The Impact of Fintech and Digital Financial Services on Financial Inclusion in India

Abstract

1. Introduction

2. Reviews of Literature

3. Research Gap and Objectives

4. Research Methodology

4.1. Sample Design

4.2. Data Collection Method

4.3. Results

4.4. Estimates

5. Conclusions

6. Implications

7. Scope of Future Research

Author Contributions

Funding

Informed Consent Statement

Data Availability Statement

Conflicts of Interest

References

- Ajzen, Icek. 1991. The Theory of Planned Behavior. Organizational Behavior and Human Decision Processes 50: 179–211. [Google Scholar] [CrossRef]

- Anagnostopoulos, Ioannis. 2018. Fintech and Regtech: Impact on Regulators and Banks. Journal of Economics and Business 100: 7–25. [Google Scholar] [CrossRef]

- Aron, Janine. 2018. Mobile Money and the Economy: A Review of the Evidence. The World Bank Research Observer 33: 135–88. [Google Scholar] [CrossRef]

- Bagozzi, Richard P., and Youjae Yi. 1988. On the Evaluation of Structural Equation Models. Journal of the Academy of Marketing Science 16: 74–94. [Google Scholar] [CrossRef]

- Banna, Hasanul, M. Kabir Hassan, and Mamunur Rashid. 2021. Fintech-Based Financial Inclusion and Bank Risk-Taking: Evidence from OIC Countries. Journal of International Financial Markets, Institutions and Money 75: 101447. [Google Scholar] [CrossRef]

- Black, William, and Barry. J. Babin. 2019. Multivariate Data Analysis: Its Approach, Evolution, and Impact. In The Great Facilitator. Berlin/Heidelberg: Springer, pp. 121–30. [Google Scholar] [CrossRef]

- Burns, Scott. 2018. M-Pesa and the ‘Market-Led’ Approach to Financial Inclusion. Economic Affairs 38: 406–21. [Google Scholar] [CrossRef]

- Cecchetti, Stephen G., and Kermit Schoenholtz. 2020. Finance and Technology: What Is Changing and What Is Not. CEPR Discussion Papers 15352: 1–40. [Google Scholar]

- Chang, Victor, Partricia Baudier, Hui Zhang, Qianwen Xu, Jingqi Zhang, and Mitra Arami. 2020. How Blockchain can Impact Financial Services–the Overview, Challenges and Recommendations from Expert Interviewees. Technological Forecasting and Social Change 158: 120–66. [Google Scholar] [CrossRef]

- Chavan, Palavi, and Bhaskar Birajdar. 2009. Micro Finance and Financial Inclusion of Women: An Evaluation. Reserve Bank of India Occasional Papers 30: 109–29. [Google Scholar]

- Chouhan, Vineet, Bibhas Chandra, Pranav Saraswat, and Shubham Goswami. 2020. Developing Sustainable Accounting Framework for Cement Industry: Evidence from India. Finance India 34: 1459–74. [Google Scholar]

- Chouhan, Vineet, Raj Bahadur Sharma, and Shubham Goswami. 2021a. Factor Affecting Audit Quality: A study of the companies listed in Bombay Stock Exchange (BSE.). International Journal of Management 25: 989–99. [Google Scholar]

- Chouhan, Vineet, Raj Bahadur Sharma, and Shubham Goswami. 2021b. Sustainable Reporting: A Case Study of Selected Cement Companies of India. Accounting 7: 151–60. [Google Scholar] [CrossRef]

- Chouhan, Vineet, Raj Bahadur Sharma, Shubham Goswami, and Abdul Wahid Ahmed Hashed. 2021c. Measuring Challenges in Adoption of Sustainable Environmental Technologies in Indian Cement Industry. Accounting 7: 339–48. [Google Scholar] [CrossRef]

- Chouhan, Vineet, Shubham Goswami, and Raj Bahadur Sharma. 2021d. Use of Proactive Spare Parts Inventory Management (PSPIM) Techniques for Material Handling Vis-À-Vis Cement Industry. Materials Today: Proceedings 45: 4383–89. [Google Scholar] [CrossRef]

- Chouhan, Vineet, Shubham Goswami, Manish Dadhich, Pranav Saraswat, and Pushpkant Shakdwipee. 2021e. Chapter 5 Emerging Opportunities for the Application of Blockchain for Energy Efficiency. In Blockchain 3.0 for Sustainable Development. Edited by Deepak Khazanchi, Ajay Kumar Vyas, Kamal Kant Hiran and Sanjeevikumar Padmanaban. Boston: De Gruyter, pp. 63–88. [Google Scholar] [CrossRef]

- Dang, Van Cuong, and Quang Khai Nguyen. 2021. Internal Corporate Governance and Stock Price Crash Risk: Evidence from Vietnam. Journal of Sustainable Finance & Investment. [Google Scholar] [CrossRef]

- Davis, Fred D., and Davis Fred. 1989. Perceived Usefulness, Perceived Ease of Use, and User Acceptance of Information Technology. MIS Quarterly 13: 319. [Google Scholar] [CrossRef]

- Demir, Ayse, Vanesa Pesqué-Cela, Yener Altunbas, and Victor Murinde. 2022. Fintech, Financial Inclusion and Income Inequality: A Quantile Regression Approach. The European Journal of Finance 28: 86–107. [Google Scholar] [CrossRef]

- Duncombe, Richard, and Richard Boateng. 2009. Mobile Phones and Financial Services in Developing Countries: A Review of Concepts, Methods, Issues, Evidence and Future Research Directions. Third World Quarterly 30: 1237–58. [Google Scholar] [CrossRef]

- Frost, Jon, Leonardo Gambacorta, Yi Huang, Hyun Song Shin, and Pablo Zbinden. 2019. BigTech and the Changing Structure of Financial Intermediation. Economic Policy 34: 761–99. [Google Scholar] [CrossRef]

- Gautam, Amit, and Siddhartha Rawat. 2017. Cashless and Digital Economy and its Effect on Financial Inclusion in India. Financial Sector in India 20: 77–85. [Google Scholar]

- Ghosh, Saibal. 2020. Financial Inclusion in India: Does Distance Matter? South Asia Economic Journal 21: 216–38. [Google Scholar] [CrossRef]

- Haque, Sabrina Sharmin, Monica Yanez-Pagans, Yurani Arias-Granada, and George Joseph. 2020. Water and Sanitation in Dhaka Slums: Access, Quality, and Informality in Service Provision. Water International 45: 791–811. [Google Scholar] [CrossRef]

- Iqbal, Sana, Ahmad Nawaz, and Sadaf Ehsan. 2019. Financial Performance and Corporate Governance in Microfinance: Evidence from Asia. Journal of Asian Economics 60: 1–13. [Google Scholar] [CrossRef]

- Jack, William, and Tavneet Suri. 2014. Risk Sharing and Transactions Costs: Evidence from Kenya’s Mobile Money Revolution. American Economic Review 104: 183–223. [Google Scholar] [CrossRef]

- Khan, Harun R. 2012. Issues and Challenges in Financial Inclusion: Policies, Partnerships, Processes and Products. Korea 18: 84–17. [Google Scholar]

- Khan, Shagufta, Vineet Chouhan, Bibhas Chandra, and Shubham Goswami. 2014. Sustainable Accounting Reporting Practices of Indian Cement Industry: An Exploratory Study. Uncertain Supply Chain Management 2: 61–72. [Google Scholar] [CrossRef]

- Kim, Minjin, Hanah Zoo, Heejin Lee, and Juhee Kang. 2018. Mobile Financial Services, Financial Inclusion, and Development: A Systematic Review of Academic Literature. The Electronic Journal of Information Systems in Developing Countries 84: e12044. [Google Scholar] [CrossRef]

- Li, Feng, Hui Lu, Meiqian Hou, Kangle Cui, and Mehdi Darbandi. 2021. Customer Satisfaction with Bank Services: The Role of Cloud Services, Security, E-Learning and Service Quality. Technology in Society 64: 101487. [Google Scholar] [CrossRef]

- Mader, Philip. 2018. Contesting Financial Inclusion. Development and Change 49: 461–83. [Google Scholar] [CrossRef]

- Maina, Enock M., Vineet Chouhan, and Shubham Goswami. 2020. Measuring Behavioral Aspect of IFRS Implementation in India and Kenya. International Journal of Scientific and Technology Research 9: 2045–48. [Google Scholar]

- Mannan, Morshed, and Simon Pek. 2021. Solidarity in the Sharing Economy: The Role of Platform Cooperatives at the Base of the Pyramid. In Sharing Economy at the Base of the Pyramid. Singapore: Springer, pp. 249–79. [Google Scholar] [CrossRef]

- Masino, Serena, and Miguel Niño-Zarazúa. 2018. Improving Financial Inclusion through the Delivery of Cash Transfer Programmes: The Case of Mexico’s Progresa-Oportunidades-Prospera Programme. The Journal of Development Studies 56: 151–68. [Google Scholar] [CrossRef]

- Mbiti, Isaac, and David N. Weil. 2013. The Home Economics of E-Money: Velocity, Cash Management, and Discount Rates of M-Pesa Users. American Economic Review 103: 369–74. [Google Scholar]

- Menz, Markus, Sven Kunisch, Julian Birkinshaw, David J. Collis, Nicolas J. Foss, Robert E. Hoskisson, and John E. Prescott. 2021. Corporate Strategy and the Theory of the Firm in the Digital Age. Journal of Management Studies 58: 1695–720. [Google Scholar] [CrossRef]

- Metzger, Martina, Tim Riedler, and Jennifer Pédussel Wu. 2019. Migrant Remittances: Alternative Money Transfer Channels, Working Paper, No. 127/2019. Berlin: Hochschule für Wirtschaft und Recht Berlin, Institute for International Political Economy (IPE). Available online: https://www.econstor.eu/bitstream/10419/204586/1/1678825786.pdf (accessed on 12 January 2023).

- Mia, Md Aslam, Miao Zhang, Cheng Zhang, and Yoomi Kim. 2018. Are Microfinance Institutions in South-East Asia Pursuing Objectives of Greening the Environment? Journal of the Asia Pacific Economy 23: 229–45. [Google Scholar] [CrossRef]

- Nguyen, Quang Khai. 2022. The effect of FinTech development on financial stability in an emerging market: The role of market discipline. Research in Globalization 5: 100105. [Google Scholar] [CrossRef]

- Okoye, Lawrence Uchenna, Kehinde Adekunle Adetiloye, Olayinka Erin, and Nwanneka Judith. 2017. Financial Inclusion as a Strategy for Enhanced Economic Growth and Development. Journal of Internet Banking and Commerce 22: 1–14. [Google Scholar]

- Omojolaibi, Joseph A., Adaobi Geraldine Okudo, and Deborah A. Shojobi. 2019. Are Women Financially Excluded from Formal Financial Services? Analysis of Some Selected Local Government Areas in Lagos State, Nigeria. Journal of Economic and Social Thought 6: 16–47. [Google Scholar]

- Orlov, Evgeniy Vladimirovi, Tatyana Mikhailo Rogulenko, Oleg Alexandr Smolyakov, Nataliya Vladimiro Oshovskaya, Tatiana Ivan Zvorykina, Victor Grigore Rostanets, and Elena Petrov Dyundik. 2021. Comparative Analysis of the Use of Kanban and Scrum Methodologies in IT Projects. Universal Journal of Accounting and Finance 9: 693–700. [Google Scholar] [CrossRef]

- Oskarsson, Patrik. 2018. Landlock: Paralyzing Dispute over Minerals on Adivasi Land in India. Canberra: Austrialian National University Press, p. 204. [Google Scholar] [CrossRef]

- Rathod, Saikumar, and Shiva Krishna Prasad Arelli. 2013. Aadhaar and Financial Inclusion: A Proposed Framework to Provide Basic Financial Services in Unbanked Rural India. In Driving the Economy through Innovation and Entrepreneurship. New Delhi: Springer New Delhi, pp. 731–44. [Google Scholar] [CrossRef]

- Reddy, Amith Kumar. 2021. Impact of E-Banking on Customer Satisfaction. PalArch’s Journal of Archaeology of Egypt/Egyptology 18: 4220–31. [Google Scholar]

- Russell, James A. 1980. A circumplex model of affect. Journal of Personality and Social Psychology 39: 1161–78. [Google Scholar] [CrossRef]

- Schuetz, Sebastian, and Viswanath Venkatesh. 2020. Blockchain, Adoption, and Financial Inclusion in India: Research Opportunities. International Journal of Information Management 52: 101936. [Google Scholar] [CrossRef]

- Singh, N. Dhaneshwar, and H. Ramananda Singh. 2012. Social Impact of Microfinance on SHG Members: A Case Study of Manipur. Prabandhan: Indian Journal of Management 5: 43–50. [Google Scholar] [CrossRef]

- Singh, Surender, S. K. Goyal, and Supran Kumar Sharma. 2013. Technical Efficiency and its Determinants in Microfinance Institutions in India: A Firm Level Analysis. Journal of Innovation Economics Management 1: 15–31. [Google Scholar] [CrossRef]

- Thomas, Howard, and Yuwa Hedrick-Wong. 2019. How Digital Finance and Fintech Can Improve Financial Inclusion 1. In Inclusive Growth. Bingley: Emerald Publishing Limited, pp. 27–41. [Google Scholar]

- Wieser, Christina, Miriam Bruhn, Johannes Philipp Kinzinger, Christian Simon Ruckteschler, and Soren Heitmann. 2019. The Impact of Mobile Money on Poor Rural Households: Experimental Evidence from Uganda. World Bank Policy Research Working Paper No. 8913. Available online: https://openknowledge.worldbank.org/handle/10986/31978 (accessed on 12 January 2023).

- Wry, Tyler, and Yanfei Zhao. 2018. Taking Trade-offs Seriously: Examining the Contextually Contingent Relationship between Social Outreach Intensity and Financial Sustainability in Global Microfinance. Organization Science 29: 507–28. [Google Scholar] [CrossRef]

{kind=link}

{kind=link}

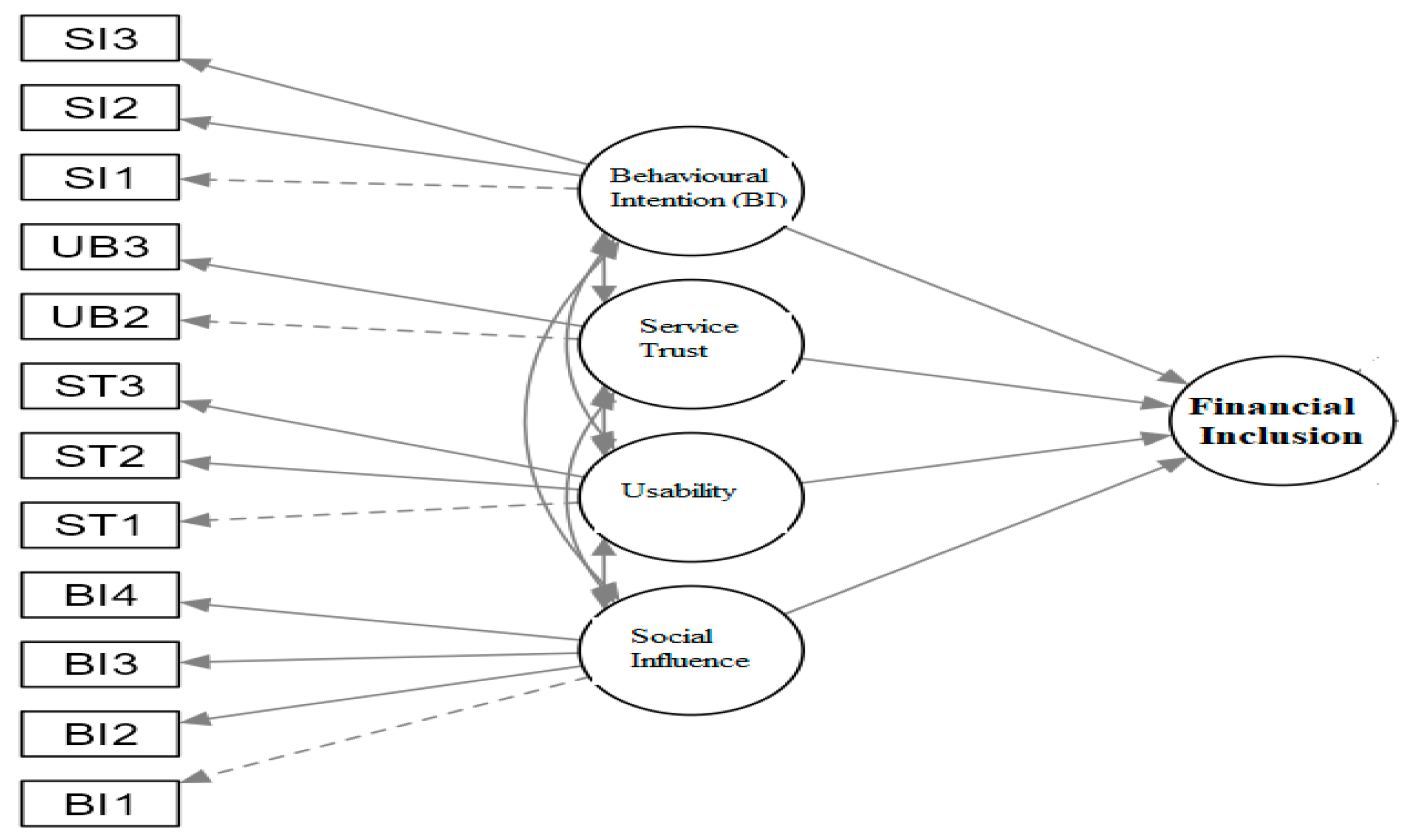

| Construct | Code | Variable |

|---|---|---|

| Behavioral intention (BI) | BI1 | I intend to contribute to the expansion of access to financial services through the application of fintech. |

| BI2 | I will always give first priority to using mobile services based on financial technology whenever possible. | |

| BI3 | I intend to keep implementing fintech for financial inclusion. | |

| BI4 | It is my Intention to contribute to financial inclusion through the application of fintech. | |

| Social influence (S.I.) | SI1 | Financial technology and services for the financially excluded are things I am supposed to use. |

| SI2 | Peers who have an impact on my decisions recommended that I try out financial inclusion offerings powered by fintech. | |

| SI3 | It is more likely that I will use financial inclusion services based on fintech if they are judged well by people whose opinion I value. | |

| Service trust (S.T.) | ST1 | Services for the financially excluded that are based on fintech have been proven to be reliable. |

| ST2 | Financial technology (fintech)-based services for the underserved must be handled with care. | |

| ST3 | Due to my prior positive experience with such services, I have faith in services based on financial technology. | |

| Usability (U.B.) | UB1 | When it comes to financial inclusion, I am likely to use services powered by financial technology. |

| UB2 | I regularly make use of services that promote financial inclusion that are enabled by advances in financial technology. | |

| UB3 | Several of the services that are based on fintech are quite important to me. | |

| Use of fintech for financial inclusion | FTFI1 | It is possible to employ fintech to expand access to banking services in India’s rural areas. |

| FTFI2 | Financial inclusion in India’s rural areas can be achieved through the usage of fintech by increasing household income. | |

| FTFI3 | Financial inclusion in rural India can be achieved through the usage of Fintech by increasing savings rates. |

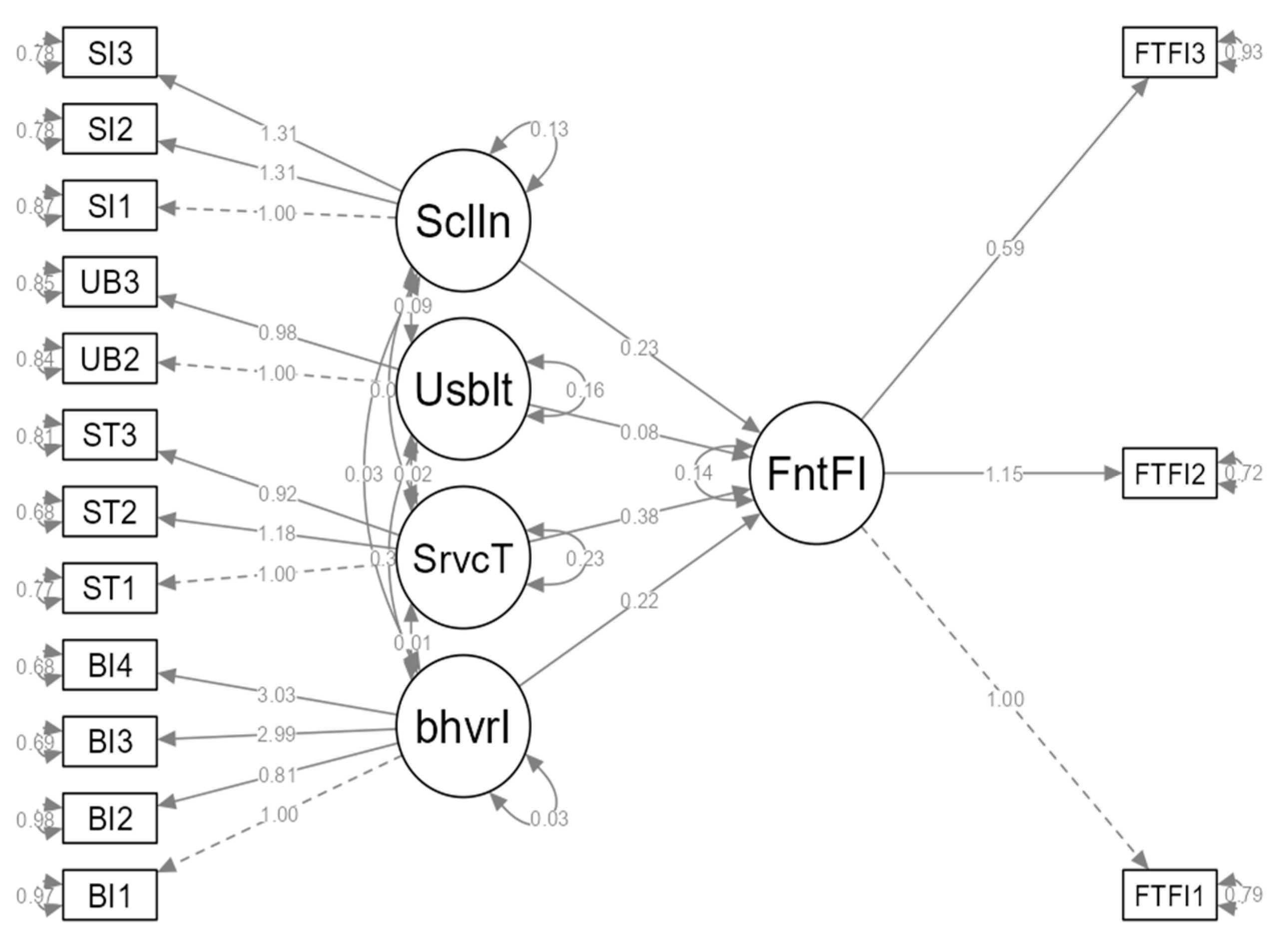

| Number of Observations | 400 |

|---|---|

| Free parameters | 85 |

| Model | Behavioral intention = I1 + BI2 + BI3 + BI4 |

| Service trust = ST1 + ST2 + ST3 | |

| Usability = UB2 + UB3 | |

| Social influence = SI1 + SI2 + SI3 | |

| Fintech for financial inclusion = FTFI1 + FTFI2 + FTFI3 | |

| Fintech for financial inclusion behavioral intention + service trust + usability + social influence |

| Model | |

|---|---|

| Comparative fit index (CFI) | 0.997 |

| Tucker–Lewis index (TLI) | 0.996 |

| 95% Confidence Intervals | ||||||||

|---|---|---|---|---|---|---|---|---|

| Dep | Pred | Estimate | SE | Lower | Upper | β | z | p |

| Fintech for financial inclusion | Behavioral intention | 0.2221 | 0.0860 | 0.0535 | 0.391 | 0.0902 | 2.58 | 0.010 |

| Fintech for financial inclusion | Service trust | 0.3823 | 0.1560 | 0.0764 | 0.688 | 0.3968 | 2.45 | 0.014 |

| Fintech for financial inclusion | Usability | 0.0839 | 0.0247 | 0.0355 | 0.132 | 0.0721 | 3.40 | <0.001 |

| Fintech for financial inclusion | Social influence | 0.2304 | 0.1795 | −0.1215 | 0.582 | 0.1794 | 1.28 | 0.199 |

| 95% Confidence Intervals | ||||||||

|---|---|---|---|---|---|---|---|---|

| Latent | Observed | Estimate | SE | Lower | Upper | β | z | p |

| Behavioral intention | BI1 | 1.000 | 0.00000 | 1.000 | 1.000 | 0.187 | ||

| BI2 | 0.814 | 0.12667 | 0.566 | 1.062 | 0.152 | 6.43 | <0.001 | |

| BI3 | 2.988 | 0.35217 | 2.297 | 3.678 | 0.557 | 8.48 | <0.001 | |

| BI4 | 3.030 | 0.35601 | 2.333 | 3.728 | 0.565 | 8.51 | <0.001 | |

| Service trust | ST1 | 1.000 | 0.00000 | 1.000 | 1.000 | 0.477 | ||

| ST2 | 1.183 | 0.23975 | 0.713 | 1.653 | 0.564 | 4.94 | <0.001 | |

| ST3 | 0.915 | 0.16722 | 0.588 | 1.243 | 0.437 | 5.47 | <0.001 | |

| Usability | UB1 | 1.000 | 0.00000 | 1.000 | 1.000 | 0.395 | ||

| UB2 | 0.983 | 0.00503 | 0.973 | 0.993 | 0.389 | 195.42 | <0.001 | |

| Social influence | SI1 | 1.000 | 0.00000 | 1.000 | 1.000 | 0.358 | ||

| SI2 | 1.307 | 0.37785 | 0.566 | 2.048 | 0.468 | 3.46 | <0.001 | |

| SI3 | 1.313 | 0.37914 | 0.570 | 2.056 | 0.470 | 3.46 | <0.001 | |

| Fintech for financial inclusion | FTFI1 | 1.000 | 0.00000 | 1.000 | 1.000 | 0.460 | ||

| FTFI2 | 1.148 | 0.24792 | 0.662 | 1.634 | 0.528 | 4.63 | <0.001 | |

| FTFI3 | 0.592 | 0.16694 | 0.265 | 0.919 | 0.272 | 3.55 | <0.001 | |

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2023 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Asif, M.; Khan, M.N.; Tiwari, S.; Wani, S.K.; Alam, F. The Impact of Fintech and Digital Financial Services on Financial Inclusion in India. J. Risk Financial Manag. 2023, 16, 122. https://doi.org/10.3390/jrfm16020122

Asif M, Khan MN, Tiwari S, Wani SK, Alam F. The Impact of Fintech and Digital Financial Services on Financial Inclusion in India. Journal of Risk and Financial Management. 2023; 16(2):122. https://doi.org/10.3390/jrfm16020122

Chicago/Turabian StyleAsif, Mohammad, Mohd Naved Khan, Sadhana Tiwari, Showkat K. Wani, and Firoz Alam. 2023. "The Impact of Fintech and Digital Financial Services on Financial Inclusion in India" Journal of Risk and Financial Management 16, no. 2: 122. https://doi.org/10.3390/jrfm16020122

APA StyleAsif, M., Khan, M. N., Tiwari, S., Wani, S. K., & Alam, F. (2023). The Impact of Fintech and Digital Financial Services on Financial Inclusion in India. Journal of Risk and Financial Management, 16(2), 122. https://doi.org/10.3390/jrfm16020122