Portfolio Diversification, Hedge and Safe-Haven Properties in Cryptocurrency Investments and Financial Economics: A Systematic Literature Review

Abstract

:1. Introduction

2. Methodology

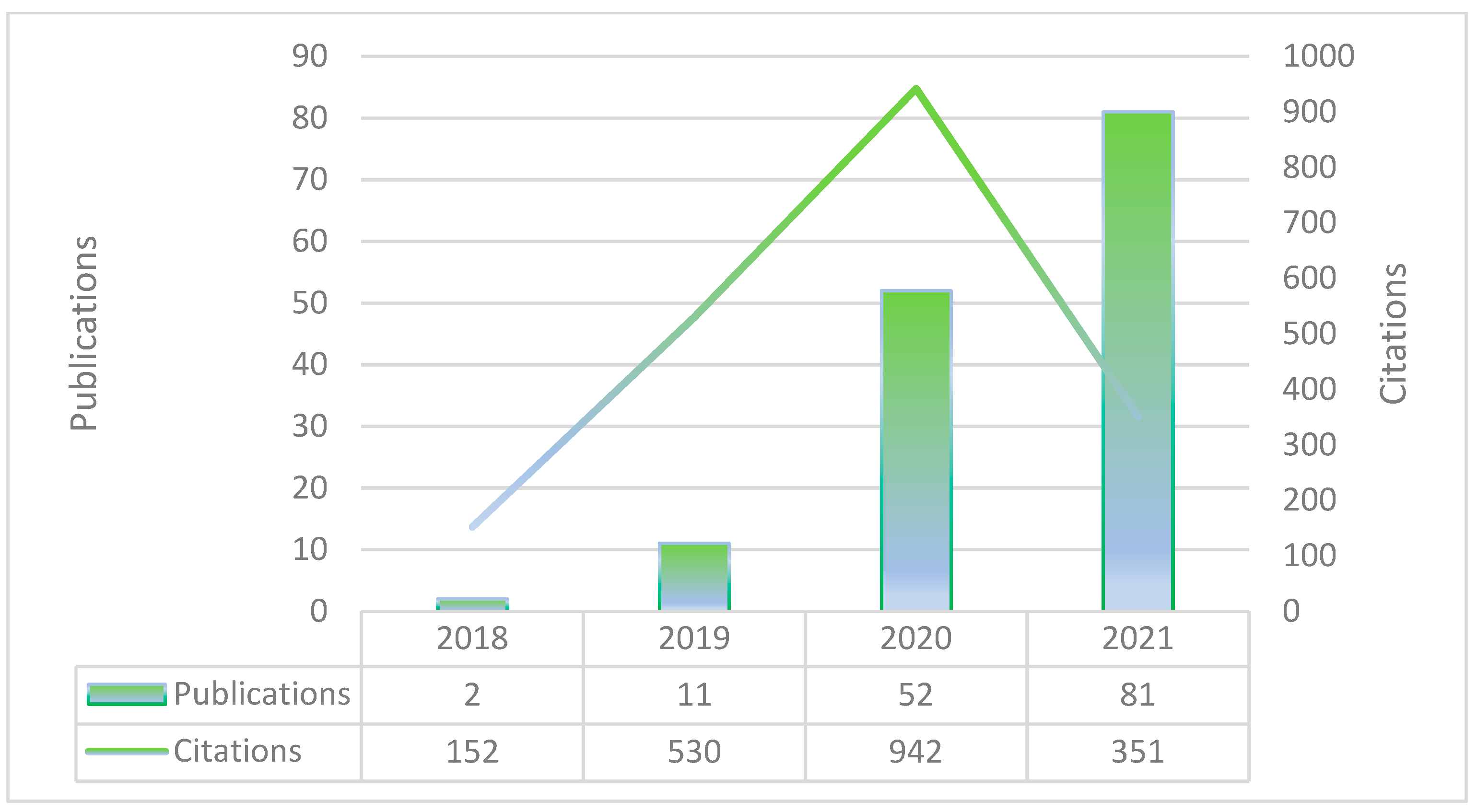

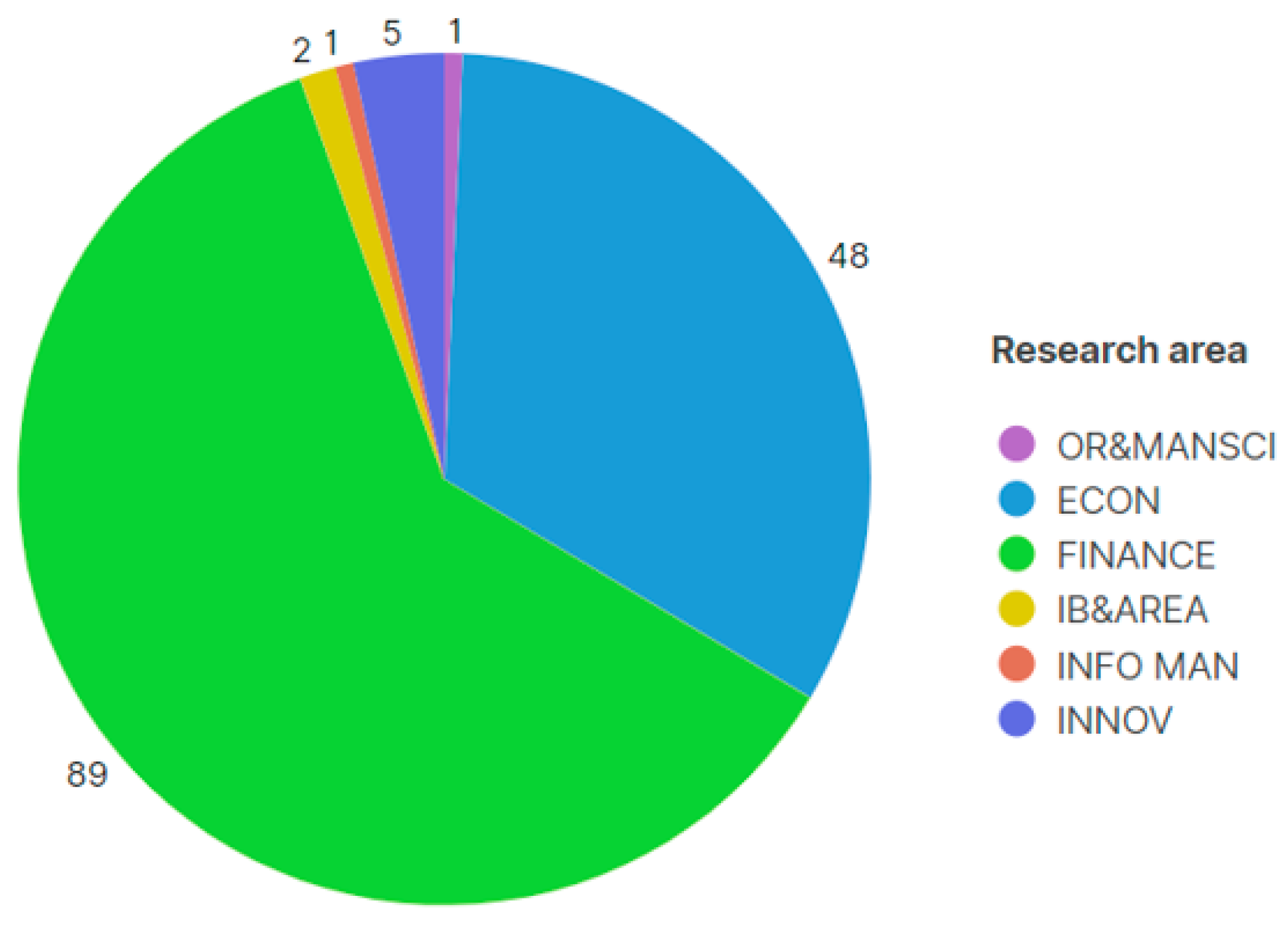

3. Literature Mapping and Bibliometric Analysis

3.1. Top Articles Analysis

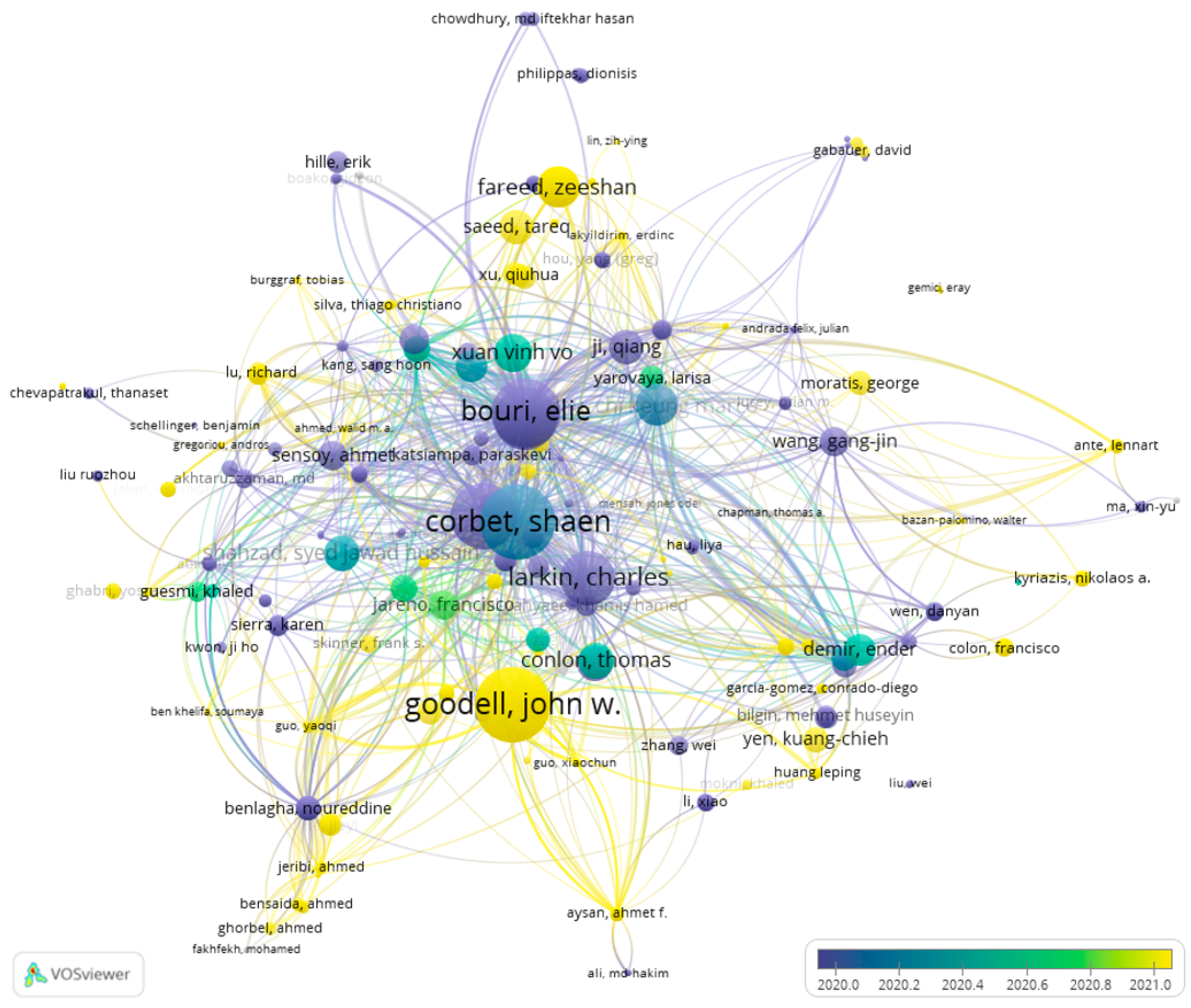

3.2. Author’s Analysis

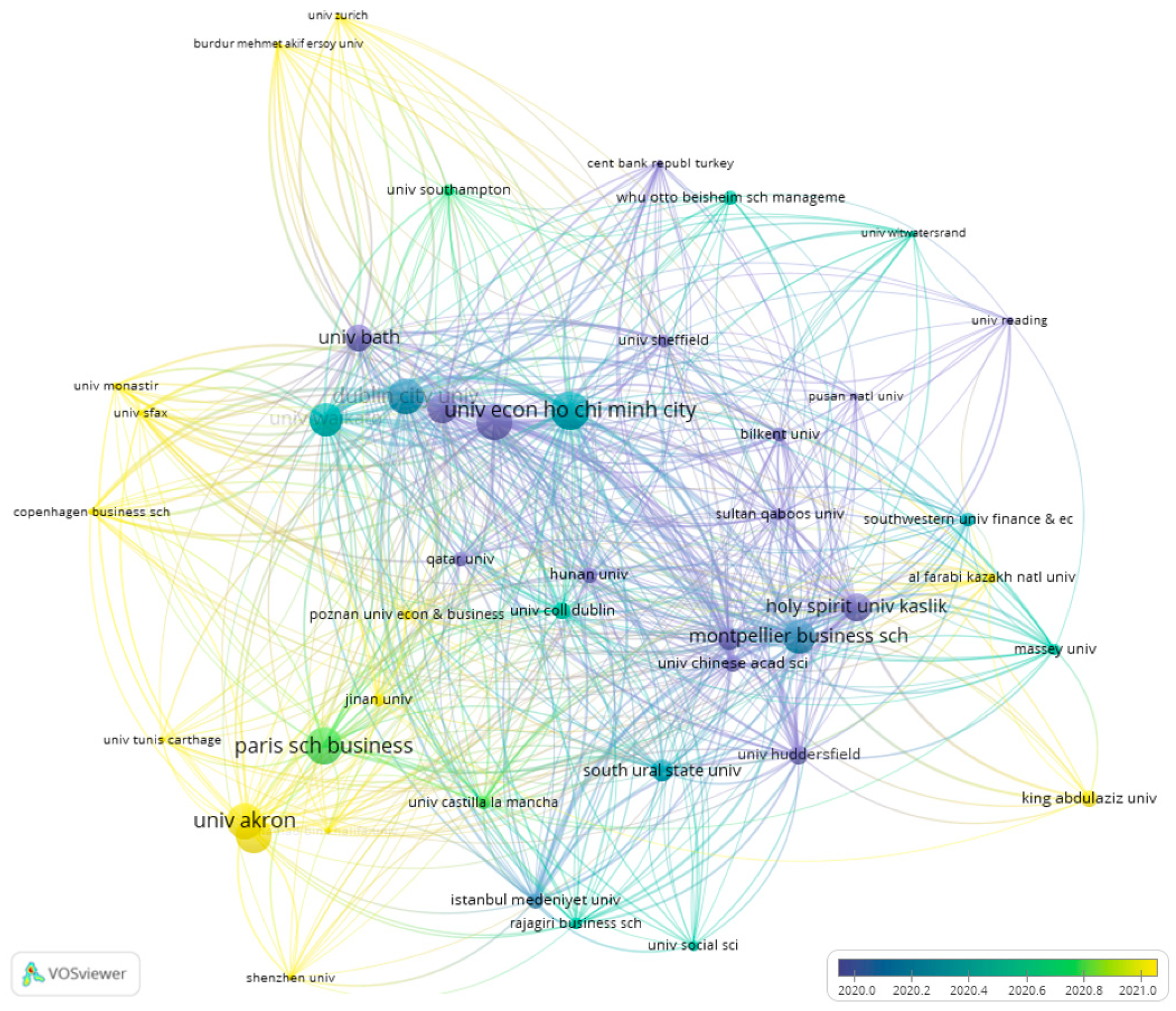

3.3. Institution’s Analysis

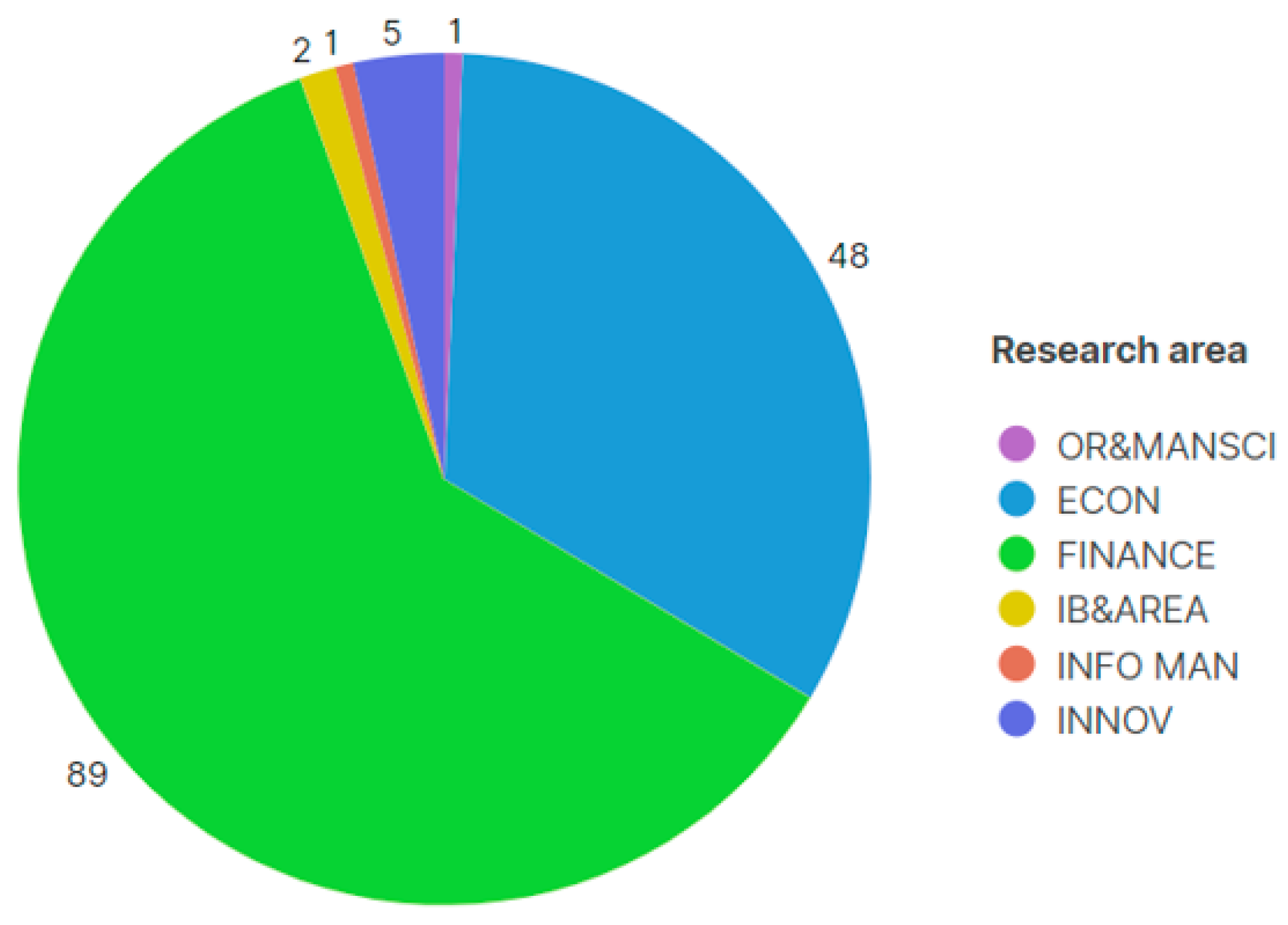

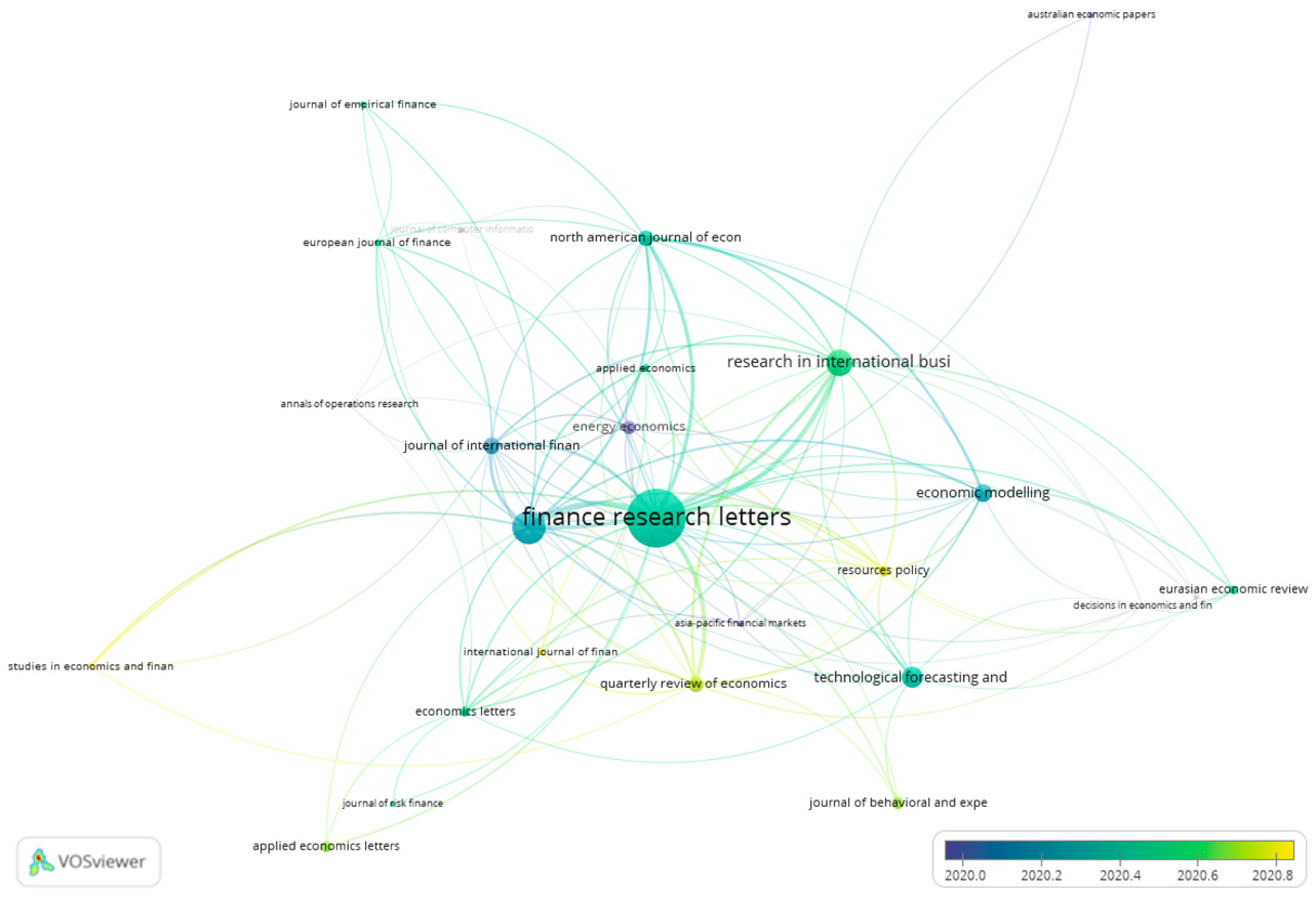

3.4. Journal Analysis

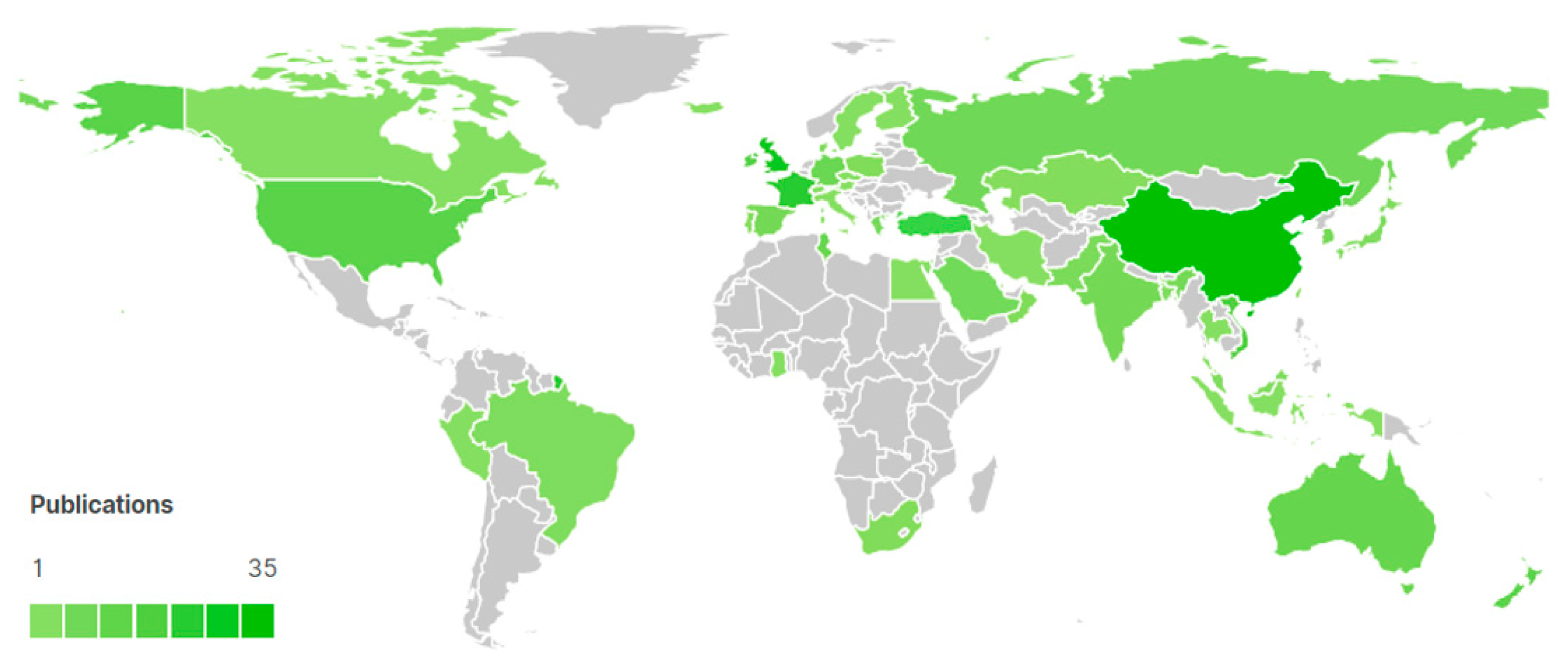

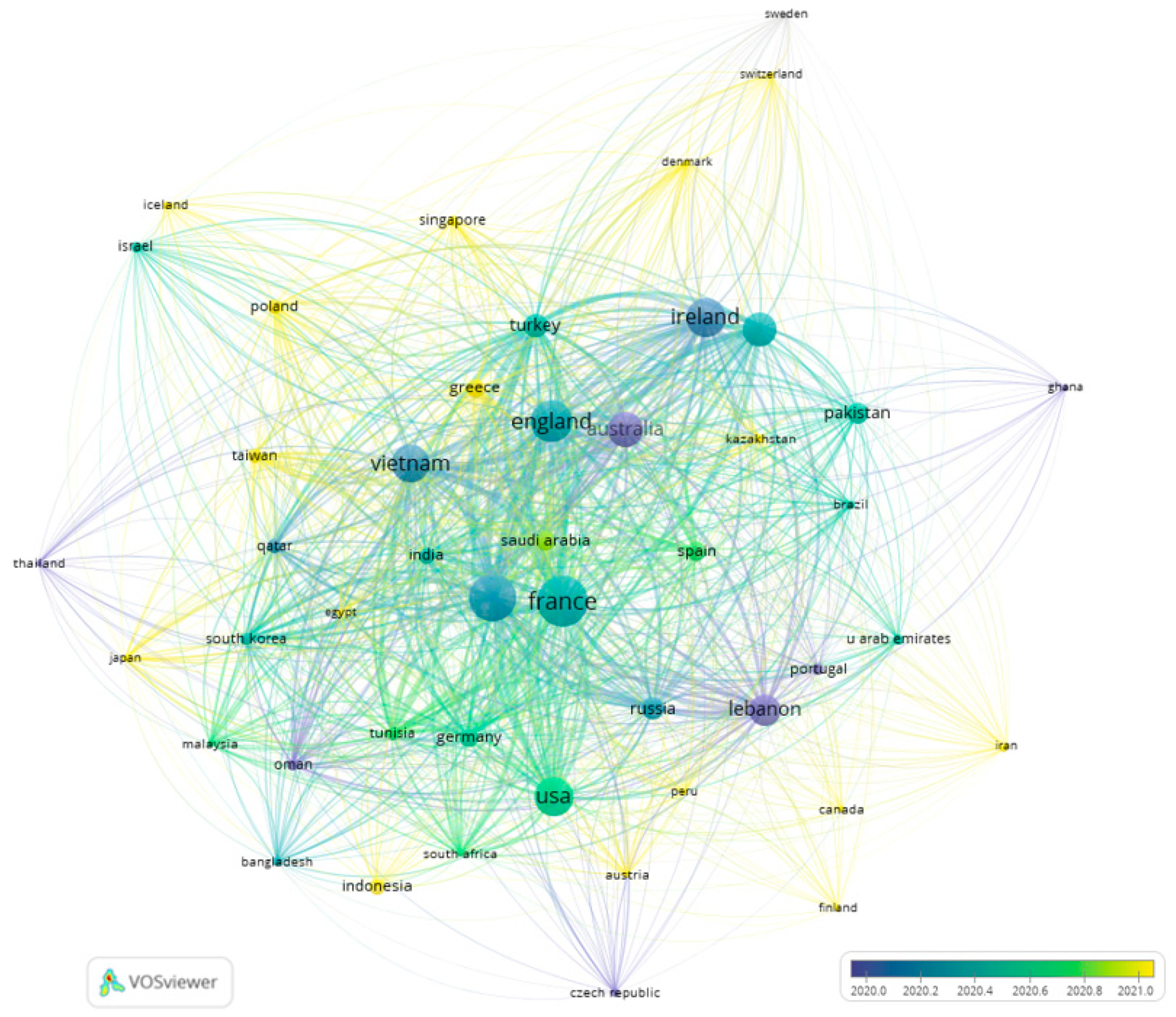

3.5. Country Analysis

4. Literature Findings on Portfolio Diversification, Hedge and Safe-Haven Properties of Cryptocurrency Investments

4.1. Do Cryptocurrencies Bear Hedging Properties?

4.2. Do Cryptocurrencies Bear Diversification Properties?

4.3. Are Cryptocurrencies Safe-Havens?

4.4. The Impact of Uncertainty on Cryptocurrency Investments

4.5. Sentiment and News Impact on Cryptocurrency Investment

4.6. Stablecoins Role in Cryptocurrency Investment

4.7. Cryptocurrency Market

Volatility

4.8. Cryptocurrency Portfolios

4.9. Future Venues of Research

5. Conclusions

Author Contributions

Funding

Data Availability Statement

Conflicts of Interest

References

- Aharon, David Y., Ender Demir, Chi Keung Marco Lau, and Adam Zaremba. 2022. Twitter-Based Uncertainty and Cryptocurrency Returns. Research in International Business and Finance 59: 101546. [Google Scholar] [CrossRef]

- Ahelegbey, Daniel Felix, Paolo Giudici, and Fatemeh Mojtahedi. 2021. Tail Risk Measurement in Crypto-Asset Markets. International Review of Financial Analysis 73: 101604. [Google Scholar] [CrossRef]

- Ahmed, Walid M. A. 2021. Stock Market Reactions to Upside and Downside Volatility of Bitcoin: A Quantile Analysis. North American Journal of Economics and Finance 57: 101379. [Google Scholar] [CrossRef]

- Ahn, Yongkil, and Dongyeon Kim. 2021. Emotional Trading in the Cryptocurrency Market. Finance Research Letters 42: 101912. [Google Scholar] [CrossRef]

- Akhtaruzzaman, Md, Ahmet Sensoy, and Shaen Corbet. 2020. The Influence of Bitcoin on Portfolio Diversification and Design. Finance Research Letters 37: 101344. [Google Scholar] [CrossRef]

- Akyildirim, Erdinc, Ahmet Faruk Aysan, Oguzhan Cepni, and S. Pinar Ceyhan Darendeli. 2021a. Do Investor Sentiments Drive Cryptocurrency Prices? Economics Letters 206: 109980. [Google Scholar] [CrossRef]

- Akyildirim, Erdinc, Oguzhan Cepni, Shaen Corbet, and Gazi Salah Uddin. 2021b. Forecasting Mid-Price Movement of Bitcoin Futures Using Machine Learning. Annals of Operations Research, 1–32. [Google Scholar] [CrossRef]

- Alexander, Carol, Jaehyuk Choi, Hamish R. A. Massie, and Sungbin Sohn. 2020. Price Discovery and Microstructure in Ether Spot and Derivative Markets. International Review of Financial Analysis 71: 101506. [Google Scholar] [CrossRef]

- Almeida, José. 2021. Cryptocurrencies and Financial Markets–Extant Literature and Future Venues. European Journal of Economics Finance and Administrative Sciences 109: 29–40. [Google Scholar]

- Almeida, José, and Tiago Cruz Gonçalves. 2022. A Systematic Literature Review of Volatility and Risk Management on Cryptocurrency Investment: A Methodological Point of View. Risks 10: 107. [Google Scholar] [CrossRef]

- Aloui, Chaker, Hela ben Hamida, and Larisa Yarovaya. 2021. Are Islamic Gold-Backed Cryptocurrencies Different? Finance Research Letters 39: 101615. [Google Scholar] [CrossRef]

- Al-Yahyaee, Khamis Hamed, Mobeen Ur Rehman, Walid Mensi, and Idries Mohammad Wanas Al-Jarrah. 2019. Can Uncertainty Indices Predict Bitcoin Prices? A Revisited Analysis Using Partial and Multivariate Wavelet Approaches. North American Journal of Economics and Finance 49: 47–56. [Google Scholar] [CrossRef]

- Andrada-Félix, Julián, Adrian Fernandez-Perez, and Simón Sosvilla-Rivero. 2020. Distant or Close Cousins: Connectedness between Cryptocurrencies and Traditional Currencies Volatilities. Journal of International Financial Markets, Institutions and Money 67: 101219. [Google Scholar] [CrossRef]

- Angerer, Martin, Christian Hugo Hoffmann, Florian Neitzert, and Sascha Kraus. 2020. Objective and Subjective Risks of Investing into Cryptocurrencies. Finance Research Letters 40: 101737. [Google Scholar] [CrossRef]

- Ante, Lennart, Ingo Fiedler, and Elias Strehle. 2021. The Influence of Stablecoin Issuances on Cryptocurrency Markets. Finance Research Letters 41: 101867. [Google Scholar] [CrossRef]

- Apergis, Nicholas, Dimitrios Koutmos, and James E. Payne. 2020. Convergence in Cryptocurrency Prices? The Role of Market Microstructure. Finance Research Letters 40: 101685. [Google Scholar] [CrossRef]

- Appel, Dominik, and Michael Grabinski. 2011. The origin of financial crisis: A wrong definition of value. Portuguese Journal of Quantitative Methods 2: 33–51. [Google Scholar]

- Aysan, Ahmet Faruk, Hüseyin Bedir Demirtaş, and Mustafa Saraç. 2021. The Ascent of Bitcoin: Bibliometric Analysis of Bitcoin Research. Journal of Risk and Financial Management 14: 427. [Google Scholar] [CrossRef]

- Balli, Faruk, Anne de Bruin, Md Iftekhar Hasan Chowdhury, and Muhammad Abubakr Naeem. 2020. Connectedness of Cryptocurrencies and Prevailing Uncertainties. Applied Economics Letters 27: 1316–22. [Google Scholar] [CrossRef]

- Bariviera, Aurelio F., and Ignasi Merediz-Solà. 2021. Where Do We Stand in Cryptocurrencies Economic Research? A Survey Based on Hybrid Analysis. Journal of Economic Surveys 35: 377–407. [Google Scholar] [CrossRef]

- Bartolacci, Francesca, Andrea Caputo, and Michela Soverchia. 2020. Sustainability and Financial Performance of Small and Medium Sized Enterprises: A Bibliometric and Systematic Literature Review. Business Strategy and the Environment 29: 1297–1309. [Google Scholar] [CrossRef]

- Bazán-Palomino, Walter. 2020. How Are Bitcoin Forks Related to Bitcoin? Finance Research Letters 40: 101723. [Google Scholar] [CrossRef]

- Bedi, Prateek, and Tripti Nashier. 2020. On the Investment Credentials of Bitcoin: A Cross-Currency Perspective. Research in International Business and Finance 51: 101087. [Google Scholar] [CrossRef]

- Będowska-Sójka, Barbara, and Agata Kliber. 2021. Is There One Safe-Haven for Various Turbulences? The Evidence from Gold, Bitcoin and Ether. North American Journal of Economics and Finance 56: 101390. [Google Scholar] [CrossRef]

- Bhuiyan, Rubaiyat Ahsan, Afzol Husain, and Changyong Zhang. 2021. A Wavelet Approach for Causal Relationship between Bitcoin and Conventional Asset Classes. Resources Policy 71: 101971. [Google Scholar] [CrossRef]

- Białkowski, Jędrzej. 2020. Cryptocurrencies in Institutional Investors’ Portfolios: Evidence from Industry Stop-Loss Rules. Economics Letters 191: 108834. [Google Scholar] [CrossRef]

- Bouri, Elie, Chi Keung Marco Lau, Brian Lucey, and David Roubaud. 2019. Trading Volume and the Predictability of Return and Volatility in the Cryptocurrency Market. Finance Research Letters 29: 340–46. [Google Scholar] [CrossRef] [Green Version]

- Bouri, Elie, Brian Lucey, and David Roubaud. 2020a. Cryptocurrencies and the Downside Risk in Equity Investments. Finance Research Letters 33: 101211. [Google Scholar] [CrossRef]

- Bouri, Elie, Brian Lucey, and David Roubaud. 2020b. The Volatility Surprise of Leading Cryptocurrencies: Transitory and Permanent Linkages. Finance Research Letters 33: 101188. [Google Scholar] [CrossRef]

- Bouri, Elie, David Roubaud, and Syed Jawad Hussain Shahzad. 2020c. Do Bitcoin and Other Cryptocurrencies Jump Together? Quarterly Review of Economics and Finance 76: 396–409. [Google Scholar] [CrossRef]

- Bouri, Elie, Syed Jawad Hussain Shahzad, and David Roubaud. 2020d. Cryptocurrencies as Hedges and Safe-Havens for US Equity Sectors. Quarterly Review of Economics and Finance 75: 294–307. [Google Scholar] [CrossRef]

- Bouri, Elie, David Gabauer, Rangan Gupta, and Aviral Kumar Tiwari. 2021a. Volatility Connectedness of Major Cryptocurrencies: The Role of Investor Happiness. Journal of Behavioral and Experimental Finance 30: 100463. [Google Scholar] [CrossRef]

- Bouri, Elie, Tareq Saeed, Xuan Vinh Vo, and David Roubaud. 2021b. Quantile Connectedness in the Cryptocurrency Market. Journal of International Financial Markets Institutions and Money 71: 101302. [Google Scholar] [CrossRef]

- Bouri, Elie, Xuan Vinh Vo, and Tareq Saeed. 2021c. Return Equicorrelation in the Cryptocurrency Market: Analysis and Determinants. Finance Research Letters 38: 101497. [Google Scholar] [CrossRef]

- Bouri, Elie, Ladislav Kristoufek, and Nehme Azoury. 2022. Bitcoin and S&P500: Co-Movements of High-Order Moments in the Time-Frequency Domain. PLoS ONE 17: e0277924. [Google Scholar] [CrossRef]

- Burggraf, Tobias. 2021. Beyond Risk Parity–A Machine Learning-Based Hierarchical Risk Parity Approach on Cryptocurrencies. Finance Research Letters 38: 101523. [Google Scholar] [CrossRef]

- Cao, Guangxi, and Wenhao Xie. 2021. The Impact of the Shutdown Policy on the Asymmetric Interdependence Structure and Risk Transmission of Cryptocurrency and China’s Financial Market. North American Journal of Economics and Finance 58: 101514. [Google Scholar] [CrossRef]

- Caputo, Andrea, Giacomo Marzi, Jane Maley, and Mario Silic. 2019. Ten Years of Conflict Management Research 2007-2017: An Update on Themes, Concepts and Relationships. International Journal of Conflict Management 30: 87–110. [Google Scholar] [CrossRef]

- Charfeddine, Lanouar, Noureddine Benlagha, and Youcef Maouchi. 2020. Investigating the Dynamic Relationship between Cryptocurrencies and Conventional Assets: Implications for Financial Investors. Economic Modelling 85: 198–217. [Google Scholar] [CrossRef]

- Chemkha, Rahma, Ahmed BenSaïda, Ahmed Ghorbel, and Tahar Tayachi. 2021. Hedge and Safe Haven Properties during COVID-19: Evidence from Bitcoin and Gold. Quarterly Review of Economics and Finance 82: 71–85. [Google Scholar] [CrossRef]

- Colon, Francisco, Chaehyun Kim, Hana Kim, and Wonjoon Kim. 2021. The Effect of Political and Economic Uncertainty on the Cryptocurrency Market. Finance Research Letters 39: 101621. [Google Scholar] [CrossRef]

- Conlon, Thomas, Shaen Corbet, and Richard J. McGee. 2020. Are Cryptocurrencies a Safe Haven for Equity Markets? An International Perspective from the COVID-19 Pandemic. Research in International Business and Finance 54: 101248. [Google Scholar] [CrossRef] [PubMed]

- Conlon, Thomas, Shaen Corbet, and Richard J. McGee. 2021. Inflation and Cryptocurrencies Revisited: A Time-Scale Analysis. Economics Letters 206: 109996. [Google Scholar] [CrossRef]

- Corbet, Shaen, Brian Lucey, Andrew Urquhart, and Larisa Yarovaya. 2019. Cryptocurrencies as a Financial Asset: A Systematic Analysis. International Review of Financial Analysis 62: 182–99. [Google Scholar] [CrossRef] [Green Version]

- Corbet, Shaen, Yang (Greg) Hou, Yang Hu, Charles Larkin, and Les Oxley. 2020a. Any Port in a Storm: Cryptocurrency Safe-Havens during the COVID-19 Pandemic. Economics Letters 194: 109377. [Google Scholar] [CrossRef] [PubMed]

- Corbet, Shaen, Paraskevi Katsiampa, and Chi Keung Marco Lau. 2020b. Measuring Quantile Dependence and Testing Directional Predictability between Bitcoin, Altcoins and Traditional Financial Assets. International Review of Financial Analysis 71: 101571. [Google Scholar] [CrossRef]

- Corbet, Shaen, Charles Larkin, and Brian Lucey. 2020c. The Contagion Effects of the COVID-19 Pandemic: Evidence from Gold and Cryptocurrencies. Finance Research Letters 35: 101554. [Google Scholar] [CrossRef]

- Corbet, Shaen, Brian Lucey, and Larisa Yarovaya. 2021. Bitcoin-Energy Markets Interrelationships—New Evidence. Resources Policy 70: 101916. [Google Scholar] [CrossRef]

- Demir, Ender, Mehmet Huseyin Bilgin, Gokhan Karabulut, and Asli Cansin Doker. 2020a. The Relationship between Cryptocurrencies and COVID-19 Pandemic. Eurasian Economic Review 10: 349–60. [Google Scholar] [CrossRef]

- Demir, Ender, Serdar Simonyan, Conrado Diego García-Gómez, and Chi Keung Marco Lau. 2020b. The Asymmetric Effect of Bitcoin on Altcoins: Evidence from the Nonlinear Autoregressive Distributed Lag (NARDL) Model. Finance Research Letters 40: 101754. [Google Scholar] [CrossRef]

- Demiralay, Sercan, and Selçuk Bayracı. 2020. Should Stock Investors Include Cryptocurrencies in Their Portfolios after All? Evidence from a Conditional Diversification Benefits Measure. International Journal of Finance and Economics 26: 6188–204. [Google Scholar] [CrossRef]

- Demiralay, Sercan, and Petros Golitsis. 2021. On the Dynamic Equicorrelations in Cryptocurrency Market. Quarterly Review of Economics and Finance 80: 524–33. [Google Scholar] [CrossRef]

- Dimpfl, Thomas, and Dalia Elshiaty. 2021. Volatility Discovery in Cryptocurrency Markets. Journal of Risk Finance. ahead-of-print. [Google Scholar] [CrossRef]

- Ding, Ying, Ronald Rousseau, and Dietmar Wolfram. 2014. Measuring Scholarly Impact. Cham: Springer. [Google Scholar] [CrossRef]

- Disli, Mustafa, Ruslan Nagayev, Kinan Salim, Siti K. Rizkiah, and Ahmet F. Aysan. 2021. In Search of Safe Haven Assets during COVID-19 Pandemic: An Empirical Analysis of Different Investor Types. Research in International Business and Finance 58: 101461. [Google Scholar] [CrossRef]

- Fakhfekh, Mohamed, Ahmed Jeribi, Ahmed Ghorbel, and Nejib Hachicha. 2021. Hedging Stock Market Prices with WTI, Gold, VIX and Cryptocurrencies: A Comparison between DCC, ADCC and GO-GARCH Models. International Journal of Emerging Markets. [Google Scholar] [CrossRef]

- Fang, Tong, Zhi Su, and Libo Yin. 2020. Economic Fundamentals or Investor Perceptions? The Role of Uncertainty in Predicting Long-Term Cryptocurrency Volatility. International Review of Financial Analysis 71: 101566. [Google Scholar] [CrossRef]

- Fang, Fan, Waichung Chung, Carmine Ventre, Michail Basios, Leslie Kanthan, Lingbo Li, and Fan Wu. 2021. Ascertaining Price Formation in Cryptocurrency Markets with Machine Learning. European Journal of Finance, 1–23. [Google Scholar] [CrossRef]

- Feng, Wenjun, Yiming Wang, and Zhengjun Zhang. 2018. Informed Trading in the Bitcoin Market. Finance Research Letters 26: 63–70. [Google Scholar] [CrossRef]

- Flori, Andrea. 2019a. Cryptocurrencies in Finance: Review and Applications. International Journal of Theoretical and Applied Finance 22. [Google Scholar] [CrossRef]

- Flori, Andrea. 2019b. News and Subjective Beliefs: A Bayesian Approach to Bitcoin Investments. Research in International Business and Finance 50: 336–56. [Google Scholar] [CrossRef]

- Galvao, Anderson, Carla Mascarenhas, Carla Marques, João Ferreira, and Vanessa Ratten. 2019. Triple Helix and Its Evolution: A Systematic Literature Review. Journal of Science and Technology Policy Management 10: 812–33. [Google Scholar] [CrossRef]

- García-Corral, Francisco Javier, José Antonio Cordero-García, Jaime de Pablo-Valenciano, and Juan Uribe-Toril. 2022. A Bibliometric Review of Cryptocurrencies: How Have They Grown? Financial Innovation 8: 1–31. [Google Scholar] [CrossRef] [PubMed]

- Gemici, Eray, and Müslüm Polat. 2020. Causality-in-Mean and Causality-in-Variance among Bitcoin, Litecoin, and Ethereum. Studies in Economics and Finance 38: 861–72. [Google Scholar] [CrossRef]

- Ghabri, Yosra, Khaled Guesmi, and Ahlem Zantour. 2020. Bitcoin and Liquidity Risk Diversification. Finance Research Letters 40: 101679. [Google Scholar] [CrossRef]

- Ghorbel, Achraf, and Ahmed Jeribi. 2021a. Investigating the Relationship between Volatilities of Cryptocurrencies and Other Financial Assets. Decisions in Economics and Finance 44: 817–843. [Google Scholar] [CrossRef]

- Ghorbel, Achraf, and Ahmed Jeribi. 2021b. Volatility Spillovers and Contagion between Energy Sector and Financial Assets during COVID-19 Crisis Period. Eurasian Economic Review 11: 449–67. [Google Scholar] [CrossRef]

- González, Maria de la O., Francisco Jareño, and Frank S. Skinner. 2021. Asymmetric Interdependencies between Large Capital Cryptocurrency and Gold Returns during the COVID-19 Pandemic Crisis. International Review of Financial Analysis 76: 101773. [Google Scholar] [CrossRef]

- Goodell, John W., and Stephane Goutte. 2021a. Co-Movement of COVID-19 and Bitcoin: Evidence from Wavelet Coherence Analysis. Finance Research Letters 38: 101625. [Google Scholar] [CrossRef]

- Goodell, John W., and Stephane Goutte. 2021b. Diversifying Equity with Cryptocurrencies during COVID-19. International Review of Financial Analysis 76: 101781. [Google Scholar] [CrossRef]

- Gozgor, Giray, Aviral Kumar Tiwari, Ender Demir, and Sagi Akron. 2019. The Relationship between Bitcoin Returns and Trade Policy Uncertainty. Finance Research Letters 29: 75–82. [Google Scholar] [CrossRef]

- Grabinski, Michael, and Galiya Klinkova. 2019. Wrong use of averages implies wrong results from many heuristic models. Applied Mathematics 10: 605. [Google Scholar] [CrossRef]

- Grabinski, Michael, and Galiya Klinkova. 2020. Scrutinizing distributions proves that IQ is inherited and explains the fat tail. Applied Mathematics 11: 957–84. [Google Scholar] [CrossRef]

- Grobys, Klaus, Juha Junttila, James W. Kolari, and Niranjan Sapkota. 2021. On the Stability of Stablecoins. Journal of Empirical Finance 64: 207–23. [Google Scholar] [CrossRef]

- Guo, Xiaochun, Fengbin Lu, and Yunjie Wei. 2021. Capture the Contagion Network of Bitcoin–Evidence from Pre and Mid COVID-19. Research in International Business and Finance 58: 101484. [Google Scholar] [CrossRef] [PubMed]

- Hairudin, Aiman, Imtiaz Mohammad Sifat, Azhar Mohamad, and Yusniliyana Yusof. 2020. Cryptocurrencies: A Survey on Acceptance, Governance and Market Dynamics. International Journal of Finance and Economics 27: 4633–59. [Google Scholar] [CrossRef]

- Haq, Inzamam Ul, Apichit Maneengam, Supat Chupradit, Wanich Suksatan, and Chunhui Huo. 2021. Economic Policy Uncertainty and Cryptocurrency Market as a Risk Management Avenue: A Systematic Review. Risks 9: 163. [Google Scholar] [CrossRef]

- Hassan, M. Kabir, Md Bokhtiar Hasan, and Md Mamunur Rashid. 2021. Using Precious Metals to Hedge Cryptocurrency Policy and Price Uncertainty. Economics Letters 206: 109977. [Google Scholar] [CrossRef]

- Hattori, Takahiro, and Ryo Ishida. 2021. Did the Introduction of Bitcoin Futures Crash the Bitcoin Market at the End of 2017? North American Journal of Economics and Finance 56: 101322. [Google Scholar] [CrossRef]

- Hoang, Lai T., and Dirk G. Baur. 2021. How Stable Are Stablecoins? European Journal of Finance, 1–17. [Google Scholar] [CrossRef]

- Holub, Mark, and Jackie Johnson. 2019. The Impact of the Bitcoin Bubble of 2017 on Bitcoin’s P2P Market. Finance Research Letters 29: 357–62. [Google Scholar] [CrossRef]

- Hsu, Shu Han, Chwen Sheu, and Jiho Yoon. 2021. Risk Spillovers between Cryptocurrencies and Traditional Currencies and Gold under Different Global Economic Conditions. North American Journal of Economics and Finance 57: 101443. [Google Scholar] [CrossRef]

- Huynh, Toan Luu Duc. 2021. Does Bitcoin React to Trump’s Tweets? Journal of Behavioral and Experimental Finance 31: 100546. [Google Scholar] [CrossRef]

- Huynh, Toan Luu Duc, Erik Hille, and Muhammad Ali Nasir. 2020a. Diversification in the Age of the 4th Industrial Revolution: The Role of Artificial Intelligence, Green Bonds and Cryptocurrencies. Technological Forecasting and Social Change 159: 120188. [Google Scholar] [CrossRef]

- Huynh, Toan Luu Duc, Muhammad Ali Nasir, Xuan Vinh Vo, and Thong Trung Nguyen. 2020b. ‘Small Things Matter Most’: The Spillover Effects in the Cryptocurrency Market and Gold as a Silver Bullet. North American Journal of Economics and Finance 54: 101277. [Google Scholar] [CrossRef]

- Huynh, Anh Ngoc Quang, Duy Duong, Tobias Burggraf, Hien Thi Thu Luong, and Nam Huu Bui. 2021. Energy Consumption and Bitcoin Market. Asia-Pacific Financial Markets 29: 79–93. [Google Scholar] [CrossRef]

- Iqbal, Najaf, Zeeshan Fareed, Guangcai Wan, and Farrukh Shahzad. 2021. Asymmetric Nexus between COVID-19 Outbreak in the World and Cryptocurrency Market. International Review of Financial Analysis 73: 101613. [Google Scholar] [CrossRef]

- Jalal, Raja Nabeel Ud Din, Ilan Alon, and Andrea Paltrinieri. 2021. A Bibliometric Review of Cryptocurrencies as a Financial Asset. Technology Analysis and Strategic Management, 1–16. [Google Scholar] [CrossRef]

- Jalan, Akanksha, Roman Matkovskyy, and Andrew Urquhart. 2021. What Effect Did the Introduction of Bitcoin Futures Have on the Bitcoin Spot Market? European Journal of Finance 27: 1251–81. [Google Scholar] [CrossRef]

- Jareño, Francisco, María de la O. González, Marta Tolentino, and Karen Sierra. 2020. Bitcoin and Gold Price Returns: A Quantile Regression and NARDL Analysis. Resources Policy 67: 101666. [Google Scholar] [CrossRef]

- Jareño, Francisco, María de la O. González, Raquel López, and Ana Rosa Ramos. 2021. Cryptocurrencies and Oil Price Shocks: A NARDL Analysis in the COVID-19 Pandemic. Resources Policy 74: 102281. [Google Scholar] [CrossRef]

- Jeribi, Ahmed, and Achraf Ghorbel. 2021. Forecasting Developed and BRICS Stock Markets with Cryptocurrencies and Gold: Generalized Orthogonal Generalized Autoregressive Conditional Heteroskedasticity and Generalized Autoregressive Score Analysis. International Journal of Emerging Markets. [Google Scholar] [CrossRef]

- Ji, Qiang, Elie Bouri, Chi Keung Marco Lau, and David Roubaud. 2019a. Dynamic Connectedness and Integration in Cryptocurrency Markets. International Review of Financial Analysis 63: 257–72. [Google Scholar] [CrossRef]

- Ji, Qiang, Elie Bouri, David Roubaud, and Ladislav Kristoufek. 2019b. Information Interdependence among Energy, Cryptocurrency and Major Commodity Markets. Energy Economics 81: 1042–55. [Google Scholar] [CrossRef]

- Jiang, Shangrong, Xuerong Li, and Shouyang Wang. 2021. Exploring Evolution Trends in Cryptocurrency Study: From Underlying Technology to Economic Applications. Finance Research Letters 38: 101532. [Google Scholar] [CrossRef]

- Jiang, Yonghong, Jiayi Lie, Jieru Wang, and Jinqi Mu. 2021a. Revisiting the Roles of Cryptocurrencies in Stock Markets: A Quantile Coherency Perspective. Economic Modelling 95: 21–34. [Google Scholar] [CrossRef]

- Jiang, Yonghong, Lanxin Wu, Gengyu Tian, and He Nie. 2021b. Do Cryptocurrencies Hedge against EPU and the Equity Market Volatility during COVID-19?–New Evidence from Quantile Coherency Analysis. Journal of International Financial Markets Institutions and Money 72: 101324. [Google Scholar] [CrossRef]

- Jin, Xuejun, Keer Zhu, Xiaolan Yang, and Shouyang Wang. 2021. Estimating the Reaction of Bitcoin Prices to the Uncertainty of Fiat Currency. Research in International Business and Finance 58: 101451. [Google Scholar] [CrossRef]

- Katsiampa, Paraskevi, Shaen Corbet, and Brian Lucey. 2019. High Frequency Volatility Co-Movements in Cryptocurrency Markets. Journal of International Financial Markets, Institutions and Money 62: 35–52. [Google Scholar] [CrossRef]

- Khelifa, Soumaya Ben, Khaled Guesmi, and Christian Urom. 2021. Exploring the relationship between cryptocurrencies and hedge funds during COVID-19 crisis. International Review of Financial Analysis 76: 101777. [Google Scholar] [CrossRef]

- Kim, Myeong Jun, Nguyen Phuc Canh, and Sung Y. Park. 2021. Causal Relationship among Cryptocurrencies: A Conditional Quantile Approach. Finance Research Letters 42: 1–8. [Google Scholar] [CrossRef]

- Kinkyo, Takuji. 2020. Hedging Capabilities of Bitcoin for Asian Currencies. International Journal of Finance and Economics 27: 1769–84. [Google Scholar] [CrossRef]

- Klinkova, G., and M. Grabinski. 2017. Due to Instability Gambling is the best Model for most Financial Products. Archives of Business Research 5: 255–61. [Google Scholar] [CrossRef] [Green Version]

- Koki, Constandina, Stefanos Leonardos, and Georgios Piliouras. 2022. Exploring the predictability of cryptocurrencies via Bayesian hidden Markov models. Research in International Business and Finance 59: 101554. [Google Scholar] [CrossRef]

- Kumah, Seyram Pearl, and Jones Odei Mensah. 2020. Are cryptocurrencies connected to gold? A wavelet-based quantile-in-quantile approach. International Journal of Finance and Economics 27: 3640–59. [Google Scholar] [CrossRef]

- Kumah, Seyram Pearl, and Jones Odei-Mensah. 2021. Are Cryptocurrencies and African stock markets integrated? Quarterly Review of Economics and Finance 81: 330–41. [Google Scholar] [CrossRef]

- Kumar, Ashish, Najaf Iqbal, Subrata Kumar Mitra, Ladislav Kristoufek, and Elie Bouri. 2022. Connectedness among major cryptocurrencies in standard times and during the COVID-19 outbreak. Journal of International Financial Markets, Institutions and Money 77: 101523. [Google Scholar] [CrossRef]

- Kwon, Ji Ho. 2020. Tail behavior of Bitcoin, the dollar, gold and the stock market index. Journal of International Financial Markets, Institutions and Money 67: 101202. [Google Scholar] [CrossRef]

- Kyriazis, Nikolaos, Stephanos Papadamou, and Shaen Corbet. 2020. A Systematic Review of the Bubble Dynamics of Cryptocurrency Prices. Research in International Business and Finance 54: 101254. [Google Scholar] [CrossRef]

- Lahiani, Amine, Ahmed jeribi, and Nabila Boukef Jlassi. 2021. Nonlinear Tail Dependence in Cryptocurrency-Stock Market Returns: The Role of Bitcoin Futures. Research in International Business and Finance 56: 101351. [Google Scholar] [CrossRef]

- Li, Rong, Sufang Li, Di Yuan, and Huiming Zhu. 2021. Investor Attention and Cryptocurrency: Evidence from Wavelet-Based Quantile Granger Causality Analysis. Research in International Business and Finance 56: 101389. [Google Scholar] [CrossRef]

- Liang, Xiaobei, Yibo Yang, and Jiani Wang. 2016. Internet Finance: A Systematic Literature Review and Bibliometric Analysis. Proceedings of the International Conference on Electronic Business (ICEB) 38. Available online: https://aisel.aisnet.org/iceb2016/38 (accessed on 14 November 2022).

- Lin, Zih Ying. 2021. Investor Attention and Cryptocurrency Performance. Finance Research Letters 40: 101702. [Google Scholar] [CrossRef]

- Linnenluecke, Martina K., Mauricio Marrone, and Abhay K. Singh. 2020. Conducting Systematic Literature Reviews and Bibliometric Analyses. Australian Journal of Management 45: 175–94. [Google Scholar] [CrossRef]

- Liu, Ruozhou, Shanfeng Wan, Zili Zhang, and Xuejun Zhao. 2020. Is the Introduction of Futures Responsible for the Crash of Bitcoin? Finance Research Letters 34: 101259. [Google Scholar] [CrossRef]

- Liu, Wei, Artur Semeyutin, Chi Keung Marco Lau, and Giray Gozgor. 2020. Forecasting Value-at-Risk of Cryptocurrencies with RiskMetrics Type Models. Research in International Business and Finance 54: 101259. [Google Scholar] [CrossRef]

- López-Cabarcos, M. Ángeles, Ada M. Pérez-Pico, Juan Piñeiro-Chousa, and Aleksandar Šević. 2021. Bitcoin Volatility, Stock Market and Investor Sentiment. Are They Connected? Finance Research Letters 38: 101399. [Google Scholar] [CrossRef]

- Ma, Yechi, Ferhana Ahmad, Miao Liu, and Zilong Wang. 2020. Portfolio Optimization in the Era of Digital Financialization Using Cryptocurrencies. Technological Forecasting and Social Change 161: 120265. [Google Scholar] [CrossRef]

- Majdoub, Jihed, Salim Ben Sassi, and Azza Bejaoui. 2021. Can Fiat Currencies Really Hedge Bitcoin? Evidence from Dynamic Short-Term Perspective. Decisions in Economics and Finance 44: 789–816. [Google Scholar] [CrossRef]

- Mariana, Christy Dwita, Irwan Adi Ekaputra, and Zaäfri Ananto Husodo. 2021. Are Bitcoin and Ethereum Safe-Havens for Stocks during the COVID-19 Pandemic? Finance Research Letters 38: 101798. [Google Scholar] [CrossRef]

- Matkovskyy, Roman, Akanksha Jalan, Michael Dowling, and Taoufik Bouraoui. 2021. From Bottom Ten to Top Ten: The Role of Cryptocurrencies in Enhancing Portfolio Return of Poorly Performing Stocks. Finance Research Letters 38: 101405. [Google Scholar] [CrossRef]

- Mensi, Walid, Ahmet Sensoy, Aylin Aslan, and Sang Hoon Kang. 2019. High-Frequency Asymmetric Volatility Connectedness between Bitcoin and Major Precious Metals Markets. North American Journal of Economics and Finance 50: 101031. [Google Scholar] [CrossRef]

- Mensi, Walid, Khamis Hamed Al-Yahyaee, Idries Mohammad Wanas Al-Jarrah, Xuan Vinh Vo, and Sang Hoon Kang. 2020a. Dynamic Volatility Transmission and Portfolio Management across Major Cryptocurrencies: Evidence from Hourly Data. North American Journal of Economics and Finance 54: 101285. [Google Scholar] [CrossRef]

- Mensi, Walid, Mobeen Ur Rehman, Debasish Maitra, Khamis Hamed Al-Yahyaee, and Ahmet Sensoy. 2020b. Does Bitcoin Co-Move and Share Risk with Sukuk and World and Regional Islamic Stock Markets? Evidence Using a Time-Frequency Approach. Research in International Business and Finance 53: 101230. [Google Scholar] [CrossRef]

- Milian, Eduardo Z., Mauro de M. Spinola, and Marly M. de Carvalho. 2019. Fintechs: A Literature Review and Research Agenda. Electronic Commerce Research and Applications 34: 100833. [Google Scholar] [CrossRef]

- Mokni, Khaled. 2021. When, Where, and How Economic Policy Uncertainty Predicts Bitcoin Returns and Volatility? A Quantiles-Based Analysis. Quarterly Review of Economics and Finance 80: 65–73. [Google Scholar] [CrossRef]

- Moratis, George. 2021. Quantifying the Spillover Effect in the Cryptocurrency Market. Finance Research Letters 38: 101534. [Google Scholar] [CrossRef]

- Naeem, Muhammad, Elie Bouri, Gideon Boako, and David Roubaud. 2020. Tail Dependence in the Return-Volume of Leading Cryptocurrencies. Finance Research Letters 36: 101326. [Google Scholar] [CrossRef]

- Naeem, Muhammad Abubakr, Saqib Farid, Faruk Balli, and Syed Jawad Hussain Shahzad. 2021a. Hedging the Downside Risk of Commodities through Cryptocurrencies. Applied Economics Letters 28: 153–60. [Google Scholar] [CrossRef]

- Naeem, Muhammad Abubakr, Saba Qureshi, Mobeen Ur Rehman, and Faruk Balli. 2021b. COVID-19 and Cryptocurrency Market: Evidence from Quantile Connectedness. Applied Economics 54: 280–306. [Google Scholar] [CrossRef]

- Nakamoto, Satoshi. 2008. Bitcoin: A Peer-to-Peer Electronic Cash System. Available online: https://bitcoin.org/en/bitcoin-paper (accessed on 10 October 2022).

- Nguyen, Thai Vu Hong, Binh Thanh Nguyen, Kien Son Nguyen, and Huy Pham. 2019. Asymmetric Monetary Policy Effects on Cryptocurrency Markets. Research in International Business and Finance 48: 335–39. [Google Scholar] [CrossRef]

- Nguyen, Linh Hoang, Thanaset Chevapatrakul, and Kai Yao. 2020. Investigating Tail-Risk Dependence in the Cryptocurrency Markets: A LASSO Quantile Regression Approach. Journal of Empirical Finance 58: 333–55. [Google Scholar] [CrossRef]

- Nguyen Quang, Binh, Thai Ha Le, and Canh Nguyen Phuc. 2020. Influences of Uncertainty on the Returns and Liquidity of Cryptocurrencies: Evidence from a Portfolio Approach. International Journal of Finance and Economics 27: 2497–513. [Google Scholar] [CrossRef]

- Okorie, David Iheke, and Boqiang Lin. 2020. Crude Oil Price and Cryptocurrencies: Evidence of Volatility Connectedness and Hedging Strategy. Energy Economics 87: 104703. [Google Scholar] [CrossRef]

- Omane-Adjepong, Maurice, and Imhotep Paul Alagidede. 2020. Dynamic Linkages and Economic Role of Leading Cryptocurrencies in an Emerging Market. In Asia-Pacific Financial Markets. Tokyo: Springer, vol. 27. [Google Scholar] [CrossRef]

- Papadamou, Stephanos, Nikolaos A. Kyriazis, and Panayiotis G. Tzeremes. 2021. Non-Linear Causal Linkages of EPU and Gold with Major Cryptocurrencies during Bull and Bear Markets. North American Journal of Economics and Finance 56: 101343. [Google Scholar] [CrossRef]

- Philippas, Dionisis, Nikolaos Philippas, Panagiotis Tziogkidis, and Hatem Rjiba. 2020. Signal-Herding in Cryptocurrencies. Journal of International Financial Markets, Institutions and Money 65: 101191. [Google Scholar] [CrossRef]

- Pho, Kim Hung, Sel Ly, Richard Lu, Thi Hong Van Hoang, and Wing Keung Wong. 2021. Is Bitcoin a Better Portfolio Diversifier than Gold? A Copula and Sectoral Analysis for China. International Review of Financial Analysis 74: 101674. [Google Scholar] [CrossRef]

- Platanakis, Emmanouil, and Andrew Urquhart. 2019. Portfolio Management with Cryptocurrencies: The Role of Estimation Risk. Economics Letters 177: 76–80. [Google Scholar] [CrossRef] [Green Version]

- Polat, Onur, and Eylül Kabakçı Günay. 2021. Cryptocurrency Connectedness Nexus the COVID-19 Pandemic: Evidence from Time-Frequency Domains. Studies in Economics and Finance 38: 946–63. [Google Scholar] [CrossRef]

- Qiao, Xingzhi, Huiming Zhu, and Liya Hau. 2020. Time-Frequency Co-Movement of Cryptocurrency Return and Volatility: Evidence from Wavelet Coherence Analysis. International Review of Financial Analysis 71: 101541. [Google Scholar] [CrossRef]

- Qiu, Yue, Yifan Wang, and Tian Xie. 2021. Forecasting Bitcoin Realized Volatility by Measuring the Spillover Effect among Cryptocurrencies. Economics Letters 208: 110092. [Google Scholar] [CrossRef]

- Raheem, Ibrahim D. 2021. COVID-19 Pandemic and the Safe Haven Property of Bitcoin. Quarterly Review of Economics and Finance 81: 370–75. [Google Scholar] [CrossRef]

- Rialti, Riccardo, Giacomo Marzi, Cristiano Ciappei, and Donatella Busso. 2019. Big Data and Dynamic Capabilities: A Bibliometric Analysis and Systematic Literature Review. Management Decision 57: 2052–68. [Google Scholar] [CrossRef] [Green Version]

- Rognone, Lavinia, Stuart Hyde, and S. Sarah Zhang. 2020. News Sentiment in the Cryptocurrency Market: An Empirical Comparison with Forex. International Review of Financial Analysis 69: 101462. [Google Scholar] [CrossRef]

- Sadeghi Moghadam, Mohammad Reza, Hossein Safari, and Narjes Yousefi. 2021. Clustering Quality Management Models and Methods: Systematic Literature Review and Text-Mining Analysis Approach. Total Quality Management and Business Excellence 32: 241–64. [Google Scholar] [CrossRef]

- Sahoo, Pradipta Kumar. 2021. COVID-19 Pandemic and Cryptocurrency Markets: An Empirical Analysis from a Linear and Nonlinear Causal Relationship. Studies in Economics and Finance 38: 454–68. [Google Scholar] [CrossRef]

- Scharnowski, Stefan. 2021. Understanding Bitcoin Liquidity. Finance Research Letters 38: 101477. [Google Scholar] [CrossRef]

- Schellinger, Benjamin. 2020. Optimization of Special Cryptocurrency Portfolios. Journal of Risk Finance 21: 127–57. [Google Scholar] [CrossRef]

- Sebastião, Helder, and Pedro Godinho. 2020. Bitcoin Futures: An Effective Tool for Hedging Cryptocurrencies. Finance Research Letters 33: 101230. [Google Scholar] [CrossRef]

- Sensoy, Ahmet, Thiago Christiano Silva, Shaen Corbet, and Benjamin Miranda Tabak. 2021. High-Frequency Return and Volatility Spillovers among Cryptocurrencies. Applied Economics 53: 4310–28. [Google Scholar] [CrossRef]

- Shi, Yongjing, Aviral Kumar Tiwari, Giray Gozgor, and Zhou Lu. 2020. Correlations among Cryptocurrencies: Evidence from Multivariate Factor Stochastic Volatility Model. Research in International Business and Finance 53: 101231. [Google Scholar] [CrossRef]

- Silahli, Baykar, Kemal Dincer Dingec, Atilla Cifter, and Nezir Aydin. 2021. Portfolio Value-at-Risk with Two-Sided Weibull Distribution: Evidence from Cryptocurrency Markets. Finance Research Letters 38: 101425. [Google Scholar] [CrossRef]

- Sun, Xiaolei, Mingxi Liu, and Zeqian Sima. 2020. A Novel Cryptocurrency Price Trend Forecasting Model Based on LightGBM. Finance Research Letters 32: 101084. [Google Scholar] [CrossRef]

- Tavares, Ricardo de Souza, João Frois Caldeira, and Gerson de Souza Raimundo Júnior. 2020. It’s All in the Timing Again: Simple Active Portfolio Strategies That Outperform Naïve Diversification in the Cryptocurrency Market. Applied Economics Letters 29: 118–22. [Google Scholar] [CrossRef]

- Thampanya, Natthinee, Muhammad Ali Nasir, and Toan Luu Duc Huynh. 2020. Asymmetric Correlation and Hedging Effectiveness of Gold & Cryptocurrencies: From Pre-Industrial to the 4th Industrial Revolution. Technological Forecasting and Social Change 159: 120195. [Google Scholar]

- Trucíos, Carlos, Aviral K. Tiwari, and Faisal Alqahtani. 2020. Value-at-Risk and Expected Shortfall in Cryptocurrencies’ Portfolio: A Vine Copula–Based Approach. Applied Economics 52: 2580–93. [Google Scholar] [CrossRef]

- Uddin, Md Akther, Md Hakim Ali, and Mansur Masih. 2020. Bitcoin—A Hype or Digital Gold? Global Evidence. Australian Economic Papers 59: 215–31. [Google Scholar] [CrossRef]

- Umar, Zaghum, and Mariya Gubareva. 2020. A Time–Frequency Analysis of the Impact of the Covid-19 Induced Panic on the Volatility of Currency and Cryptocurrency Markets. Journal of Behavioral and Experimental Finance 28: 100404. [Google Scholar] [CrossRef]

- Umar, Muhammad, Chi Wei Su, Syed Kumail Abbas Rizvi, and Xue Feng Shao. 2021. Bitcoin: A Safe Haven Asset and a Winner amid Political and Economic Uncertainties in the US? Technological Forecasting and Social Change 167: 120680. [Google Scholar] [CrossRef]

- Umar, Zaghum, Francisco Jareño, and María de la O. González. 2021. The Impact of COVID-19-Related Media Coverage on the Return and Volatility Connectedness of Cryptocurrencies and Fiat Currencies. Technological Forecasting and Social Change 172: 121025. [Google Scholar] [CrossRef]

- Urom, Christian, Ilyes Abid, Khaled Guesmi, and Julien Chevallier. 2020. Quantile Spillovers and Dependence between Bitcoin, Equities and Strategic Commodities. Economic Modelling 93: 230–58. [Google Scholar] [CrossRef]

- Van Eck, Nees Jan, and Ludo Waltman. 2017. Citation-based clustering of publications using CitNetExplorer and VOSviewer. Scientometrics 111: 1053–1070. [Google Scholar] [CrossRef] [PubMed] [Green Version]

- Vo, Au, Thomas A. Chapman, and Yen Sheng Lee. 2021. Examining Bitcoin and Economic Determinants: An Evolutionary Perspective. Journal of Computer Information Systems 62: 572–86. [Google Scholar] [CrossRef]

- Wang, Jinghua, and Geoffrey M. Ngene. 2020. Does Bitcoin Still Own the Dominant Power? An Intraday Analysis. International Review of Financial Analysis 71: 101551. [Google Scholar] [CrossRef]

- Wang, Gang Jin, Chi Xie, Danyan Wen, and Longfeng Zhao. 2019. When Bitcoin Meets Economic Policy Uncertainty (EPU): Measuring Risk Spillover Effect from EPU to Bitcoin. Finance Research Letters 31: 489–97. [Google Scholar] [CrossRef]

- Wang, Gang Jin, Xin yu Ma, and Hao yu Wu. 2020. Are Stablecoins Truly Diversifiers, Hedges, or Safe Havens against Traditional Cryptocurrencies as Their Name Suggests? Research in International Business and Finance 54: 101225. [Google Scholar] [CrossRef]

- Wang, Pengfei, Xiao Li, Dehua Shen, and Wei Zhang. 2020. How Does Economic Policy Uncertainty Affect the Bitcoin Market? Research in International Business and Finance 53: 101234. [Google Scholar] [CrossRef]

- Wang, Peijin, Hongwei Zhang, Cai Yang, and Yaoqi Guo. 2021. Time and Frequency Dynamics of Connectedness and Hedging Performance in Global Stock Markets: Bitcoin versus Conventional Hedges. Research in International Business and Finance 58: 101479. [Google Scholar] [CrossRef]

- Wang, Jiqian, Feng Ma, Elie Bouri, and Yangli Guo. 2022. Which Factors Drive Bitcoin Volatility: Macroeconomic, Technical, or Both? Journal of Forecasting 1–19. [Google Scholar] [CrossRef]

- Wu, Wanshan, Aviral Kumar Tiwari, Giray Gozgor, and Huang Leping. 2021. Does Economic Policy Uncertainty Affect Cryptocurrency Markets? Evidence from Twitter-Based Uncertainty Measures. Research in International Business and Finance 58: 101478. [Google Scholar] [CrossRef]

- Xu, Qiuhua, Yixuan Zhang, and Ziyang Zhang. 2021. Tail-Risk Spillovers in Cryptocurrency Markets. Finance Research Letters 38: 101453. [Google Scholar] [CrossRef]

- Yang, Lu, and Shigeyuki Hamori. 2021. The Role of the Carbon Market in Relation to the Cryptocurrency Market: Only Diversification or More? International Review of Financial Analysis 77: 101864. [Google Scholar] [CrossRef]

- Yang, Boyu, Yuying Sun, and Shouyang Wang. 2020. A Novel Two-Stage Approach for Cryptocurrency Analysis. International Review of Financial Analysis 72: 101567. [Google Scholar] [CrossRef]

- Yen, Kuang Chieh, and Hui Pei Cheng. 2021. Economic Policy Uncertainty and Cryptocurrency Volatility. Finance Research Letters 38: 101428. [Google Scholar] [CrossRef]

- Yi, Shuyue, Zishuang Xu, and Gang Jin Wang. 2018. Volatility Connectedness in the Cryptocurrency Market: Is Bitcoin a Dominant Cryptocurrency? International Review of Financial Analysis 60: 98–114. [Google Scholar] [CrossRef]

- Yue, Yao, Xuerong Li, Dingxuan Zhang, and Shouyang Wang. 2021. How Cryptocurrency Affects Economy? A Network Analysis Using Bibliometric Methods. International Review of Financial Analysis 77: 101869. [Google Scholar] [CrossRef]

- Zeng, Ting, Mengying Yang, and Yifan Shen. 2020. Fancy Bitcoin and Conventional Financial Assets: Measuring Market Integration Based on Connectedness Networks. Economic Modelling 90: 209–20. [Google Scholar] [CrossRef]

- Zhang, Sijia, and Andros Gregoriou. 2021. Cryptocurrencies in Portfolios: Return–Liquidity Trade-off around China Forbidding Initial Coin Offerings. Applied Economics Letters 28: 1–5. [Google Scholar] [CrossRef]

- Zhang, Wei, and Yi Li. 2020. Is Idiosyncratic Volatility Priced in Cryptocurrency Markets? Research in International Business and Finance 54: 101252. [Google Scholar] [CrossRef]

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| Rank | Article | Citations |

|---|---|---|

| 1 | Corbet et al. (2020c) | 171 |

| 2 | Ji et al. (2019a) | 136 |

| 3 | Yi et al. (2018) | 104 |

| 4 | Conlon et al. (2020) | 83 |

| 5 | Goodell and Goutte (2021a) | 74 |

| 6 | Ji et al. (2019b) | 67 |

| 7 | Katsiampa et al. (2019a) | 59 |

| 8 | Bouri et al. (2019) | 57 |

| 9 | G. J. Wang et al. (2019) | 56 |

| 10 | Sun et al. (2020) | 54 |

| Rank | Authors | Publications | Citations | Citations per Publications |

|---|---|---|---|---|

| 1 | Bouri, Elie | 11 | 404 | 36.73 |

| 2 | Roubaud, David | 9 | 389 | 43.22 |

| 3 | Corbet, Shaen | 11 | 379 | 34.45 |

| 4 | Lucey, Brian | 6 | 346 | 57.67 |

| 5 | Lau, Chi Keung Marco | 6 | 206 | 34.33 |

| 6 | Ji, Qiang | 2 | 203 | 101.50 |

| 7 | Larkin, Charles | 3 | 198 | 66.00 |

| 8 | Wang, Gang-Jin | 3 | 168 | 56.00 |

| 9 | Xu, Zishuang | 1 | 104 | 104.00 |

| 10 | Yi, Shuyue | 1 | 104 | 104.00 |

| Rank | Institutions | Publications | Citations | Citations per Publications |

|---|---|---|---|---|

| 1 | Trinity College Dublin | 9 | 386 | 42.89 |

| 2 | Dublin City University | 11 | 379 | 34.45 |

| 3 | Montpellier Business School | 12 | 372 | 31.00 |

| 4 | Holy Spirit University Kaslik | 8 | 363 | 45.38 |

| 5 | University Economics Ho Chi Minh City | 15 | 361 | 24.07 |

| 6 | University Waikato | 9 | 293 | 32.56 |

| 7 | University Sydney | 5 | 276 | 55.20 |

| 8 | Chinese Academy of Science | 6 | 261 | 43.50 |

| 9 | University Bath | 4 | 235 | 58.75 |

| 10 | University Huddersfield | 6 | 223 | 37.17 |

| Rank | Journals | Publications | Citations | Citations per Publications |

|---|---|---|---|---|

| 1 | Finance research letters | 34 | 716 | 21.06 |

| 2 | International review of financial analysis | 16 | 345 | 21.56 |

| 3 | Research in international business and finance | 17 | 178 | 10.47 |

| 4 | Energy economics | 2 | 100 | 50.00 |

| 5 | Journal of international financial markets institutions and money | 6 | 93 | 15.50 |

| 6 | North American journal of economics and finance | 10 | 92 | 9.20 |

| 7 | Economic modeling | 4 | 79 | 19.75 |

| 8 | Technological forecasting and social change | 5 | 73 | 14.60 |

| 9 | Quarterly review of economics and finance | 7 | 65 | 9.29 |

| 10 | Economics letters | 6 | 53 | 8.83 |

| Rank | Country | Publications | Citations | Citations per Publications |

|---|---|---|---|---|

| 1 | Peoples R. China | 35 | 686 | 19.60 |

| 2 | England | 27 | 614 | 22.74 |

| 3 | France | 23 | 567 | 24.65 |

| 4 | Ireland | 16 | 505 | 31.56 |

| 5 | Vietnam | 18 | 415 | 23.06 |

| 6 | Lebanon | 11 | 404 | 36.73 |

| 7 | Australia | 11 | 363 | 33.00 |

| 8 | New Zealand | 14 | 316 | 22.57 |

| 9 | USA | 14 | 180 | 12.86 |

| 10 | Turkey | 17 | 163 | 9.59 |

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2022 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Almeida, J.; Gonçalves, T.C. Portfolio Diversification, Hedge and Safe-Haven Properties in Cryptocurrency Investments and Financial Economics: A Systematic Literature Review. J. Risk Financial Manag. 2023, 16, 3. https://doi.org/10.3390/jrfm16010003

Almeida J, Gonçalves TC. Portfolio Diversification, Hedge and Safe-Haven Properties in Cryptocurrency Investments and Financial Economics: A Systematic Literature Review. Journal of Risk and Financial Management. 2023; 16(1):3. https://doi.org/10.3390/jrfm16010003

Chicago/Turabian StyleAlmeida, José, and Tiago Cruz Gonçalves. 2023. "Portfolio Diversification, Hedge and Safe-Haven Properties in Cryptocurrency Investments and Financial Economics: A Systematic Literature Review" Journal of Risk and Financial Management 16, no. 1: 3. https://doi.org/10.3390/jrfm16010003

APA StyleAlmeida, J., & Gonçalves, T. C. (2023). Portfolio Diversification, Hedge and Safe-Haven Properties in Cryptocurrency Investments and Financial Economics: A Systematic Literature Review. Journal of Risk and Financial Management, 16(1), 3. https://doi.org/10.3390/jrfm16010003