Initial Value Estimation of Uncertain Differential Equations Based on Residuals with Application in Financial Market

Abstract

1. Introduction

- •

- The confidence interval and point estimation of the initial value based on the residuals corresponding to the observed data are derived.

- •

- The expressions of initial value estimations of several specific uncertain differential equations are provided, including linear, exponential, and mean-reversion uncertain differential equations.

- •

- Two numerical examples and an empirical study are also provided to illustrate the effectiveness of the proposed method.

2. Preliminaries

2.1. Uncertainty Theory

2.2. Uncertainty Differential Equation

- (i)

- and nearly all of its sample paths are Lipschitz continuous;

- (ii)

- has stationary and independent increments;

- (iii)

- Every increment is a normal uncertain variable with an expected value of 0 and a variance of .

3. Initial Value Estimation Problem of Uncertain Differential Equations

| Algorithm 1: Numerical solution of initial value estimation |

Step 0: Input observed values , initial time , and confidence level . Step 1: Determine the possible regions of the initial value. Step 2: Set initial confidence interval , a step size , , and . Step 3: For each , set Step 4: Set . Step 5: Compute and by Step 6: If , then set Otherwise, go to Step 5. Step 7: If , then . Otherwise, go to Step 9. Step 8: If , then go to Step 4. Step 9: If , then . Step 10: Repeat Steps 3 through 9 to iterate over the possible regions and obtain the confidence interval . Step 11: Compute the average value of the set , and set as the point estimation of the initial value if . Step 12: Output and (if exists). |

4. Initial Value Estimation of Several Specific Uncertain Differential Equations

5. Numerical Examples

6. IPO Price Estimation in Stock Market

6.1. Data Source

6.2. Uncertain Stock Prices Model

6.3. IPO Price Estimation

7. Conclusions

Author Contributions

Funding

Institutional Review Board Statement

Informed Consent Statement

Data Availability Statement

Acknowledgments

Conflicts of Interest

References

- Kolmogorov, A. Grundbegriffe der Wahrscheinlichkeitsrechnung; Springer: Berlin/Heidelberg, Germany, 1933. [Google Scholar]

- Itô, K. On Stochastic Differential Equations; American Mathematical Society: Providence, RI, USA, 1951. [Google Scholar]

- Kloeden, P.; Platen, E. Stochastic Differential Equations; Springer: Berlin/Heidelberg, Germany, 1992. [Google Scholar]

- Oksendal, B. Stochastic Differential Equations: An Introduction with Applications; Springer Science & Business Media: Berlin/Heidelberg, Germany, 2013. [Google Scholar]

- Higham, D.; Kloeden, P. An Introduction to the Numerical Simulation of Stochastic Differential Equations; Society for Industrial and Applied Mathematics: Philadelphia, PA, USA, 2021. [Google Scholar]

- Ye, T.; Liu, B. Uncertain significance test for regression coefficients with application to regional economic analysis. Commun. Stat.-Theory Methods 2023, 52, 7271–7288. [Google Scholar] [CrossRef]

- Jia, L.; Li, D.; Guo, F.; Zhang, B. Knock-in options of mean-reverting stock model with floating interest rate in uncertain environment. Int. J. Gen. Syst. 2024, 53, 331–351. [Google Scholar] [CrossRef]

- Liu, Z. Uncertain growth model for the cumulative number of COVID-19 infections in China. Fuzzy Optim. Decis. Mak. 2021, 20, 229–242. [Google Scholar] [CrossRef]

- Yang, L. Analysis of death toll from COVID-19 in China with uncertain time series and uncertain regression analysis. J. Uncertain Syst. 2022, 15, 2243007. [Google Scholar] [CrossRef]

- Ding, C.; Ye, T. Uncertain logistic growth model for confirmed COVID-19 cases in Brazil. J. Uncertain Syst. 2022, 15, 2243008. [Google Scholar] [CrossRef]

- Xie, J.; Lio, W. Uncertain nonlinear time series analysis with applications to motion analysis and epidemic spreading. Fuzzy Optim. Decis. Mak. 2024, 23, 279–294. [Google Scholar] [CrossRef]

- Liu, B. Fuzzy process, hybrid process and uncertain process. J. Uncertain Syst. 2008, 2, 3–16. [Google Scholar]

- Liu, B. Uncertainty Theory, 2nd ed.; Springer: Berlin/Heidelberg, Germany, 2007. [Google Scholar]

- Liu, B. Some research problems in uncertainty theory. J. Uncertain Syst. 2009, 3, 3–10. [Google Scholar]

- Chen, X.; Liu, B. Existence and uniqueness theorem for uncertain differential equations. Fuzzy Optim. Decis. Mak. 2010, 9, 69–81. [Google Scholar] [CrossRef]

- Yao, K.; Gao, J.; Gao, Y. Some stability theorems of uncertain differential equation. Fuzzy Optim. Decis. Mak. 2013, 12, 3–13. [Google Scholar] [CrossRef]

- Sheng, Y.; Wang, C. Stability in the p-th moment for uncertain differential equation. J. Intell. Fuzzy Syst. 2014, 26, 1263–1271. [Google Scholar] [CrossRef]

- Yao, K.; Ke, H.; Sheng, Y. Stability in mean for uncertain differential equation. Fuzzy Optim. Decis. Mak. 2015, 14, 365–379. [Google Scholar] [CrossRef]

- Yang, X.; Ni, Y.; Zhang, Y. Stability in inverse distribution for uncertain differential equations. J. Intell. Fuzzy Syst. 2017, 32, 2051–2059. [Google Scholar] [CrossRef]

- Yao, K.; Chen, X. A numerical method for solving uncertain differential equations. J. Intell. Fuzzy Syst. 2013, 25, 825–832. [Google Scholar] [CrossRef]

- Yang, X.; Shen, Y. Runge-Kutta method for solving uncertain differential equations. J. Uncertain Anal. Appl. 2015, 3, 17. [Google Scholar] [CrossRef]

- Yang, X.; Ralescu, D. Adams method for solving uncertain differential equations. Appl. Math. Comput. 2015, 270, 993–1003. [Google Scholar] [CrossRef]

- Gao, R. Milne method for solving uncertain differential equations. Appl. Math. Comput. 2016, 274, 774–785. [Google Scholar] [CrossRef]

- Yao, K.; Liu, B. Parameter estimation in uncertain differential equations. Fuzzy Optim. Decis. Mak. 2020, 19, 1–12. [Google Scholar] [CrossRef]

- Liu, Y.; Liu, B. Estimating unknown parameters in uncertain differential equation by maximum likelihood estimation. Soft Comput. 2022, 26, 2773–2780. [Google Scholar] [CrossRef]

- Liu, Y.; Liu, B. Residual analysis and parameter estimation of uncertain differential equations. Fuzzy Optim. Decis. Mak. 2022, 21, 513–530. [Google Scholar] [CrossRef]

- Liu, Y.; Liu, B. A modified uncertain maximum likelihood estimation with applications in uncertain statistics. Commun. Stat.-Theory Methods 2023, 53, 6649–6670. [Google Scholar] [CrossRef]

- Liu, Y.; Liu, B. Estimation of uncertainty distribution function by the principle of least squares. Commun. Stat.-Theory Methods 2023, 53, 7624–7641. [Google Scholar] [CrossRef]

- Lio, W.; Liu, B. Initial value estimation of uncertain differential equations and zero-day of COVID-19 spread in China. Fuzzy Optim. Decis. Mak. 2021, 20, 177–188. [Google Scholar] [CrossRef]

{kind=link}

{kind=link}

{kind=link}

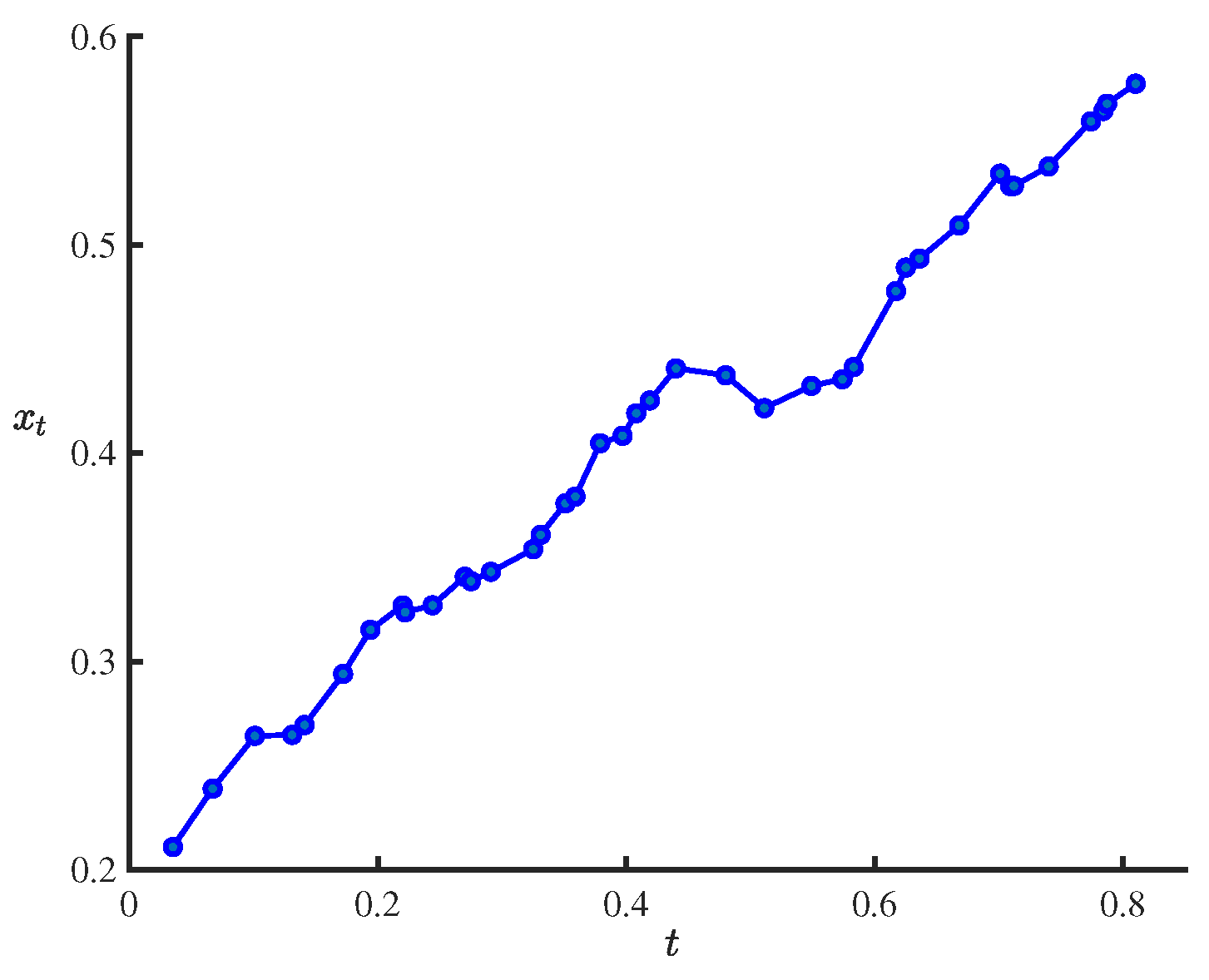

| 0.035 | 0.2109 | 0.067 | 0.2389 | 0.101 | 0.2643 | 0.131 | 0.2647 |

| 0.141 | 0.2695 | 0.172 | 0.2940 | 0.194 | 0.3152 | 0.220 | 0.3269 |

| 0.222 | 0.3236 | 0.244 | 0.3270 | 0.270 | 0.3407 | 0.275 | 0.3385 |

| 0.291 | 0.3430 | 0.325 | 0.3539 | 0.331 | 0.3608 | 0.351 | 0.3759 |

| 0.359 | 0.3792 | 0.379 | 0.4048 | 0.397 | 0.4083 | 0.408 | 0.4191 |

| 0.419 | 0.4253 | 0.440 | 0.4407 | 0.480 | 0.4374 | 0.511 | 0.4216 |

| 0.549 | 0.4323 | 0.574 | 0.4355 | 0.583 | 0.4413 | 0.617 | 0.4777 |

| 0.625 | 0.4891 | 0.636 | 0.4934 | 0.668 | 0.5093 | 0.701 | 0.5342 |

| 0.709 | 0.5283 | 0.712 | 0.5283 | 0.740 | 0.5376 | 0.774 | 0.5593 |

| 0.784 | 0.5642 | 0.787 | 0.5677 | 0.810 | 0.5773 |

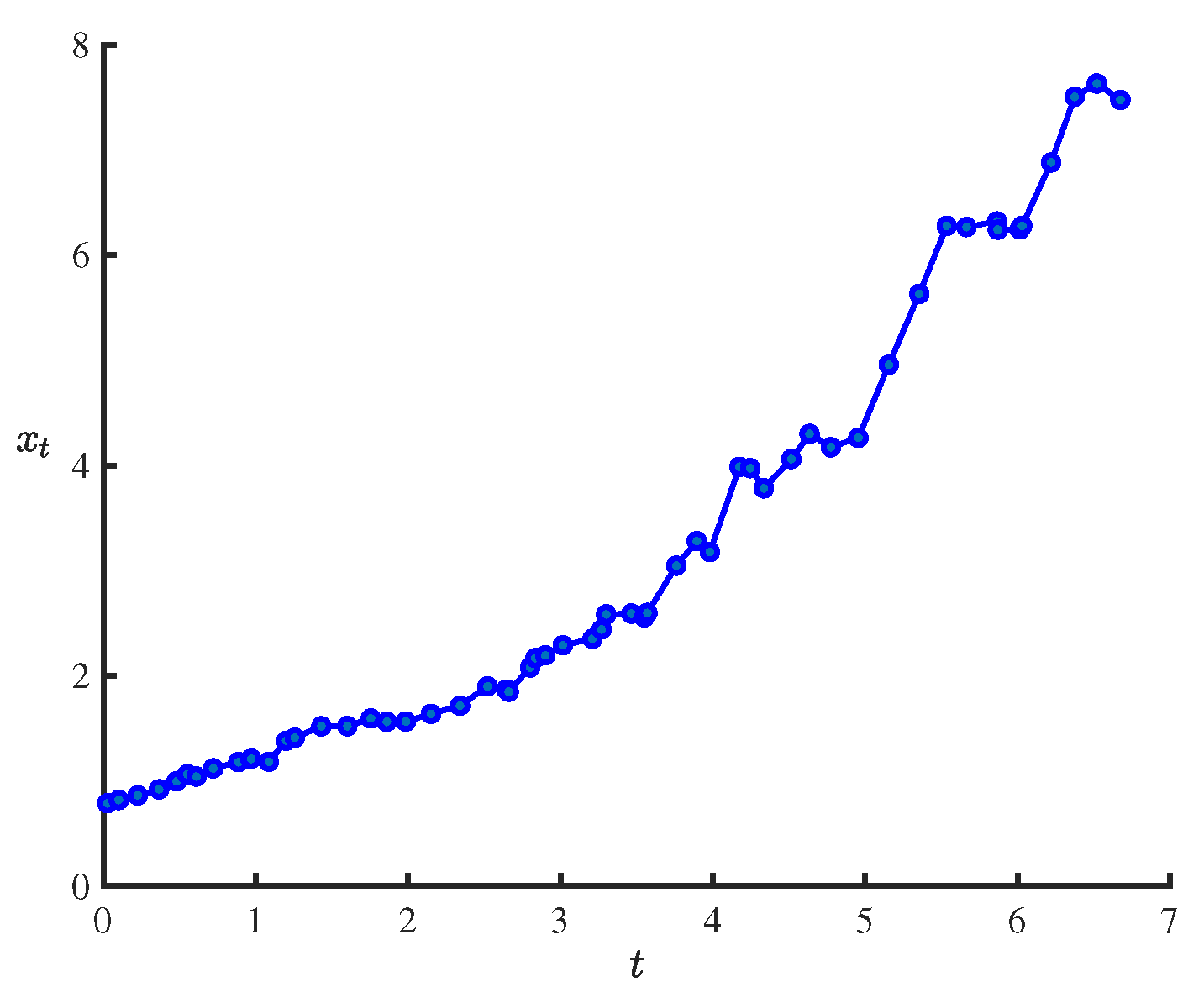

| 0.0250 | 0.7881 | 0.1000 | 0.8189 | 0.2250 | 0.8635 | 0.3650 | 0.9208 |

| 0.4800 | 0.9969 | 0.5500 | 1.0627 | 0.6100 | 1.0420 | 0.7200 | 1.1202 |

| 0.8850 | 1.1795 | 0.9650 | 1.2064 | 0.9700 | 1.2108 | 1.0850 | 1.1824 |

| 1.2000 | 1.3831 | 1.2550 | 1.4113 | 1.4300 | 1.5200 | 1.6000 | 1.5213 |

| 1.7550 | 1.5946 | 1.8600 | 1.5631 | 1.9850 | 1.5653 | 2.1500 | 1.6372 |

| 2.3400 | 1.7156 | 2.5200 | 1.8997 | 2.6450 | 1.8707 | 2.6600 | 1.8482 |

| 2.8000 | 2.0791 | 2.8350 | 2.1684 | 2.9000 | 2.1943 | 3.0150 | 2.2907 |

| 3.2100 | 2.3519 | 3.2700 | 2.4408 | 3.3000 | 2.5845 | 3.4650 | 2.5918 |

| 3.5500 | 2.5569 | 3.5700 | 2.5979 | 3.7600 | 3.0474 | 3.8950 | 3.2799 |

| 3.9800 | 3.1765 | 4.1750 | 3.9873 | 4.2450 | 3.9745 | 4.3350 | 3.7825 |

| 4.5150 | 4.0610 | 4.6350 | 4.2998 | 4.7750 | 4.1735 | 4.9550 | 4.2633 |

| 5.1550 | 4.9579 | 5.3550 | 5.6321 | 5.5350 | 6.2784 | 5.6650 | 6.2671 |

| 5.8650 | 6.3201 | 5.8700 | 6.2420 | 6.0150 | 6.2449 | 6.0300 | 6.2781 |

| 6.2200 | 6.8810 | 6.3750 | 7.5052 | 6.5200 | 7.6322 | 6.6750 | 7.4769 |

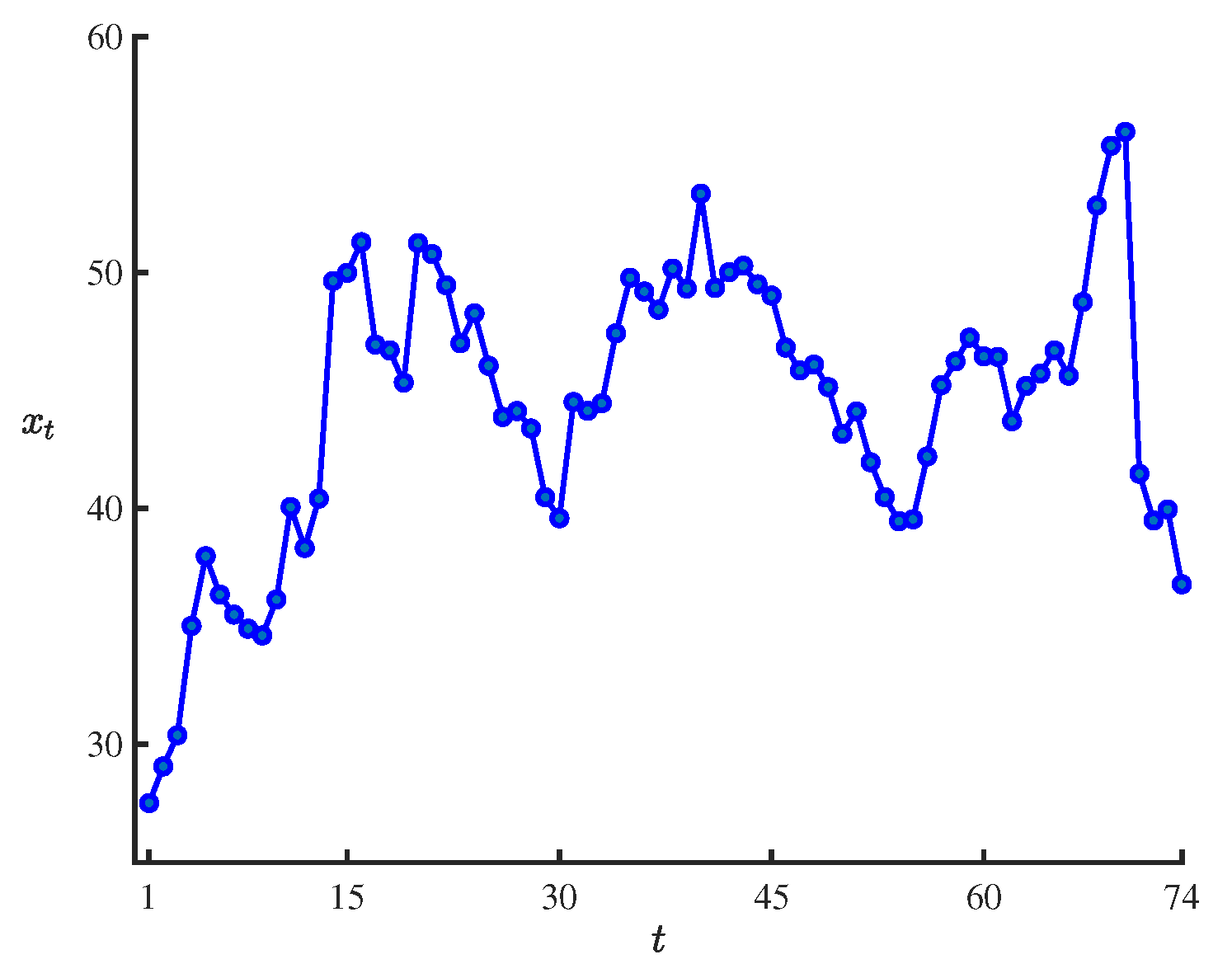

| 27.5225 | 29.0720 | 30.3960 | 35.0280 | 37.9820 | 36.3560 | 35.5040 | 34.9060 | 34.6220 |

| 36.1400 | 40.0660 | 38.3300 | 40.4225 | 49.6440 | 49.9920 | 51.2880 | 46.9500 | 46.7060 |

| 45.3400 | 51.2520 | 50.7860 | 49.4660 | 47.0040 | 48.2733 | 46.0500 | 43.8820 | 44.1300 |

| 43.3920 | 40.4820 | 39.5900 | 44.5140 | 44.1420 | 44.4600 | 47.4280 | 49.7780 | 49.1960 |

| 48.4260 | 50.1675 | 49.3260 | 53.3400 | 49.3540 | 50.0200 | 50.2900 | 49.5060 | 49.0240 |

| 46.8240 | 45.8560 | 46.1000 | 45.1460 | 43.1680 | 44.1125 | 41.9620 | 40.4820 | 39.4640 |

| 39.5460 | 42.2050 | 45.2280 | 46.2360 | 47.2440 | 46.4520 | 46.4280 | 43.7020 | 45.1967 |

| 45.7200 | 46.6980 | 45.6320 | 48.7500 | 52.8420 | 55.3740 | 55.9640 | 41.4760 | 39.4940 |

| 39.9575 | 36.7900 |

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2025 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Lio, W.; Liu, Y. Initial Value Estimation of Uncertain Differential Equations Based on Residuals with Application in Financial Market. Axioms 2025, 14, 133. https://doi.org/10.3390/axioms14020133

Lio W, Liu Y. Initial Value Estimation of Uncertain Differential Equations Based on Residuals with Application in Financial Market. Axioms. 2025; 14(2):133. https://doi.org/10.3390/axioms14020133

Chicago/Turabian StyleLio, Waichon, and Yang Liu. 2025. "Initial Value Estimation of Uncertain Differential Equations Based on Residuals with Application in Financial Market" Axioms 14, no. 2: 133. https://doi.org/10.3390/axioms14020133

APA StyleLio, W., & Liu, Y. (2025). Initial Value Estimation of Uncertain Differential Equations Based on Residuals with Application in Financial Market. Axioms, 14(2), 133. https://doi.org/10.3390/axioms14020133