Hospital Costing Methods: Four Decades of Literature Review

Abstract

1. Introduction

2. Methodology

3. Results and Discussion

3.1. Status of Empirical Research

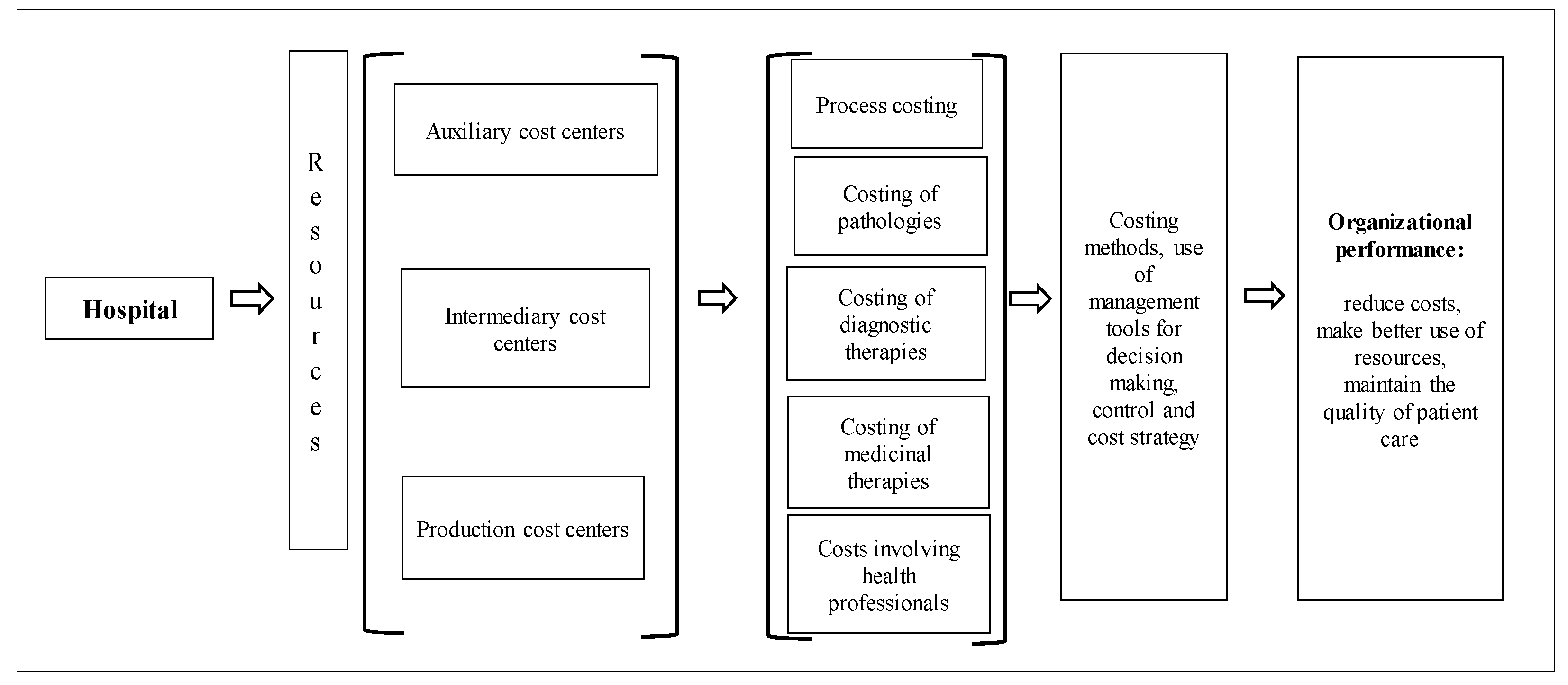

3.2. Content Analysis and Development of Hospital Costing Methods

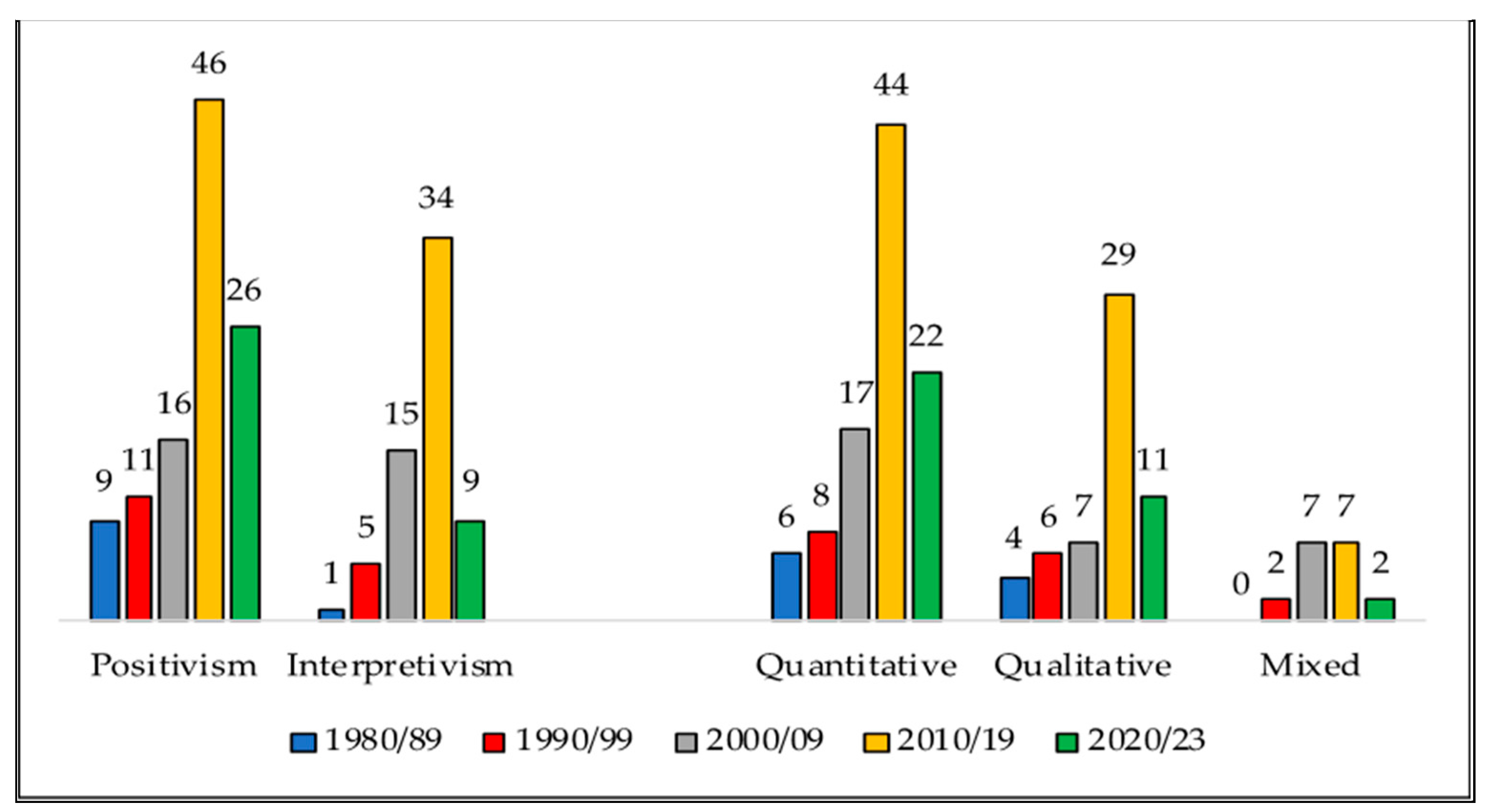

3.3. Research Paradigms and Tools for Hospital Cost Management

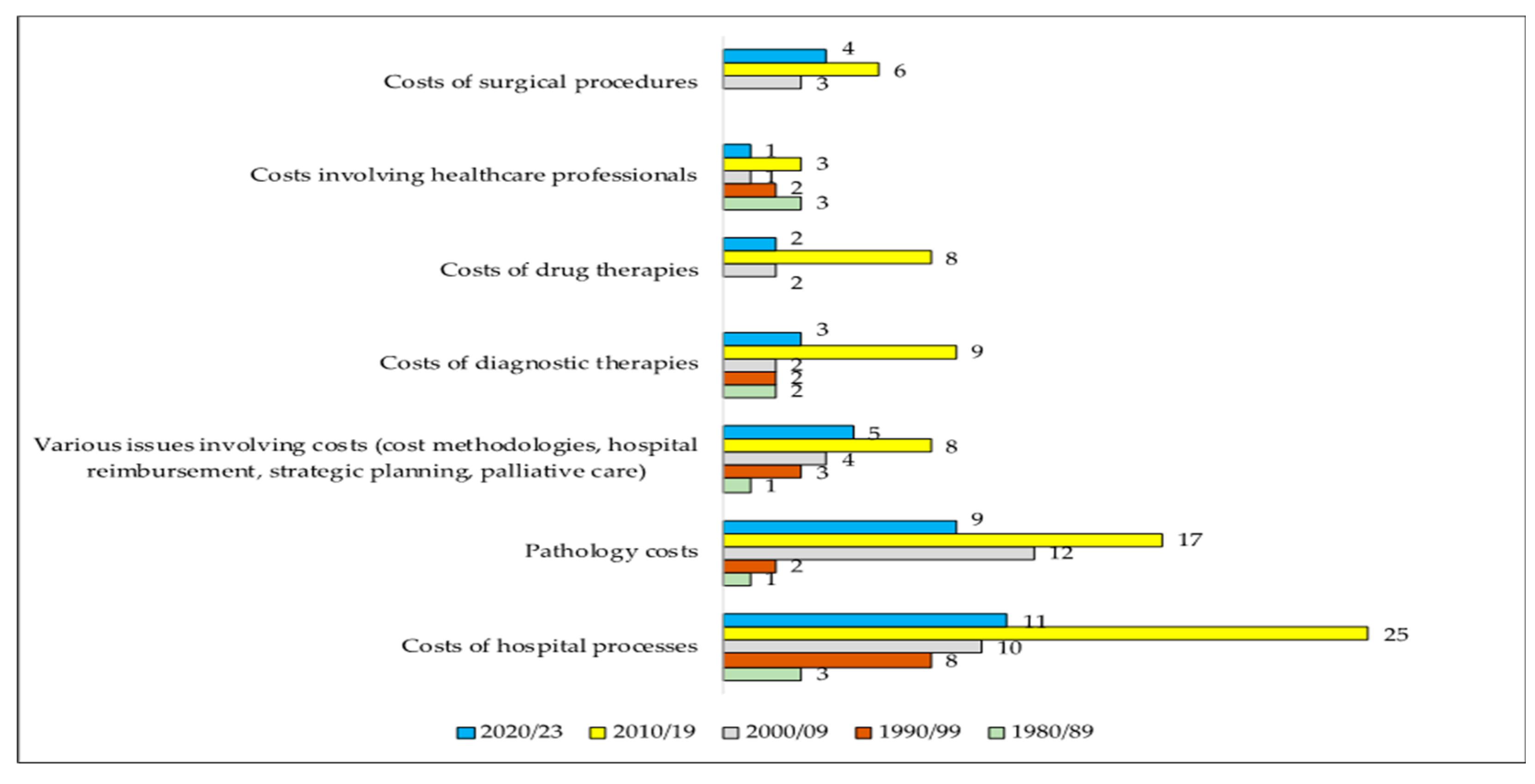

3.4. Main Lines of Research and Their Development

4. Conclusions

Author Contributions

Funding

Data Availability Statement

Acknowledgments

Conflicts of Interest

References

- Abernethy, Margaret A., Wai F. Chua, Jennifer Grafton, and Habbib Mahama. 2006. Accounting and Control in Health Care: Behavioural, Organisational, Sociological and Critical Perspectives. Science Direct 2: 805–29. [Google Scholar] [CrossRef]

- Afzali, Anita, Kristine Ogden, Michael L. Friedman, Jingdong Chao, and Anthony Wang. 2017. Costs of providing infusion therapy for patients with inflammatory bowel disease in a hospital-based infusion center setting. Journal of Medical Economics 20: 409–22. [Google Scholar] [CrossRef]

- Akhavan, Sina, Lorrayne Ward, and Kevin J. Bozic. 2016. Time-driven activity-based costing more accurately reflects costs in arthroplasty surgery. Clinical Orthopaedics and Related Research 474: 8–15. [Google Scholar] [CrossRef]

- Alves, Rafael J. V., Ana P. B. D. S. Etges, Giácomo B. Neto, and Carisi A. Polanczyk. 2018. Activity-based costing and time-driven activity-based costing for assessing the costs of cancer prevention, diagnosis, and treatment: A systematic review of the literature. Value in Health Regional Issues 17: 142–47. [Google Scholar] [CrossRef]

- Atif, Muhammad, Ssyed A. S. Sulaiman, Asrul A. Shafie, Fahad Saleem, and Nafees Ahmad. 2012. Determination of chest x-ray cost using activity based costing approach at Penang General Hospital, Malaysia. Pan African Medical Journal 12: 40. [Google Scholar]

- Au, Jennifer, and Luke Rudmik. 2013. Cost of outpatient endoscopic sinus surgery from the perspective of the Canadian government: A time-driven activity-based costing approach. International Forum of Allergy and Rhinology 3: 748–54. [Google Scholar] [CrossRef]

- Balakrishnan, Karthik, Brian Goico, and Ellis M. Arjmand. 2015. Applying cost accounting to operating room staffing in otolaryngology: Time-driven activity-based costing and outpatient adenotonsillectomy. Otolaryngology—Head and Neck Surgery (United States) 152: 684–90. [Google Scholar] [CrossRef]

- Bauer-Nilsen, Kristine, Colin Hill, Daniel M. Trifiletti, Bruce Libby, Donna H. Lash, Melody Lain, Deborah Christodoulou, Constance Hodge, and Timothy N. Showalter. 2018. Evaluation of delivery costs for external beam radiation therapy and brachytherapy for locally advanced cervical cancer using time-driven activity-based costing. International Journal of Radiation Oncology Biology Physics 100: 88–94. [Google Scholar] [CrossRef]

- Baxter, Jane, and Wai F. Chua. 2003. Alternative management accounting research—Whence and whither. Accounting, Organizations and Society 28: 97–126. [Google Scholar] [CrossRef]

- Bayati, Mohsen, Alireza M. Ahari, Abbas Badakhshan, Mahin Gholipour, and Hassan Joulaei. 2015. Cost analysis of MRI services in Iran: An application of activity based costing technique. Iranian Journal of Radiology 12: e18372. [Google Scholar] [CrossRef]

- Bennett, Joseph P. 1985. Standard cost systems lead to efficiency and profitability. Healthcare Financial Management: Journal of the Healthcare Financial Management Association 39: 46–52. [Google Scholar]

- Bermudez-Tamayo, Clara, Mira Johri, Francisco J. Perez-Ramos, Gracia Maroto-Navarro, Africa Cano-Aguilar, Letícia Garcia-Mochon, Longinos Aceituno, François Audibert, and Nils Chaillet. 2014. Evaluation of quality improvement for cesarean sections programmes through mixed methods. Implementation Science 9: 182. [Google Scholar] [CrossRef]

- Bertapelle, Maria P., Mario Vottero, Giulio D. Popolo, Marco Mencarini, Edoardo Ostardo, Michele Spinelli, Antonella Giannantoni, and Anna D’Ausilio. 2015. Sacral neuromodulation and botulinum toxin A for refractory idiopathic overactive bladder: A cost-utility analysis in the perspective of the Italian healthcare system. World Journal of Urology 33: 1109–17. [Google Scholar] [PubMed]

- Bertoni, Michele, Bruno De Rosa, and Ivana D. Lutilsky. 2017. Opportunities for the improvement of cost accounting systems in public hospitals in Italy and Croatia: A case study. [Mogućnosti unapređenja sustava troškovnog računovodstva u javnim bolnicama u italiji i hrvatskoj: Studija slučaja]. Management 22: 109–28. [Google Scholar]

- Boonen, Annelies, Johannes L. Severens, and Sjef van der Linden. 2004. A tale of two cities: Hospitalization costs in 1897 and 1997. International Journal of Technology Assessment in Health Care 20: 236–41. [Google Scholar] [CrossRef]

- Bretland, P. M. 1988. Costing imaging procedures. British Journal of Radiology 61: 54–61. [Google Scholar] [CrossRef]

- Burrell, Gibson, and Gareth Morgan. 1979. Sociological Paradigms and Organisational Analyses. London: Heinemann Educational Books. [Google Scholar]

- Busse, Monica E., Hanan Khalil, Lori Quinn, and Anne E. Rosser. 2008. Physical therapy intervention for people with Huntington’s disease. Physical Therapy 88: 820–31. [Google Scholar] [CrossRef] [PubMed]

- Campos, Domingos F., and Isabel C. P. Marques. 2011. ABC Costing in a Private Hospital Organization: A Comparative Study of the Cost of Elective Surgeries with Values Refunded by Health Plans. Rio de Janeiro: EnANPAD, XXXV Encontro da ANPAD. [Google Scholar]

- Cao, Pengyu, Shin-Ichi Toyabe, and Kouhei Akazawa. 2006a. Development of a practical costing method for hospitals. Tohoku Journal of Experimental Medicine 208: 213–24. [Google Scholar] [CrossRef] [PubMed]

- Cao, Pengyu, Shin-Ichi Toyabe, S. Kurashima, M. Okada, and Kouhei Akazawa. 2006b. A modified method of activity-based costing for objectively reducing cost drivers in hospitals. Methods of Information in Medicine 45: 462–69. [Google Scholar] [PubMed]

- Caputo, Andrea, Simone Pizzi, Massimiliano Pellegrini, and Marina Dabic. 2021. Digitalization and business models: Where are we going? A science map of the field. Journal of Business Research 123: 489–501. [Google Scholar]

- Cardinaels, Eddy, and Naomi Soderstrom. 2013. Managing in a Complex World: Accounting and Governance Choices in Hospitals. European Accounting Review 22: 647–84. [Google Scholar] [CrossRef]

- Cardoso, Ricardo B., Miriam A. A. Marcolino, Milena S. Marcolino, Camila F. Fortis, Leila B. Moreira, Ana P. Coutinho, Nadine O. Clausell, Junaid Nabi, Robert S. Kaplan, Ana P. B. Da Silva Etges, and et al. 2023. Comparison of COVID-19 hospitalization costs across care pathways: A patient-level time-driven activity-based costing analysis in a Brazilian hospital. BMC Health Services Research 23: 198. [Google Scholar]

- Castriotta, Manuel, Michela Loi, Elona Marku, and Luca Naitana. 2019. What’s in a name? Exploring the conceptual structure of emerging organizations. Scientometrics 118: 407–37. [Google Scholar]

- Chapman, Christopher, Anja Kern, and Aziza Laguecir. 2014. Costing Practices in Healthcare. Accounting Horizons 28: 353–64. [Google Scholar] [CrossRef]

- Chapman, Christopher, Anja Kern, Aziza Laguecir, and Wilm Quentin. 2016. Management accounting and efficiency in health services: The foundational role of cost analysis. In Health System Efficiency: How to Make Measurement Matter for Policy and Management; Edited by J. Cylus, I. Papanicolas and P. C. Smith. Geneva: World Health Organization, pp. 75–98. Available online: https://www.ncbi.nlm.nih.gov/books/NBK436887/ (accessed on 1 January 2023).

- Choi, Sung. 2017. Hospital capital investment during the Great Recession. Inquiry 54: 004695801770839. [Google Scholar] [CrossRef]

- Chung, Wei-C., Pao-Luo Fan, Herng-Chia Chiu, Chun-Yuh Yang, Kun-Lun Huang, and Dong-Sheng Tzeng. 2010. Operating room cost for coronary artery bypass graft procedures: Does experience or severity of illness matter? Journal of Evaluation in Clinical Practice 16: 1063–70. [Google Scholar] [CrossRef]

- Cinquini, Lino, Paola M. Vitali, Arianna Pitzalis, and Cristina Campanale. 2009. Process view and cost management of a new surgery technique in hospital. Business Process Management Journal 15: 895–919. [Google Scholar]

- Colin, Xavier, Antoine Lafuma, Dominique Costagliola, Jean-Marie Lang, and Pascal Guillon. 2010. The Cost of Managing HIV Infection in Highly Treatment-Experienced, HIV-Infected Adults in France. Pharmaco Economics 28 Suppl. S1: 59–68. [Google Scholar] [CrossRef]

- Cook, Deborah. J., Cynthia D. Mulrow, and R. Brian Haynes. 1997. Systematic reviews: Synthesis of best evidence for clinical decisions. Annals of Internal Medicine 126: 376. [Google Scholar] [CrossRef]

- Cooper, Robin, and Robert S. Kaplan. 1988a. How cost accounting distorts product costs. Management Accounting 69: 20–27. [Google Scholar]

- Cooper, Robin, and Robert S. Kaplan. 1988b. Measure Costs Right: Make the Right Decision. Harvard Business Review 66: 96–103. [Google Scholar]

- Cooper, Robin, and Robert S. Kaplan. 1991. Profit Priorities from Activity-Based Costing. Harvard Business Review 69: 130–35. [Google Scholar]

- Corral, Julieta, Josep A. Espinàs, Francesc Cots, Laura Pareja, Judit Solà, Rebeca Font, and Josep M. Borràs. 2015. Estimation of lung cancer diagnosis and treatment costs based on a patient-level analysis in Catalonia (Spain). BMC Health Services Research 15: 70. [Google Scholar] [CrossRef]

- Crane, Glenis J., Steven M. Kymes, Janet E. Hiller, Robert Casson, Adam Martin, and Jonathan D. Karnon. 2013. Accounting for Costs, QALYs, and Capacity Constraints: Using Discrete-Event Simulation to Evaluate Alternative Service Delivery and Organizational Scenarios for Hospital-Based Glaucoma Services. Medical Decision Making 33: 986–97. [Google Scholar] [CrossRef]

- Cunha, Julio A. C., and Hamilton L. Corrêa. 2013. Evaluation of organizational performance: A study applied in philanthropic hospitals. Revista de Administração de Empresas\FGV-EAESP 53: 458–99. [Google Scholar]

- Cyganska, Malgorzata. 2017. Analysis of High-Cost Outliers in a Polish Reference Hospital. E & M Ekonomie a Management 4: 59–69. [Google Scholar]

- De Mars Martin, P., and J. France Boyer. 1985. Developing a Consistent Method for Costing Hospital Services. Healthcare Financial Management 39: 30–37. [Google Scholar]

- Dugel, Pravin U., and Kuo Bianchini Tong. 2011. Development of an activity-based costing model to evaluate physician office practice profitability. Ophthalmology 118: 203–8.e3. [Google Scholar] [CrossRef]

- Eastaugh, Steven R. 1998. Financial issues in defining levels for HIV/AIDS research. Journal of Health Care Finance 25: 19–25. [Google Scholar]

- Edbrooke, David L., A. J. Wilson, P. Gerrish, and A. J. Mann. 1995. The Sheffield costing system for intensive care. Care of the Critically Ill 11: 106–10. [Google Scholar]

- Ektare, Varun, Alexandra Khachatryan, Mei Xue, Michael Dunne, K. Johnson, and Jennifer Stephens. 2015. Assessing the economic value of avoiding hospital admissions by shifting the management of gram plus acute bacterial skin and skin-structure infections to an outpatient care setting. Journal of Medical Economics 18: 1092–101. [Google Scholar] [CrossRef]

- Eldenburg, Leslle. 1994. The Use of Information in Total Cost Management. The Accounting Review 69: 96–121. [Google Scholar]

- Eldenburg, Leslle, and Ranjani Krishnan. 2006. Management Accounting and Control in Health Care: An Economics Perspective. Science Direct 6: 859–83. [Google Scholar] [CrossRef]

- Ellram, Lisa M. 2006. The Implementation of Target Costing in the United States: Theory versus practice. The Journal of Supply Chain Management 42: 13–26. [Google Scholar] [CrossRef]

- Emmett, Dennis, and Robert Forget. 2005. The utilization of activity-based cost accounting in hospitals. Journal of Hospital Marketing and Public Relations 15: 79–89. [Google Scholar] [CrossRef]

- Espinoza, Alexis V., Stefanie Devos, Robbert-Jan van Hooff, Maaike Fobelets, Alain Dupont, Maarten Moens, Ives Hubloue, Door Lauwaert, Pieter Cornu, Raf Brouns, and et al. 2017. Time Gain Needed for In-Ambulance Telemedicine: Cost-Utility Model. JMIR Mhealth and Uhealth 5: e8288. [Google Scholar]

- Eti, SSerife, Sean O’Mahony, Marlene McHugh, Rose Guilbe, Arthur Blank, and Peter Selwyn. 2014. Outcomes of the Acute Palliative Care Unit in an Academic Medical Center. American Journal of Hospice and Palliative Medicine® 31: 380–84. [Google Scholar] [CrossRef]

- Fang, Christopher J., Jonathan M. Shaker, Jacob M. Drew, Andrew Jawa, David A. Mattingly, and Eric L. Smith. 2021. The cost of hip and knee revision arthroplasty by diagnosis-related groups: Comparing time-driven activity-based costing and traditional accounting. Journal of Arthroplasty 36: 2674–79. [Google Scholar] [CrossRef]

- Ferreira, Fernando A. F. 2018. Mapping the field of arts-based management: Bibliographic coupling and co-citation analyses. Journal of Business Research 85: 348–57. [Google Scholar] [CrossRef]

- Ghaffari, Shahram, Chrisphoer Doran, Andrew Wilson, Chris Aisbett, and Terri Jackson. 2009. Investigating DRG cost weights for hospitals in middle income countries. International Journal of Health Planning and Management 24: 251–64. [Google Scholar] [CrossRef]

- Ghate, Sameer R., Joseph Biskupiak, Xiangyang Ye, Winghan J. Kwong, and Diana I. Brixner. 2011. All-Cause and Bleeding-Related Health Care Costs in Warfarin-Treated Patients with Atrial Fibrillation. Journal of Managed Care Pharmacy 17: 672–84. [Google Scholar]

- Glick, Noah D., Craig C. Blackmore, and William N. Zelman. 2000. Extending simulation modeling to activity-based costing for clinical procedures. Journal of Medical Systems 24: 77–89. [Google Scholar] [CrossRef]

- Gray, Paul, M. Abernethy, and J. Stoelwinder. 1987. Models for costing patient care services. part 1: Costing diagnostic laboratory services. Australian Health Review 10: 69–88. [Google Scholar]

- Guz, A. N., and J. J. Rushchitsky. 2009. Scopus: A system for the evaluation of scientific journals. International Applied Mechanics 45: 351–62. [Google Scholar]

- Harper, Paul R., N. H. Powell, and Janet E. Williams. 2010. Modelling the size and skill-mix of hospital nursing teams. Journal of the Operational Research Society 61: 768–79. [Google Scholar] [CrossRef]

- Hartmann, Marconi. 2013. Cost Mapping Through the RKW Method Applied in a Thermoplastic Industry. Bachelor’s thesis. Available online: http://www.fahor.com.br/images/Documentos/Biblioteca/TFCs/Eng_Producao/2013/Pro_Marconi.pdf (accessed on 2 May 2022).

- Hidalgo-Vega, Álvaro, Elham Askari, Rosa Vidal, Isaac Aranda-Reneo, Almudena Gonzalez-Dominguez, Alexandra Ivanova, Gabriela Ene, and Pilar Llamas. 2014. Direct vitamin K antagonist anticoagulant treatment health care costs in patients with non-valvular atrial fibrillation. BMC Health Services Research 14: 46. [Google Scholar] [CrossRef] [PubMed]

- Hongoro, Charles, and Natalya Dinat. 2011. A cost analysis of a hospital-based palliative care outreach program: Implications for expanding public sector palliative care in South Africa. Journal of Pain and Symptom Management 41: 1015–24. [Google Scholar] [CrossRef] [PubMed]

- Hopper, Trevor. 2005. Management Accounting Theory in Europe: Thirty Years Hard Labour. Presented at the Plenary Session, European Accounting Association 2005 Congress, Gothenburg, Sweden, 18–20 May. [Google Scholar]

- Hopper, Trevor, and Andrew Powell. 1985. Making sense of research into the organizations and social aspects of management accounting: A review of its underlying assumptions. Journal of Management Studies 22: 429–65. [Google Scholar] [CrossRef]

- Hopwood, Anthony G. 2007. Whither accounting research? The Accounting Review 82: 1365–74. [Google Scholar] [CrossRef]

- Horngren, Charles T., George Foster, and Srikant M. Datar. 2000. Cost Accounting, 9th ed. Translated by José Luiz Paravato. Rio de Janeiro: LTC. [Google Scholar]

- Jackson, Taylor J., Todd Blumberg, Apurva S. Shah, and Wudbhav N. Sankar. 2018. Inappropriately timed pediatric orthopaedic referrals from the emergency department result in unnecessary appointments and financial burden for patients. Journal of Pediatric Orthopaedics 38: e128–e132. [Google Scholar] [CrossRef]

- Jakovljevic, Mihajlo, Mirjana Varjacic, and Slobodan M. Jankovic. 2008. Cost-Effectiveness of Ritodrine and Fenoterol for Treatment of Preterm Labor in a Low–Middle-Income Country: A Case Study. Value in Health 11: 149–53. [Google Scholar] [CrossRef] [PubMed][Green Version]

- Jarlier, Agnes, and Suzanne Charvet-Protat. 2000. Can improving quality decrease hospital costs? International Journal for Quality in Health Care 12: 125–31. [Google Scholar] [CrossRef] [PubMed]

- Javid, Mahdi, Mohammad Hadian, Hossein Ghaderi, Shahram Ghaffari, and Masoud Salehi. 2016. Application of the activity-based costing method for unit-cost calculation in a hospital. Global Journal of Health Science 8: 165–72. [Google Scholar] [CrossRef] [PubMed]

- Joret, Maximilian O., Anastasia Dean, Colin Cao, Joanna Stewart, and Venu Bhamidipaty. 2016. The financial burden of surgical and endovascular treatment of diabetic foot wounds. Journal of Vascular Surgery 64: 648–55. [Google Scholar] [CrossRef]

- Kakkuri-Knuuttila, Marja-Liisa, Kari Lukka, and Jaakko Kuorikoski. 2008. Straddling between paradigms: A naturalistic philosophical case study on interpretive research in management accounting. Accounting, Organizations and Society 33: 267–91. [Google Scholar] [CrossRef]

- Kaplan, Robert S., and Steven R. Anderson. 2004. Time driven activity-based costing. Harvard Business Review, 131–38. [Google Scholar]

- Kaplan, Robert S., and Steven R. Anderson. 2007. The innovation of time-driven activity-based costing. Cost Management 21: 5–15. [Google Scholar]

- Kawamata, Minoru, Yasuhiko Yamane, Takashi Horinouchi, Katsuyuki Nakanishi, Kenichirou Shimai, and Horoki Moriguchi. 2017. Assessment of methods used to import external brought-in image data using activity-based costing/activity-based management. Journal of Medical Imaging and Health Informatics 7: 764–70. [Google Scholar] [CrossRef]

- Keel, George, Rafiq Muhammad, Carl Savage, Jonas Spaak, Ismael Gonzalez, Peter Lindgren, Christian Gurrmann, and Pamela Mazzocato. 2020. Time-driven activity-based costing for patients with multiple chronic conditions: A mixed-method study to cost care in a multidisciplinary and integrated care delivery centre at a university-affiliated tertiary teaching hospital in Stockholm, Sweden. BMJ Open 10: e032573. [Google Scholar] [CrossRef]

- Kempeneers, Noah, L. Van Aken, and G. Van Herck. 1995. Toward more economic rationality in hospital cost accounting. Acta Hospitalia 35: 35–41. [Google Scholar]

- Kim, Eugene, Hye-Young Kwon, Sang H. Baek, Haeyoung Lee, Byung-Su Yoo, Seok-Min Kang, Youngkeun Ahn, and Bong-Min Yang. 2018. Medical costs in patients with heart failure after acute heart failure events: One-year follow-up study. Journal of Medical Economics 21: 288–93. [Google Scholar] [CrossRef]

- Koster, Fiona, Marc R. Kok, Jaco van der Kooij, Geeke Waverijn, Angelineque E. A. M. Weel-KoendersM, and Deirisa L. Barreto. 2023. Dealing with Time Estimates in Hospital Cost Accounting: Integrating Fuzzy Logic into Time-Driven Activity-Based Costing. Pharmacoecon Open 7: 593–603. [Google Scholar] [CrossRef] [PubMed]

- Kroon, Nanja, and Maria Alves. 2023a. Examining the Fit between Supply and Demand of the Accounting Professional’s Competencies: A Systematic Literature Review. International Journal of Management Education 21: 100872. [Google Scholar] [CrossRef]

- Kroon, Nanja, and Maria Alves. 2023b. Fifteen Years of Accounting Professional’s Competencies Supply and Demand: Evidencing Actors, Competency Assessment Strategies, and ‘Top Three’ Competencies. Administrative Sciences 13: 70. [Google Scholar] [CrossRef]

- Kroon, Nanja, Maria. C. Alves, and Isabel Martins. 2021. The Impacts of Emerging Technologies on Accountants’ Role and Skills: Connecting to Open Innovation—A Systematic Literature Review. Journal of Open Innovation: Technology, Market, and Complexity 7: 163. [Google Scholar]

- Labro, Eva, and Lorien Stice-Lawrence. 2020. Updating Accounting Systems: Longitudinal Evidence from the Healthcare Sector. Management Science 66: 6042–61. [Google Scholar] [CrossRef]

- Laurila, J., I. Suramo, E. M. Tolppanen, P. Koivukangas, P. Lanning, and C. G. Standertskjöld-Nordenstam. 2000. Activity-based costing in radiology: Application in a pediatric radiological unit. Acta Radiologica 41: 189–95. [Google Scholar] [CrossRef]

- Law, Mary, Debra Stewart, N. Pollock, Lori Letts, Jackie Bosch, and M. Westmorland. 1998. Critical Review Form—Quantitative Studies. Hamilton: Mac-Master University. [Google Scholar]

- Lee, Jeong-Min, Myeong-Jin Kim, Sith Phongkitkarun, Abhasnee Sobhonslidsuk, Anke-Peggy Holtorf, Harald Rinde, and Karsten Bergmann. 2016. Health economic evaluation of Gd-EOB-DTPA MRI vs. ECCM-MRI and multi-detector computed tomography in patients with suspected hepatocellular carcinoma in Thailand and South Korea. Journal of Medical Economics 19: 759–68. [Google Scholar] [CrossRef][Green Version]

- Letts, Lori, S. Wilkins, Mary Law, Debra Stewart, Jackie Bosch, and M. Westmorland. 2007. Critical Review Form—Qualitative Studies (Version 2.0). Hamilton: Mac- Master University. [Google Scholar]

- Levy-Piedbois, C., I. Durand-Zaleski, H. Juhel, C. Schmitt, A. Bellanger, and P. Piedbois. 2000. Cost-effectiveness of second-line treatment with irinotecan or infusional 5-fluorouracil in metastatic colorectal cancer. Annals of Oncology 11: 157–61. [Google Scholar] [CrossRef]

- Levy, Emile, Sylvie Gabriel, and Jérôme Dinet. 2003. The Comparative Medical Costs of Atherothrombotic Disease in European Countries. Pharmaco Economics 21: 651–59. [Google Scholar] [CrossRef]

- Liberati, Alessandro, Douglas G. Altman, Jennifer Tetzlaff, Cynthia Mulrow, Peter C. Gøtzsche, John P. A. Ioannidis, Mike Clarke, P. J. Devereaux, Jos Kleijnen, and David Moher. 2009. The PRISMA statement for reporting systematic reviews and meta-analyses of studies that evaluate health care interventions: Explanation and elaboration. PLoS Medicine 6: e1000100. [Google Scholar] [CrossRef]

- Loizzo, M., F. Gallo, and D. Caruso. 2018. Reducing complications and overall healthcare costs of hip fracture management: A retrospective study on the application of a Diagnostic Therapeutic Pathway in the Cosenza General Hospital. Annali di Igiene Medicina Preventiva e di Comunita 30: 191–99. [Google Scholar] [PubMed]

- Lunney, Meaghan, Arian Samimi, Mohamad Osman, Kailash Jindal, Natasha Wiebe, Feng Ye, David W. Johnson, Adeera Levin, and Aminu K. Bello. 2019. Capacity of Kidney Care in Canada: Identifying barriers and opportunities. Canadian Journal of Kidney Health and Disease 6: 205435811987054. [Google Scholar] [CrossRef] [PubMed]

- Lynch, Wendy D., Karine Markosyan, Arthur K. Melkonian, Jacqueline Pesa, and Nathan L. Kleinman. 2009. Effect of Antihypertensive Medication Adherence Among Employees with Hypertension. American Journal of Managed Care 15: 871–80. [Google Scholar] [PubMed]

- Mahon, N. G., P. Rahallaigh, J. Brennan, M. B. Codd, H. A. McCann, and D. D. Sugrue. 1997. Cost of management of acute myocardial infarction in the thrombolytic era. Heart 77 Suppl. S1. [Google Scholar]

- Major, Maria J. 2017. Positivism and ‘alternative’ research in Accounting. Financial Accounting Magazine 28: 173–78. [Google Scholar] [CrossRef]

- Maniadakis, Nikos, Georgia Kourlaba, J. Shen, and Anke-Peggy Holtorf. 2017. Comprehensive taxonomy and worldwide trends in pharmaceutical policies in relation to country income status. BMC Health Services Research 17: 371. [Google Scholar] [CrossRef]

- Marques, Isabel C. P., and Alba K. M. Carvalho. 2020. Evolution of studies on orthopaedic surgery regarding cost management tools: A systematic literature review. Journal of Orthopaedics and Sports Medicine 2: 1–28. [Google Scholar] [CrossRef]

- Martins, E. 2000. Cost Accounting, 7th ed. São Paulo: Atlas. [Google Scholar]

- Massaro, Maurizio, John Dumay, and James Guthrie. 2016. On the shoulders of giants: Undertaking a structured literature review in accounting. Accounting, Auditing and Accountability Journal 29: 767–801. [Google Scholar] [CrossRef]

- Mercier, Gregoire, and Gerald Naro. 2014. Costing hospital surgery services: The method matters. PLoS ONE 9: e97290. [Google Scholar] [CrossRef]

- Merollini, Katharina M., Ross W. Crawford, and Nicholas Graves. 2013. Surgical treatment approaches and reimbursement costs of surgical site infections post hip arthroplasty in Australia: A retrospective analysis. BMC Health Services Research 13: 91. [Google Scholar] [CrossRef]

- Monnickendam, Giles, and Carlo de Asmundis. 2018. Why the distribution matters: Using discrete event simulation to demonstrate the impact of the distribution of procedure times on hospital operating room utilization and average procedure cost. Operations Research for Health Care 16: 20–28. [Google Scholar] [CrossRef]

- Morgan, David. L. 2007. Paradigms lost and pragmatism regained: Methodological implications of combining qualitative and quantitative methods. Journal of Mixed Method Research 1: 48–76. [Google Scholar] [CrossRef]

- Mori, Amani Thomas, and Cecilia J. Nyabakari. 2023. Cost of image-guided percutaneous nephrostomy among cervical cancer patients at Muhimbili National Hospital in Tanzania. Cost Effectiveness and Resource Allocation 21: 33. [Google Scholar] [CrossRef] [PubMed]

- Mortuaire, G., D. Theis, R. Fackeure, D. Chevalier, and I. Gengler. 2018. Cost-effectiveness assessment in outpatient sinonasal surgery. European Annals of Otorhinolaryngology. Head and Neck Diseases 135: 11–15. [Google Scholar]

- Myint, Phyo K., John F. Potter, Gill M. Price, Garry R. Barton, Anthony K. Metcalf, Rachel Hale, Genevieve Dalton, Stanley D. Musgrave, Abraham George, Raj Shekhar, and et al. 2011. Evaluation of stroke services in Anglia stroke clinical network to examine the variation in acute services and stroke outcomes. BMC Health Services Research 11: 50. [Google Scholar] [CrossRef]

- Nakagawa, Yoshiaki, Tadamasa Takemura, Hiroyuki Yoshihara, and Yoshinobu Nakagawa. 2011. A New Accounting System for Financial Balance Based on Personnel Cost After the Introduction of a DPC/DRG System. Journal of Medical Systems 35: 251–64. [Google Scholar] [CrossRef]

- Nayak, Bishwajit, Som S. Bhattacharyya, and Bala Krishnamoorthy. 2022. Exploring the black box of competitive advantage—An integrated bibliometric and chronological literature review approach. Journal of Business Research 139: 964–82. [Google Scholar] [CrossRef]

- Neriz, Liliana, Alicia Núñez, and Freancisco Ramis. 2014. A cost management model for hospital food and nutrition in a public hospital. BMC Health Services Research 14: 542. [Google Scholar] [CrossRef]

- Noronha, Marina F., Claudia T. Veras, Iuri C. Leite, Monica S. Martins, Francisco Braga Neto, and Lynn Silver. 1991. The development of” Diagnosis Related Groups “-DRGs. Methodology of classification of hospital patients. Journal of Public Health 25: 198–208. [Google Scholar]

- Oostenbrink, Rianne, Jan B. Oostenbrink, Karel G. M. Moons, Gerarda Derksen-Lubsen, Diederick E. Grobbee, W. Ken Redekop, and Henriette A. Moll. 2003. Application of a Diagnostic Decision Rule in Children with Meningeal Sins: A Cost-minimization Study. International Journal of Technology Assessment in Health Care 19: 698–704. [Google Scholar] [CrossRef]

- Orloff, Tracey M., Candace L. Littell, Christopher Clune, David Klingman, and Bonnie Preston. 1990. Hospital cost accounting: Who’s doing what and why. Health Care Management Review 15: 73–78. [Google Scholar] [CrossRef]

- Orrick, Joanne J., Richard Segal, Thomas E. Johns, Wayne Russel, Feng Wang, and Donald D. Yin. 2004. Resource use and cost of care for patients hospitalised with community-acquired pneumonia: Impact of adherence to infectious diseases society of America guidelines. Pharmacoeconomics 22: 751–57. [Google Scholar] [CrossRef] [PubMed]

- Owens, Jacqueline K. 2021. Systematic reviews: Brief overview of methods, limitations, and resources. Nurse Author & Editor 31: 69–72. [Google Scholar]

- Özyapici, Hasan, and Veyis N. Taniş. 2017. Comparison of cost determination of both resource consumption accounting and time-driven activity-based costing systems in a healthcare setting. Australian Health Review 4: 201–6. [Google Scholar] [CrossRef]

- Page, Matthew J., Joanne E. McKenzie, Patrick M. Bossuyt, Isabelle Boutron, Tammy C. Hoffmann, Cynthia D. Mulrow, Larissa Shamseer, Jennifer M. Tetzlaff, Elie A. Akl, Sue E. Brennan, and et al. 2021. The PRISMA 2020 statement: An updated guideline for reporting systematic reviews. BMJ 372: n71. [Google Scholar] [CrossRef]

- Petticrew, Mark, and Helen Roberts. 2008. Systematic Reviews in the Social Sciences: A Practical Guide, Kindle ed. Oxford: Wiley-Blackwell. [Google Scholar]

- Plantier, Morgane, Nathalie Havet, Thierry Durand, Nicolas Caquot, Camille Amaz, Irene Philip, Pierre Biron, and Lionel Perrier. 2017. Does adoption of electronic health records improve organizational performances of hospital surgical units? Results from the French e-SI (PREPS-SIPS) study. International Journal of Medical Informatics 98: 47–55. [Google Scholar] [CrossRef] [PubMed]

- Popesko, Boris. 2013. Specifics of the Activity-Based Costing applications in hospital management. International Journal of Collaborative Research on Internal Medicine & Public Health 5: 179–86. [Google Scholar]

- Popesko, Boris, Petr Novák, and Šarka Papadaki. 2015. Measuring diagnosis and patient profitability in healthcare: Economics vs ethics. Economics and Sociology 8: 234–45. [Google Scholar] [CrossRef]

- Powe, Neil R., Jonathan P. Weiner, Barbara Starfield, Mary Stuart, Andrew Baker, and Donald M. Steinwachs. 1996. System wide Provider Performance in a Medicaid Program: Profiling the Care of Patients with Chronic Illnesses. Medical Care 34: 798–810. [Google Scholar] [CrossRef]

- Prescott, Jeff D., Saul Factor, Michael Pill, and Gary Levi. 2007. Descriptive analysis of the direct medical costs of multiple sclerosis in 2004 using administrative claims in a large nationwide database. Journal of Managed Care Pharmacy 13: 44–52. [Google Scholar] [CrossRef]

- Raven, Maria C., Kelly M. Doran, Shannon Kostrowski, Colleen C. Gillespie, and Brian D. Elbel. 2011. An intervention to improve care and reduce costs for high-risk patients with frequent hospital admissions: A pilot study. BMC Health Services Research 11: 270. [Google Scholar] [CrossRef]

- Rego, Guilhermina, Rui Nunes, and José Costa. 2010. The challenge of corporatisation: The experience of Portuguese public hospitals. The European Journal of Health Economics 11: 367–81. [Google Scholar] [CrossRef] [PubMed]

- Reuben, David B., Emmett Keeler, Teresa Seeman, Ase Sewall, Susan H. Hirsch, and Jack M. Guralnik. 2002. Development of a Method to Identify Seniors at High Risk for High Hospital Utilization. Medical Care 40: 782–93. [Google Scholar] [CrossRef] [PubMed]

- Riewpaiboon, Arthorn, Penkae Pornlertwadee, and Kwanjai Pongsawat. 2007. Diabetes Cost Model of a Hospital in Thailand. Value in Health 10: 223–30. [Google Scholar] [CrossRef] [PubMed]

- Rigby, K. D., and J. C.B. Litt. 2000. Errors in health care management: What do they cost? Quality in Health Care 9: 216–21. [Google Scholar] [CrossRef] [PubMed]

- Rinaldo, J. A., Jr., D. J. McCubbrey, and J. R. Shryock. 1981. The care monitoring, cost forecasting and cost monitoring system. Journal of Clinical Computing 9: 72–85. [Google Scholar] [CrossRef]

- Rodrigues, Margarida, Maria-C. Alves, Cidália Oliveira, Vera Vale, José Vale, and Rui Silva. 2021. Dissemination of Social Accounting Information: A Bibliometric Review. Economies 9: 41. [Google Scholar] [CrossRef]

- Rodrigues, Margarida, Maria-C. Alves, Rui Silva, and Cidália Oliveira. 2022. Mapping the Literature on Social Responsibility and Stakeholders’ Pressures in the Mining Industry. Journal of Risk and Financial Management 15: 425. [Google Scholar] [CrossRef]

- Rojas-Lamorena, Álvaro J., Salvador Del Barrio-García, and Juan M. Alcántara-Pilar. 2022. A review of three decades of academic research on brand equity: A bibliometric approach using co-word analysis and bibliographic coupling. Journal of Business Research 139: 1067–83. [Google Scholar] [CrossRef]

- Rosenbaum, H. L., T. M. Willert, E. A. Kelly, J. F. Grey, and B. R. McDonald. 1988. Costing out nursing services based on acuity. Journal of Nursing Administration 18: 10–15. [Google Scholar] [CrossRef]

- Russell, Heidi, Andrew Street, and Vivian Ho. 2016. How Well Do All Patient Refined–Diagnosis-Related Groups Explain Costs of Pediatric Cancer Chemotherapy Admissions in the United States? Journal of Oncology Practice 12: e564–e575. [Google Scholar] [CrossRef]

- Ryan, J. 1997. Enhanced ABC costing for hospitals: Directed expense costing. Hospital Cost Management and Accounting 9: 5–8. [Google Scholar] [PubMed]

- Salas, J. del Diego, A. Orly L. Lima, J. Espin Balbino, C. Bermudez Tamayo, and J. Fernandez-Crehuet Navajas. 2016. An economic evaluation of two interventions for the prevention of post-surgical infections in cardiac surgery. Revista de Calidad Asistencial 31: 27–33. [Google Scholar] [CrossRef]

- Saraswathula, Anirudh, Samantha J. Merck, Ge Bai, Christinne M. Weston, Elizabeth A. Skinner, April Taylor, Allen Kachalia, Renee Demski, Albert W. Wu, and Stephen A. Berry. 2023. The Volume and Cost of Quality Metric Reporting. JAMA 329: 1840–47. [Google Scholar]

- Sopariwala, P. R. 1997. How much does excess inpatient capacity really cost? Healthcare Financial Management 51: 54–58+60+62. [Google Scholar] [PubMed]

- Stahl, James E., Warren S. Sandberg, Bethany Daily, Richard Wiklund, Marie T. Egan, Julian M. Goldman, Keith B. Isaacson, Scott Gazelle, and David W. Rattner. 2006. Reorganizing patient care and workflow in the operating room: A cost-effectiveness study. Surgery 139: 717–28. [Google Scholar] [CrossRef]

- Strauss, Anselm, and Juliet Corbin. 1990. Basics of Qualitative Research, 1st ed. London: Sage. [Google Scholar]

- Tarbit, I. F. 1986. Costing clinical biochemistry services as part of an operational management budgeting system. Journal of Clinical Pathology 39: 817–27. [Google Scholar] [CrossRef]

- Thomson, Kalen K., Arifur Rahman, Tom J. Cooper, and Atanu Sarkar. 2019. Exploring relevance, public perceptions, and business models for establishment of private well water quality monitoring service. International Journal of Health Planning and Management 34: e1098–e1118. [Google Scholar] [CrossRef]

- Tran, Phung T. H., Trung Q. Vo, Duyen T. P. Huynh, Luyen D. Pham, and Thuy Van Ha. 2018. Medical services for a provincial hospital in Vietnam: Cost analysis for data management. Journal of Clinical and Diagnostic Research 12: LC33–LC37. [Google Scholar] [CrossRef]

- Tranfield, David, David Denyer, and Palminder Smart. 2003. Towards a methodology for developing evidence informed management knowledge by means of systematic review. Journal British Academy of Management 14: 207–22. [Google Scholar] [CrossRef]

- Trenchard, P. M., and R. Dixon. 1997a. The practice of quality-associated costing: Application to transfusion manufacturing processes. Quality Management in Health Care 5: 53–65. [Google Scholar] [CrossRef]

- Trenchard, P. M., and R. Dixon. 1997b. The principles of quality-associated costing: Derivation from clinical transfusion practice. Quality Management in Health Care 5: 43–52. [Google Scholar] [CrossRef] [PubMed]

- Urquhart, Cathy. 2013. Grounded Theory for Qualitative Research: A Practical Guide. London: SAGE Publications, Ltd. [Google Scholar] [CrossRef]

- Uyar, Ali, Merve Kılıç, and Mehmet A. Köseoglu. 2020. Exploring the conceptual structure of the auditing discipline through co-word analysis: An international perspective. International Journal of Auditing 24: 53–72. [Google Scholar] [CrossRef]

- Vergara, Sylvia C. 2005. Administration Research Method. São Paulo: Atlas. [Google Scholar]

- Vogl, Matthias. 2012. Assessing DRG cost accounting with respect to resource allocation and tariff calculation: The case of Germany. Health Economics Review 2: 1–12. [Google Scholar] [CrossRef] [PubMed]

- Vogl, Matthias. 2013. Improving patient-level costing in the english and the German ‘DRG’ system. Health Policy 109: 290–300. [Google Scholar] [CrossRef]

- Vogl, Thomas J., Nagy N. Naguib, Nour-Eldin A. Nour-Eldin, Wolf O. Bechstein, Stefan Zeuzem, Jorg Trojan, and Tatjana Gruber-Rouh. 2012. Transarterial chemoembolization in the treatment of patients with unresectable cholangiocarcinoma: Results and prognostic factors governing treatment success. International Journal of Cancer 131: 733–40. [Google Scholar] [CrossRef]

- Weaver, Marcia R., Christopher J. Conover, Rae J. Proescholdbell, Peter S. Arno, Alfonso Ang, Karina K. Uldall, and Susan L. Ettner. 2009. Cost-effectiveness Analysis of Integrated Care for People with HIV, Chronic Mental Illness and Substance Abuse Disorders. Journal of Mental Policy and Economics 12: 33–46. [Google Scholar]

- Wenzel, Richard P. 1987. The economics of nosocomial infections. The Journal of Hospital Infection 31: 79–87. [Google Scholar] [CrossRef]

- Whiting, Penny, Maiwenn Al, Marie Westwood, Isaac C. Ramos, Steve Ryder, Nigel Armstrong, Kate Misso, Janine Ross, Hans Severens, and Joseph Kleijnen. 2015. Viscoelastic point-of-care testing to assist with the diagnosis, management and monitoring of haemostasis: A systematic review and cost-effectiveness analysis. Health Technology Assessment 19: 1–228. [Google Scholar] [CrossRef]

- Zeller, Thomas L., Anthony J. Senagore, and Gary Siegel. 1999. Manage indirect practice expense the way you practice medicine: With information. Diseases of the Colon and Rectum 42: 579–89. [Google Scholar] [CrossRef]

- Zhang, Yuna, and Godfried Augenbroe. 2018. Optimal demand charge reduction for commercial buildings through a combination of efficiency and flexibility measures. Applied Energy 221: 180–94. [Google Scholar] [CrossRef]

- Zheng, Xiaosong S., Jixuan Chen, Linhui Wang, and Pengyu Li. 2018. Application of ABC in Small and Medium-sized Public Hospitals: A Case Study of a Maternal and Child Health Hospital. Transformations in Business & Economics 17: 507–23. [Google Scholar]

- Zulman, Donna M., Stephen C. Ezeji-Okoye, Jonathan G. Shaw, Debra L. Hummel, Katie S. Holloway, Sasha F. Smither, Jessica Y. Breland, John F. Chardos, Susan Kirsh, James S. Kahn, and et al. 2014. Partnered Research in Healthcare Delivery Redesign for High-Need, High-Cost Patients: Development and Feasibility of an Intensive Management Patient-Aligned Care Team (ImPACT). Journal of General Internal Medicine 29 Suppl. S4: 861–69. [Google Scholar] [CrossRef] [PubMed]

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| Countries | Studies (n = 172) |

|---|---|

| EUA | 27 |

| England | 14 |

| France | 12 |

| Germany, Italy—11 studies per country | 22 |

| Australia, Japan—9 studies per country | 18 |

| Spain, Canada—8 studies per country | 16 |

| China, Finland, Iran, Poland, Portugal, Czech Republic, Vietnam, Belgium—4 studies per country | 32 |

| Austria, Brazil, Chile, Denmark, Ghana, Greece, Malaysia, Norway, New Zealand, Netherlands, Peru, Serbia, South Africa, Thailand, Turkey, South Korea—1 study per country | 16 |

| Joint studies (Austria, Italy, Portugal, Sweden, Belgium, France, Spain, Switzerland; Holland, Belgium; Austria, New Zealand; England, Germany; Canada, Spain; South Korea, Thailand; Italy, Croatia) | 15 |

| Journal | Impact Factor (2018) | Number of Articles |

|---|---|---|

| Annals of Oncology | 13.93 | 1 |

| International Journal of Radiation Oncology Biology Physics | 5.55 | 1 |

| Value in Health | 5.49 | 3 |

| Heart | 5.42 | 1 |

| JMIR Mhealth and Uhealth | 4.54 | 1 |

| Clinical Orthopaedics and Related Research | 4.09 | 1 |

| Health Technology Assessment | 4.06 | 1 |

| Surgery | 3.57 | 1 |

| Pharmacoeconomics | 3.24 | 3 |

| Journal of Medical Systems | 2.83 | 2 |

| Management Science | 2.83 | 1 |

| Costing Methods and Analyses | 1980–1989 | 1990–1999 | 2000–2009 | 2010–2019 | 2020–2023 |

|---|---|---|---|---|---|

| Descriptive analysis | 0 | 0 | 10 | 28 | 12 |

| Activity-based costing (ABC) | 0 | 4 | 4 | 13 | 9 |

| Management models, methods, and tools | 1 | 3 | 4 | 11 | 4 |

| Costs of diagnosis-related groups (DRGs) | 1 | 1 | 3 | 8 | 8 |

| Standard cost | 4 | 4 | 0 | 4 | 0 |

| ABC costing and other methods | 0 | 0 | 2 | 5 | 0 |

| Cost-effectiveness analyses | 0 | 1 | 1 | 4 | 0 |

| Miscellaneous mixed costs | 0 | 2 | 2 | 2 | 0 |

| Departmental costs | 2 | 0 | 1 | 0 | 0 |

| Average cost | 0 | 0 | 0 | 2 | 0 |

| Variable cost | 0 | 0 | 0 | 2 | 0 |

| DRG costs and other methods | 2 | 0 | 0 | 0 | 0 |

| Econometrics | 0 | 0 | 2 | 0 | 0 |

| Microcosting | 0 | 0 | 0 | 1 | 0 |

| Statistical analysis; marginal cost | 0 | 0 | 0 | 2 | 0 |

| Systematic literature review | 0 | 0 | 1 | 2 | 0 |

| Elements for | Variables | Number of Articles | Frequency (%) | Total (%) |

|---|---|---|---|---|

| Measurement methods | Activity-based cost (ABC) | 31 | 18.02 | 45.93 |

| Mixed cost | 19 | 11.05 | ||

| Standard cost | 16 | 9.30 | ||

| Variable costing, departmental costing, microcosting | 13 | 7.56 | ||

| Costs for decision making and control | Break-even point, contribution margin, management models, methods and tools, cost-effectiveness | 23 | 13.37 | 13.37 |

| Strategic cost management | Cost-effectiveness, competitor analysis, value chain analysis | 46 | 26.74 | 38.37 |

| Diagnosis-related groups analyses | 14 | 8.14 | ||

| Statistical analyses | 3 | 1.74 | ||

| Quality costs | 3 | 1.74 | ||

| Others | Systematic literature review | 4 | 2.33 | 2.33 |

| Total | 172 | 100 | 100 |

| Hospital Costs | Number of Articles | Frequency (%) |

|---|---|---|

| Costs of hospital processes (examples: laundry, material, and sterilization, nutrition) | 57 | 33.1 |

| Treatment costs for specific pathologies | 41 | 23.8 |

| Miscellaneous issues involving hospital costs (examples: cost methodologies, hospital reimbursement, strategic planning) | 21 | 12.2 |

| Costs of diagnostic therapies (examples: X-ray, ultrasound, tomography, echocardiogram, cardiac catheterization, laboratory tests) | 18 | 10.5 |

| Costs of surgical procedures (examples: gastroplasty, appendectomy, cholecystectomy) | 13 | 7.6 |

| Drug therapy costs | 12 | 7 |

| Costs involving health professionals (examples: doctors, nurses, physiotherapists, speech therapists) | 10 | 5.8 |

| 172 | 100 |

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2023 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Marques, I.C.P.; Alves, M.-C. Hospital Costing Methods: Four Decades of Literature Review. J. Risk Financial Manag. 2023, 16, 433. https://doi.org/10.3390/jrfm16100433

Marques ICP, Alves M-C. Hospital Costing Methods: Four Decades of Literature Review. Journal of Risk and Financial Management. 2023; 16(10):433. https://doi.org/10.3390/jrfm16100433

Chicago/Turabian StyleMarques, Isabel C. P., and Maria-Ceu Alves. 2023. "Hospital Costing Methods: Four Decades of Literature Review" Journal of Risk and Financial Management 16, no. 10: 433. https://doi.org/10.3390/jrfm16100433

APA StyleMarques, I. C. P., & Alves, M.-C. (2023). Hospital Costing Methods: Four Decades of Literature Review. Journal of Risk and Financial Management, 16(10), 433. https://doi.org/10.3390/jrfm16100433