Abstract

We use a quasi-exogenous shock to information asymmetry among shareholders to evaluate the effect of information asymmetry on corporate disclosure. In the post-Regulation Fair Disclosure (FD) period, the merger between a shareholder and a lender of the same firm provides a shock to the information asymmetry among equity investors, because Regulation FD applies to shareholders but not lenders. After the merger, the shareholder gains access to the firm-specific private information held by the lender, which produces an asymmetry in the information held by shareholders. We first provide evidence that information asymmetry among shareholders indeed increases after the shareholder–lender mergers. We then use a difference-in-differences research design to show that after shareholder–lender merger transactions, firms issue more quarterly forecasts (including earnings, sales, capital expenditure, earnings before interest, taxes, amortization (EBITDA), and gross margin), and the quarterly earnings forecasts are more precise. This study provides direct empirical evidence that information asymmetry among shareholders affects corporate disclosure. Firms can address increased information asymmetry by providing more disclosures, fostering a more equitable information environment. Additionally, policymakers might consider these results when evaluating the implications of Regulation FD, particularly in the context of mergers and acquisitions (M&A) of financial institutions where a shareholder gains access to private information held by a debt holder.

JEL Codes:

G10; G20; G30; G34; M40; M41

1. Introduction

Prior empirical studies found that information asymmetry among equity investors affects firm disclosure (e.g., Coller & Yohn, 1997). However, the endogenous relation between information asymmetry and disclosure can impair inferences in studies examining the effects of information asymmetry on disclosure (e.g., Healy & Palepu, 2001; Leuz & Verrecchia, 2000; Cohen, 2003; Beyer et al., 2010). Both theory and empirical evidence suggest that information asymmetry drives demand for financial disclosure and financial disclosure reduces information asymmetry (e.g., Diamond, 1985; Verrecchia, 2001; S. Brown et al., 2004; S. Brown & Hillegeist, 2007; Shroff et al., 2013). Thus, estimating the effect of information asymmetry on disclosure is difficult because of the inherent endogenous relation between the two constructs. This study seeks to fill this gap in the literature by using a quasi-exogenous shock to information asymmetry to evaluate the effect of information asymmetry on corporate disclosure.

Information asymmetry among equity investors exists when investors are differentially informed about a firm’s value.1 For example, information asymmetry exists when one or more investors possess private information about the firm’s value while other less-informed investors have access to only public information. The prior literature documents that disclosure reduces information asymmetry among investors by either directly lowering the amount of private information relative to publicly available information or indirectly reducing private information search incentives (e.g., Diamond, 1985; Verrecchia, 2001; S. Brown & Hillegeist, 2007).2

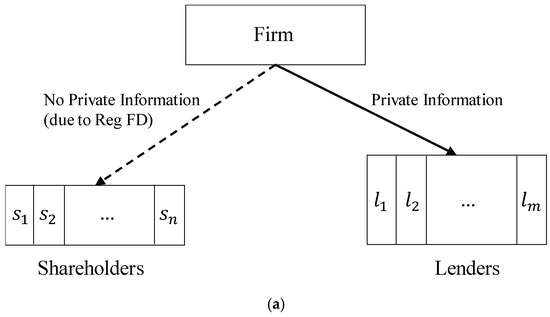

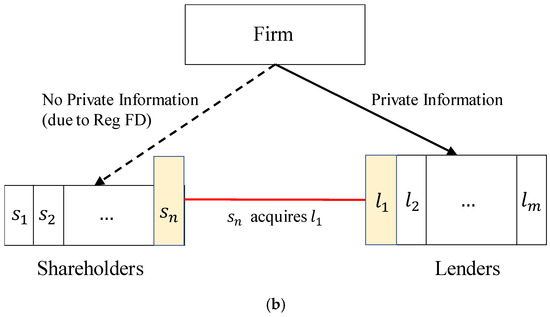

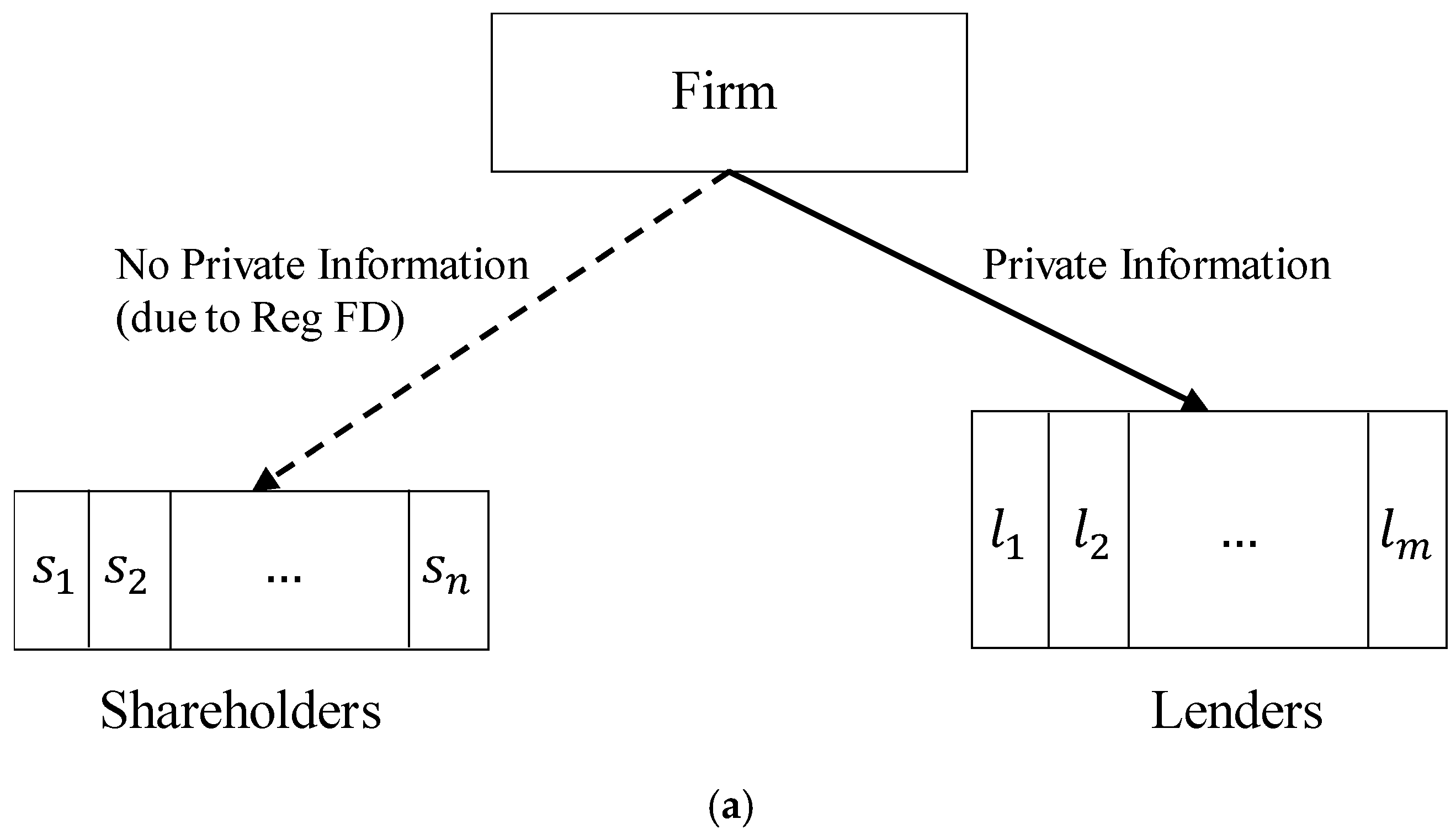

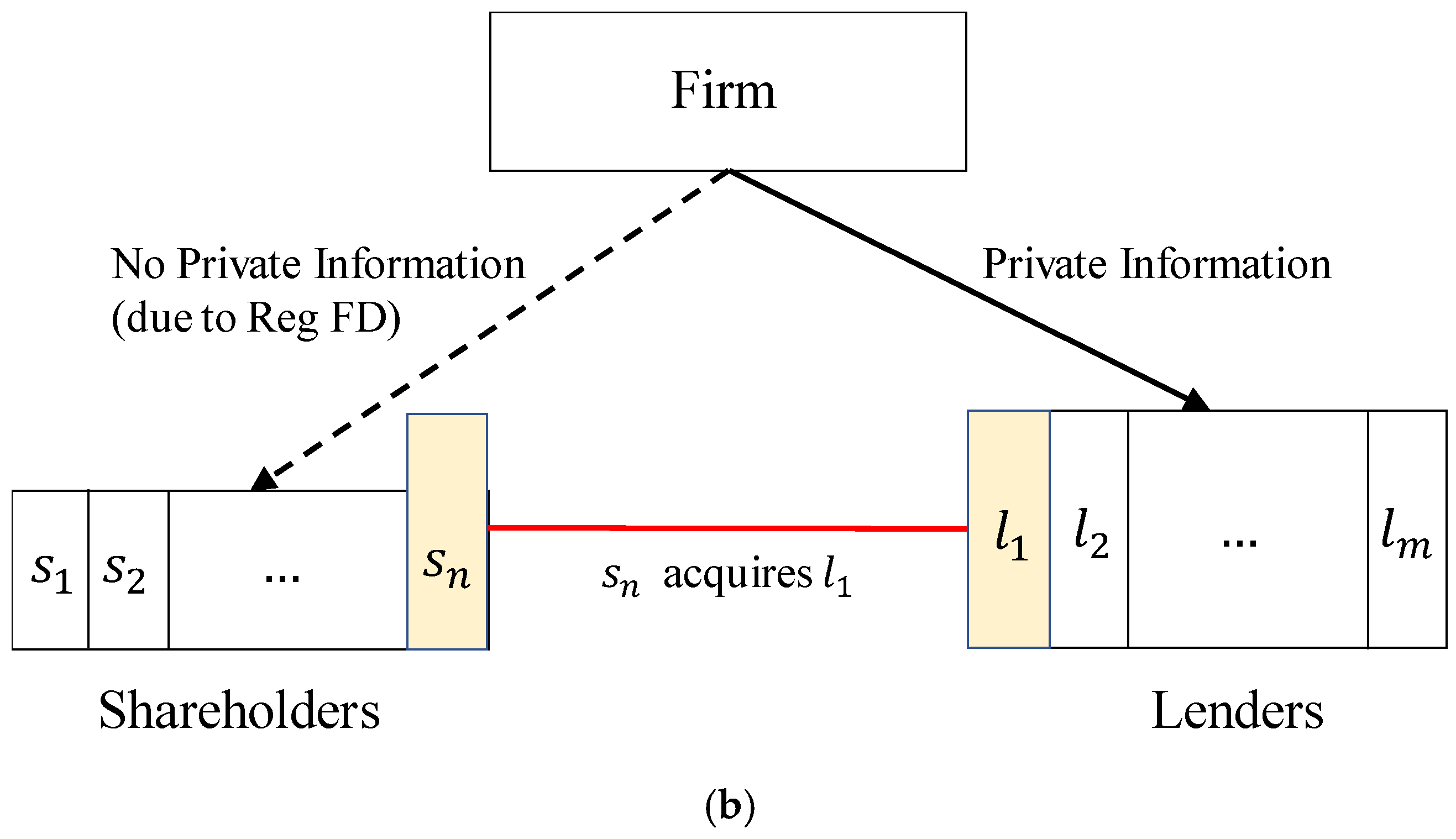

In 2000, the Securities and Exchange Commission (SEC) issued Regulation FD, which mandates that firms disclose material information to all shareholders at the same time.3 The objective of Regulation FD is to eliminate selective disclosure, where firms selectively disclose value-relevant information to certain stock market participants (including analysts and other professionals) before publicly disclosing the information. In the post-Regulation FD period, the merger between a shareholder and a lender of the same firm provides a quasi-exogenous shock to the information asymmetry among shareholders. Because Regulation FD constrains the communication of private information from managers to shareholders but not to lenders, lenders have access to private firm-specific information that is not available to shareholders.4 For example, Petacchi (2015) provides evidence that firms disclose private firm-specific information to creditors to reduce the cost of debt post-Regulation FD. The confidential information available to lenders includes timely financial disclosures, covenant compliance information, amendment and waiver requests, financial projections, and plans for acquisitions or dispositions (Standard & Poor’s, 2011). Suppose that before a shareholder–lender merger takes place, neither the shareholder nor the lender is a dual-holder of the firm, i.e., neither the shareholder nor the lender holds both equity and debt of the firm. After the merger, the acquiring shareholder gains access to the firm-specific private information held by the lender, producing a quasi-exogenous shock to the information asymmetry among shareholders (see Figure 1 for an illustration).5 Therefore, we expect that information asymmetry among equity investors increases after a shareholder of a firm acquires or merges with a lender of the same firm.

Figure 1.

Shareholder–lender merger and private information flow. Before the merger takes place, neither the shareholder nor the lender involved in the M&A transaction holds both equity and debt of the firm. Because Regulation FD applies to shareholders but not lenders, the acquiring shareholder () gains access to the firm-specific private information held by the lender () after the merger transaction, and the flow of private information leads to an increase in information asymmetry among shareholders. (a) Information held by shareholders and lenders before shareholder–lender merger. (b) Information held by shareholders and lenders after shareholder–lender merger.

To test this conjecture, we use bid–ask spread and Amihud’s (2002) illiquidity measure (AIM) as proxies for the information asymmetry among shareholders, and compare the average level of information asymmetry in the period before the announcement with the asymmetry in the period after the completion of the merger. We find that after the merger of a shareholder and a lender of the same firm, both bid–ask spreads and AIMs of treatment firms increase, relative to the changes in bid–ask spreads and AIMs of control firms. This finding is consistent with the conjecture that shareholders obtain private firm-specific information after merging with lenders, and the flow of private information leads to an increase in information asymmetry among shareholders. This evidence is also consistent with prior literature that documents private firm-specific information transfers from the loan market to the stock market (e.g., Bushman et al., 2010; Ivashina & Sun, 2011; T. Chen & Martin, 2011; Cicero et al., 2011; Massa & Rehman, 2008; Massoud et al., 2011; Sargent, 2005; Anderson, 2006).

We next examine whether firms respond to increased information asymmetry among shareholders by increasing disclosure and improving disclosure quality in order to mitigate the increase in information asymmetry. We hypothesize this relation between information asymmetry and disclosure because prior research suggests information asymmetry among shareholders negatively impacts firms’ market liquidity and cost of equity.6 Analytical models show that information asymmetry among investors can increase adverse selection risk for liquidity providers. To compensate for the increased risk, liquidity providers demand a larger risk premium and set a wider bid–ask spread, thereby reducing liquidity and raising the cost of capital (e.g., Copeland & Galai, 1983; Glosten & Milgrom, 1985; Kyle, 1985; Amihud & Mendelson, 1986; Easley & O’Hara, 2004; Hughes et al., 2007; Lambert et al., 2012). Empirical research reports similar findings (e.g., Brennan & Subrahmanyam, 1996; Easley et al., 2002; Bhattacharya et al., 2012; Armstrong et al., 2011; Akins et al., 2012).

Prior research also suggests that increasing disclosure and improving disclosure quality can mitigate the reduction in market liquidity and the increase in the cost of capital associated with elevated information asymmetry. Classic disclosure models show that a greater level of corporate disclosure mitigates information asymmetry among market participants, increases market liquidity, and, as a result, reduces the cost of capital (e.g., Diamond, 1985; Diamond & Verrecchia, 1991). Extensive empirical studies document evidence consistent with these predictions (Welker, 1995; Coller & Yohn, 1997; Leuz & Verrecchia, 2000; Heflin et al., 2005; S. Brown et al., 2004; Botosan & Plumlee, 2002; Shroff et al., 2013; see Healy & Palepu, 2001; Beyer et al., 2010; and Leuz & Wysocki, 2016 for reviews). For instance, Shroff et al. (2013) use the Securities Offering Reform enacted in 2005, which allows firms to more freely disclose information before equity offerings, as an exogenous shock to voluntary disclosure, and find greater disclosure is associated with a decrease in information asymmetry and a reduction in firms’ cost of capital. This study complements Shroff et al. (2013) by examining a quasi-exogenous shock to information asymmetry and its effect on disclosure. We predict that firms increase disclosure and improve disclosure quality to mitigate the negative effects of increased information asymmetry among shareholders following shareholder–lender mergers.

We adopt a difference-in-differences design to test the prediction. We employ two proxies for disclosure: (1) the number of quarterly management forecasts (including earnings, sales, capital expenditure, EBITDA, and gross margin), and (2) the precision of quarterly management earnings forecasts. Using the difference-in-differences design, we compare the two disclosure proxies for treatment firms and control firms matched on size and book-to-market in the period before the announcement and the period after the completion of the merger transactions.

Consistent with the hypothesis, we find that relative to control firms, treatment firms issue more quarterly forecasts and more precise earnings forecasts after the merger transactions. These results suggest that firms increase disclosure and improve disclosure quality after the mergers in response to increased information asymmetry. This is consistent with prior research that suggests disclosure is an effective channel for mitigating the level of information asymmetry among equity investors (e.g., Diamond, 1985; Diamond & Verrecchia, 1991; Coller & Yohn, 1997; Healy et al., 1999; Leuz & Verrecchia, 2000; Heflin et al., 2005; S. Brown et al., 2004; S. Brown & Hillegeist, 2007; Fu et al., 2012; Shroff et al., 2013). In sum, the findings provide evidence that a quasi-exogenous increase in information asymmetry among shareholders leads to an increase in corporate disclosure and disclosure quality.

This study makes several contributions to the literature. First, this study uses a quasi-exogenous shock to information asymmetry among shareholders to provide direct evidence that information asymmetry affects corporate disclosure. The endogenous nature of the relation between information asymmetry and disclosure makes it difficult to estimate the impact of information asymmetry on disclosure. This study also contributes to the literature documenting that financial reporting and disclosure are shaped by feedback effects from the stock market (e.g., Badertscher, 2011; Sletten, 2012; Li & Zhang, 2015; Zuo, 2016). Additionally, this study contributes to the growing literature that explores the impact of financial institutions’ mergers on firm policies (e.g., Chu, 2017; Q. Chen & Vashishtha, 2017).

The findings of this study also have implications for regulators. We highlight how debt holders, who often gain access to private, nonpublic information through their unique position, can indirectly transmit this information to shareholders during mergers and acquisitions. Unlike the information disclosure requirements imposed by Regulation FD, the private information held by debt holders falls outside its scope. This creates opportunities for selective information sharing, potentially undermining market fairness and transparency. Therefore, addressing this gap in the regulatory framework is crucial for promoting a level playing field and safeguarding the integrity of the marketplace.

Significant concerns have been raised about the extent to which institutional investors exploit the confidential information obtained from the loan market to engage in insider trading in the stock market (e.g., Sargent, 2005; Anderson, 2006; Bushman et al., 2010; Standard & Poor’s, 2011; Ivashina & Sun, 2011). Recently, the SEC has tightened private information flows from firms to outsiders. On 4 October 2010, the SEC enacted a Regulation FD amendment to remove the specific exemption from the rule for disclosures made to nationally recognized statistical rating organizations and credit rating agencies.7 The results of this study suggest that one way shareholders can gain access to private firm-specific information is by merging with one of the firm’s lenders. These results are relevant to the SEC given its objective to create a level playing field for all investors in accessing material corporate information.

2. Literature Review and Hypothesis Development

There is a large stream of literature documenting the relationship between M&A activity and information asymmetry, either between targets and acquirers or between firm managers and investors (e.g., Draper & Paudyal, 2008; Officer et al., 2009; Raman et al., 2013; Jansen, 2020; Song et al., 2021). Another stream of research examines the relationship between M&A and firm disclosure practices (e.g., Ge & Lennox, 2011; Erickson et al., 2012; Ahern & Sosyura, 2014; Goodman et al., 2014; Amel-Zadeh & Meeks, 2019). For example, Ahern and Sosyura (2014) demonstrate that acquirers significantly increase their disclosure during the period between the initiation of merger negotiations and the public announcement. In this study, we focus on mergers between a firm’s shareholders and its lenders. Specifically, we investigate whether shareholder–lender merger transactions lead to an increase in information asymmetry among investors and whether managers increase disclosure to mitigate the resulting information asymmetry among shareholders.

2.1. Information Flows from Lenders to Shareholders

A large body of empirical literature examines whether Regulation FD facilitates equal access to information among investors (e.g., Bushee et al., 2004; Chiyachantana et al., 2004; Wang, 2007; Ke et al., 2008; Bhojraj et al., 2012). Overall, the findings suggest that Regulation FD reduces selective disclosure and the information advantage of certain investors, and creates a more level playing field (see Koch et al., 2013 for a review of the literature on Regulation FD). Thus, the passage of Regulation FD reduced the use of firm-provided private information in equity market investment decisions and increased investors’ use of public information.

Importantly, however, the provisions of Regulation FD do not apply to credit providers, as firms are still allowed to selectively disclose private information to lenders. Thus, lenders have access to private firm-specific information that is not available to equity investors. This is important because loan contracts are typically designed according to confidential information between lenders and borrowers (e.g., Diamond, 1984; Fama, 1985), and loan covenants often obligate borrowers to provide timely covenant reports to lenders, which are likely to preempt public disclosures in upcoming quarterly earnings releases. In other words, the origination and ongoing maintenance of loan contracts rely on firms providing lenders with confidential private information (e.g., Dennis & Mullineaux, 2000; Sufi, 2007). Unless the information provided by the borrower to its lenders is already publicly available, it is protected by a confidentiality agreement and not subject to Regulation FD. According to Standard & Poor’s (2011), lenders typically have access to borrowers’ timely financial disclosures, covenant compliance information, amendment and waiver requests, financial projections, and plans for acquisitions or dispositions. In addition, to efficiently monitor borrowers, lenders often set fairly tight financial covenants (e.g., Dennis & Mullineaux, 2000; Sufi, 2007). Borrowers facing challenges that could lead to the violation of loan terms need to disclose these issues to their lenders (Anderson, 2006); borrowers considering refinancing debt or securing financing for a business transaction need to share their intentions with lenders. Overall, the prior literature provides strong evidence that the private information conveyed in loan markets is timely and material (e.g., Bushman et al., 2010; Ivashina & Sun, 2011).

Similar to brokerage mergers (e.g., Hong & Kacperczyk, 2010), the mergers and acquisitions of financial institutions (banks, asset management firms, etc.) have been used as a natural experiment in finance and accounting studies (e.g., Huang, 2013, 2016; Chu, 2017; H. Yang, 2017; Q. Chen & Vashishtha, 2017). In particular, Chu (2017) and H. Yang (2017) focus on the unique setting where the financial institutions involved in an M&A transaction are a shareholder and a lender of the same firm. These studies use the shareholder–lender merger as a shock to a firm’s shareholder–creditor conflicts. Relatedly, He and Huang (2017) use financial institution mergers to examine the effects of institutional cross-ownership of same-industry firms on product market performance and behavior. Peyravan (2020) documents that the financial reporting quality of a firm influences the propensity of institutional investors to simultaneously hold the firm’s debt and equity. Lewellen and Lowry (2021) leverage financial institution mergers to investigate the impact of common ownership on firm cooperation and competition. Peyravan and Wittenberg-Moerman (2022) investigate how institutional investors that simultaneously invest in a firm’s debt and equity influence the firm’s voluntary disclosure. In this study, we use the shareholder–lender merger as a shock to the information asymmetry among equity investors, since the acquiring shareholder gains access to the firm-specific private information held by the lender.

There are two ways a shareholder obtains private firm-specific information after merging with a lender of the same firm. First, the shareholder gains access to the lender’s private information received before the completion date of a proposed merger transaction. In the merger process, the acquiring shareholder evaluates the quality of loans held by the lender, and likely acquires much of the private information held by the lender. The shareholder can use this private information to help complete the mosaic of information about the firm in which they hold an equity interest. In other words, the information the shareholder obtains can become useful within the context of other information the shareholder already possesses. In their survey, L. D. Brown et al. (2015) find that “private communication with management is a more useful input to analysts’ earnings forecasts and stock recommendations than their own primary research, recent earnings performance, and recent 10-K and 10-Q reports,” because analysts can get nonpublic information from private communication with management and incorporate this information into a broader information set used to form judgement about the firm. In addition, the acquiring shareholder can exploit the obtained private information to better interpret new public information released in the future.

Second, the shareholder becomes a dual-holder of the firm after the merger and has access to timely private firm-specific information, and thus can trade on the confidential information. Although financial institutions are legally required to have a “wall” in place to prevent equity trading based on private information obtained in the loan market, both the media and academic studies have documented evidence suggesting within-firm information flow from lenders to equity holders. For example, in 2006, a front-page article in the New York Times reported evidence suggesting this type of information flow. Movie Gallery, the second largest US movie and game rental company, held a confidential conference call with its lenders in which it discussed its financial results and desired to amend its credit agreement in order to avoid covenant violation. The information released in the conference call was private information, and Movie Gallery did not issue any public news release. However, Movie Gallery’s stock price dropped by 25% in the two days following the conference call.

In addition, prior research documents private information transfers from loan market participants to stock market participants. For example, Bushman et al. (2010) find the flow of confidential information to loan syndicate participants is “sufficiently pervasive to significantly affect the speed of stock price discovery during regular earnings cycles”. They find the access to private information in the loan market accelerates the speed of information arrival in stock prices. They document a positive relation between institutional lending and the speed of stock price discovery, and the relation is more pronounced in relatively weak public disclosure environments. They also provide evidence that financial covenants, especially earnings-based covenants, prompt borrowers to provide timely private information to lenders. Addoum and Murfin (2020) examine the speed with which private information flows from the syndicated loan market to the equity market, and document that a long-short strategy that buys (sells) the equities of firms with recently appreciated (depreciated) loans earns large risk-adjusted returns. Kumar et al. (2020) find evidence that certain hedge funds obtain private information from their prime broker banks about the banks’ corporate borrowers.

More direct evidence of within-firm information flow is provided by Ivashina and Sun (2011), who find that institutional investors use private information obtained from lending relationships to trade stocks. They show that institutional participants in loan renegotiations subsequently trade stocks of the borrowing firm and outperform other investors. Chen and Martin (2011) and Cicero et al. (2011) document that bank-affiliated analysts issue more accurate forecasts after the followed firm borrows from the affiliated bank, suggesting information flows from the loan division to the equity research division within a bank. In addition, Massa and Rehman (2008) document that information flow occurs between mutual funds and banks that belong to the same financial group. They find that mutual funds increase (decrease) their stock holdings in the firms that borrow from their affiliated banks, and the firms subsequently have positive (negative) abnormal returns, suggesting mutual funds exploit private information not available to other market participants. Massoud et al. (2011) find evidence that hedge funds make profits in equity markets by lending to firms in order to gain access to private information.8 In summary, there is considerable evidence suggesting that within a financial institution, equity holders have access to private information held by lenders. Thus, we state the first hypothesis as follows:

H1:

Information asymmetry among firm shareholders increases after a shareholder and a lender of the same firm merge, where the lender and the shareholder are not dual-holders before the merger.

2.2. Information Asymmetry and Voluntary Disclosure

In this study, we focus on the information asymmetry among investors, rather than the information asymmetry between firm managers and outsider investors. Information asymmetry among investors has been a long-standing concern to regulators and has received considerable attention in the literature. Information asymmetry among shareholders exists when investors are differentially informed about a firm’s value. A common scenario that creates information asymmetry is when one or more investors possess private information about the firm’s value while other less-informed investors have access to only public information. Agarwal and O’Hara (2007) define the information asymmetry among investors as extrinsic because it indicates heterogeneity across investors’ information sets; they define the information asymmetry between firm managers and outside investors as intrinsic because firm managers have better information than outsiders and this is intrinsic to the firm. Prior studies typically use stock market data, such as bid–ask spreads, to proxy for extrinsic information asymmetry; studies often use the market reactions to important firm-specific events to proxy for intrinsic information asymmetry (e.g., Dierkens, 1991; Agarwal & O’Hara, 2007), as larger market reactions imply greater information gaps between firm managers and outside investors.

Prior research finds that information asymmetry among shareholders is negatively related to market liquidity and positively related to the cost of capital. Analytical studies show that information asymmetry among shareholders increases the adverse selection risk for liquidity providers. To compensate for the increase in risk, liquidity providers demand a larger risk premium and set a wider bid–ask spread, thereby lowering liquidity and raising the cost of capital (e.g., Glosten & Milgrom, 1985; Kyle, 1985; Easley & O’Hara, 2004; Lambert et al., 2012). Numerous empirical studies document that an increased level of information asymmetry negatively affects the cost of capital (e.g., Brennan & Subrahmanyam, 1996; Easley et al., 2002; Bhattacharya et al., 2012; Armstrong et al., 2011; Akins et al., 2012). Brennan and Subrahmanyam (1996) find a negative relation between required rates of return and measures of liquidity after adjusting for the Fama and French three risk factors (Fama & French, 1992). Easley et al. (2002) provide evidence that the level of information asymmetry is positively associated with firms’ cost of capital, i.e., information asymmetry is priced in the cross-section. More recently, Kelly and Ljungqvist (2012) provide evidence that information asymmetry has a substantial effect on asset prices and that a primary channel that links information asymmetry to prices is liquidity. Bhattacharya et al. (2012) document that earnings quality affects the cost of capital indirectly through its effect on information asymmetry. Armstrong et al. (2011) and Akins et al. (2012) both find that information asymmetry has a positive relation with firms’ cost of capital in excess of standard risk factors when markets are imperfectly competitive. In summary, extant research indicates increases in information asymmetry are accompanied by decreases in market liquidity and increases in the cost of capital.

One potential way firms can mitigate the negative effects of increased information asymmetry is by increasing disclosure and improving disclosure quality.9 Prior literature examines the relation between the level of disclosure or disclosure quality and firm characteristics, including information asymmetry, liquidity, and the cost of capital. Classic disclosure models show that disclosure mitigates the information asymmetry among market participants, increases market liquidity, and, as a result, reduces the cost of capital (e.g., Diamond, 1985; Diamond & Verrecchia, 1991). Lev (1988) also argues that disclosing financial information can decrease information asymmetry among investors, improve liquidity, and decrease the cost of capital. Many empirical studies document evidence consistent with the predictions of analytical research (see Healy & Palepu, 2001; Beyer et al., 2010; Leuz & Wysocki, 2016 for reviews). Welker (1995), Greenstein and Sami (1994), and Coller and Yohn (1997) find a negative association between disclosure and bid–ask spreads. Healy et al. (1999) document a positive relation between expanded disclosure (using AIMR scores) and capital market benefits, including improved liquidity and greater analyst following. Leuz and Verrecchia (2000) show that the improved disclosure standards for a sample of German firms are associated with lower bid–ask spreads. Heflin et al. (2005) provide evidence that enhanced financial disclosure is related to improved market liquidity and lower information asymmetry. S. Brown et al. (2004) and S. Brown and Hillegeist (2007) also find that financial disclosures mitigate information asymmetry among equity investors. Botosan (1997) and Botosan and Plumlee (2002) suggest a negative relation between disclosure and the cost of capital. More recently, using data on firms’ reporting frequency from 1951 to 1973, Fu et al. (2012) provide evidence that increased financial reporting frequency reduces information asymmetry and the cost of capital. Shroff et al. (2013) document that an increase in voluntary disclosure as a result of the 2005 Securities Offering Reform led to a decrease in information asymmetry and a reduction in firms’ cost of capital.

Therefore, if the information asymmetry among a firm’s shareholders increases after a shareholder–lender merger transaction, the firm has incentives to increase disclosure and improve disclosure quality to mitigate the increased level of information asymmetry. This reasoning leads to the second hypothesis, stated as follows:

H2:

A firm increases disclosure and improves disclosure quality after the merger between a shareholder and a lender of the same firm in order to mitigate the increased information asymmetry among shareholders resulting from the merger.

In a related study, Balakrishnan et al. (2014) use the closures and mergers of brokerage houses’ research operations as plausibly exogenous shocks to liquidity and find that firms respond to the resulting liquidity shocks by increasing disclosure.10 However, Balakrishnan et al. (2014) do not distinguish whether the shock to liquidity is due to an increase in the information asymmetry among investors or the deterioration of firm’s overall information environment. Empirical evidences from tests of our hypotheses complement Balakrishnan et al. (2014) in that they speak to whether information asymmetry among shareholders affects corporate disclosures.

3. Research Design

3.1. Information Asymmetry and Shareholder–Lender Merger Transactions

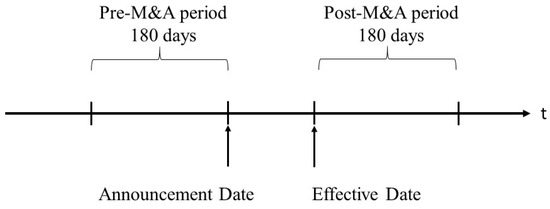

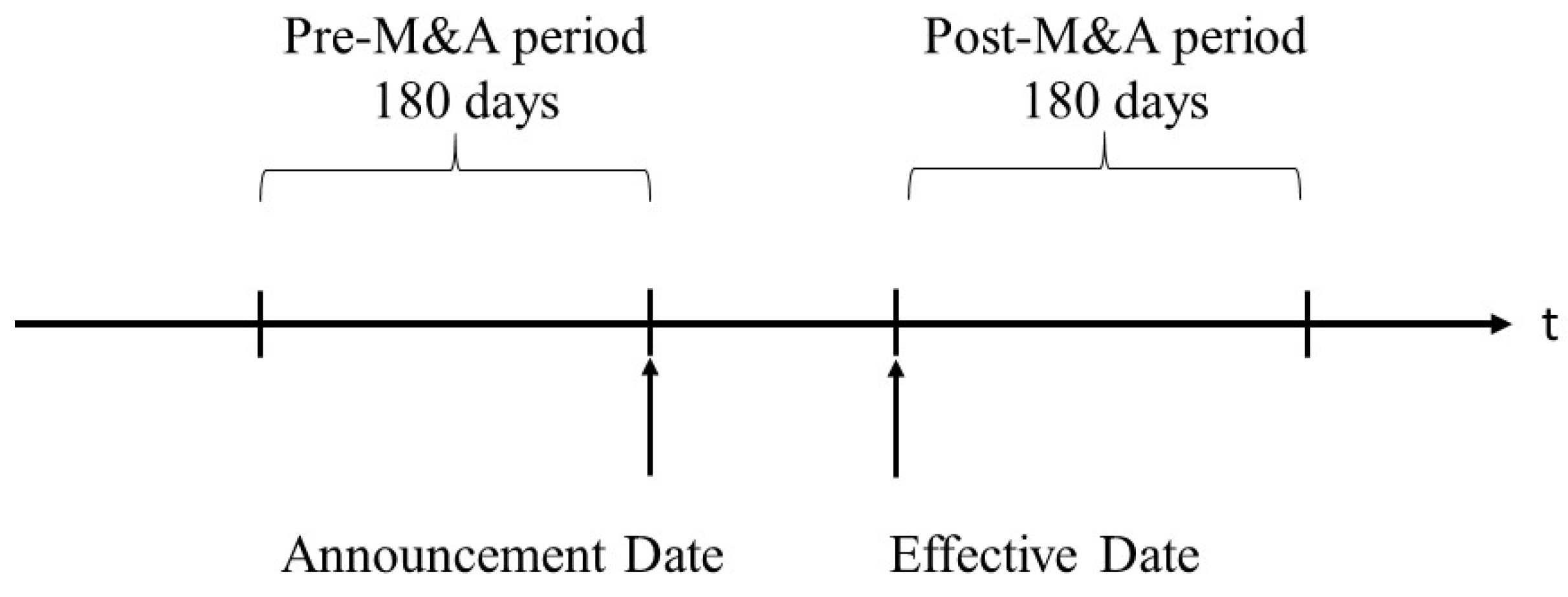

We begin the empirical analysis by examining whether information asymmetry increases after a shareholder acquires a lender of the same firm. Consistent with prior literature (e.g., Brennan & Subrahmanyam, 1996; Armstrong et al., 2011; Heflin et al., 2005; Balakrishnan et al., 2014), we use bid–ask spread and Amihud’s (2002) illiquidity measure (AIM) as proxies for information asymmetry among equity investors. To construct the bid–ask spread, we scale the daily bid–ask spread by the mid-point of bid and ask prices. To calculate the AIM, we follow Amihud (2002) by taking the natural log of one plus the ratio of daily absolute return and dollar volume. Both bid–ask spreads and AIMs are averaged over a 180-day window. We compare the level of information asymmetry over the 180-day window before the merger announcement date and the 180-day window after the merger effective date, as illustrated in Figure 2.11 To control for time-specific effects, we adopt a difference-in-differences research design where the control observations for each treatment observation consist of ten Compustat observations in the same size and book-to-market quintile but that do not experience a shareholder–lender merger during the same time period.12 We require control observations to have the data required to compute the regression variables. In cases where more than ten control observations are available, we choose ten observations that are closest in size to the corresponding treatment observation. We examine the effect of the shareholder–lender merger by estimating the following OLS regression:

where i and t denote firm and time, respectively. IA indicates either Spread or AIM. Spread is the bid–ask spread averaged over a 180-day window, and AIM is Amihud’s (2002) illiquidity measure averaged over a 180-day window. Post is an indicator variable set to one for observations after the shareholder–lender merger transactions, and zero otherwise. Treat is an indicator variable equal to one for treatment firms, and zero otherwise. We predict the coefficient on Post*Treat () is positive, consistent with an increase in information asymmetry following the merger transactions. Equation (1) also includes several control variables used in prior studies to capture aspects of firms’ information environments (e.g., M. H. Lang & Lundholm, 2000; Bushee et al., 2010; Shroff et al., 2013). These controls include the natural logarithm of the market value of equity (LnSize), market-to-book ratio (MTB), return on assets (ROA), and the percentage of firms’ shares owned by institutional investors (PerctInst). LnSize, MTB, and ROA are each measured at the fiscal year-end immediately preceding the announcement of the shareholder–lender merger transactions. PerctInst is measured at the quarter-end immediately preceding the announcement of the mergers. Equation (1) also includes as a control variable the natural logarithm of one plus the number of analysts covering the firm during a 365-day window preceding the announcement of the mergers (LnNumAF). Additionally, we include shareholder–lender merger fixed effect in Equation (1).13 Appendix A provides precise variable definitions.

Figure 2.

Timeline of a shareholder–lender merger transaction. The pre-merger period is a 180-day window before the merger announcement date, and the post-merger period is a 180-day window after the merger effective date. We compare the information asymmetry and disclosure in the pre-M&A period with these in the post-M&A period. We use bid–ask spread and AIM as proxies for information asymmetry among equity investors. We use the number of quarterly management forecasts (including earnings, sales, capital expenditure, EBITDA, and gross margin) as the proxy for the level of disclosure and the precision of quarterly management earnings forecasts as the proxy for disclosure quality. See Appendix A for detailed variable definitions.

3.2. Disclosure and Shareholder–Lender Merger Transactions

To test whether firms increase disclosure and improve disclosure quality in the post-merger period, we examine two proxies for disclosure: (1) the number of quarterly management forecasts (including forecasts of earnings, sales, capital expenditure, EBITDA, and gross margin); and (2) the precision of quarterly management earnings forecasts. A convenient way for firms to enhance disclosure is by supplementing earnings forecasts with verifiable forward-looking information, such as forecasts of sales and gross margin; prior research finds that these supplemental forecasts make earnings forecasts more informative (e.g., Hutton et al., 2003). We focus on quarterly forecasts because research shows that quarterly forecasts are more accurate than annual forecasts, and forecasts that are more accurate are more informative and have a larger impact on the stock market (e.g., Pownall et al., 1993; Hirst et al., 2008). Using the number of quarterly management forecasts issued during a 180-day window to proxy for the level of disclosure, we compare the level of disclosure before the merger announcement date with the level of disclosure after the merger effective date, as illustrated in Figure 2. Similar to the information asymmetry analysis in Section 3.1, we adopt a difference-in-differences research design to control for time-specific effects, and use a control group of observations in the same size and book-to-market quintile as the treatment observation but that do not experience a shareholder–lender merger during the same time period. Specifically, we estimate the following OLS regression:

where i and t denote firm and time, respectively. Frequency indicates the natural logarithm of one plus the number of quarterly management forecasts issued in a 180-day window. The coefficient on Post*Treat () is predicted to be positive, i.e., firms issue more forecasts after the shareholder–lender merger transactions.

We also examine the effects of shareholder–lender mergers on forecast precision, a widely used measure for disclosure quality (e.g., Rogers & Stocken, 2005; Cheng et al., 2013; Li & Zhang, 2015; Hirst et al., 2008). Again, we use a difference-in-differences research design, and compare the forecast precision of quarterly management earnings forecasts issued in the 180-day window before and after merger transactions by estimating the following regression:

where i and t denote firm and time, respectively. Precision is the forecast precision associated with the quarterly management earnings forecast, measured as the negative of the forecast width (the magnitude of the range for range forecasts and zero for point forecasts), scaled by the beginning-of-quarter stock price. Post*Treat () captures the incremental effect of Post and Treat beyond their individual effects on management forecast precision. Post*Treat is the variable of interest in Equation (3), and the coefficient on this variable is predicted to be positive, consistent with treatment firms issuing more precise earnings forecasts relative to control firms after a shareholder–lender merger. We also include the following control variables to capture the characteristics of management earnings forecasts. LnHorizon is the natural logarithm of one plus the number of days between management earnings forecasts and forecast period end date. LnPRC indicates the natural logarithm of the beginning-of-quarter stock price. Point is an indicator variable set to one for a point estimate, and zero otherwise. Loss is an indicator variable equal to one if a management earnings forecast is negative, and zero otherwise. We exclude earnings preannouncement (i.e., management earnings forecasts issued after the forecast period end date), as prior literature suggests that earnings preannouncements are often used by firms to avoid negative earnings announcement surprises (e.g., Soffer et al., 2000; Hirst et al., 2008).

4. Empirical Analyses

4.1. Sample and Descriptive Statistics

The sample selection process for treatment observations begins with identifying all mergers and acquisitions (M&A) between financial firms with primary SIC codes in the range 6000 to 6999. A treatment observation is a firm with a shareholder that acquires one of its lenders. We exclude M&A transactions before 2005 due to several major economic events that affected the information environment and firms’ bid–ask spreads and AIMs.14 We end the sample in 2016 because (i) we need a 6-month window after merger transactions for the investigation and (ii) two regulations that could confound our analysis came into effect in early 2018.15 We obtained M&A transactions from the Securities Data Company (SDC) Platinum database, lenders’ information from the LPC DealScan database, and institutional investors’ (shareholders) information from Thomson Reuter’s 13F database. To ensure acquiring shareholders have a measurable impact on stock liquidity and information asymmetry, we follow Jiang et al. (2010) and require that shareholders have significant equity holdings, defined as exceeding either 1% of the firm’s outstanding shares or USD 2 million in 2009 constant dollars.

We manually examined each M&A transaction to ensure that it meets the following criteria: (1) it is between two financial firms with primary SIC codes in the range 6000 to 6999; (2) it consists of an institutional investor acquiring a lender of the same firm; (3) the acquiring institutional investors have significant equity holdings of the firm at the end of the quarter immediately before the M&A announcement date, and target lenders hold loans of the same firm that were initiated before the M&A announcement date and do not expire before the M&A effective date; (4) the acquiring institutional investor and target lender are not controlled by the same parent firm before the M&A transaction; and (5) neither acquiring institutional investor nor target lender is a dual-holder of the firm (i.e., shareholder and lender) before the M&A transaction. We matched both acquirers and acquirers’ parents in SDC’s M&A transactions with shareholder observations in Thomson Reuters’ 13F database under the assumption that if a subsidiary firm gains access to private information, its parent firm also gains access to the information.

Bid–ask spreads, stock returns, trading volumes, and prices come from CRSP, and financial information comes from Compustat. We require that all observations have the necessary Compustat/CRSP data to derive the regression variables discussed in Section 3. This procedure leads to a final treatment sample of 531 firm-years (i.e., there are 531 firm-year observations where a shareholder of a firm acquires a lender of the same firm subject to the requirements above) and a control sample of 4824 firm-years. We obtained management forecasts and analyst forecasts from I/B/E/S. In tests of H2, to avoid the impact of sporadic observations, we require each treatment and control firm to have at least one quarterly management forecast (including earnings, sales, capital expenditure, EBITDA, and gross margin) both in the 365-day period preceding the announcement date of merger transactions and in the 365-day period post the effective date of merger transactions. We also require each treatment and control firm to have at least ten quarterly management forecast observations in I/B/E/S from 2005 to 2016.

Table 1, Panel A illustrates the number of treatment observations by year from 2005 to 2016. As expected, 483 firm-years (approximately 91% of the sample) are observed in 2008 and 2009, as the 2008 financial crisis led to a wave of M&A among financial institutions. During crisis periods, the impact of information asymmetry on disclosure is expected to be more pronounced, because managers have stronger incentives to mitigate elevated information asymmetry resulting from private information transfer. There is no observation in 2012, 2013, and 2014. Table 1, Panel B shows the distribution of the treatment sample across industries as defined in Fama and French (1997) and indicates that observations are not concentrated in any specific industry. The three industries with the most observations are Other (71, 13.37%), Finance (68, 12.81%), and Manufacturing (67, 12.62%); the three industries with the least observations are Consumer Durables (16, 3.01%), Chemicals (22, 4.14%), and Telecom (26, 4.90%).

Table 1.

Distribution of the Sample.

Table 2, Panel A reports descriptive statistics for treatment firms’ bid–ask spread (Spread), Amihud’s (2002) illiquidity measure (AIM), number of analyst forecasts (LnNumAF), market value of equity (LnSize), return on asset (ROA), market-to-book ratio (MTB), the percentage of firms’ shares owned by institutional investors (PerctInst), number of quarterly management forecasts (Frequency), quarter-end stock price (LnPRC), and characteristics of quarterly management earnings forecasts (Precision, LnHorizon, Point, and Loss); all variables are measured prior to the shareholder–lender merger transactions. Specifically, the mean (median) value of LnSize is 8.391 (8.341), the mean (median) value of Spread is 0.160 (0.128), and the mean (median) value of AIM is 0.022 (0.005). Panel B of Table 2 reports descriptive statistics for the control observations. Overall, the control firms exhibit similar characteristics to the treatment firms. For example, the mean (median) value of LnSize is 8.297 (8.283), the mean (median) value of Spread is 0.156 (0.134), and the mean (median) value of AIM is 0.017 (0.005).

Table 2.

Summary statistics of variables.

4.2. Information Asymmetry and Shareholder–Lender Merger Transactions (H1)

Before examining the impact of information asymmetry on corporate disclosure, we first examine whether shareholder–lender mergers produce a shock to the level of information asymmetry among shareholders (H1). Table 3 presents the results from regressing Equation (1) using Spread and AIM as the dependent variable. Column (1) shows the results of comparing Spread before and after shareholder–lender merger transactions. The coefficient for Post*Treat is positive and significant at the 5% level (coef = 0.022, t-statistic = 2.55), indicating the bid–ask spreads are higher after the shareholder–lender merger transactions. For a treatment firm with a stock price of USD 100, the estimated coefficient indicates that as compared to the control firms, the treatment firms’ bid–ask spreads increase by an additional USD .022 (0.022*100/100). This finding is consistent with the notion that after a shareholder–lender merger, the acquiring shareholder gains access to private firm-specific information from the lender, and this access to private information increases information asymmetry among shareholders (e.g., Ivashina & Sun, 2011; Massa & Rehman, 2008; T. Chen & Martin, 2011). The signs of the coefficients on the control variables are consistent with prior studies. For example, the coefficient on LnSize is negative and significant (coef = −0.03, t-statistic = −21.02), consistent with larger firms having higher liquidity. The coefficient on ROA is negative and significant (coef = −0.265, t-statistic = −16.07), suggesting firms with good performance have better liquidity. The coefficient on PerctInst is negative and significant (coef = −0.054, t-statistic = −13.30), consistent with institutional investors reducing information asymmetry and enhancing liquidity (e.g., Gompers & Metrick, 2001; Blume & Keim, 2012).

Table 3.

Information asymmetry and shareholder–lender mergers.

Column (2) of Table 3 reports the results from estimating Equation (1) using AIM as the dependent variable. The coefficient on Post*Treat is positive and significant at the 1% level (coef = 0.014, t-statistic = 2.65), suggesting AIM increases after the merger transactions. The estimated coefficient indicates that compared with control firms, the average treatment firm’s AIM increases by 0.014 after the shareholder–lender merger transactions. The coefficient estimates on control variables are as predicted by prior literature. For example, the coefficients on LnSize, ROA, and PerctInst are all negative and significant. Overall, the results in Table 3 suggest that as a result of a shareholder–lender merger, the acquiring shareholder obtains private firm-specific information from the lender, and this flow of private information leads to an increase in the level of information asymmetry among shareholders.

4.3. Disclosure and Shareholder–Lender Merger Transactions (H2)

Having found that information asymmetry increases after shareholder–lender merger transactions, we next examine whether firms increase disclosure and improve disclosure quality in order to mitigate the increased level of information asymmetry among investors. We first consider the frequency of forecasts and examine the number of quarterly management forecasts before and after the merger transactions. Column (1) of Table 4 presents the results from estimating Equation (2) and shows the results of comparing the number of management forecasts over a 180-day window before and after shareholder–lender merger transactions. The coefficient on Post*Treat is positive and significant (coef = 0.102, t-statistic = 1.93), indicating that treatment firms issue more forecasts after the shareholder–lender merger transactions. This result suggests firms increase voluntary disclosure in response to the increased level of information asymmetry. The coefficients on control variables are consistent with findings in prior literature. For example, the coefficient on LnNumAF is positive and significant, indicating the number of analyst forecasts covering a firm is higher for firms that provide more management forecasts (e.g., Graham et al., 2005; Cotter et al., 2006; Wang, 2007). The coefficient on ROA is also positive and significant, suggesting firms with better performance tend to issue more forecasts. In summary, column (1) of Table 4 provides evidence that after shareholder–lender mergers, firms increase disclosure to reduce the level of information asymmetry among shareholders. This finding is consistent with prior literature that suggests disclosing financial information can decrease information asymmetry across investors and improve liquidity (e.g., Diamond, 1985; Welker, 1995; Coller & Yohn, 1997; S. Brown et al., 2004; Fu et al., 2012; Shroff et al., 2013).

Table 4.

Disclosure and shareholder–lender mergers.

Next, we investigate whether managers provide more precise earnings forecasts following the merger transactions by estimating Equation (3). Column (2) of Table 4 presents the results of comparing the precision of quarterly management earnings forecasts before and after shareholder–lender merger transactions. Post indicates the effect of shareholder–lender mergers on forecast precision, Treat represents the difference in precision between treatment and control firm-years, and the coefficient on Post*Treat is the variable of interest, capturing the incremental effect of Post and Treat beyond their individual effects on forecast precision. The results show that the coefficient on Post*Treat is positive and significant at the 1% level (coef = 0.104, t-statistic = 2.91), indicating that firms issue more precise earnings forecasts after the merger transactions. The magnitude of the coefficient on Post*Treat suggests that for a treatment firm with a stock price of USD 25, the firm’s earnings forecast is USD .026 (0.104*25/100)—more precise after the merger transaction, compared with its control firms. This result provides evidence that firms enhance their disclosure quality by issuing more precise management earnings forecasts in the wake of the shareholder–lender merger transactions. As in the other tests, the coefficients on control variables are consistent with the prior literature. For example, the coefficient on ROA is positive and significant, indicating firms with better performance issue more precise earnings forecasts. The coefficient on LnHorizon is negative and significant, consistent with forecast precision decreases in horizon. The coefficient on Loss is negative and significant, indicating earnings forecasts are less precise in loss quarters. Overall, the results in column (2) suggest firms enhance disclosure quality to reduce information asymmetry after the shareholder–lender merger transactions. These results provide additional support to the findings in the prior literature that enhanced disclosure quality can mitigate the negative effects of increased information asymmetry (e.g., Healy et al., 1999; Leuz & Verrecchia, 2000; Heflin et al., 2005; Beyer et al., 2010).

Our findings carry significant implications for managers, investors, and regulators. The empirical results indicate that information asymmetry among investors rises following shareholder–lender merger transactions. Given the adverse consequences linked to heightened information asymmetry, managers and market participants must remain vigilant to address these challenges. Our results also highlight the potential for managers to mitigate the negative impacts of increased information asymmetry through enhanced disclosure practices. Additionally, our study offers critical insights for regulators. We demonstrate that private information acquired by debt holders—information not governed by Regulation FD—can be shared with shareholders via M&A activities. These findings may assist regulators in evaluating the implications of Regulation FD, supporting their goal of promoting fairness and transparency in the marketplace.

5. Robustness Analyses

In this section, we examine the robustness of the findings related to our main hypotheses. We adopt a two-stage least squares (2SLS) regression analysis to examine the direct impact of information asymmetry on disclosure. As discussed in Section 2, we hypothesize that shareholder–lender merger transactions lead to an increase in firm’s information asymmetry, and firms respond by enhancing disclosure. Because firm disclosures can affect information asymmetry, the observed post-merger information asymmetry reflects the joint effects of the shareholder–lender merger transaction and firm disclosure. To investigate the direct effect of information asymmetry on disclosure, we need to first isolate the “clean” part of information asymmetry. Toward that end, we use the shareholder–lender mergers as an instrument to estimate the “clean” part of information asymmetry. Then we examine the effect of estimated information asymmetry on disclosure. Specifically, we investigate the effect on quarterly management forecast frequency with the following OLS regression:

where indicates or , and is the estimated Spread (AIM) from Equation (1).

Table 5 reports the results of the 2SLS regression analysis regarding management forecast frequency (Frequency). Column (1) shows the first-stage regression results with Spread as the dependent variable. This column is the same as column (1) in Table 3. Based on the estimated coefficients in column (1), we calculate the predicted component of spread () and use it as an independent variable in the second-stage regression. Column (2) presents the second-stage regression results. The coefficient on is positive and significant (coef = 5.102, t-statistic = 2.10), suggesting firms enhance management forecasts in response to the increase in information asymmetry attributable to the shareholder–lender mergers. Column (3) shows the first-stage regression results with AIM as the dependent variable, which is the same as column (2) in Table 3. Similarly, we then use the predicted value of AIM () as an independent variable in the second-stage regression. Column (4) of Table 5 shows the result. The coefficient on is positive and significant (coef = 7.490, t-statistic = 1.93), indicating firms increase disclosure following the elevated information asymmetry. The coefficients on control variables are consistent with the prior literature. Overall, the results in Table 5 are consistent with the hypothesis that increased information asymmetry prompts firms to increase disclosure.

Table 5.

Management Forecasts Frequency and Shareholder–lender Mergers: 2SLS.

Next, we repeat the analysis above, except we use the precision of earnings forecasts (Precision) as the dependent variable to examine the effect of estimated information asymmetry on disclosure quality with the following OLS regression:

where indicates or , and is the estimated Spread (AIM) from Equation (1).

Table 6 presents the results of the 2SLS regression analysis. Column (1) shows the first-stage regression results with Spread as the dependent variable, which is the same as column (1) of Table 3. Using the predicted Spread (), we examine its effect on management earnings forecast precision. Column (2) of Table 6 reports the second-stage regression results. The coefficient on is positive and significant at the 1% level (coef = 5.060, t-statistic = 3.00), suggesting forecast precision increases following increased information asymmetry resulting from shareholder–lender merger transactions. Column (3) presents the first-stage regression results with AIM as the dependent variable, which is the same as column (2) in Table 3. Column (4) reports the second-stage regression results. The coefficient on is positive and significant at the 1% level (coef = 7.630, t-statistics = 2.91), indicating firms increase forecast precision in response to increased information asymmetry. The coefficients on control variables are as expected. For example, in columns (2) and (4), the coefficient on LnNumAF is positive and significant, indicating management forecast precision is positively correlated with the number of analysts covering the firm; the coefficient on ROA is positive and significant, suggesting management forecast precision is positively correlated with firm performance; the coefficient on LnHorizon is negative and significant, which indicates forecast precision is negatively correlated with forecast horizon.

Table 6.

Management earnings forecast precision and shareholder–lender mergers: 2SLS.

6. Conclusions

In this study, we use a quasi-exogenous shock to information asymmetry to examine the effect of information asymmetry on corporate disclosure. Numerous studies have examined the relation between information asymmetry among investors and disclosure. However, due to the endogenous nature of the relation between the two constructs, it is difficult to estimate the effect of information asymmetry on disclosure. We use the merger between a shareholder and a lender of the same firm as a quasi-exogenous shock to the information asymmetry among shareholders. Because Regulation FD applies to shareholders but not lenders, following a shareholder–lender merger transaction, the acquiring shareholder gains access to the firm-specific private information held by the lender, and this flow of private information leads to an increase in the information asymmetry among shareholders.

We provide empirical evidence that shareholder–lender mergers do indeed represent a shock to the level of information asymmetry among shareholders. Specifically, we document that after the merger of a shareholder and a lender of the same firm, both the bid–ask spread and Amihud’s (2002) measure of illiquidity (AIM) of the treatment firms increase, relative to the changes in the bid–ask spreads and AIMs of control firms. We then adopt a difference-in-differences design to examine whether firms increase disclosure and improve disclosure quality after the increase in information asymmetry induced by the mergers. We find that after the shareholder–lender merger transactions, firms issue more quarterly forecasts (including earnings, sales, capital expenditure, EBITDA, and gross margin), and quarterly earnings forecasts are more precise. These results suggest that firms increase disclosure and improve disclosure quality after shareholder–lender mergers to mitigate the increased level of information asymmetry. This study complements Shroff et al. (2013) by using a quasi-exogenous shock in information asymmetry to demonstrate that information asymmetry among equity investors affects corporate disclosure.

These findings have implications for regulators. A primary objective of the SEC is to create a level playing field for all investors in terms of access to material corporate information. Significant concerns have been raised about the extent to which institutional investors obtain confidential private information from lenders and use this information to engage in insider trading in equity markets. The findings of this study suggest that one way shareholders can gain access to private firm-specific information is by merging with one of the firm’s lenders. More specifically, an issue related to M&A of financial institutions is that a shareholder could gain access to private information held by a debt holder, and the issue hinders the regulatory framework that aims to create healthy competition and maintain market integrity.

There are two caveats to our study. First, we use managerial forecasts as a proxy for disclosure because IBES provides machine-readable quantitative data. However, disclosure encompasses other aspects, such as the quality and depth of information conveyed in textual disclosures, conference calls, as well as firm’s information environment (e.g., Yan & Yang, 2022). Consequently, managerial forecasts may not fully capture the overall quality of disclosure. Second, a significant portion of our sample is concentrated during the 2007–2008 financial crisis. While our difference-in-differences research design helps mitigate concerns about omitted variable bias, we cannot completely rule out the possibility that the financial crisis influenced our findings (e.g., X. Yang & Kazemi, 2020; X. Yang & Chen, 2021).

Future research could explore alternative or more comprehensive measures of disclosure quality beyond managerial forecasts. For instance, textual analysis of earnings announcements, conference call transcripts, or qualitative evaluations of narrative disclosures could provide better insights into the depth, tone, and quality of communication. Additionally, researchers might examine periods of economic stability or other financial crises (such as COVID−19) to isolate the influence of macroeconomic factors and assess whether the findings hold beyond the context of the 2007–2008 financial crisis. Future studies could also consider other empirical methods, such as structural modeling, to reduce concerns about omitted variable bias in contexts affected by economic shocks.

Author Contributions

Conceptualization, B.C., W.C. and X.Y.; methodology, B.C. and W.C.; software, W.C. and X.Y.; validation, B.C., W.C. and X.Y.; formal analysis, W.C. and X.Y.; investigation, B.C and W.C.; resources, B.C. and W.C.; data curation, B.C. and X.Y.; writing—original draft preparation, W.C.; writing—review and editing, B.C., W.C. and X.Y.; visualization, X.Y.; supervision, W.C.; project administration, W.C.; funding acquisition, B.C., W.C., and X.Y. All authors have read and agreed to the published version of the manuscript.

Funding

This research received no external funding.

Institutional Review Board Statement

Not applicable.

Informed Consent Statement

Not applicable.

Data Availability Statement

Dataset available on request from the authors.

Acknowledgments

We thank the School of Business at the University of Connecticut, the College of Business at Wenzhou-Kean University, and Silberman College of Business at Fairleigh Dickinson University for financial support.

Conflicts of Interest

The authors declare no conflicts of interest.

Appendix A. Variable Definitions

| Variables | Definition |

| Spread | The daily bid–ask spreads averaged over a 180-day window, multiplied by 100. A daily bid–ask spread is calculated as the closing bid–ask spread from CRSP scaled by the mid-point of bid and ask prices. Spread = 100 * (ask − bid)/[(ask + bid)/2]. |

| AIM | Amihud’s (2002) illiquidity measure, averaged over a 180-day window. The daily AIM is calculated from CRSP as follows: AIM = log (1 + 10,000,000 × abs (ret)/(prc × vol)). |

| Frequency | The natural logarithm of one plus the number of quarterly management forecasts (including earnings, sales, capital expenditure, EBITDA, and gross margin) issued in a 180-day window. |

| Precision | The precision of a quarterly management earnings forecast, measured as the negative of the forecast width (the magnitude of the range for range forecasts and zero for point forecasts), scaled by the beginning-of-quarter stock price and multiplied by 100. |

| Post | An indicator variable equal to one for observations after the shareholder–lender merger transactions, and zero otherwise. |

| Treat | An indicator variable equal to one for treatment firms, and zero otherwise. |

| LnSize | The natural logarithm of the market value of equity, measured at the fiscal year-end preceding the announcement of the shareholder–lender merger transactions. |

| LnNumAF | The natural logarithm of one plus the number of analysts covering a firm during a 365-day window preceding the announcement of the shareholder–lender merger transactions. |

| ROA | Return on assets, income before extraordinary income divided by lagged total assets, measured at the fiscal year-end preceding the announcement of the shareholder–lender merger transactions. |

| MTB | Market-to-book ratio, the market value of equity divided by the book value of equity, measured at the fiscal year-end preceding the announcement of the shareholder–lender merger transactions. |

| LnPRC | Natural logarithm of stock price at the fiscal quarter-end preceding the announcement of the shareholder–lender merger transactions. |

| PerctInst | Percentage of firms’ shares owned by institutional investors, measured at the fiscal quarter-end immediately preceding the announcement of the shareholder–lender merger transactions. |

| Point | An indicator variable equal to one if a management earnings forecast is a point estimate, and zero otherwise. |

| Loss | An indicator variable equal to one if a management earnings forecast is negative, and zero otherwise. |

| LnHorizon | The natural logarithm of one plus the number of days between the management earnings forecast date and the end of the fiscal period to which the management forecast applies. |

Notes

| 1 | Two types of information asymmetry discussed in the literature are information asymmetry among equity investors and information asymmetry between firm managers and investors. Section 2 discusses these two types of information asymmetry in more detail. In this study, we focus on the information asymmetry among equity investors. |

| 2 | Disclosure can also reduce information asymmetry between managers and investors (e.g., M. H. Lang & Lundholm, 2000; Botosan, 2000; Healy & Palepu, 2001; Beyer et al., 2010). |

| 3 | The timing of the required public disclosure depends on whether the selective disclosure was intentional or non-intentional. For an intentional disclosure, the issuer must make public disclosure simultaneously; for a non-intentional disclosure, the issuer must make public disclosure within 24 h. |

| 4 | Regulation FD prohibits any selective disclosure of material information by a firm to its shareholders, but Regulation FD does not apply to loan lenders. Rule 100(b)(2) of Regulation FD outlines four coverage exclusions of the regulation. |

| 5 | The merger between a shareholder and a lender of the same firm represents an exogenous shock to information asymmetry because it is not related to the firm’s operation and performance. As we cannot rule out the possibility that the merger transaction is completed mainly for the equity holder to gain firm-specific private information from the lender, the shock on information asymmetry is termed quasi-exogenous. |

| 6 | Prior literature finds that information asymmetry between managers and investors also negatively affects market liquidity and cost of equity (e.g., Myers & Majluf, 1984; Merton, 1987; M. Lang & Lundholm, 1993; Healy & Palepu, 1995; Botosan, 2000; Healy & Palepu, 2001; Beyer et al., 2010). Note that the shareholder–lender merger leads to a decrease, rather than an increase, in the level of information asymmetry between managers and investors, because the acquiring shareholder gains access to firm-specific private information after the merger. The decrease in information asymmetry between managers and investors is unlikely to prompt firms to increase disclosure and improve disclosure quality. |

| 7 | Statistical rating organizations and credit rating agencies were originally exempt from Regulation FD. |

| 8 | Previous studies provide substantial evidence that hedge funds obtain and utilize private information (e.g., Yang et al., 2021; B. Chen et al., 2025). |

| 9 | We acknowledge it is possible that mergers between a shareholder and a lender of the same firm affect disclosure in an indirect way. These mergers could increase the information asymmetry perceived by other shareholders observing the merger transactions, and prompt them to demand a larger risk premium as compensation for the perceived increase in risk associated with the perceived increase in information asymmetry (e.g., Copeland & Galai, 1983; Glosten & Milgrom, 1985; Kyle, 1985). Firms might then respond by increasing disclosure and improving disclosure quality to mitigate these negative effects. |

| 10 | Kelly and Ljungqvist (2012) find evidence that the closures and mergers of brokerage houses’ research operations represent a plausibly exogenous shock to information asymmetry and use this setting to show that information asymmetry is priced. While a brokerage closure can increase the information asymmetry among investors, it can also increase the information asymmetry between managers and investors. |

| 11 | There are two reasons for using a 180-day window both before and after shareholder–lender merger transactions. First, we use quarterly forecasts (including earnings, sales, capital expenditures, EBITDA, and gross margin) as proxies for disclosure. Second, it takes time for the effects of shareholder–lender mergers to manifest and for managers to adjust their disclosure practices. |

| 12 | There are many firm-specific factors that affect a firm’s bid–ask spread and AIM (such as new product releases or media coverage). Therefore, we use multiple control observations for each treatment observation to mitigate the impact of idiosyncratic factors in the analysis. |

| 13 | Each shareholder–lender merger transaction is associated with multiple treatment observations. For example, suppose financial institution A is a shareholder of firms C1 and C2, and financial institution B is a lender of firms C1 and C2, then the merger of A and B leads to two treatment observations (C1 and C2). |

| 14 | In 2001, the stock exchanges (NYSE, AMEX, and NASDAQ) completed a process of decimalization, changing security price quotes from a minimum price movement of USD 0.0625 (1/16th of a dollar) to decimals with a minimum price movement of USD 0.01; Sarbanes–Oxley was enacted in 2002; the Global Analyst Research Settlement was completed in 2003; and the 8-K regulation went to effect in 2004. |

| 15 | Specifically, MiFID II came into effect in January 2018 and Regulatory Notice 18−08 was issued in February 2018. Although MiFID II primarily applies to firms operating within the European Union (EU), US firms that have EU clients or engage in transactions involving EU financial instruments may be subject to MiFID II requirements. Regulatory Notice 18−08 reminds firms of their obligations under FINRA rules to prevent the misuse of nonpublic information and to ensure effective supervision and control of insider trading risks. |

References

- Addoum, J., & Murfin, J. R. (2020). Equity price discovery with informed private debt. The Review of Financial Studies, 33(8), 3766–3803. [Google Scholar] [CrossRef]

- Agarwal, P., & O’Hara, M. (2007). Information risk and capital structure (Working paper). Cornell University. [Google Scholar]

- Ahern, K., & Sosyura, D. (2014). Who writes the news? Corporate press releases during merger negotiations. The Journal of Finance, 69(1), 241–291. [Google Scholar] [CrossRef]

- Akins, B. K., Ng, J., & Verdi, R. S. (2012). Investor competition over information and the pricing of information asymmetry. Accounting Review, 87(1), 35–58. [Google Scholar] [CrossRef]

- Amel-Zadeh, A., & Meeks, G. (2019). Bidder earnings forecasts in mergers and acquisitions. Journal of Corporate Finance, 58, 373–392. [Google Scholar] [CrossRef]

- Amihud, Y. (2002). Illiquidity and stock returns: Cross-section and time-series effects. Journal of Financial Markets, 5(1), 31–56. [Google Scholar] [CrossRef]

- Amihud, Y., & Mendelson, H. (1986). Asset pricing and the bid-ask spread. Journal of Financial Economics, 17(2), 223–249. [Google Scholar] [CrossRef]

- Anderson, J. (2006, October 16). Hedge funds draw insider scrutiny. The New York Times. [Google Scholar]

- Armstrong, C. S., Core, J. E., Taylor, D. J., & Verrecchia, R. E. (2011). When does information asymmetry affect the cost of capital? Journal of Accounting Research, 49(1), 1–40. [Google Scholar] [CrossRef]

- Badertscher, B. A. (2011). Overvaluation and the choice of alternative earnings management mechanisms. The Accounting Review, 86(5), 1491–1518. [Google Scholar] [CrossRef]

- Balakrishnan, K., Billings, M., Kelly, B., & Ljungqvist, A. (2014). Shaping liquidity: On the causal effects of voluntary disclosure. Journal of Finance, 69, 2237–2278. [Google Scholar] [CrossRef]

- Beyer, A., Cohen, D. A., Lys, T. Z., & Walther, B. R. (2010). The financial reporting environment: Review of the recent literature. Journal of Accounting and Economics, 50(2–3), 296–343. [Google Scholar] [CrossRef]

- Bhattacharya, N., Ecker, F., Olsson, P. M., & Schipper, K. (2012). Direct and mediated associations among earnings quality, information asymmetry, and the cost of equity. Accounting Review, 87(2), 449–482. [Google Scholar] [CrossRef]

- Bhojraj, S., Cho, Y. J., & Yehuda, N. I. R. (2012). Mutual fund family size and mutual fund performance: The role of regulatory changes. Journal of Accounting Research, 50(3), 647–684. [Google Scholar] [CrossRef]

- Blume, M. E., & Keim, D. B. (2012). Institutional investors and stock market liquidity: Trends and relationships (Working paper). University of Pennsylvania. [Google Scholar]

- Botosan, C. A. (1997). Disclosure level and the cost of equity capital. The Accounting Review, 72(3), 323–349. [Google Scholar]

- Botosan, C. A. (2000). Evidence that greater disclosure lowers the cost of equity capital. Journal of Applied Corporate Finance, 12(4), 60–69. [Google Scholar] [CrossRef]

- Botosan, C. A., & Plumlee, M. A. (2002). A Re-examination of disclosure level and the expected cost of equity capital. Journal of Accounting Research, 40(1), 21–40. [Google Scholar] [CrossRef]

- Brennan, M. J., & Subrahmanyam, A. (1996). Market microstructure and asset pricing: On the compensation for illiquidity in stock returns. Journal of Financial Economics, 41(3), 441–464. [Google Scholar] [CrossRef]

- Brown, L. D., Call, A. C., Clement, M. B., & Sharp, N. Y. (2015). Inside the “Black Box” of sell-side financial analysts. Journal of Accounting Research, 53(1), 1–47. [Google Scholar] [CrossRef]

- Brown, S., & Hillegeist, S. A. (2007). How disclosure quality affects the level of information asymmetry. Review of Accounting Studies, 12(2), 443–477. [Google Scholar] [CrossRef]

- Brown, S., Hillegeist, S. A., & Lo, K. (2004). Conference calls and information asymmetry. Journal of Accounting and Economics, 37(3), 343–366. [Google Scholar] [CrossRef]

- Bushee, B. J., Core, J. E., Guay, W., & Hamm, S. J. W. (2010). The role of the business press as an information intermediary. Journal of Accounting Research, 48(1), 1–19. [Google Scholar] [CrossRef]

- Bushee, B. J., Matsumoto, D. A., & Miller, G. S. (2004). Managerial and investor responses to disclosure regulation: The case of reg FD and conference calls. The Accounting Review, 79(3), 617–643. [Google Scholar]

- Bushman, R. M., Smith, A. J., & Wittenberg-Moerman. (2010). Price discovery and dissemination of private information by loan syndicate participants. Journal of Accounting Research, 48(5), 921–972. [Google Scholar] [CrossRef]

- Chen, B., Kazemi, M. M., & Yang, X. (2025). Do hedge fund clients of prime brokers front-run their analysts? International Review of Economics & Finance, 97, 103824. [Google Scholar]

- Chen, Q., & Vashishtha, R. (2017). The effects of bank mergers on corporate information disclosure. Journal of Accounting and Economics, 64(1), 56–77. [Google Scholar] [CrossRef]

- Chen, T., & Martin, X. (2011). Do bank-affiliated analysts benefit from lending relationships? Journal of Accounting Research, 49(3), 633–675. [Google Scholar] [CrossRef]

- Cheng, Q., Luo, T., & Yue, H. (2013). Managerial incentives and management forecast precision. The Accounting Review, 88(5), 1575–1602. [Google Scholar] [CrossRef]

- Chiyachantana, C. N., Jiang, C. X., Taechapiroontong, N., & Wood, R. A. (2004). The impact of regulation fair disclosure on information asymmetry and trading: An intraday analysis. Financial Review, 39(4), 549–577. [Google Scholar] [CrossRef]

- Chu, Y. (2017). Shareholder-creditor conflict and payout policy: Evidence from mergers between lenders and shareholders (Working paper). University of South Carolina. [Google Scholar]

- Cicero, D. C., Kalpathy, S., & Sulaeman, J. (2011). Equity analysts affiliated with corporate lenders (Working paper). University of Tennessee, Southern Methodist University. [Google Scholar]

- Cohen, D. A. (2003). Quality of financial reporting choice: Determinants and economic consequences (Working paper). University of Texas at Dallas. [Google Scholar]

- Coller, M., & Yohn, T. L. (1997). Management forecasts and information asymmetry: An examination of bid-ask spreads. Journal of Accounting Research, 35(2), 181–191. [Google Scholar] [CrossRef]

- Copeland, T. E., & Galai, D. (1983). Information effects on the bid-ask spread. The Journal of Finance, 38(5), 1457–1469. [Google Scholar]

- Cotter, J., Tuna, I., & Wysocki, P. D. (2006). Expectations management and beatable targets: How do analysts react to explicit earnings guidance? Contemporary Accounting Research, 23(3), 593–624. [Google Scholar] [CrossRef]

- Dennis, S. A., & Mullineaux, D. J. (2000). Syndicated loans. Journal of Financial Intermediation, 9(4), 404–426. [Google Scholar] [CrossRef]

- Diamond, D. W. (1984). Financial intermediation and delegated monitoring. The Review of Economic Studies, 51(3), 393–414. [Google Scholar] [CrossRef]

- Diamond, D. W. (1985). Optimal release of information by firms. The Journal of Finance, 40(4), 1071–1094. [Google Scholar] [CrossRef]

- Diamond, D. W., & Verrecchia, R. E. (1991). Disclosure, liquidity, and the cost of capital. The Journal of Finance, 46(4), 1325–1359. [Google Scholar] [CrossRef]

- Dierkens, N. (1991). Information asymmetry and equity issues. The Journal of Financial and Quantitative Analysis, 26(2), 181–199. [Google Scholar] [CrossRef]

- Draper, P., & Paudyal, K. (2008). Information asymmetry and bidders’ gains. Journal of Business Finance & Accounting, 35(3–4), 376–405. [Google Scholar]

- Easley, D., Hvidkjaer, S., & O’Hara, M. (2002). Is information risk a determinant of asset returns? The Journal of Finance, 57(5), 2185–2221. [Google Scholar] [CrossRef]

- Easley, D., & O’Hara, M. (2004). Information and the cost of capital. The Journal of Finance, 59(4), 1553–1583. [Google Scholar] [CrossRef]

- Erickson, M., Wang, S. W., & Zhang, X. F. (2012). The change in information uncertainty and acquirer wealth losses. Review of Accounting Studies, 17, 913–943. [Google Scholar] [CrossRef]

- Fama, E. F. (1985). What’s different about banks? Journal of Monetary Economics, 15(1), 29–39. [Google Scholar] [CrossRef]

- Fama, E. F., & French, K. R. (1992). The cross-section of expected stock returns. The Journal of Finance, 47(2), 427–465. [Google Scholar]

- Fama, E. F., & French, K. R. (1997). Industry costs of equity. Journal of Financial Economics, 43(2), 153–193. [Google Scholar] [CrossRef]