On the Risk Spillover from Bitcoin to Altcoins: The Fear of Missing Out and Pump-and-Dump Scheme Effects

Abstract

1. Introduction

2. Methodology

3. Data and Descriptive Statistics

4. Empirical Results and Discussion

5. Conclusions

Author Contributions

Funding

Data Availability Statement

Conflicts of Interest

Appendix A

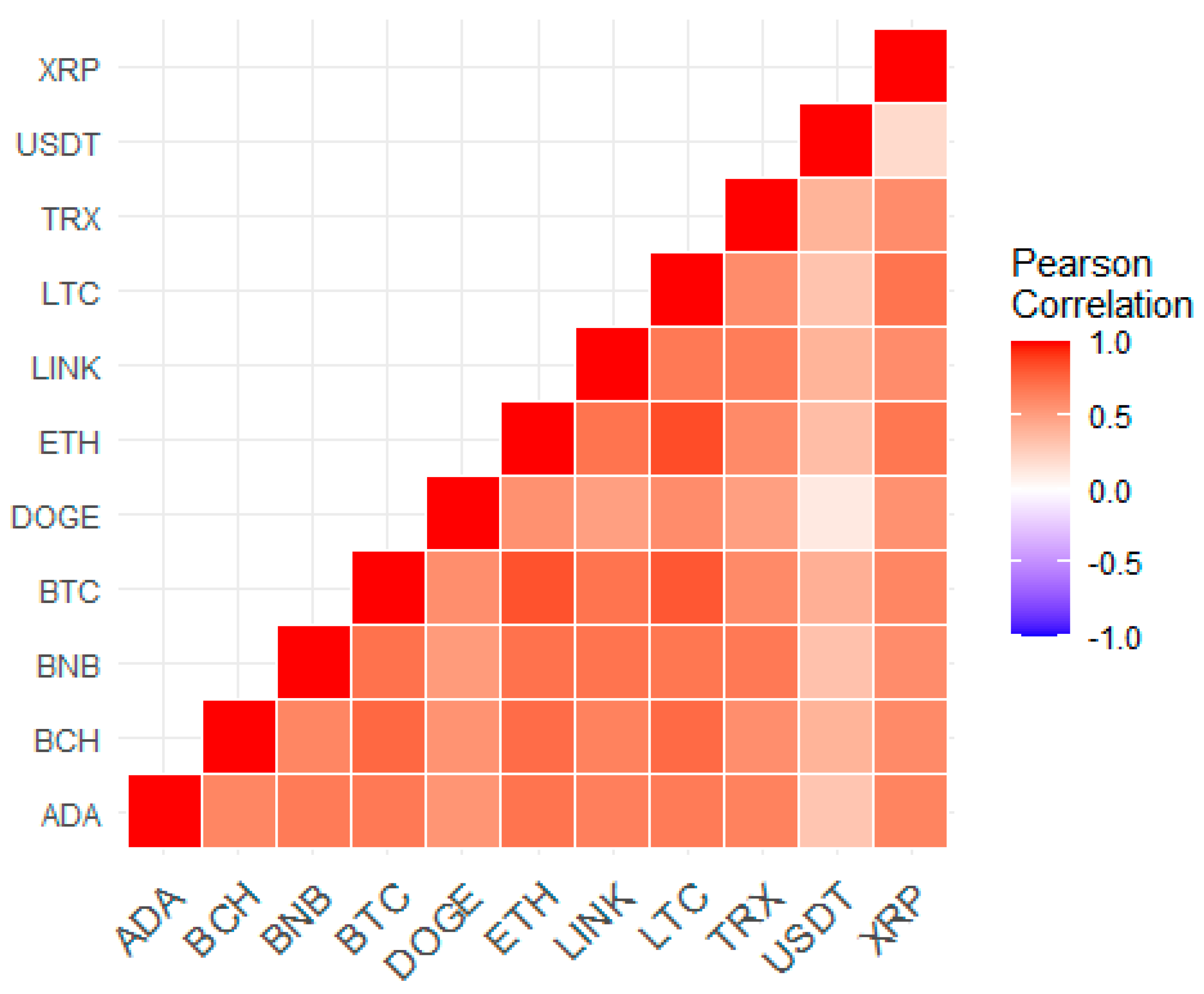

| 1 | Bitcoin (BTC), Cardano (ADA), Binance Coin (BNB), Bitcoin Cash (BCH), Dogecoin (Doge), Ethereum (ETH), Chainlink (LINK), Litecoin (LTC), Tron (TRX), Tether (USDT), and Ripple (XRP). |

| 2 | See, e.g., Nelson (1991) for E-GARCH, Glosten et al. (1993) for leverage effect GARCH, and (Zakoian 1994) for TGARCH. |

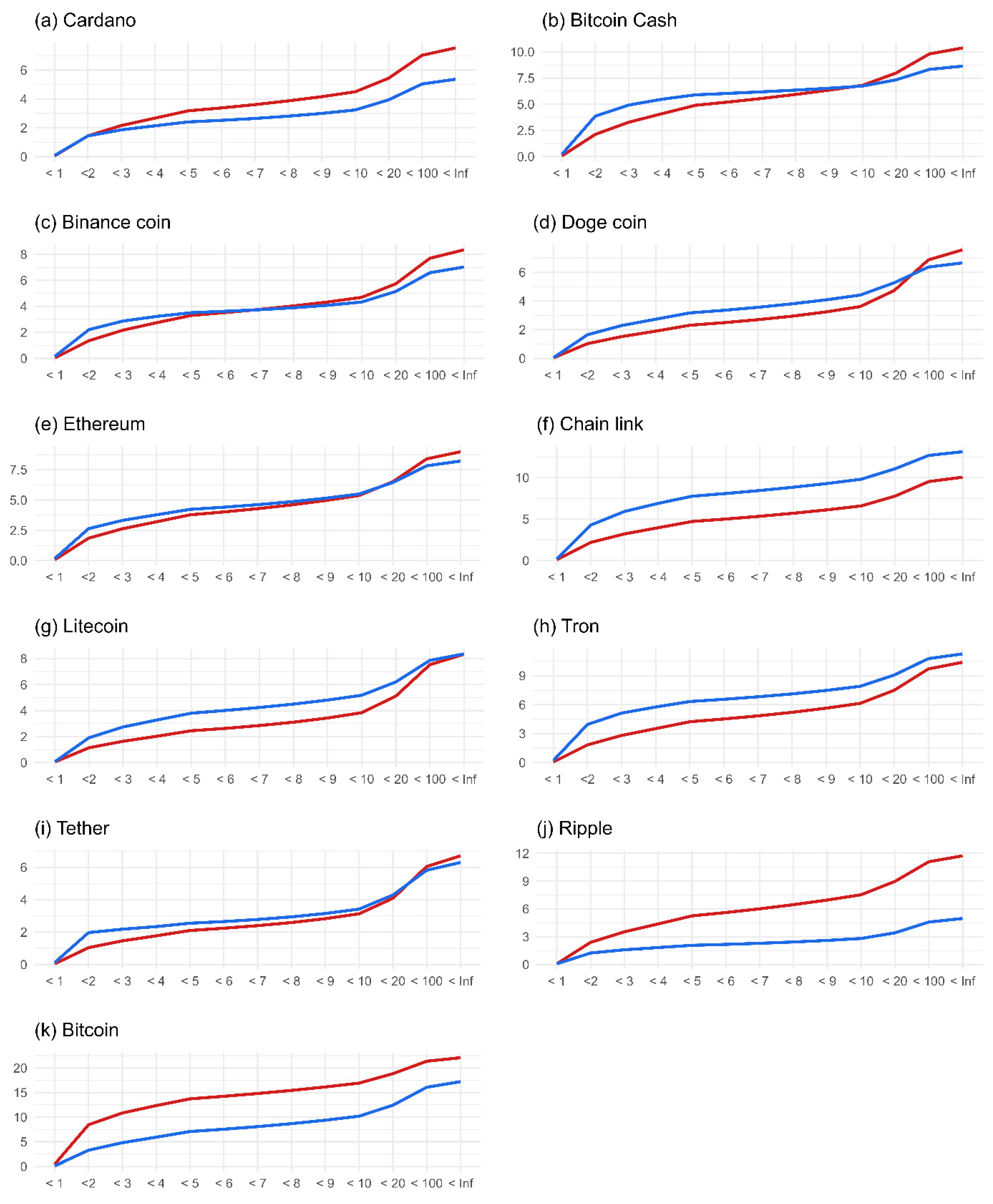

| 3 | Following Garman and Klass (1980), we calculate the daily volatility series using the daily opening, closing, high, and low prices. Firstly, the daily volatility is calculated as , where , , , and show the minimum, the maximum, the close, and the opening price of the market i on day t, respectively. Second, we annualize the volatility series utilizing the formula . |

| 4 | We calculate the daily returns of Bitcoin by taking the logarithm of the close price divided by the open price as . The daily observations span from 1 September 2017, to 2 March 2022. |

| 5 | The behavior of informed investors is consistent with the basic suggestions of economic theory. They put more emphasis on investment knowledge and economic-related criteria than uninformed investors, who are more influenced by behavioral elements such as personality and sentiment (Jalilvand et al. 2018). Based on this fact, it is fair to think that uninformed investors are more open to market rumors with no economic justification. |

References

- Ang, Andrew, and Joseph Chen. 2002. Asymmetric correlations of equity portfolios. Journal of Financial Economics 63: 443–94. [Google Scholar] [CrossRef]

- Aslanidis, Nektarios, Aurelio F. Bariviera, and Alejandro Perez-Laborda. 2021. Are cryptocurrencies becoming more interconnected? Economics Letters 199: 109725. [Google Scholar] [CrossRef]

- Balcilar, Mehmet, Elie Bouri, Rangan Gupta, and David Roubaud. 2017. Can volume predict Bitcoin returns and volatility? A quantiles-based approach. Economic Modelling 64: 74–81. [Google Scholar] [CrossRef]

- Barndorff-Nielsen, Ole E., Silja Kinnebrock, and Neil Shephard. 2010. Measuring Downside Risk—Realized Semivariance. In Volatility and Time Series Econometrics: Essays in Honor of Robert Engle. Oxford: Oxford Academic. [Google Scholar] [CrossRef]

- Baruník, Jozef, and Tomáš Křehlík. 2018. Measuring the frequency dynamics of financial connectedness and systemic risk. Journal of Financial Econometrics 16: 271–96. [Google Scholar] [CrossRef]

- Baruník, Jozef, Evžen Kočenda, and Lukáš Vácha. 2016. Asymmetric connectedness on the U.S. stock market: Bad and good volatility spillovers. Journal of Financial Markets 27: 55–78. [Google Scholar] [CrossRef]

- Baruník, Jozef, Evžen Kočenda, and Lukáš Vácha. 2017. Asymmetric volatility connectedness on the forex market. Journal of International Money and Finance 77: 39–56. [Google Scholar] [CrossRef]

- Baur, Dirk G., and Thomas Dimpfl. 2018. Asymmetric volatility in cryptocurrencies. Economics Letters 173: 148–51. [Google Scholar] [CrossRef]

- Bernabe, Jorge Bernal, Jose Luis Canovas, Jose L. Hernandez-Ramos, Rafael Torres Moreno, and Antonio Skarmeta. 2019. Privacy-Preserving Solutions for Blockchain: Review and Challenges. IEEE Access 7: 164908–164940. [Google Scholar] [CrossRef]

- Blau, Benjamin M. 2018. Price dynamics and speculative trading in Bitcoin. Research in International Business and Finance 43: 493–99. [Google Scholar] [CrossRef]

- Böhme, Rainer, Nicolas Christin, Benjamin Edelman, and Tyler Moore. 2015. Bitcoin: Economics, technology, and governance. Journal of Economic Perspectives 29: 213–38. [Google Scholar] [CrossRef]

- Bollerslev, Tim. 1987. A Conditionally Heteroskedastic Time Series Model for Speculative Prices and Rates of Return. The Review of Economics and Statistics 69: 542–47. [Google Scholar] [CrossRef]

- Bouri, Elie, Mahamitra Das, Rangan Gupta, and David Roubaud. 2018. Spillovers between Bitcoin and other assets during bear and bull markets. Applied Economics 50: 5935–49. [Google Scholar] [CrossRef]

- Brandvold, Morten, Peter Molnár, Kristian Vagstad, and Ole Christian Andreas Valstad. 2015. Price discovery on Bitcoin exchanges. Journal of International Financial Markets, Institutions and Money 36: 18–35. [Google Scholar] [CrossRef]

- Brik, Hatem, el Ouakdi Jihene, and Ftiti Zied. 2022. Roles of stable versus nonstable cryptocurrencies in Bitcoin market dynamics. Research in International Business and Finance 62: 101720. [Google Scholar] [CrossRef]

- Cappiello, Lorenzo, Robert F. Engle, and Kevin Sheppard. 2006. Asymmetric dynamics in the correlations of global equity and bond returns. Journal of Financial Econometrics 4: 537–72. [Google Scholar] [CrossRef]

- Charfeddine, Lanouar, Noureddine Benlagha, and Youcef Maouchi. 2020. Investigating the dynamic relationship between cryptocurrencies and conventional assets: Implications for financial investors. Economic Modelling 85: 198–217. [Google Scholar] [CrossRef]

- Chemkha, Rahma, Ahmed BenSaïda, Ahmed Ghorbel, and Tahar Tayachi. 2021. Hedge and safe haven properties during COVID-19: Evidence from Bitcoin and gold. Quarterly Review of Economics and Finance 82: 71–85. [Google Scholar] [CrossRef]

- Ciaian, Pavel, Rajcaniova Miroslava, and Kancs d’Artis. 2018. Virtual relationships: Short- and long-run evidence from BitCoin and altcoin markets. Journal of International Financial Markets, Institutions and Money 52: 173–95. [Google Scholar] [CrossRef]

- Corbet, Shaen, Andrew Meegan, Charles Larkin, Brian Lucey, and Larisa Yarovaya. 2018a. Exploring the dynamic relationships between cryptocurrencies and other financial assets. Economics Letters 165: 28–34. [Google Scholar] [CrossRef]

- Corbet, Shaen, Brian Lucey, and Larisa Yarovaya. 2018b. Datestamping the Bitcoin and Ethereum bubbles. Finance Research Letters 26: 81–88. [Google Scholar] [CrossRef]

- Corbet, Shaen, Brian Lucey, Andrew Urquhart, and Larisa Yarovaya. 2019. Cryptocurrencies as a financial asset: A systematic analysis. International Review of Financial Analysis 62: 182–99. [Google Scholar] [CrossRef]

- De Filippi, Primavera. 2014. Bitcoin: A regulatory nightmare to a libertarian dream. Internet Policy Review 3. [Google Scholar] [CrossRef]

- Delfabbro, Paul, Daniel L. King, and Jennifer Williams. 2021. The psychology of cryptocurrency trading: Risk and protective factors. Journal of Behavioral Addictions 10: 201–7. [Google Scholar] [CrossRef]

- Demir, Ender, Serdar Simonyan, Conrado-Diego García-Gómez, and Chi Keung Marco Lau. 2021. The asymmetric effect of bitcoin on altcoins: Evidence from the nonlinear autoregressive distributed lag (NARDL) model. Finance Research Letters 40: 101754. [Google Scholar] [CrossRef]

- Diebold, Francis X., and Kamil Yilmaz. 2009. Measuring financial asset return and volatility spillovers, with application to global equity markets. Economic Journal 119: 158–71. [Google Scholar] [CrossRef]

- Diebold, Francis X., and Kamil Yilmaz. 2012. Better to give than to receive: Predictive directional measurement of volatility spillovers. International Journal of Forecasting 28: 57–66. [Google Scholar] [CrossRef]

- Engle, Robert F. 1982. Autoregressive Conditional Heteroscedasticity with Estimates of the Variance of United Kingdom Inflation. Econometrica 50: 987–1007. [Google Scholar] [CrossRef]

- Fasanya, Ismail Olaleke, Oluwatomisin Oyewole, and Temitope Odudu. 2021. Returns and volatility spillovers among cryptocurrency portfolios. International Journal of Managerial Finance 17: 327–41. [Google Scholar] [CrossRef]

- Fletcher, Emily, Charles Larkin, and Shaen Corbet. 2021. Countering money laundering and terrorist financing: A case for bitcoin regulation. Research in International Business and Finance 56: 101387. [Google Scholar] [CrossRef]

- Fousekis, Panos, and Dimitra Tzaferi. 2021. Returns and volume: Frequency connectedness in cryptocurrency markets. Economic Modelling 95: 13–20. [Google Scholar] [CrossRef]

- Garman, Mark B., and Michael J. Klass. 1980. On the Estimation of Security Price Volatilities from Historical Data. The Journal of Business 53: 67–78. [Google Scholar] [CrossRef]

- Glosten, Lawrence R., Ravi Jagannathan, and David E. Runkle. 1993. On the Relation between the Expected Value and the Volatility of the Nominal Excess Return on Stocks. The Journal of Finance 48: 1779–801. [Google Scholar] [CrossRef]

- Jalilvand, Abolhassan, Mojtaba Rostami Noroozabad, and Jeannette Switzer. 2018. Informed and uninformed investors in Iran: Evidence from the Tehran Stock Exchange. Journal of Economics and Business 95: 47–58. [Google Scholar] [CrossRef]

- Katsiampa, Paraskevi, Larisa Yarovaya, and Damian Zięba. 2022. High-Frequency connectedness between bitcoin and other top-traded crypto assets during the COVID-19 crisis. Journal of International Financial Markets, Institutions and Money 79: 101578. [Google Scholar] [CrossRef]

- Katsiampa, Paraskevi, Shaen Corbet, and Brian Lucey. 2019. High frequency volatility co-movements in cryptocurrency markets. Journal of International Financial Markets, Institutions and Money 62: 35–52. [Google Scholar] [CrossRef]

- Khuntia, Sashikanta, and J. K. Pattanayak. 2018. Adaptive market hypothesis and evolving predictability of bitcoin. Economics Letters 167: 26–28. [Google Scholar] [CrossRef]

- Koop, Gary, M. Hashem Pesaran, and Simon M. Potter. 1996. Impulse response analysis in nonlinear multivariate models. Journal of Econometrics 74: 119–47. [Google Scholar] [CrossRef]

- Koutmos, Dimitrios. 2018. Return and volatility spillovers among cryptocurrencies. Economics Letters 173: 122–27. [Google Scholar] [CrossRef]

- Kumar, Ashish, Najaf Iqbal, Subrata Kumar Mitra, Ladislav Kristoufek, and Elie Bouri. 2022. Connectedness among major cryptocurrencies in standard times and during the COVID-19 outbreak. Journal of International Financial Markets, Institutions and Money 77: 101523. [Google Scholar] [CrossRef]

- Mensi, Walid, Khamis Hamed Al-Yahyaee, Idries Mohammad Wanas Al-Jarrah, Xuan Vinh Vo, and Sang Hoon Kang. 2021. Does volatility connectedness across major cryptocurrencies behave the same at different frequencies? A portfolio risk analysis. International Review of Economics and Finance 76: 96–113. [Google Scholar] [CrossRef]

- Nakamoto, Satoshi. 2008. Bitcoin: A Peer-to-Peer Electronic Cash System. Available online: https://bitcoin.org/bitcoin.pdf (accessed on 10 December 2022).

- Nan, Zheng, and Taisei Kaizoji. 2019. Market efficiency of the bitcoin exchange rate: Weak and semi-strong form tests with the spot, futures and forward foreign exchange rates. International Review of Financial Analysis 64: 273–81. [Google Scholar] [CrossRef]

- Nelson, Daniel B. 1991. Conditional Heteroskedasticity in Asset Returns: A New Approach. Econometrica 59: 347–70. [Google Scholar] [CrossRef]

- Park, Minjung, and Sangmi Chai. 2020. The effect of information asymmetry on investment behavior in cryptocurrency market. Paper presented at the Annual Hawaii International Conference on System Sciences, Maui, HI, USA, January 7–10. [Google Scholar]

- Pesaran, H. Hashem, and Yongcheol Shin. 1998. Generalized impulse response analysis in linear multivariate models. Economics Letters 58: 17–29. [Google Scholar] [CrossRef]

- Pinzón, Carlos, and Camilo Rocha. 2016. Double-spend Attack Models with Time Advantange for Bitcoin. Electronic Notes in Theoretical Computer Science 329: 79–103. [Google Scholar] [CrossRef]

- Sensoy, Ahmet, Thiago Christiano Silva, Shaen Corbet, and Benjamin Miranda Tabak. 2021. High-frequency return and volatility spillovers among cryptocurrencies. Applied Economics 53: 4310–28. [Google Scholar] [CrossRef]

- Smaniotto, Emanuelle Nava, and Giacomo Balbinotto Neto. 2020. Speculative trading in Bitcoin: A Brazilian market evidence. Quarterly Review of Economics and Finance 85: 47–54. [Google Scholar] [CrossRef]

- Urquhart, Andrew, and Hanxiong Zhang. 2019. Is Bitcoin a hedge or safe haven for currencies? An intraday analysis. International Review of Financial Analysis 63: 49–57. [Google Scholar] [CrossRef]

- Vidal-Tomás, David, and Ana Ibañez. 2018. Semi-strong efficiency of Bitcoin. Finance Research Letters 27: 259–65. [Google Scholar] [CrossRef]

- Vranken, Harald. 2017. Sustainability of bitcoin and blockchains. Current Opinion in Environmental Sustainability 28: 1–9. [Google Scholar] [CrossRef]

- Wang, Jying-Nan, Hung-Chun Liu, Shuang Zhang, and Yuan-Teng Hsu. 2021. How does the informed trading impact Bitcoin returns and volatility? Applied Economics 53: 3223–33. [Google Scholar] [CrossRef]

- Wang, Qin, Bo Qin, Jiankun Hu, and Fu Xiao. 2020. Preserving transaction privacy in bitcoin. Future Generation Computer Systems 107: 793–804. [Google Scholar] [CrossRef]

- Xu, Jiahua, and Benjamin Livshits. 2019. The anatomy of a cryptocurrency pump-and-dump scheme. Paper presented at the 28th USENIX Security Symposium, Santa Clara, CA, USA, August 14–16. [Google Scholar]

- Yi, Shuyue, Zishuang Xu, and Gang-Jin Wang. 2018. Volatility connectedness in the cryptocurrency market: Is Bitcoin a dominant cryptocurrency? International Review of Financial Analysis 60: 98–114. [Google Scholar] [CrossRef]

- Zakoian, Jean-Michel. 1994. Threshold heteroskedastic models. Journal of Economic Dynamics and Control 18: 931–55. [Google Scholar] [CrossRef]

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| Mean | Max | Min | Std. dev. | Skewness | Kurtosis | Jarque-Bera | |

|---|---|---|---|---|---|---|---|

| ADA | 102.77 | 905.00 | 11.00 | 83.68 | 3.74 | 25.19 | 36,860.69 *** |

| BCH | 91.20 | 961.29 | 11.96 | 75.46 | 3.90 | 30.42 | 54,594.35 *** |

| BNB | 90.25 | 748.61 | 12.50 | 74.03 | 3.35 | 19.90 | 22,219.43 *** |

| DOGE | 100.28 | 1484.94 | 12.54 | 107.43 | 4.62 | 38.64 | 91,120.25 *** |

| ETH | 75.16 | 664.39 | 7.52 | 55.11 | 3.38 | 23.20 | 30,504.73 *** |

| LINK | 124.77 | 791.07 | 17.72 | 86.49 | 2.62 | 13.61 | 9415.126 *** |

| LTC | 85.19 | 762.61 | 10.11 | 63.62 | 3.53 | 24.63 | 34,783.51 *** |

| TRX | 103.08 | 952.12 | 13.95 | 99.28 | 3.66 | 22.07 | 28,045.39 *** |

| USDT | 17.05 | 248.74 | 0.35 | 17.97 | 3.41 | 29.10 | 48,899.68 *** |

| XRP | 89.22 | 920.59 | 9.96 | 87.52 | 3.64 | 22.65 | 29,525.00 *** |

| BTC | 58.71 | 459.05 | 5.85 | 46.02 | 2.85 | 16.54 | 14,491.33 *** |

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2023 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Balcilar, M.; Ozdemir, H. On the Risk Spillover from Bitcoin to Altcoins: The Fear of Missing Out and Pump-and-Dump Scheme Effects. J. Risk Financial Manag. 2023, 16, 41. https://doi.org/10.3390/jrfm16010041

Balcilar M, Ozdemir H. On the Risk Spillover from Bitcoin to Altcoins: The Fear of Missing Out and Pump-and-Dump Scheme Effects. Journal of Risk and Financial Management. 2023; 16(1):41. https://doi.org/10.3390/jrfm16010041

Chicago/Turabian StyleBalcilar, Mehmet, and Huseyin Ozdemir. 2023. "On the Risk Spillover from Bitcoin to Altcoins: The Fear of Missing Out and Pump-and-Dump Scheme Effects" Journal of Risk and Financial Management 16, no. 1: 41. https://doi.org/10.3390/jrfm16010041

APA StyleBalcilar, M., & Ozdemir, H. (2023). On the Risk Spillover from Bitcoin to Altcoins: The Fear of Missing Out and Pump-and-Dump Scheme Effects. Journal of Risk and Financial Management, 16(1), 41. https://doi.org/10.3390/jrfm16010041