Optimal Consumption, Investment, and Housing Choice: A Dynamic Programming Approach

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Abstract

:1. Introduction

2. Related Literature

3. Model

4. Analytic Solutions

4.1. Value Function after Time of Purchase

4.2. Value Function before Time of Purchase

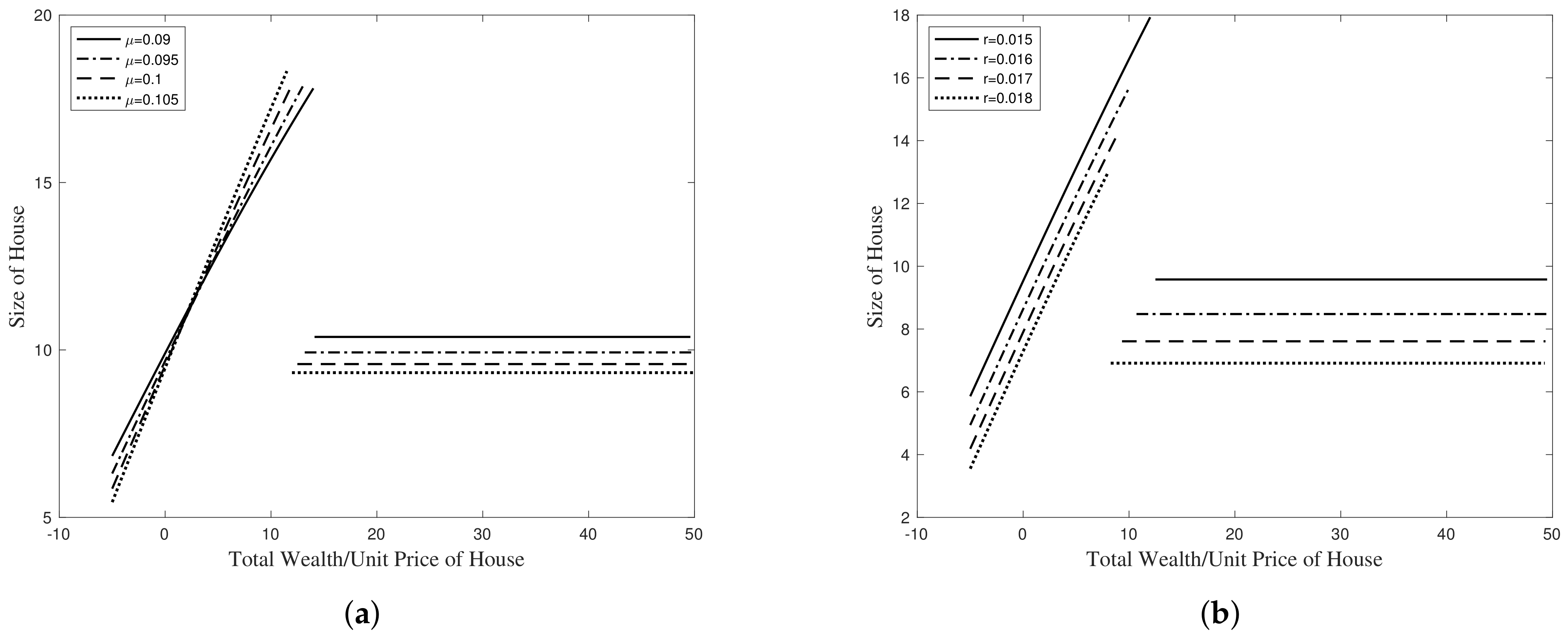

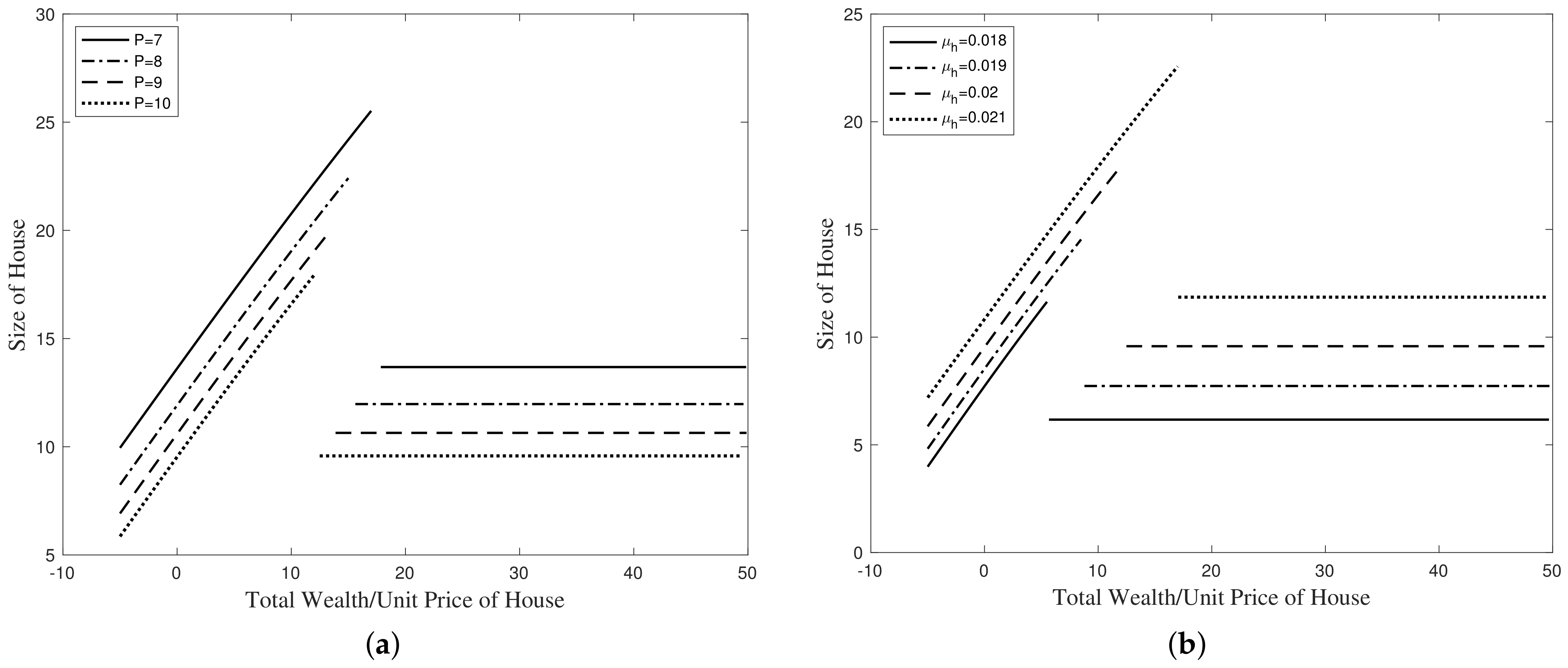

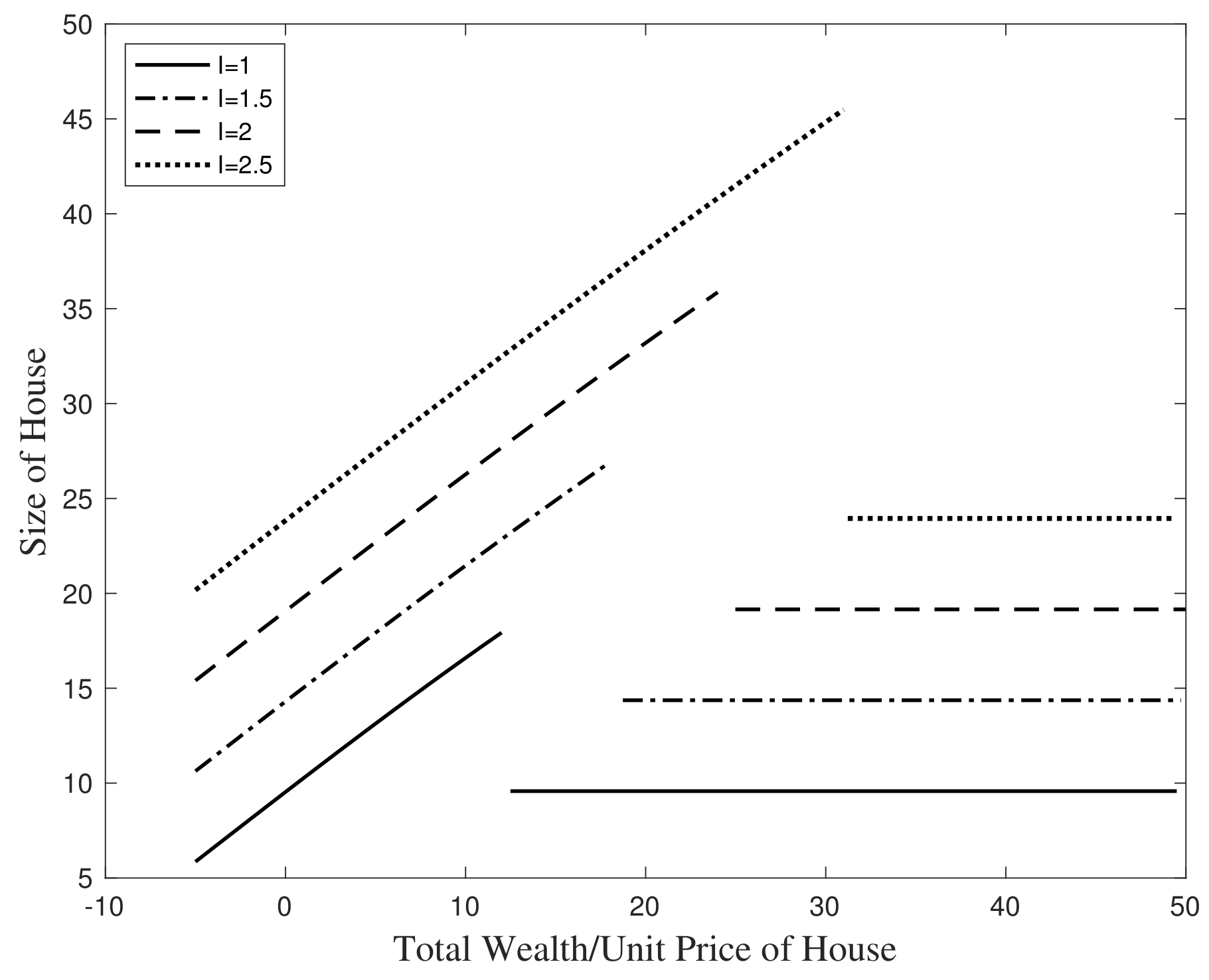

5. Numerical Demonstrations and Implications

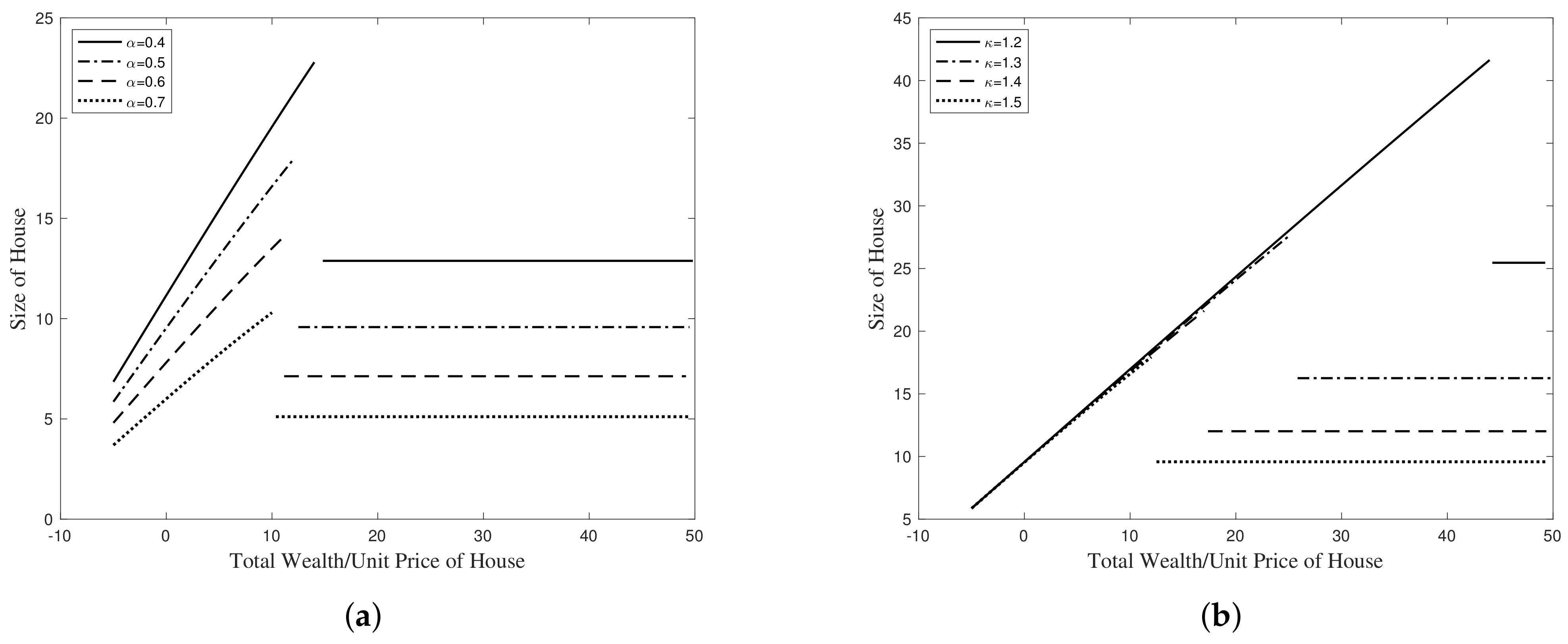

5.1. Housing Choice

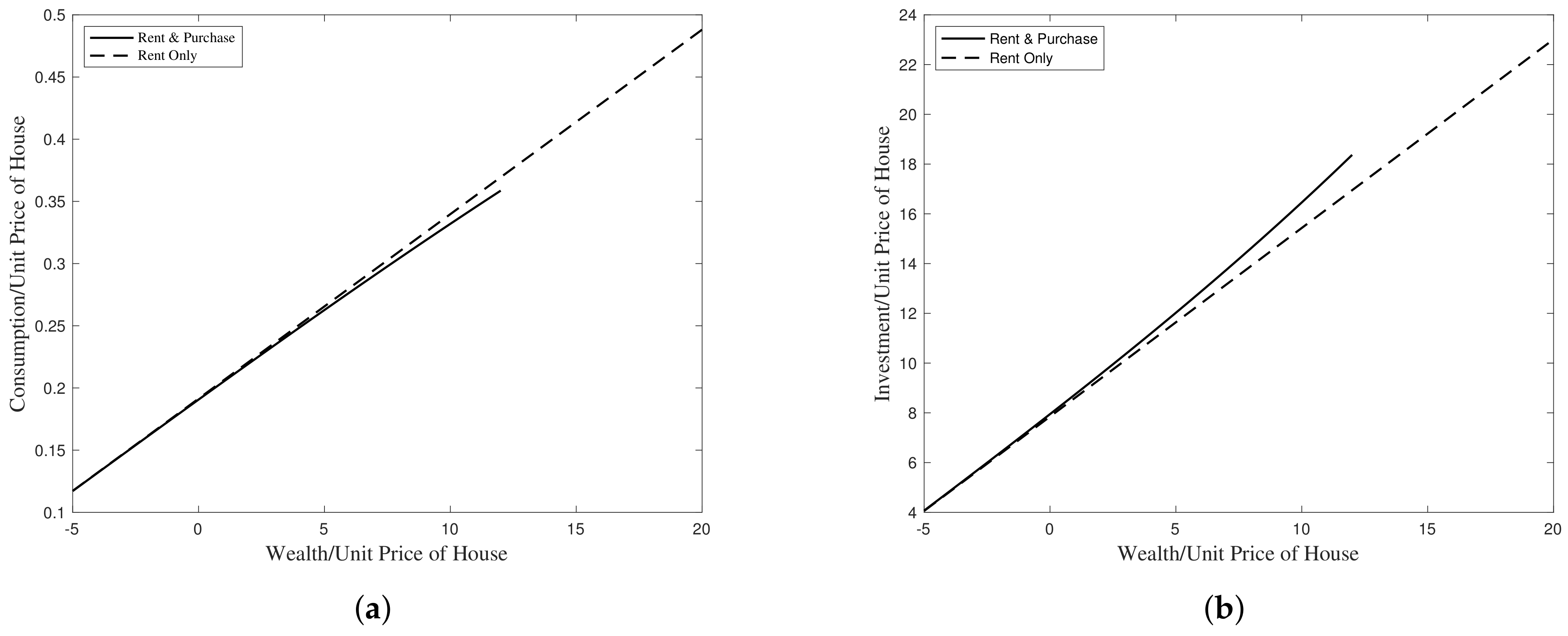

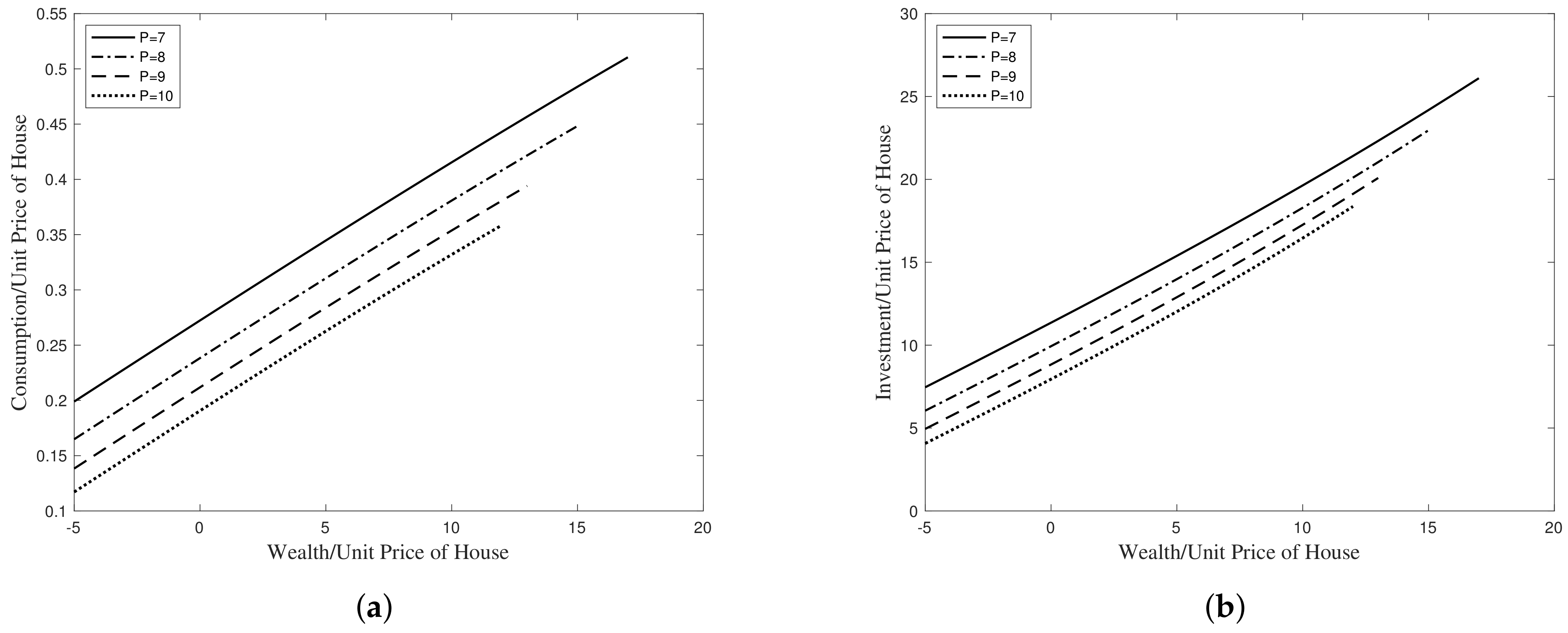

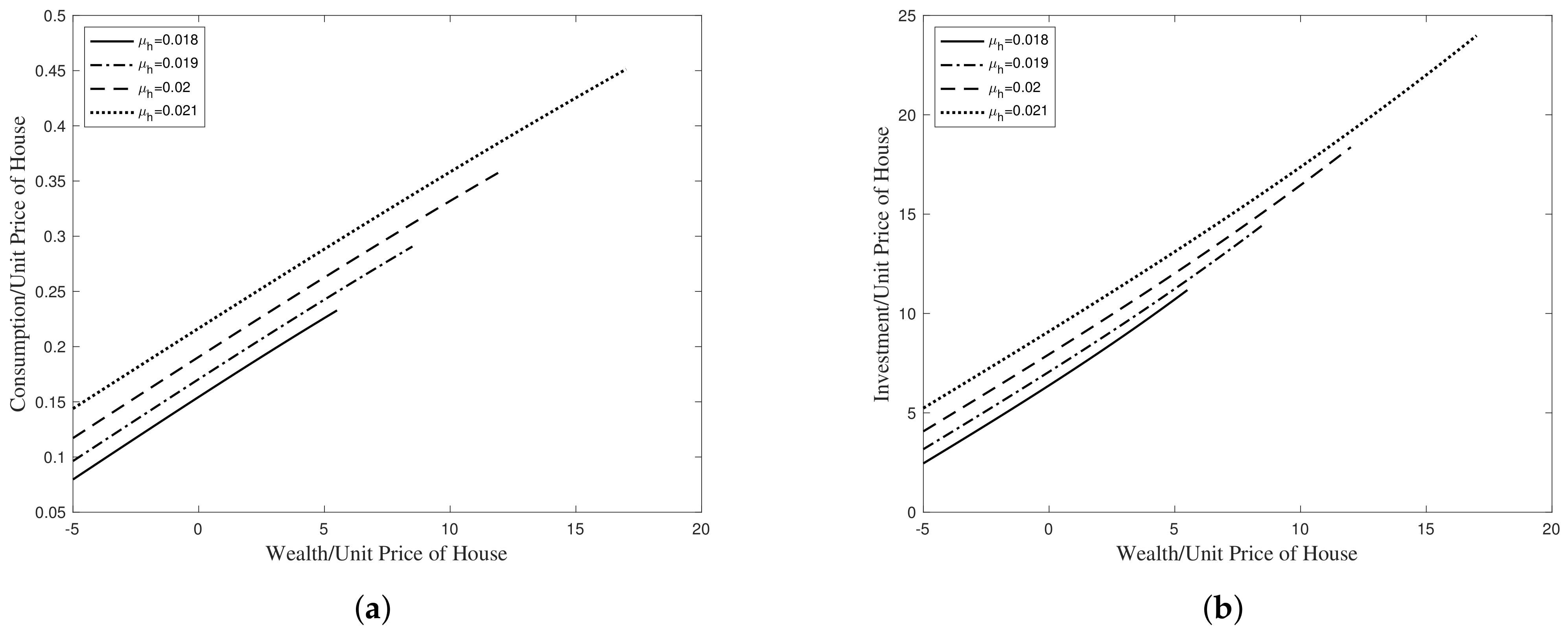

5.2. Consumption and Investment

6. Conclusions

Author Contributions

Funding

Institutional Review Board Statement

Informed Consent Statement

Data Availability Statement

Conflicts of Interest

Appendix A. Detailed Proof of Theorem 2

Appendix B. Solution to Problem 3

References

- Grossman, S.J.; Laroque, G. Asset Pricing and Optimal Portfolio Choice in the Presence of Illiquid Durable Consumption Goods. Econometrica 1990, 58, 25–51. [Google Scholar] [CrossRef]

- Cocco, J.F. Portfolio Choice in the Presence of Housing. Rev. Financ. Stud. 2005, 18, 535–567. [Google Scholar] [CrossRef]

- Karatzas, I.; Lehoczky, J.P.; Sethi, S.P.; Shreve, S.E. Explicit Solution of a General Consumption/Investment Problem. Math. Oper. Res. 1986, 11, 261–294. [Google Scholar] [CrossRef]

- Merton, R.C. Lifetime Portfolio Selection under Uncertainty: The Continuous-Time Case. Rev. Econ. Stat. 1969, 51, 247–257. [Google Scholar] [CrossRef] [Green Version]

- Merton, R.C. Optimum Consumption and Portfolio Rules in a Continuous-Time Model. J. Econ. Theory 1971, 3, 373–413. [Google Scholar] [CrossRef] [Green Version]

- Choi, K.J.; Shim, G. Disutility, Optimal Retirement, and Portfolio Selection. Math. Financ. 2006, 16, 443–467. [Google Scholar] [CrossRef]

- Farhi, E.; Panageas, S. Saving and Investing for Early Retirement: A Theoretical Analysis. J. Financ. Econ. 2007, 83, 87–121. [Google Scholar] [CrossRef]

- Dybvig, P.H.; Liu, H. Lifetime Consumption and Investment: Retirement and Constrained Borrowing. J. Econ. Theory 2010, 145, 885–907. [Google Scholar] [CrossRef] [Green Version]

- Lim, B.H.; Shin, Y.H.; Choi, U.J. Optimal Investment, Consumption, and Retirement Choice Problem with Disutility and Subsistence Consumption Constraints. J. Math. Anal. Appl. 2008, 345, 109–122. [Google Scholar] [CrossRef]

- Lee, H.-S.; Shin, Y.H. An Optimal Consumption, Investment and Voluntary Retirement Choice Problem with Disutility and Subsistence Consumption Constraints: A Dynamic Programming Approach. J. Math. Anal. Appl. 2015, 428, 762–771. [Google Scholar] [CrossRef]

- Choi, K.J.; Shim, G.; Shin, Y.H. Optimal Portfolio, Consumption-Leisure and Retirement Choice Problem with CES Utility. Math. Financ. 2008, 18, 445–472. [Google Scholar] [CrossRef]

- Shin, Y.H. Voluntary Retirement and Portfolio Selection: Dynamic Programming Approaches. Appl. Math. Lett. 2012, 25, 1087–1093. [Google Scholar] [CrossRef] [Green Version]

- Ahn, S.; Choi, K.J.; Lim, B.H. Optimal Consumption and Investment under Time-Varying Liquidity Constraints. J. Financ. Quant. Anal. 2019, 54, 1643–1681. [Google Scholar] [CrossRef]

- Detemple, J.; Serrat, A. Dynamic Equilibrium with Liquidity Constraints. Rev. Financ. Stud. 2003, 16, 597–629. [Google Scholar] [CrossRef]

- Duffie, D.; Fleming, W.H.; Soner, H.M.; Zariphopoulou, T. Hedging in Incomplete Markets with HARA Utility. J. Econ. Dyn. Control 1997, 21, 753–782. [Google Scholar] [CrossRef] [Green Version]

- El Karoui, N.; Jeanblanc-Picqué, M. Optimization of Consumption with Labor Income. Financ. Stoch. 1998, 2, 409–440. [Google Scholar] [CrossRef]

- He, H.; Pagès, H.F. Labor Income, Borrowing Constraints, and Equilibrium Asset Prices. Econ. Theory 1993, 3, 663–696. [Google Scholar] [CrossRef]

- Dybvig, P.H. Dusenberry’s Ratcheting of Consumption: Optimal Dynamic Consumption and Investment Given Intolerance for Any Decline in Standard of Living. Rev. Econ. Stud. 1995, 62, 287–313. [Google Scholar] [CrossRef]

- Gong, N.; Li, T. Role of Index Bonds in an Optimal Dynamic Asset Allocation Model with Real Subsistence Consumption. Appl. Math. Comput. 2006, 174, 710–731. [Google Scholar] [CrossRef]

- Koo, J.L.; Ahn, S.; Koo, B.L.; Koo, H.K.; Shin, Y.H. Optimal Consumption and Portfolio Selection with Quadratic Utility and a Subsistence Consumption Constraint. Stoch. Anal. Appl. 2016, 34, 165–177. [Google Scholar] [CrossRef]

- Shin, Y.H.; Koo, J.L.; Roh, K.-H. An Optimal Consumption and Investment Problem with Quadratic Utility and Subsistence Consumption Constraints: A Dynamic Programming Approach. Math. Model. Anal. 2018, 23, 627–638. [Google Scholar] [CrossRef]

- Yuan, H.; Hu, Y. Optimal Consumption and Portfolio Policies with the Consumption Habit Constraints and the Terminal Wealth Downside Constraints. Insur. Math. Econ. 2009, 45, 405–409. [Google Scholar] [CrossRef]

- Ahn, S.; Ryu, D. The Optimal Chonsei to Monthly-Rent Conversion Choice Given Borrowing Constraints; Working Paper; Pukyong National University: Busan, Korea, 2022. [Google Scholar]

- Yao, R.; Zhang, H.H. Optimal Consumption and Portfolio Choices with Risky Housing and Borrowing Constraints. Rev. Financ. Stud. 2005, 18, 197–239. [Google Scholar] [CrossRef]

- Yogo, M. Portfolio Choice in Retirement: Health Risk and the Demand for Annuities, Housing, and Risky Assets. J. Monet. Econ. 2016, 80, 17–34. [Google Scholar] [CrossRef] [Green Version]

- Flavin, M.; Yamashita, T. Owner-Occupied Housing and the Composition of the Household Portfolio. Am. Econ. Rev. 2002, 92, 345–362. [Google Scholar] [CrossRef]

- Chetty, R.; Sándor, L.; Szeidl, A. The Effect of Housing on Portfolio Choice. J. Financ. 2017, 72, 1171–1212. [Google Scholar] [CrossRef]

- Nils, C.F.; Bernt, Ø.; Agnès, S. Optimal Consumption and Portfolio in a Jump Diffusion Market with Proportional Transaction Costs. J. Math. Econ. 2001, 35, 233–257. [Google Scholar]

- Aït-Sahalia, Y.; Cacho-Diaz, J.; Hurd, T.R. Portfolio Choice with Jumps: A Closed-Form Solution. Ann. Appl. Probab. 2009, 19, 556–584. [Google Scholar] [CrossRef]

- Chacko, G.; Viceira, L.M. Dynamic Consumption and Portfolio Choice with Stochastic Volatility in Incomplete Markets. Rev. Financ. Stud. 2005, 18, 1369–1402. [Google Scholar] [CrossRef] [Green Version]

- Liu, J. Portfolio Selection in Stochastic Environments. Rev. Financ. Stud. 2006, 20, 1–39. [Google Scholar] [CrossRef]

- Lin, M.; SenGupta, I. Analysis of Optimal Portfolio on Finite and Small-Time Horizons for a Stochastic Volatility Market Model. SIAM J. Financ. Math. 2021, 12, 1596–1624. [Google Scholar] [CrossRef]

- Hu, Y.; Øksendal, B.; Sulem, A. Optimal Consumption and Portfolio in a Black-Scholes Market Driven by Fractional Brownian Motion. Infin. Dimens. Anal. Quantum Probab. Relat. Top. 2003, 6, 519–536. [Google Scholar] [CrossRef]

- Salmon, N.; SenGupta, I. Fractional Barndorff-Nielsen and Shephard Model: Applications in Variance and Volatility Swaps, and Hedging. Ann. Financ. 2021, 17, 529–558. [Google Scholar] [CrossRef]

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2022 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Li, Q.; Ahn, S. Optimal Consumption, Investment, and Housing Choice: A Dynamic Programming Approach. Axioms 2022, 11, 127. https://doi.org/10.3390/axioms11030127

Li Q, Ahn S. Optimal Consumption, Investment, and Housing Choice: A Dynamic Programming Approach. Axioms. 2022; 11(3):127. https://doi.org/10.3390/axioms11030127

Chicago/Turabian StyleLi, Qi, and Seryoong Ahn. 2022. "Optimal Consumption, Investment, and Housing Choice: A Dynamic Programming Approach" Axioms 11, no. 3: 127. https://doi.org/10.3390/axioms11030127

APA StyleLi, Q., & Ahn, S. (2022). Optimal Consumption, Investment, and Housing Choice: A Dynamic Programming Approach. Axioms, 11(3), 127. https://doi.org/10.3390/axioms11030127