From Bitcoin to Central Bank Digital Currencies: Making Sense of the Digital Money Revolution

Abstract

:1. Introduction

- How does the inception of Bitcoin and other cryptocurrencies contribute to the conceptualization of CBCDs?

- What are the common patterns underlying the central banks’ experiments, proofs-of-concept, and pilots?

- What are the main benefits and risks of introducing CBDCs?

- What issues related to CBCD are still at an early stage of formulation? For instance, how can smart contracts be used to create programmable money? What are the impacts of these features in terms of money usage and monetary policy? What can be done to improve interoperability between CBDCs, without conditioning the monetary policy tools, especially in small economies? What can be done in terms of offline payments? How does replacing a crucial part of the monetary infrastructure affect cybersecurity?

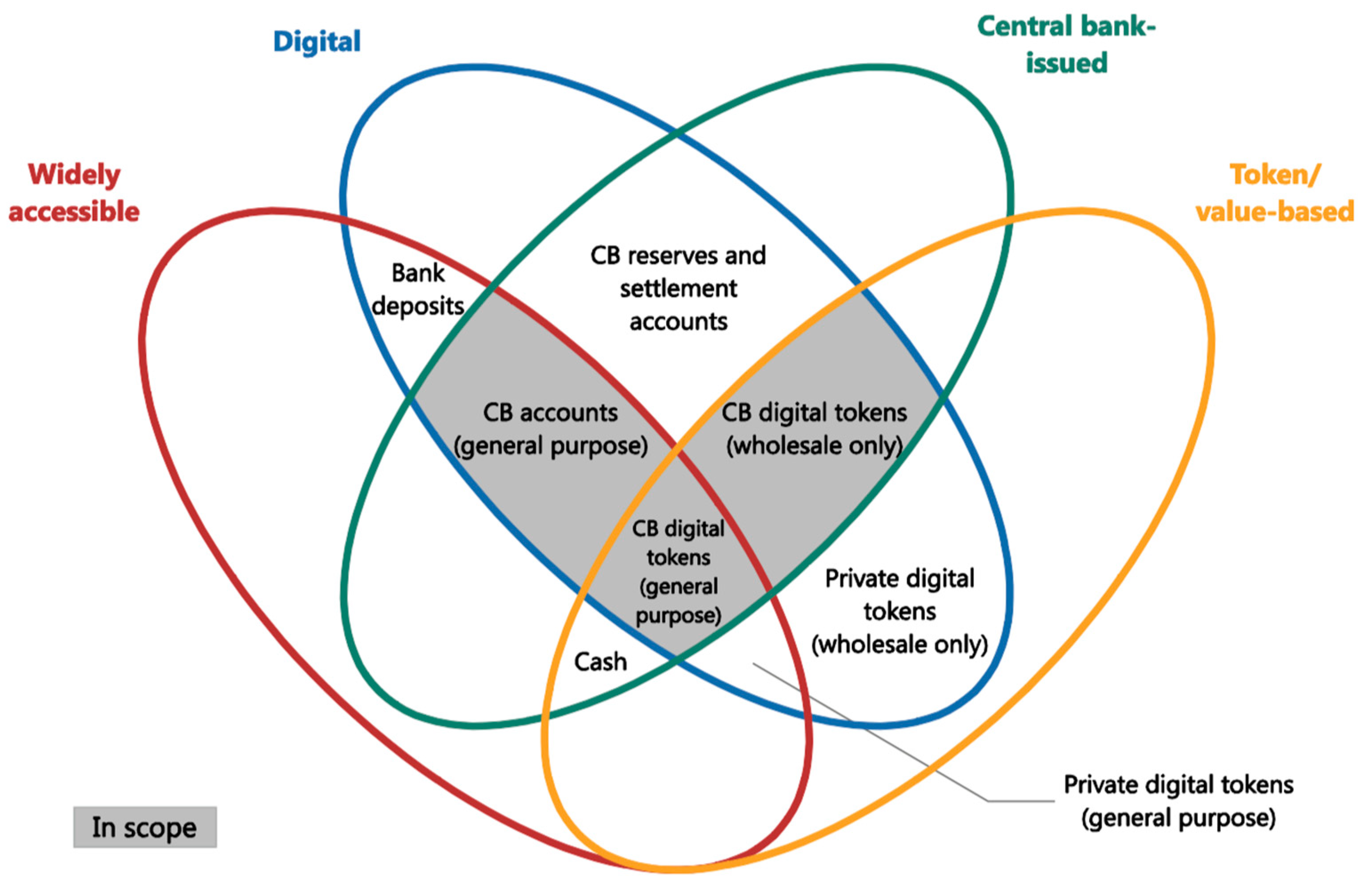

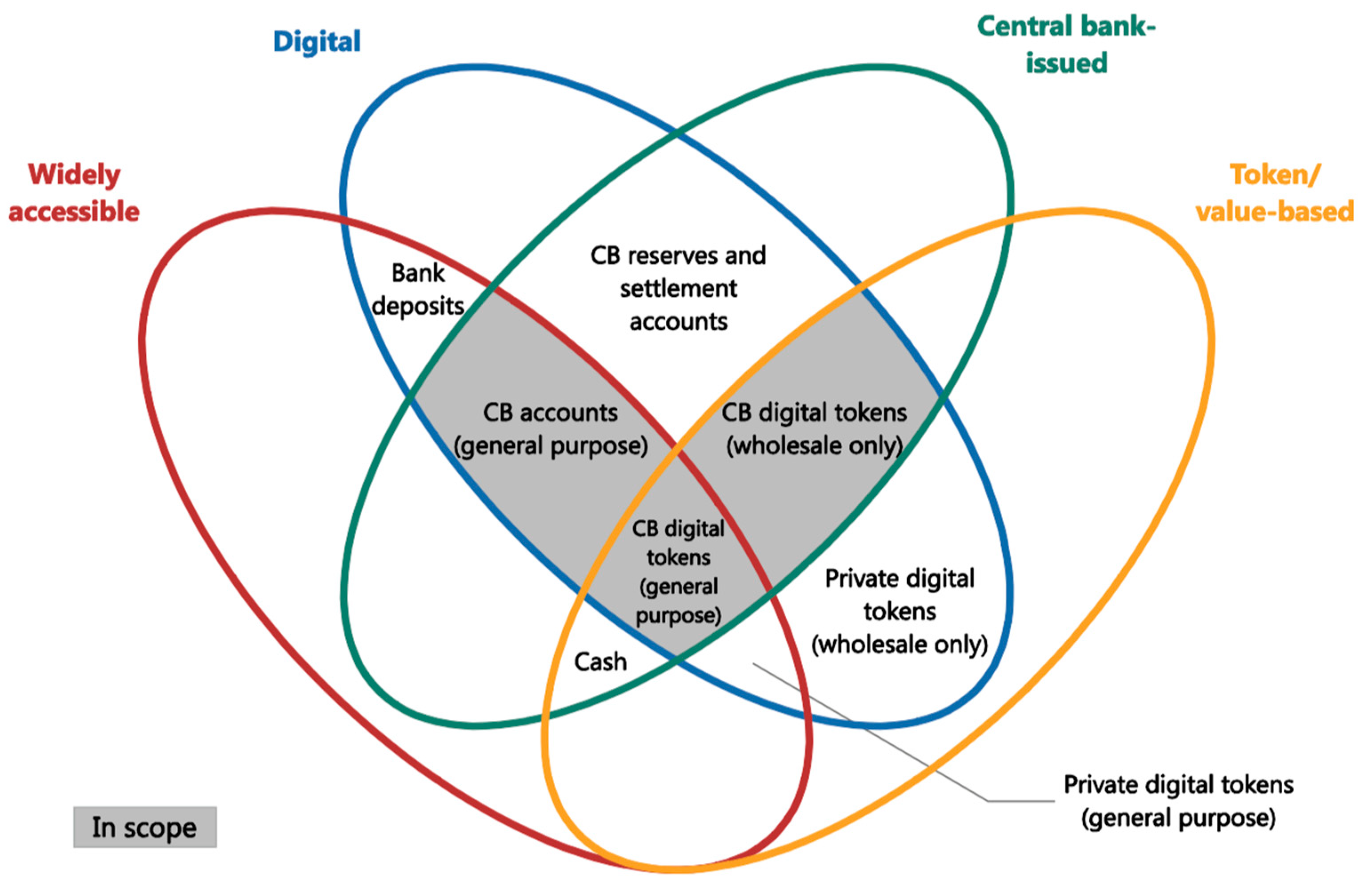

2. From Bitcoin to Central Bank Digital Currencies (CBDCs)

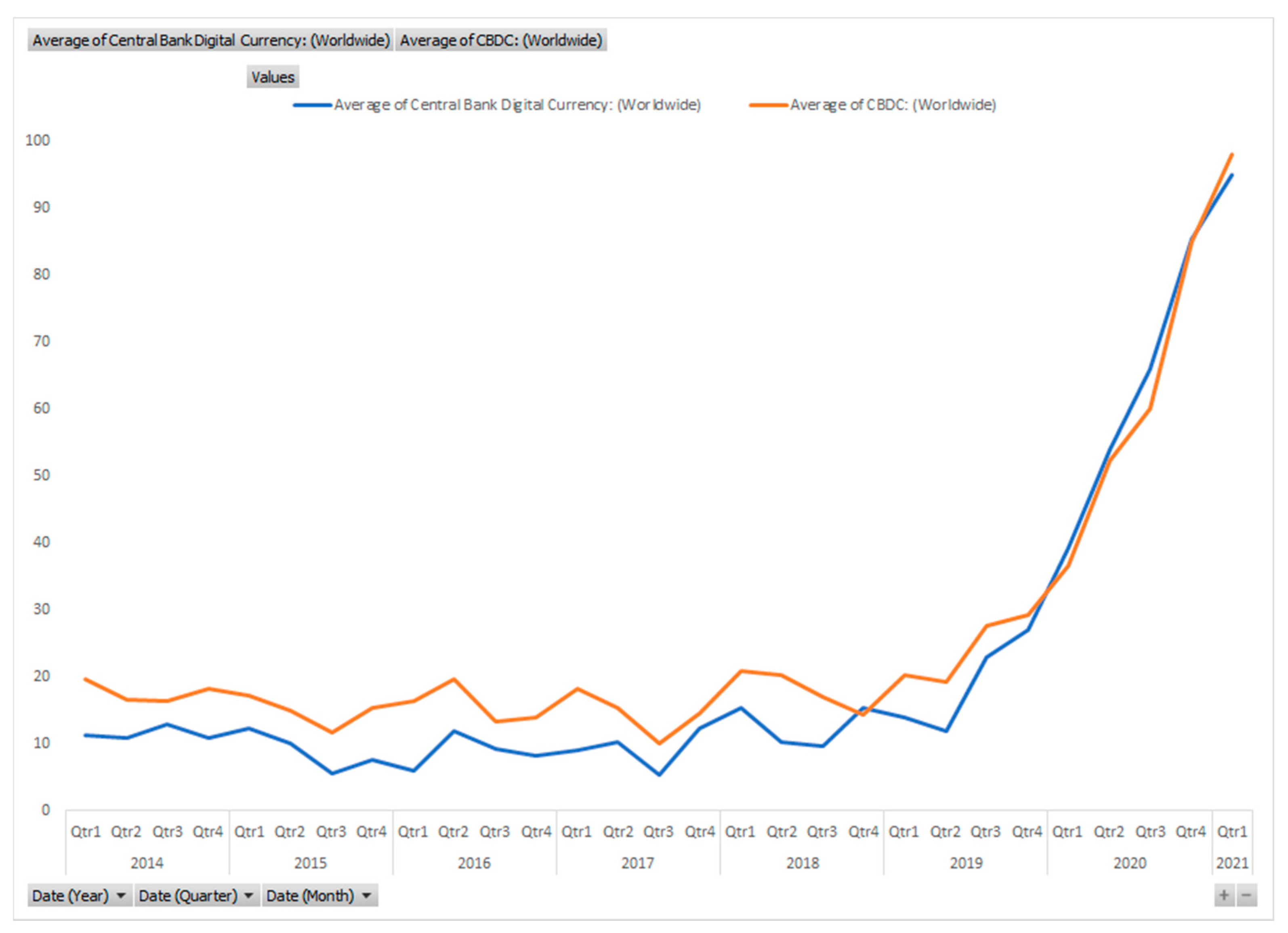

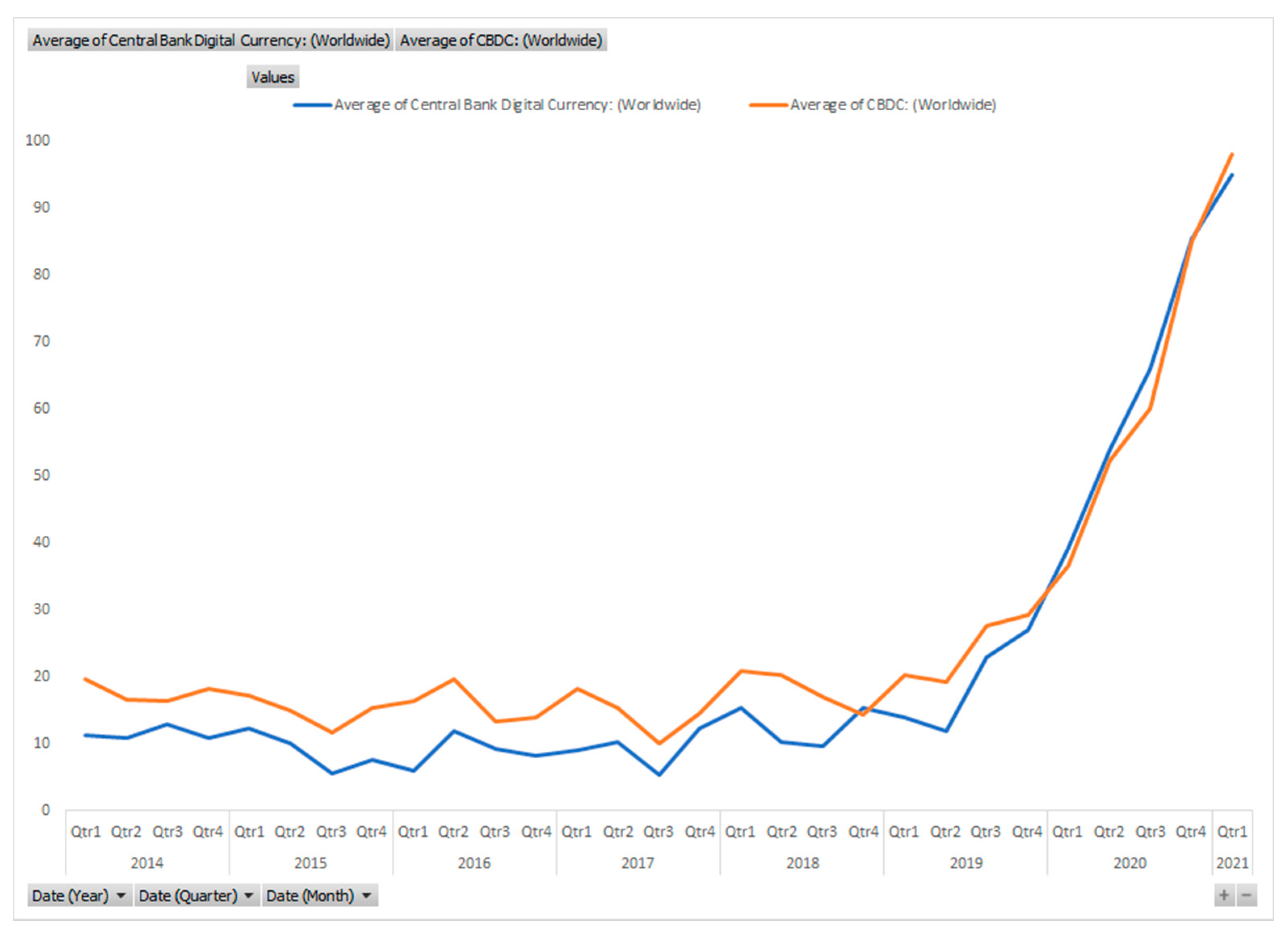

3. Experiments, Proofs-of-Concept, and Pilots

4. Benefits and Risks of CBDCs

4.1. Benefits of CBDCs

4.2. Risks of CBDCs

- The European Central Bank [91] made a proof-of-concept using time-limited “anonymity vouchers” that afford their owners the possibility of performing restricted value transactions with details not relayed to the monetary authorities. These vouchers are issued freely, but at a defined rate. Since a user is free to use or not each voucher, this limits the information regarding actual usage that the monetary authority can store.

- Project Stella [59] explored the concept of privacy-enhanced transactions (PETs) using three mechanisms, based on different technological support, to assure privacy: (a) segregating PETs, where information is segregated between participants and shared only on a “need to know” basis. Instead of a “common ledger,” there are separated “ledger subsets,” which means that parties will not have access to the full set of transactions, but only to those that include them; (b) hiding PETs, where, while there is a common ledger, various cryptographic techniques protect the stored information to prevent access from unauthorized parties; and (c) unlinking PETs, where the information present in the ledger is unlinked from the actual actors or actual transactions. Therefore, unauthorized third parties of a transaction can observe the transaction information and the amount but cannot determine the transacting relationships (i.e., that an Entity A transacted with an Entity B).

5. The Road Ahead

6. Conclusions

Author Contributions

Funding

Data Availability Statement

Conflicts of Interest

References

- Jevons, W.S. Money and the Mechanism of Exchange; D. Appleton: New York, NY, USA, 1876; Available online: https://books.google.pt/books?id=D3QqAAAAYAAJ&printsec=frontcover&source=gbs_ge_summary_r&cad=0#v=onepage&q&f=false (accessed on 25 June 2021).

- Sawyer, M. Money: Means of Payment or Store of Wealth? In Modern Theories of Money: The Nature and Role of Money in Capitalist Economies; Rochon, L.-P., Rossi, S., Eds.; Edward Elgar Publishing: Cheltenham, UK, 2003; pp. 3–17. [Google Scholar]

- Smith, A. Of the origin and use of money. In General Equilibrium Models of Monetary Economies; Starr, R.M., Ed.; Academic Press: Cambridge, MA, USA, 1989; pp. 47–53. [Google Scholar] [CrossRef]

- Humphrey, C. Barter and Economic Disintegration. Man 1985, 20, 48–72. [Google Scholar] [CrossRef]

- Hoang, P.; Ducie, M. Cambridge IGCSE and O Level Economics, 2nd ed.; Hachette: London, UK, 2018; Available online: https://books.google.pt/books?id=gRdSDwAAQBAJ (accessed on 25 June 2021).

- Menger, K. On the Origin of Money. Econ. J. 1892, 2, 239–255. [Google Scholar] [CrossRef]

- European Central Bank. Electronic Money. European Central Bank. 16 November 2016. Available online: https://www.ecb.europa.eu/stats/money_credit_banking/electronic_money/html/index.en.html (accessed on 15 May 2021).

- Ammous, S. The Bitcoin Standard: The Decentralized Alternative to Central Banking; John Wiley & Sons: Hoboken, NJ, USA, 2018. [Google Scholar]

- Barontini, C.; Holden, H. Proceeding with caution—A Survey on Central Bank Digital Currency. Bank of International Settlements, 101. January 2019. Available online: https://www.bis.org/publ/bppdf/bispap101.htm (accessed on 25 June 2021).

- Omarini, A.E. Fintech and the Future of the Payment Landscape: The Mobile Wallet Ecosystem—A Challenge for Retail Banks? Int. J. Financ. Res. 2018, 9, 97. [Google Scholar] [CrossRef]

- Ley, S.; Foottit, I.; Honig, H.; King, D.; Doyle, M.; Turan, C.; Sonnad, V. Payments Disrupted. The Emerging Challenge for European Retail Banks. Deloitte. 2015. Available online: https://www2.deloitte.com/content/dam/Deloitte/uk/Documents/financial-services/deloitte-uk-payments-disrupted-2015.pdf (accessed on 15 May 2021).

- Riksbank, S. Payments in Sweden 2019. Sveriges Riksbank. November 2019. Available online: https://www.riksbank.se/en-gb/payments--cash/payments-in-sweden/payments-in-sweden-2019/ (accessed on 25 June 2021).

- Nakamoto, S. Bitcoin: A Peer-to-Peer Electronic Cash System. 31 October 2008. Available online: https://nakamotoinstitute.org/bitcoin/ (accessed on 15 May 2021).

- CoinMarketCap: Cryptocurrency Prices, Charts and Market Capitalizations. CoinMarketCap. 5 May 2021. Available online: https://coinmarketcap.com/ (accessed on 15 May 2021).

- Sebastião, H.M.C.V.; da Cunha, P.J.O.R.; Godinho, P.M.C. Cryptocurrencies and blockchain. Overview and future perspectives. Int. J. Econ. Bus. Res 2021, 21, 305–342. [Google Scholar] [CrossRef]

- Ammous, S. Can cryptocurrencies fulfil the functions of money? Q. Rev. Econ. Financ. 2018, 70, 38–51. [Google Scholar] [CrossRef]

- Constine, J. Facebook Announces Libra Cryptocurrency: All You Need to Know. TechCrunch. 18 June 2019. Available online: https://social.techcrunch.com/2019/06/18/facebook-libra/ (accessed on 15 May 2021).

- Inman, P.; Monaghan, A. Facebook’s LIBRA Cryptocurrency Poses Risks to Global Banking. The Guardian. 23 June 2019. Available online: http://www.theguardian.com/technology/2019/jun/23/facebook-libra-cryptocurrency-poses-risks-to-global-banking (accessed on 15 May 2021).

- Tercero-Lucas, D. A Global Digital Currency to Rule Them All? A Monetary-Financial View of the Facebook’s LIBRA for the Euro Area; Univeristat Autònoma de Barcelona: Barcelona, Spain, June 2020; Available online: https://ddd.uab.cat/record/232413 (accessed on 15 June 2021).

- Inman, P. Bank of England to Consider Adopting Cryptocurrency. The Guardian. 21 January 2020. Available online: http://www.theguardian.com/technology/2020/jan/21/bank-of-england-to-consider-adopting-cryptocurrency (accessed on 15 May 2021).

- Wohlin, C. Guidelines for snowballing in systematic literature studies and a replication in software engineering. In Proceedings of the 18th International Conference on Evaluation and Assessment in Software Engineering, New York, NY, USA, 13 May 2014; pp. 1–10. [Google Scholar] [CrossRef]

- Chaum, D. Blind Signatures for Untraceable Payments. In Advances in Cryptology; Springer: Boston, MA, USA, 1983; pp. 199–203. [Google Scholar] [CrossRef]

- Schoenmakers, B. Basic security of the ecash payment system. In State of the Art in Applied Cryptography, Course on Computer Security and Industrial Cryptography; Preneel, B., Rijmen, V., Eds.; Springer: Leuven, Belgium, 1997; pp. 342–356. Available online: http://www.win.tue.nl/~berry/papers/cosic.pdf?q=ecash (accessed on 25 June 2021).

- Swan, M. Blockchain: Blueprint for a New Economy, 1st ed.; O’Reilly Media Inc.: Sebastopol, CA, USA, 2015. [Google Scholar]

- European Central Bank. Virtual Currency Schemes; European Central Bank: Frankfurt am Main, Germany, 2012. [Google Scholar]

- Hayek, F.A. Denationalisation of Money: The Argument Refined, 3rd ed.; Institute of Economic Affairs; 1990; Available online: https://mises.org/library/denationalisation-money-argument-refined (accessed on 10 May 2021).

- Phillips, D.; Chipolina, S. What Will Happen to Bitcoin After All 21 Million Are Mined? Decrypt. 20 April 2021. Available online: https://decrypt.co/33124/what-will-happen-to-bitcoin-after-all-21-million-are-mined (accessed on 15 May 2021).

- Carlsten, M.; Kalodner, H.; Weinberg, S.M.; Narayanan, A. On the Instability of Bitcoin Without the Block Reward. In Proceedings of the 2016 ACM SIGSAC Conference on Computer and Communications Security, Vienna, Austria, 24 October 2016; pp. 154–167. [Google Scholar] [CrossRef]

- Easley, D.; O’Hara, M.; Basu, S. From mining to markets: The evolution of bitcoin transaction fees. J. Financ. Econ. 2019, 134, 91–109. [Google Scholar] [CrossRef]

- Ali, R.; Barrdear, J.; Clews, R.; Southgate, J. The Economics of Digital Currencies. Bank of England. 2014 Q3. September 2014. Available online: https://papers.ssrn.com/abstract=2499418 (accessed on 15 May 2021).

- Baur, D.G.; Dimpfl, T. The volatility of Bitcoin and its role as a medium of exchange and a store of value. Empir. Econ. 2021. [Google Scholar] [CrossRef] [PubMed]

- Yermack, D. Is Bitcoin a Real Currency? An Economic Appraisal. In Handbook of Digital Currency; Chuen, D.L.K., Ed.; Academic Press: San Diego, CA, USA, 2015; pp. 31–43. [Google Scholar] [CrossRef]

- Bação, P.; Duarte, A.P.; Sebastião, H.; Redzepagic, S. Information Transmission between Cryptocurrencies: Does Bitcoin Rule the Cryptocurrency World? Sci. Ann. Econ. Bus. 2018, 65, 97–117. [Google Scholar] [CrossRef]

- Hazlett, P.K.; Luther, W.J. Is bitcoin money? And what that means. Q. Rev. Econ. Financ. 2020, 77, 144–149. [Google Scholar] [CrossRef]

- Tesla, Inc. Annual Report on form 10-K for the Year Ended 31 December 2020. United States—Securities and Exchange Commission; 8 February 2021. Available online: https://www.sec.gov/ix?doc=/Archives/edgar/data/1318605/000156459021004599/tsla-10k_20201231.htm (accessed on 15 May 2021).

- Lambert, F. Tesla Explains How Dumb It Is to Buy a Car with Bitcoin in Its Own Disclosure. Electrek. 24 March 2021. Available online: https://electrek.co/2021/03/24/tesla-dumb-buy-car-with-bitcoin/ (accessed on 15 May 2021).

- Kolodny, L. Elon Musk Says Tesla Will Stop Accepting Bitcoin for Car Purchases, Citing Environmental Concerns. CNBC. 12 May 2021. Available online: https://www.cnbc.com/2021/05/12/elon-musk-says-tesla-will-stop-accepting-bitcoin-for-car-purchases.html (accessed on 15 May 2021).

- Kharpal, A. As Much as $365 Billion Wiped off Cryptocurrency Market after Tesla Stops Car Purchases with Bitcoin; NBC News: London, UK, 13 May 2021; Available online: https://www.nbcnews.com/tech/tech-news/365-billion-wiped-cryptocurrency-market-musks-tweet-rcna922 (accessed on 15 May 2021).

- Dion-Schwarz, C.; Manheim, D.; Johnston, P. Terrorist Use of Cryptocurrencies: Technical and Organizational Barriers and Future Threats; RAND Corporation: Santa Monica, CA, USA, 2019. [Google Scholar] [CrossRef]

- Hurlburt, G.F.; Bojanova, I. Bitcoin: Benefit or Curse? IT Prof. 2014, 16, 10–15. [Google Scholar] [CrossRef]

- Bryans, D. Bitcoin and Money Laundering: Mining for an Effective Solution. Indiana Law J. 2014, 89, 13. [Google Scholar]

- Foley, S.; Karlsen, J.R.; Putniņš, T.J. Sex, Drugs, and Bitcoin: How Much Illegal Activity Is Financed through Cryptocurrencies? Rev. Financ. Stud. 2019, 32, 1798–1853. [Google Scholar] [CrossRef]

- CPMI-MC. Central Bank Digital Currencies. Bank of International Settlements, 174. March 2018. Available online: https://www.bis.org/cpmi/publ/d174.htm (accessed on 10 May 2021).

- Groß, J.; Herz, B.; Schiller, J. Libra—Concept and Policy Implications. Wirtschaftswissenschaftliche Diskussionspapiere, Working Paper 02–19. 2019. Available online: https://www.econstor.eu/handle/10419/205241 (accessed on 15 May 2021).

- Brühl, V. Libra—A Differentiated View on Facebook’s Virtual Currency Project. Intereconomics 2020, 55, 54–61. [Google Scholar] [CrossRef] [Green Version]

- Schmeling, M. What is Libra? Understanding Facebook’s Currency. Goethe University Frankfurt, SAFE—Sustainable Architecture for Finance in Europe, Research Report 76. 2019. Available online: https://www.econstor.eu/handle/10419/204501 (accessed on 15 May 2021).

- Abraham, L.; Guégan, D. The other side of the Coin: Risks of the Libra Blockchain. arXiv 2020, arXiv:191007775. [Google Scholar] [CrossRef] [Green Version]

- Bursztynsky, J. Facebook-backed Libra Association Has Been Renamed DIEM. CNBC. 1 December 2020. Available online: https://www.cnbc.com/2020/12/01/facebook-backed-libra-digital-currency-has-been-renamed-diem.html (accessed on 15 May 2021).

- Panetta, F. 21st century cash: Central banking, technological innovation and digital currencies. In Do We Need Central Bank Digital Currency? Economics, Technology and Institutions; Milan, Italy, June 2018; pp. 28–31. Available online: https://www.suerf.org/studies/7025/do-we-need-central-bank-digital-currency-economics-technology-and-institutions (accessed on 17 June 2021).

- Alonso, S.L.N.; Fernández, M.Á.E.; Bas, D.S.; Kaczmarek, J. Reasons Fostering or Discouraging the Implementation of Central Bank-Backed Digital Currency: A Review. Economies 2020, 8, 41. [Google Scholar] [CrossRef]

- Bech, M.L.; Garratt, R. Central Bank Cryptocurrencies; Bank of International Settlements: Rochester, NY, USA, September 2017; Available online: https://papers.ssrn.com/abstract=3041906 (accessed on 15 May 2021).

- Tobin, J. Financial Innovation and Deregulation in Perspective. Bank Jpn. Monet. Econ. Stud. 1985, 3, 19–29. [Google Scholar]

- Tobin, J. A Case for Preserving Regulatory Distinctions. Challenge 1987, 30, 10–17. [Google Scholar] [CrossRef] [Green Version]

- Bank of England. Central Bank Digital Currency: Opportunities, Challenges and Design. Bank of England, Discussion Paper. March 2020. Available online: https://www.bankofengland.co.uk/-/media/boe/files/paper/2020/central-bank-digital-currency-opportunities-challenges-and-design.pdf?la=en&hash=DFAD18646A77C00772AF1C5B18E63E71F68E4593 (accessed on 25 June 2021).

- Alun, J. Explainer: How Does China’s Digital Yuan Work? Reuters. 19 October 2020. Available online: https://www.reuters.com/article/us-china-currency-digital-explainer-idUSKBN27411T (accessed on 28 April 2021).

- Auer, R.; Cornelli, G.; Frost, J. Rise of the Central Bank Digital Currencies: Drivers, Approaches and Technologies. Bank of International Settlements, 880. August 2020. Available online: https://www.bis.org/publ/work880.htm (accessed on 22 March 2021).

- Boar, C.; Holden, H.; Wadsworth, A. Impending Arrival—A Sequel to the Survey on Central Bank Digital Currency. Bank of International Settlements, 107. January 2020. Available online: https://www.bis.org/publ/bppdf/bispap107.htm (accessed on 25 June 2021).

- Pocher, N.; Veneris, A. Privacy and Transparency in CBDCs: A Regulation-by-Design AML/CFT Scheme. SSRN Electron. J. 2021. [Google Scholar] [CrossRef]

- Bank of Japan and European Central Bank. Balancing Confidentiality and Auditability in a Distributed Ledger Environment. BoJ & ECB, Project Stella Report Phase 4. February 2020. Available online: https://www.boj.or.jp/en/announcements/release_2020/data/rel200212a1.pdf (accessed on 1 May 2021).

- Da Cunha, P.J.O.R.; Soja, P.; Themistocleous, M. Blockchain for development: A guiding framework. Inf. Technol. Dev. 2021, 27. [Google Scholar] [CrossRef]

- Areddy, J.T. China Creates Its Own Digital Currency, a First for Major Economy. Wall Street Journal. 5 April 2021. Available online: https://www.wsj.com/articles/china-creates-its-own-digital-currency-a-first-for-major-economy-11617634118 (accessed on 28 April 2021).

- Popper, N.; Li, C. China Charges Ahead with a National Digital Currency. The New York Times. 1 March 2021. Available online: https://www.nytimes.com/2021/03/01/technology/china-national-digital-currency.html (accessed on 13 May 2021).

- McNally, C.A. The DCEP: Developing the Globe’s First Major Central Bank Digital Currency. China-US Focus. 28 December 2020. Available online: https://www.chinausfocus.com/finance-economy/the-dcep-developing-the-globes-first-major-central-bank-digital-currency (accessed on 28 April 2021).

- Eastern Caribbean Central Bank. Public Roll-Out of the Eastern Caribbean Central Bank’s Digital Currency—DCash! Eastern Caribbean Central Bank. 25 March 2021. Available online: https://www.eccb-centralbank.org/news/view/public-roll-out-of-the-eastern-caribbean-central-bankas-digital-currency-a-dcash (accessed on 1 May 2021).

- Boar, C.; Wehrli, A. Ready, Steady, Go?—Results of the Third BIS Survey on Central Bank Digital Currency. Bank of International Settlements, 114. January 2021. Available online: https://www.bis.org/publ/bppdf/bispap114.htm (accessed on 22 May 2021).

- Google Trends. 2021. Available online: https://trends.google.com/trends/explore?date=2014-01-01%202021-04-01&q=CBDC,%2Fg%2F11g9svs5sb (accessed on 2 May 2021).

- Auer, R.; Boehme, R. The Technology of Retail Central Bank Digital Currency. Bank of International Settlements. March 2020. Available online: https://www.bis.org/publ/qtrpdf/r_qt2003j.htm (accessed on 22 March 2021).

- HLTF-CBDC. Report on a Digital Euro. European Central Bank, High-Level Task Force on Central Bank Digital Currency. October 2020. Available online: https://www.ecb.europa.eu/pub/pdf/other/Report_on_a_digital_euro~4d7268b458.en.pdf (accessed on 25 June 2021).

- Kiff, J.; Alwazir, J.; Davidovic, S.; Farias, A.; Khan, A.; Khiaonarong, T.; Malaika, M.; Monroe, H.; Sugimoto, N.; Tourpe, H.; et al. A Survey of Research on Retail Central Bank Digital Currency; International Monetary Fund: Rochester, NY, USA, July 2020; SSRN Scholarly Paper ID 3639760. [Google Scholar] [CrossRef]

- Kahn, C.M.; Roberds, W. Why pay? An introduction to payments economics. J. Financ. Intermed. 2009, 18, 1–23. [Google Scholar] [CrossRef]

- Bank of England. New Forms of Digital Money. Bank of England, Discussion Paper. June 2021. Available online: http://www.bankofengland.co.uk/paper/2021/new-forms-of-digital-money (accessed on 17 June 2021).

- Choi, K.J.; Henry, R.; Lehar, A.; Reardon, J.; Safavi-Naini, R. A Proposal for a Canadian CBDC; Social Science Research Network: Rochester, NY, USA, February 2021; SSRN Scholarly Paper ID 3786426. [Google Scholar] [CrossRef]

- Alonso, S.L.N.; Jorge-Vazquez, J.; Forradellas, R.F.R. Central Banks Digital Currency: Detection of Optimal Countries for the Implementation of a CBDC and the Implication for Payment Industry Open Innovation. J. Open Innov. Technol. Mark. Complex. 2021, 7, 72. [Google Scholar] [CrossRef]

- Bordo, M.D.; Levin, A.T. Central Bank Digital Currency and the Future of Monetary Policy; National Bureau of Economic Research: Cambridge, MA, USA, August 2017; p. w23711. [Google Scholar] [CrossRef]

- Mersch, Y. Why Europe Still Needs Cash. Project Syndicate. 28 April 2017. Available online: https://www.ecb.europa.eu/press/key/date/2017/html/ecb.sp170428.en.html (accessed on 11 May 2021).

- Huang, X. China’s DCEP project launches biggest digital yuan test yet. Forkast. 3 March 2021. Available online: https://forkast.news/china-dcep-digital-yuan-pros-cons/ (accessed on 11 May 2021).

- Sveriges Riksbank. E-Krona Project, Report 1. Report 1. September 2017. Available online: https://www.riksbank.se/en-gb/payments--cash/e-krona/e-krona-reports/e-krona-project-report-1/ (accessed on 15 May 2021).

- Office on Drugs and Crime. Money Laundering. United Nations: Office on Drugs and Crime. 2021. Available online: http://www.unodc.org/unodc/en/money-laundering/overview.html (accessed on 21 April 2021).

- Dupuis, D.; Gleason, K.; Wang, Z. Money laundering in a CBDC World: A Game of Cats and Mice. SSRN Electron. J. 2021. [Google Scholar] [CrossRef]

- Bijlsma, M.; van der Cruijsen, C.; Jonker, N.; Reijerink, J. What Triggers Consumer Adoption of CBDC? De Nederlandsche Bank: Rochester, NY, USA, April 2021; Working Paper 709. [Google Scholar] [CrossRef]

- Scher, I. 14 Million American Adults Don’t Have a Bank Account. They’re Still Waiting for a Stimulus Payment. Business Insider. 5 May 2020. Available online: https://www.businessinsider.com/coronavirus-stimulus-check-payment-no-bank-account-waiting-2020-5 (accessed on 15 May 2021).

- Alonso, S.L.N.; Jorge-Vazquez, J.; Forradellas, R.F.R. Detection of Financial Inclusion Vulnerable Rural Areas through an Access to Cash Index: Solutions Based on the Pharmacy Network and a CBDC. Evidence Based on Ávila (Spain). Sustainability 2020, 12, 7480. [Google Scholar] [CrossRef]

- Barrdear, J.; Kumhof, M. The Macroeconomics of Central Bank Issued Digital Currencies. BoE Staff Work. Pap. 2016, 605. [Google Scholar] [CrossRef]

- Davoodalhosseini, M. Central Bank Digital Currency and Monetary Policy. Bank of Canada, 2018–36. July 2018. Available online: https://www.bankofcanada.ca/2018/07/staff-working-paper-2018-36/ (accessed on 18 May 2021).

- Raskin, M.; Yermack, D. Digital currencies, decentralized ledgers and the future of central banking. In Research Handbook on Central Banking; Conti-Brown, P., Lastra, R.M., Eds.; Edward Elgar Publishing: Amsterdam, The Netherlands, 2018; pp. 476–486. Available online: https://www.elgaronline.com/view/edcoll/9781784719210/9781784719210.00028.xml (accessed on 18 May 2021).

- Thakor, A.V. Fintech and banking: What do we know? J. Financ. Intermed. 2020, 41, 100833. [Google Scholar] [CrossRef]

- Niepelt, D. Reserves for All? Central Bank Digital Currency, Deposits, and Their (Non)-Equivalence. Int. J. Cent. Bank. 2020, 62. Available online: https://www.ijcb.org/journal/ijcb20q2a6.htm (accessed on 18 May 2021).

- Tolle, M. Central Bank Digital Currency: The End of Monetary Policy as We Know It? Bank Underground. 25 July 2016. Available online: https://bankunderground.co.uk/2016/07/25/central-bank-digital-currency-the-end-of-monetary-policy-as-we-know-it/ (accessed on 30 April 2021).

- Sanchez-Roger, M.; Puyol-Antón, E. Digital Bank Runs: A Deep Neural Network Approach. Sustainability 2021, 13, 1513. [Google Scholar] [CrossRef]

- Hustinx, P. Privacy by design: Delivering the Promises. Identity Inf. Soc. 2010, 3, 253–255. [Google Scholar] [CrossRef] [Green Version]

- European Central Bank. In Focus—Exploring Anonymity in Central Bank Digital Currencies. European Central Bank, 4/2019. December 2019. Available online: https://www.ecb.europa.eu/paym/intro/publications/pdf/ecb.mipinfocus191217.en.pdf (accessed on 30 April 2021).

- Auer, R.; Boehme, R. Central Bank Digital Currency: The Quest for Minimally Invasive Technology. Bank of International Settlements, BIS Working Papers 948. June 2021. Available online: https://www.bis.org/publ/work948.htm (accessed on 17 June 2021).

- Directive (EU) 2015/2366 of the European Parliament and of the Council of 25 November 2015 on Payment Services in the Internal Market, Amending Directives 2002/65/EC, 2009/110/EC and 2013/36/EU and Regulation (EU) No 1093/2010, and Repealing Directive 2007/64/EC (Text with EEA Relevance); Volume OJ L; 2015; Available online: http://data.europa.eu/eli/dir/2015/2366/oj/eng (accessed on 21 April 2021).

- McCaleb, J.; Lin, L.; Lund, J. Programmable money: Will central banks take the lead? IBM Institute for Business Value. February 2018. Available online: https://www.ibm.com/downloads/cas/WVJNWYO4 (accessed on 15 May 2021).

- Bechtel, A.; Gross, J.; Sandner, P.; von Wachter, V. Programmable Money and Programmable Payments. Medium. 29 September 2020. Available online: https://jonasgross.medium.com/programmable-money-and-programmable-payments-c0f06bbcd569 (accessed on 15 May 2021).

- Lewis, A. What Actually is Programmable Money? LinkedIn. 26 April 2020. Available online: https://www.linkedin.com/pulse/what-actually-programmable-money-antony-lewis/ (accessed on 15 May 2021).

- Lund, J.; McCaleb, J.; Kennedy, M.; Drury, N. Charting the evolution of programmable money. IBM Institute for Business Value. March 2019. Available online: https://www.ibm.com/thought-leadership/institute-business-value/report/programmoneyevo (accessed on 15 May 2021).

- Auer, R.; Haene, P.; Holden, H. Multi-CBDC Arrangements and the Future of Cross-Border Payments. Bank of International Settlements, 115. March 2021. Available online: https://www.bis.org/publ/bppdf/bispap115.htm (accessed on 25 June 2021).

- Lim, M. 4 Central Banks and BIS Exploring CBDC Bridge for Asia and Middle East. Forkast. 25 February 2021. Available online: https://forkast.news/central-banks-bis-cbdc-bridge-asia-middle-east/ (accessed on 11 May 2021).

- Obstfeld, M.; Shambaugh, J.C.; Taylor, A.M. The Trilemma in History: Tradeoffs Among Exchange Rates, Monetary Policies, and Capital Mobility. Rev. Econ. Stat. 2005, 87, 423–438. [Google Scholar] [CrossRef]

- Christodorescu, M.; Gu, W.C.; Kumaresan, R.; Minaei, M.; Ozdayi, M.; Price, B.; Raghuraman, S.; Saad, M.; Sheffield, C.; Xu, M.; et al. Towards a Two-Tier Hierarchical Infrastructure: An Offline Payment System for Central Bank Digital Currencies. arXiv 2020, arXiv:201208003. [Google Scholar]

- Sheffield, C. Central Bank Digital Currency and the Future: Visa Publishes New Research. VISA Blog. 17 December 2020. Available online: https://usa.visa.com/visa-everywhere/blog/bdp/2020/12/17/central-bank-digital-1608165518834.html (accessed on 15 May 2021).

- Phillips, T. Chinese Banks Unveil CBDC Hardware Prototypes for Multiple Use Cases. NFC World. 4 May 2021. Available online: https://www.nfcw.com/2021/05/04/371992/chinese-banks-unveil-cbdc-hardware-prototypes-for-multiple-use-cases/ (accessed on 6 May 2021).

- Irrera, A. PayPal Launches Crypto Checkout Service. Reuters. 30 March 2021. Available online: https://www.reuters.com/article/us-crypto-currency-paypal-exclusive-idUSKBN2BM10N (accessed on 15 May 2021).

- Harper, C. Visa Settles USDC Transaction on Ethereum, Plans Rollout to Partners. CoinDesk. 29 March 2021. Available online: https://www.coindesk.com/visa-uses-anchorage-to-settle-usdc-transaction-on-ethereum-in-further-crypto-push (accessed on 15 May 2021).

- Le, K. New China digital yuan wallet with fingerprint ID raises privacy worries. Forkast. 12 May 2021. Available online: https://forkast.news/chinas-new-digital-yuan-wallet-with-fingerprint-id-causes-privacy-worries/ (accessed on 18 May 2021).

- Ahya, C.; Kam, D.; Richers, J.; Stanley, M. Digital Disruption: The Inevitable Rise of CBDC. SUERF, SUERF Policy Note 241. May 2021. Available online: https://www.suerf.org/docx/f_86a9d09856a0f9f7a762ddce0af753ce_25525_suerf.pdf (accessed on 25 June 2021).

- Panetta, F. A Digital Euro to Meet the Expectations of EUROPEANS. SUERF, SUERF Policy Brief 95. May 2021. Available online: https://www.suerf.org/docx/f_51b68f5195a2b629640c55358cd4a7f5_25599_suerf.pdf (accessed on 25 June 2021).

{kind=link}

{kind=link}

| Feature | Bitcoin | Fiat Money |

|---|---|---|

| Issuance | Decentralized, regulated by underlying algorithm | Centralized, regulated by central bank mandates |

| Supply | Capped at 21 million units | No hard cap |

| Liability | Not the liability of anyone | Liability of the central bank or commercial banks |

| Liquidity | Not guaranteed | Absolute |

| Stability | Volatile | Stable, except in face of hyperinflation |

| Acceptability as medium of payment | Limited | Universal in a given economy |

| Privacy of user identity | Pseudonymous, no link between addresses and natural persons | Anonymous if cash is used, Know Your Customer (KYC) enforced for accounts in commercial banks |

| Confidentiality of transactions | Ledger is public | Restricted to parties, visible to financial institutions, accessible to law enforcement |

| Geographical scope | Global | Limited |

| Characteristic | Alternatives | Description |

|---|---|---|

| Application Area [43,51] | Wholesale | The currency is intended only for financial institutions which hold accounts in the central bank |

| Retail | The currency is intended for use by the general public | |

| Architecture [56]—related to Operating Model [69], Access Model [68] | Direct CBDC | CDBC is a claim on the central bank; onboarding is performed by either central bank or intermediaries (respecting KYC regulations); all payments handled by central bank |

| Indirect/Synthetic CBDC | CBDC is a claim on an intermediary, onboarding is performed by intermediaries (respecting KYC regulations); retail payments are handled by intermediaries, wholesale payments handled by the central bank | |

| Hybrid CBDC | CDBC is a claim on the central bank; onboarding is performed by intermediaries (respecting KYC regulations); retail payments are handled by intermediaries, but the central bank periodically records all retail balances and operates a backup technical infrastructure allowing it to restart the payment system if intermediaries fail | |

| Intermediated CBDC | Like Hybrid CDBC, but the central bank maintains only a wholesale ledger, rather than all transactions | |

| Access Technology [67] based on ideas from [70] | Account-based access | The value is linked to an account, with ownership tied to identity; no privacy by default |

| Token-based access | The value is linked to demonstrated knowledge, like a digital signature, eventually stored in a hardware device; provides privacy by default | |

| Central Bank Infrastructure [67] | Conventional | The transactions are stored in a logically centralized ledger; the actual storage may be distributed, but the control over the information is centralized |

| Distributed ledger technologies (DLT)-based | The transactions are stored in a logically distributed ledger; the control over information must be harmonized with a consensus mechanism; may make use of Blockchain technology (like R3 Corda or Quorum) | |

| Interlinkages [67] | National | Access is reserved to residents of a particular monetary |

| International | Accessible to non-residents, allowing for cross-border retail payments; this is allowed by default if the access is token-based | |

| Authority [69], maps partially with Infrastructure [67] and Access Technology [67] | Centralized | Only the central bank can verify and commit transactions |

| Partially Decentralized | The central bank provides tokens to selected financial institutions to either safeguard or act as intermediaries | |

| Decentralized | The ledger is run on a DLT, allowing for decentralized transaction verification and commit | |

| Availability and Limitations [69] and Restrictions on Access [68] | Unlimited usage | While theoretically possible, it may conflict with particular central bank goals due to effects on the banking sector, monetary policy, and financial stability |

| Geographical limits | Only accessible to current residents of a monetary area | |

| Value limits | Maximum limits on the amount that can be stored in a particular account or instrument |

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2021 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Cunha, P.R.; Melo, P.; Sebastião, H. From Bitcoin to Central Bank Digital Currencies: Making Sense of the Digital Money Revolution. Future Internet 2021, 13, 165. https://doi.org/10.3390/fi13070165

Cunha PR, Melo P, Sebastião H. From Bitcoin to Central Bank Digital Currencies: Making Sense of the Digital Money Revolution. Future Internet. 2021; 13(7):165. https://doi.org/10.3390/fi13070165

Chicago/Turabian StyleCunha, Paulo Rupino, Paulo Melo, and Helder Sebastião. 2021. "From Bitcoin to Central Bank Digital Currencies: Making Sense of the Digital Money Revolution" Future Internet 13, no. 7: 165. https://doi.org/10.3390/fi13070165

APA StyleCunha, P. R., Melo, P., & Sebastião, H. (2021). From Bitcoin to Central Bank Digital Currencies: Making Sense of the Digital Money Revolution. Future Internet, 13(7), 165. https://doi.org/10.3390/fi13070165