Tradeoffs in Timber, Carbon, and Cash Flow under Alternative Management Systems for Douglas-Fir in the Pacific Northwest

Abstract

1. Introduction

1.1. The Productivity and Management of Coastal Douglas-Fir Forests

1.2. Policy Interest in Forest Sector Engagement in Climate Change Mitigation and Adaptation

1.3. Interest in the Carbon Footprint of Wood, and the Central Role Certification Has Come to Play

1.4. Research Objectives and Working Hypotheses

2. Materials and Methods

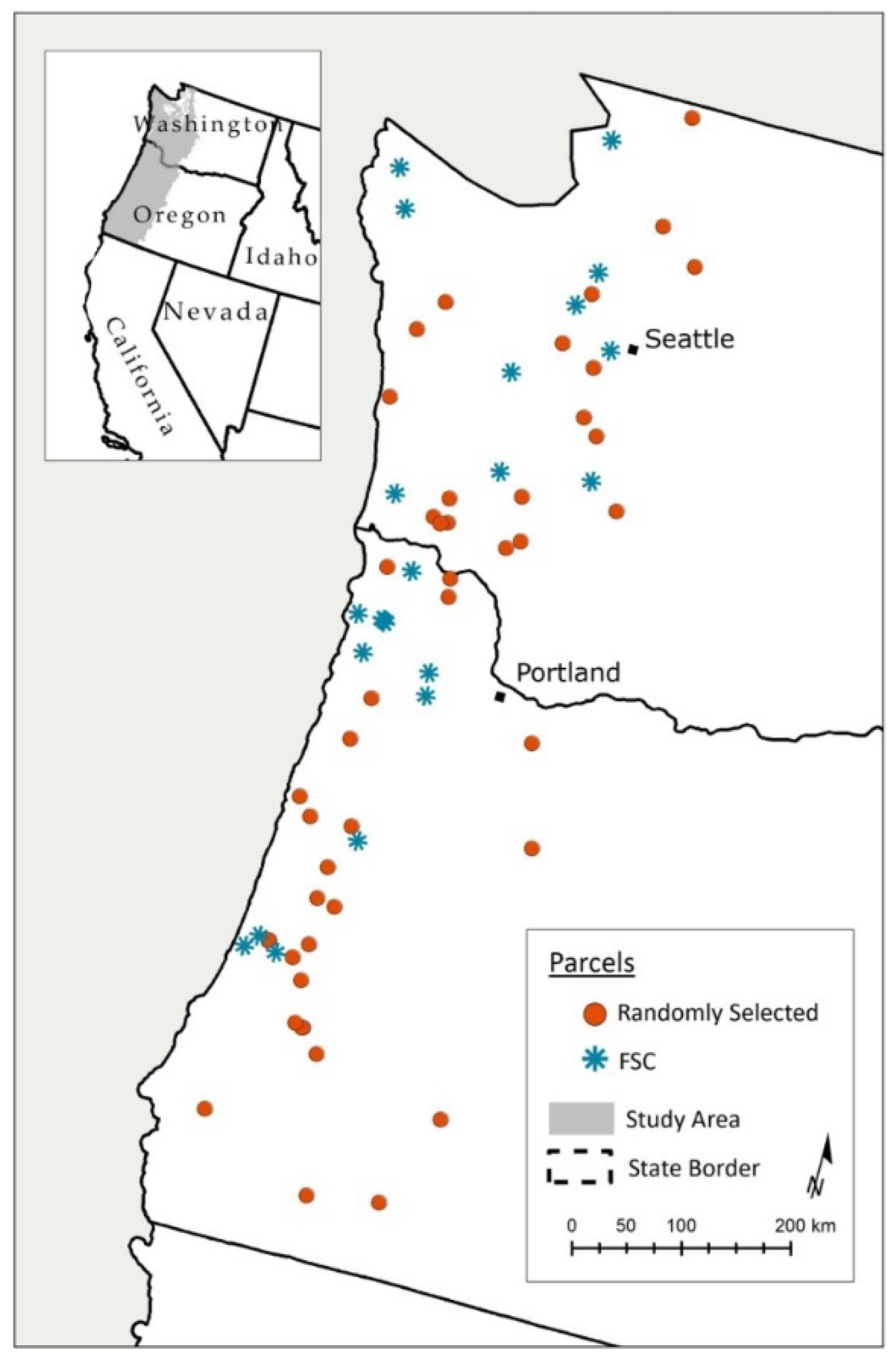

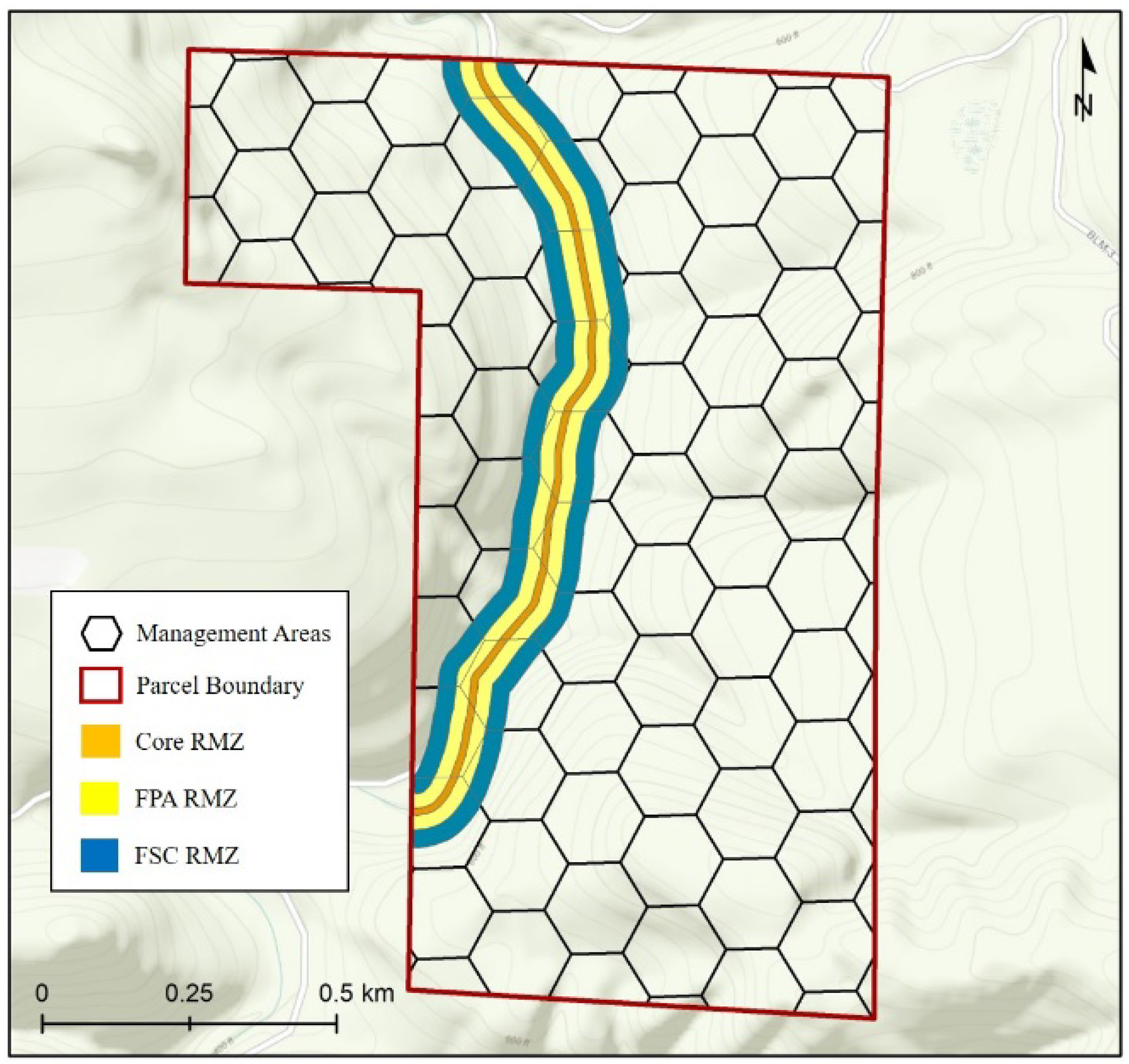

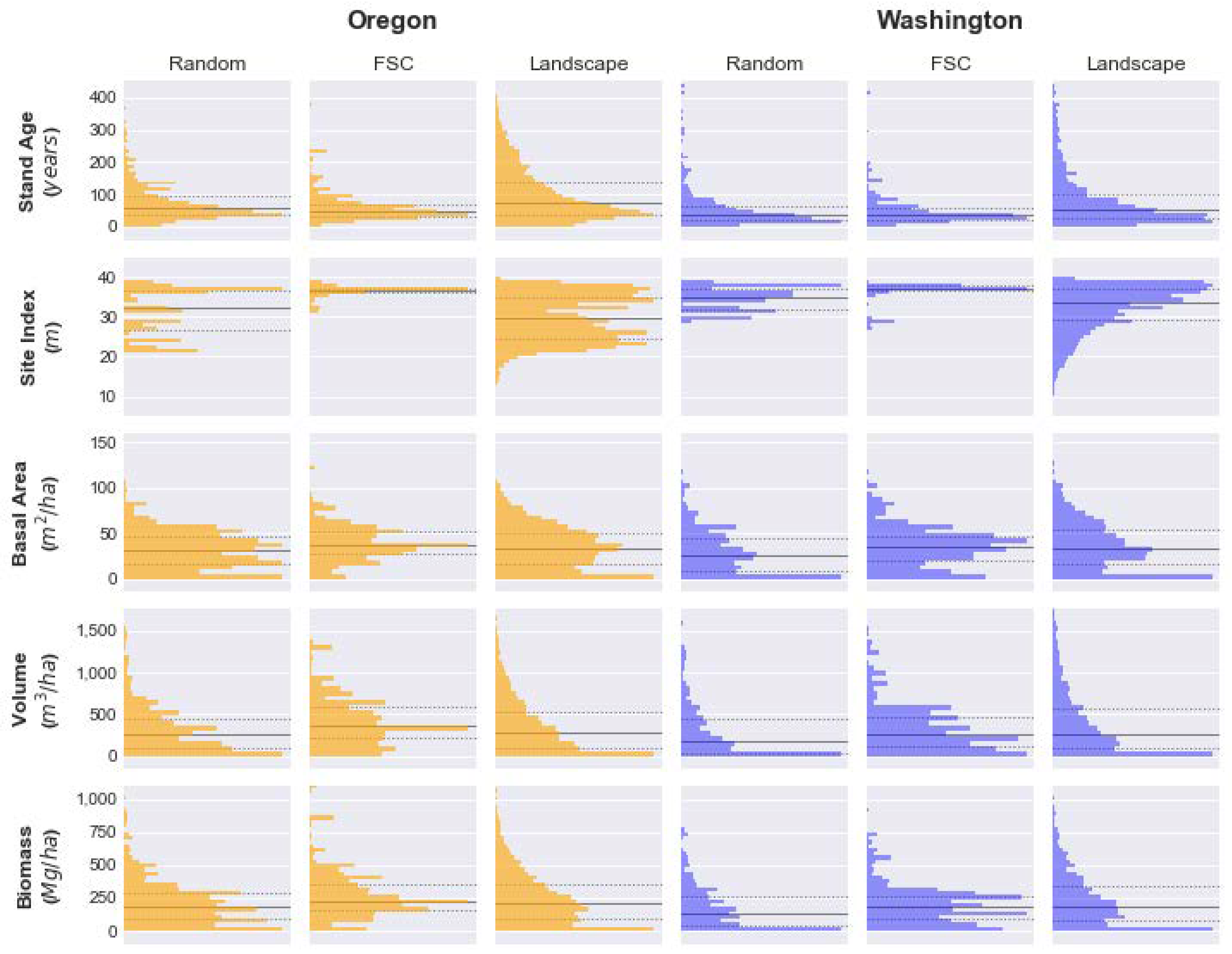

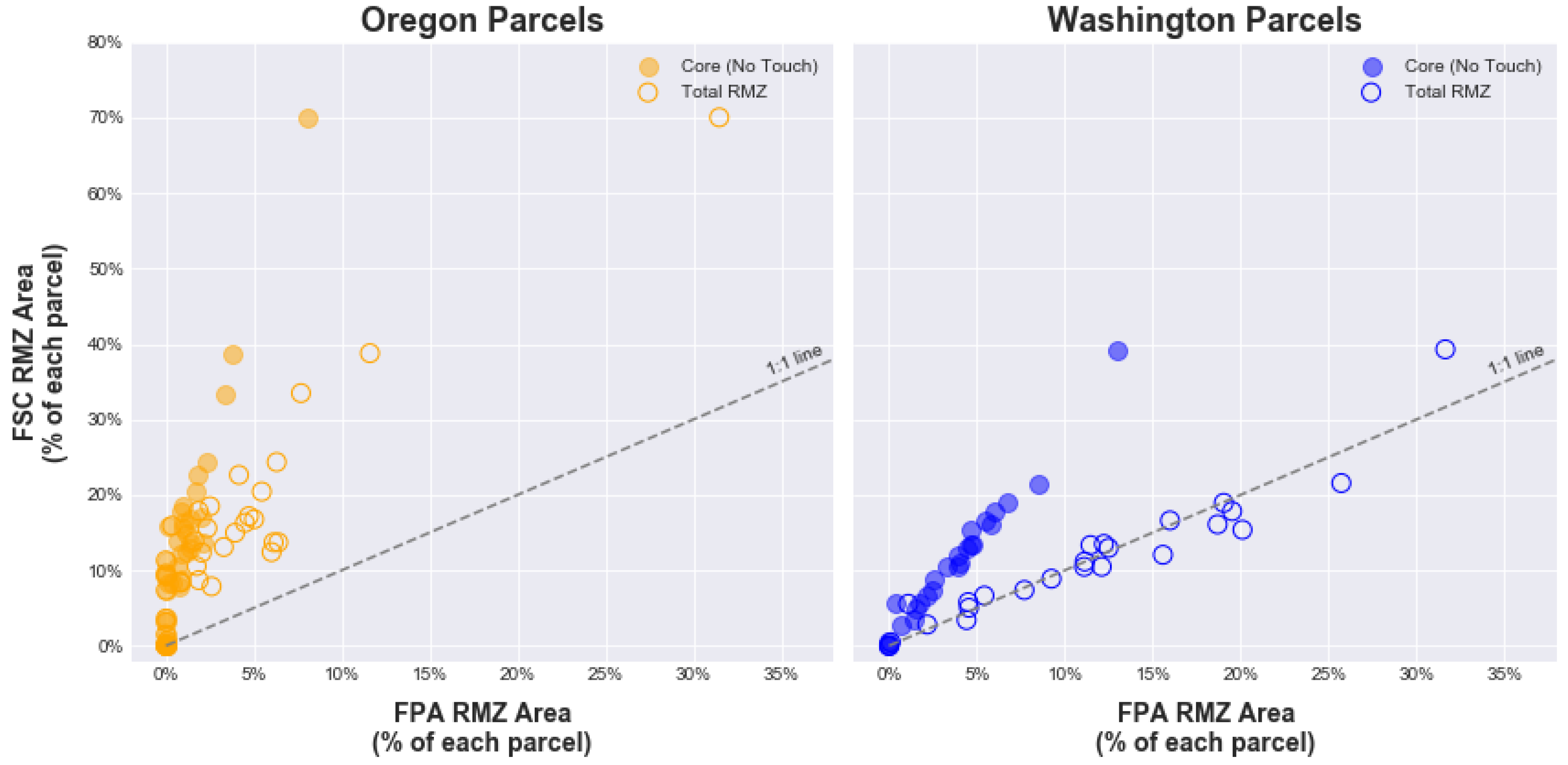

2.1. Initial Forest Conditions

2.2. Management Systems

2.2.1. Management Objectives

2.2.2. Management Constraints

2.2.3. Silvicultural Systems

- BAU or SHORT~FPA. “Business-as-usual” (BAU) management to maximize NPV under the selected constraints of State FPA rules. This scenario represents common practice in production forests of western Oregon and Washington.

- SHORT~FSC. Management to maximize NPV under the green tree retention and RMZ constraints required by FSC. “Short” refers to the relative length of the rotation age compared to MSY-oriented scenarios.

- LONG~FPA. Management to maximize the sustained yield of timber under the selected constraints of State FPA rules. “Long” refers to the relative length of the rotation age relative to the NPV-based management scenarios.

- LONG~FSC. Management to maximize the sustained yield of timber under the selected constraints of FSC certification.

2.3. Key Performance Indicators

2.3.1. Carbon Storage in the Forest and Wood Products

2.3.2. Cumulative Timber Output

2.3.3. Discounted Cash Flow

2.3.4. Embodied Carbon

2.3.5. Incentives or Price Premiums that Close the Financial Gap with BAU

2.4. Growth-and-Yield Simulation

Computing Environment for Simulations, Data Analysis, and Visualization

3. Results

3.1. Calibration of FVS

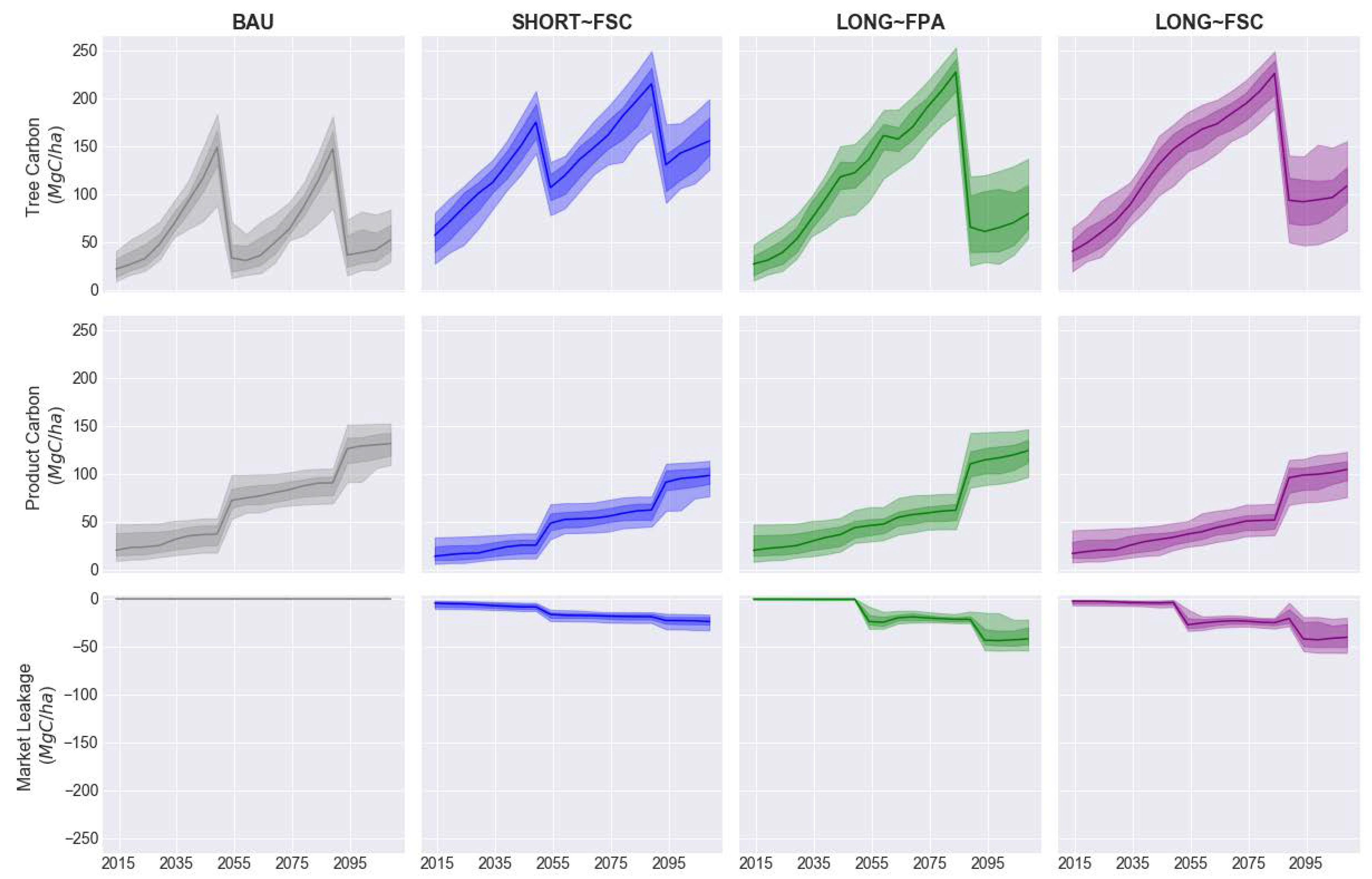

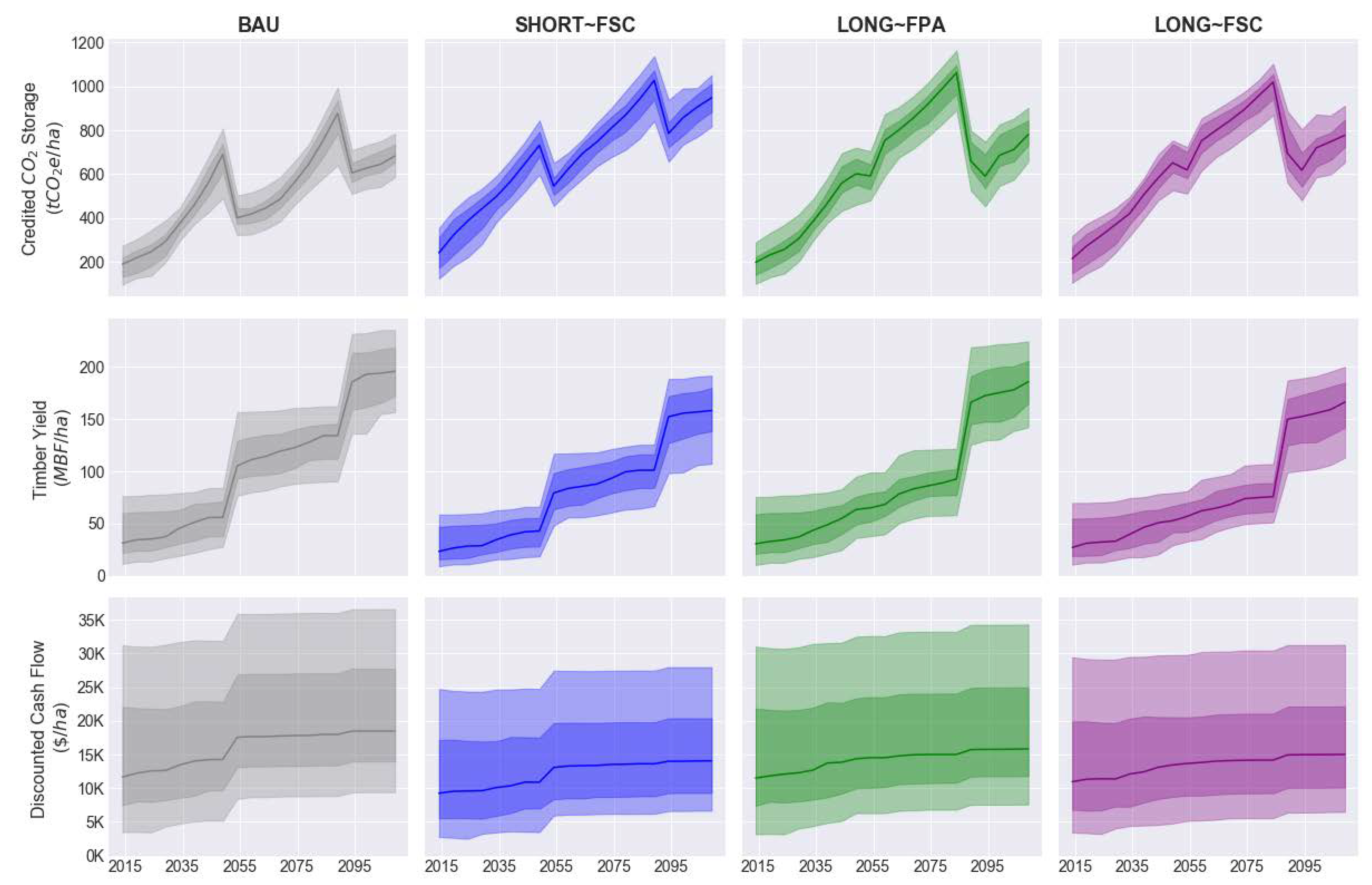

3.2. Simulated Forest Dynamics

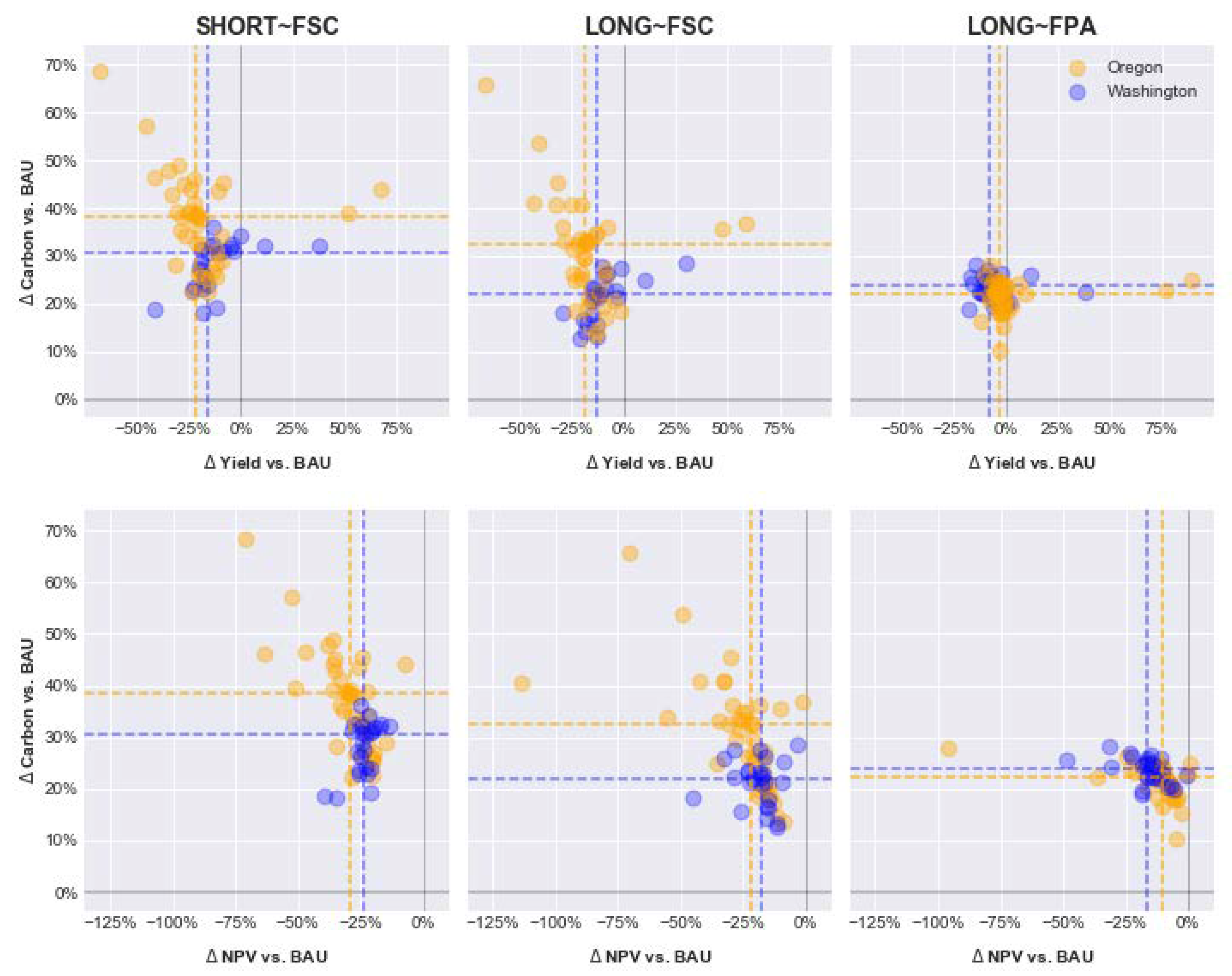

3.3. Key Performance Indicators

3.4. Values that Close the Financial Gap with BAU

4. Discussion

4.1. Fundamental Importance of FVS Calibration

4.2. Tradeoffs in Timber Production, Carbon Storage, and Cash Flow

4.3. Multiple Financial Gap-Closing Strategies Would Likely Need to be Used for FSC to Compete with BAU

4.4. Policy Implications

4.4.1. State FPA Rules Fundamentally Affect the Landscape and New Policy Opportunities

4.4.2. FSC-Certification Appears to Offer a Clear Surrogate for Increased Forest Carbon Storage

4.4.3. Lower Variability in LONG~FPA Suggest Extending Rotation Ages alone as a Viable Option

5. Conclusions

Supplementary Materials

Author Contributions

Funding

Conflicts of Interest

References

- Waring, R.H.; Franklin, J.F. Evergreen Coniferous Forests of the Pacific Northwest. Science 1979, 204, 1380–1386. [Google Scholar] [CrossRef] [PubMed]

- Gholz, H.L. Environmental Limits on Aboveground Net Primary Production, Leaf Area, and Biomass in Vegetation Zones of the Pacific Northwest. Ecology 1982, 63, 469–481. [Google Scholar] [CrossRef]

- Franklin, J.F.; Dyrness, C.T. Natural Vegetation of Oregon and Washington; Oregon State University Press: Corvallis, OR, USA, 1988; ISBN 978-0-87071-356-9. [Google Scholar]

- Oregon Forest Resources Institute. Oregon Forest Facts: 2017-18 Edition; Oregon Forest Resources Institute: Portland, OR, USA, 2017; p. 32.

- Haynes, R.W. An Analysis of the Timber Situation in the United States: 1952 to 2050; U.S. Department of Agriculture, Forest Service, Pacific Northwest Research Station: Portland, OR, USA, 2003.

- Van Kooten, G.C.; Binkley, C.S.; Delcourt, G. Effect of Carbon Taxes and Subsidies on Optimal Forest Rotation Age and Supply of Carbon Services. Am. J. Agric. Econ. 1995, 77, 365–374. [Google Scholar] [CrossRef]

- Talbert, C.; Marshall, D. Plantation Productivity in the Douglas-Fir Region under Intensive Silvicultural Practices: Results from Research and Operations. J. For. 2005, 103, 65–70. [Google Scholar] [CrossRef]

- Binkley, C.S. The rise and fall of the timber investment management organizations: Ownership changes in US forestlands. In Proceedings of the 2007 Pinchot Distinguished Lecture, Washington, DC, USA, 2 March 2007; Pinchot Institute for Conservation: Washington, DC, USA, 2007; p. 12. [Google Scholar]

- Gunnoe, A. The Financialization of the US Forest Products Industry: Socio-Economic Relations, Shareholder Value, and the Restructuring of an Industry. Soc. Forces 2016, 94, 1075–1101. [Google Scholar] [CrossRef]

- Bliss, J.C.; Kelly, E.C.; Abrams, J.; Bailey, C.; Dyer, J. Disintegration of the U. S. Industrial Forest Estate: Dynamics, Trajectories, and Questions. Small-Scale For. 2010, 9, 53–66. [Google Scholar] [CrossRef]

- Brazee, R.J. Introduction—The Faustmann Formula: Fundamental to Forest Economics 150 Years after Publication. For. Sci. 2001, 47, 441–442. [Google Scholar] [CrossRef]

- Curtis, R.O. Extended rotations and culmination age of coast Douglas-fir: Old studies speak to current issues. US Dep. Agric. For. Serv. Pac. Northwest Res. 1995, 485. [Google Scholar] [CrossRef]

- Curtis, R.O.; Marshall, D.D. Douglas-fir rotations—Time for reappraisal? West. J. Appl. For. 1993, 8, 81–85. [Google Scholar]

- Curtis, R.O. Volume growth trends in a Douglas-fir levels-of-growing-stock study. West. J. Appl. For. 2006, 21, 79–86. [Google Scholar]

- Curtis, R.O. The Role of Extended Rotations. In Creating a Forestry for the 21st Century: The Science of Ecosystem Management; Island Press: Washington, DC, USA, 1997; pp. 165–170. ISBN 978-1-61091-392-8. [Google Scholar]

- Curtis, R.O.; Marshall, D.D.; DeBell, D.S. Silvicultural options for young-growth Douglas-fir forests: The Capitol Forest study—Establishment and first results. U.S. Dep. Agric. For. Serv. Pac. Northwest Res. 2004. [Google Scholar] [CrossRef]

- Foley, T.G.; deB. Richter, D.; Galik, C.S. Extending rotation age for carbon sequestration: A cross-protocol comparison of North American forest offsets. For. Ecol. Manag. 2009, 259, 201–209. [Google Scholar] [CrossRef]

- Sohngen, B.; Brown, S. Extending timber rotations: Carbon and cost implications. Clim. Policy 2008, 8, 435–451. [Google Scholar] [CrossRef]

- Law, B.E.; Hudiburg, T.W.; Berner, L.T.; Kent, J.J.; Buotte, P.C.; Harmon, M.E. Land use strategies to mitigate climate change in carbon dense temperate forests. Proc. Natl. Acad. Sci. USA 2018, 115, 3663–3668. [Google Scholar] [CrossRef] [PubMed]

- Tóth, S.F.; Ettl, G.J.; Könnyű, N.; Rabotyagov, S.S.; Rogers, L.W.; Comnick, J.M. ECOSEL: Multi-objective optimization to sell forest ecosystem services. For. Policy Econ. 2013, 35, 73–82. [Google Scholar] [CrossRef]

- Fischer, P.W.; Cullen, A.C.; Ettl, G.J. The Effect of Forest Management Strategy on Carbon Storage and Revenue in Western Washington: A Probabilistic Simulation of Tradeoffs: Effects of Forest Management on Carbon and Timber Revenue. Risk Anal. 2017, 37, 173–192. [Google Scholar] [CrossRef] [PubMed]

- Harmon, M.E.; Marks, B. Effects of silvicultural practices on carbon stores in Douglas-fir western hemlock forests in the Pacific Northwest, USA: Results from a simulation model. Can. J. For. Res. 2002, 32, 863–877. [Google Scholar] [CrossRef]

- Sathre, R.; O’Connor, J. Meta-analysis of greenhouse gas displacement factors of wood product substitution. Environ. Sci. Policy 2010, 13, 104–114. [Google Scholar] [CrossRef]

- Bergman, R.; Taylor, A. EPD—Environmental Product Declarations for Wood Products—An Application of Life Cycle Information about Forest Products. For. Prod. J. 2011, 61, 192–201. [Google Scholar] [CrossRef]

- Cowan, S.; Davies, B.; Diaz, D.; Enelow, N.; Halsey, K.; Langstaff, K. Optimizing Urban Ecosystem Services: The Bullitt Center Case Study; Ecotrust: Portland, OR, USA, 2014; p. 141. [Google Scholar]

- Hamrick, K.; Gallant, M. Fertile Ground: State of Forest Carbon Finance 2017; Forest Trends’ Ecosystem Marketplace: Washington, DC, USA, 2017; p. 88. [Google Scholar]

- Mendell, B.; Lang, A.H. Comparing Forest Certification Standards in the U.S.: Economic Analysis and Practical Considerations; EconoSTATS: Fairfax, VA, USA, 2013. [Google Scholar]

- Eriksson, L.O.; Sallnäs, O.; Ståhl, G. Forest certification and Swedish wood supply. For. Policy Econ. 2007, 9, 452–463. [Google Scholar] [CrossRef]

- Nebel, G.; Quevedo, L.; Bredahl Jacobsen, J.; Helles, F. Development and economic significance of forest certification: The case of FSC in Bolivia. For. Policy Econ. 2005, 7, 175–186. [Google Scholar] [CrossRef]

- Bouslah, K.; M’Zali, B.; Turcotte, M.-F.; Kooli, M. The Impact of Forest Certification on Firm Financial Performance in Canada and the U.S. J. Bus. Ethics 2010, 96, 551–572. [Google Scholar] [CrossRef]

- FSC International. FSC Principles and Criteria for Forest Stewardship; Forest Stewardship Council: Bonn, Germany, 2015; p. 32. [Google Scholar]

- Rabotyagov, S.S.; Lin, S. Small forest landowner preferences for working forest conservation contract attributes: A case of Washington State, USA. J. For. Econ. 2013, 19, 307–330. [Google Scholar] [CrossRef]

- Ohmann, J.L.; Gregory, M.J. Predictive mapping of forest composition and structure with direct gradient analysis and nearest- neighbor imputation in coastal Oregon, U.S.A. Can. J. For. Res. 2002, 32, 725–741. [Google Scholar] [CrossRef]

- Ohmann, J.L.; Gregory, M.J.; Henderson, E.B.; Roberts, H.M. Mapping gradients of community composition with nearest-neighbour imputation: Extending plot data for landscape analysis: Extending plot data for landscape analysis. J. Veg. Sci. 2011, 22, 660–676. [Google Scholar] [CrossRef]

- LEMMA GNN Plot Database. Available online: https://lemma.forestry.oregonstate.edu/data/plot-database (accessed on 16 May 2018).

- Latta, G.; Temesgen, H.; Barrett, T.R. Mapping and imputing potential productivity of Pacific Northwest forests using climate variables. Can. J. For. Res. 2009, 39, 1197–1207. [Google Scholar] [CrossRef]

- Martin, F.C. User Guide to the Economic Extension (ECON) of the Forest Vegetation Simulator; U.S. Department of Agriculture, Forest Service, Forest Management Service Center: Fort Collins, CO, USA, 2013; p. 43.

- Washington Department of Natural Resources. Washington State Forest Practices Rules (Title 222 WAC). Available online: https://www.dnr.wa.gov/about/boards-and-councils/forest-practices-board/rules-and-guidelines/forest-practices-rules (accessed on 22 June 2018).

- Oregon Secretary of State. Oregon Administrative Rules Database. Available online: https://secure.sos.state.or.us/oard/displayChapterRules.action?selectedChapter=82 (accessed on 22 June 2018).

- FSC-US. FSC-US Forest Management Standard (v1.0); Forest Stewardship Council International: Bonn, Germany, 2012; p. 109. [Google Scholar]

- California Air Resources Board. Compliance Offset Protocol: U.S. Forest Projects; California Environmental Protection Agency, Air Resources Board: Sacramento, CA, USA, 2015; p. 146.

- Wang, Y. Volume Estimator Library Equations; USDA Forest Service, Forest Management Service Center: Fort Collins, CO, USA, 2017; p. 77.

- Waddell, K.L.; Campbell, K.; Kuegler, O.; Christensen, G. FIA Volume Equation Documentation Updated on 9-19-2014. 2014. Available online: https://www.arb.ca.gov/cc/capandtrade/offsets/copupdatereferences/qm_volume_equations_pnw_updated_091914.pdf (accessed on 27 April 2018).

- Blacklock, N. 2016 Strategic Issues for US Pacific Northwest Timberlands. In Proceedings of the 3rd Annual Western Forest Industry Conference: Mapping the Course—Timberlands, Forest Products Processing and Energy Issues for 2016, Vancouver, WA, USA, 28 January 2016; Western Forestry and Conservation Association: Vancouver, WA, USA, 2016; p. 23. [Google Scholar]

- New Forests. Timberland Investment Outlook 2013–2017; New Forests: Chatswood, Australia, 2013; p. 32. [Google Scholar]

- Washington Department of Natural Resources Mill Log Prices—Domestically Processed (28 February 2018). Available online: http://www.dnr.wa.gov/publications/psl_ts_feb18_logprices.pdf (accessed on 13 June 2018).

- Arney, J.D. The Economic Results of a PNW Silvicultural Costs Survey: Are You Swimming above or Below the Financial Waterline? In Proceedings of the 2016 PNW Reforestation Council Annual Meeting, Vancouver, WA, USA, 4 October 2016; Forest Biometrics Research Institute: Portland, OR, USA, 2016; p. 41. [Google Scholar]

- Clean Development Mechanism Executive Board. Tool for the Demonstration and Assessment of Additionality in A/R CDM Project Activities (Version 02). Available online: https://cdm.unfccc.int/methodologies/ARmethodologies/tools/ar-am-tool-01-v2.pdf/history_view (accessed on 25 June 2018).

- Verra. Tool for the Demonstration and Assessment of Additionality in VCS Agriculture, Forestry and Other Land Use (AFOLU) Project Activities (Version 3.0); Verified Carbon Standard: Washington, DC, USA, 2012; p. 13. [Google Scholar]

- American Carbon Registry. The American Carbon Registry Standard; Winrock International: Arlington, VA, USA, 2018; p. 103. [Google Scholar]

- Von Hagen, B. Unexplored Potential of Pacific Northwest Forests. In Old Growth in a New World: A Pacific Northwest Icon Reexamined; Island Press: Washington, DC, USA, 2009; pp. 286–299. [Google Scholar]

- Keyser, C. Pacific Northwest Coast (PN) Variant Overview—Forest Vegetation Simulator; U.S. Department of Agriculture, Forest Service, Forest Management Service Center: Fort Collins, CO, USA, 2017; p. 67.

- Dixon, G.E. Essential FVS: A User’s Guide to the Forest Vegetation Simulator; USDA Forest Service, Forest Management Service Center: Fort Collins, CO, USA, 2017; p. 226.

- Crookston, N.L.; Dixon, G.E. The forest vegetation simulator: A review of its structure, content, and applications. Comput. Electron. Agric. 2005, 49, 60–80. [Google Scholar] [CrossRef]

- Crookston, N.L.; Gammel, D.L.; Rebain, S.; Robinson, D.C.E.; Keyser, C.; Dahl, C. Users Guide to the Database Extension of the Forest Vegetation Simulator Version 2.0; U.S. Department of Agriculture, Forest Service, Forest Management Service Center: Fort Collins, CO, USA, 2003; p. 60.

- Chambers, C.J. Empirical Growth and Yield Tables for the Douglas Fir Zone; Washington Department of Natural Resources: Olympia, WA, USA, 1980; p. 56.

- Curtis, R.O.; Clendenen, G.W.; Reukema, D.L.; DeMars, D.J. Yield Tables for Managed Stands of Coast Douglas-Fir; USDA Forest Service, Pacific Northwest Forest and Range Experiment Station: Portland, OR, USA, 1982; p. 182.

- McArdle, R.E.; Meyer, W.H.; Bruce, D. The Yield of Douglas fir in the Pacific Northwest; USDA Forest Service, Pacific Northwest Forest and Range Experiment Station: Washington, DC, USA, 1961; p. 74.

- Mitchell, K.J.; Cameron, I.R. Managed Stand Yield Tables for Coastal Douglas-fir: Initial Density and Precommercial Thinning; British Columbia Ministry of Forests, Research Branch: Victoria, BC, Canada, 1985; p. 81.

- Schumacher, F.X. Yield, Stand and Volume Tables for Douglas Fir in California; University of California, Berkeley, Agricultural Experiment Station: Berkeley, CA, USA, 1930; p. 41. [Google Scholar]

- Stand Management Cooperative SMC Plantation Yield Calculator. Available online: http://www.sefs.washington.edu/research.smc/research/pyc/index.html (accessed on 4 May 2018).

- Williamson, R.L. Growth and Yield Records from Well-Stocked Stands of Douglas-Fir; U.S. Department of Agriculture, Forest Service, Pacific Northwest Forest and Range Experiment Station: Portland, OR, USA, 1963; p. 27.

- Curtis, R.O.; Marshall, D.D. Levels-of-Growing-Stock Cooperative Study in Douglas-Fir: Report No. 14—Stampede Creek, 30-Year Results; U.S. Department of Agriculture, Forest Service, Pacific Northwest Research Station: Portland, OR, USA, 2002; p. 77.

- USDA Forest Service Pacific Northwest Research Station. PNW-FIADB: Pacific Northwest Annual Forest Inventory Database. Available online: https://www.fs.fed.us/pnw/rma/fia-topics/inventory-data/ (accessed on 13 June 2018).

- USDA Forest Service Forest Management Service Center. open-fvs: The Forest Vegetation Simulator (FVS) Forest Growth Model. Available online: https://sourceforge.net/projects/open-fvs/ (accessed on 5 November 2017).

- Ecotrust FSC. Case Studies. Available online: https://github.com/Ecotrust/FSC_Case_Studies (accessed on 21 May 2018).

- Thomas, K.; Benjamin, R.-K.; Fernando, P.; Brian, G.; Matthias, B.; Jonathan, F.; Kyle, K.; Jessica, H.; Jason, G.; Sylvain, C.; et al. Jupyter Notebooks—A publishing format for reproducible computational workflows. In Proceedings of the 20th International Conference on Electronic Publishing, Göttingen, Germany, 9 June 2016; IOS Press: Amsterdam, The Netherlands, 2016; pp. 87–90. [Google Scholar]

- McGaughey, R.J. Stand Visualization System; USDA Forest Service, Pacific Northwest Research Station: Portland, OR, USA, 2004; p. 140.

- Vandendriesche, D. FVS out of the box—Assembly required. In Proceedings of the 2009 National Silviculture Workshop, Boise, ID, USA, 15–18 June 2009; U.S. Department of Agriculture, Forest Service, Rocky Mountain Research Station: Fort Collins, CO, USA, 2010; pp. 289–306. [Google Scholar]

- Haynes, R. Will Markets Provide Sufficient Incentive for Sustainable Forest Management? In Understanding Key Issues of Sustainable Wood Production in the Pacific Northwest; Deal, R.L., White, S.M., Eds.; U.S. Department of Agriculture, Forest Service, Pacific Northwest Research Station: Portland, OR, USA, 2005; pp. 13–19. [Google Scholar]

- Kerchner, C.D.; Keeton, W.S. California’s regulatory forest carbon market: Viability for northeast landowners. For. Policy Econ. 2015, 50, 70–81. [Google Scholar] [CrossRef]

- Galik, C.S.; Cooley, D.M.; Baker, J.S. Analysis of the production and transaction costs of forest carbon offset projects in the USA. J. Environ. Manag. 2012, 112, 128–136. [Google Scholar] [CrossRef] [PubMed]

- Cacho, O.J.; Lipper, L.; Moss, J. Transaction costs of carbon offset projects: A comparative study. Ecol. Econ. 2013, 88, 232–243. [Google Scholar] [CrossRef]

- Cacho, O.J.; Wise, R.M.; MacDicken, K.G. Carbon Monitoring Costs and their Effect on Incentives to Sequester Carbon through Forestry. Mitig. Adapt. Strateg. Glob. Chang. 2004, 9, 273–293. [Google Scholar] [CrossRef]

- Charnley, S.; Diaz, D.; Gosnell, H. Mitigating climate change through small-scale forestry in the USA: Opportunities and challenges. Small-Scale For. 2010, 9, 445–462. [Google Scholar] [CrossRef]

- Bigsby, H. Carbon banking: Creating flexibility for forest owners. For. Ecol. Manag. 2009, 257, 378–383. [Google Scholar] [CrossRef]

- Forest Climate Working Group. Forest Carbon Solutions for Mitigating Climate Change: A Toolkit for State Governments; American Forest Foundation: Washington, DC, USA, 2015; p. 24. [Google Scholar]

- Pinchot Institute for Conservation. Forest Carbon Incentives: Options for Landowner Incentives to Increase Forest Carbon Sequestration; Pinchot Institute for Conservation: Washington, DC, USA, 2011; p. 48. [Google Scholar]

- Agne, M.C.; Beedlow, P.A.; Shaw, D.C.; Woodruff, D.R.; Lee, E.H.; Cline, S.P.; Comeleo, R.L. Interactions of predominant insects and diseases with climate change in Douglas-fir forests of western Oregon and Washington, U.S.A. For. Ecol. Manag. 2018, 409, 317–332. [Google Scholar] [CrossRef] [PubMed]

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| Activity | BAU | SHORT~FSC 1 | LONG~FPA | LONG~FSC 1 |

|---|---|---|---|---|

| Planting Douglas-fir | 1075 tph (435 tpa) | 1075 tph (435 tpa) | 1075 tph (435 tpa) | 1075 tph (435 tpa) |

| Commercial Thinning 2 | None | None | @ 55% SDImax 3, thin to 45% SDImax | @ 55% SDImax, thin to 45% SDImax |

| Regeneration Harvest | @ 38–44 years | @ 38–44 years | @ 75 years | @ 75 years |

| retain 10 tph ≥ 30.5 cm DBH (4 tpa ≥ 12 in DBH) | retain 30% pre-harvest basal area | retain 10 tph ≥ 30.5 cm DBH (4 tpa ≥ 12 in DBH) | retain 10% of pre-harvest basal area |

| Species | $/MBF |

|---|---|

| Douglas-fir | 796 |

| Sitka spruce | 450 |

| Western hemlock | 640 |

| Noble fir | 640 |

| Grand fir | 640 |

| Pacific silver fir | 640 |

| Yellow cedar | 640 |

| Western redcedar | 1263 |

| Red alder | 852 |

| Bigleaf maple | 499 |

| Activity | $ | Per |

|---|---|---|

| General administration | 86 | ha/year |

| Site preparation | 210 | ha |

| Tree planting | 0.73 | seedling |

| Brush control (@ age 5) | 334 | ha |

| Harvest administration | 5 | MBF |

| Hauling | 100 | MBF |

| Road maintenance | 15 | MBF |

| Ground-based harvest: | ||

| Regeneration harvest | 150 | MBF |

| Commercial thin | 175 | MBF |

| Cable logging: | ||

| Regeneration harvest | 200 | MBF |

| Commercial thin | 300 | MBF |

| SHORT~FPA | SHORT~FSC | LONG~FPA | LONG~FSC | |||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|

| OREGON | MBF | tCO2e | $K | MBF | tCO2e | $K | MBF | tCO2e | $K | MBF | tCO2e | $K |

| ~FPA Buffers | 199 | 497 | 19.1 | 169 | 634 | 15.3 | 197 | 608 | 17.1 | 183 | 595 | 15.9 |

| ~FSC Buffers | 176 | 553 | 18.0 | 153 | 679 | 14.3 | 163 | 686 | 15.7 | 168 | 646 | 15.3 |

| WASHINGTON | ||||||||||||

| ~FPA Buffers | 185 | 518 | 18.0 | 166 | 663 | 14.6 | 174 | 639 | 15.6 | 170 | 620 | 15.5 |

| ~FSC Buffers | 178 | 527 | 17.2 | 159 | 659 | 14.0 | 158 | 656 | 13.9 | 165 | 616 | 14.4 |

| SHORT~FSC | LONG~FSC | LONG~FPA | |||||||

|---|---|---|---|---|---|---|---|---|---|

| OREGON | 25% | median | 75% | 25% | median | 75% | 25% | median | 75% |

| Wood Premium (%) | 9.8 | 15.0 | 21.3 | 3.0 | 5.2 | 9.8 | 0.0 | 1.4 | 2.5 |

| Carbon Value ($/tCO2e) | 27.90 | 41.21 | 49.43 | 30.84 | 42.68 | 51.50 | 0.00 | 17.94 | 23.99 |

| WASHINGTON | |||||||||

| Wood Premium (%) | 8.7 | 10.7 | 12.0 | 5.1 | 5.9 | 9.6 | 2.3 | 4.7 | 6.2 |

| Carbon Value ($/tCO2e) | 10.96 | 26.03 | 39.56 | 26.91 | 32.76 | 40.03 | 20.61 | 33.83 | 38.02 |

© 2018 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).

Share and Cite

Diaz, D.D.; Loreno, S.; Ettl, G.J.; Davies, B. Tradeoffs in Timber, Carbon, and Cash Flow under Alternative Management Systems for Douglas-Fir in the Pacific Northwest. Forests 2018, 9, 447. https://doi.org/10.3390/f9080447

Diaz DD, Loreno S, Ettl GJ, Davies B. Tradeoffs in Timber, Carbon, and Cash Flow under Alternative Management Systems for Douglas-Fir in the Pacific Northwest. Forests. 2018; 9(8):447. https://doi.org/10.3390/f9080447

Chicago/Turabian StyleDiaz, David D., Sara Loreno, Gregory J. Ettl, and Brent Davies. 2018. "Tradeoffs in Timber, Carbon, and Cash Flow under Alternative Management Systems for Douglas-Fir in the Pacific Northwest" Forests 9, no. 8: 447. https://doi.org/10.3390/f9080447

APA StyleDiaz, D. D., Loreno, S., Ettl, G. J., & Davies, B. (2018). Tradeoffs in Timber, Carbon, and Cash Flow under Alternative Management Systems for Douglas-Fir in the Pacific Northwest. Forests, 9(8), 447. https://doi.org/10.3390/f9080447