An Assessment of Stumpage Price and the Price Index of Chinese Fir Timber Forests in Southern China Using a Hedonic Price Model

Abstract

1. Introduction

2. Materials and Methods

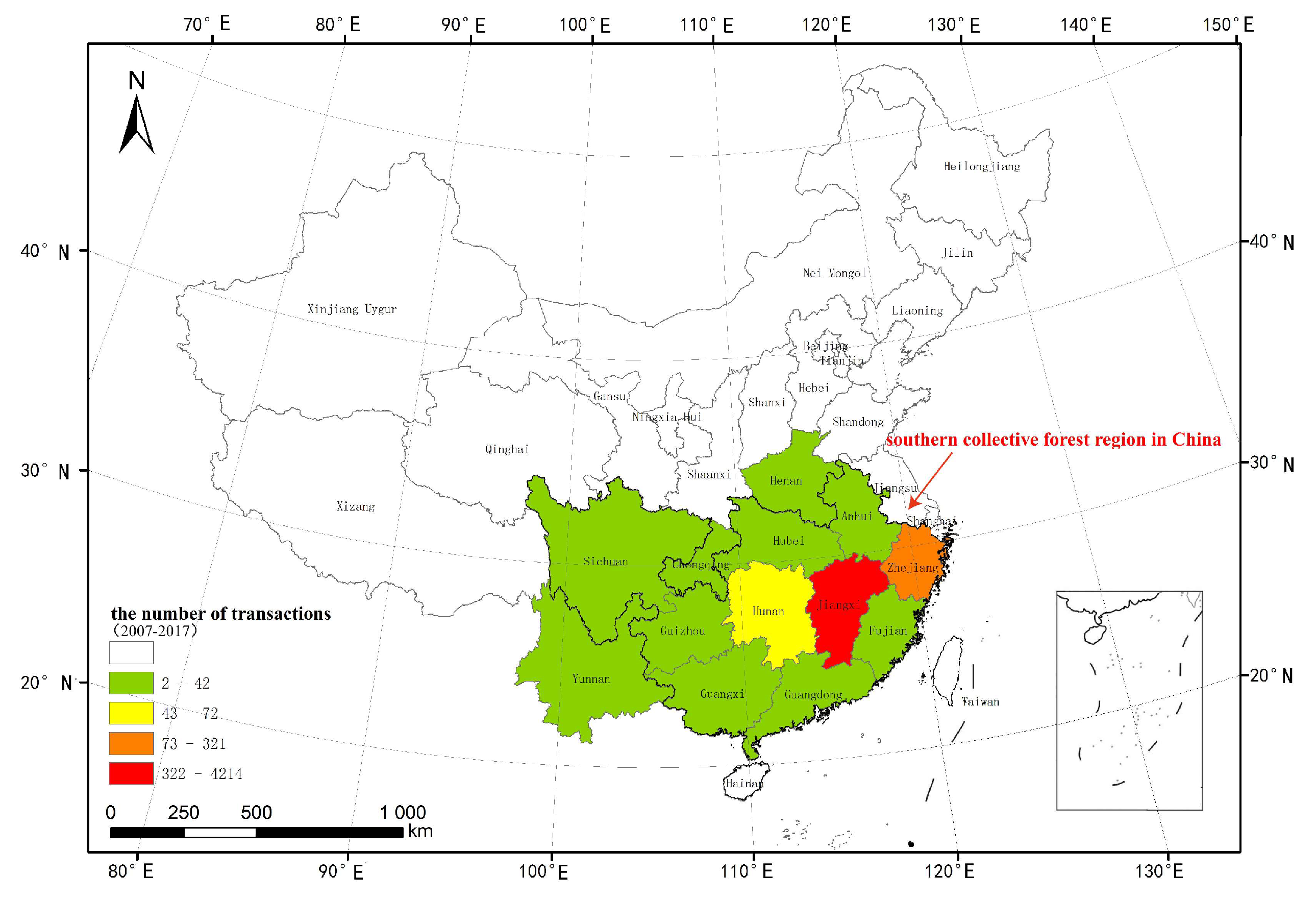

2.1. Data Collection

2.2. Hedonic Price Method

2.3. Dummy Time Hedonic Index

3. Results

3.1. Actual Stumpage Prices of Chinese Fir Timber Forests

3.2. Selection of a Hedonic Price Model for Chinese Fir Timber Forests

3.3. Determination of the Hedonic Price Method for Chinese Fir Timber Forests

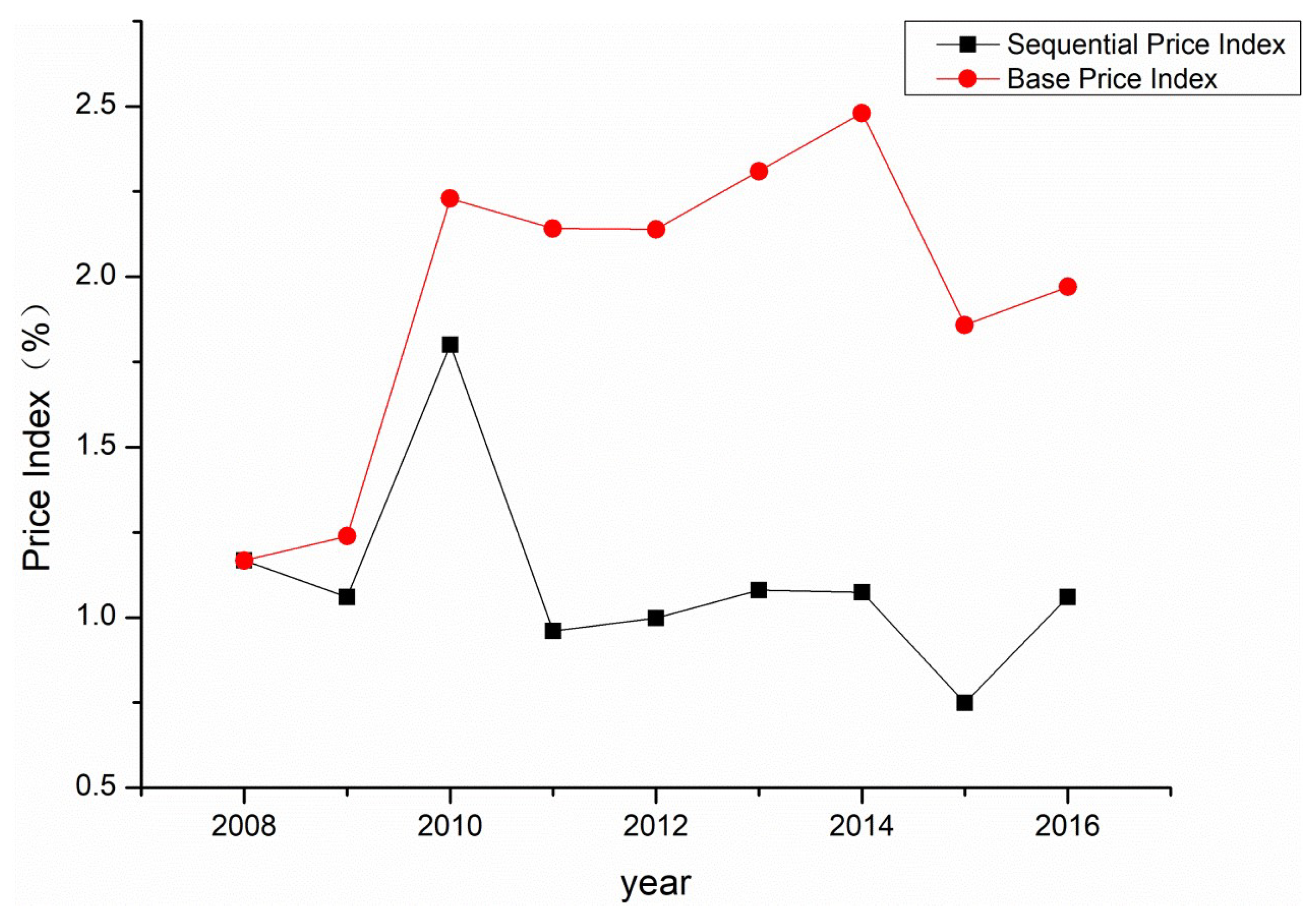

3.4. Index of Stumpage Prices of Chinese Fir Timber Forests

4. Discussion

4.1. Choice of HPM Form

4.2. Factors Driving Stumpage Prices of Chinese Fir Timber Forests

4.3. The Difference between Forestry Exchange and Timber Markets in China

4.4. Impact on Forest Accounting

4.5. Further Studies

5. Conclusions

Author Contributions

Funding

Acknowledgments

Conflicts of Interest

References

- Wagner, J.E.; Sendak, P.E. The annual increase of Northeastern regional timber stumpage prices: 1961 to 2002. For. Prod. J. 2005, 55, 36–45. [Google Scholar]

- Howard, T.E.; Chase, W.E. Maine stumpage prices: Characteristics and trends from 1963 to 1990. For. Prod. J. 1995, 45, 31–36. [Google Scholar]

- Linehan, P.E.; Jacobson, M.G.; McDill, M.E. Hardwood Stumpage Price Trends and Regional Market Differences in Pennsylvania. North. J. Appl. For. 2003, 20, 124–130. [Google Scholar] [CrossRef][Green Version]

- Linehan, P.E.; Jacobson, M.G. Forecasting hardwood stumpage price trends in Pennsylvania. For. Prod. J. 2005, 55, 47–52. [Google Scholar]

- Mei, B.; Clutter, M.; Harris, T. Modeling and forecasting pine sawtimber stumpage prices in the US South by various time series models. Can. J. For. Res. 2010, 40, 1506–1516. [Google Scholar] [CrossRef]

- Bayazidi, S.; Yoshimoto, A. Appropriate stochastic price models for the finnish stumpage market. Formath 2011, 10, 123–142. [Google Scholar] [CrossRef]

- Duval, R.P.; McConnell, T.E.; Hix, D.M. Annual Change in Ohio Hardwood Stumpage Prices, 1960 to 2011. For. Prod. J. 2014, 64, 19–25. [Google Scholar] [CrossRef]

- Hultkrantz, L.; Andersson, L.; Mantalos, P. Stumpage prices in Sweden 1909–2012: Testing for non-stationarity. J. For. Econ. 2014, 20, 33–46. [Google Scholar] [CrossRef][Green Version]

- Parajuli, R.; Tanger, S.; Joshi, O.; Henderson, J. Modeling Prices for Sawtimber Stumpage in the South-Central United States. Forests 2016, 7, 148. [Google Scholar] [CrossRef]

- Nautiyal, J.C. Stumpage price function for hardwoods in the Niagara district of Ontario. Can. J. For. Res. 1982, 12, 210–214. [Google Scholar] [CrossRef]

- Xu, Z.H.; McKetta, C.W. Understanding log and stumpage prices in China: A primer for capitalist forest economists. Can. J. For. Res. 1986, 16, 1123–1127. [Google Scholar] [CrossRef]

- Sedjo, R.A. Comparative views of different stumpage pricing systems: Canada and the United States. For. Sci. 2006, 52, 446–450. [Google Scholar]

- Niquidet, K.; van Kooten, G.C. Transaction Evidence Appraisal: Competition in British Columbia’s Stumpage Markets. For. Sci. 2006, 52, 451–459. [Google Scholar]

- Brown, R.N.; Kilgore, M.A.; Coggins, J.S.; Blinn, C.R. The impact of timber-sale tract, policy, and administrative characteristics on state stumpage prices: An econometric analysis. For. Policy Econ. 2012, 21, 71–80. [Google Scholar] [CrossRef]

- Brown, R.N.; Kilgore, M.A.; Blinn, C.R.; Coggins, J.S. The impact of reserve prices and contract length on stumpage bid prices: An empirical assessment. North. J. Appl. For. 2013, 30, 85–91. [Google Scholar] [CrossRef]

- Nepal, P.; Grala, R.K.; Grebner, D.L.; ABT, R.C. Impact of harvest-level changes on carbon accumulation and timber stumpage prices in Mississippi. South. J. Appl. For. 2013, 37, 160–168. [Google Scholar] [CrossRef]

- Luppold, W.; Bumgardner, M.; Mcconnell, T.E. Impacts of changing hardwood lumber consumption and price on stumpage and sawlog prices in Ohio. For. Sci. 2014, 60, 994–999. [Google Scholar] [CrossRef]

- Klepacka, A.M.; Siry, J.P.; Bettinger, P. Stumpage prices: A review of influential factors. Int. For. Rev. 2017, 19, 158–169. [Google Scholar] [CrossRef]

- Yin, R.; Yao, S.; Huo, X. China’s forest tenure reform and institutional change in the new century: What has been implemented and what remains to be pursued? Land Use Policy 2013, 30, 825–833. [Google Scholar] [CrossRef]

- Han, X.; Kant, S.S.; Xie, Y.A. spatial hedonic stumpage analysis of standing timber auctions in Jiangxi Province of China. For. Policy Econ. 2018, 96, 63–74. [Google Scholar] [CrossRef]

- Ladd, G.W.; Martin, M.B. Prices and demands for input characteristics. Am. J. Agric. Econ. 1976, 58, 21–30. [Google Scholar] [CrossRef]

- Calderon, A.D.; Caudill, S.B.; Mixon, F.G. Valuing Recreational Water Clarity and Quality: Evidence from Hedonic Pricing Models of Lakeshore Properties. Appl. Econ. Lett. 2019, 26, 237–244. [Google Scholar] [CrossRef]

- Cavallo, C.; Caracciolo, F.; Cicia, G.; Del Giudice, T. Extra-virgin olive oil: Are consumers provided with the sensory quality they want? A hedonic price model with sensory attributes. J. Sci. Food Agric. 2018, 98, 1591–1598. [Google Scholar] [CrossRef] [PubMed]

- Ready, R.C.; Abdalla, C.W. The Amenity and Disamenity Impacts of Agriculture: Estimates from a Hedonic Pricing Model. Am. J. Agric. Econ. 2005, 87, 314–326. [Google Scholar] [CrossRef]

- Humphreys, B.R.; Mondello, M. Determinants of Franchise Values in North American Professional Sports Leagues: Evidence from a Hedonic Price Model. Int. J. Sport. Financ. 2008, 3, 98. [Google Scholar]

- Kwong, L.M.K.; Ogwang, T.; Sun, L. Semiparametric versus parametric hedonic wine price models: An empirical investigation. Appl. Econ. Lett. 2017, 24, 897–901. [Google Scholar] [CrossRef]

- Van der Merwe, J.D.; Cloete, P.C.; van Schalkwyk, H.D. Factors Influencing the Competitiveness of the South African Wheat Industry: A Hedonic Price Model. Agrekon 2016, 55, 411–435. [Google Scholar] [CrossRef]

- Yim, E.S.; Lee, S.; Kim, W.G. Determinants of a restaurant average meal price: An application of the hedonic pricing model. Int. J. Hosp. Manag. 2014, 39, 11–20. [Google Scholar] [CrossRef]

- Wang, Z.G.; Zheng, S.; Lambert, D.M.; Fukuda, S.A. Hedonic Price Model for Rice Market in China. J. Fac. Agric. Kyushu. Univ. 2009, 54, 541–548. [Google Scholar]

- Nepal, M.; Nepal, A.K.; Apsara; Berrens, R.P. Where gathering firewood matters: Proximity and forest management effects in hedonic pricing models for rural Nepal. J. For. Econ. 2017, 27, 28–37. [Google Scholar] [CrossRef]

- Randeniya, T.D.; Ranasinghe, G.; Amarawickrama, S. A model to Estimate the Implicit Values of Housing Attributes by Applying the Hedonic Pricing Method. Int. J. Built. Environ. Sustain. 2017, 4, 113–120. [Google Scholar] [CrossRef]

- Bonnetain, P. A hedonic price model for islands. J. Urban. Econ. 2003, 54, 368–377. [Google Scholar] [CrossRef]

- Escobedo, F.J.; Adams, D.C.; Timilsina, N. Urban forest structure effects on property value. Ecosyst. Serv. 2015, 12, 209–217. [Google Scholar] [CrossRef]

- Puttock, G.D.; Meilke, K.D.; Prescott, D.M. Stumpage prices in southwestern Ontario: A hedonic function approach. For. Sci. 1990, 36, 1119–1132. [Google Scholar]

- Aronsson, T.; Carlén, O. The determinants of forest land prices: An empirical analysis. Can. J. For. Res. 2000, 30, 589–595. [Google Scholar] [CrossRef]

- Leefers, L.A.; Potter, W.K. Timber sale characteristics and competition for public Lands Stumpage: A case study from the Lake States. For. Sci. 2006, 52, 460–467. [Google Scholar]

- Kolis, K.; Hiironen, J.; Ärölä, E.; Vitikainen, A. Effects of sale-specific factors on stumpage prices in Finland. Silva Fenn. 2014, 48. [Google Scholar] [CrossRef]

- Kim, H.; Cieszewski, C. The Analysis of Pine Stumpage Prices Based on Timber Sale Characteristics of the Southern United States. J. For. Environ. Sci. 2015, 31, 38–46. [Google Scholar] [CrossRef]

- Wigren, R. House Price Indexes: The Hedonic Technique, and Some Other Methods Applied to Price Movements of Single Family Houses in Sweden. Scand. Hous. Plan. Res. 1984, 1, 81–98. [Google Scholar] [CrossRef]

- Gouriéroux, C.; Laferrère, A. Managing hedonic housing price indexes: The French experience. J. Hous. Econ. 2009, 18, 206–213. [Google Scholar] [CrossRef]

- Du, Y.; Sun, H.Q.; Zhang, S.Y.; Tian, Q. Design of Real Estate Price Index System Based on Hedonic Price Method. Appl. Mech. Mater. 2014, 488, 1463–1466. [Google Scholar]

- Hill, R.J. Hedonic Price Indexes for residential housing: A survey, evaluation and taxonomy. J. Econ. Surv. 2013, 27, 879–914. [Google Scholar] [CrossRef]

- Glumac, B.; Herrera, G.M.; Licheron, J. A hedonic urban land price index. Land Use Policy 2019, 81, 802–812. [Google Scholar] [CrossRef]

- Witkowska, D. Evaluation of the Individual Hedonic Art Price Indexes for the Polish Painters Representing the Auction Market in Poland. Transform. Bus. Econ. 2016, 15, 61–77. [Google Scholar]

- Pradier, P.C.; Gardes, F.; Greffe, X.; Mendoza, I.M. Autographs and the global art market: The case of hedonic prices for French autographs (1960–2005). J. Cult. Econ. 2016, 40, 453–485. [Google Scholar] [CrossRef]

- Bocart, F.; Hafner, C.M. Econometric analysis of volatile art markets. Comput. Stat. Data Anal. 2012, 56, 3091–3104. [Google Scholar] [CrossRef][Green Version]

- Berndt, E.R.; Griliches, Z.; Rappaport, N.J. Econometric estimates of price indexes for personal computers in the 1990’s. J. Econom. 1995, 68, 243–268. [Google Scholar] [CrossRef]

- Pakes, A. A reconsideration of hedonic price indexes with an application to PC’s. Am. Econ. Rev. 2003, 93, 1578–1596. [Google Scholar] [CrossRef]

- Benkard, C.L.; Bajari, P. Hedonic price indexes with unobserved product characteristics, and application to personal computers. J. Bus. Econ. Stat. 2005, 23, 61–75. [Google Scholar] [CrossRef]

- Silver, M.; Heravi, S. The difference between Hedonic Imputation Indexes and Time Dummy Hedonic Indexes. J. Bus. Econ. Stat. 2007, 25, 239–246. [Google Scholar] [CrossRef][Green Version]

- De Haan, J. Hedonic price indexes: A comparison of imputation, time dummy and Re-Pricing methods. Jahrb. Natl. Stat. 2010, 230, 772–791. [Google Scholar]

- De Haan, J. Direct and indirect time dummy approaches to hedonic price measurement. J. Econ. Soc. Meas. 2004, 29, 427–443. [Google Scholar] [CrossRef]

- Hill, R.J.; Melser, D. Hedonic imputation and the price index problem: An application to housing. Econ. Inq. 2008, 46, 593–609. [Google Scholar] [CrossRef]

- Liu, X.; Fu, Z.Y.; Zhang, B. Effects of sulfuric, nitric, and mixed acid rain on Chinese fir sapling growth in Southern China. Ecotoxicol. Environ. Saf. 2018, 160, 154–161. [Google Scholar] [CrossRef] [PubMed]

- Waugh, F.V. Quality factors influencing vegetable prices. J. Farm. Econ. 1928, 10, 185–196. [Google Scholar] [CrossRef]

- Griliches, Z. Price Indexes and Quality Change; Griliches, Z., Ed.; Harvard University Press: Cambridge, MA, USA, 1971; pp. 3–15. [Google Scholar]

- Rosen, S. Hedonic prices and implicit markets: Product differentiation in pure competition. J. Polit. Econ. 1974, 82, 34–55. [Google Scholar] [CrossRef]

- Fleischer, A. A room with a view—A valuation of the Mediterranean Sea view. Tour. Manag. 2012, 33, 598–602. [Google Scholar] [CrossRef]

- Hamilton, J.M. Costal landscape and the hedonic price of accommodation. Ecol. Econ. 2007, 62, 594–602. [Google Scholar] [CrossRef]

- Munn, L.A.; Palmquist, R.B. Estimating hedonic price equations for a timber stumpage market using stochastic frontier estimation procedures. Can. J. For. Res. 1997, 27, 1276–1280. [Google Scholar] [CrossRef]

- Zhang, D.W.; Meng, L.; Polyakov, M. Determinants of the Prices of Bare Forestland and Premerchantable Timber Stands: A Spatial Hedonic Study. For. Sci. 2013, 59, 400–406. [Google Scholar] [CrossRef]

- Zeide, B. Analysis of growth equations. For. Sci. 1993, 39, 594–616. [Google Scholar] [CrossRef]

- Liu, Z.; Li, F. The generalized Chapman-Richards function and application to tree and stand growth. J. For. Res. 2003, 14, 19–26. [Google Scholar]

- Bartelmus, P. Environmental-Economic Accounting: Progress and digression in the SEEA revision. Rev. Income Wealth. 2014, 60, 887–904. [Google Scholar] [CrossRef]

- El Serafy, S. System of Environmental-Economic Accounting 2012-Central Framework, United Nations, European Commission, Food and Agriculture Organisation of the United Nations, International Monetary Fund, Organisation for Economic Co-operation and Development and World Bank. Ecol. Econ. 2015, 112, 161–163. [Google Scholar] [CrossRef]

- Song, M.L.; Zhu, S.; Wang, J. China’s natural resources balance sheet from the perspective of government oversight: Based on the analysis of governance and accounting attributes. J. Environ. Manag. 2019, 248, 109–232. [Google Scholar] [CrossRef]

{kind=link}

{kind=link}

{kind=link}

| Fields | Expected Sign | Examples |

|---|---|---|

| Location | Chengjia Dock, Fangpo Village, Suzhuang Town, Kaihua County, Quzhou City, Zhejiang Province. | |

| Type | Ownership of standing trees | |

| Ownership | Collective ownership | |

| Distance to nearest simple road (km) | - | 2 |

| Distance to nearest national, provincial or county roads (km) | - | 20 |

| Structure | +/- | 70% Chinese fir + 30% Masson pine |

| Age (year) | + | 20 |

| Age group | + | mature age |

| Category | +/- | timber forest |

| Transfer period (year) | +/- | 5 |

| Area (ha) | +/- | 11.67 |

| The average diameter at breast height (cm) | + | 17.4 |

| The average high (m) | + | 12.5 |

| Volume (m3) | + | Chinese fir-333 m3, Masson pine-143 m3, total- 476 m3 |

| Total price (104RMB) | 18.7 | |

| Transaction date | 2017.7.21 |

| Age Group (year) | Trading Volume (case) | Average Price | ||

| Unit Stock Price (yuan/m3) | Unit Area Price (yuan/ha) | |||

| 0–10 | 13 | 574.6199 | 2638.0159 | |

| 10–20 | 142 | 714.6930 | 4872.8164 | |

| 20–30 | 601 | 599.5162 | 4483.3684 | |

| 30–40 | 161 | 736.7439 | 6571.9358 | |

| 40–50 | 10 | 689.4719 | 6699.8284 | |

| other | 1 | 901.4534 | 12404.0000 | |

| total | 928 | 641.8940 | 4911.8777 | |

| Age Group (year) | Unit Stock Price (yuan/m3) | Unit Area Price (yuan/ha) | ||

| min | max | min | max | |

| 0–10 | 206.0687 | 1056.4235 | 162.4129 | 6442.8945 |

| 10–20 | 106.6666 | 1418.4397 | 147.3414 | 13,157.8947 |

| 20–30 | 131.1991 | 2500.0000 | 284.3601 | 54,545.4545 |

| 30–40 | 233.3816 | 1700.5128 | 982.3736 | 17,439.3305 |

| 40–50 | 98.4009 | 1260.6599 | 487.8048 | 20,000.0000 |

| other | 901.4534 | 901.4534 | 12,404.0000 | 12,404.0000 |

| Total | 98.4009 | 2500.0000 | 147.3414 | 54,545.4545 |

| Model | SS | df | MS | F | Sig. | |

|---|---|---|---|---|---|---|

| 1 | Regression | 8,381,455.863 | 3 | 2,793,818.621 | 2109.826 | 0.000 *** |

| Residuals | 1,185,153.470 | 895 | 1324.194 | |||

| Total | 9,566,609.333 | 898 | ||||

| 2 | Regression | 352.851 | 3 | 117.617 | 116.412 | 0.000 *** |

| Residuals | 904.267 | 895 | 1.010 | |||

| Total | 1257.117 | 898 | ||||

| 3 | Regression | 1071.793 | 3 | 357.264 | 1725.365 | 0.000 *** |

| Residuals | 185.324 | 895 | 0.207 | |||

| Total | 1257.117 | 898 |

| Model | Coefficients | ||||||

|---|---|---|---|---|---|---|---|

| B | Std. Error | Beta | t | Sig. | |||

| 1 | Constant | 7.007 | 3.331 | 2.104 | 0.036 | R2ad = 0.876 Std. Error = 36.389 | |

| Age | 0.516 | 0.126 | 0.048 | 4.093 | 0.000 *** | ||

| Volume | 0.045 | 0.001 | 0.916 | 58.696 | 0.000 *** | ||

| Area | 0.008 | 0.005 | 0.022 | 1.426 | 0.154 | ||

| 2 | Constant | 3.024 | 0.092 | 32.873 | 0.000 | R2ad = 0.278 Std. Error = 1.005 | |

| Age | 0.014 | 0.003 | 0.116 | 4.085 | 0.000 *** | ||

| Volume | 0.000 | 0.000 | 0.381 | 10.122 | 0.000 *** | ||

| Area | 0.001 | 0.001 | 0.172 | 4.589 | 0.000 *** | ||

| 3 | Constant | −3.439 | 0.146 | −23.626 | 0.000 | R2ad = 0.852 Std. Error = 0.455 | |

| Age | −0.023 | 0.038 | −0.008 | −0.591 | 0.555 | ||

| Volume | 1.102 | 0.027 | 0.932 | 40.969 | 0.000 *** | ||

| Area | −0.010 | 0.026 | −0.009 | −0.396 | 0.692 | ||

| Group | N | Mean | Std. Deviation | Std. Error Mean |

|---|---|---|---|---|

| 1 | 30 | 3.1614 | 1.1510 | 0.2101 |

| 2 | 30 | 3.5895 | 1.0194 | 0.1861 |

| t value | df | Sig.(2-tailed) | ||

| −1.525 | 58 | 0.133 |

| Year | Model | Test |

|---|---|---|

| 2008 | t = (−11.263) (1.730) (0.988) (34.455) | n = 170, sigF = 0.000 ***, R2ad = 88%, Std.Error = 0.414 |

| 2009 | t = (−9.427)(0.996)(0.206)(35.535) | n = 260, sigF = 0.000 ***, R2ad = 83.8%, Std.Error = 0.462 |

| 2010 | t = (−11.502)(8.560)(−0.346)(29.802) | n = 207, sigF = 0.000 ***, R2ad = 86.5%, Std.Error =0.446 |

| 2011 | t = (-11.330)(−0.839)(0.459)(36.965) | n = 200, sigF = 0.000 ***, R2ad = 87.5%, Std. Error = 0.333 |

| 2012 | t = (−14.552)(−0.032)(−2.483)(50.935) | n = 276, sigF = 0.000 ***, R2ad = 90.6%, Std. Error = 0.308 |

| 2013 | t = (−15.591)(1.975)(-3.257)(56.460) | n =2 49, sigF = 0.000 ***, R2ad = 93, Std. Error = 0.283 |

| 2014 | t = (−13.027)(1.554)(2.319)(43.665) | n = 148, sigF = 0.000 ***, R2ad = 93.8%, Std. Error = 0.272 |

| 2015 | t = (−8.913)(−6.180)(2.861)(38.544) | n = 114, sigF = 0.000 ***, R2ad = 93.7%, Std. Error = 0.246 |

| 2016 | t = (−9.365)(1.136)(4.252)(37.748) | n = 98, sigF = 0.000***, R2ad = 94.3%, Std. Error = 0.251 |

| Age (year) | Stock (m3) | △Stock/Stock | Price (104 yuan) | △Price/Price | Sensitivity |

|---|---|---|---|---|---|

| 20 | 5000 | - | 237.20 | - | - |

| 20 | 10,000 | 1 | 468.52 | 0.98 | 0.98 |

| 20 | 15,000 | 2 | 697.67 | 1.94 | 0.97 |

| 20 | 20,000 | 3 | 925.42 | 2.90 | 0.97 |

| 20 | 25,000 | 4 | 1152.14 | 3.86 | 0.97 |

| 20 | 30,000 | 5 | 1378.03 | 4.81 | 0.96 |

| 20 | 35,000 | 6 | 1603.25 | 5.76 | 0.96 |

| 20 | 40,000 | 7 | 1827.89 | 6.71 | 0.96 |

| 20 | 45,000 | 8 | 2052.02 | 7.65 | 0.96 |

| 20 | 50,000 | 9 | 2275.70 | 8.59 | 0.95 |

| Age (year) | Stock (m3) | △Age/Age | Price (104 yuan) | △Price/Price | Sensitivity |

|---|---|---|---|---|---|

| 5 | 1200 | - | 22.19 | - | - |

| 10 | 1200 | 1 | 36.01 | 0.62 | 0.62 |

| 15 | 1200 | 2 | 47.78 | 1.15 | 0.58 |

| 20 | 1200 | 3 | 58.41 | 1.63 | 0.54 |

| 25 | 1200 | 4 | 68.25 | 2.08 | 0.52 |

| 30 | 1200 | 5 | 77.52 | 2.49 | 0.50 |

| 35 | 1200 | 6 | 86.32 | 2.89 | 0.48 |

| 40 | 1200 | 7 | 94.75 | 3.27 | 0.47 |

| Year | |||

|---|---|---|---|

| 2016 | 0.058 | 105.99% | 197.00% |

| 2015 | −0.288 | 74.95% | 185.87% |

| 2014 | 0.071 | 107.36% | 247.99% |

| 2013 | 0.077 | 107.99% | 230.99% |

| 2012 | −0.001 | 99.87% | 213.90% |

| 2011 | −0.04 | 96.08% | 214.18% |

| 2010 | 0.588 | 180.01% | 222.92% |

| 2009 | 0.059 | 106.07% | 123.84% |

| 2008 | 0.155 | 116.75% | 116.75% |

© 2020 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).

Share and Cite

Chen, H.; He, Z.; Hong, W.; Liu, J. An Assessment of Stumpage Price and the Price Index of Chinese Fir Timber Forests in Southern China Using a Hedonic Price Model. Forests 2020, 11, 436. https://doi.org/10.3390/f11040436

Chen H, He Z, Hong W, Liu J. An Assessment of Stumpage Price and the Price Index of Chinese Fir Timber Forests in Southern China Using a Hedonic Price Model. Forests. 2020; 11(4):436. https://doi.org/10.3390/f11040436

Chicago/Turabian StyleChen, Hong, Zhongsheng He, Wei Hong, and Jinfu Liu. 2020. "An Assessment of Stumpage Price and the Price Index of Chinese Fir Timber Forests in Southern China Using a Hedonic Price Model" Forests 11, no. 4: 436. https://doi.org/10.3390/f11040436

APA StyleChen, H., He, Z., Hong, W., & Liu, J. (2020). An Assessment of Stumpage Price and the Price Index of Chinese Fir Timber Forests in Southern China Using a Hedonic Price Model. Forests, 11(4), 436. https://doi.org/10.3390/f11040436