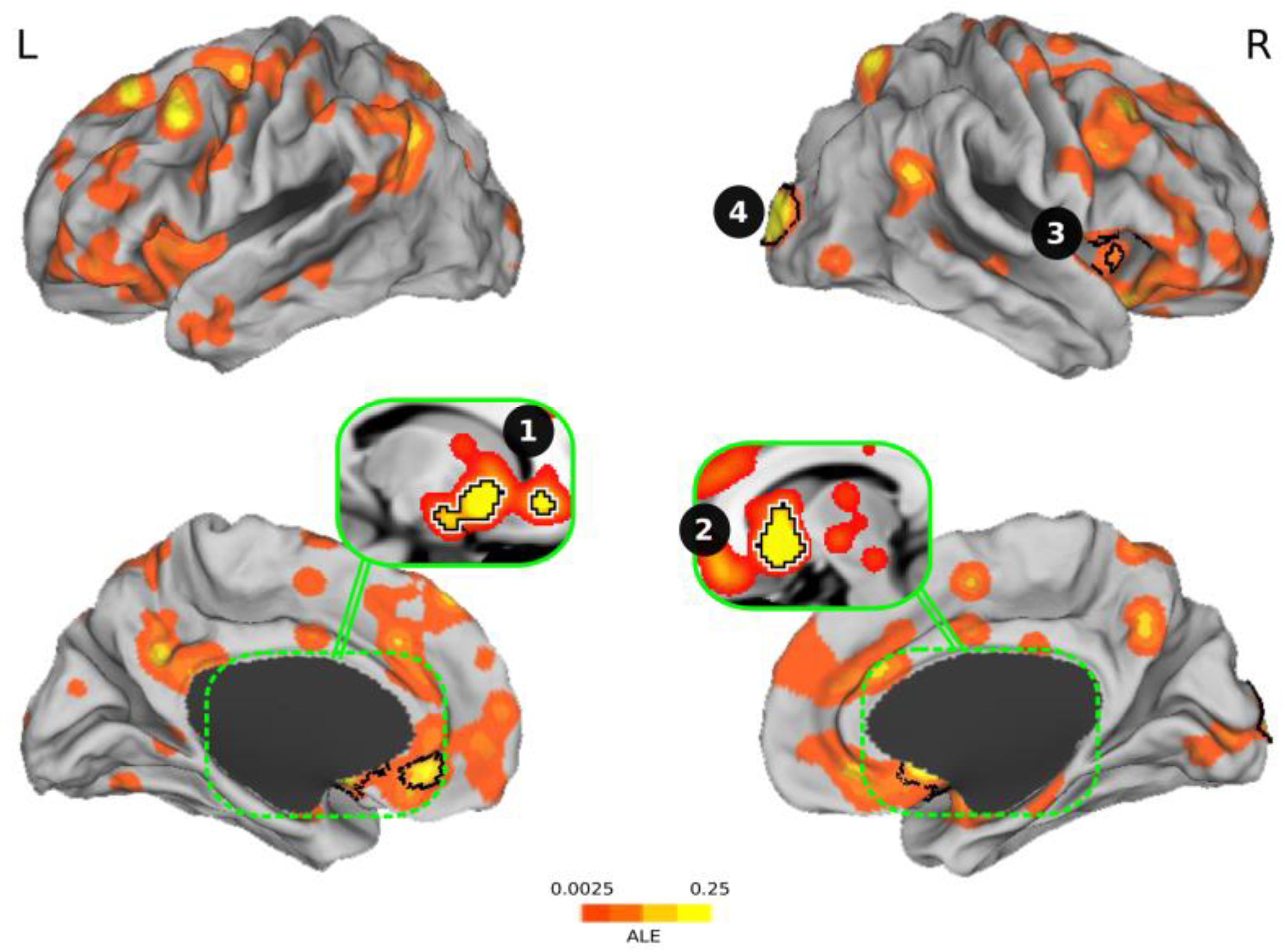

3.4. Meta-analysis of Brain Activation Results

4. Discussion

5. Conclusions

Author Contributions

Funding

Institutional Review Board Statement

Informed Consent Statement

Data Availability Statement

Conflicts of Interest

Code Availability

Appendix A

References

- Buffett, W.E. Preface. In The Intelligent Investor; Graham, B., Ed.; HarperCollins: New York, NY, USA, 2003; p. ix. [Google Scholar]

- Schultz, W.; Dayan, P.; Montague, R. A neural substrate of prediction and reward. Science 1997, 275, 1593–1599. [Google Scholar] [CrossRef]

- Chew, B.; Hauser, T.U.; Papoutsi, M.; Magerkurth, J.; Dolan, R.J.; Rutledge, R.B. Endogenous fluctuations in the dopaminergic midbrain drive behavioral choice variability. Proc. Natl. Acad. Sci. USA 2019, 116, 18732–18737. [Google Scholar] [CrossRef] [PubMed]

- Haber, S.N. Anatomy and connectivity of the reward circuit. In Decision Neuroscience: An Integrative Perspective; Dreher, J.C., Tremblay, L., Eds.; Academic Press: Cambridge, MA, USA, 2017; pp. 3–19. [Google Scholar]

- McClure, S.M.; Laibson, D.I.; Loewenstein, G.; Cohen, J.D. Separate neural systems value immediate and delayed monetary rewards. Science 2004, 306, 503–507. [Google Scholar] [CrossRef]

- Diekhof, E.K.; Kaps, L.; Falkai, P.; Gruber, O. The role of the human ventral striatum and the medial orbitofrontal cortex in the representation of reward magnitude—An activation likelihood estimation meta-analysis of neuroimaging studies of passive reward expectancy and outcome processing. Neuropsychologia 2012, 50, 1252–1266. [Google Scholar] [CrossRef]

- Kennerley, S.W.; Wallis, J.D. Reward-dependent modulation of working memory in lateral prefrontal cortex. J. Neurosci. 2009, 29, 3259–3270. [Google Scholar] [CrossRef]

- Wisniewski, D.; Reverberi, C.; Momennejad, I.; Kahnt, T.; Haynes, J.D. The role of the parietal cortex in the representation of task-reward associations. J. Neurosci. 2015, 35, 12355–12365. [Google Scholar] [CrossRef] [PubMed]

- Levy, D.J.; Glimcher, P.W. The root of all value: A neural common currency for choice. Curr. Opin. Neurobiol. 2012, 22, 1027–1038. [Google Scholar] [CrossRef] [PubMed]

- Basten, U.; Biele, G.; Heekeren, H.R.; Fiebach, C.J. How the brain integrates costs and benefits during decision making. Proc. Natl. Acad. Sci. USA 2010, 107, 21767–21772. [Google Scholar] [CrossRef] [PubMed]

- Kim, H.; Shimojo, S.; O’Doherty, J.P. Overlapping responses for the expectation of juice and money rewards in human ventromedial prefrontal cortex. Cereb. Cortex 2011, 21, 769–776. [Google Scholar] [CrossRef]

- Pochon, J.-B.; Riis, J.; Sanfey, A.G.; Nystrom, L.E.; Cohen, J.D. Functional imaging of decision conflict. J. Neurosci. 2008, 28, 3468–3473. [Google Scholar] [CrossRef]

- Miendlarzewska, E.A.; Kometer, M.; Preuschoff, K. Neurofinance. Organ Res. Methods 2019, 22, 196–222. [Google Scholar] [CrossRef]

- Preuschoff, K.; Quartz, S.R.; Bossaerts, P. Human insula activation reflects risk prediction errors as well as risk. J. Neurosci. 2008, 28, 2745–2752. [Google Scholar] [CrossRef] [PubMed]

- Hsu, M.; Bhatt, M.; Adolphs, R.; Tranel, D.; Camerer, C.F. Neural systems responding to degrees of uncertainty in human decision-making. Science 2005, 310, 1680–1683. [Google Scholar] [CrossRef]

- FeldmanHall, O.; Glimcher, P.; Baker, A.L.; Phelps, E.A. The functional roles of the amygdala and prefrontal cortex in processing uncertainty. J. Cogn. Neurosci. 2019, 31, 1742–1754. [Google Scholar] [CrossRef]

- Huettel, S.A.; Stowe, J.C.; Gordon, E.M.; Warner, B.T.; Platt, M.L. Neural signatures of economic preference for risk and ambiguity. Neuron 2006, 49, 765–775. [Google Scholar] [CrossRef]

- Etkin, A.; Büchel, C.; Gross, J.J. The neural bases of emotion regulation. Nat. Rev. Neurosci. 2015, 16, 693–700. [Google Scholar] [CrossRef] [PubMed]

- Viviani, R. Neural correlates of emotion regulation in the ventral prefrontal cortex and the encoding of subjective value and economic utility. Front. Psychiatry 2014, 5. [Google Scholar] [CrossRef] [PubMed]

- Knutson, B.; Greer, S.M. Anticipatory affect: Neural correlates and consequences for choice. Philos. Trans. R. Soc. Lond. B Biol. Sci. 2008, 363, 3771–3786. [Google Scholar] [CrossRef]

- Kuhnen, C.M.; Knutson, B. The neural basis of financial risk taking. Neuron 2005, 47, 763–770. [Google Scholar] [CrossRef]

- Mohr, P.N.; Biele, G.; Heekeren, H.R. Neural processing of risk. J. Neurosci. 2010, 30, 6613–6619. [Google Scholar] [CrossRef] [PubMed]

- Moher, D.; Liberati, A.; Tetzlaff, J.; Altman, D.G. The PRISMA Group. Preferred reporting items for systematic reviews and meta-analyses: The PRISMA statement. PLoS Med. 2009, 6, e1000097. [Google Scholar] [CrossRef]

- Eickhoff, S.B.; Bzdok, D.; Laird, A.R.; Kurth, F.; Fox, P.T. Activation likelihood estimation meta-analysis revisited. Neuroimage 2012, 59, 2349–2361. [Google Scholar] [CrossRef]

- Turkeltaub, P.E.; Eickhoff, S.B.; Laird, A.R.; Fox, M.; Wiener, M.; Fox, P. Minimizing within-experiment and within-group effects in activation likelihood estimation meta-analyses. Hum. Brain Mapp. 2012, 33. [Google Scholar] [CrossRef] [PubMed]

- Eickhoff, S.B.; Laird, A.R.; Grefkes, C.; Wang, L.E.; Zilles, K.; Fox, P.T. Coordinate-based activation likelihood estimation meta-analysis of neuroimaging data: A random-effects approach based on empirical estimates of spatial uncertainty. Hum. Brain Mapp. 2009, 30, 2907–2926. [Google Scholar] [CrossRef] [PubMed]

- Eickhoff, S.B.; Nichols, T.E.; Laird, A.R.; Hoffstaedter, F.; Amunts, K.; Fox, P.T.; Eickhoff, C.R. Behavior, sensitivity, and power of activation likelihood estimation characterized by massive empirical simulation. Neuroimage 2016, 137, 70–85. [Google Scholar] [CrossRef]

- van Essen, D.C.; Drury, H.A.; Dickson, J.; Harwell, J.; Hanlon, D.; Anderson, C.H. An integrated software suite for surface-based analyses of cerebral cortex. J. Am. Med. Inform. Assoc. 2001, 8, 443–459. [Google Scholar] [CrossRef] [PubMed]

- Majer, P.; Mohr, P.N.; Heekeren, H.R.; Härdle, W.K. Portfolio decisions and brain reactions via the CEAD method. Psychometrika 2016, 81, 881–903. [Google Scholar] [CrossRef] [PubMed]

- Haller, A.; Schwabe, L. Sunk costs in the human brain. Neuroimage 2014, 97, 127–133. [Google Scholar] [CrossRef]

- Zeng, J.; Zhang, Q.; Chen, C.; Yu, R.; Gong, Q. An fMRI study on sunk cost effect. Brain Res. 2013, 1519, 63–70. [Google Scholar] [CrossRef]

- Mohr, P.N.; Biele, G.; Krugel, L.K.; Li, S.-C.; Heekeren, H.R. Neural foundations of risk-return trade-off in investment decisions. Neuroimage 2009, 49, 2556–2563. [Google Scholar] [CrossRef]

- Huber, R.E.; Klucharev, V.; Rieskamp, J. Neural correlates of informational cascades: Brain mechanisms of social influence on belief updating. Soc. Cogn. Affect. Neurosci. 2015, 10, 589–597. [Google Scholar] [CrossRef]

- Burke, C.J.; Tobler, P.N.; Schultz, W.; Baddeley, M. Striatal BOLD response reflects the impact of herd information on financial decisions. Front. Hum. Neurosci. 2010, 4, 48. [Google Scholar] [CrossRef] [PubMed]

- Bruguier, A.J.; Quartz, S.R.; Bossaerts, P. Exploring the nature of “trader intuition”. J. Financ. 2010, 65, 1703–1723. [Google Scholar] [CrossRef]

- Lohrenz, T.; Bhatt, M.; Apple, N.; Montague, R. Keeping up with the Joneses: Interpersonal prediction errors and the correlation of behavior in a tandem sequential choice task. PLoS Comput. Biol. 2013, 9, e1003275. [Google Scholar] [CrossRef]

- Häusler, A.N.; Kuhnen, C.M.; Rudorf, S.; Weber, B. Preferences and beliefs about financial risk taking mediate the association between anterior insula activation and self-reported real-life stock trading. Sci. Rep. 2018, 8, 11207. [Google Scholar] [CrossRef] [PubMed]

- Smith, A.; Lohrenz, T.; King, J.; Montague, R.; Camerer, C.F. Irrational exuberance and neural crash warning signals during endogenous experimental market bubbles. Proc. Natl. Acad. Sci. USA 2014, 111, 10503–10508. [Google Scholar] [CrossRef] [PubMed]

- Ogawa, A.; Onozaki, T.; Mizuno, T.; Asamizuya, T.; Ueno, K.; Cheng, K.; Iriki, A. Neural basis of economic bubble behavior. Neurosci. J. 2014, 265, 37–47. [Google Scholar] [CrossRef]

- de Martino, B.; O’Doherty, J.P.; Ray, D.; Bossaerts, P.; Camerer, C. In the mind of the market: Theory of mind biases value computation during financial bubbles. Neuron 2013, 79, 1222–1231. [Google Scholar] [CrossRef]

- Brooks, A.; Capra, M.C.; Berns, G.S. Neural insensitivity to upticks in value is associated with the disposition effect. Neuroimage 2012, 59, 4086–4093. [Google Scholar] [CrossRef]

- Gu, X.; Kirk, U.; Lohrenz, T.M.; Montague, R. Cognitive strategies regulate fictive, but not reward prediction error signals in a sequential investment task. Hum. Brain Mapp. 2014, 35, 3738–3749. [Google Scholar] [CrossRef]

- Lohrenz, T.; McCabe, K.; Camerer, C.F.; Montague, R. Neural signature of fictive learning signals in a sequential investment task. Proc. Natl. Acad. Sci. USA 2007, 104, 9493–9498. [Google Scholar] [CrossRef]

- Levy, I.; Snell, J.; Nelson, A.J.; Rustichini, A.; Glimcher, P.W. Neural representation of subjective value under risk and ambiguity. J. Neurophysiol. 2010, 103, 1036–1047. [Google Scholar] [CrossRef] [PubMed]

- Lux, T. Herd behavior, bubbles and crashes. Econ. J. 1995, 105, 881–896. [Google Scholar] [CrossRef]

- Baddeley, M. Herding, social influence and economic decision-making: Socio-psychological and neuroscientific analyses. Philos. Trans. R. Soc. Lond. B Biol. Sci. 2010, 365, 281–290. [Google Scholar] [CrossRef] [PubMed]

- Arkes, H.R.; Blumer, C. The psychology of sunk cost. Organ Behav. Hum. Decis. Process. 1985, 35, 124–140. [Google Scholar] [CrossRef]

- Kahneman, D.; Tversky, A. Prospect theory: An analysis of decision under risk. Econometrica 1979, 47, 263–291. [Google Scholar] [CrossRef]

- Shefrin, H.; Statman, M. The disposition to sell winners too early and ride losers too long: Theory and evidence. J. Financ. 1984, 40, 777–790. [Google Scholar] [CrossRef]

{kind=link}

{kind=link}

{kind=link}

| Cluster # | Brain Areas | Size (mm3) | Center Coordinate | Peak Coordinate | ALE | P | Z |

|---|---|---|---|---|---|---|---|

| 1 | Ventral striatum + amygdala + ACC 1 | 6360 | (−11.8, 13.3, −7.8) | (−10, 16, −4) | 0.0439 | p < 0.0001 | 6.59 |

| 2 | Ventral striatum | 3976 | (11.2, 13.1, −5.8) | (10, 14, −6) | 0.0748 | p < 0.0001 | 9.44 |

| 3 | Anterior insula | 2048 | (22.6, −95.3, 8.8) | (22, −96, 8) | 0.0611 | p < 0.0001 | 8.24 |

| 4 | Occipital cortex | 1544 | (49.1, 18.6, −3.9) | (54, 16, −4) | 0.0303 | p < 0.0001 | 5.11 |

| References | Stimuli | Brain and Behavioral Results | Cluster # |

|---|---|---|---|

| Kuhnen et al., 2005 | Two stocks (one good and the other bad) and a bond | Anticipatory nucleus accumbens activity preceded risky choices, and excessive levels of activation led to risk-seeking mistakes. Anticipatory anterior insula activity preceded riskless choices, and excessive levels of activation led to risk-aversion mistakes. | 1 2 |

| Lohrenz et al., 2007 | Market information in live and not live conditions, gains and losses, portfolio value and percentage already invested | Higher levels of ventral caudate activity correlated with fictive error signals, driving investment behavior. | 1 2 3 |

| Mohr et al., 2009 | Streams of 10 past returns from an investment | Risk and value are represented in the brain during investment decisions in discrete (simple gambles) and continuous distributions (stocks). Risk–return models support the correlation between risk and anterior insula activation. | 1 4 |

| Bruguier et al., 2010 | Replay of market experiment sessions (order and trade flow) with and without insiders | Theory of mind is involved in forecasting price changes in markets with insiders and related to increased activation in the paracingulate cortex. | |

| Burke et al., 2010 | Stock information and social information (four human faces or four chimpanzee faces) | Higher levels of ventral striatum activity correlated with the participants´ likelihood to follow herd behavior, especially in the number of buying decisions. Going against the group involves activity in the anterior cingulate cortex to resolve the conflict. | 1 2 |

| Brooks et al., 2012 | Purchase prices and asset prices (random walk) | The irrational belief in mean reversion better explains the disposition effect. Participants with a large disposition effect exhibited lower levels of ventral striatum activity in response to upticks in value when the asset price was below the purchase price. | 1 2 3 |

| De Martino et al., 2013 | Portfolio value and trading prices (asks and bids) in bubble and non-bubble markets | The evaluation of social signals in dorsomedial prefrontal cortex activity affects value representations in the ventromedial prefrontal cortex. Higher levels of ventromedial prefrontal cortex activity predict an investor’s propensity to ride bubbles and, therefore, lose money. | |

| Zeng et al., 2013 | Amounts already invested in a company´s project where sunk costs and incremental costs are manipulated | Higher levels of lateral frontal and parietal cortex activity are related to higher sunk costs and more risk-taking behavior. Higher levels of striatum and medial prefrontal cortex activity are linked to smaller incremental costs and continued investing. | |

| Lohrenz et al., 2013 | Market data and social information (other players´ bets) | Interpersonal fictive errors guide behavior and highly correlate with striatum activity. | 1 2 |

| Ogawa et al., 2014 | Stock and asset information in a virtual stock exchange with two non-bubble stocks and one bubble stock | In market bubbles, brain networks switch toward dorsolateral prefrontal cortex and inferior parietal lobule connectivity, in which buying decisions are made in the former based on the information gathered by the latter region. Cash holdings were positively correlated with activation in the ventromedial prefrontal cortex, while trading during large price fluctuations were associated with superior parietal lobule activity. | |

| Smith et al., 2014 | Trading prices of risk-free and risky assets (stocks) in markets where endogenous bubbles are formed and crash | Higher levels of nucleus accumbens activity are associated with buying decisions, lower earnings, and increased likelihood of a crash. Higher levels of anterior insula activity are correlated with selling decisions before the price peak and higher earnings. | 1 2 |

| Haller et al., 2014 | Project costs and success probabilities | Higher levels of dorsolateral prefrontal cortex and lower levels of ventromedial prefrontal cortex activity are related to higher sunk costs and being prone to continue investing in previous investments. | 1 2 |

| Gu et al., 2014 | Market prices where choices are made under two conditions: regulate and attend | Only fictive errors are susceptible to reappraisal strategies by changes in activation in anterior insula and anterior insula–amygdala connectivity, modulating subjective feelings that affect behavior directly. | 1 3 |

| Huber et al., 2015 | Two stocks with social (decisions made by two fictitious traders) and private information (personal recommendation from a rating agency) | Higher levels of inferior frontal gyrus/anterior insula activity and lower levels of parietal-temporal cortex activity are correlated with overweighting private information, which can influence the probability in the formation of informational cascades. | 2 |

| Majer et al., 2016 | Past returns of investments and investment choices with fixed or risky returns | Higher levels of anterior insula and dorsomedial prefrontal cortex activity correlated with risk and decision-making. | |

| Häusler et al., 2018 | Stocks (risky option) and bonds (non-risky option) in gain and loss domains | Lower levels of anterior insula activity are connected to risky decisions in real-life stock traders. These choices are based on personal beliefs about risky choices and the willingness to bear risk. | 1 3 |

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2021 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).

Share and Cite

Ortiz-Teran, E.; Diez, I.; Lopez-Pascual, J. An ALE Meta-Analysis on Investment Decision-Making. Brain Sci. 2021, 11, 399. https://doi.org/10.3390/brainsci11030399

Ortiz-Teran E, Diez I, Lopez-Pascual J. An ALE Meta-Analysis on Investment Decision-Making. Brain Sciences. 2021; 11(3):399. https://doi.org/10.3390/brainsci11030399

Chicago/Turabian StyleOrtiz-Teran, Elena, Ibai Diez, and Joaquin Lopez-Pascual. 2021. "An ALE Meta-Analysis on Investment Decision-Making" Brain Sciences 11, no. 3: 399. https://doi.org/10.3390/brainsci11030399

APA StyleOrtiz-Teran, E., Diez, I., & Lopez-Pascual, J. (2021). An ALE Meta-Analysis on Investment Decision-Making. Brain Sciences, 11(3), 399. https://doi.org/10.3390/brainsci11030399