Does FDI Promote the Resource Curse in Nigeria?

Abstract

:1. Introduction

2. Related Literature

Research Questions

3. Data and Methodology

4. Methodology

4.1. Baseline Model

4.2. A Prior Expectation

5. Empirical Strategy

5.1. Motivation

5.2. Time Series Modelling

6. Results

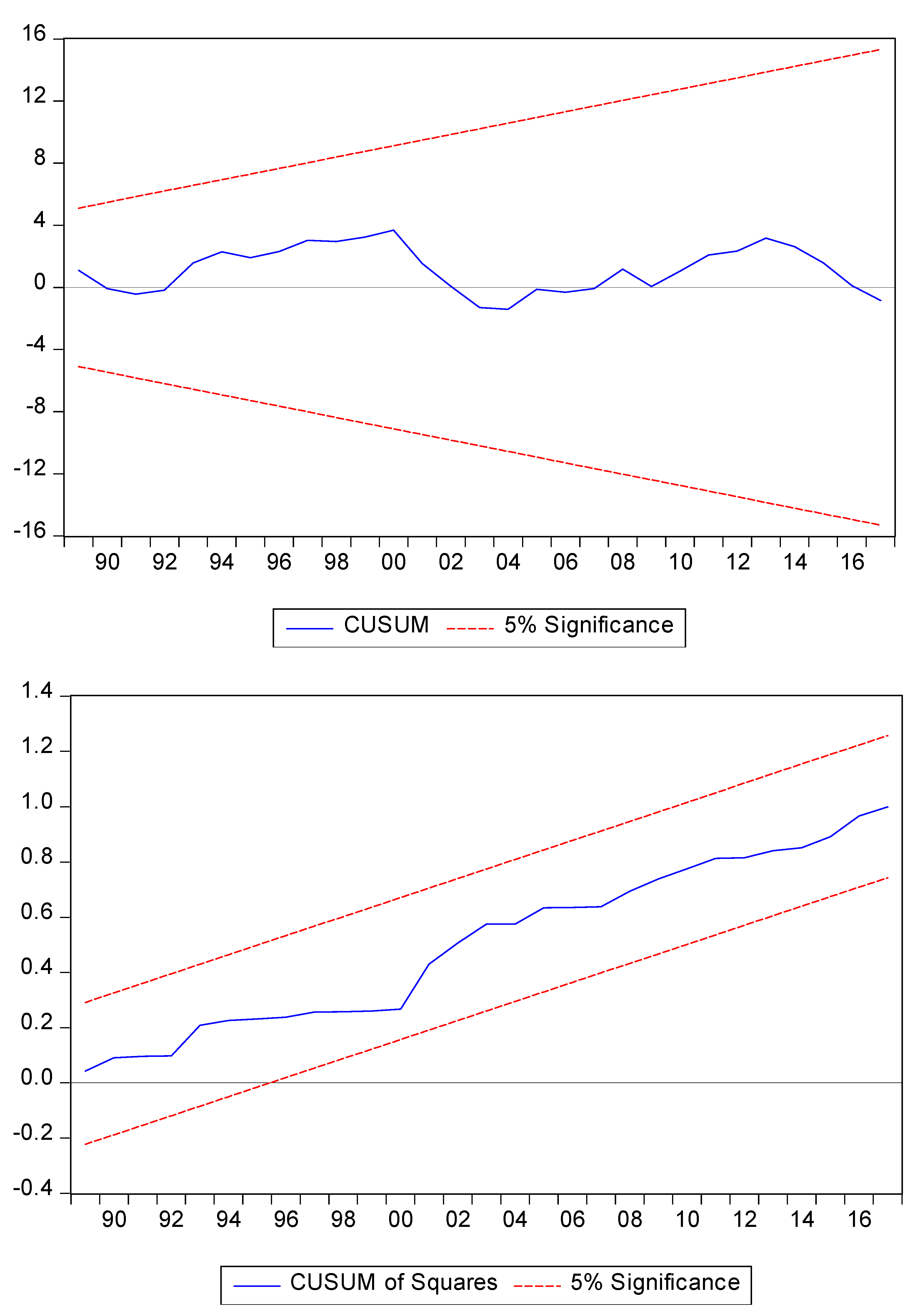

6.1. Preliminary Checks

6.2. Unit Root Test—Modified Efficient PP Test

6.3. Granger Causality Tests

7. Conclusions

Funding

Data Availability Statement

Acknowledgments

Conflicts of Interest

Appendix A

{kind=link}

{kind=link}

| Variables | Measurement | Sources | Symbols |

|---|---|---|---|

| Economic welfare | Our welfare variable is computed by combing the real domestic absorption, capital stock, and real total factor productivity (TFP) | Penn World Table (PWT 9.1) | |

| Natural resources | |||

| Natural resources driven by GDP | Natural resources to GDP (oil rent, mineral rent, and forest rent) (see, Asiedu 2013; Bokpin et al. 2015) | Central Bank of Nigeria (CBN) | |

| Natural resources driven by export | Natural resource to export (fuel export (FE) and mineral export). | Central Bank of Nigeria (CBN) | |

| Total natural resources | Total natural resource rent computed as the sum of oil rent (%GDP), natural gas, coal rents, regional rental ratem and average price (Bokpin et al. 2015; Ndikumana and Sarr 2019) | Central Bank of Nigeria (CBN) | |

| FDI | Net inward FDI inflows (% GDP) (Ndikumana and Sarr 2019) | UNCTAD stat | |

| Trade openness | It is measured as trade (% GDP) | World Bank (WDI) | |

| Real exchange rate | It is a measure of the value of a currency against weighted average of several foreign currencies by divided by price deflator. | World Bank (WDI) |

References

- Acheampong, Prince, and Victor Osei. 2014. Foreign direct investment (FDI) inflows into Ghana: Should the focus be on infrastructure or natural resources? Short-run and long-run analyses. International Journal of Financial Research 5: 42–51. [Google Scholar] [CrossRef]

- Adekoya, Oluwasegun B. 2020. Revisiting oil consumption-economic growth nexus: Resource-curse and scarcity tales. Resources Policy 70: 101911. [Google Scholar] [CrossRef]

- Aleksynska, Mariya, and Olena Havrylchyk. 2013. FDI from the south: The role of institutional distance and natural resources. European Journal of Political Economy 29: 38–53. [Google Scholar] [CrossRef]

- Anarfo, Ebenezer Bugri, Abel Mawuko Agoba, and Robert Abebreseh. 2017. Foreign direct investment in Ghana: The role of infrastructural development and natural resources. African Development Review 29: 575–88. [Google Scholar] [CrossRef]

- Anyanwu, John. C. 2012. Why Does Foreign Direct Investment Go Where it Goes? New Evidence from African Countries. Annals of Economics & Finance 13: 425–62. [Google Scholar]

- Asamoah, Michael Effah, Charles K. D. Adjasi, and Abdul Latif Alhassan. 2016. Macroeconomic uncertainty, foreign direct investment, and institutional quality: Evidence from Sub-Saharan Africa. Economic Systems 40: 612–21. [Google Scholar] [CrossRef]

- Asiedu, Elizabeth. 2002. On the Determinants of Foreign Direct Investment to Developing Countries: Is Africa Different? World Development 30: 107–19. [Google Scholar] [CrossRef]

- Asiedu, Elizabeth. 2004. The Determinants of Employment of Affiliates of US Multinational Enterprises in Africa. Development Policy Review 22: 371–39. [Google Scholar] [CrossRef]

- Asiedu, Elizabeth. 2006. Foreign Direct Investment in Africa: The Role of Natural Resources, Market Size, Government Policy, Institutions and Political Instability. The Word Economy 29: 63–77. [Google Scholar] [CrossRef]

- Asiedu, Elizabeth. 2013. Foreign Direct Investment, Natural Resources and Institutions. Available online: http://www.theigc.org/wp-content/uploads/2014/09/asiedu-2013-working-Paper.pdf (accessed on 12 September 2022).

- Asiedu, Elizabeth, and D. Lien. 2011. Democracy, foreign direct investment, and natural resources. Journal of International Economics 84: 99–111. [Google Scholar] [CrossRef]

- Asif, Muhammad, Khan Burhan Khan, Muhammad Khalid Anser, Abdelmohsen A. Nassani, Muhammad Moinuddin Qazi Abro, and Khalid Zaman. 2020. Dynamic interaction between financial development and natural resources: Evaluating the ‘Resource curse’ hypothesis. Resources Policy 65: 101566. [Google Scholar] [CrossRef]

- Basu, P., C. Chakraborty, and D. Reagle. 2003. Liberalization, FDI, and Growth in Developing Countries: A Panel Co- Integration Approach. Economic Inquiry 51: 510–16. [Google Scholar] [CrossRef]

- Bokpin, Godfred Alufar, Lord Mensah, and Michael E. Asamoah. 2015. Foreign direct investment and natural resources in Africa. Journal of Economic Studies 42: 608–21. [Google Scholar] [CrossRef]

- Bouoiyour, J., and S. Rey. 2005. Exchange rate regime, real exchange rate, trade flows and foreign direct investments: The case of Morocco. African Development Review 17: 302–34. [Google Scholar] [CrossRef]

- BP Energy Outlook. 2019. Edition. London: Spring. [Google Scholar]

- Bressler, Steven L., and Anil K Seth. 2011. Wiener–Granger causality: A well-established methodology. Neuroimage 58: 323–29. [Google Scholar] [CrossRef]

- Büthe, Tim, and Helen V. Milner. 2008. The politics of foreign direct investment into developing countries: Increasing FDI through international trade agreements? American Journal of Political Science 52: 741–62. [Google Scholar] [CrossRef]

- Conde, Marta. 2017. Resistance to mining. A review. Ecological Economics 132: 80–90. [Google Scholar] [CrossRef]

- Dogan, Eyup, Buket Altinoz, and Panayiotis Tzeremes. 2020. The analysis of ‘Financial Resource Curse’hypothesis for developed countries: Evidence from asymmetric effects with quantile regression. Resources Policy 68: 101773. [Google Scholar] [CrossRef]

- Dumitrescu, Elena Ivona, and Christophe Hurlin. 2012. Testing for Granger non-causality in heterogeneous panels. Economic Modelling 29: 1450–60. [Google Scholar] [CrossRef]

- Eissa, Mohamed Abdelaziz, and Mohammed M. Elgammal. 2020. Foreign Direct Investment Determinants in Oil Exporting Countries: Revisiting the Role of Natural Resources. Journal of Emerging Market Finance 19: 33–65. [Google Scholar] [CrossRef]

- Granger, C. W. 1969. Investigating causal relations by econometric models and cross-spectral methods. Econometrica: Journal of the Econometric Society 37: 424–38. [Google Scholar] [CrossRef]

- Guan, Jialin, Dervis Kirikkaleli, Ayesha Bibi, and Weike Zhang. 2020. Natural resources rent nexus with financial development in the presence of globalization: Is the “resource curse” exist or myth? Resources Policy 66: 101641. [Google Scholar] [CrossRef]

- Hussain, Muzzammil, Zhi Wei Ye, Muhammad Usman, Ghulam Mustafa Mir, Ahmad Usman, and Syed Kumail Abbas Rizvi. 2020. Re-investigation of the resource curse hypothesis: The role of political institutions and energy prices in BRIC countries. Resources Policy 69: 101833. [Google Scholar] [CrossRef]

- Idemudia, Uwafiokun. 2012. The resource curse and the decentralization of oil revenue: The case of Nigeria. Journal of Cleaner Production 35: 183–93. [Google Scholar] [CrossRef]

- Kuruppuarachchi, Duminda, and I. M. Premachandra. 2016. Information spillover dynamics of the energy futures market sector: A novel common factor approach. Energy Economics 57: 277–94. [Google Scholar] [CrossRef]

- Li, Yumei, Bushra Naqvi, Ersin Caglar, and Chien-Chi Chu. 2020. N-11 countries: Are the new victims of resource-curse? Resources Policy 67: 101697. [Google Scholar] [CrossRef]

- Mejía Acosta, Andrés. 2013. The impact and effectiveness of accountability and transparency initiatives: The governance of natural resources. Development Policy Review 31: s89–s105. [Google Scholar] [CrossRef]

- Ndikumana, Leonce, and Mare Sarr. 2019. Capital flight, foreign direct investment and natural resources in Africa. Resources Policy 63: 101427. [Google Scholar] [CrossRef]

- Ng, Serena, and Pierre Perron. 2001. Lag length selection and the construction of unit root tests with good size and power. Econometrica 69: 1519–54. [Google Scholar] [CrossRef]

- Okpanachi, E., and N. Andrews. 2012. Preventing the oil “resource curse” in Ghana: Lessons from Nigeria. World Futures 68: 430–50. [Google Scholar] [CrossRef]

- Olayungbo, D. O. 2019. Effects of oil export revenue on economic growth in Nigeria: A time varying analysis of resource curse. Resources Policy 64: 101469. [Google Scholar] [CrossRef]

- Omri, A., D. K. Nguyen, and C. Rault. 2014. Causal interactions between CO2 emissions, FDI, and economic growth: Evidence from dynamic simultaneous-equation models. Economic Modelling 42: 382–89. [Google Scholar] [CrossRef]

- Onditi, Francis. 2019. From resource curse to institutional incompatibility: A comparative study of Nigeria and Norway oil resource governance. Africa Review 11: 152–71. [Google Scholar] [CrossRef]

- Onyeiwu, Steve, and H. Shrestha. 2004. Determinants of foreign direct investment in Africa. Journal of Developing Societies 20: 89–106. [Google Scholar] [CrossRef]

- Onyeukwu, Agwara John. 2007. Resource Curse in Nigeria: Perception and Challenges. Policy Paper. Budapest: International Policy Fellowship Programme of the Open Society Institute. Available online: http://www.policy.hu/themes06/resource/index.html (accessed on 21 April 2010).

- Orogun, Paul. S. 2010. Resource control, revenue allocation and petroleum politics in Nigeria: The Niger Delta question. GeoJournal 75: 459–507. [Google Scholar] [CrossRef]

- Perron, Pierre, and Serena Ng. 1996. Useful modifications to some unit root tests with dependent errors and their local asymptotic properties. The Review of Economic Studies 63: 435–63. [Google Scholar] [CrossRef]

- Poelhekke, Steven, and Frederick Van Der Ploeg. 2009. Foreign direct investments and urban concentration: Unbundling Spatial lags. Journal of Regional Science 48: 749–75. [Google Scholar] [CrossRef]

- Poelhekke, Steven, and Frederick Van der Ploeg. 2010. Do Natural Resources Attract FDI? Evidence from Non-Stationary Sector-Level Data. CEPR Discussion Paper No. 8079. Amsterdam: CEPR. [Google Scholar]

- Porter, Doug, and Michael Watts. 2017. Righting the resource curse: Institutional politics and state capabilities in Edo state, Nigeria. The Journal of Development Studies 53: 249–63. [Google Scholar] [CrossRef]

- Rudra, Nita, and Nathan. M. Jensen. 2011. Globalization and the politics of natural resources. Comparative Political Studies 44: 639–61. [Google Scholar] [CrossRef]

- Sachs, Jeffrey D., and Andrew M. Warner. 1995. Natural Resource Abundance and Economic Growth. (No. w5398). Cambridge: National Bureau of Economic Research. [Google Scholar]

- Sachs, Jeffrey D., and Andrew Warner. 2001. The curse of natural resources. European Economic Review 45: 827–38. [Google Scholar] [CrossRef]

- Sala-i-Martin, Xavier, and Arvind Subramanian. 2013. Addressing the natural resource curse: An illustration from Nigeria. Journal of African Economies 22: 570–615. [Google Scholar] [CrossRef]

- Shobande, Olatunji A., and Simplice A. Asongu. 2021. Has knowledge improved economic growth? Evidence from Nigeria and South Africa. Journal of Public Affairs, e2763. [Google Scholar] [CrossRef]

- Shobande, Olatunji A., and Simplice A. Asongu. 2022. The Critical Role of Education and ICT in Promoting Environmental Sustainability in Eastern and Southern Africa: A Panel VAR Approach. Technological Forecasting and Social Change 176: 121480. [Google Scholar] [CrossRef]

- Shobande, Olatunji A., and Joseph Onuche Enemona. 2021. A multivariate VAR model for evaluating sustainable finance and natural resource curse in West Africa: Evidence from Nigeria and Ghana. Sustainability 13: 2847. [Google Scholar] [CrossRef]

- Solarin, Sakiru Adebola. 2020. The effects of shale oil production, capital, and labour on economic growth in the United States: A maximum likelihood analysis of the resource curse hypothesis. Resources Policy 68: 101799. [Google Scholar] [CrossRef]

- Stevens, Paul, Glada Lahn, and Jaakko Kooroshy. 2015. The Resource Curse Revisited. London: Chatham House for the Royal Institute of International Affairs. [Google Scholar]

- Tekin, Rıfat Barış. 2012. Economic growth, exports, and foreign direct investment in Least Developed Countries: A panel Granger causality analysis. Economic Modelling 29: 868–78. [Google Scholar] [CrossRef]

- Wang, Pan, and Zhihong Yu. 2014. China’s Outward Foreign Direct Investment: The Role of Natural Resources and Technology. Economic and Political Studies 2: 89–120. [Google Scholar] [CrossRef]

- Watts, Michael. 2004. Resource curse? Governmentality, oil and power in the Niger Delta, Nigeria. Geopolitics 9: 50–80. [Google Scholar] [CrossRef]

- Xie, Bai-Chen, Li-Feng Shang, Si-Bo Yang, and Bo-Wen Yi. 2014. Dynamic environmental efficiency evaluation of electric power industries: Evidence from OECD (Organization for Economic Cooperation and Development) and BRIC (Brazil, Russia, India and China) countries. Energy 74: 147–57. [Google Scholar] [CrossRef]

- Xue, Yawei, Xuanting Ye, Wei Zhang, Jian Zhang, Yu Liu, Chuanbao Wu, and Qi Li. 2020. Reverification of the “resource curse” hypothesis based on industrial agglomeration: Evidence from China. Journal of Cleaner Production 275: 124075. [Google Scholar] [CrossRef]

| Variables | Mean | Std. Dev. | Obs |

|---|---|---|---|

| 1825 | 51.1 | 38 | |

| 86.16 | 33.58 | 38 | |

| 11.85 | 0.57 | 38 | |

| 0.36 | 0.02 | 38 | |

| 0.97 | 0.36 | 38 | |

| 0.75 | 0.04 | 38 | |

| 0.015 | 0.002 | 38 |

| Variables | ||||

|---|---|---|---|---|

| Level | ||||

| 1.33898 | 0.96977 | 0.72427 | 42.0692 | |

| −3.14978 | −0.95999 | 0.30478 | 7.37479 | |

| −3.48683 | −1.31790 | 0.37796 | 7.02560 | |

| −0.73262 | −0.39994 | 0.54591 | 18.4265 | |

| −1.5906 | −2.73658 | 0.17553 | 6.16880 | |

| −5.32248 | −2.13291 | 0.22879 | 272837 | |

| −1.79961 | −0.94623 | 0.52580 | 13.5804 | |

| First Difference | ||||

| −16.6052 ** | −2.87546 | 0.17317 | 1.49748 | |

| −9.94932 ** | −2.08835 | 0.20990 | 2.99738 | |

| −6.22189 ** | −1.62495 | 0.26177 | 4.37141 | |

| −15.3025 ** | −2.75571 | 0.18008 | 6.01582 | |

| −18.6885 ** | −2.96797 | 0.15881 | 5.40432 | |

| −15.4669 ** | −2.778836 | 0.17963 | 1.59357 | |

| −16.1275 ** | −2.79524 | 0.17332 | 5.91221 | |

| Critical Value | ||||

| 1% | −13.8000 | |||

| 5% | −8.1000 |

| Lag Tests | ||||||

|---|---|---|---|---|---|---|

| Lag | Lolo | LR | FPE | AIC | SC | HQ |

| 0 | 95.94877 | NA | 1.26e-11 | −5.232280 | −4.918030 | −5.125112 |

| 1 | 366.7270 | 414.1314 | 2.90e-17 | −18.27806 | −15.76405 * | −17.42071 |

| 2 | 436.4031 | 77.87333 * | 1.27e-17 * | −19.49430 * | −14.78054 | −17.88677 * |

| Trace Test | Max. Eigen Value Test | ||||

|---|---|---|---|---|---|

| Null Hypotheses | Eigenvalue | Statistics | 95% Critical Value | Statistics | 95% Critical Value |

| 0.97 | 370.33 * | 95.75 | 126.0 * | 49.58 | |

| 0.94 | 244.23 * | 65.81 | 95.8 * | 43.41 | |

| 0.85 | 148.43 * | 47.84 | 64.5 * | 37.16 | |

| 0.66 | 83.91 | 95.2 | 35.9 | 40.81 | |

| Independent | Short: Direction of Causality | Long Run | ||||||

|---|---|---|---|---|---|---|---|---|

| Dependent Variables | ||||||||

| - | 3.13 [0.92] | 5.61 ** [0.00] | 2.70 [0.57] | 1.24 [0.85] | 18 ** [0.00] | 1.24 [0.69] | −0.02 ** [0.00] | |

| 10.6 ** [0.00] | - | 5.9 ** [0.00] | 5.8 * [0.00] | 3.89 [0.28] | 0.53 [0.90] | 0.69 [0.84] | −0.08 ** [0.00] | |

| 21.5 ** [0.00] | 2.15 [1.45] | - | 7.1 ** [0.00] | 2.27 [0.58] | 5.90 ** [0.00] | 2.97 [0.64] | 0.001 * [0.00] | |

| 6.69 * [0.01] | 4.08 ** [0.00] | 9.58 ** [0.00] | - | 8.45 ** [0.00] | 1.95 [0.45] | 2.23 [0.59] | −0.04 * [0.00] | |

| 11.04 * [0.00] | 5.12 ** [0.00] | 3.16 [0.63] | 12.3 ** [0.00] | - | 8.42 ** [0.00] | 4.85 * [0.00] | 0.09 * [0.00] | |

| 9.10 ** [0.00] | 1.66 [0.16] | 6.79 ** [0.00] | 1.25 [0.84] | 1.22 [0.94] | - | 0.53 [0.61] | 0.001 [0.27] | |

| 14.5 ** [0.00] | 2.5 [0.38] | 4.65 * [0.371] | 1.56 [0.66] | 2.33 [0.87] | 1.41 [0.72] | - | −0.02 ** [0.00] | |

| Variables | Coefficient | Std. Error. |

|---|---|---|

| −1.51 * | 0.04 | |

| 0.25 ** | 0.06 | |

| 0.034 * | 0.00 | |

| 1.42 | 6.78 | |

| 0.007 ** | 0.00 | |

| 1.52 | 9.73 | |

| −0.03 * | 0.00 | |

| R-squared | 0.91 | |

| Adj R-squared | 0.89 | |

| S.E. of regression | 0.013 | |

| Akaike info criterion | −6.96 | |

| Schwarz criterion | −7.64 | |

| F-statistics | 134.6 | |

| Dublin–Watson | 1.78 | |

| Diagnostic tests | Statistics | p-value |

| J–B normality test | 0.813 | 0.7757 |

| Breusch–Godfrey LM test | 1.981 | 0.5668 |

| ARCH LM test | 1.567 | 0.6803 |

| White heteroscedasticity | 2.989 | 0.2404 |

| Ramsey RESET | 1.549 | 0.3722 |

| Variables | Coefficient | Std. Error. |

|---|---|---|

| −0.338 ** | 0.15 | |

| 0.104 ** | 0.03 | |

| 0.481 *** | 0.16 | |

| −2.37 | 5.20 | |

| 0.873 ** | 0.24 | |

| 0.901 * | 0.54 | |

| −0.337 | 0.29 | |

| −0.005 ** | 0.00 | |

| R-squared | 0.77 | |

| Adj R-squared | 0.73 | |

| S.E. of regression | 0.008 | |

| Akaike info criterion | −5.54 | |

| Schwarz criterion | −6.81 | |

| F-statistics | 134.6 | |

| Dublin–Watson | 1.78 | |

| Diagnostic tests | Statistics | p-value |

| J-B normality test | 0.7888 | 0.6740 |

| Breusch–Godfrey LM test | 1.713 | 0.1993 |

| ARCH LM test | 1.0157 | 0.9186 |

| White heteroscedasticity | 1.0234 | 0.5248 |

| Ramsey RESET | 1.9260 | 0.7251 |

| Forecast Period | F-Statistics | p-Value of F-Statistics | Log-Likelihood Ratio | p-Value of Log of Likelihood |

|---|---|---|---|---|

| 1989–2010 | 1.258 | 0.619 | 56.18 | 0.895 |

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2022 by the author. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Shobande, O.A. Does FDI Promote the Resource Curse in Nigeria? J. Risk Financial Manag. 2022, 15, 415. https://doi.org/10.3390/jrfm15090415

Shobande OA. Does FDI Promote the Resource Curse in Nigeria? Journal of Risk and Financial Management. 2022; 15(9):415. https://doi.org/10.3390/jrfm15090415

Chicago/Turabian StyleShobande, Olatunji Abdul. 2022. "Does FDI Promote the Resource Curse in Nigeria?" Journal of Risk and Financial Management 15, no. 9: 415. https://doi.org/10.3390/jrfm15090415

APA StyleShobande, O. A. (2022). Does FDI Promote the Resource Curse in Nigeria? Journal of Risk and Financial Management, 15(9), 415. https://doi.org/10.3390/jrfm15090415