Here, we carry out a stability analysis of the order (1,2) predictor–corrector fourth-order compact finite difference scheme. Because we use a one-step predictor scheme and three implicit correction steps at each time-level, it is observable that the influence of the correction scheme will become dominant. Moreover, the optimal exercise boundary, left boundary values and the time dependent coefficient in the model are predicted and further corrected at each stage of the three implicit correction step based on the optimal exercise boundary equation and the scheme presented in (

31) and (

27), respectively. To this end, we first investigate the stability of the high-order correction scheme with three iterative steps as given below.

Our analysis follows the matrix form of the von Neumann stability analysis and we let the Fourier modes

Note that

Let

. Substituting (

54) into (

52) and (

51), we obtain

If we denote

then we obtain two systems of equations as follows:

Presenting (

61) and (

62) in matrix form, we obtain

Denote

Thus, we have

Here, it is important to observe that the two matrices

and

are not constant due to the time-dependent coefficients. We have to ensure that

is invertible. This indicates that the determinant of

should not be zero at any time-level

n. Note that

Furthermore, because

, we have

, implying

Hence, we can invert both matrices

and

even though both matrices are time-dependent, which gives

Simplifying further, we obtain

where

is the amplification matrix. Let

represent the eigenvalue of the matrix

. To confirm the unconditional stability of the coupled implicit discrete system, we need to show that

. It can be seen that

satisfies

in which the solutions are

Note that we obtain

and the complex solutions

where

j =

. For simplicity, let

. Hence, we obtain

Simplifying further, we then obtain that

Hence, the interior implicit three-step correction scheme based on the second-order CN time integration method and fourth-order compact finite difference scheme is unconditionally stable.

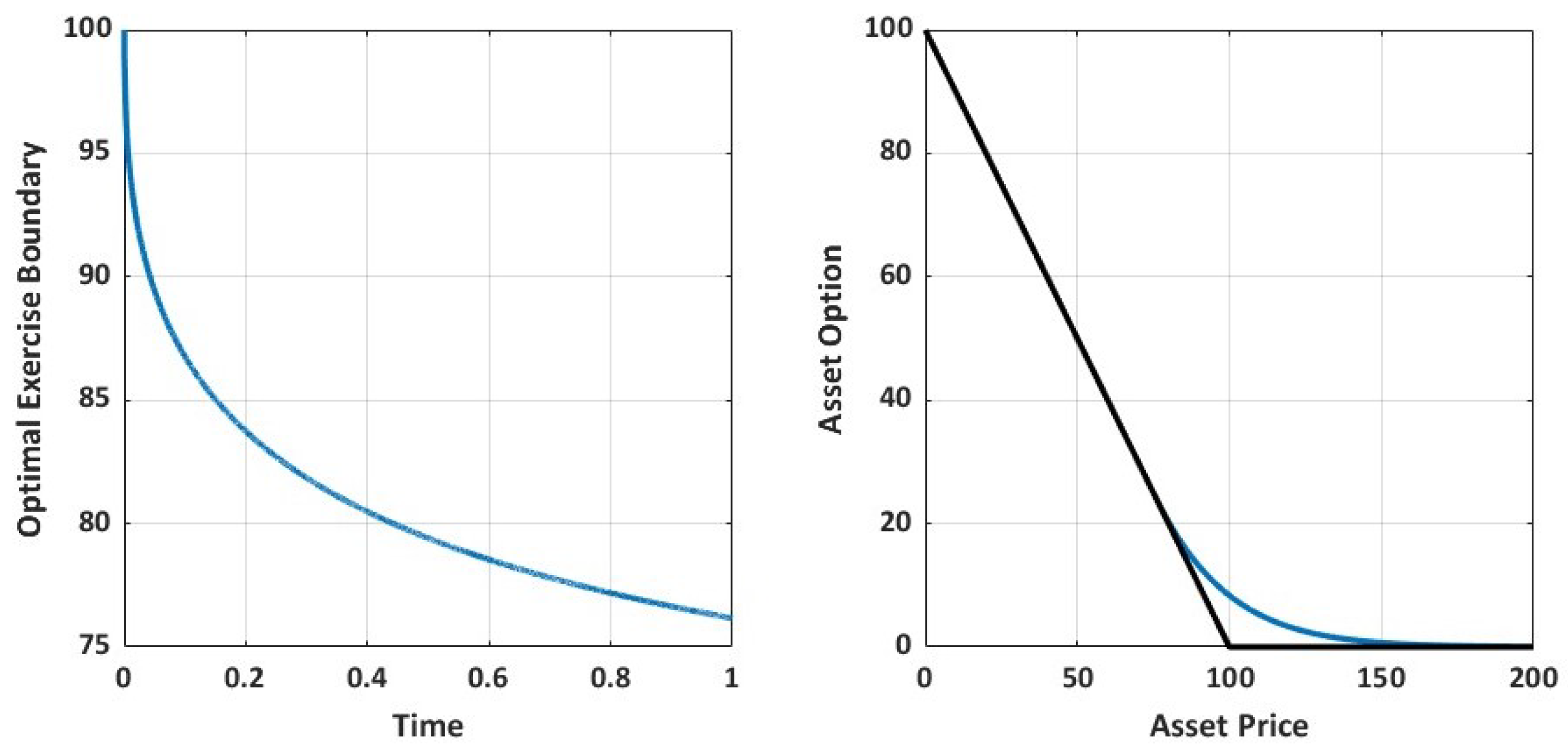

Next, we navigate the stability of the boundary Euler scheme for predicting the optimal exercise boundary, left boundary values of the option value and the delta sensitivity, and the time-dependent coefficient of the convective term. To this end, we recall the optimal exercise boundary predictor equation:

where

To ensure the stability of (

71), we need

which implies

From (

30), we can further deduce the term in (

74) as follows:

where

. For simplicity, let

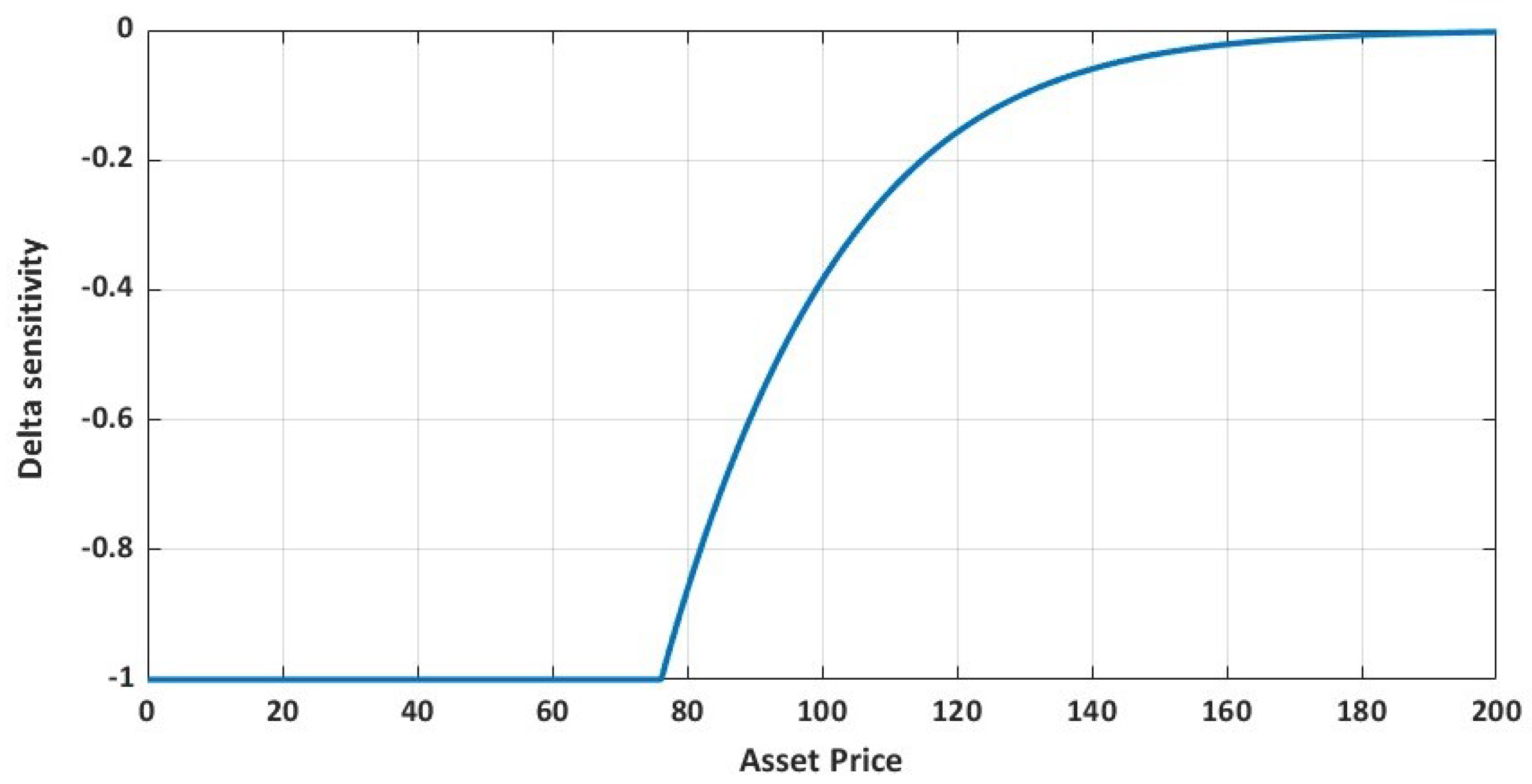

Note that the delta sensitivity is monotonically increasing and non-positive with

Moreover, the optimal exercise boundary is monotonically decreasing with

We refer the reader to the work of Kwok [

14], Musiela [

15], and Zhang et al. [

16] for details. Thus, we have

and

. Denote

Then, (

74) becomes

Note that

implying that

To ensure that

, we have to confirm

From (

76)–(

79), we have confirmed that

. Moreover, we see that

Since the first derivative of the optimal exercise boundary

is non-positive

, when

h is very small, we obtain

and

Next, we verify the right bound as given below

Simplifying further, we then obtain

Considering the non-positivity of the delta sensitivity coupled with an extrapolated Taylor series expansion, we can further obtain

Considering the left boundary value of the delta sensitivity and implied second derivative left boundary condition, we further obtain

Hence, with (

76) and a very small

h, we can obtain

Substituting to (

90), we then obtain

Note that

Let

Thus,

Here, we need to further obtain at least a reasonable upper bound for

in (

98) given as

To this end, we further simplify the denominator of (

99). Let

. If we derive Taylor series expansion around

, we further obtain the following:

If we consider (

100), (

101), left boundary values of the option value and delta sensitivity, and the implied left boundary value of the second derivative of the option value, we can further simplify the terms in

and

given in (

96) and (

97) as follows:

Note that

Substituting them into (

96) and (

97), we obtain

Furthermore, for a very small

h, we have

With further simplification of (

112), we obtain

Hence, we have

Here,

, where

is defined in (

78). For a very small

h, we further obtain

Thus, we have

and

To conclude our proof, we need to ensure that

which implies that

Hence, we conclude that if the assumption in (

119) holds, then

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}