Cryptocurrencies and Fraudulent Transactions: Risks, Practices, and Legislation for Their Prevention in Europe and Spain

and

and

Abstract

:1. Introduction

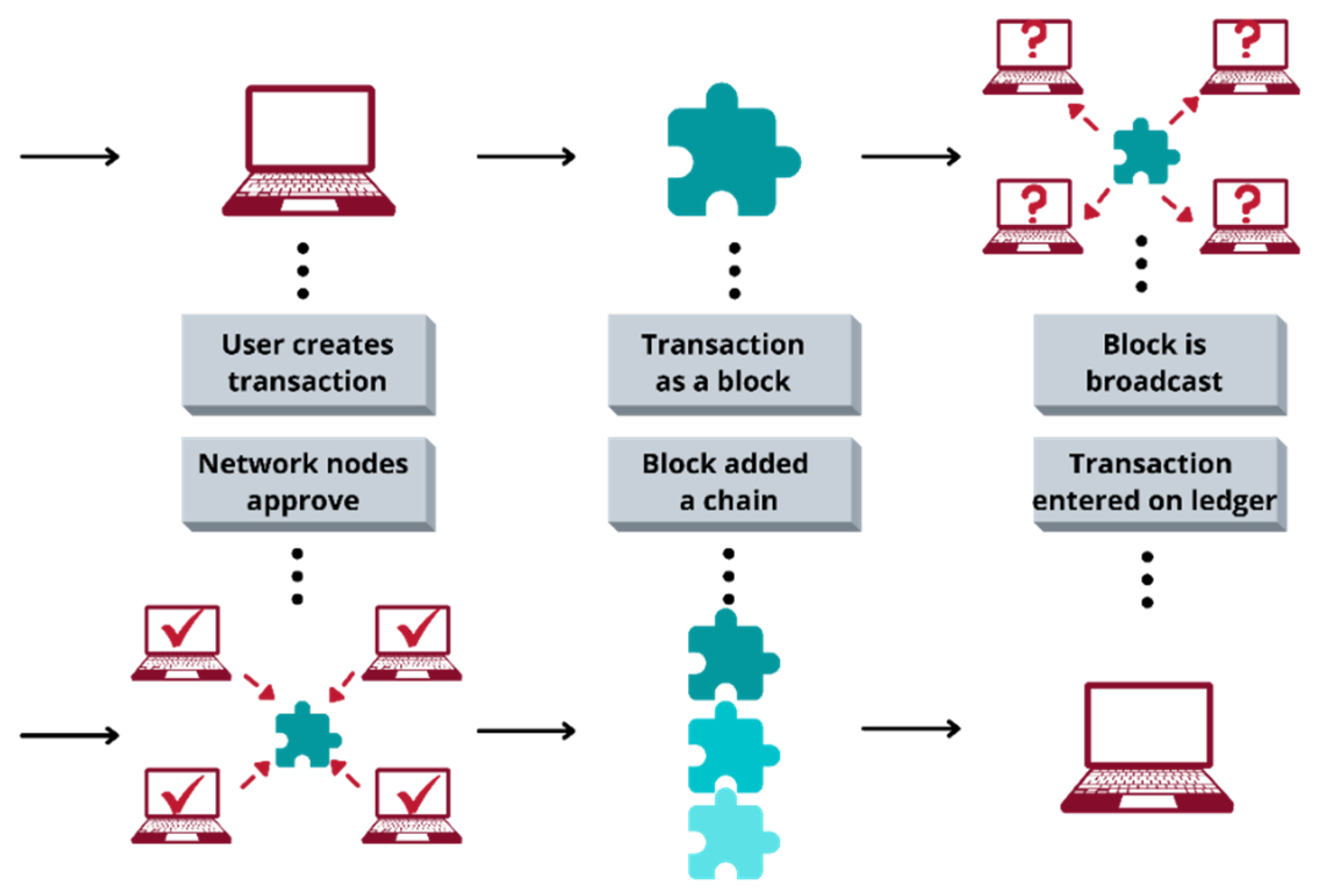

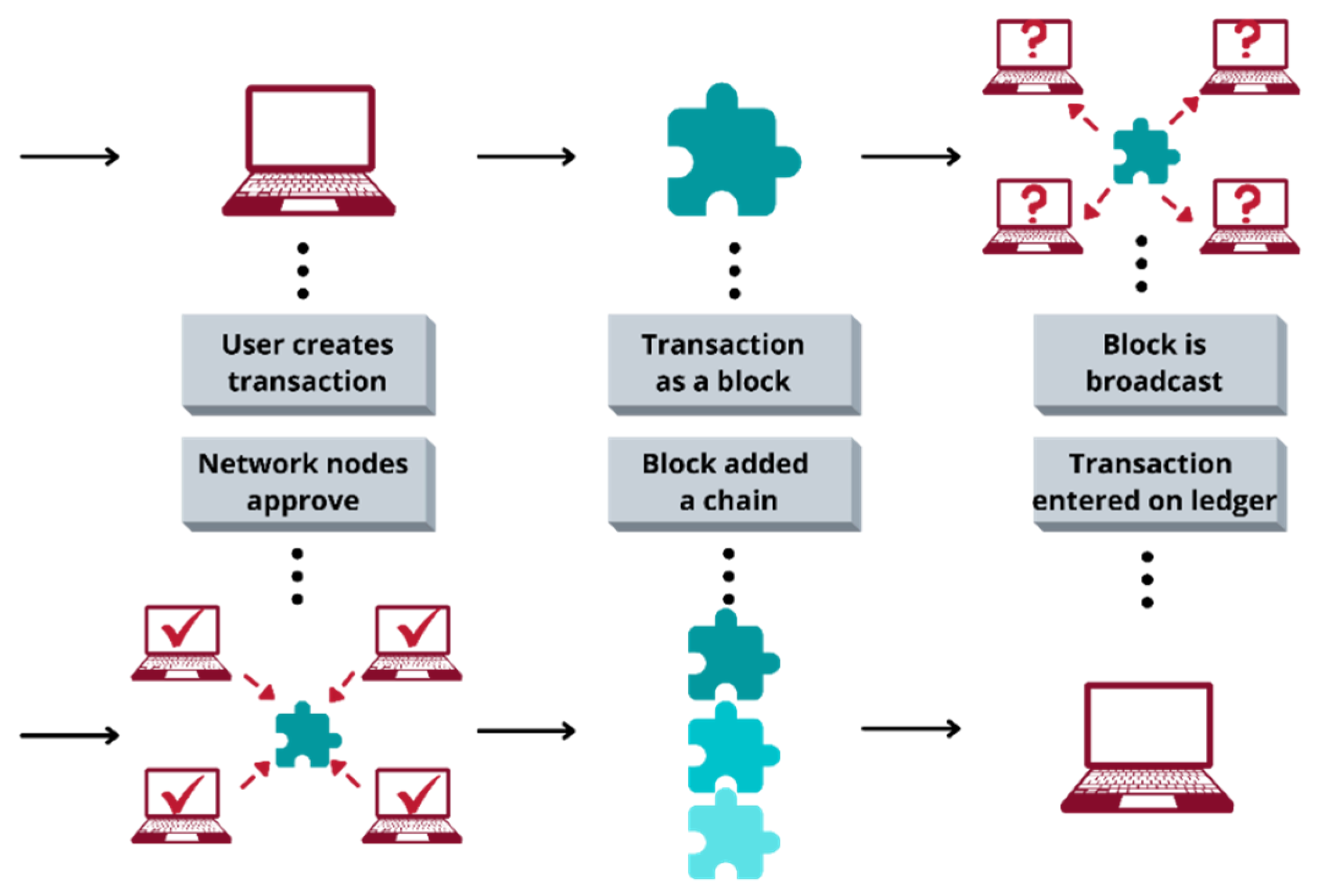

2. Approach to Cryptocurrencies

3. Legislation Applicable to Cryptocurrencies in Europe and Spain

- −

- FATF Guide on Virtual Assets and Service Providers, published in June 2019.

- −

- Fifth Directive, 2018/843 EU, on the Prevention of Money Laundering.

- −

- Royal Decree-Law 7/2021 transposing EU directives, including the one on the prevention of money laundering (Royal Decree-Law 7/2021 Transposing EU Directives, Including the One on the Prevention of Money Laundering 2021)2.

- −

- VA’s consideration is property, income, funds. It is a risk-based approach, risks must be identified, and preventive and repressive measures must be taken.

- −

- VASPs should be required to be licensed or registered.

- −

- At a minimum, VASPs should be licensed or registered in the jurisdictions where they are created.

- −

- When the VASP is an individual, they should be required to be licensed or registered in the jurisdiction where their place of business is located.

- −

- Jurisdictions may require VASPs offering products in their jurisdiction to be registered in that jurisdiction.

- −

- VASPs must be subject to appropriate regulation and supervision.

- −

- ASPs must be controlled by a competent authority that should conduct risk-based supervision, have adequate powers to supervise, conduct inspections, compel the production of information, and impose sanctions.

- ○

- VASP: CDD (Customer Due Diligence) from 1000 USD/EUR.

- ○

- VA: Accurate information, payer-beneficiary, and make it available at the request of the authorities.

- ○

- Measures: Blocking, prohibition of transactions with persons and entities.

- ○

- International cooperation, VASP supervisors should exchange information quickly and constructively with their foreign counterparts.

- −

- It incorporates new obligated parties: the providers of services for the exchange of virtual currencies for fiat currencies (cryptocurrency exchange operators or exchanges) and the providers of custody services for electronic wallets or private keys or wallets or electronic wallets (entities that provide services for the safeguarding of private cryptographic keys on behalf of their clients, for the holding, storage, and transfer of virtual currencies).

- −

- It aims to make providers report suspicious transactions, in addition to partially restricting the anonymity that cryptocurrencies supposedly allow.The competent authorities should be empowered, through the obliged entities, to monitor the use of virtual currencies.

- −

- Another measure in relation to these new subjects is the obligation for them to be registered, although it is not specified in what type of registration or the terms and conditions of this. The Directive itself sets a date of January 10, 2020 for its transposition.

- −

- New obligated parties are incorporated, including electronic wallet custody service providers, which are defined as “those natural persons or entities that provide safeguarding or custody services of private cryptographic keys on behalf of their clients for the holding, storage and transfer of virtual currencies”.

- −

- Persons providing services for the exchange of virtual currency into legal tender must be subject to the preventive obligations established.

- −

- Virtual currency is defined as “a digital representation of value not issued or guaranteed by a central bank or public authority, not necessarily associated with a legally established currency and which does not have the legal status of currency, but which is accepted as a medium of exchange and can be transferred, stored or traded electronically”. The exchange of virtual currency for fiat currency is understood as “the purchase and sale of virtual currencies through the delivery or receipt of euros or any other foreign currency of legal tender or electronic money accepted as a means of payment in the country in which it was issued”.

- −

- The Registry of service providers for the exchange of virtual currency for fiat currency and the custody of electronic purses is regulated.Natural or legal persons, regardless of their nationality, who offer or provide in Spain services for the following must be registered in the registry set up at the Bank of Spain:

- −

- Sale of virtual currencies through the delivery or receipt of euros or any other foreign currency of legal tender or electronic money accepted as a means of payment in the country in which it has been issued.

- −

- Providers of electronic purse custody services.

- −

- The following must be registered: “Natural persons who provide these services, when the base, direction or management of these activities is located in Spain, regardless of the location of the recipients of the service” and “Legal persons established in Spain who provide these services, regardless of the location of the recipients”.

- −

- Supervisory powers are delegated to the Bank of Spain, related to compliance with the obligation to register and the conditions of honorability of registration.

- −

- A sanctioning regime is established by the Bank of Spain, when the provision of services is carried out without the mandatory registration as a very serious infringement, being serious if the activity has been carried out on an occasional basis.

- −

- The entry of this law into force is established on the day following its publication in the BOE; however, several exceptions are established, related to virtual currencies.

- −

- Sale of virtual currencies through the delivery or receipt of euros or any other foreign currency of legal tender or electronic money accepted as a means of payment in the country in which it has been issued.

- −

- Electronic wallet custody service providers.

- Utility tokens: these are those that are normally used to obtain initial funding for the development of a specific project, used, for example, by some startups. They can be issued without the need for authorization, being sufficient to notify the competent national authority (in Spain, probably the CNMV) and submit a White Paper (the document containing all the technical details and description of the product).

- Asset-Referenced Token: These cryptoassets serve as a medium of exchange, as they aim to keep stable the value of one or several commodities or one or several cryptocurrencies, or a combination of both, referenced to several national currencies of legal tender. In order to authorize their issuance, it is necessary to approve their White Paper and comply with certain requirements.

- Electronic money token (e-money token): This is another cryptoasset used as a medium of exchange, but whose value is intended to be maintained by denominating it in units of a national currency. For its issuance, a notification must be sent to the competent authority and be a credit or e-money institution.

- −

- Have custody of and provide access to cryptoassets to their clients.

- −

- Have cryptoasset exchange platforms.

- −

- Execute cryptoasset purchase orders.

- −

- Issue cryptoassets (when they are both the issuer and service provider).

- −

- Receive and transmit orders related to cryptoassets.

- −

- Provide advisory services in the field of cryptoassets.

- −

- Make payments of tokens referenced to assets.

4. Money Laundering

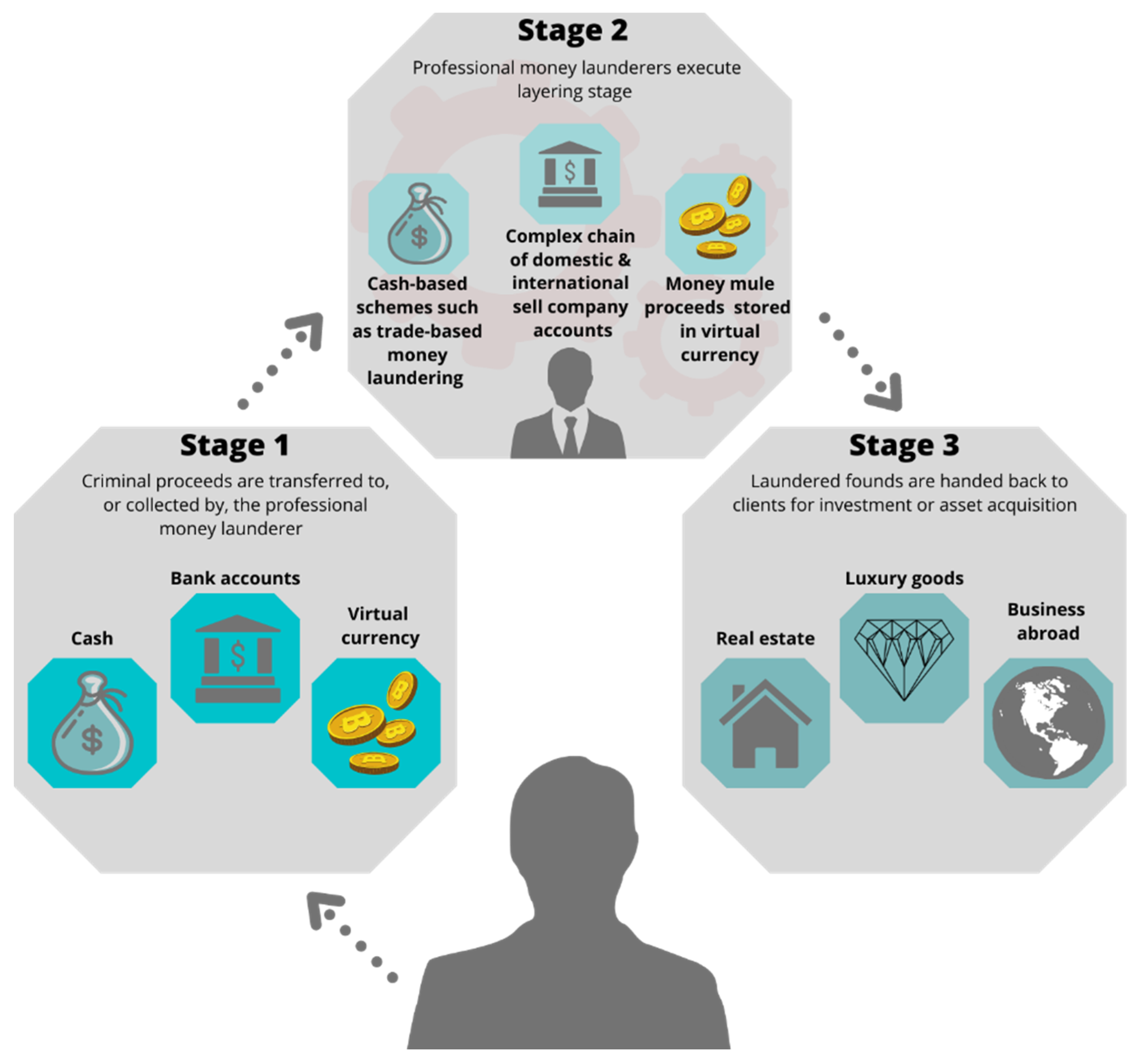

- Placement: This is the first stage of the laundering process, in which the “dirty” money, whether in cash or materialized in any type of illicitly obtained goods, changes location, and is placed beyond the control of the authorities.

- Layering or intermingling or diversification or conversion: This is the second stage of the money laundering process and consists of intermingling the money or goods in various businesses and financial institutions. The money is transported to other places to disguise its illicit origin. The important thing here is to acquire assets in order to transfer or exchange them with others of licit origin. At this stage, once the money enters the financial circuits, movements are made to hide its origin, in order to eradicate any possible link between the money placed and its origin. The most frequent techniques are to send the money to tax havens or offshore centers, to ensure that the funds circulate throughout different countries, institutions, and accounts held by different individuals or legal entities.

- Integration or investment: This is the last stage of the money laundering process. The money from criminal activities is used for financial business, which may be legitimate. In this stage, commercial investments are made, loans are granted to individuals, goods are purchased, and all kinds of transactions are carried out through accounting and tax records, which justify the capital in a legal manner, making control difficult. Therefore, the money is placed back into the economy, with the appearance of legality. In this phase, once the capital has been placed and stratified, the money returns to the legal financial circuit mixed with other licit elements, thus giving it the appearance of legality.

5. Methodologies for Money Laundering with Cryptocurrencies

- Use of cryptocurrencies to pay for criminal services: a whole series of crimes linked to cybercrime are encompassed, in which payments are made through these currencies. Illegal transactions take place on the dark internet (Darknet), including the purchase and sale of narcotic substances, counterfeit banknotes and products and false identity documents, the sale of cloned or stolen bank card data, software containing viruses (malware), images and videos with pedophile content, weapons, and explosives. For example, Silken Road, an illegal market within the Darknet, in which the sale and purchase of illicit products was carried out through cryptocurrencies, was closed by the Federal Bureau of Investigation (FBI) on 2 October 2013.

- Use of virtual currencies as a form of fraud: The revaluation that virtual currencies have had in recent years, has led to the emergence of new forms of business through ICOs (Initial Coin Offer). “An initial coin offering (ICO) is the cryptocurrency industry’s equivalent to an initial public offering (IPO). A company looking to raise money to create a new coin, app, or service launches an ICO as a way to raise funds...Initial Coin Offerings (ICOs) are a popular fundraising method used primarily by startups wishing to offer products and services, usually related to the cryptocurrency and blockchain space”. (...) “No ‘cryptocurrency’ issuance nor any ICO has been registered, authorized or verified by any supervisory body in Spain. This implies that there are no ‘cryptocurrencies’, or ‘tokens’ issued in ICOs whose acquisition or holding in Spain can benefit from any of the guarantees or protections provided for in the regulations relating to banking or investment products” (BE and CNMV 2018, p. 2; cf. Frankenfield 2020). Among the priorities of the BE and the CNMV is to “provide information to the public so that investors and users of financial services are in a position to face the increasing complexity of the financial environment with confidence” (BE and CNMV 2018, p. 2). They consider that it is essential that all individuals or entities that decide to buy digital currencies or invest in these products, consider the risks associated with them, and that the decision is made with all the available and sufficient information to understand the product they are going to acquire.

- Use of virtual currencies for laundering money of illicit origin: First, the money generated in an illicit activity is transformed into virtual currency. Second, operations are carried out to erase the traceability of the cryptocurrency, such as the use of mixers. Third, after the stratification phase, it is introduced into the real circuit to monetize these illicit profits. The criminal organization that generates the illegal money from some kind of criminal activity may have the structure and know-how to perform the self-laundering of that money or contact an organization that is dedicated to laundering the money, co-charging a commission in proportion to the amount laundered. According to reports from the following different agencies analyzed by Navarro Cardoso (2019): National Crime Agency (NCA), United Nations Office on Drugs and Crime (UNODC), and United States Drug Enforcement Agency (DEA), it is found that, due to anonymity, speed, transnationality, and non-presence, new technologies have favored criminal activity in the field of money laundering and tax fraud, in addition to other types of activities (means of payment in drug trafficking or extortion). It is clear from these reports that virtual currencies are becoming a relatively safe method for criminals to move illicit profits around the world with a lower risk than traditional methods (Navarro Cardoso 2019). The different ways of laundering money through cryptocurrencies are presented below.

5.1. Mining

5.2. Exchanges

- −

- They have not been obliged subjects in terms of money laundering prevention, with the entry of the new Royal Decree-Law 7/2021, on 27 April 2021, they are incorporated as new obliged subjects and a term of six months from the entry into force is established for their registration in the registry created.

- −

- The principals do not operate from Spain; however, Royal Decree-Law 7/2021 establishes that natural or legal persons, offering or providing services in Spain, must be registered in the registry.

- −

- They can be directly controlled by the money laundering organization.

5.3. Local Traders

- −

- Trading virtual currency against cash in significant volumes.

- −

- Conducting exchanges of virtual currency against cash using channels that involve paying high commissions and/or enduring worse exchange rates than alternative methods.

- −

- Exchanges made in unusual, anonymous locations. In many cases, sales and purchases are arranged through internet forums (p2p) and the exchanges take place physically to ensure that the buyer of the cryptocurrencies pays in cash and the seller simply provides his account password.

- −

- The purchase is made with direct profits from other illicit activities.

5.4. ATMS

- −

- The customer introduces cash into the ATM that he/she wants to transform into virtual money.

- −

- The ATM sends the customer the equivalent amount in virtual currency, minus the commission charged for the operation, to the wallet indicated by the customer.

- −

- The exchange linked to the cashier delivers the same amount of virtual currency to the operator at market price.

- −

- The operator reloads the cashier’s purse by transferring the virtual currency from the exchange.

- −

- The operator collects cash from the ATM.

- −

- Finally, the operator deposits the cash in the bank and makes a transfer to the exchange.

5.5. Online Videogames

5.6. Mixers

5.7. Suppliers of Services and Goods

5.8. Bitcoin Cards

- −

- It is a prepaid Visa or Mastercard, issued by a card issuer that is licensed to operate.

- −

- It is a card in euros, dollars, or other official currency.

- −

- It is marketed to end users by a card provider, which has some kind of agreement with a card issuer or is a card issuer.

- −

- There is a web page for the user, offered by the card provider.

- −

- Physical or virtual, depending on whether the card is issued physically or only virtually.

- −

- Verified or unverified: It depends on whether the identity has been verified by the issuer of the card provider. When such verification has not been carried out or has not been efficiently checked, it is unverified.

6. Conclusions

Author Contributions

Funding

Institutional Review Board Statement

Informed Consent Statement

Acknowledgments

Conflicts of Interest

References

- Albrecht, Chad, Kristopher McKay Duffin, Steven Hawkins, and Victor Manuel Morales Rocha. 2019. The Use of Cryptocurrencies in the Money Laundering Process. Journal of Money Laundering Control 22: 210–16. [Google Scholar] [CrossRef]

- Argañaraz, Agustín, Agostina Mazzuchelli, Diana Albanese, and María de los Ángeles López. 2019. Blockchain: Un Nuevo Desafío Para la Contabilidad y Auditoría. Available online: http://sedici.unlp.edu.ar/bitstream/handle/10915/89919/Documento_completo.pdf-PDFA.pdf?sequence=1&isAllowed=y (accessed on 20 May 2021).

- Bank of Spain [BE], and the National Securities Market Commission [CNMV]. 2018. Comunicado Conjunto de la CNMV y del Banco de España Sobre “Criptomonedas” y “Ofertas Iniciales de Criptomonedas” (ICOs). Available online: https://www.cnmv.es/loultimo/NOTACONJUNTAriptoES%20final.pdf (accessed on 20 May 2021).

- Bank of Spain [BE], and the National Securities Market Co-mission [CNMV]. 2021. Comunicado Conjunto de la CNMV y del Banco de España Sobre el Riesgo de las Criptomonedas Como Inversión. Available online: https://www.cnmv.es/Portal/verDoc.axd?t=%7Be14ce903-5161-4316-a480-eb1916b85084%7D (accessed on 2 May 2021).

- Barroilhet Díez, Agustin. 2019. Cryptocurrencies, economic and legal aspects. Revista Chilena de Derecho y Tecnología 8: 29–67. [Google Scholar] [CrossRef]

- Bedecarratz Scholz, Francisco. 2018. Riesgos delictivos de las monedas virtuales: Nuevos desafíos para el derecho penal. Revista Chilena de Derecho y Tecnología 7: 79–105. [Google Scholar] [CrossRef] [Green Version]

- Bloomberg Galaxy Crypto Index [BGCI]. 2021. Bloomberg Crypto Outlook Bitcoin Making Gold Redundant? Available online: https://assets.bbhub.io/promo/sites/12/1029441_Crypto-Mar2021Outlook.pdf (accessed on 5 June 2021).

- Bouri, Elie, Syed Jawad Hussain Shahzad, and David Roubaud. 2019. Co-explosivity in the cryptocurrency market. Finance Research Letters 29: 178–83. [Google Scholar] [CrossRef]

- Butler, Simon. 2019. Criminal Use of Cryptocurrencies: A Great New Threat or Is Cash Still King? Journal of Cyber Policy 4: 326–45. [Google Scholar] [CrossRef]

- Cheah, Eng-Tuck, and John Fry. 2015. Speculative bubbles in Bitcoin markets? An empirical investigation into the fundamental value of Bitcoin. Economics Letters 130: 32–36. [Google Scholar] [CrossRef] [Green Version]

- Chowdhury, Niaz. 2019. Crime, Criminals and Cryptocurrencies. In Inside Blockchain, Bitcoin, and Cryptocurrencies. Edited by Niaz Chowdhury. London: CRC Press, pp. 295–316. [Google Scholar] [CrossRef]

- CoinMarketCap. 2021a. Available online: https://coinmarketcap.com/charts/ (accessed on 10 June 2021).

- CoinMarketCap. 2021b. Bitcoin Adoption: Why Paraguay Could Follow in El Salvador’s Footsteps. Available online: https://coinmarketcap.com/es/headlines/news/bitcoin-adoption-why-paraguay-could-follow-in-el-salvadors-footsteps/ (accessed on 8 June 2021).

- Corredor Higuera, Jorge Armando, and David Díaz Guzmán. 2018. Blockchain y mercados financieros: Aspectos generales del impacto regulatorio de la aplicación de la tecnología blockchain en los mercados de crédito de América Latina. Derecho PUCP 81: 405–39. [Google Scholar] [CrossRef] [Green Version]

- Dyntu, Valeriia, and Oleh Dykyi. 2019. Cryptocurrency in the System of Money Laundering. Baltic Journal of Economic Studies 4: 75–81. [Google Scholar] [CrossRef]

- Dyson, Simon, William Buchanan, and Liam Bell. 2018. The Challenges of Investigating Cryptocurrencies and Blockchain Related Crime. The Journal of the British Blockchain Association 1: 1–6. [Google Scholar] [CrossRef] [Green Version]

- Echarte Fernández, Miguel Ángel, Sergio Luis Náñez Alonso, Javier Jorge-Vázquez, and Ricardo Francisco Reier Forradellas. 2021. Central Banks’ Monetary Policy in the Face of the COVID-19 Economic Crisis: Monetary Stimulus and the Emergence of CBDCs. Sustainability 13: 4242. [Google Scholar] [CrossRef]

- Enguix, Jaime Criado. 2020. Blockchain: Criptomonedas y tokenización de activos inmobiliarios. Efectos en el ámbito registral. Revista de Derecho, Empresa y Sociedad 16: 253–77. [Google Scholar]

- EU. 2018. European Union, on 30 May 2018, Directive (EU) 2018/843, of 30 May 2018, por la que se Modifica la Directiva (UE) 2015/849 Relativa a la Prevención de la Utilización del Sistema Financiero para el Blanqueo de Capitales o la Financiación del Terrorismo, y por la que se Modifican las Directivas 2009/138/CE y 2013/36/UE. Available online: http://data.europa.eu/eli/dir/2018/843/oj (accessed on 25 May 2021).

- European Central Bank [ECB]. 2012. Virtual Currency Schemes. Available online: https://www.ecb.europa.eu/pub/pdf/other/virtualcurrencyschemes201210en.pdf (accessed on 5 April 2021).

- European Commission. 2020. Proposal for a Regulation of the European Parliament and of the Council on Markets in Crypto-Assets and Amending Directive (EU) 2019/1937. Available online: https://eur-lex.europa.eu/legal-content/EN/TXT/HTML/?uri=CELEX:52020PC0593&from=ES (accessed on 15 May 2021).

- Farrugia, Steven, Joshua Ellul, and George Azzopardi. 2020. Detection of Illicit Accounts over the Ethereum Blockchain. Expert Systems with Applications 150: 113318. [Google Scholar] [CrossRef] [Green Version]

- Fernández Bermejo, Daniel. 2016. En torno al concepto del blanqueo de capitales evolución normativa y análisis del fenómeno desde el derecho penal. Anuario de Derecho Penal y Ciencias Penales 69: 211–76. [Google Scholar]

- Financial Action Task Force [FATF]. 2012. Estándares Internacionales Sobre la Lucha Contra el Lavado de Activos y el Financiamiento del Terrorismo y la Proliferación. Las Recomendaciones del GAFI. Available online: https://www.fatf-gafi.org/media/fatf/documents/recommendations/pdfs/FATF-40-Rec-2012-Spanish.pdf (accessed on 12 April 2021).

- Financial Action Task Force [FATF]. 2015. Informe: Directrices para un Enfoque Basado en Riesgo para Monedas Virtuales. Available online: https://www.fatf-gafi.org/media/fatf/documents/Directrices-para-enfoque-basada-en-riesgo-Monedas-virtuales.pdf (accessed on 21 March 2021).

- Financial Action Task Force [FATF]. 2018. Professional Money Laundering. Available online: https://www.fatf-gafi.org/publications/methodsandtrends/documents/professional-money-laundering.html (accessed on 11 April 2021).

- Financial Action Task Force [FATF]. 2019. Guidance for a Risk-Based Approach to Virtual Assets and Virtual Asset Service Providers. Available online: https://www.fatf-gafi.org/publications/fatfrecommendations/documents/guidance-rba-virtual-assets.html (accessed on 1 May 2021).

- Frankenfield, Jake. 2020. Initial Coin Offering (ICO). Investopedia. Available online: https://www.investopedia.com/terms/i/initial-coin-offering-ico.asp (accessed on 23 May 2021).

- Gallardo, Ignacio, Patricia Bazan, and Paula Venosa. 2019. Análisis del anonimato aplicado a criptomonedas. In XXV Congreso Argentino de Ciencias de la Computación (CACIC) (Universidad Nacional de Río Cuarto, Córdoba, 14 al 18 de Octubre de 2019). Available online: http://sedici.unlp.edu.ar/handle/10915/91324 (accessed on 2 April 2021).

- Geography of Cryptocurrency Report. 2020. Available online: https://go.chainalysis.com/2020-geography-of-crypto-report.html. (accessed on 8 June 2021).

- Hancock, Matt, and Ed Vaizey. 2016. Government Office for Science. Distributed Ledger Technology: Beyond Blockchain. Available online: https://www.gov.uk/government/news/distributed-ledger-technology-beyond-block-chain (accessed on 12 April 2021).

- Hornuf, Lars, Theresa Kück, and Armin Schwienbacher. 2021. Initial Coin Offerings, Information Disclosure, and Fraud. Small Business Economics. [Google Scholar] [CrossRef]

- Jiang, Shangrong, Yuze Li, Quanying Lu, Yongmiao Hong, Dabo Guan, Yu Xiong, and Shouyang Wang. 2021. Policy assessments for the carbon emission flows and sustainability of Bitcoin blockchain operation in China. Nature Communications 12. [Google Scholar] [CrossRef] [PubMed]

- Kfir, Isaac. 2020. Cryptocurrencies, National Security, Crime and Terrorism. Comparative Strategy 39: 113–27. [Google Scholar] [CrossRef]

- Law 10/2010 of April 28 on the Prevention of Money Laundering and Terrorist Financing. 2010. «BOE» núm. 103, de 29/04. Available online: https://www.boe.es/eli/es/l/2010/04/28/10/con (accessed on 12 June 2021).

- López Domínguez, Ignacio, and José Antonio Medina Melón. 2020. Análisis financiero de las nuevas monedas digitales (criptomonedas). Revista Internacional Jurídica y Empresarial 3: 19–43. [Google Scholar] [CrossRef]

- Marrero Travieso, Yran. 2003. La criptografía como elemento de la seguridad informática. ACIMED 11. Available online: http://scielo.sld.cu/scielo.php?script=sci_arttext&pid=S1024-94352003000600012&lng=es&tlng=pt (accessed on 6 June 2021).

- Martínez, Julio César. 2017. El Delito de Blanqueo de Capitales. Doctoral dissertation. Available online: https://eprints.ucm.es/id/eprint/41080/1/T38338.pdf (accessed on 16 May 2021).

- Mora, Edwin Alberto. 2016. Monedas Virtuales se Suman al Comercio Electrónico. Available online: http://hdl.handle.net/10654/14892 (accessed on 13 April 2021).

- Nakamoto, Sathoshi. 2008. Bitcoin: A Peer-to-Peer Electronic Cash System. Available online: https://bitcoin.org/bitcoin.pdf (accessed on 13 May 2021).

- Náñez Alonso, Sergio Luis, Javier Jorge-Vazquez, and Ricardo Francisco Reier Forradellas. 2021. Central Banks Digital Currency: Detection of Optimal Countries for the Implementation of a CBDC and the Implication for Payment Industry Open Innovation. Journal of Open Innovation: Technology, Market, and Complexity 7: 72. [Google Scholar] [CrossRef]

- Náñez Alonso, Sergio Luis, Miguel Ángel Echarte Fernández, David Sanz Bas, and Jarosław Kaczmarek. 2020. Reasons fostering or discouraging the implementation of central bank-backed digital currency: A review. Economies 8: 41. [Google Scholar] [CrossRef]

- Náñez Alonso, Sergio Luis. 2019. Activities and Operations with Cryptocurrencies and Their Taxation Implications: The Spanish Case. Laws 8: 16. [Google Scholar] [CrossRef] [Green Version]

- Navarro Cardoso, Fernando. 2019. Criptomonedas (en especial, Bitcóin) y Blanqueo de Dinero. Revista Electrónica de Ciencia Penal y Criminología 14: 1–45. Available online: http://criminet.ugr.es/recpc/21/recpc21-14.pdf (accessed on 1 May 2021).

- Nikolova, Bozhidara. 2019. Cryptocurrencies—The Future of Payment Systems or a Modern Way to Fraud. VUZF Review 2. Available online: https://papersvuzf.net/index.php/VUZF/article/view/28 (accessed on 22 June 2021).

- Ordinas, Miriam. 2017. Las Criptomonedas: ¿Oportunidad o burbuja. Bancamarch. Available online: https://www.bancamarch.es/recursos/doc/bancamarch/20170109/2017/informe-mensualoctubre-2017-historia.pdf (accessed on 28 May 2021).

- Organic Law 10/1995, of 23 November 1995, of the Penal Code. 1995. «BOE» núm. 281, de 24/11. Available online: https://www.boe.es/eli/es/lo/1995/11/23/10/con (accessed on 12 March 2021).

- Palomo-Zurdo, Ricardo. 2018. Blockchain: La descentralización del poder y su aplicación en la defensa. Boletín IEEE 10: 885–904. Available online: http://www.ieee.es/en/Galerias/fichero/docs_opinion/2018/DIEEEO70-2018_Blockchain_PalomoZurdo.pdf (accessed on 16 May 2021).

- Parrondo, Luz. 2018. Tecnología Blockchain, Una Nueva Era Para La Empresa. Revista de Contabilidad y Dirección 27: 11–31. [Google Scholar]

- Podgor, Ellen S. 2019. Cryptocurrencies and Securities Fraud: In Need of Legal Guidance. SSRN Electronic Journal. [Google Scholar] [CrossRef]

- Porxas Roig, Nuria, and María Conejero. 2018. Tecnología blockchain: Funcionamiento, aplicaciones y retos jurídicos relacionados. Actualidad jurídica Uría Menéndez 48: 24–36. [Google Scholar]

- Royal Decree-Law 7/2021 Transposing EU Directives, Including the One on the Prevention of Money Laundering. 2021. «BOE» núm. 101, de 28 de abril de 2021, páginas 49749 a 49924. Available online: https://www.boe.es/eli/es/rdl/2021/04/27/7 (accessed on 11 May 2021).

- Sanz Bas, David. 2020. Hayek and the cryptocurrency revolution. Iberian Journal of the History of Economic Thought 7: 15–28. [Google Scholar] [CrossRef]

- Shier, Charlie, Muhammad Izhar Mehar, Alana Giambattista, Elgar Gong, Gabrielle Fletcher, Ryan Sanayhie, Marek Laskowski, and Henry M. Kim. 2019. Understanding a Revolutionary and Flawed Grand Experiment in Blockchain: The DAO Attack. Journal of Cases on Information Technology 21: 19–32. [Google Scholar] [CrossRef]

- Teichmann, Fabian Maximilian Johannes, and Marie-Christin Falker. 2020. Cryptocurrencies and Financial Crime: Solutions from Liechtenstein. Journal of Money Laundering Control. [Google Scholar] [CrossRef]

- Tondini, Bruno. 2009. Nuevas proyecciones del derecho internacional penal de los delitos de lavado de dinero, corrupción internacional y tráfico de personas. Recordip 1: 1–58. [Google Scholar]

- Tradingview. 2021. Available online: https://es.tradingview.com/ (accessed on 8 June 2021).

- US Department of Justice. 2018. Drug Enforcement Administration: National Drug Threat Assessment 2018. Available online: https://www.dea.gov/sites/default/files/2018-11/DIR-032-18%202018%20NDTA%20final%20low%20resolution.pdf (accessed on 17 May 2021).

- Wronka, Christoph. 2021. Money Laundering through Cryptocurrencies—Analysis of the Phenomenon and Appropriate Prevention Measures. Journal of Money Laundering Control. [Google Scholar] [CrossRef]

| 1 | Authors’s translation. In Spanish: “Ley 10/2010, de 28 de abril, de prevención del blanqueo de capitales y de la financiación del terrorismo. «BOE» núm. 103, de 29/04/2010”. |

| 2 | Authors’s translation. In Spanish: “Real Decreto-ley 7/2021, de 27 de abril, de transposición de directivas de la Unión Europea en las materias de competencia, prevención del blanqueo de capitales, entidades de crédito, telecomunicaciones, medidas tributarias, prevención y reparación de daños medioambientales, desplazamiento de trabajadores en la prestación de servicios transnacionales y defensa de los consumidores. 2021. «BOE» núm. 101, de 28 de abril de 2021, páginas 49749 a 49924”. |

| 3 | Authors’s translation. In Spanish: “Ley Orgánica 10/1995, de 23 de noviembre, del Código Penal. «BOE» núm. 281, de 24/11/1995”. |

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| 1. Cryptocurrency mining |

| 2. Exchanges |

| 3. Local traders |

| 4. ATM |

| 5. Online videogames |

| 6. Mixers |

| 7. Suppliers of services and goods |

| 8. Bitcoin cards |

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2021 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Sanz-Bas, D.; del Rosal, C.; Náñez Alonso, S.L.; Echarte Fernández, M.Á. Cryptocurrencies and Fraudulent Transactions: Risks, Practices, and Legislation for Their Prevention in Europe and Spain. Laws 2021, 10, 57. https://doi.org/10.3390/laws10030057

Sanz-Bas D, del Rosal C, Náñez Alonso SL, Echarte Fernández MÁ. Cryptocurrencies and Fraudulent Transactions: Risks, Practices, and Legislation for Their Prevention in Europe and Spain. Laws. 2021; 10(3):57. https://doi.org/10.3390/laws10030057

Chicago/Turabian StyleSanz-Bas, David, Carlos del Rosal, Sergio Luis Náñez Alonso, and Miguel Ángel Echarte Fernández. 2021. "Cryptocurrencies and Fraudulent Transactions: Risks, Practices, and Legislation for Their Prevention in Europe and Spain" Laws 10, no. 3: 57. https://doi.org/10.3390/laws10030057

APA StyleSanz-Bas, D., del Rosal, C., Náñez Alonso, S. L., & Echarte Fernández, M. Á. (2021). Cryptocurrencies and Fraudulent Transactions: Risks, Practices, and Legislation for Their Prevention in Europe and Spain. Laws, 10(3), 57. https://doi.org/10.3390/laws10030057