A Decision Support Model for Measuring Technological Progress and Productivity Growth: The Case of Commercial Banks in Vietnam

Abstract

1. Introduction

2. Literature Review

3. Materials and Methods

3.1. Research Methodology

3.2. Mathematical Modeling Approach

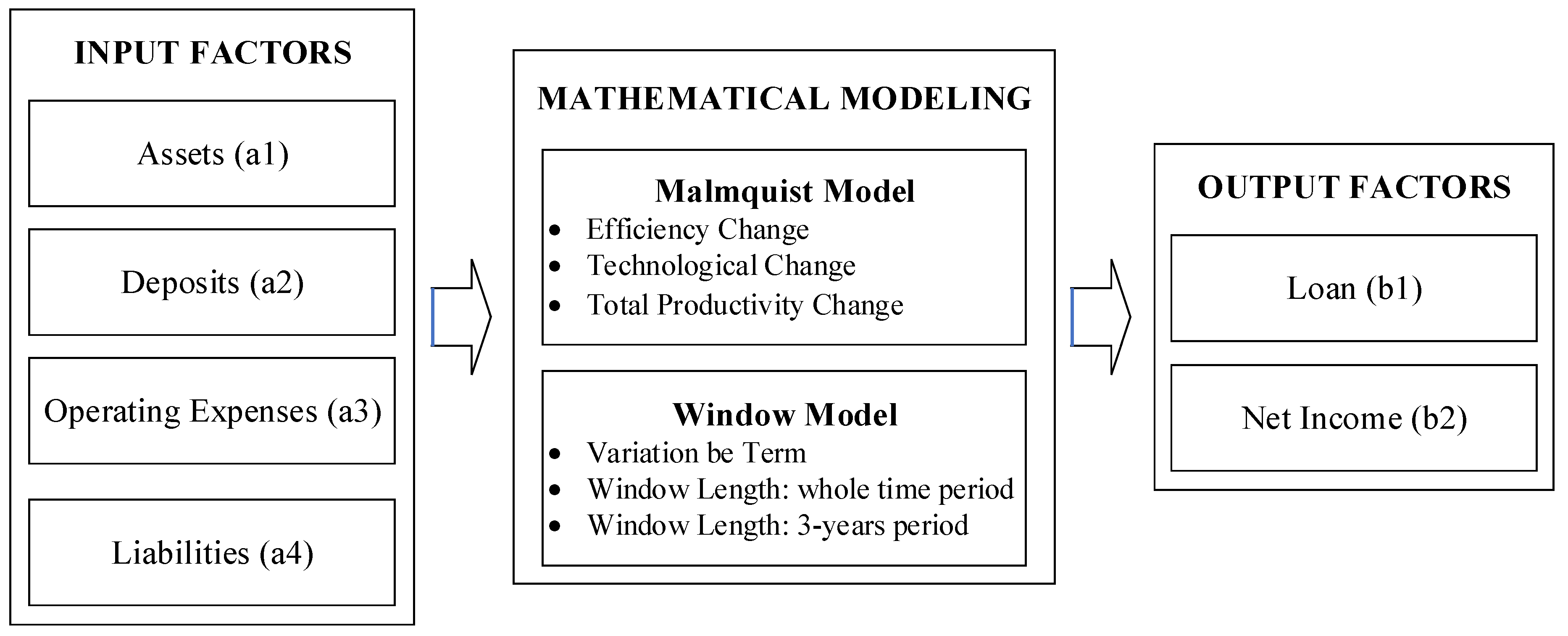

3.2.1. Modeling Framework

- 1.

- Assets (a1): the amount of the total assets maintained by the bank that can be sold for value (i.e., belongings, interchange assets, customer’s loans, deposits to the headquarter).

- 2.

- Deposits (a2): the total amount of deposits from customers and other banks.

- 3.

- Operating expenses (a3): expenditure incurred by banking firms (i.e., employee compensation and benefits, information technology, legal fees).

- 4.

- Liabilities (a4): a commitment that must eventually be paid (i.e., loans from the headquarter, customer’s deposits, interchange liabilities, non-performing loans).

- 5.

- Loan (b1): referred to as a lending of money by customers, business, or company. It reflects the ability to provide financial services.

- 6.

- Net Income (b2): refer to net interest income of the bank, is calculated by the interest payment on assets minus the interest payment on liabilities.

3.2.2. Pearson Correlation

3.2.3. DEA Malmquist Model

3.2.4. DEA Window Model

4. A Case Study

4.1. The Selection of DMUs

4.2. Data Collection

5. Results Analysis

5.1. Pearson Correlation Coefficient Test

5.2. Productivity Growth Evaluation

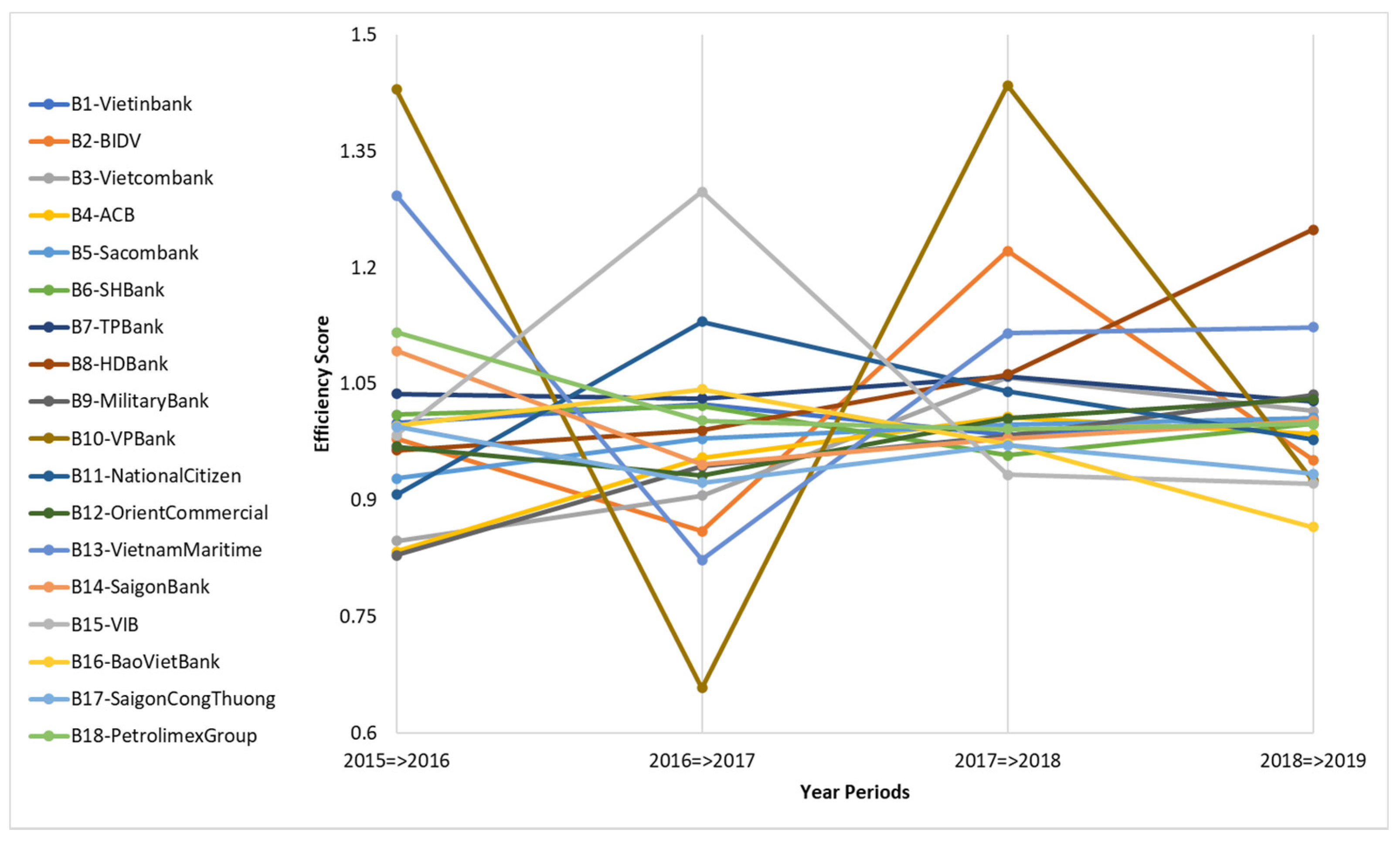

5.2.1. Technical Efficiency Change (Catch-Up Index)

5.2.2. Technological Change (Frontier-Shift Index)

5.2.3. Malmquist Productivity Indicator (MPI)

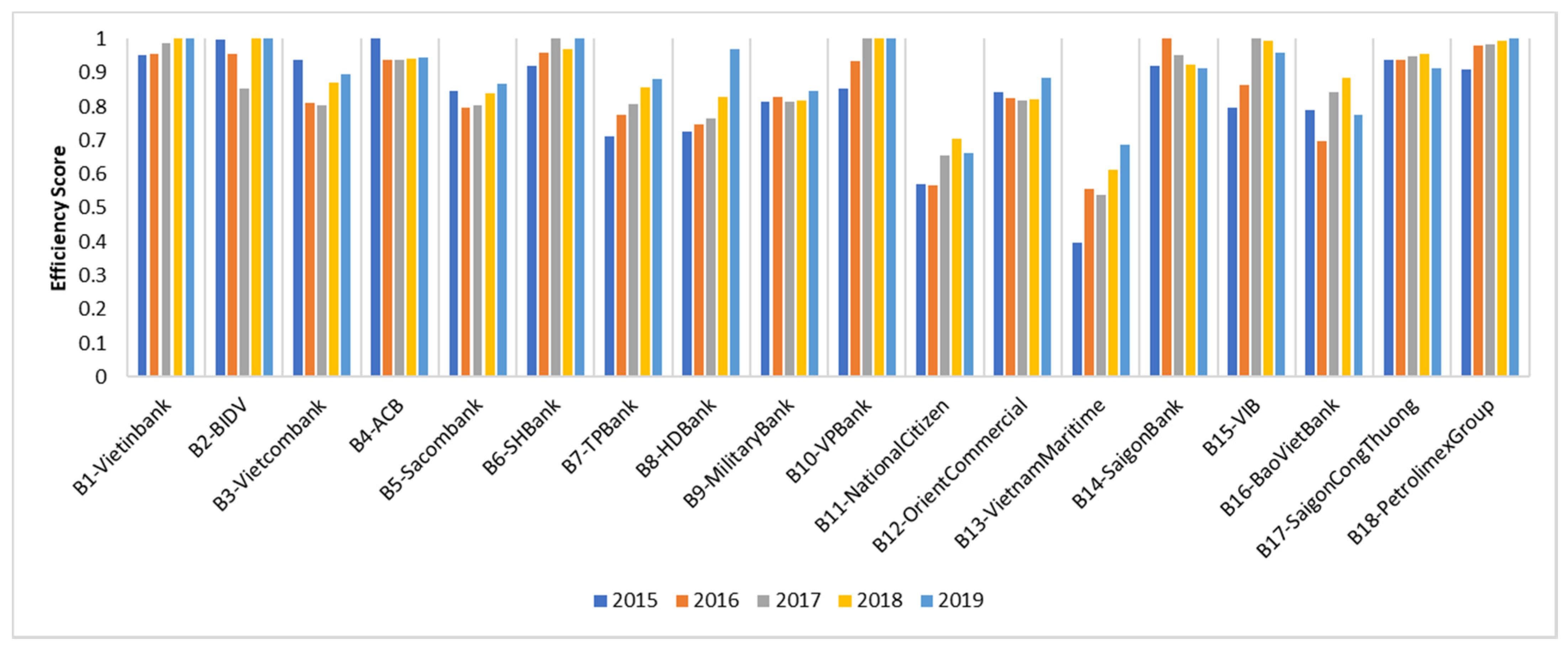

5.3. DEA Window Analysis

5.3.1. DEA Window of the Whole Period

5.3.2. DEA Window of 3-Year Period

6. Discussions and Conclusions

Author Contributions

Funding

Acknowledgments

Conflicts of Interest

References

- COVID-19 Hits Profitability of National Banking Sector. Available online: https://customsnews.vn/covid-19-hits-profitability-of-national-banking-sector-14135.html (accessed on 14 May 2021).

- Banking Sector Reviews Effects of Covid-19 Pandemic Prepare for Difficult Year. Available online: https://vietnamnews.vn/economy/business-beat/716434/banking-sector-reviews-effects-of-covid-19-pandemic-prepare-for-difficult-year.html (accessed on 14 May 2021).

- Batten, J.A.; Vo, X.V. Determinants of Bank Profitability–Evidence from Vietnam. Emerg. Markets Financ. Trade 2019, 55, 1417–1428. [Google Scholar] [CrossRef]

- Assaf, A.G.; Berger, A.N.; Roman, R.A.; Tsionas, M.G. Does efficiency help banks survive and thrive during financial crises? J. Bank. Financ. 2019, 106, 445–470. [Google Scholar] [CrossRef]

- Paradi, J.C.; Zhu, H. A survey on bank branch efficiency and performance research with data envelopment analysis. Omega 2013, 41, 61–79. [Google Scholar] [CrossRef]

- Avkiran, N.K.; Cai, L. Identifying distress among banks prior to a major crisis using non-oriented super-SBM. Ann. Oper. Res. 2014, 217, 31–53. [Google Scholar] [CrossRef]

- Avkiran, N.K. An illustration of dynamic network DEA in commercial banking including robustness tests. Omega 2015, 55, 141–150. [Google Scholar] [CrossRef]

- Mohtashami, A.; Ghiasvand, B.M. Z-ERM DEA integrated approach for evaluation of banks & financial institutes in stock exchange. Expert Syst. Appl. 2020, 147, 113218. [Google Scholar]

- Dang-Thanh, N. Measuring the performance of the banking system: Case of Vietnam (1990–2010). J. Appl. Financ. Bank. 2012, 2, 289–312. [Google Scholar]

- Cuong, D.X.; Hien, H.T.; Long, T. Multi-Criteria Decision-Making Model Evaluating the Performance of Vietnamese Commercial Banks. Int. J. Financ. Res. 2018, 9, 132–141. [Google Scholar] [CrossRef]

- Tlig, H.; Hamed, A. Assessing the Efficiency of commercial Tunisian Banks using Fuzzy Data Envelopment Analysis. J. Data Envel. Anal. Decis. Sci. 2017, 2, 14–27. [Google Scholar] [CrossRef][Green Version]

- Banker, R.D.; Chang, H.; Lee, S.Y. Differential impact of Korean banking system reforms on bank productivity. J. Bank. Financ. 2010, 34, 1450–1460. [Google Scholar] [CrossRef]

- Paradi, J.C.; Sherman, H.D.; Tam, F.K. Bank branch benchmarking with quality as a component. In Data Envelopment Analysis in the Financial Services Industry; Springer: Cham, Switzerland, 2018; pp. 159–184. [Google Scholar]

- Avkiran, N.K. Measuring the systemic risk of regional banks in Japan with PLS-SEM. Theor. Econ. Lett. 2018, 8, 2024. [Google Scholar] [CrossRef]

- Dincer, H.; Hacioglu, Ü.; Celik, I.E. The Game Theory and Reflections on Competitive Strategies in the Banking Sector. In Managerial Issues in Finance and Banking; Springer: Cham, Switzerland, 2014; pp. 145–153. [Google Scholar]

- Dahlstrom, R.; Nygaard, A.; Kimasheva, M.; Ulvnes, A.M. How to recover trust in the banking industry? A game theory approach to empirical analyses of bank and corporate customer relationships. Int. J. Bank Mark. 2014, 32, 268–278. [Google Scholar] [CrossRef]

- Khanizad, R.; Montazer, G. Participation against competition in banking markets based on cooperative game theory. J. Financ. Data Sci. 2018, 4, 16–28. [Google Scholar] [CrossRef]

- Panjaitan, A. Application of Game Theory in Determining the Optimum Marketing Mix Strategy in Banking Companies. Int. J. Basic Appl. Sci. 2020, 9, 53–57. [Google Scholar]

- Zandi, F.; Tavana, M.; O’Connor, A. A strategic cooperative game-theoretic model for market segmentation with application to banking in emerging economies. Technol. Econ. Dev. Econ. 2012, 18, 389–423. [Google Scholar] [CrossRef]

- Wang, C.N.; Tsai, T.T.; Hsu, H.P.; Nguyen, L.H. Performance evaluation of major Asian airline companies using DEA window model and grey theory. Sustainability 2019, 11, 2701. [Google Scholar] [CrossRef]

- Wang, C.N.; Tibo, H.; Duong, D.H. Renewable Energy Utilization Analysis of Highly and Newly Industrialized Countries Using an Undesirable Output Model. Energies 2020, 13, 2629. [Google Scholar] [CrossRef]

- Novickytė, L.; Droždz, J. Measuring the efficiency in the Lithuanian banking sector: The DEA application. Int. J. Financ. Stud. 2018, 6, 37. [Google Scholar] [CrossRef]

- Xu, T.; You, J.; Shao, Y. Efficiency of China’s Listed Securities Companies: Estimation through a DEA-Based Method. Mathematics 2020, 8, 589. [Google Scholar] [CrossRef]

- Wang, C.N.; Hsu, H.P.; Wang, Y.H.; Nguyen, T.T. Eco-Efficiency Assessment for Some European Countries Using Slacks-Based Measure Data Envelopment Analysis. Appl. Sci. 2020, 10, 1760. [Google Scholar] [CrossRef]

- Liu, F.H.F.; Wang, P.H. DEA Malmquist productivity measure: Taiwanese semiconductor companies. Int. J. Prod. Econ. 2008, 112, 367–379. [Google Scholar] [CrossRef]

- Estache, A.; de la Fe, B.T.; Trujillo, L. Sources of efficiency gains in port reform: A DEA decomposition of a Malmquist TFP index for Mexico. Util. Policy 2004, 12, 221–230. [Google Scholar] [CrossRef]

- Odeck, J. Assessing the relative efficiency and productivity growth of vehicle inspection services: An application of DEA and Malmquist indices. Eur. J. Oper. Res. 2000, 126, 501–514. [Google Scholar] [CrossRef]

- Huang, J.; Du, D.; Hao, Y. The driving forces of the change in China’s energy intensity: An empirical research using DEA-Malmquist and spatial panel estimations. Econ. Model. 2017, 65, 41–50. [Google Scholar] [CrossRef]

- Chung, S.H.; Lee, A.H.I.; Kang, H.Y.; Lai, C.W. A DEA window analysis on the product family mix selection for a semiconductor fabricator. Expert Syst. Appl. 2008, 35, 379–388. [Google Scholar] [CrossRef]

- Vlontzos, G.; Pardalos, P.M. Assess and prognosticate greenhouse gas emissions from agricultural production of EU countries, by implementing, DEA Window analysis and artificial neural networks. Renew. Sustain. Energy Rev. 2017, 76, 155–162. [Google Scholar] [CrossRef]

- Halkos, G.E.; Tzeremes, N.G. Exploring the existence of Kuznets curve in countries’ environmental efficiency using DEA window analysis. Ecol. Econ. 2009, 68, 2168–2176. [Google Scholar] [CrossRef]

- Řepková, I. Efficiency of the Czech banking sector employing the DEA window analysis approach. Procedia Econ. Financ. 2014, 12, 587–596. [Google Scholar] [CrossRef]

- Le, T.N.; Wang, C.N. The integrated approach for sustainable performance evaluation in value chain of Vietnam textile and apparel industry. Sustainability 2017, 9, 477. [Google Scholar] [CrossRef]

- Wang, C.-N.; Nguyen, N.-A.-T.; Fu, H.-P.; Hsu, H.-P.; Dang, T.-T. Efficiency Assessment of Seaport Terminal Operators Using DEA Malmquist and Epsilon-Based Measure Models. Axioms 2021, 10, 48. [Google Scholar] [CrossRef]

- Charnes, A.; Cooper, W.W.; Rhodes, E. Measuring the efficiency of decision-making units. Eur. J. Oper. Res. 1979, 2, 429–444. [Google Scholar] [CrossRef]

- Wang, C.-N.; Dang, T.-T.; Nguyen, N.-A.-T.; Le, T.-T.-H. Supporting Better Decision-Making: A Combined Grey Model and Data Envelopment Analysis for Efficiency Evaluation in E-Commerce Marketplaces. Sustainability 2020, 12, 10385. [Google Scholar] [CrossRef]

- Jablonsky, J.; Fiala, P.; Smirlis, Y.; Despotis, D.K. DEA with interval data: An illustration using the evaluation of branches of a Czech bank. Cent. Eur. J. Oper. Res. 2004, 12, 323. [Google Scholar]

- Emrouznejad, A.; Anouze, A.L. Data envelopment analysis with classification and regression tree—A case of banking efficiency. Expert Syst. 2010, 27, 231–246. [Google Scholar] [CrossRef]

- Lin, T.Y.; Chiu, S.H. Using independent component analysis and network DEA to improve bank performance evaluation. Econ. Model. 2013, 32, 608–616. [Google Scholar] [CrossRef]

- Fujii, H.; Managi, S.; Matousek, R. Indian bank efficiency and productivity changes with undesirable outputs: A disaggregated approach. J. Bank. Financ. 2014, 38, 41–50. [Google Scholar] [CrossRef]

- Wang, K.; Huang, W.; Wu, J.; Liu, Y.N. Efficiency measures of the Chinese commercial banking system using an additive two-stage DEA. Omega 2014, 44, 5–20. [Google Scholar] [CrossRef]

- Wanke, P.; Barros, C.P.; Emrouznejad, A. Assessing productive efficiency of banks using integrated Fuzzy-DEA and bootstrapping: A case of Mozambican banks. Eur. J. Oper. Res. 2016, 249, 378–389. [Google Scholar] [CrossRef]

- Mahmoudabadi, M.Z.; Emrouznejad, A. Comprehensive performance evaluation of banking branches: A three-stage slacks-based measure (SBM) data envelopment analysis. Int. Rev. Econ. Financ. 2019, 64, 359–376. [Google Scholar] [CrossRef]

- Yu, M.M.; Lin, C.I.; Chen, K.C.; Chen, L.H. Measuring Taiwanese bank performance: A two-system dynamic network data envelopment analysis approach. Omega 2021, 98, 102145. [Google Scholar] [CrossRef]

- Sáez-Fernández, F.J.; Picazo-Tadeo, A.J.; Jiménez-Hernández, I. Performance and risk in the Brazilian banking industry. Heliyon 2021, 7, e06524. [Google Scholar] [CrossRef] [PubMed]

- Wang, C.-N.; Nguyen, T.-L.; Dang, T.-T. Analyzing Operational Efficiency in Real Estate Companies: An Application of GM (1,1) and DEA Malmquist Model. Mathematics 2021, 9, 202. [Google Scholar] [CrossRef]

- Wang, C.-N.; Nguyen, T.-L.; Dang, T.-T.; Bui, T.-H. Performance Evaluation of Fishery Enterprises Using Data Envelopment Analysis—A Malmquist Model. Mathematics 2021, 9, 469. [Google Scholar] [CrossRef]

- Charnes, A.; Clark, C.T.; Cooper, W.W.; Golany, B. A Developmental Study of Data Envelopment Analysis in Measuring the Efficiency of Maintenance Units in the U.S. Air Forces. Ann. Oper. Res. 1985, 2, 95–112. [Google Scholar] [CrossRef]

- Yue, P. Data Envelopment Analysis and Commercial Bank Performance: A Primer with Applications to Missouri Banks. Fed. Reserve Bank St. Louis Rev. 1992, 74, 31–45. [Google Scholar] [CrossRef]

- Charnes, A.; Cooper, W.W.; Lewin, A.Y.; Seiford, L.M. Data Envelopment Analysis: Theory, Methodology and Applications; Springer: New York, NY, USA, 1995. [Google Scholar]

- Vietnam Online Stock Market. Available online: http://vietstock.vn/ (accessed on 18 June 2020).

- VPBank in Sustainable Development Strategy. Available online: https://tuoitre.vn/vpbank-duy-tri-tang-truong-ben-vung-20200717151111649.htm (accessed on 1 June 2021).

- Top 10 Vietnamese Commercial Banks in 2020. Available online: https://vietnamnet.vn/vn/kinh-doanh/vef/top-10-ngan-hang-thuong-mai-viet-nam-uy-tin-nam-2020-657568.html (accessed on 4 June 2021).

- Vietnamese Commercial Banks in COVID-19. Available online: http://tapchinganhang.gov.vn/thach-thuc-cho-cac-ngan-hang-thuong-mai-trong-va-sau-dich-covid-19.htm?fbclid=IwAR3eK8PKYl2PO7l5yjGgMIhAsW7DRXnEyUgUQ52tPGgkjJQa99BfuZLpQtY (accessed on 1 June 2021).

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| No. | Authors [Citation] | Input Factors | Output Factors | # of DMUs | Research Scopes |

|---|---|---|---|---|---|

| 1 | Jablonsky et al., (2004) [37] | Employees Operating expense Space | Number of accounts Number of transactions Savings | 81 | Reflecting the productive efficiency of the branches in Czech Republic |

| 2 | Emrouznejad and Anouze, (2010) [38] | Assets Equity Deposit | Loan Profit | 36 | Assessing the efficiency and productivity of the banking sector in the Gulf Cooperation Council countries |

| 3 | Lin and Chiu, (2013) [39] | Fixed assets Operating expense Capital | Non-interest income Interest income Profit | 30 | Investigating performance evaluation for the Taiwanese domestic banks |

| 4 | Fujii et al., (2014) [40] | Employees Deposits Fixed assets | Acquired assets Customer loans Bad loans | 24 | Examining technical efficiency and productivity growth in the Indian banking sector |

| 5 | Wang et al., (2014) [41] | Employees Fixed assets | Non-interest income Interest income Non-performing loans | 16 | Measuring efficiency of the Chinese commercial banking system |

| 6 | Wanke et al., (2016) [42] | Total costs Employee costs | Total deposits Income before tax Total credit | 117 | Assessing productive efficiency of Mozambican banks |

| 7 | Mahmoudabadi and Emrouznejad, (2019) [43] | Employees Fixed assets Non-operating costs Interest expenses | Bank facilities Interest income Non-interest income | 37 | Evaluating operational efficiency, service effectiveness, and social effectiveness of commercial banks in Iran |

| 8 | Yu et al., (2021) [44] | Fixed assets Labor Operating expenses | Loan Securities investment Non-interest income | 22 | Measuring Taiwanese bank performance |

| 9 | Sáez-Fernández et al., (2021) [45] | Staff expenses Non-earning assets Equity Customer deposits Market liabilities | Loan Securities | 124 | Assessing the technical performance of Brazilian banks |

| 10 | This paper | Assets Deposits Operating expenses Liabilities | Loan Net income | 18 | Measuring technological and productivity growth of commercial banks in Vietnam |

| DMUs | Name of Banks | Code | Net Profit after Tax in 2019 (Mil. USD) | Rank by Net Profit after Tax in 2019 |

|---|---|---|---|---|

| B1 | Vietinbank | CTG | 406.119 | 2 |

| B2 | BIDV | BID | 366.298 | 3 |

| B3 | Vietcombank | VCB | 793.897 | 1 |

| B4 | ACB | ACB | 257.545 | 6 |

| B5 | Sacombank | STB | 105.199 | 11 |

| B6 | SHBank | SHB | 103.614 | 12 |

| B7 | TPBank | TPB | 132.581 | 9 |

| B8 | HDBank | HDB | 172.284 | 7 |

| B9 | MilitaryBank | MBB | 345.765 | 5 |

| B10 | VPBank | VPB | 353.978 | 4 |

| B11 | NationalCitizen | NVB | 1.849 | 18 |

| B12 | OrientCommercial | OCB | 110.657 | 10 |

| B13 | VietnamMaritime | MSB | 44.720 | 13 |

| B14 | SaigonBank | SCB | 7.292 | 14 |

| B15 | VIB | VIB | 139.976 | 8 |

| B16 | BaoVietBank | BVB | 3.641 | 16 |

| B17 | SaigonCongThuong | SGB | 6.198 | 15 |

| B18 | PetrolimexGroup | PGB | 3.198 | 17 |

| Period | Statistics | Input Factors | Output Factors | ||||

|---|---|---|---|---|---|---|---|

| a1 | a2 | a3 | a4 | b1 | b2 | ||

| 2015 | Max | 36,453.89 | 24,194.17 | 475.12 | 34,639.68 | 25,322.68 | 827.71 |

| Min | 760.59 | 563.17 | 14.56 | 615.28 | 493.68 | 20.30 | |

| Avg | 10,168.83 | 7065.65 | 148.94 | 9329.91 | 6187.13 | 248.47 | |

| SD | 10,904.51 | 7215.26 | 143.55 | 10,302.97 | 7386.57 | 259.12 | |

| 2016 | Max | 43,126.47 | 31,112.33 | 579.89 | 41,236.13 | 30,581.42 | 1002.49 |

| Min | 816.26 | 607.18 | 16.94 | 665.64 | 532.70 | 26.34 | |

| Avg | 12,030.80 | 8722.56 | 176.60 | 11,306.56 | 7572.66 | 289.57 | |

| SD | 12,963.90 | 9476.58 | 172.60 | 12,288.67 | 8913.86 | 318.27 | |

| 2017 | Max | 51,521.67 | 36,853.09 | 664.41 | 49,428.97 | 33,527.68 | 1326.53 |

| Min | 913.60 | 636.35 | 17.24 | 767.16 | 599.45 | 28.14 | |

| Avg | 14,550.00 | 10,128.80 | 215.04 | 13,698.36 | 8805.55 | 371.36 | |

| SD | 15,672.62 | 11,162.80 | 202.58 | 14,954.91 | 9859.45 | 404.71 | |

| 2018 | Max | 56,267.82 | 42,410.54 | 690.66 | 53,930.12 | 41,839.00 | 1497.97 |

| Min | 873.07 | 629.02 | 19.25 | 725.88 | 581.07 | 27.08 | |

| Avg | 15,980.49 | 11,386.86 | 244.22 | 15,013.35 | 10,396.45 | 423.62 | |

| SD | 16,677.50 | 12,595.49 | 210.89 | 15,886.91 | 11,896.95 | 443.57 | |

| 2019 | Max | 63,849.38 | 47,745.39 | 739.52 | 60,521.71 | 47,239.86 | 1541.76 |

| Min | 977.60 | 671.41 | 20.84 | 824.99 | 618.90 | 30.76 | |

| Avg | 17,999.59 | 12,972.07 | 276.86 | 16,818.52 | 11,904.13 | 518.52 | |

| SD | 18,522.97 | 14,075.98 | 235.76 | 17,494.69 | 13,242.19 | 527.24 | |

| Period | Factors | Input Factors | Output Factors | ||||

|---|---|---|---|---|---|---|---|

| a1 | a2 | a3 | a4 | b1 | b2 | ||

| 2015 | Assets | 1 | |||||

| Deposits | 0.9860 | 1 | |||||

| Operating Expenses | 0.9594 | 0.9541 | 1 | ||||

| Liabilities | 0.9985 | 0.9820 | 0.9527 | 1 | |||

| Loans | 0.9927 | 0.9861 | 0.9605 | 0.9909 | 1 | ||

| Net Income | 0.9612 | 0.9461 | 0.9905 | 0.9564 | 0.9590 | 1 | |

| 2016 | Assets | 1 | |||||

| Deposits | 0.9947 | 1 | |||||

| Operating Expenses | 0.9593 | 0.9457 | 1 | ||||

| Liabilities | 0.9998 | 0.9946 | 0.9568 | 1 | |||

| Loans | 0.9941 | 0.9856 | 0.9578 | 0.9948 | 1 | ||

| Net Income | 0.9219 | 0.8931 | 0.9732 | 0.9191 | 0.9205 | 1 | |

| 2017 | Assets | 1 | |||||

| Deposits | 0.9948 | 1 | |||||

| Operating Expenses | 0.9415 | 0.9272 | 1 | ||||

| Liabilities | 0.9999 | 0.9955 | 0.9372 | 1 | |||

| Loans | 0.9868 | 0.9822 | 0.9461 | 0.9860 | 1 | ||

| Net Income | 0.8910 | 0.8580 | 0.9697 | 0.8863 | 0.8948 | 1 | |

| 2018 | Assets | 1 | |||||

| Deposits | 0.9961 | 1 | |||||

| Operating Expenses | 0.9199 | 0.9048 | 1 | ||||

| Liabilities | 0.9998 | 0.9969 | 0.9141 | 1 | |||

| Loans | 0.9907 | 0.9860 | 0.9105 | 0.9911 | 1 | ||

| Net Income | 0.8708 | 0.8483 | 0.9628 | 0.8651 | 0.8655 | 1 | |

| 2019 | Assets | 1 | |||||

| Deposits | 0.9963 | 1 | |||||

| Operating Expenses | 0.9102 | 0.8967 | 1 | ||||

| Liabilities | 0.9998 | 0.9969 | 0.9034 | 1 | |||

| Loans | 0.9914 | 0.9854 | 0.9005 | 0.9916 | 1 | ||

| Net Income | 0.8773 | 0.8487 | 0.9694 | 0.8689 | 0.8714 | 1 | |

| DMUs | Name of Banks | 2015–2016 | 2016–2017 | 2017–2018 | 2018–2019 | Average |

|---|---|---|---|---|---|---|

| B1 | Vietinbank | 1.0000 | 1.0235 | 0.9846 | 1.0044 | 1.0032 |

| B2 | BIDV | 0.9792 | 0.8600 | 1.2214 | 0.9521 | 1.0032 |

| B3 | Vietcombank | 0.8475 | 0.9061 | 1.0586 | 1.0152 | 0.9569 |

| B4 | ACB | 0.8342 | 0.9553 | 1.0075 | 0.9856 | 0.9456 |

| B5 | Sacombank | 0.9281 | 0.9792 | 0.9974 | 1.0062 | 0.9777 |

| B6 | SHBank | 1.0105 | 1.0220 | 0.9580 | 0.9987 | 0.9973 |

| B7 | TPBank | 1.0374 | 1.0311 | 1.0599 | 1.0279 | 1.0391 |

| B8 | HDBank | 0.9646 | 0.9904 | 1.0626 | 1.2491 | 1.0667 |

| B9 | MilitaryBank | 0.8290 | 0.9438 | 0.9836 | 1.0361 | 0.9481 |

| B10 | VPBank | 1.4299 | 0.6582 | 1.4351 | 0.9253 | 1.1121 |

| B11 | NationalCitizen | 0.9075 | 1.1306 | 1.0401 | 0.9781 | 1.0141 |

| B12 | OrientCommercial | 0.9695 | 0.9320 | 1.0058 | 1.0307 | 0.9845 |

| B13 | VietnamMaritime | 1.2933 | 0.8232 | 1.1156 | 1.1234 | 1.0889 |

| B14 | SaigonBank | 1.0930 | 0.9461 | 0.9801 | 1.0029 | 1.0055 |

| B15 | VIB | 0.9843 | 1.2981 | 0.9331 | 0.9219 | 1.0344 |

| B16 | BaoVietBank | 0.9961 | 1.0435 | 0.9727 | 0.8657 | 0.9695 |

| B17 | SaigonCongThuong | 0.9949 | 0.9231 | 0.9711 | 0.9342 | 0.9558 |

| B18 | PetrolimexGroup | 1.1167 | 1.0027 | 0.9918 | 0.9986 | 1.0274 |

| Average | 1.0120 | 0.9705 | 1.0433 | 1.0031 | 1.0072 | |

| Max | 1.4299 | 1.2981 | 1.4351 | 1.2491 | 1.1121 | |

| Min | 0.8290 | 0.6582 | 0.9331 | 0.8657 | 0.9456 | |

| SD | 0.1512 | 0.1306 | 0.1187 | 0.0831 | 0.0478 |

| DMUs | Name of Banks | 2015–2016 | 2016–2017 | 2017–2018 | 2018–2019 | Average |

|---|---|---|---|---|---|---|

| B1 | Vietinbank | 1.0001 | 1.0175 | 1.0287 | 1.0054 | 1.0129 |

| B2 | BIDV | 1.0064 | 1.0941 | 1.0150 | 1.0290 | 1.0361 |

| B3 | Vietcombank | 1.0821 | 1.0407 | 1.0299 | 1.0114 | 1.0410 |

| B4 | ACB | 1.0674 | 1.0378 | 1.0258 | 1.0127 | 1.0359 |

| B5 | Sacombank | 1.0007 | 1.0321 | 1.0296 | 1.0094 | 1.0179 |

| B6 | SHBank | 1.0092 | 1.0208 | 1.0123 | 1.0391 | 1.0204 |

| B7 | TPBank | 1.0484 | 1.0516 | 1.0093 | 1.0118 | 1.0303 |

| B8 | HDBank | 1.0724 | 1.0565 | 1.0041 | 0.9709 | 1.0260 |

| B9 | MilitaryBank | 1.0751 | 1.0596 | 1.0036 | 1.0094 | 1.0369 |

| B10 | VPBank | 1.0336 | 1.3578 | 0.8370 | 1.0540 | 1.0706 |

| B11 | NationalCitizen | 1.0110 | 1.0319 | 1.0335 | 1.0106 | 1.0218 |

| B12 | OrientCommercial | 1.0384 | 1.0463 | 1.0080 | 1.0117 | 1.0261 |

| B13 | VietnamMaritime | 1.0847 | 1.0526 | 1.0101 | 1.0123 | 1.0400 |

| B14 | SaigonBank | 1.0034 | 0.9800 | 0.9606 | 1.0012 | 0.9863 |

| B15 | VIB | 1.0390 | 1.0276 | 1.0029 | 1.0086 | 1.0195 |

| B16 | BaoVietBank | 1.0139 | 1.0424 | 1.0209 | 1.0090 | 1.0215 |

| B17 | SaigonCongThuong | 0.9861 | 1.0714 | 1.0250 | 1.0160 | 1.0246 |

| B18 | PetrolimexGroup | 1.0113 | 1.0112 | 1.0074 | 1.0078 | 1.0094 |

| Average | 1.0324 | 1.0573 | 1.0035 | 1.0128 | 1.0265 | |

| Max | 1.0847 | 1.3578 | 1.0335 | 1.0540 | 1.0706 | |

| Min | 0.9861 | 0.9800 | 0.8370 | 0.9709 | 0.9863 | |

| SD | 0.0323 | 0.0790 | 0.0448 | 0.0166 | 0.0171 |

| DMUs | Name of Banks | 2015–2016 | 2016–2017 | 2017–2018 | 2018–2019 | Average |

|---|---|---|---|---|---|---|

| B1 | Vietinbank | 1.0001 | 1.0415 | 1.0129 | 1.0099 | 1.0161 |

| B2 | BIDV | 0.9855 | 0.9409 | 1.2397 | 0.9797 | 1.0365 |

| B3 | Vietcombank | 0.9171 | 0.9429 | 1.0903 | 1.0268 | 0.9943 |

| B4 | ACB | 0.8904 | 0.9914 | 1.0335 | 0.9981 | 0.9784 |

| B5 | Sacombank | 0.9287 | 1.0107 | 1.0269 | 1.0156 | 0.9955 |

| B6 | SHBank | 1.0198 | 1.0433 | 0.9698 | 1.0378 | 1.0177 |

| B7 | TPBank | 1.0876 | 1.0843 | 1.0698 | 1.0401 | 1.0705 |

| B8 | HDBank | 1.0345 | 1.0463 | 1.0670 | 1.2127 | 1.0901 |

| B9 | MilitaryBank | 0.8913 | 1.0000 | 0.9871 | 1.0458 | 0.9810 |

| B10 | VPBank | 1.4779 | 0.8937 | 1.2012 | 0.9752 | 1.1370 |

| B11 | NationalCitizen | 0.9175 | 1.1666 | 1.0749 | 0.9885 | 1.0369 |

| B12 | OrientCommercial | 1.0067 | 0.9751 | 1.0138 | 1.0428 | 1.0096 |

| B13 | VietnamMaritime | 1.4028 | 0.8666 | 1.1269 | 1.1373 | 1.1334 |

| B14 | SaigonBank | 1.0968 | 0.9273 | 0.9415 | 1.0041 | 0.9924 |

| B15 | VIB | 1.0226 | 1.3340 | 0.9358 | 0.9298 | 1.0556 |

| B16 | BaoVietBank | 1.0099 | 1.0877 | 0.9931 | 0.8735 | 0.9910 |

| B17 | SaigonCongThuong | 0.9810 | 0.9890 | 0.9954 | 0.9491 | 0.9786 |

| B18 | PetrolimexGroup | 1.1293 | 1.0139 | 0.9992 | 1.0064 | 1.0372 |

| Average | 1.0444 | 1.0197 | 1.0433 | 1.0152 | 1.0306 | |

| Max | 1.4779 | 1.3340 | 1.2397 | 1.2127 | 1.1370 | |

| Min | 0.8904 | 0.8666 | 0.9358 | 0.8735 | 0.9784 | |

| SD | 0.1598 | 0.1071 | 0.0820 | 0.0738 | 0.0497 |

| DMUs | Name of Banks | 2015 | 2016 | 2017 | 2018 | 2019 | Average | Rank |

|---|---|---|---|---|---|---|---|---|

| B1 | Vietinbank | 0.9515 | 0.9543 | 0.9889 | 1 | 1 | 0.9789 | 1 |

| B2 | BIDV | 0.9979 | 0.9539 | 0.8548 | 1 | 1 | 0.9613 | 4 |

| B3 | Vietcombank | 0.9384 | 0.8103 | 0.8041 | 0.8700 | 0.8966 | 0.8639 | 10 |

| B4 | ACB | 1 | 0.9381 | 0.9388 | 0.9424 | 0.9449 | 0.9528 | 6 |

| B5 | Sacombank | 0.8463 | 0.7959 | 0.8039 | 0.8385 | 0.8661 | 0.8301 | 12 |

| B6 | SHBank | 0.9190 | 0.9605 | 1 | 0.9712 | 1 | 0.9701 | 3 |

| B7 | TPBank | 0.7113 | 0.7760 | 0.8065 | 0.8569 | 0.8810 | 0.8063 | 15 |

| B8 | HDBank | 0.7255 | 0.7476 | 0.7645 | 0.8294 | 0.9681 | 0.8070 | 14 |

| B9 | MilitaryBank | 0.8153 | 0.8291 | 0.8151 | 0.8185 | 0.8459 | 0.8248 | 13 |

| B10 | VPBank | 0.8529 | 0.9359 | 1 | 1 | 1 | 0.9578 | 5 |

| B11 | NationalCitizen | 0.5694 | 0.5678 | 0.6560 | 0.7058 | 0.6624 | 0.6323 | 17 |

| B12 | OrientCommercial | 0.8440 | 0.8258 | 0.8172 | 0.8225 | 0.8853 | 0.8390 | 11 |

| B13 | VietnamMaritime | 0.3969 | 0.5551 | 0.5394 | 0.6145 | 0.6856 | 0.5583 | 18 |

| B14 | SaigonBank | 0.9201 | 1 | 0.9537 | 0.9223 | 0.9137 | 0.9420 | 7 |

| B15 | VIB | 0.7951 | 0.8641 | 1 | 0.9960 | 0.9584 | 0.9227 | 9 |

| B16 | BaoVietBank | 0.7901 | 0.6968 | 0.8421 | 0.8867 | 0.7752 | 0.7982 | 16 |

| B17 | SaigonCongThuong | 0.9374 | 0.9367 | 0.9490 | 0.9542 | 0.9138 | 0.9382 | 8 |

| B18 | PetrolimexGroup | 0.9092 | 0.9803 | 0.9851 | 0.9948 | 1 | 0.9739 | 2 |

| DMUs | Name of Banks | 2015 | 2016 | 2017 | 2018 | 2019 | Average | Rank |

|---|---|---|---|---|---|---|---|---|

| B1 | Vietinbank | 0.9706 | 0.9730 | 1 | ||||

| 0.9579 | 0.9906 | 1 | ||||||

| 0.9889 | 1 | 1 | ||||||

| Average | 0.9706 | 0.9655 | 0.9932 | 1 | 1 | 0.9859 | 2 | |

| B2 | BIDV | 1 | 0.9963 | 0.8996 | ||||

| 0.9652 | 0.8560 | 1 | ||||||

| 0.8548 | 1 | 1 | ||||||

| Average | 1 | 0.9807 | 0.8701 | 1 | 1 | 0.9702 | 4 | |

| B3 | Vietcombank | 0.9401 | 0.8571 | 0.8266 | ||||

| 0.8115 | 0.8053 | 0.8711 | ||||||

| 0.8041 | 0.8700 | 0.8966 | ||||||

| Average | 0.9401 | 0.8343 | 0.8120 | 0.8706 | 0.8966 | 0.8707 | 10 | |

| B4 | ACB | 1 | 0.9643 | 0.9651 | ||||

| 0.9404 | 0.9404 | 0.9450 | ||||||

| 0.9388 | 0.9424 | 0.9449 | ||||||

| Average | 1 | 0.9524 | 0.9481 | 0.9437 | 0.9449 | 0.9578 | 7 | |

| B5 | Sacombank | 0.8694 | 0.8179 | 0.8262 | ||||

| 0.8002 | 0.8076 | 0.8419 | ||||||

| 0.8039 | 0.8385 | 0.8661 | ||||||

| Average | 0.8694 | 0.8090 | 0.8125 | 0.8402 | 0.8661 | 0.8395 | 12 | |

| B6 | SHBank | 0.9687 | 0.9971 | 1 | ||||

| 0.9795 | 1 | 0.9843 | ||||||

| 1 | 0.9782 | 1 | ||||||

| Average | 0.9687 | 0.9883 | 1 | 0.9813 | 1 | 0.9876 | 1 | |

| B7 | TPBank | 0.7277 | 0.7771 | 0.8072 | ||||

| 0.7760 | 0.8065 | 0.8571 | ||||||

| 0.8065 | 0.8569 | 0.8810 | ||||||

| Average | 0.7277 | 0.7765 | 0.8067 | 0.8570 | 0.8810 | 0.8098 | 15 | |

| B8 | HDBank | 0.7486 | 0.7723 | 0.7880 | ||||

| 0.7490 | 0.7699 | 0.8300 | ||||||

| 0.7645 | 0.8294 | 0.9681 | ||||||

| Average | 0.7486 | 0.7606 | 0.7741 | 0.8297 | 0.9681 | 0.8162 | 14 | |

| B9 | MilitaryBank | 0.8424 | 0.8592 | 0.8458 | ||||

| 0.8426 | 0.8312 | 0.8224 | ||||||

| 0.8174 | 0.8185 | 0.8459 | ||||||

| Average | 0.8424 | 0.8509 | 0.8315 | 0.8205 | 0.8459 | 0.8382 | 13 | |

| B10 | VPBank | 0.8870 | 0.9622 | 1 | ||||

| 0.9417 | 1 | 1 | ||||||

| 1 | 1 | 1 | ||||||

| Average | 0.8870 | 0.9519 | 1 | 1 | 1 | 0.9678 | 5 | |

| B11 | NationalCitizen | 0.6023 | 0.5694 | 0.6572 | ||||

| 0.5678 | 0.6560 | 0.7058 | ||||||

| 0.6560 | 0.7058 | 0.6646 | ||||||

| Average | 0.6023 | 0.5686 | 0.6564 | 0.7058 | 0.6646 | 0.6395 | 17 | |

| B12 | OrientCommercial | 0.8472 | 0.8463 | 0.8241 | ||||

| 0.8340 | 0.8181 | 0.8236 | ||||||

| 0.8172 | 0.8225 | 0.8853 | ||||||

| Average | 0.8472 | 0.8402 | 0.8198 | 0.8231 | 0.8853 | 0.8431 | 11 | |

| B13 | VietnamMaritime | 0.4056 | 0.5692 | 0.5394 | ||||

| 0.5614 | 0.5394 | 0.6145 | ||||||

| 0.5394 | 0.6145 | 0.6856 | ||||||

| Average | 0.4056 | 0.5653 | 0.5394 | 0.6145 | 0.6856 | 0.5621 | 18 | |

| B14 | SaigonBank | 0.9349 | 1 | 0.9537 | ||||

| 1 | 0.9537 | 0.9223 | ||||||

| 1 | 0.9554 | 0.9621 | ||||||

| Average | 0.9349 | 1 | 0.9691 | 0.9388 | 0.9621 | 0.9610 | 6 | |

| B15 | VIB | 0.8135 | 0.8666 | 1 | ||||

| 0.8644 | 1 | 0.9969 | ||||||

| 1 | 0.9960 | 0.9584 | ||||||

| Average | 0.8135 | 0.8655 | 1 | 0.9964 | 0.9584 | 0.9268 | 9 | |

| B16 | BaoVietBank | 0.7914 | 0.7110 | 0.8461 | ||||

| 0.7057 | 0.8437 | 0.8867 | ||||||

| 0.8421 | 0.8867 | 0.7752 | ||||||

| Average | 0.7914 | 0.7084 | 0.8440 | 0.8867 | 0.7752 | 0.8011 | 16 | |

| B17 | SaigonCongThuong | 0.9491 | 0.9493 | 0.9669 | ||||

| 0.9767 | 0.9576 | 0.9742 | ||||||

| 0.9542 | 0.9659 | 0.9191 | ||||||

| Average | 0.9491 | 0.9630 | 0.9596 | 0.9701 | 0.9191 | 0.9522 | 8 | |

| B18 | PetrolimexGroup | 0.9274 | 0.9999 | 1 | ||||

| 0.9908 | 1 | 1 | ||||||

| 0.9937 | 0.9992 | 1 | ||||||

| Average | 0.9274 | 0.9953 | 0.9979 | 0.9996 | 1 | 0.9841 | 3 |

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2021 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Wang, C.-N.; Nguyen, N.-A.-T.; Dang, T.-T.; Trinh, T.-T.-Q. A Decision Support Model for Measuring Technological Progress and Productivity Growth: The Case of Commercial Banks in Vietnam. Axioms 2021, 10, 131. https://doi.org/10.3390/axioms10030131

Wang C-N, Nguyen N-A-T, Dang T-T, Trinh T-T-Q. A Decision Support Model for Measuring Technological Progress and Productivity Growth: The Case of Commercial Banks in Vietnam. Axioms. 2021; 10(3):131. https://doi.org/10.3390/axioms10030131

Chicago/Turabian StyleWang, Chia-Nan, Ngoc-Ai-Thy Nguyen, Thanh-Tuan Dang, and Thi-Thuy-Quynh Trinh. 2021. "A Decision Support Model for Measuring Technological Progress and Productivity Growth: The Case of Commercial Banks in Vietnam" Axioms 10, no. 3: 131. https://doi.org/10.3390/axioms10030131

APA StyleWang, C.-N., Nguyen, N.-A.-T., Dang, T.-T., & Trinh, T.-T.-Q. (2021). A Decision Support Model for Measuring Technological Progress and Productivity Growth: The Case of Commercial Banks in Vietnam. Axioms, 10(3), 131. https://doi.org/10.3390/axioms10030131