Asymmetric Effects of Uncertainty and Commodity Markets on Sustainable Stock in Seven Emerging Markets

Abstract

1. Introduction

2. Literature Review

2.1. Uncertainty Effects on Sustainable Stock

2.2. Gold and Crude Oil Prices Effects on Sustainable Stock

3. Data and Methodology

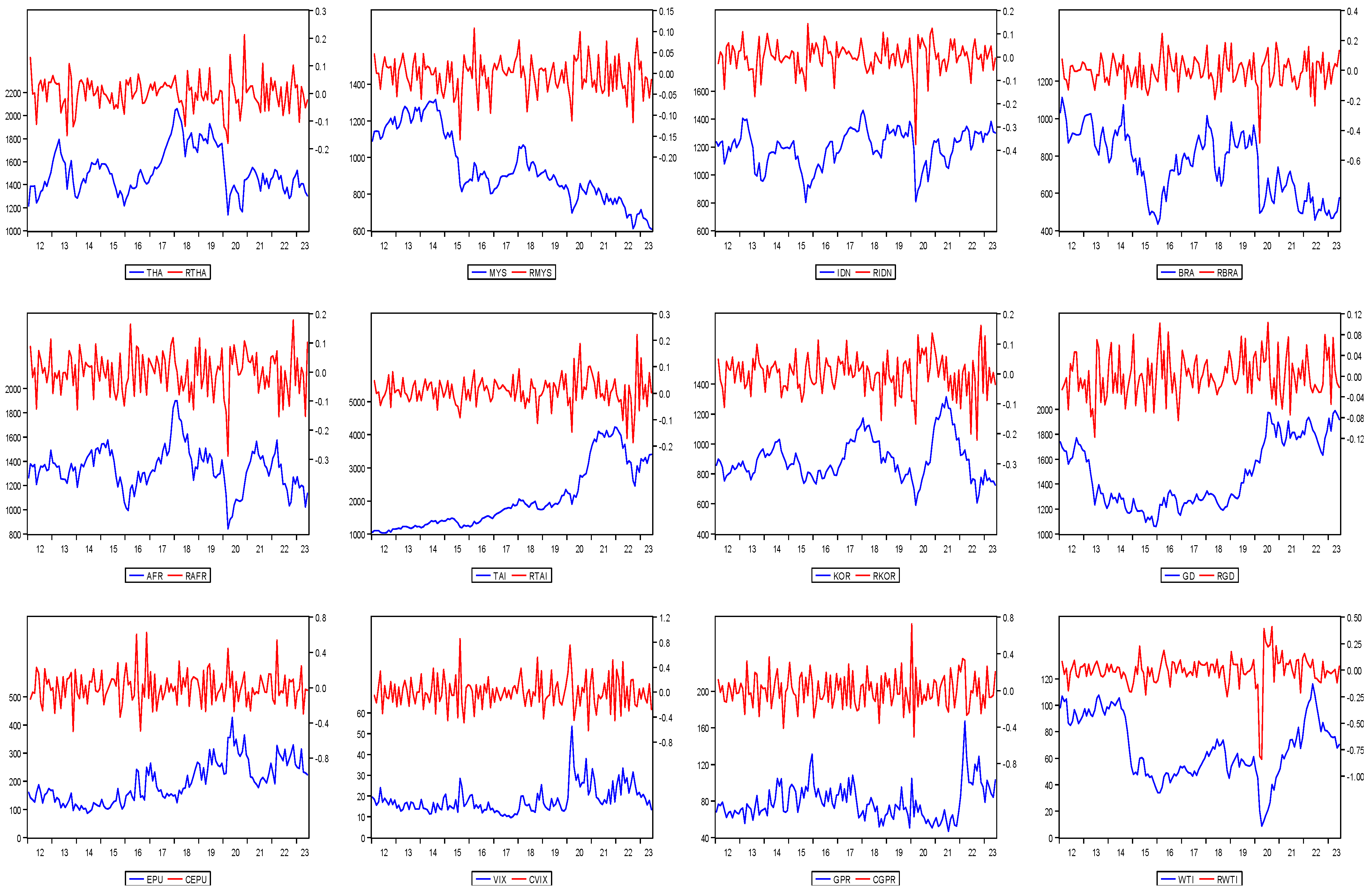

3.1. Data

3.2. Methodology

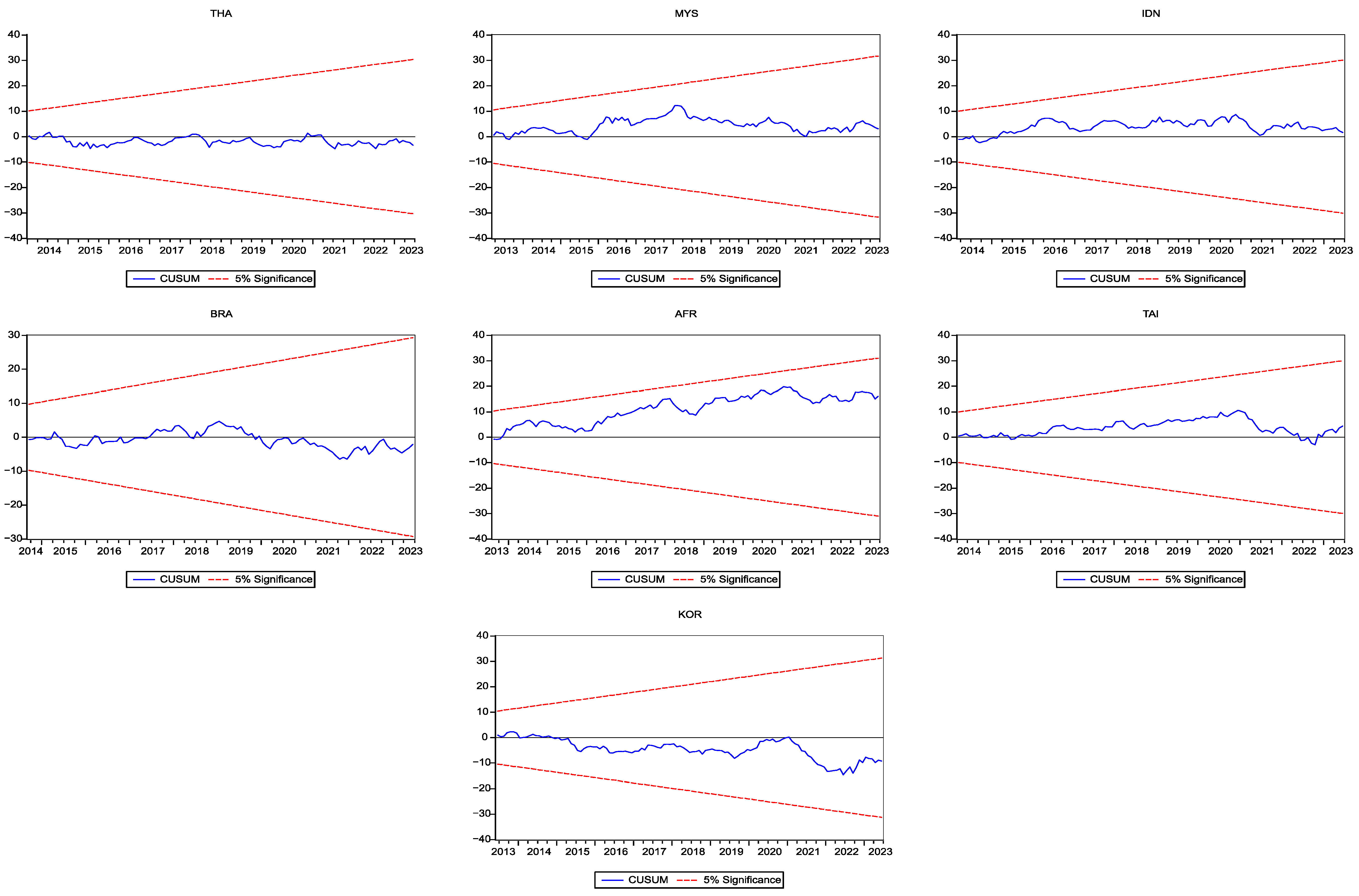

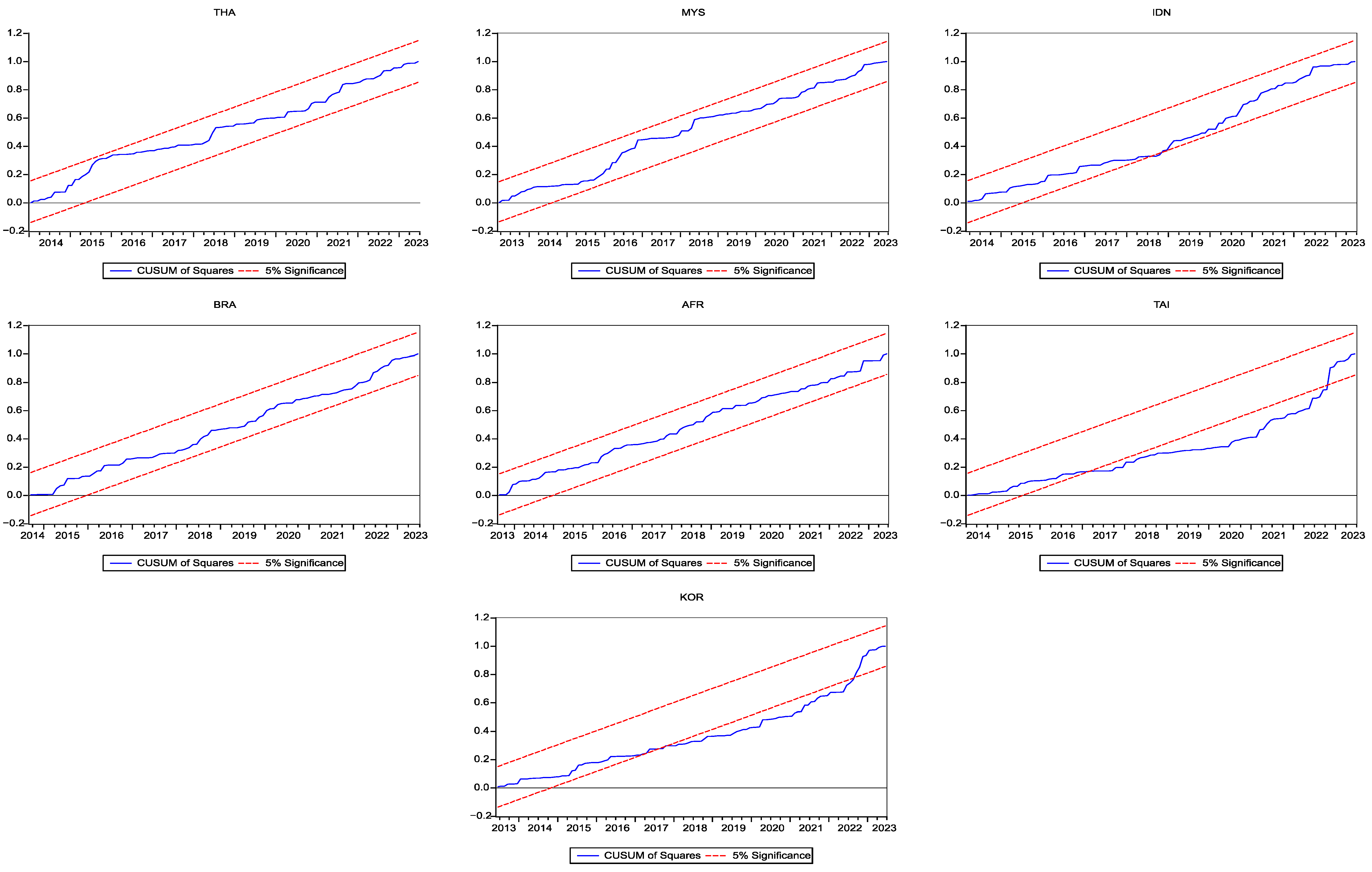

4. Result and Discussion

4.1. Descriptive Statistics

4.2. Asymmetric Effects of EPU, VIX, GPR, GD, and WTI on Sustainable Stock

5. Conclusions and Policy Implications

Author Contributions

Funding

Data Availability Statement

Acknowledgments

Conflicts of Interest

Appendix A

References

- Ali, Sajid, Elie Bouri, Robert Lukas Czudaj, and Syed Jawad Hussain Shahzad. 2020. Revisiting the valuable roles of commodities for international stock markets. Resources Policy 66: 101603. [Google Scholar] [CrossRef]

- Andersson, Emil, Mahim Hoque, Md Lutfur Rahman, Gazi Salah Uddin, and Ranadeva Jayasekera. 2022. ESG investment: What do we learn from its interaction with stock, currency and commodity markets? International Journal of Finance and Economics 27: 3623–39. [Google Scholar] [CrossRef]

- Atri, Hanen, Hanen Teka, and Saoussen Kouki. 2023. Does US full vaccination against COVID-19 immunize correspondingly S&P500 index: Evidence from the NARDL approach. Heliyon 9: e15332. [Google Scholar] [CrossRef] [PubMed]

- Baker, Scott R., Nicholas Bloom, and Steven J. Davis. 2016. Measuring economic policy uncertainty. Quarterly Journal of Economics 131: 1593–636. [Google Scholar] [CrossRef]

- Baur, Dirk G., and Brian M. Lucey. 2010. Is gold a hedge or a safe haven? An analysis of stocks, bonds and gold. The Financial Review 45: 217–29. [Google Scholar] [CrossRef]

- Baur, Dirk G., and Lee A. Smales. 2020. Hedging geopolitical risk with precious metals. Journal of Banking & Finance 117: 105823. [Google Scholar] [CrossRef]

- Bernanke, Ben S. 1983. Irreversibility, uncertainty, and cyclical investment. The Quarterly Journal of Economics 98: 85–106. [Google Scholar] [CrossRef]

- Bhattacherjee, Purba, Sibanjan Mishra, and Sang Hoon Kang. 2023. Does market sentiment and global uncertainties influence ESG-oil nexus? A time-frequency analysis. Resources Policy 86: 104130. [Google Scholar] [CrossRef]

- Bloom, Nicholas. 2009. The impact of uncertainty shocks. Econometrica 77: 623–85. [Google Scholar] [CrossRef]

- Bossman, Ahmed, and Mariya Gubareva. 2023. Asymmetric impacts of geopolitical risk on stock markets: A comparative analysis of the E7 and G7 equities during the Russian-Ukrainian conflict. Heliyon 9: e13626. [Google Scholar] [CrossRef]

- Cagli, Efe C. Caglar, Pinar Evrim Mandaci, and Dilvin Taşkın. 2023. Environmental, social, and governance (ESG) investing and commodities: Dynamic connectedness and risk management strategies. Sustainability Accounting, Management and Policy Journal 14: 1052–74. [Google Scholar] [CrossRef]

- Caldara, Dario, and Matteo Iacoviello. 2022. Measuring geopolitical risk. American Economic Review 112: 1194–225. [Google Scholar] [CrossRef]

- Chancharat, Surachai, and Parichat Sinlapates. 2023. Dependences and dynamic spillovers across the crude oil and stock markets throughout the COVID-19 pandemic and Russia-Ukraine conflict: Evidence from the ASEAN+6. Finance Research Letters 57: 104249. [Google Scholar] [CrossRef]

- Darsono, Susilo Nur Aji Cokro, Wing-Keung Wong, Tran Thai Ha Nguyen, and Dyah Titis Kusuma Wardani. 2022. The economic policy uncertainty and its effect on sustainable investment: A panel ARDL approach. Journal of Risk and Financial Management 15: 254. [Google Scholar] [CrossRef]

- Das, Debojyoti, M. Kannadhasan, and Malay Bhattacharyya. 2019. Do the emerging stock markets react to international economic policy uncertainty, geopolitical risk and financial stress alike? The North American Journal of Economics and Finance 48: 1–19. [Google Scholar] [CrossRef]

- Davis, Steven J. 2016. An index of global economic policy uncertainty. Macroeconomic Review 15: 91–97. [Google Scholar]

- Diab, Adeline. 2022. ESG May Surpass $41 Trillion Assets in 2022, But Not without Challenges. Bloomberg Intelligence. Available online: https://www.bloomberg.com/company/press/esg-may-surpass-41-trillion-assets-in-2022-but-not-without-challenges-finds-bloomberg-intelligence/ (accessed on 4 November 2023).

- Donadelli, Michael. 2015. Asian stock markets, US economic policy uncertainty and US macro-shocks. New Zealand Economic Papers 49: 103–33. [Google Scholar] [CrossRef]

- Erdoğan, Levent, Reşat Ceylan, and Mutawakil Abdul-Rahman. 2022. The impact of domestic and global risk factors on Turkish stock market: Evidence from the NARDL approach. Emerging Markets Finance and Trade 58: 1961–74. [Google Scholar] [CrossRef]

- Garel, Alexandre, and Arthur Petit-Romec. 2021. Investor rewards to environmental responsibility: Evidence from the COVID-19 crisis. Journal of Corporate Finance 68: 101948. [Google Scholar] [CrossRef]

- Gheraia, Zouheyr. 2022. The asymmetric impact of COVID-19 pandemic on the crude oil-stock markets nexus in KSA: Evidence from a NARDL model. International Journal of Energy Economics and Policy 12: 137–45. [Google Scholar] [CrossRef]

- Ghosh, Sudeshna. 2022. COVID-19, clean energy stock market, interest rate, oil prices, volatility index, geopolitical risk nexus: Evidence from quantile regression. Journal of Economics and Development 24: 329–44. [Google Scholar] [CrossRef]

- Ghumro, Niaz Hussain, Ishfaque Ahmed Soomro, and Ghulam Abbas. 2022. Asymmetric effect of exchange rate and investors’ sentiments on stock market performance. Journal of Economic and Administrative Sciences. Published electronically April 25. [Google Scholar] [CrossRef]

- Hoque, Mohammad Enamul, and Mohd Azlan Shah Zaidi. 2020. Global and country-specific geopolitical risk uncertainty and stock return of fragile emerging economies. Borsa Istanbul Review 20: 197–213. [Google Scholar] [CrossRef]

- Hoque, Mohammad Enamul, Low Soo Wah, and Mohd Azlan Shah Zaidi. 2019. Oil price shocks, global economic policy uncertainty, geopolitical risk, and stock price in Malaysia: Factor augmented VAR approach. Economic Research-Ekonomska Istraživanja 32: 3700–32. [Google Scholar] [CrossRef]

- Kamal, Javed Bin, Mark Wohar, and Khaled Bin Kamal. 2022. Do gold, oil, equities, and currencies hedge economic policy uncertainty and geopolitical risks during covid crisis? Resources Policy 78: 102920. [Google Scholar] [CrossRef]

- Lean, Hooi Hooi, and Duc Khuong Nguyen. 2014. Policy uncertainty and performance characteristics of sustainable investments across regions around the global financial crisis. Applied Financial Economics 24: 1367–73. [Google Scholar] [CrossRef]

- Lei, Heng, Huiling Liu, Minggao Xue, and Jing Ye. 2023. Precious metal as a safe haven for global ESG stocks: Portfolio implications for socially responsible investing. Resources Policy 80: 103170. [Google Scholar] [CrossRef]

- Mousa, Musaab, Adil Saleem, and Judit Sági. 2022. Are ESG shares a safe haven during COVID-19? Evidence from the Arab region. Sustainability 14: 208. [Google Scholar] [CrossRef]

- Naeem, Muhammad Abubakr, Sitara Karim, Imran Yousaf, Aviral Kumar Tiwari, and Saqib Farid. 2023. Comparing asymmetric price efficiency in regional ESG markets before and during COVID-19. Economic Modelling 118: 106095. [Google Scholar] [CrossRef] [PubMed]

- Narayan, Paresh Kumar, and Russell Smyth. 2006. What determines migration flows from low-income to high-income countries? An empirical investigation of Fiji–U.S. migration 1972–2001. Contemporary Economic Policy 24: 332–42. [Google Scholar] [CrossRef]

- Nusair, Salah A., and Jamal A. Al-Khasawneh. 2023. Changes in oil price and economic policy uncertainty and the G7 stock returns: Evidence from asymmetric quantile regression analysis. Economic Change and Restructuring 56: 1849–93. [Google Scholar] [CrossRef]

- Pástor, Lŭboš, and Pietro Veronesi. 2012. Uncertainty about government policy and stock prices. The Journal of Finance 67: 1219–64. [Google Scholar] [CrossRef]

- Pástor, Lŭboš, and Pietro Veronesi. 2013. Political uncertainty and risk premia. Journal of Financial Economics 110: 520–45. [Google Scholar] [CrossRef]

- Pesaran, M. Hashem, Yongcheol Shin, and Richard J. Smith. 2001. Bounds testing approaches to the analysis of level relationships. Journal of Applied Econometrics 16: 289–326. [Google Scholar] [CrossRef]

- Piserà, Stefano, and Helen Chiappini. 2024. Are ESG indexes a safe-haven or hedging asset? Evidence from the COVID-19 pandemic in China. International Journal of Emerging Markets 19: 56–75. [Google Scholar] [CrossRef]

- Prukumpai, Suthawan, Yuthana Sethapramote, and Pongsak Luangaram. 2022. Political uncertainty and the Thai stock market. Southeast Asian Journal of Economics 10: 227–57. [Google Scholar]

- Raza, Naveed, Syed Jawad Hussain Shahzad, Aviral Kumar Tiwari, and Muhammad Shahbaz. 2016. Asymmetric impact of gold, oil prices and their volatilities on stock prices of emerging markets. Resources Policy 49: 290–301. [Google Scholar] [CrossRef]

- Rubbaniy, Ghulame, Ali Awais Khalid, Muhammad Faisal Rizwan, and Shoaib Ali. 2022. Are ESG stocks safe-haven during COVID-19? Studies in Economics and Finance 39: 239–55. [Google Scholar] [CrossRef]

- Sarker, Provash Kumer, Elie Bouri, and Chi Keung Lau Marco. 2023. Asymmetric effects of climate policy uncertainty, geopolitical risk, and crude oil prices on clean energy prices. Environmental Science and Pollution Research 30: 15797–807. [Google Scholar] [CrossRef] [PubMed]

- Shaikh, Imlak. 2022. On the relationship between policy uncertainty and sustainable investing. Journal of Modelling in Management 17: 1504–23. [Google Scholar] [CrossRef]

- Sharpe, William F. 1964. Capital asset prices: A theory of market equilibrium under conditions of risk. The Journal of Finance 19: 425–42. [Google Scholar] [CrossRef]

- Shin, Yongcheol, Byungchul Yu, and Matthew Greenwood-Nimmo. 2014. Modelling asymmetric cointegration and dynamic multipliers in a nonlinear ARDL framework. In Festschrift in Honor of Peter Schmidt: Econometric Methods and Applications. Edited by William C. Horrace and Robin C. Sickles. New York: Springer Science and Business Media, pp. 281–314. [Google Scholar] [CrossRef]

- Sohag, Kazi, Shawkat Hammoudeh, Ahmed H. Elsayed, Oleg Mariev, and Yulia Safonova. 2022. Do geopolitical events transmit opportunity or threat to green markets? Decomposed measures of geopolitical risks. Energy Economics 111: 106068. [Google Scholar] [CrossRef]

- Taera, Edosa Getachew, Budi Setiawan, Adil Saleem, Andi Sri Wahyuni, Daniel KS Chang, Robert Jeyakumar Nathan, and Zoltan Lakner. 2023. The impact of Covid-19 and Russia-Ukraine war on the financial asset volatility: Evidence from equity, cryptocurrency and alternative assets. Journal of Open Innovation: Technology, Market, and Complexity 9: 100116. [Google Scholar] [CrossRef]

- Tang, Yumei, Xihui Haviour Chen, Provash Kumer Sarker, and Sarra Baroudi. 2023. Asymmetric effects of geopolitical risks and uncertainties on green bond markets. Technological Forecasting & Social Change 189: 122348. [Google Scholar] [CrossRef]

- Tran, Minh Phuoc-Bao, and Duc Hong Vo. 2023. Asia-Pacific stock market return and volatility in the uncertain world: Evidence from the nonlinear autoregressive distributed lag approach. PLoS ONE 18: e2085279. [Google Scholar] [CrossRef] [PubMed]

- Umar, Zaghum, Sun-Yong Choi, Onur Polat, and Tamara Teplova. 2022. The impact of the Russia-Ukraine conflict on the connectedness of financial markets. Finance Research Letters 48: 102976. [Google Scholar] [CrossRef]

- Wang, Yihan, Zeeshan Fareed, Elie Bouri, and Yuhui Dai. 2022. Geopolitical risk and the systemic risk in the commodity markets under the war in Ukraine. Finance Research Letters 49: 103066. [Google Scholar] [CrossRef]

{kind=link}

{kind=link}

{kind=link}

| Variables | Abbreviation | Description |

|---|---|---|

| Sustainable stock | THA | Thailand MSCI ESG leaders standard (USD) |

| MYS | Malaysia MSCI ESG leaders standard (USD) | |

| IDN | Indonesia MSCI ESG leaders standard (USD) | |

| BRA | Brazil MSCI ESG leaders standard (USD) | |

| AFR | South Africa MSCI ESG leaders standard (USD) | |

| TAI | Taiwan MSCI ESG leaders standard (USD) | |

| KOR | South Korea ESG leaders standard (USD) | |

| Uncertainty | EPU | Global economic policy uncertainty index |

| VIX | CBOE volatility index | |

| GPR | Geopolitical risk index | |

| Commodity | GD | Gold: Gold price (USD per troy ounce) |

| WTI | Crude oil: West Texas intermediate crude oil price (USD per barrel) |

| Variables | THA | MYS | IDN | BRA | AFR | TAI | KOR | EPU | VIX | GPR | GD | WTI |

|---|---|---|---|---|---|---|---|---|---|---|---|---|

| Panel A: Descriptive statistics and unit root tests | ||||||||||||

| Average (%) | 0.050 | −0.426 | 0.037 | −0.426 | −0.078 | 0.858 | −0.122 | 0.237 | −0.261 | 0.301 | 0.072 | −0.244 |

| S.D. (%) | 5.778 | 4.247 | 6.600 | 9.877 | 7.174 | 5.670 | 6.356 | 18.395 | 24.656 | 18.471 | 4.170 | 14.794 |

| Max (%) | 21.245 | 10.800 | 14.277 | 24.742 | 17.851 | 22.169 | 16.136 | 62.525 | 85.259 | 72.449 | 10.342 | 41.334 |

| Min (%) | −17.999 | −15.883 | −37.498 | −48.520 | −28.766 | −18.689 | −22.040 | −49.540 | −61.428 | −50.856 | −11.715 | −84.414 |

| Skewness | −0.087 | −0.439 | −1.581 | −0.744 | −0.518 | 0.011 | −0.490 | 0.414 | 0.439 | 0.307 | 0.148 | −2.209 |

| Kurtosis | 4.448 | 4.020 | 9.800 | 6.090 | 3.963 | 5.646 | 4.071 | 4.363 | 3.759 | 3.789 | 2.851 | 15.860 |

| J-B | 12.151 a | 10.344 a | 321.05 a | 67.153 a | 11.420 a | 39.969 a | 12.042 a | 14.521 a | 7.689 b | 5.708 c | 0.624 | 1055.5 a |

| ADF | −11.555 a | −11.447 a | −11.124 a | −11.361 a | −12.414 a | −13.011 a | −12.083 a | −15.476 a | −16.484 a | −16.480 a | −11.933 a | −8.558 a |

| PP | −11.790 a | −11.587 a | −11.468 a | −11.990 a | −12.508 a | −12.941 a | −12.074 a | −20.488 a | −26.302 a | −25.470 a | −12.007 a | −8.198 a |

| Panel B: Correlation matrix and multicollinearity | ||||||||||||

| THA | 1.000 | |||||||||||

| MYS | 0.583 a | 1.000 | ||||||||||

| IDN | 0.620 a | 0.525 a | 1.000 | |||||||||

| BRA | 0.507 a | 0.553 a | 0.514 a | 1.000 | ||||||||

| AFR | 0.632 a | 0.638 a | 0.556 a | 0.639 a | 1.000 | |||||||

| TAI | 0.512 a | 0.616 a | 0.414 a | 0.422 a | 0.587 a | 1.000 | ||||||

| KOR | 0.580 a | 0.640 a | 0.425 a | 0.471 a | 0.674 a | 0.722 a | 1.000 | |||||

| EPU | −0.039 | −0.114 | −0.180 b | −0.045 | −0.074 | −0.083 | −0.118 | 1.000 | ||||

| VIX | −0.481 a | −0.442 a | −0.274 a | −0.327 a | −0.481 a | −0.414 a | −0.509 a | −0.055 | 1.000 | |||

| GPR | −0.096 | 0.029 | −0.088 | 0.048 | −0.057 | −0.148 c | −0.141 c | 0.040 | 0.079 | 1.000 | ||

| GD | 0.188 b | 0.241 a | 0.247 a | 0.253 a | 0.272 a | 0.250 a | 0.261 a | 0.084 | −0.034 | 0.005 | 1.000 | |

| WTI | 0.159 c | 0.206 b | 0.197 b | 0.325 a | 0.317 a | 0.168 b | 0.276 a | −0.204 b | −0.170 b | −0.084 | −0.012 | 1.000 |

| VIF | 1.060 | 1.012 | 1.045 | 1.008 | 1.085 | |||||||

| Variables | Lag Structure | FPSS | Conclusion |

|---|---|---|---|

| THA | 1, 0, 1, 2, 2, 0, 0, 1, 0, 2, 0 | 13.100 a | Cointegration |

| MYS | 1, 0, 0, 0, 0, 0, 0, 0, 0, 0, 0 | 11.830 a | Cointegration |

| IDN | 1, 0, 0, 2, 1, 3, 0, 0, 0, 0, 3 | 12.220 a | Cointegration |

| BRA | 1, 0, 1, 4, 0, 3, 3, 0, 0, 3, 0 | 11.371 a | Cointegration |

| AFR | 1, 0, 0, 0, 0, 0, 0, 1, 0, 0, 2 | 16.013 a | Cointegration |

| TAI | 1, 0, 2, 3, 3, 0, 1, 0, 1, 0, 0 | 12.528 a | Cointegration |

| KOR | 1, 0, 1, 0, 0, 0, 0, 0, 0, 1, 0 | 13.304 a | Cointegration |

| Variables | THA | MYS | IDN | BRA | AFR | TAI | KOR |

|---|---|---|---|---|---|---|---|

| Panel A: Short-run asymmetric effects | |||||||

| EPU+t | −0.035 | −0.027 | −0.030 | 0.032 | −0.058 c | −0.063 c | −0.045 c |

| EPU−t | 0.051 | −0.035 c | −0.043 | 0.004 | −0.001 | −0.006 | −0.056 b |

| VIX+t | −0.087 a | −0.078 a | −0.063 b | −0.033 | −0.125 a | −0.137 a | −0.125 a |

| VIX+t−1 | − | − | −0.059 b | −0.039 | − | − | − |

| VIX+t−2 | − | − | 0.037 | 0.143 b | − | − | − |

| VIX−t | −0.083 a | −0.070 a | −0.064 c | −0.260 a | −0.105 a | −0.049 b | −0.108 a |

| VIX−t−1 | − | − | − | 0.189 b | − | − | − |

| VIX−t−2 | − | − | − | 0.072 | − | − | − |

| GPR+t | −0.079 a | 0.013 | −0.089 b | 0.040 | −0.030 | −0.026 | −0.057 b |

| GPR+t−1 | −0.033 | − | − | 0.164 a | − | − | − |

| GPR+t−2 | − | − | − | −0.101 c | − | − | − |

| GPR−t | 0.042 | 0.020 | 0.038 | 0.080 | 0.050 | −0.014 | 0.011 |

| GPR−t−1 | − | − | 0.112 a | − | 0.079 b | − | − |

| GPR−t−2 | − | − | 0.070 b | − | − | − | − |

| GD+t | 0.343 a | 0.275 a | 0.335 b | 0.813 a | 0.494 a | 0.493 a | 0.625 a |

| GD−t | 0.099 | 0.262 a | 0.259 b | 0.391 | 0.390 a | −0.019 | 0.193 |

| GD−t−1 | − | − | − | − | − | −0.188 | − |

| WTI+t | 0.022 | 0.033 | −0.082 | 0.199 b | 0.099 b | −0.035 | 0.061 c |

| WTI+t−1 | 0.077 b | − | 0.086 c | 0.011 | − | −0.019 | − |

| WTI+t−2 | − | − | − | 0.167 b | − | 0.075 c | − |

| WTI+t−3 | − | − | − | −0.164 b | − | − | − |

| WTI−t | −0.024 | 0.021 | 0.011 | 0.133 | 0.083 c | 0.011 | 0.047 |

| WTI−t−1 | −0.141 b | − | − | − | − | −0.074 | − |

| WTI−t−2 | − | − | − | − | − | −0.114 b | − |

| ECMt−1 | −0.951 a | −1.004 a | −0.947 a | −1.023 a | −1.143 a | −1.258 a | −1.105 a |

| Panel B: Long-run asymmetric effects | |||||||

| C | −0.012 | 0.009 | 0.008 | −0.014 | 0.021 | 0.002 | 0.007 |

| EPU+ | 0.086 b | −0.027 | −0.032 | 0.031 | 0.001 | −0.050 c | −0.041 c |

| EPU− | 0.054 | −0.035 c | −0.045 | 0.004 | −0.001 | −0.061 b | −0.051 b |

| VIX+ | −0.091 a | −0.078 a | −0.083 b | −0.411 a | −0.109 a | −0.109 a | −0.114 a |

| VIX− | −0.088 a | −0.070 a | −0.068 c | −0.420 a | −0.092 a | −0.099 a | −0.098 c |

| GPR+ | −0.011 | 0.013 | −0.094 b | 0.048 | −0.026 | −0.021 | 0.004 |

| GPR− | 0.044 | 0.020 | −0.077 c | 0.078 | −0.021 | −0.011 | 0.010 |

| GD+ | 0.360 a | 0.274 a | 0.354 b | 0.794 a | 0.432 a | 0.391 a | 0.565 a |

| GD− | 0.293 b | 0.261 a | 0.273 b | 0.821 a | 0.341 a | 0.351 a | 0.520 a |

| WTI+ | −0.023 | 0.033 | −0.152 b | 0.124 | 0.087 a | 0.048 | 0.055 c |

| WTI− | −0.062 | 0.021 | −0.171 b | 0.130 | 0.072 c | 0.039 | 0.042 |

| Panel C: Diagnostic tests | |||||||

| Serial correlation | 0.871 | 1.289 | 0.029 | 1.078 | 5.352 c | 0.352 | 1.725 |

| Heteroskedasticity | 25.307 | 11.401 | 35.321 b | 21.573 | 9.459 | 39.559 a | 31.562 a |

| Normality | 1.015 | 0.322 | 1.428 | 1.824 | 0.349 | 9.203 a | 0.777 |

| Variables | THA | MYS | IDN | BRA | AFR | TAI | KOR |

|---|---|---|---|---|---|---|---|

| Panel A: Short-run | |||||||

| EPU | 6.547 b | 0.027 | 0.004 | 0.148 | 1.525 | 1.336 | 0.204 |

| VIX | 0.079 | 0.760 | 0.043 | 2.991 c | 0.082 | 4.631 b | 0.034 |

| GPR | 10.669 a | 0.174 | 28.532 a | 0.640 | 7.205 a | 0.400 | 1.895 |

| GD | 0.545 | 0.006 | 0.066 | 0.260 | 0.227 | 6.664 b | 3.407 c |

| WTI | 9.271 a | 0.011 | 0.001 | 0.549 | 0.355 | 13.713 a | 0.035 |

| Panel B: Long-run | |||||||

| EPU | 4.956 b | 0.765 | 0.597 | 1.081 | 0.016 | 0.939 | 0.638 |

| VIX | 0.224 | 1.246 | 1.644 | 0.252 | 2.998 c | 1.623 | 3.197 c |

| GPR | 8.360 a | 0.342 | 0.529 | 0.647 | 0.084 | 0.459 | 0.121 |

| GD | 1.319 | 0.088 | 1.243 | 0.072 | 2.385 | 0.782 | 0.723 |

| WTI | 3.696 c | 0.775 | 0.630 | 0.028 | 0.555 | 0.286 | 0.566 |

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2024 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Nittayakamolphun, P.; Bejrananda, T.; Pholkerd, P. Asymmetric Effects of Uncertainty and Commodity Markets on Sustainable Stock in Seven Emerging Markets. J. Risk Financial Manag. 2024, 17, 155. https://doi.org/10.3390/jrfm17040155

Nittayakamolphun P, Bejrananda T, Pholkerd P. Asymmetric Effects of Uncertainty and Commodity Markets on Sustainable Stock in Seven Emerging Markets. Journal of Risk and Financial Management. 2024; 17(4):155. https://doi.org/10.3390/jrfm17040155

Chicago/Turabian StyleNittayakamolphun, Pitipat, Thanchanok Bejrananda, and Panjamapon Pholkerd. 2024. "Asymmetric Effects of Uncertainty and Commodity Markets on Sustainable Stock in Seven Emerging Markets" Journal of Risk and Financial Management 17, no. 4: 155. https://doi.org/10.3390/jrfm17040155

APA StyleNittayakamolphun, P., Bejrananda, T., & Pholkerd, P. (2024). Asymmetric Effects of Uncertainty and Commodity Markets on Sustainable Stock in Seven Emerging Markets. Journal of Risk and Financial Management, 17(4), 155. https://doi.org/10.3390/jrfm17040155