Trading Activity in Public Real Estate Markets

Abstract

:1. Introduction

2. Literature Review

3. Data and Variable Definition

4. Empirical Analysis

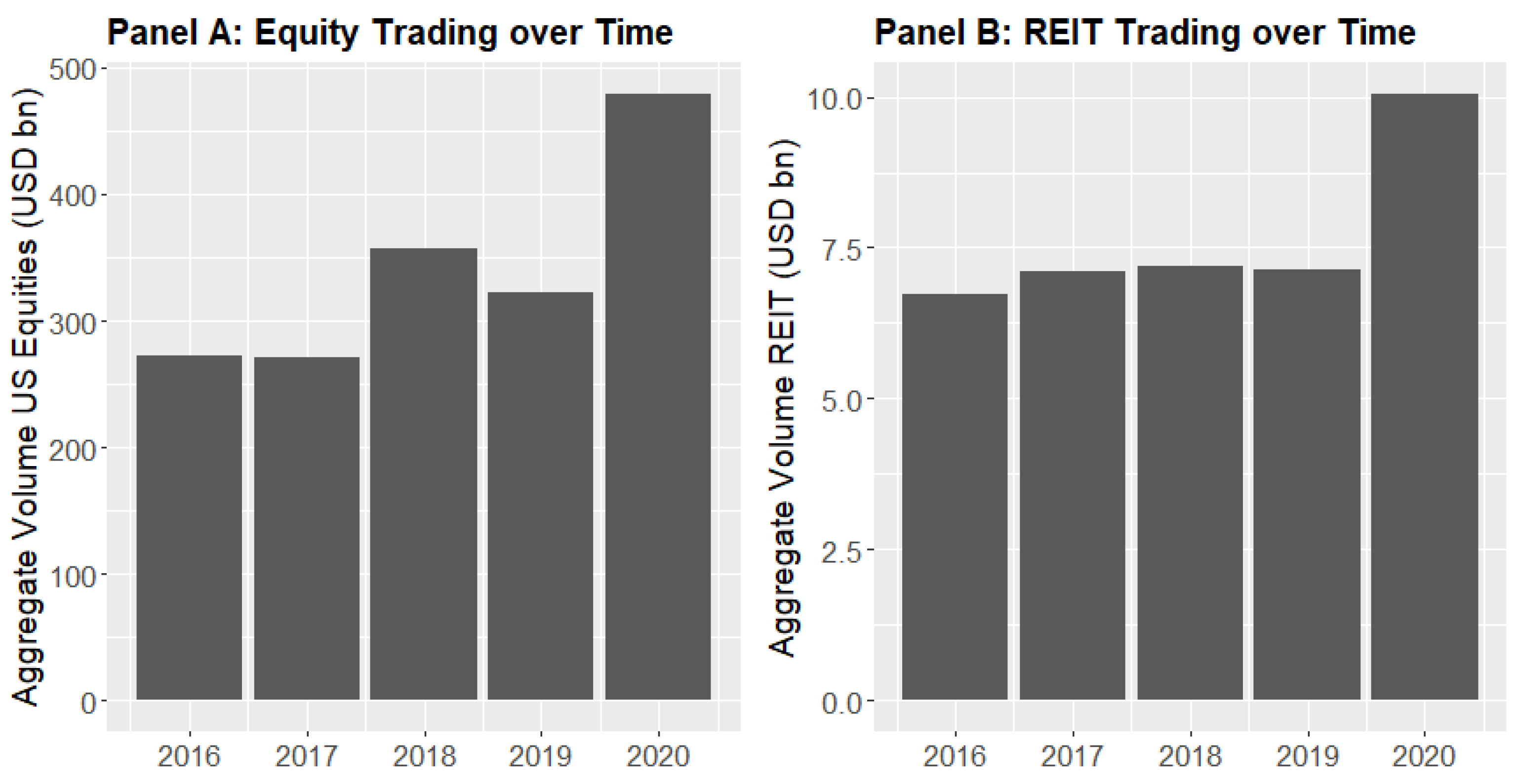

4.1. Descriptive Statistics

4.2. Baseline Results

4.3. Trading in Times of Crises

5. Conclusions

Funding

Institutional Review Board Statement

Informed Consent Statement

Data Availability Statement

Conflicts of Interest

| 1 | The results from Hoesli et al. (2017) show that commonality in liquidity for REITs is distinct from the broader equity markets such as in Chordia et al. (2000). The asset class specific aspects are also highlighted in Richter (2022). |

| 2 | To decide whether a fixed effects or random effects model should be used we estimated a Hausman test. The p-value of the test was smaller than 0.01 and therefore indicated the use of a fixed effects model. |

References

- Akinsomi, Omokolade. 2020. How resilient are REITs to a pandemic? The COVID-19 effect. Journal of Property Investment & Finance 39: 19–24. [Google Scholar]

- Ametefe, Frank, Steven Devaney, and Gianluca Marcato. 2016. Liquidity: A review of dimensions, causes, measures, and empirical applications in real estate markets. Journal of Real Estate Literature 24: 1–29. [Google Scholar]

- Barclay, Michael J., and Terrence Hendershott. 2003. Price discovery and trading after hours. Review of Financial Studies 16: 1041–73. [Google Scholar]

- Benveniste, Lawrence, Dennis R. Capozza, and Paul J. Seguin. 2001. The value of liquidity. Real Estate Economics 29: 633–60. [Google Scholar] [CrossRef]

- Bessembinder, Hendrik. 1994. Bid-ask spreads in the interbank foreign exchange markets. Journal of Financial Economics 35: 317–48. [Google Scholar] [CrossRef]

- Brennan, Michael J., and Patricia J. Hughes. 1991. Stock prices and the supply of information. The Journal of Finance 46: 1665–91. [Google Scholar] [CrossRef]

- Brennan, Michael J., Narasimhan Jegadeesh, and Bhaskaran Swaminathan. 1993. Investment analysis and the adjustment of stock prices to common information. The Review of Financial Studies 6: 799–824. [Google Scholar]

- Cajias, Marcelo, Philipp Freudenreich, Anna Freudenreich, and Wolfgang Schäfers. 2020. Liquidity and prices: A cluster analysis of the German residential real estate market. Journal of Business Economics 90: 1021–56. [Google Scholar] [CrossRef]

- Calvet, Laurent E., John Y. Campbell, and Paolo Sodini. 2009. Fight or flight? Portfolio rebalancing by individual investors. Quarterly Journal of Economics 124: 301–48. [Google Scholar]

- Chordia, Tarun, Avanidhar Subrahmanyam, and V. Ravi Anshuman. 2001a. Trading activity and expected stock returns. Journal of Financial Economics 59: 3–32. [Google Scholar]

- Chordia, Tarun, Richard Roll, and Avanidhar Subrahmanyam. 2000. Commonality in liquidity. Journal of Financial Economics 56: 3–28. [Google Scholar] [CrossRef]

- Chordia, Tarun, Richard Roll, and Avanidhar Subrahmanyam. 2001b. Market liquidity and trading activity. The Journal of Finance 56: 501–30. [Google Scholar] [CrossRef]

- Chordia, Tarun, Sahn-Wook Huh, and Avanidhar Subrahmanyam. 2007. The cross-section of expected trading activity. The Review of Financial Studies 20: 709–40. [Google Scholar] [CrossRef] [Green Version]

- Chou, Wen-Hsiu, William G. Hardin, Matthew D. Hill, and G. Wayne Kelly. 2013. Dividends, values and agency costs in REITs. The Journal of Real Estate Finance and Economics 46: 91–114. [Google Scholar] [CrossRef]

- Coles, Jeffrey L., and Uri Loewenstein. 1988. Equilibrium pricing and portfolio composition in the presence of uncertain parameters. Journal of Financial Economics 22: 279–303. [Google Scholar] [CrossRef]

- Danthine, Jean-Pierre, and Serge Moresi. 1993. Volatility, information and noise trading. European Economic Review 37: 961–82. [Google Scholar] [CrossRef]

- Diamond, Douglas W., and Robert E. Verrecchia. 1987. Constraints on short-selling and asset price adjustment to private information. Journal of Financial Economics 18: 277–311. [Google Scholar] [CrossRef]

- DiBartolomeo, Jeffrey A., Vladimir A. Gatchev, and David M. Harrison. 2021. The liquidity risk of REITs. Journal of Real Estate Research 43: 47–95. [Google Scholar] [CrossRef]

- Fleming, Michael J. 2003. Measuring treasury market liquidity. FRBNY Economic Policy Review 2003: 83–99. [Google Scholar] [CrossRef] [Green Version]

- Glosten, Lawrence R., and Paul R. Milgrom. 1985. Bid, ask and transaction prices in a specialist market with heterogeneously informed traders. Journal of Financial Economics 14: 71–100. [Google Scholar] [CrossRef] [Green Version]

- Grossman, Sanford J., and Joseph E. Stiglitz. 1980. On the impossibility of informationally efficient markets. The American Economic Review 70: 393–408. [Google Scholar]

- Harris, Milton, and Artur Raviv. 1991. The theory of capital structure. The Journal of Finance 46: 297–355. [Google Scholar] [CrossRef]

- Hartmann, Philipp. 1999. Trading volumes and transaction costs in the foreign exchange market: Evidence from daily dollar–yen spot data. Journal of Banking & Finance 23: 801–24. [Google Scholar]

- Hoesli, Martin, Anjeza Kadilli, and Kustrim Reka. 2017. Commonality in liquidity and real estate securities. The Journal of Real Estate Finance and Economics 55: 65–105. [Google Scholar] [CrossRef] [Green Version]

- Jensen, Michael C. 1986. Agency costs of free cash flow, corporate finance, and takeovers. The American Economic Review 76: 323–29. [Google Scholar]

- Kandel, Eugene, and Neil D. Pearson. 1995. Differential interpretation of public signals and trade in speculative markets. Journal of Political Economy 103: 831–72. [Google Scholar] [CrossRef]

- Kluger, Brian D., and Norman G. Miller. 1990. Measuring residential real estate liquidity. Real Estate Economics 18: 145–59. [Google Scholar] [CrossRef]

- Kyle, Albert S. 1985. Continuous auctions and insider trading. Econometrica: Journal of the Econometric Society 53: 1315–35. [Google Scholar] [CrossRef] [Green Version]

- Kyriakou, Maria I., Athanasios Koulakiotis, Apostolos Kiohos, and Vassilios Babalos. 2021. Fractional Integration and Volatility Transmission Between Real Estate and Stock Markets: Novel Evidence from a FIGARCH-BEKK Approach. The Journal of Real Estate Finance and Economics. [Google Scholar] [CrossRef]

- Lin, Yu Cheng, Chyi Lin Lee, and Graeme Newell. 2019. The significance of residential REITs in Japan as an institutionalised property sector. Journal of Property Investment & Finance 37: 363–79. [Google Scholar]

- Mancini, Loriano, Angelo Ranaldo, and Jan Wrampelmeyer. 2013. Liquidity in the foreign exchange market: Measurement, commonality, and risk premiums. Journal of Finance 68: 1805–41. [Google Scholar] [CrossRef] [Green Version]

- Marshall, John M. 1974. Private incentives and public information. The American Economic Review 64: 373–90. [Google Scholar]

- Marzuki, Muhammad Jufri, and Graeme Newell. 2018. The emergence of Spanish REITs. Journal of Property Investment & Finance 36: 495–508. [Google Scholar]

- Merton, Robert C. 1987. A Simple Model of Capital Market Equilibrium with Incomplete Information. Journal of Finance 42: 483–510. [Google Scholar] [CrossRef]

- Milgrom, Paul, and Nancy Stokey. 1982. Information, trade and common knowledge. Journal of Economic Theory 26: 17–27. [Google Scholar] [CrossRef] [Green Version]

- Nelling, Edward, and Joseph Gyourko. 1998. The predictability of equity REIT returns. Journal of Real Estate Research 16: 251–68. [Google Scholar] [CrossRef]

- Newell, Graeme, and Muhammad Jufri Marzuki. 2018. The emergence and performance of German REITs. Journal of Property Investment & Finance 36: 91–103. [Google Scholar]

- Newell, Graeme, Alastair Adair, and Thi Kim Nguyen. 2013. The significance and performance of French REITs (SIICs) in a mixed-asset portfolio. Journal of Property Investment & Finance 31: 575–88. [Google Scholar]

- Östberg, Per, and Thomas Richter. 2018. The Sovereign Debt Crisis: Rebalancing or Freezes? Swiss Finance Institute Research Paper, No. 17-32. Available online: https://papers.ssrn.com/sol3/papers.cfm?abstract_id=3060504 (accessed on 22 August 2022).

- Parker, David. 2014. Property investment decision making by Australian REITs. Journal of Property Investment & Finance 32: 456–73. [Google Scholar]

- Petersen, Mitchell A. 2009. Estimating standard errors in finance panel data sets: Comparing approaches. The Review of Financial Studies 22: 435–80. [Google Scholar] [CrossRef] [Green Version]

- Richter, Thomas. 2022. Liquidity commonality in sovereign bond markets. International Review of Economics & Finance 78: 501–18. [Google Scholar]

- Schacht, Ulrich, and Jens Wimschulte. 2008. German property investment vehicles and the introduction of G-REITs: An analysis. Journal of Property Investment & Finance 26: 232–46. [Google Scholar]

- Subrahmanyam, Avanidhar. 1991. A theory of trading in stock index futures. The Review of Financial Studies 4: 17–51. [Google Scholar] [CrossRef]

- Van Dijk, Dorinth, Anne Kinsella Thompson, and David Geltner. 2020. Recent Drops in Market Liquidity May Foreshadow Major Drops in US Commerical Real Estate Markets. Available online: https://ssrn.com/abstract=3604606 (accessed on 21 June 2022).

- Wang, F. Albert. 1998. Strategic trading, asymmetric information, and heterogeneous prior beliefs. Journal of Financial Markets 1: 321–52. [Google Scholar] [CrossRef]

- Womack, Kent L. 1996. Do brokerage analysts’ recommendations have investment value? The Journal of Finance 51: 137–67. [Google Scholar] [CrossRef]

- Yat-Hung, Chiang, So Chun-Kei Joinkey, and Tang Bo-Sin. 2008. Time-varying performance of four Asia-Pacific REITs. Journal of Property Investment and Finance 26: 210–31. [Google Scholar] [CrossRef]

{kind=link}

{kind=link}

| Mean | Median | SD | Min | Max | |

|---|---|---|---|---|---|

| Variables for trading activity | |||||

| VOL | 0.6 | 0.29 | 0.92 | 0 | 36.1 |

| Variables for rebalancing and liquidity trading | |||||

| LMVL | 21.95 | 21.93 | 1.18 | 16.58 | 25.48 |

| TRE | 1.42 | 1.01 | 1.36 | 0.27 | 13.08 |

| PCL | 3.46 | 3.41 | 0.82 | 0.3 | 6.68 |

| BTM | 0.62 | 0.55 | 0.34 | 0.14 | 1.39 |

| Variables for differences in beliefs and information-based trading | |||||

| BET | 0.86 | 0.81 | 0.38 | 0.33 | 1.67 |

| NAN | 1.9 | 1.95 | 0.6 | 0 | 3.43 |

| LEV | 0.58 | 0.56 | 0.17 | 0 | 0.89 |

| SUP | 0 | 0.01 | 0.27 | −0.71 | 0.58 |

| EVO | 0.21 | 0.11 | 0.25 | 0.02 | 0.99 |

| USD Volume (VOL) | ||||

|---|---|---|---|---|

| (1) | (2) | (3) | (4) | |

| LMVL | 0.248 *** | 0.354 *** | 0.438 *** | 0.434 *** |

| (0.059) | (0.048) | (0.044) | (0.044) | |

| TRE | 0.087 *** | 0.102 *** | 0.121 *** | 0.103 *** |

| (0.027) | (0.02) | (0.033) | (0.021) | |

| PCL | 0.417 *** | 0.332 *** | 0.196 *** | 0.195 *** |

| (0.104) | (0.092) | (0.051) | (0.05) | |

| BTM | 0.234 ** | 0.297 *** | 0.245 *** | 0.280 *** |

| (0.096) | (0.098) | (0.072) | (0.073) | |

| BET | −0.05 | −0.005 | −0.108 | −0.012 |

| (0.059) | (0.049) | (0.078) | (0.053) | |

| NAN | −0.039 | 0.054 | 0.103 *** | 0.117 *** |

| (0.048) | (0.042) | (0.039) | (0.036) | |

| LEV | 0.107 | 0.153 | 0.442 * | 0.435 * |

| (0.233) | (0.246) | (0.235) | (0.23) | |

| SUP | −0.024 | −0.018 | 0.023 | 0.024 |

| (0.022) | (0.026) | (0.03) | (0.031) | |

| EVO | 0.077 | 0.137 * | 0.045 | 0.047 |

| (0.079) | (0.079) | (0.088) | (0.085) | |

| Time Fixed Effects | Yes | No | Yes | No |

| Firm Fixed Effects | Yes | Yes | No | No |

| N | 14,781 | 14,781 | 14,781 | 14,781 |

| Trading Motive | Proxy | Relation with Volume | Explanation | REIT Specialness | |

|---|---|---|---|---|---|

| Prediction | Actual | ||||

| Portfolio Rebalancing Price changes passively change portfolio allocations leading to a desire to rebalance. | Absolute total return TRE | + | + | The higher the price changes the more trading activity (to offset the passive changes in the portfolio allocation). | These trading motives are expected to also play an important role for REIT trading |

| Liquidity Trading-Stock Visibility Liquidity needs are realized mainly in highly visible stocks. | Price level (log) PCL | +/- | + | High priced stocks have lower transaction costs and are favored by mutual funds and thus experience more trading. | |

| Book-to-market-ratio BTM | - | + | Growth stocks receive more attention and are therefore traded more frequently. | ||

| Market value (log) LMVL | + | + | Large stocks (high market capitalization) are more visible and thus more frequently traded. | ||

| Private Information: Superior information leads to trade | Analyst Coverage NAN | + | is | The more Analyst follow a stock the more production of private information happens and the more frequently a stock is traded | REITs are very transparent and therefore the value of private information is low |

| Beta BET | is | low information or high estimation uncertainty securities have higher betas. | |||

| Differences in beliefs: Difference in beliefs lead to disagreement about prices and thus trade. | LEV | + | is | Enhanced risk is associated with more uncertain projects and are thus more likely to be traded by disagreeing investors | REITs have very stable cash flows and transparent benchmarks which limits the disagreement among market participants |

| SUP | + | is | Stocks with higher earnings surprises are more likely to be traded by disagreeing investors | ||

| EVO | + | is | Stocks with higher earnings volatility are more likely to be traded by disagreeing investors. | ||

| USD Volume (VOL) | |||

|---|---|---|---|

| (1) | (2) | (3) | |

| BETC | −0.115 | −0.122 | |

| (0.13) | (0.133) | ||

| NANC | 0.432 *** | 0.395 ** | |

| (0.163) | (0.16) | ||

| LEVC | 0.144 | 0.192 | |

| (0.355) | (0.352) | ||

| SUPC | −0.106 | −0.097 | |

| (0.097) | (0.098) | ||

| EVOC | 0.146 | 0.199 | |

| (0.141) | (0.141) | ||

| BETG | −0.032 | −0.054 | |

| (0.15) | (0.15) | ||

| NANG | −0.199 *** | −0.176 *** | |

| (0.061) | (0.059) | ||

| LEVG | 0.280 * | 0.288 * | |

| (0.161) | (0.154) | ||

| SUPG | 0.066 | 0.048 | |

| (0.042) | (0.044) | ||

| EVOG | 0.122 | 0.154 | |

| (0.104) | (0.11) | ||

| N | 14,781 | 14,781 | 14,781 |

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2022 by the author. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Richter, T. Trading Activity in Public Real Estate Markets. J. Risk Financial Manag. 2022, 15, 374. https://doi.org/10.3390/jrfm15090374

Richter T. Trading Activity in Public Real Estate Markets. Journal of Risk and Financial Management. 2022; 15(9):374. https://doi.org/10.3390/jrfm15090374

Chicago/Turabian StyleRichter, Thomas. 2022. "Trading Activity in Public Real Estate Markets" Journal of Risk and Financial Management 15, no. 9: 374. https://doi.org/10.3390/jrfm15090374

APA StyleRichter, T. (2022). Trading Activity in Public Real Estate Markets. Journal of Risk and Financial Management, 15(9), 374. https://doi.org/10.3390/jrfm15090374