Credit Access and the Firm–Government Connection: Is There Any Link?

Abstract

:1. Introduction

2. Literature Review

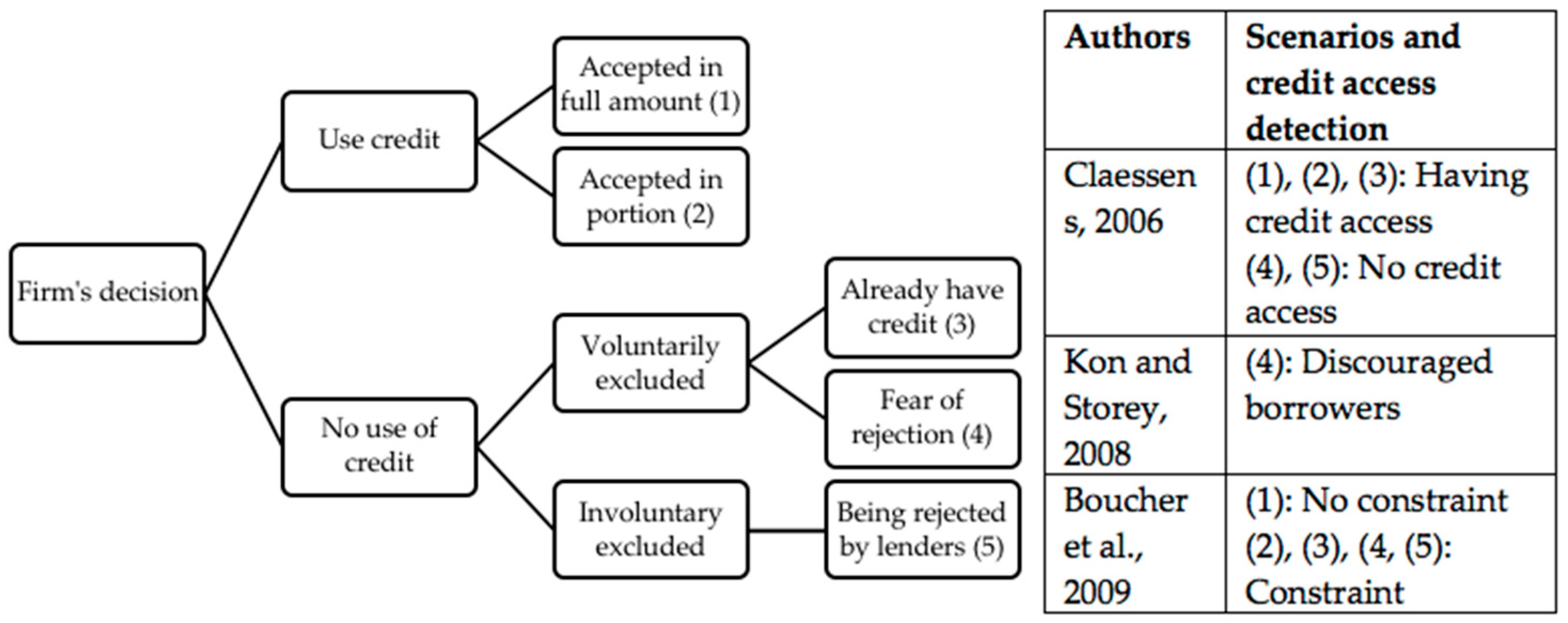

2.1. Overview on Credit Access

2.2. Government Connections and Impacts on Firms’ Business Actitivies

3. Materials and Methods

3.1. Research Design and Data Collection

3.2. Empirical Models

3.3. Variables Descriptives

4. Main Findings

4.1. Descriptives Statistic

4.2. Multivariate Analysis

4.2.1. Determinants of Credit Access

4.2.2. Credit Access and Firm–Government Connections

4.3. Other Measurements of Firm–Government Connections

5. Conclusions

Author Contributions

Funding

Data Availability Statement

Conflicts of Interest

References

- Acemoglu, Daron, and James Robinson. 2008. The Role of Institutions in Growth and Development. Washington, DC: World Bank, vol. 10. [Google Scholar]

- Alence, Rod. 2004. Political institutions and developmental governance in sub-Saharan Africa. The Journal of Modern African Studies 42: 163–87. [Google Scholar] [CrossRef]

- Alonso, José Antonio, and Carlos Garcimartín. 2013. The determinants of institutional quality. More on the debate. Journal of International Development 25: 206–26. [Google Scholar] [CrossRef]

- Andrieu, Guillaume, Raffaele Staglianò, and Peter Van Der Zwan. 2018. Bank debt and trade credit for SMEs in Europe: Firm-, industry-, and country-level determinants. Small Business Economics 51: 245–64. [Google Scholar] [CrossRef]

- Ault, Joshua. 2016. An institutional perspective on the social outcome of entrepreneurship: Commercial microfinance and inclusive markets. Journal of International Business Studies 47: 951–67. [Google Scholar] [CrossRef]

- Ayyagari, Meghana, Asli Demirgüç-Kunt, and Vojislav Maksimovic. 2011. Firm innovation in emerging markets: The role of finance, governance, and competition. Journal of Financial and Quantitative Analysis 46: 1545–80. [Google Scholar] [CrossRef]

- Banerji, Sanjay, Meryem Duygun, and Mohamed Shaban. 2018. Political connections, bailout in financial markets and firm value. Journal of Corporate Finance 50: 388–401. [Google Scholar] [CrossRef]

- Beck, Thorsten, and Asli Demirgüç-Kunt. 2008. Access to finance: An unfinished agenda. The World Bank Economic Review 22: 383–96. [Google Scholar] [CrossRef]

- Beck, Thorsten, Asli Demirgüç-Kunt, and Patrick Honohan. 2009. Access to Financial Services: Measurement, Impact, and Policies. World Bank Research Observer 24: 119–45. [Google Scholar] [CrossRef]

- Berger, Allen N., and Gregory F. Udell. 1998. The economics of small business finance: The roles of private equity and debt markets in the financial growth cycle. Journal of Banking & Finance 22: 613–73. [Google Scholar]

- Bonnet, Jean, Sylvie Cieply, and Marcus Dejardin. 2016. Credit rationing or overlending? An exploration into financing imperfection. Applied Economics 48: 5563–80. [Google Scholar] [CrossRef]

- Boucher, Stephen R., Catherine Guirkinger, and Carolina Trivelli. 2009. Direct elicitation of credit constraints: Conceptual and practical issues with an application to Peruvian agriculture. Economic Development and Cultural Change 57: 609–40. [Google Scholar] [CrossRef]

- Brown, Jeffrey R., and Jiekun Huang. 2020. All the president’s friends: Political access and firm value. Journal of Financial Economics 138: 415–31. [Google Scholar] [CrossRef]

- Chaudhry, Sohail, Li Da Xu, and Xiong Fei Cao. 2018. Technological Entrepreneurship and Socio-Economic Change in BRIC Countries. Amsterdam: Elsevier, pp. 64–65. [Google Scholar]

- Chaudhuri, Kausik, Subash Sasidharan, and Rajesh Seethamma Natarajan Raj. 2020. Gender, small firm ownership, and credit access: Some insights from India. Small Business Economics 54: 1165–81. [Google Scholar] [CrossRef]

- Claessens, Stijn. 2006. Access to financial services: A review of the issues and public policy objectives. The World Bank Research Observer 21: 207–40. [Google Scholar] [CrossRef]

- Claessens, Stijn, and Luc Laeven. 2004. What drives bank competition? Some international evidence. Journal of Money, Credit and Banking 36: 563–83. [Google Scholar] [CrossRef]

- Coeurdacier, Nicolas, Stéphane Guibaud, and Keyu Jin. 2015. Credit constraints and growth in a global economy. American Economic Review 105: 2838–81. [Google Scholar] [CrossRef]

- Dang, Quyen Thao, Pavlina Jasovska, and Hussain Gulzar Rammal. 2020. International business-government relations: The risk management strategies of MNEs in emerging economies. Journal of World Business 55: 101042. [Google Scholar] [CrossRef]

- Diagne, Aliou, and Manfred Zeller. 2001. Access to Credit and Its Impact on Welfare in Malawi. Washington, DC: International Food Policy Research Institute, vol. 116. [Google Scholar]

- Dollar, David, and Aart Kraay. 2003. Institutions, trade, and growth. Journal of Monetary Economics 50: 133–62. [Google Scholar] [CrossRef]

- Fowowe, Babajide. 2017. Access to finance and firm performance: Evidence from African countries. Review of Development Finance 7: 6–17. [Google Scholar] [CrossRef]

- Getachew, Yoseph Yilma. 2016. Credit constraints, growth and inequality dynamics. Economic Modelling 54: 364–76. [Google Scholar] [CrossRef]

- Hawawini, Gabriel, Venkat Subramanian, and Paul Verdin. 2004. The home country in the age of globalization: How much does it matter for firm performance? Journal of World Business 39: 121–35. [Google Scholar] [CrossRef]

- Helmke, Gretchen, and Steven Levitsky. 2004. Informal institutions and comparative politics: A research agenda. Perspectives on Politics 2: 725–40. [Google Scholar] [CrossRef]

- Hewa Wellalage, Nirosha, Stuart Locke, and Helen Samujh. 2020. Firm bribery and credit access: Evidence from Indian SMEs. Small Business Economics 55: 283–304. [Google Scholar] [CrossRef]

- Jaffee, Dwight, and Joseph Stiglitz. 1990. Credit rationing. Handbook of Monetary Economics 2: 837–88. [Google Scholar]

- Jiang, Fuxiu, and Kenneth A. Kim. 2015. Corporate Governance in China: A Modern Perspective. Amsterdam: Elsevier, pp. 190–216. [Google Scholar]

- Khan, Safi Ullah. 2022. Financing constraints and firm-level responses to the COVID-19 pandemic: International evidence. Research in International Business and Finance 59: 101545. [Google Scholar] [CrossRef] [PubMed]

- Khwaja, Asim Ijaz, and Atif Mian. 2005. Do lenders favor politically connected firms? Rent provision in an emerging financial market. The Quarterly Journal of Economics 120: 1371–411. [Google Scholar] [CrossRef]

- Kistruck, Geoffrey M., Justin W. Webb, Christopher J. Sutter, and Anastasia VG Bailey. 2015. The double-edged sword of legitimacy in base-of-the-pyramid markets. Journal of Business Venturing 30: 436–51. [Google Scholar] [CrossRef]

- Kon, Yoshinori, and David J. Storey. 2003. A theory of discouraged borrowers. Small Business Economics 21: 37–49. [Google Scholar] [CrossRef]

- Krasniqi, Besnik A. 2007. Barriers to entrepreneurship and SME growth in transition: The case of Kosova. Journal of Developmental Entrepreneurship 12: 71–94. [Google Scholar] [CrossRef]

- Krasniqi, Besnik A., and Colin C. Williams. 2020. Does informality help entrepreneurs achieve firm growth? Evidence from a post-conflict economy. Economic Research-Ekonomska Istraživanja 33: 1581–99. [Google Scholar] [CrossRef]

- La Porta, Rafael, and Andrei Shleifer. 2014. Informality and development. Journal of Economic Perspectives 28: 109–26. [Google Scholar] [CrossRef]

- Lester, Richard H., Amy Hillman, Asghar Zardkoohi, and Albert A. Cannella Jr. 2008. Former government officials as outside directors: The role of human and social capital. Academy of Management Journal 51: 999–1013. [Google Scholar] [CrossRef]

- Li, Hongbin, Lingsheng Meng, Qian Wang, and Li-An Zhou. 2008. Political connections, financing and firm performance: Evidence from Chinese private firms. Journal of Development Economics 87: 283–99. [Google Scholar] [CrossRef]

- Linh, Ta Nhat, Dang Anh Tuan, Phan Thu Trang, Hoang Trung Lai, Do Quynh Anh, Nguyen Viet Cuong, and Philippe Lebailly. 2020. Determinants of farming households’ credit accessibility in rural areas of Vietnam: A case study in Haiphong City, Vietnam. Sustainability 12: 4357. [Google Scholar] [CrossRef]

- Lin, Karen Jingrong, Jinsong Tan, Liming Zhao, and Khondkar Karim. 2015. In the name of charity: Political connections and strategic corporate social responsibility in a transition economy. Journal of Corporate Finance 32: 327–46. [Google Scholar] [CrossRef]

- Love, Inessa. 2003. Financial development and financing constraints: International evidence from the structural investment model. The Review of Financial Studies 16: 765–91. [Google Scholar] [CrossRef]

- Luo, Yadong, and Rosalie L. Tung. 2007. International Expansion of Emerging Market Enterprises: A Springboard Perspective. Berlin/Heidelberg: Springer, pp. 481–98. [Google Scholar]

- Marquis, Christopher, and Cuili Qian. 2014. Corporate social responsibility reporting in China: Symbol or substance? Organization Science 25: 127–48. [Google Scholar] [CrossRef]

- Michelacci, Claudio, and Olmo Silva. 2007. Why so many local entrepreneurs? The Review of Economics and Statistics 89: 615–33. [Google Scholar] [CrossRef]

- Michelson, Ethan. 2006. Connected Contention: Social Resources and Petitioning the State in Rural China. Available at SSRN 922104. Available online: https://papers.ssrn.com/sol3/papers.cfm?abstract_id=922104 (accessed on 1 August 2023).

- Nikolova, Elena Veselinova, Frantisek Ricka, and Dora Simroth. 2012. Entrepreneurship in the Transition Region: An Analysis Based on the Life in Transition Survey. London: European Bank for Reconstruction and Development. [Google Scholar]

- North, Douglass C. 1990. A transaction cost theory of politics. Journal of Theoretical Politics 2: 355–67. [Google Scholar] [CrossRef]

- Ogunsade, Isaac A., and Demola Obembe. 2016. The influence of informal institutions on informal sector entrepreneurship: A study of Nigeria’s hand-woven textile industry. Journal of Small Business & Entrepreneurship 28: 413–29. [Google Scholar]

- Petrick, Martin. 2004. Farm investment, credit rationing, and governmentally promoted credit access in Poland: A cross-sectional analysis. Food Policy 29: 275–94. [Google Scholar] [CrossRef]

- Qi, Shusen, and Duc Duy Nguyen. 2021. Government connections and credit access around the world: Evidence from discouraged borrowers. Journal of International Business Studies 52: 321–33. [Google Scholar] [CrossRef]

- Rajan, Raghuram G., and Luigi Zingales. 2003. The great reversals: The politics of financial development in the twentieth century. Journal of Financial Economics 69: 5–50. [Google Scholar] [CrossRef]

- Schaffartzik, Anke, Andreas Mayer, Simone Gingrich, Nina Eisenmenger, Christian Loy, and Fridolin Krausmann. 2014. The global metabolic transition: Regional patterns and trends of global material flows, 1950–2010. Global Environmental Change 26: 87–97. [Google Scholar] [CrossRef] [PubMed]

- Siqueira, Ana Cristina O., Justin W. Webb, and Garry D. Bruton. 2016. Informal entrepreneurship and industry conditions. Entrepreneurship Theory and Practice 40: 177–200. [Google Scholar] [CrossRef]

- Skinner, Burrhus Frederic. 1950. Are theories of learning necessary? Psychological Review 57: 193. [Google Scholar] [CrossRef]

- Smallbone, David, and Friederike Welter. 2012. Entrepreneurship and institutional change in transition economies: The Commonwealth of Independent States, Central and Eastern Europe and China compared. Entrepreneurship & Regional Development 24: 215–33. [Google Scholar]

- Stefani, Maria Lucia, and Valerio Vacca. 2015. Small firms’ credit access in the euro area: Does gender matter? CESifo Economic Studies 61: 165–201. [Google Scholar] [CrossRef]

- United Nations New York. 2020. World Economic Situation and Prospects. Available online: https://www.un.org/development/desa/dpad/wp-content/uploads/sites/45/WESP2020_Annex.pdf (accessed on 1 August 2023).

- Wang, Heli, and Cuili Qian. 2011. Corporate philanthropy and corporate financial performance: The roles of stakeholder response and political access. Academy of Management Journal 54: 1159–81. [Google Scholar] [CrossRef]

- Wang, Yizhong, Chengxue Yao, and Di Kang. 2019. Political connections and firm performance: Evidence from government officials’ site visits. Pacific-Basin Finance Journal 57: 101021. [Google Scholar] [CrossRef]

- Webb, Justin W., Theodore A. Khoury, and Michael A. Hitt. 2020. The influence of formal and informal institutional voids on entrepreneurship. Entrepreneurship Theory and Practice 44: 504–26. [Google Scholar] [CrossRef]

- Williams, Nick, and Tim Vorley. 2015. Institutional asymmetry: How formal and informal institutions affect entrepreneurship in Bulgaria. International Small Business Journal 33: 840–61. [Google Scholar] [CrossRef]

- Wu, Jie, and Xiaoyun Chen. 2014. Home country institutional environments and foreign expansion of emerging market firms. International Business Review 23: 862–72. [Google Scholar] [CrossRef]

- Yadav, Priyanka, and Anil K. Sharma. 2015. Agriculture credit in developing economies: A review of relevant literature. International Journal of Economics and Finance 7: 219–44. [Google Scholar] [CrossRef]

- Zeller, Manfred, Aliou Diagne, and Charles Mataya. 1998. Market access by smallholder farmers in Malawi: Implications for technology adoption, agricultural productivity and crop income. Agricultural Economics 19: 219–29. [Google Scholar] [CrossRef]

- Zhang, Huiming, Lianshui Li, Dequn Zhou, and Peng Zhou. 2014. Political connections, government subsidies and firm financial performance: Evidence from renewable energy manufacturing in China. Renewable Energy 63: 330–36. [Google Scholar] [CrossRef]

{kind=link}

{kind=link}

{kind=link}

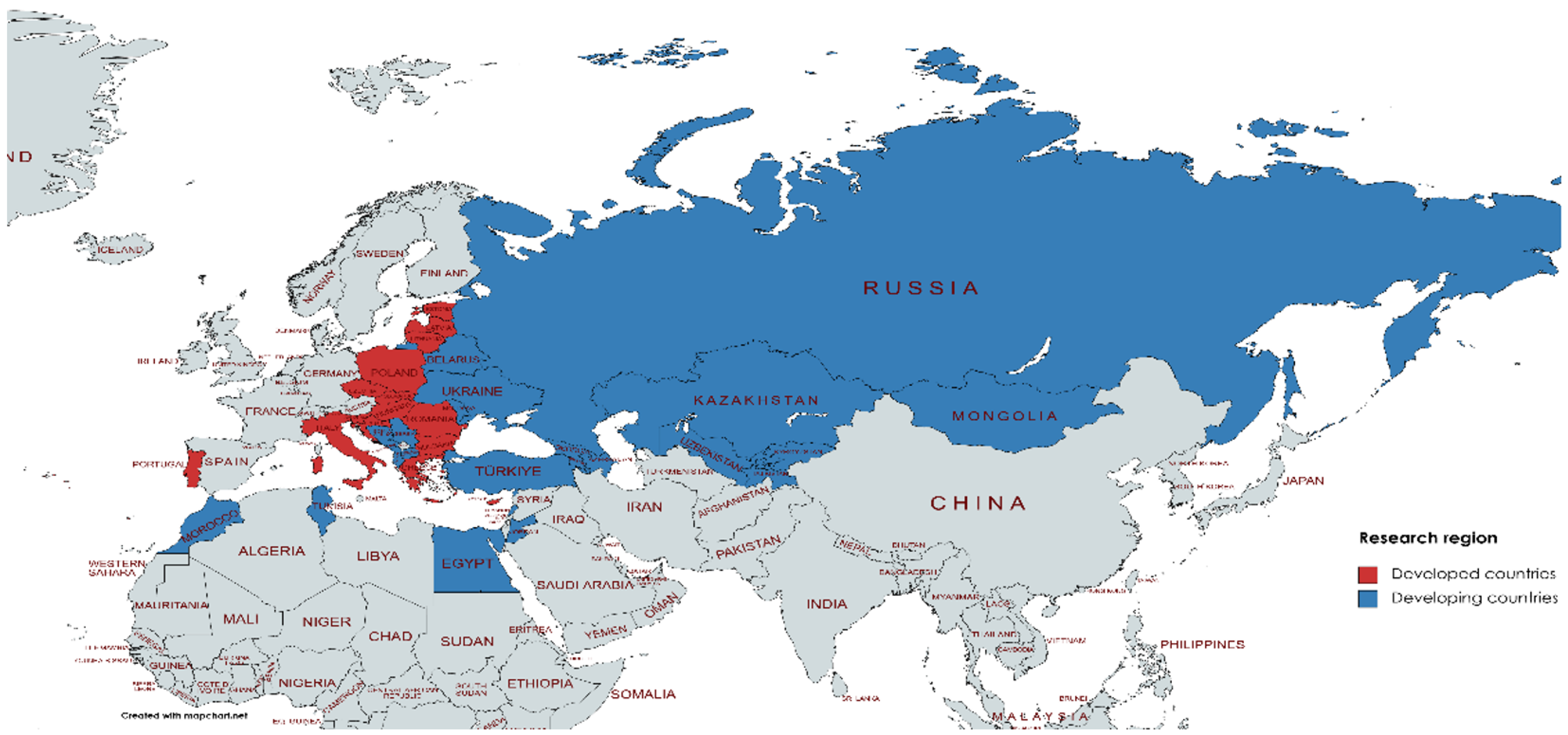

| Developed Countries | Developing Countries | |

|---|---|---|

| Italy | Transitional economies | Other |

| Cyprus | Albania | Jordan |

| Greece | Bosnia and Herzegovina | Egypt |

| Romania | Montenegro | Lebanon |

| Czech Rep. | North Macedonia | Mongolia |

| Croatia | Serbia | Morocco |

| Estonia | Armenia | Tunisia |

| Slovak Rep. | Azerbaijan | Turkey |

| Slovenia | Belarus | |

| Bulgaria | Georgia | |

| Portugal | Kyrgyz Rep. | |

| Lithuania | Kazakhstan | |

| Latvia | Moldova | |

| Hungary | Russia | |

| Poland | Tajikistan | |

| Ukraine | ||

| Uzbekistan | ||

| Variable | Description | Measurement |

|---|---|---|

| credit_access | Firm’s credit access | =1 if firms applied and got full amount of money needed =0 otherwise |

| governconnect | Firm–government connection | =1 if firms secured government contract(s) =0 otherwise |

| foreign_firm | Firms were established as foreign-owned | =1 if the percentage owned by foreigners equals or is more than 50% =0 otherwise |

| private_firm | Firms were established as private-owned | =1 if the percentage owned by domestic individuals or companies equals or is more than 50% =0 otherwise |

| state_firm | Firms were established as state-owned | =1 if the percentage owned by governments or states equals or is more than 50% =0 otherwise |

| female_mang | Female managers | =1 if there are females among managers and owners =0 otherwise |

| manager_exp | The experience of managers | Measured in years |

| lnsales | The ln of firms’ sale | |

| firm_growth | The growth of firms | =1 if firms’ sales increased =0 otherwise |

| firm_size | The size of firms | =1 if the number or permanent full-time employees in the firm equals or exceeds 100 =0 otherwise |

| innovation | The state when firms experienced innovation | =1 if firm introduced new or improved products and services during the last three years =0 otherwise |

| audited | The state when firms are audited | =1 if firms have annual financial statement checked and certified by external auditors =0 otherwise |

| purchased_credit | The percentage of total annual purchases of inputs in credit | % |

| credit_line | The existing credit line | =1 if firms have a line of credit with a financial institutions |

| main_market | The main market where firms operate | =1 if the main market of the firm’s main products is international =0 otherwise |

| developed | The status of the country where firms work | =1 if the countries that the firm works in are developed =0 otherwise |

| All Data | Access | No Access | |||||||

|---|---|---|---|---|---|---|---|---|---|

| Variable | Obs | Mean | Std. Dev. | Min | Max | Mean | Std. Dev. | Mean | Std. Dev. |

| credit_access | 9563 | 0.4504 | 0.4976 | 0 | 1 | ||||

| governconnect | 26,576 | 0.1621 | 0.3686 | 0 | 1 | 0.2360 | 0.4247 | 0.1472 | 0.3543 |

| main_market | 26,722 | 0.1229 | 0.3284 | 0 | 1 | 0.2004 | 0.4003 | 0.0719 | 0.2584 |

| foreign_firm | 26,495 | 0.0644 | 0.2454 | 0 | 1 | 0.066 | 0.2486 | 0.0343 | 0.1819 |

| private_firm | 26,503 | 0.9110 | 0.28467 | 0 | 1 | 0.9103 | 0.2858 | 0.9343 | 0.2477 |

| state_firm | 26,513 | 0.0081 | 0.0895 | 0 | 1 | 0.0146 | 0.1199 | 0.0038 | 0.0617 |

| female_mang | 26,592 | 0.2973 | 0.4570 | 0 | 1 | 0.3386 | 0.4733 | 0.2893 | 0.4535 |

| manager_exp | 26,195 | 20.3906 | 16.8349 | 1 | 70 | 22.1620 | 32.6978 | 19.2404 | 11.0484 |

| lnsales | 24,160 | 16.3315 | 2.8585 | 7.6009 | 30.6755 | 17.3030 | 2.9272 | 16.0904 | 2.7769 |

| firm_growth | 25,740 | 0.5361 | 0.4987 | 0 | 1 | 0.5995 | 0.4900 | 0.4817 | 0.4997 |

| innovation | 26,677 | 0.2442 | 0.4296 | 0 | 1 | 0.3821328 | 0.4859 | 0.1738 | 0.3789 |

| audited | 26,380 | 0.4003 | 0.4899 | 0 | 1 | 0.5057417 | 0.5000 | 0.3370 | 0.4727 |

| purchased_credit | 24,430 | 30.3431 | 35.1561 | 0 | 100 | 42.31046 | 37.0768 | 27.6911 | 30.8691 |

| developed | 26,849 | 0.34872 | 0.4766 | 0 | 1 | 0.40065 | 0.4901 | 0.2346 | 0.4238 |

| credit_line | 26,354 | 0.35463 | 0.4784 | 0 | 1 | 0.9019334 | 0.2974 | 0.2547 | 0.4357 |

| firmsize | 26,669 | 0.2016 | 0.4012 | 0 | 1 | 0.3034965 | 0.4598 | 0.1442252 | 0.3513516 |

| Main Market | Local and National Markets | International Markets | ||||||

|---|---|---|---|---|---|---|---|---|

| Access to Credit Status | Have Access | No Access | Have Access | No Access | ||||

| Freq. | Percent | Freq. | Percent | Freq. | Percent | Freq. | Percent | |

| Having government connection | 885 | 25.92 | 723 | 14.97 | 122 | 14.20 | 44 | 11.73 |

| Not having government connection | 2.529 | 74.08 | 4108 | 85.03 | 737 | 85.80 | 331 | 88.27 |

| OLS Regression | Logit Regression | |||

|---|---|---|---|---|

| Robust | Robust | |||

| Credit_Access | Coefficient | std. err. | Coefficient | std. err. |

| governconnect | 0.0209365 ** | 0.0111234 | 0.175585 ** | 0.0929263 |

| main_market | 0.0466474 *** | 0.0128938 | 0.3834697 *** | 0.1106174 |

| foreign_firm | 0.0159856 | 0.0263647 | 0.2512683 | 0.2570128 |

| private_firm | 0.0091816 | 0.0209206 | 0.1834811 | 0.220174 |

| state_firm | 0.0083895 | 0.0561211 | −0.0088763 | 0.452529 |

| female_mang | 0.0097508 | 0.0090418 | 0.0705454 | 0.0770195 |

| manager_exp | 0.000412 *** | 0.0001215 | 0.0070458 ** | 0.0033259 |

| lnsales | 0.0278627 *** | 0.0029388 | 0.2295181 *** | 0.0251442 |

| firm_growth | 0.0196083 ** | 0.008581 | 0.2008557 *** | 0.0720461 |

| innovation | 0.0741038 *** | 0.010082 | 0.5756328 *** | 0.0825376 |

| audited | 0.043598 *** | 0.0099411 | 0.4162117 *** | 0.0802769 |

| purchased_credit | 0.0009542 *** | 0.00014 | 0.0077883 *** | 0.0011769 |

| developed | 0.2394206 *** | 0.053525 | 1.738563 *** | 0.5616032 |

| credit_line | 0.5165336 *** | 0.0109331 | 3.08098 *** | 0.0862904 |

| firmsize | −0.0004478 | 0.0127644 | −0.0368867 | 0.1091499 |

| Country FE | YES | YES | ||

| Sector FE | YES | YES | ||

| Year FE | YES | YES | ||

| Observations | 7744 | 7743 | ||

| R-squared | 0.5326 | |||

| Pseudo R2 | 0.4697 |

| Panel A. | OLS Regression | OLS Regression | ||

|---|---|---|---|---|

| Domestic Market | International Market | |||

| Robust | Robust | |||

| Credit_Access | Coefficient | std. err. | Coefficient | std. err. |

| governconnect | 0.0267812 ** | 0.0119485 | −0.0408491 | 0.0311004 |

| foreign_firm | 0.0050628 | 0.030186 | 0.0294626 | 0.0823499 |

| private_firm | 0.0151669 | 0.0215814 | −0.0092703 | 0.083758 |

| state_firm | −0.0042807 | 0.0586561 | 0.1360075 | 0.1814738 |

| female_mang | 0.0112706 | 0.0100185 | −0.0055056 | 0.0215929 |

| manager_exp | 0.0003896 *** | 0.0001056 | 0.0010589 | 0.0009832 |

| lnsales | 0.0271619 *** | 0.0031463 | 0.0358212 *** | 0.0087486 |

| firm_growth | 0.0173928 ** | 0.0093961 | 0.0368617 * | 0.0220943 |

| innovation | 0.0770364 *** | 0.0113427 | 0.055905 ** | 0.0216531 |

| audited | 0.0440751 *** | 0.0108464 | 0.0385322 | 0.0262339 |

| purchased_credit | 0.0009667 *** | 0.0001565 | 0.0009426 *** | 0.0003284 |

| developed | 0.2436328 *** | 0.0554467 | 0.1725976 | 0.1865976 |

| credit_line | 0.5139784 *** | 0.0116147 | 0.5340571 *** | 0.0337033 |

| firmsize | −0.0021074 | 0.0147374 | −0.008441 | 0.0277787 |

| Country FE | YES | YES | ||

| Sector FE | YES | YES | ||

| Year FE | YES | YES | ||

| Observations | 6685 | 1059 | ||

| R-squared | 0.5062 | 0.5478 | ||

| Panel b. | Logit Regression | Logit Regression | ||

| Domestic Market | International Market | |||

| Robust | Robust | |||

| Credit_Access | Coefficient | std. err. | Coefficient | std. err. |

| governconnect | 0.23124 ** | 0.0978012 | −0.4962416 | 0.3464139 |

| foreign_firm | 0.1628892 | 0.2801423 | 0.5210463 | 1.46363 |

| private_firm | 0.2715771 | 0.2303876 | 0.0217728 | 1.409156 |

| state_firm | −0.1127508 | 0.4499458 | 1.941971 | 2.517831 |

| female_mang | 0.0887728 | 0.0832094 | −0.0947777 | 0.2408591 |

| manager_exp | 0.0062877 | 0.0035817 | 0.0142179 | 0.010714 |

| lnsales | 0.2241249 *** | 0.0266486 | 0.4289459 *** | 0.1003604 |

| firm_growth | 0.1843081 ** | 0.077589 | 0.4244306 * | 0.2249413 |

| innovation | 0.5735981 *** | 0.0893924 | 0.6260676 *** | 0.2410605 |

| audited | 0.4228991 *** | 0.0861838 | 0.4314003 * | 0.2596691 |

| purchased_credit | 0.0076551 *** | 0.0012758 | 0.0112053 *** | 0.0034869 |

| developed | 1.854543 *** | 0.5784227 | −0.9608744 | 0.8673186 |

| credit_line | 3.103038 *** | 0.09259 | 3.486382 *** | 0.3181397 |

| firmsize | −0.0693225 | 0.1220315 | −0.1211175 | 0.3271965 |

| Country FE | YES | YES | ||

| Sector FE | YES | YES | ||

| Year FE | YES | YES | ||

| Observations | 6684 | 1013 | ||

| Pseudo R2 | 0.4553 | 0.5228 |

| OLS Regression | ||

|---|---|---|

| Robust | ||

| Credit_Access | Coefficient | std. err. |

| 1.governconnect | 0.025259 ** | 0.0117818 |

| 1.main_market | 0.0527146 *** | 0.0137319 |

| governconnect#main_market | ||

| 1 1 | −0.0404767 | 0.031968 |

| foreign_firm | 0.015928 | 0.0263334 |

| private_firm | 0.0092789 | 0.0209106 |

| state_firm | 0.0102553 | 0.0560889 |

| female_mang | 0.0099103 | 0.0090467 |

| manager_exp | 0.0004106 *** | 0.0001203 |

| lnsales | 0.0278481 *** | 0.0029382 |

| firm_growth | 0.0195862 ** | 0.0085818 |

| innovation | 0.0741059 *** | 0.0100815 |

| audited | 0.0434484 *** | 0.0099457 |

| purchased_credit | 0.0009518 *** | 0.00014 |

| developed | 0.2397157 *** | 0.0535644 |

| credit_line | 0.5164188 *** | 0.010933 |

| firmsize | −0.0005874 | 0.012765 |

| Country FE | YES | |

| Sector FE | YES | |

| Year FE | YES | |

| Observations | 7744 | |

| R-squared | 0.5237 |

| OLS Regression | Logit Regression | |||

|---|---|---|---|---|

| Robust | Robust | |||

| Credit_Access | Coefficient | std. err. | Coefficient | std. err. |

| governtime | 0.0010712 *** | 0.0002723 | 0.0086052 *** | 0.0021329 |

| main_market | 0.0442196 *** | 0.0132324 | 0.3622347 *** | 0.1142047 |

| foreign_firm | 0.0097245 | 0.0269333 | 0.2181048 | 0.271316 |

| private_firm | 0.0097709 | 0.0213095 | 0.206033 | 0.2340198 |

| state_firm | 0.0011414 | 0.0577336 | −0.0302601 | 0.4734311 |

| female_mang | 0.0074014 | 0.0094331 | 0.0470922 | 0.080178 |

| manager_exp | 0.000389 *** | 0.0001059 | 0.0065362 ** | 0.0034349 |

| lnsales | 0.0278536 *** | 0.0030599 | 0.2285698 *** | 0.0262615 |

| firm_growth | 0.0163446 ** | 0.0088689 | 0.176225 ** | 0.0747214 |

| innovation | 0.072864 *** | 0.0104599 | 0.5584937 *** | 0.0855745 |

| audited | 0.0427718 *** | 0.0103555 | 0.4068815 *** | 0.0842671 |

| purchased_credit | 0.0010746 *** | 0.0001461 | 0.00877 *** | 0.001231 |

| developed | 0.226572 *** | 0.0534017 | 1.552112 *** | 0.5625899 |

| credit_line | 0.5150807 *** | 0.0113429 | 3.073989 *** | 0.0890883 |

| firmsize | −0.0048306 | 0.0133411 | −0.0753502 | 0.1142516 |

| Country FE | YES | YES | ||

| Sector FE | YES | YES | ||

| Year FE | YES | YES | ||

| Observations | 7229 | 7228 | ||

| R-squared | 0.5240 | |||

| Pseudo R2 | 0.4705 |

| Panel A. | OLS Regression | OLS Regression | ||

|---|---|---|---|---|

| Domestic Market | International Market | |||

| Robust | Robust | |||

| Credit_Access | Coefficient | std. err. | Coefficient | std. err. |

| governtime | 0.0010977 *** | 0.0002928 | 0.000217 | 0.0007153 |

| foreign_firm | −0.0081349 | 0.0307118 | 0.0660552 | 0.0961314 |

| private_firm | 0.0099332 | 0.0218897 | 0.0247695 | 0.099099 |

| state_firm | −0.0196096 | 0.0605905 | 0.151136 | 0.1901056 |

| female_mang | 0.0084567 | 0.0104469 | −0.0036933 | 0.0223523 |

| manager_exp | 0.0003651 *** | 0.0000891 | 0.0014239 | 0.0010042 |

| lnsales | 0.0276639 *** | 0.0032736 | 0.0302289 *** | 0.0096093 |

| firm_growth | 0.0140902 | 0.0097094 | 0.0405349 * | 0.0228511 |

| innovation | 0.0758878 *** | 0.0117864 | 0.0550385 ** | 0.0224324 |

| audited | 0.0447164 *** | 0.0113031 | 0.0284062 | 0.0269001 |

| purchased_credit | 0.0011081 *** | 0.000163 | 0.0009858 *** | 0.0003482 |

| developed | 0.2293676 *** | 0.0552663 | 0.1832202 | 0.192256 |

| credit_line | 0.5123492 *** | 0.0120375 | 0.5355719 *** | 0.0361078 |

| firmsize | −0.0066067 | 0.0154379 | −0.0021057 | 0.0295608 |

| Country FE | YES | YES | ||

| Sector FE | YES | YES | ||

| Year FE | YES | YES | ||

| Observations | 6249 | 980 | ||

| R Squared | 0.5058 | 0.5475 | ||

| Panel b. | Logit Regression | Logit Regression | ||

| Domestic market | International market | |||

| Robust | Robust | |||

| Credit_Access | Coefficient | std. err. | Coefficient | std. err. |

| governtime | 0.0089248 *** | 0.0022317 | −0.0006286 | 0.0084678 |

| foreign_firm | 0.0460699 | 0.2917169 | 0.963692 | 1.788953 |

| private_firm | 0.2301966 | 0.2413958 | 0.3923589 | 1.734228 |

| state_firm | −0.2169917 | 0.4689108 | 2.143092 | 2.729872 |

| female_mang | 0.0621899 | 0.0864926 | −0.0407682 | 0.2504103 |

| manager_exp | 0.0055742 | 0.0036927 | 0.0175061 | 0.0109155 |

| lnsales | 0.227224 *** | 0.0278339 | 0.364095 *** | 0.1066143 |

| firm_growth | 0.1622806 ** | 0.0804869 | 0.5213513 ** | 0.2361899 |

| innovation | 0.5579072 *** | 0.0927952 | 0.6209382 ** | 0.2438208 |

| audited | 0.430503 *** | 0.0903385 | 0.3112077 | 0.2759973 |

| purchased_credit | 0.0087521 *** | 0.0013301 | 0.0115493 *** | 0.0036521 |

| developed | 1.630155 *** | 0.5827996 | −0.8844369 | 0.8847935 |

| credit_line | 3.089671 *** | 0.0950989 | 3.514702 *** | 0.3426694 |

| firmsize | −0.1087144 | 0.1281895 | −0.0407205 | 0.3405306 |

| Country FE | YES | YES | ||

| Sector FE | YES | YES | ||

| Year FE | YES | YES | ||

| Observations | 6245 | 937 | ||

| Pseudo R2 | 0.4551 | 0.5245 |

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2023 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Phan, T.T.; Ta, L.N.; Pham, T.T.M.; Pham, D.T.T. Credit Access and the Firm–Government Connection: Is There Any Link? J. Risk Financial Manag. 2023, 16, 482. https://doi.org/10.3390/jrfm16110482

Phan TT, Ta LN, Pham TTM, Pham DTT. Credit Access and the Firm–Government Connection: Is There Any Link? Journal of Risk and Financial Management. 2023; 16(11):482. https://doi.org/10.3390/jrfm16110482

Chicago/Turabian StylePhan, Trang Thu, Linh Nhat Ta, Trang Tran Minh Pham, and Dung Thi Thuy Pham. 2023. "Credit Access and the Firm–Government Connection: Is There Any Link?" Journal of Risk and Financial Management 16, no. 11: 482. https://doi.org/10.3390/jrfm16110482

APA StylePhan, T. T., Ta, L. N., Pham, T. T. M., & Pham, D. T. T. (2023). Credit Access and the Firm–Government Connection: Is There Any Link? Journal of Risk and Financial Management, 16(11), 482. https://doi.org/10.3390/jrfm16110482