The Impacts of the Russia–Ukraine Invasion on Global Markets and Commodities: A Dynamic Connectedness among G7 and BRIC Markets

Abstract

:1. Introduction

2. Literature Review

Theoretical Review

3. Data and Methodology

4. Results and Discussion

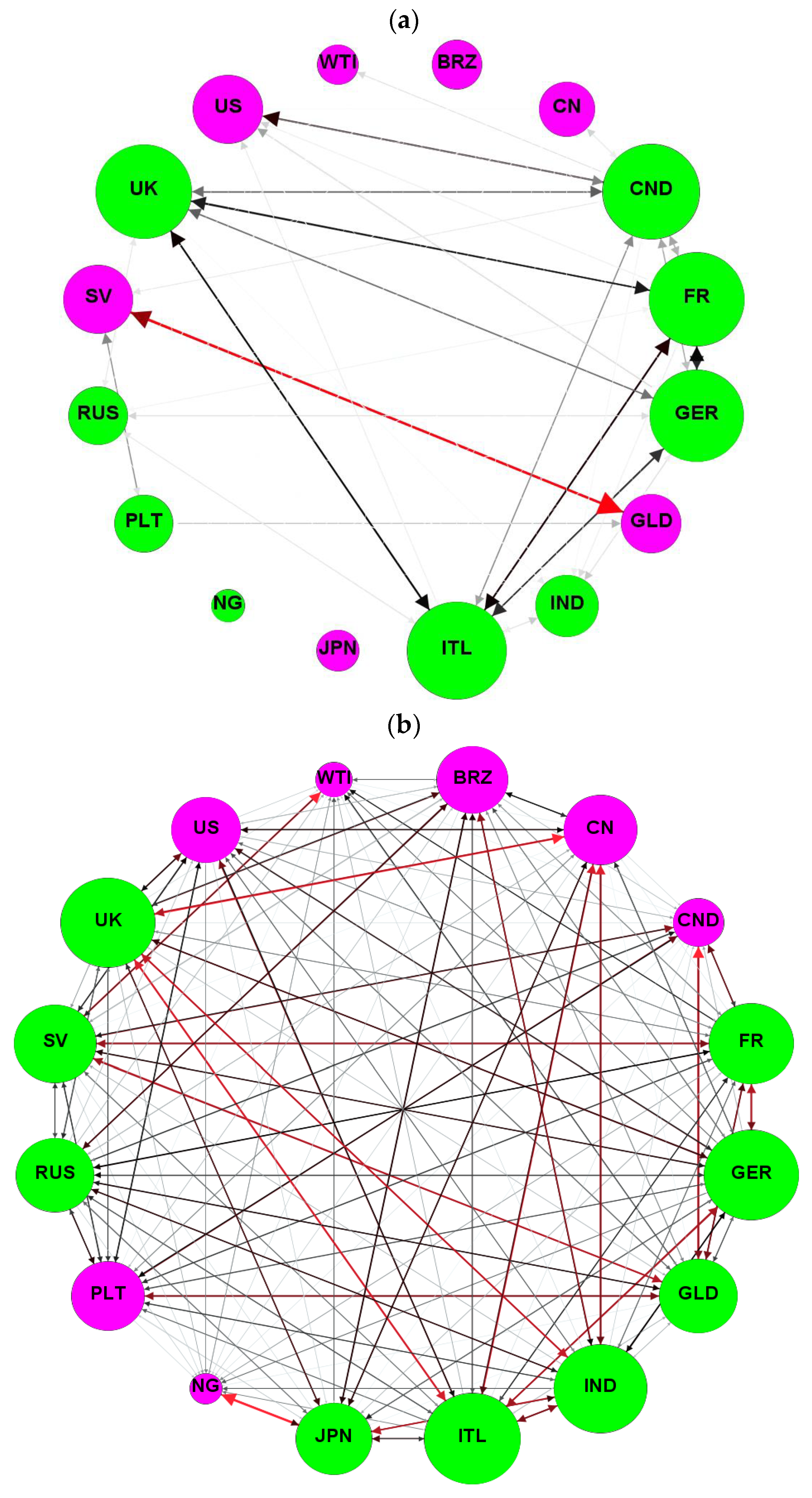

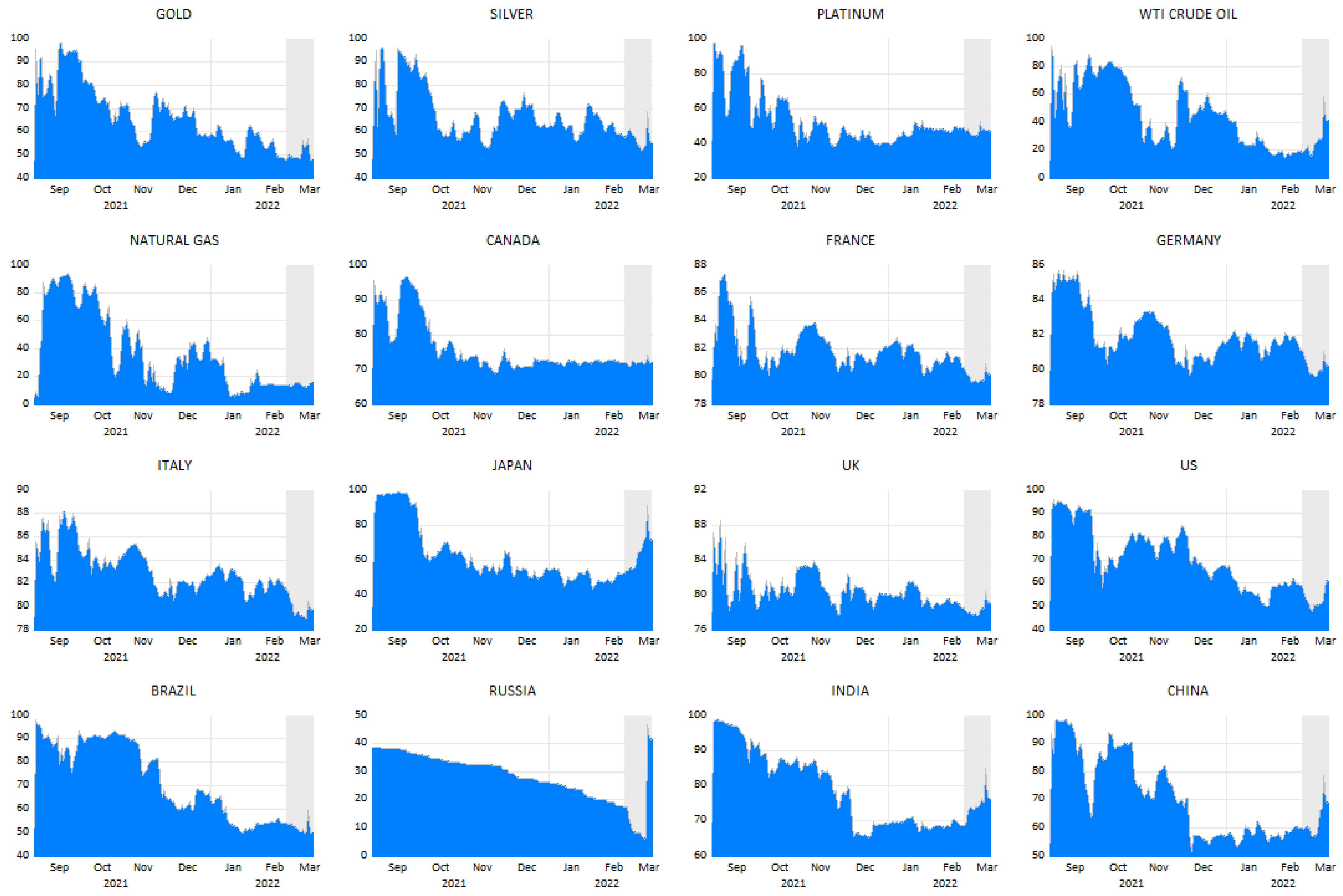

4.1. The Connectedness Network Spillovers

4.2. Averaged Total Returns Spillovers

4.3. Net Total, “To”, and “From” Return Spillovers

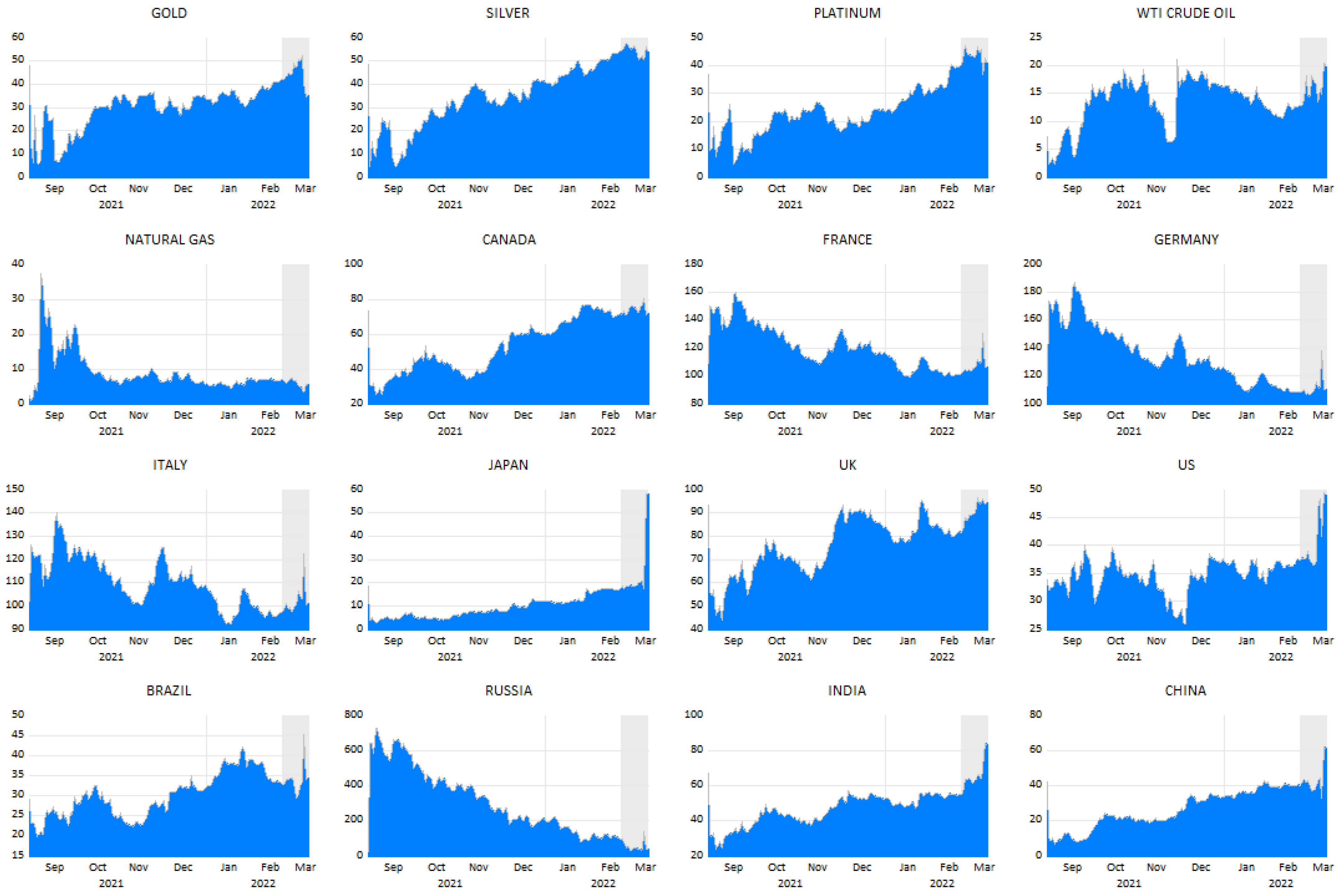

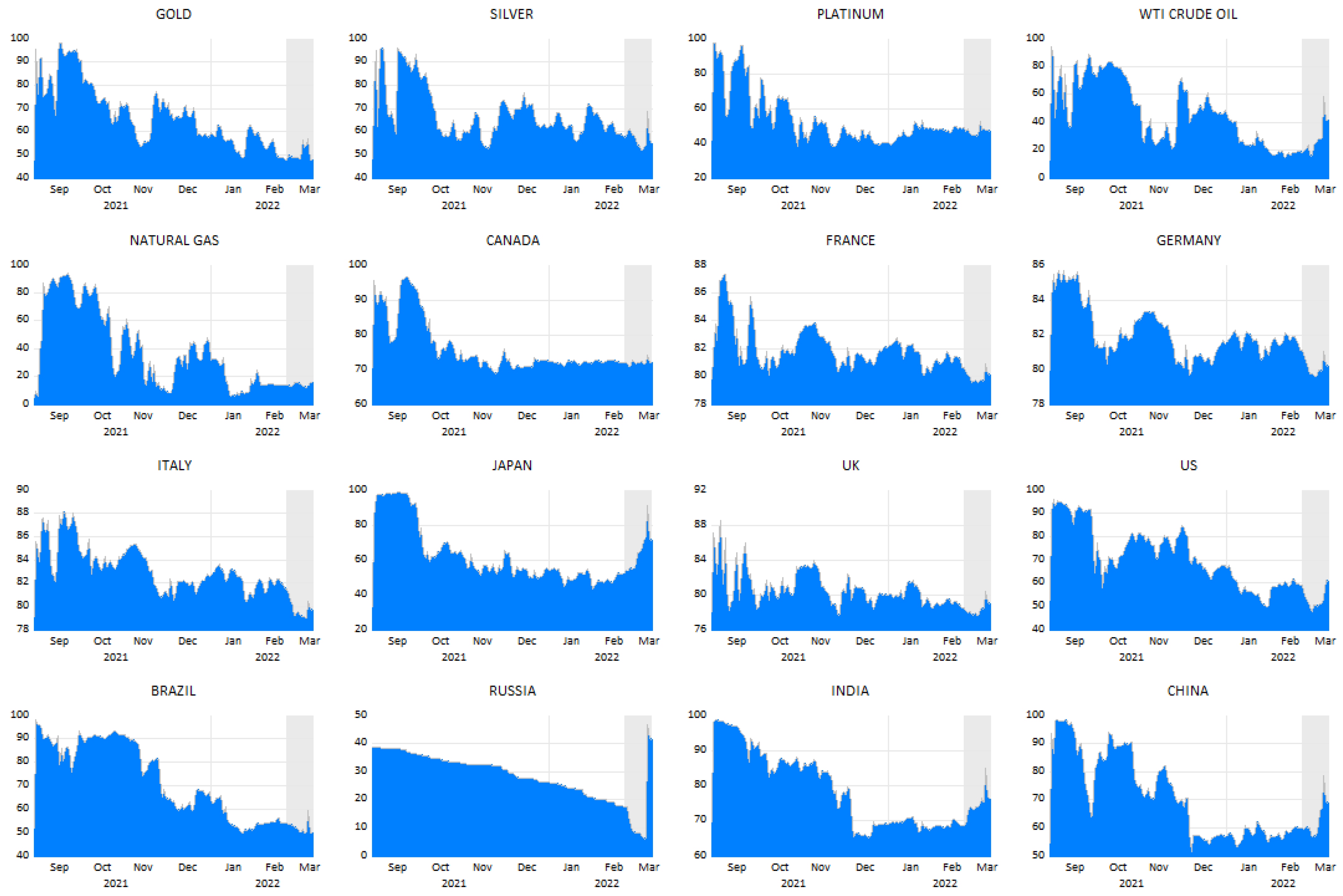

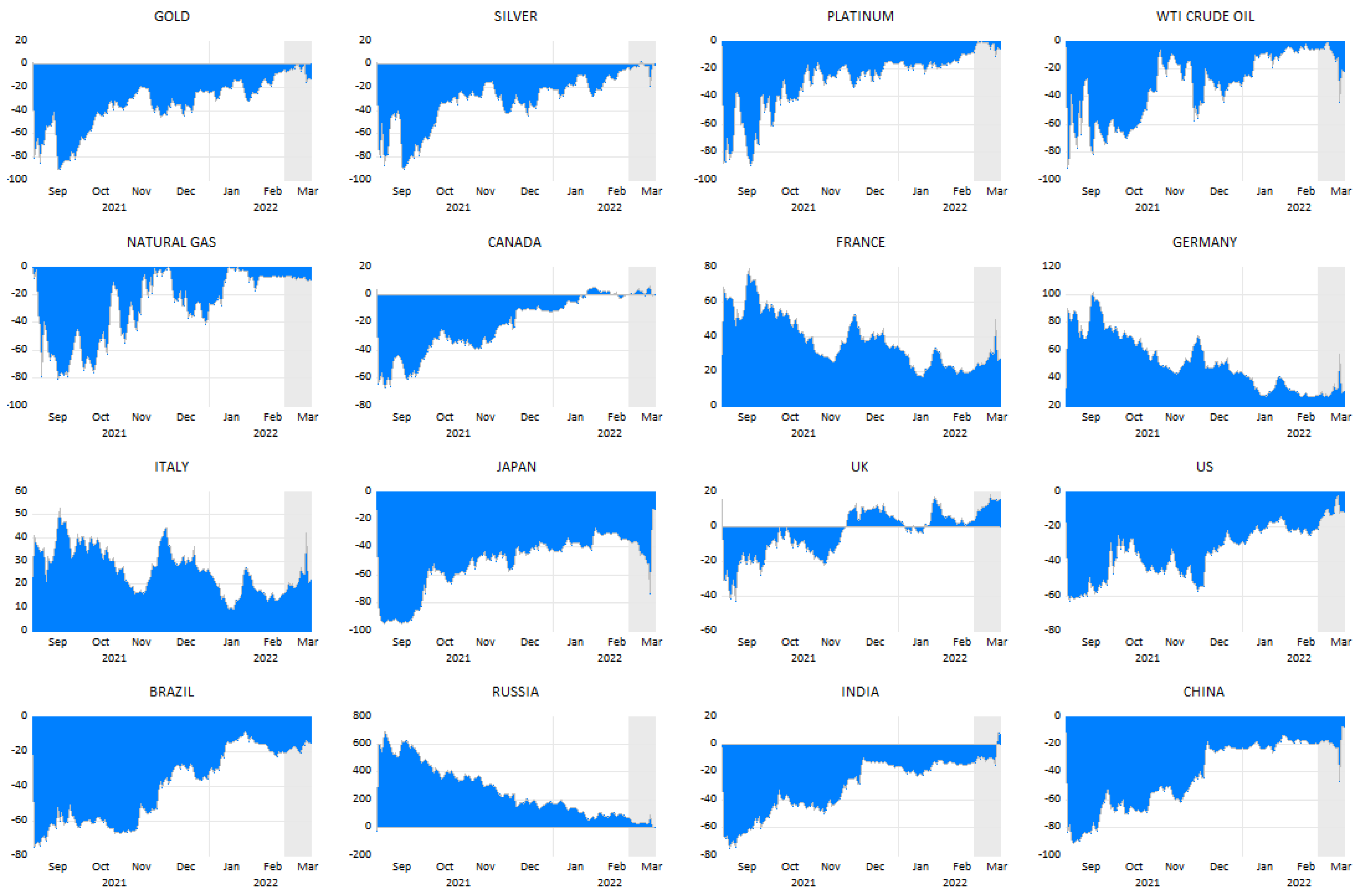

4.4. Robustness Checks

5. Conclusions, Policy Implications, and Limitations of the Study

Author Contributions

Funding

Institutional Review Board Statement

Informed Consent Statement

Data Availability Statement

Conflicts of Interest

References

- Abuzayed, Bana, EElie Bouri, Nedal Al-Fayoumi, and Naji Jalkh. 2021. Systemic risk spillover across global and country stock markets during the COVID-19 pandemic. Economic Analysis and Policy 71: 180–97. [Google Scholar] [CrossRef]

- Adams, Zeno, Roland Füss, and Felix Schindler. 2015. The sources of risk spillovers among US REITs: Financial characteristics and regional proximity. Real Estate Economics 43: 67–100. [Google Scholar] [CrossRef]

- Adekoya, Oluwasegun Babatunde, Johnson Ayobami Oliyide, OlaOluwa Simon Yaya, and Mamdouh Abdulaziz SalehAl-Faryan. 2022. Does oil connect differently with prominent assets during war? Analysis of intra-day data during the Russia-Ukraine saga. Resources Policy 77: 102728. [Google Scholar] [CrossRef]

- Antonakakis, Nikolaos, David Gabauer, Rangan Gupta, and Vasilios Plakandaras. 2018. Dynamic connectedness of uncertainty across developed economies: A time-varying approach. Economics Letters 166: 63–75. [Google Scholar] [CrossRef] [Green Version]

- Antonakakis, Nikolaos, Ioannis Chatziantoniou, and David Gabauer. 2020. Refined measures of dynamic connectedness based on time-varying parameter vector autoregressions. Journal of Risk and Financial Management 13: 23. [Google Scholar] [CrossRef]

- Aromi, Daniel, and Adam Clements. 2019. Spillovers between the oil sector and the S&P500: The impact of information flow about crude oil. Energy Economics 81: 187–96. [Google Scholar]

- Balcilar, Mehmet, David Gabauer, and Zaghum Umar. 2021. Crude oil future contracts and commodity markets: New evidence from a TVP-VAR extended joint connectedness approach. Resource Policy 73: 102219. [Google Scholar] [CrossRef]

- Balli, Faruk, Muhammad Abubakr Naeem, Syed Jawad Hussain Shahzad, and Anne de Bruin. 2019. Spillover network of commodity uncertainties. Energy Economics 81: 914–27. [Google Scholar] [CrossRef]

- Bedowska-Sojka, Barbara, Ender Demir, and Adam Zaremba. 2022. Hedging Geopolitical Risks with Different Asset Classes: A Focus on the Russian Invasion of Ukraine. Finance Research Letters 50: 103192. [Google Scholar] [CrossRef]

- Beitz, Charles R. 1979. Political Theory and International Relations. Cambridge: Cambridge University Press, vol. 13. [Google Scholar]

- Belyi, Andrei V. 2016. Limitations of resource determinism in international energy studies. Energy Research & Social Science 12: 1–4. [Google Scholar] [CrossRef]

- Berninger, Marc, Florian Kiesel, and Sascha Kolaric. 2022. Should I stay or should I go? Stock Market Reactions to Companies’ Decisions in the Wake of the Russia-Ukraine Conflict. April 20. Available online: https://papers.ssrn.com/sol3/papers.cfm?abstract_id=4088159 (accessed on 20 June 2022).

- Billah, Mabruk, Sitara Karim, Muhammad Abubakr Naeem, and Samuel Azhgaliyeva Vigne. 2021. Return and volatility spillovers between energy and BRIC markets: Evidence from quantile connectedness. Research in International Business and Finance 62: 101680. [Google Scholar] [CrossRef]

- Boubaker, Sabri, John William Goodell, Dharen Kumar Pandey, and Vineeta Kumari. 2022. Heterogeneous impacts of wars on global equity markets: Evidence from the invasion of Ukraine. Finance Research Letters 48: 102934. [Google Scholar] [CrossRef]

- Boungou, Whelsy, and Alhonita Yatié. 2022. The impact of the Ukraine–Russia war on world stock market returns. Economics Letters 215: 110516. [Google Scholar] [CrossRef]

- Bouri, Elie, Oguzhan Cepni, David Gabauer, and Rangan Gupta. 2021a. Return connectedness across asset classes around the COVID-19 outbreak. International Review of Financial Analysis 73: 101646. [Google Scholar] [CrossRef]

- Bouri, Elie, Xiaojie Lei, Naji Jalkh, Yahua Xu, and Hongwei Zhang. 2021b. Spillovers in higher moments and jumps across US stock and strategic commodity markets. Resources Policy 72: 102060. [Google Scholar] [CrossRef]

- Cepoi, Cosmin Octavian. 2020. Asymmetric dependence between stock market returns and news during COVID19 financial turmoil. Finance Research Letters 36: 101658. [Google Scholar] [CrossRef]

- Chatziantoniou, Ioannis, Christos Floros, and David Gabauer. 2022. Volatility Contagion Between Crude Oil and G7 Stock Markets in the Light of Trade Wars and COVID-19: A TVP-VAR Extended Joint Connectedness Approach. In Applications in Energy Finance. Cham: Palgrave Macmillan, pp. 145–68. [Google Scholar]

- Colgan, Jeff D. 2013. Fueling the fire: Pathways from oil to war. International Security 38: 147–80. [Google Scholar] [CrossRef]

- Costola, Michele, and Marco Lorusso. 2022. Spillovers among energy commodities and the Russian stock market. Journal of Commodity Markets, 100249. [Google Scholar] [CrossRef]

- Davidson, William H. 1980. The location of foreign direct investment activity: Country characteristics and experience effects. Journal of International Business Studies 11: 9–22. [Google Scholar] [CrossRef]

- Deng, Ming, Markus Leippold, Akexander F. Wagner, and Qian Wang. 2022. Stock Prices and the Russia-Ukraine War: Sanctions, Energy and ESG(April 2022). CEPR Discussion Paper No. DP17207. Available online: https://ssrn.com/abstract=4121382 (accessed on 20 June 2022).

- Dickey, David A., and Wayne A. Fuller. 1979. Distribution of the Estimators for Autoregressive Time Series With a Unit Root. Journal of the American Statistical Association 74: 427. [Google Scholar] [CrossRef]

- Diebold, Francis X., and Kamil Yilmaz. 2009. Measuring financial asset return and volatility spillovers, with application to global equity markets. The Economic Journal 119: 158–71. [Google Scholar] [CrossRef] [Green Version]

- Diebold, Francis X., and Kamil Yilmaz. 2012. Better to give than to receive: Predictive directional measurement of volatility spillovers. International Journal of Forecasting 28: 57–66. [Google Scholar] [CrossRef] [Green Version]

- Diebold, Francis X., and Kamil Yilmaz. 2014. On the network topology of variance decompositions: Measuring the connectedness of financial firms. Journal of Econometrics 182: 119–34. [Google Scholar] [CrossRef] [Green Version]

- Dimitriou, Dimitrios, Dimitris Kenourgios, and Theodore Simos. 2013. Global financial crisis and emerging stock market contagion: A multivariate FIAPARCH–DCC approach. International Review of Financial Analysis 30: 46–56. [Google Scholar] [CrossRef]

- Dodd, Olga, Adrian Fernandez-Perez, and Simon Sosvilla-Rivero. 2022. Currency and commodity return relationship under extreme geopolitical risks: Evidence from the invasion of Ukraine. Available online: https://papers.ssrn.com/sol3/papers.cfm?abstract_id=4089030 (accessed on 20 June 2022).

- European Central Bank. 2022. Economic, Financial and Monetary Developments. Economic Bulletin Issue 2. Available online: https://www.ecb.europa.eu/pub/economic-bullein/html/eb202202.en.html (accessed on 8 April 2022).

- Federle, Jonathan, Andre Meier, Gernot J. Müller, and Victor Sehn. 2022. Proximity to War: The stock market response to the Russian invasion of Ukraine. Available online: https://papers.ssrn.com/sol3/papers.cfm?abstract_id=4121360 (accessed on 20 June 2022).

- Gabauer, David, and Rangan Gupta. 2018. On the transmission mechanism of country-specific and international economic uncertainty spillovers: Evidence from a TVP-VAR connectedness decomposition approach. Economics Letters 171: 63–71. [Google Scholar] [CrossRef] [Green Version]

- Huynh, Toan Luu Duc, Erik Hille, and Muhammad Ali Nasir. 2020. Diversification in the Age of the 4th Industrial Revolution: The Role of Artificial Intelligence, Green Bonds and Cryptocurrencies. Technological Forecasting and Social Change 159: 120188. [Google Scholar] [CrossRef]

- Iqbal, Badar Alam. 2021. BRICS as a Driver of Global Economic Growth and Development. Global Journal of Emerging Market Economies 14: 7–8. [Google Scholar] [CrossRef]

- Iqbal, Najaf, Elie Bouri, Oksana Grebinevych, and David Roubaud. 2022. Modelling extreme risk spillovers in the commodity markets around crisis periods including COVID19. Annals of Operations Research, 1–30. [Google Scholar] [CrossRef]

- Jiang, Yonghong, Gengyu Tian, and Bin Mo. 2020. Spillover and quantile linkage between oil price shocks and stock returns: New evidence from G7 countries. Financial Innovation 6: 1–26. [Google Scholar] [CrossRef]

- Koop, Gary, and Dimitris Korobilis. 2014. A new index of financial conditions. European Economic Review 71: 101–16. [Google Scholar] [CrossRef] [Green Version]

- Koop, Gary, Mohammad Hashem Pesaran, and Simon M. Potter. 1996. Impulse response analysis in nonlinear multivariate models. Journal of Econometrics 74: 119–47. [Google Scholar] [CrossRef]

- Korobilis, Dimitris, and Kamil Yilmaz. 2018. Measuring Dynamic Connectedness with Large Bayesian VAR Models. Available online: https://papers.ssrn.com/sol3/papers.cfm?abstract_id=3099725 (accessed on 20 June 2022).

- Lee, Yusin. 2017. Interdependence, issue importance, and the 2009 Russia-Ukraine gas conflict. Energy Policy 102: 199–209. [Google Scholar] [CrossRef]

- Liadze, Iana, Corrado Macchiarelli, Paul Mortimer-Lee, and Patricia Sanchez Juanino. 2022. The Economic Costs of the Russia-Ukraine Conflict. Available online: https://www.niesr.ac.uk/wp-content/uploads/2022/03/PP32-Economic-Costs-Russia-Ukraine.pdf (accessed on 2 March 2022).

- Lin, Boqiang, and Tong Su. 2020. Mapping the oil price-stock market nexus research: A scientometric review. International Review of Economics and Finance 67: 133–47. [Google Scholar] [CrossRef]

- Mazur, Mieszko, Man Dang, and Miguel Vega. 2020. COVID-19 and the march 2020 stock market crash. Evidence from S&P1500. Finance Research Letters 38: 101690. [Google Scholar] [PubMed]

- Mbah, Ruth Endam, and Divine Forcha Wasum. 2022. Russian-Ukraine 2022 War: A Review of the Economic Impact of Russian-Ukraine Crisis on the USA, UK, Canada, and Europe. Advances in Social Sciences Research Journal 9: 144–53. [Google Scholar] [CrossRef]

- Mensi, Walid, Imran Yousaf, Xuan Vinh Vo, and Sang Hoon Kang. 2022. Asymmetric spillover and network connectedness between gold, BRENT oil and EU subsector markets. Journal of International Financial Markets, Institutions and Money 76: 101487. [Google Scholar] [CrossRef]

- Mirzaei, A., M. Saad, and A. Emrouznejad. 2021. Bank Stock Performance During the COVID-19 Crisis: Does Efficiency Explain Why Islamic Banks Fared Relatively Better? Available online: https://link.springer.com/article/10.1007/s10479-022-04600-y (accessed on 20 June 2022).

- Mohamad, Azhar. 2022. Safe flight to which haven when Russia invades Ukraine? A 48-hour story. Economics Letters 216: 110558. [Google Scholar] [CrossRef]

- Mokni, Khaled, Mohammed Al-Shboul, and Ata Assaf. 2021. Economic policy uncertainty and dynamic spillover among precious metals under market conditions: Does COVID-19 have any effects? Resources Policy 74: 102238. [Google Scholar] [CrossRef]

- Naeem, Muhammad Abubakr, Linh Pham, Arunachalam Senthilkumar, and Sitara Karim. 2022. Oil shocks and BRIC markets: Evidence from extreme quantile approach. Energy Economics 108: 105932. [Google Scholar] [CrossRef]

- Orhan, Ebru. 2022. The Effects of the Russia-Ukraine War on Global Trade. Journal of International Trade, Logistics and Law 8: 141. [Google Scholar]

- Papathanasiou, Spyros, Dimitrios Vasiliou, Anastasios Magoutas, and Drosos Koutsokostas. 2021. Do hedge and merger arbitrage funds actually hedge? A time-varying volatility spillover approach. Finance Research Letters 44: 102088. [Google Scholar] [CrossRef]

- Peng, Qing, Fenghua Wen, and Xu Gong. 2021. Time-dependent intrinsic correlation analysis of crude oil and the US dollar based on CEEMDAN. International Journal of Finance and Economics 26: 834–48. [Google Scholar] [CrossRef]

- Pesaran, H. Hashem, and Yongcheol Shin. 1998. Generalized impulse response analysis in linear multivariate models. Economics Letters 58: 17–29. [Google Scholar] [CrossRef]

- Pfeffer, Jeffrey, and Gerald R. Salancik. 2003. The External Control of Organizations: A Resource Dependence Perspective. Stanford: Stanford University Press. [Google Scholar]

- Phillips, Peter, and Pierre Perron. 1988. Testing for a unit root in time series regression. Biometrika 75: 335–46. [Google Scholar] [CrossRef]

- Radulescu, Irina Gabriela, Mirela Panaita, and Catalin Voica. 2014. BRICS countries challenge to the world economy new trends. Procedia Economics and Finance 8: 605–13. [Google Scholar] [CrossRef] [Green Version]

- Reuveny, Rafael, and Katherine Barbieri. 2014. On the effect of natural resources on interstate war. Progress in Physical Geography 38: 786–806. [Google Scholar] [CrossRef]

- Saâdaoui, Foued Saâdaoui, Sami Ben Jabeur, and John W. Goodell. 2022. Causality of geopolitical risk on food prices: Considering the Russo–Ukrainian conflict. Finance Research Letters 49: 103103. [Google Scholar] [CrossRef]

- Sauvant, Karl P. 2005. New sources of FDI: The BRICs-outward FDI from Brazil, Russia, India and China. Journal World Investment & Trade 6: 639. [Google Scholar]

- Schiffling, S., and N. Valantasis Kanellos. 2022. Five Essential Commodities That Will Be Hit by War in Ukraine. The Conversation. Available online: https://researchonline.ljmu.ac.uk/id/eprint/16422/1/Five%20essential%20commodities%20that%20will%20be%20hit%20by%20war%20in%20Ukraine.pdf (accessed on 20 June 2022).

- Selznick, Philip. 1949. TVA and the Grass Roots: A Study of Politics and Organization. Berkley: University of California Press, vol. 3. [Google Scholar]

- Sharif, Arshian, Chaker Aloui, and Yarovaya Larisa. 2020. COVID-19 pandemic, oil prices, stock market, geopolitical risk and policy uncertainty nexus in the US economy: Fresh evidence from the wavelet-based approach. International Review of Financial Analysis 70: 101496. [Google Scholar] [CrossRef]

- Shahzad, Syed Jawad Hussain, Elie Bouri, David Roubaud, Ladislav Kristoufek, and Brian Lucey. 2019. Is Bitcoin a better safe-haven investment than gold and commodities? International Review of Financial Analysis 63: 322–30. [Google Scholar] [CrossRef]

- Sher, Leo. 2020. The impact of the COVID-19 pandemic on suicide rates. QJM: An International Journal of Medicine 113: 707–12. [Google Scholar] [CrossRef] [PubMed]

- Siddiqui, Kalim. 2016. Will the growth of the BRICs cause a shift in the global balance of economic power in the 21st century? International Journal of Political Economy 45: 315–38. [Google Scholar] [CrossRef]

- Singhania, Monika, and Neha Saini. 2018. Determinants of FPI in developed and developing countries. Global Business Review 19: 187–213. [Google Scholar] [CrossRef]

- Sprout, Harold, and Margaret Sprout. 1957. Environmental factors in the study of international politics. Journal of Conflict Resolution 1: 309–28. [Google Scholar] [CrossRef]

- Stulberg, Adam N. 2017. Natural gas and the Russia-Ukraine crisis: Strategic restraint and the emerging Europe-Eurasia gas network. Energy Research & Social Science 24: 71–85. [Google Scholar] [CrossRef]

- Tosun, Onur Kemal, and Arman Eshraghi. 2022. Corporate decisions in times of war: Evidence from the Russia-Ukraine Conflict. Finance Research Letters 48: 102920. [Google Scholar] [CrossRef]

- Umar, Zaghum, Mariya Gubareva, and Tamara Teplova. 2021. The impact of Covid-19 on commodity markets volatility: Analyzing time-frequency relations between commodity prices and coronavirus panic levels. Resources Policy 73: 102164. [Google Scholar] [CrossRef]

- Umar, Zaghum, Ahmed Bossman, Sun-Yong Choi, and Tamara Teplova. 2022a. Does geopolitical risk matter for global asset returns? Evidence from quantile-on-quantile regression. Finance Research Letters 48: 102991. [Google Scholar] [CrossRef]

- Umar, Zaghum, Onur Polat, Sun-Yong Choi, and Tamara Teplova. 2022b. The impact of the Russia-Ukraine conflict on the connectedness of financial markets. Finance Research Letters 48: 102976. [Google Scholar] [CrossRef]

- Van Bergeijk, Peter. 1995. The impact of economic sanctions in the 1990s. The World Economy 18: 443–55. [Google Scholar] [CrossRef]

- Van de Graaf, Thijs, and Jeff D. Colgan. 2017. Russian gas games or well-oiled conflict? Energy security and the 2014 Ukraine crisis. Energy Research & Social Science 24: 59–64. [Google Scholar] [CrossRef] [Green Version]

- Waheeduzzaman, A. N. M. 2011. Competitiveness and convergence in G7 and emerging markets. Competitiveness Review: An International Business Journal 21: 110–28. [Google Scholar] [CrossRef]

- Wang, Yihan, Elie Bouri, Zeeshan Fareed, and Yuhui Dai. 2022. Geopolitical risk and the systemic risk in the commodity markets under the war in Ukraine. Finance Research Letters 49: 103066. [Google Scholar] [CrossRef]

- Wei, Hua, Syed Kumail Abbas Rizvi, Ferhana Ahmad, and Yuchen Zhang. 2020. Resource cursed or resource blessed? The role of investment and energy prices in G7 countries. Resources Policy 67: 101663. [Google Scholar] [CrossRef]

- Wen, Fenghua, Longhao Xu, Guangda Ouyang, and Gang Kou. 2019. Retail investor attention and stock price crash risk: Evidence from China. International Review of Financial Analysis 65: 101376. [Google Scholar] [CrossRef]

- Wen, Fenghua, Yujie Yuan, and Wei-Xing Zhou. 2020a. Cross-shareholding networks and stock price synchronicity: Evidence from China. International Journal of Finance & Economics 26: 914–48. [Google Scholar]

- Wen, Fenghua, Cui Li, Han Sha, and Liuguo Shao. 2020b. How does economic policy uncertainty affect corporate risk-taking? Evidence from China. Finance Research Letters 41: 101840. [Google Scholar] [CrossRef]

- World Bank. 2022. Global Growth to Slow through 2023, Adding to Risk of ‘Hard Landing’ in Developing Economies. Report. Available online: https://www.worldbank.org/en/news/press-release/2022/01/11/global-recovery-economics-debt-commodity-inequality (accessed on 20 June 2022).

- Yoon, Seong-Min, Md Al Mamun, Gazi Salah Uddin, and Sang Hoon Kang. 2019. Network connectedness and net spillover between financial and commodity markets. The North American Journal of Economics and Finance 48: 801–18. [Google Scholar] [CrossRef]

- Yousaf, Imran, Ritesh Patel, and Larisa Yarovaya. 2022. The Reaction of G20+ Stock Markets to the Russia-Ukraine Conflict ‘Black-Swan’ Event: Evidence from Event Study Approach. March 29. Available online: https://ssrn.com/abstract=4069555 (accessed on 20 June 2022).

- Zhang, Dayong, Min Hu, and Qiang Ji. 2020. Financial markets under the global pandemic of COVID-19. Finance Research Letters 36: 101528. [Google Scholar] [CrossRef]

- Zhang, Hua, Jinyu Chen, and Liuguo Shao. 2021. Dynamic spillovers between energy and stock markets and their implications in the context of COVID-19. International Review of Financial Analysis 77: 101828. [Google Scholar] [CrossRef]

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| Commodities and Stock Markets | Mean | Std. Dev. | Skewness | Kurtosis | JB | ADF | PP |

|---|---|---|---|---|---|---|---|

| Gold | 0.001 | 0.008 | −0.477 | 3.728 | 8.34 *** | −26.01 *** | −25.58 *** |

| Silver | 0.001 | 0.016 | −0.395 | 3.806 | 7.38 *** | −17.34 *** | −17.40 *** |

| Platinum | 0.001 | 0.017 | 0.323 | 3.685 | 5.13 *** | −16.04 *** | −16.06 *** |

| WTI Crude Oil | 0.004 | 0.023 | −0.685 | 8.375 | 178.17 *** | −19.66 *** | −19.72 *** |

| Natural Gas | 0.001 | 0.058 | 0.559 | 5.960 | 57.96 *** | −16.76 *** | −16.93 *** |

| Canada | 0.001 | 0.010 | −0.291 | 4.018 | 7.97 *** | −23.75 *** | −24.80 *** |

| France | −0.001 | 0.014 | −0.987 | 6.573 | 96.50 *** | −17.83 *** | −18.98 *** |

| Germany | −0.002 | 0.015 | −0.618 | 7.370 | 119.45 *** | −19.66 *** | −18.76 *** |

| Italy | −0.002 | 0.024 | −2.521 | 32.564 | 5209.36 *** | −25.55 *** | −24.57 *** |

| Japan | −0.001 | 0.011 | −0.325 | 3.326 | 3061.89 *** | −13.04 *** | −13.03 *** |

| UK | −0.002 | 0.024 | −5.770 | 58.843 | 18,832.04 *** | −15.27 *** | −16.18 *** |

| US | −0.001 | 0.011 | −0.258 | 3.168 | 1703.51 *** | −11.49 *** | −11.46 *** |

| Brazil | −0.001 | 0.017 | −0.308 | 3.173 | 2369.90 *** | −12.32 *** | −12.35 *** |

| Russia | −0.009 | 0.065 | −3.918 | 28.792 | 4208.21 *** | −18.93 *** | −18.65 *** |

| India | −0.001 | 0.016 | −2.902 | 20.200 | 1908.44 *** | −11.29 *** | −11.29 *** |

| China | −0.002 | 0.019 | −1.629 | 14.153 | 781.84 *** | −15.21 *** | −15.22 *** |

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2022 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Alam, M.K.; Tabash, M.I.; Billah, M.; Kumar, S.; Anagreh, S. The Impacts of the Russia–Ukraine Invasion on Global Markets and Commodities: A Dynamic Connectedness among G7 and BRIC Markets. J. Risk Financial Manag. 2022, 15, 352. https://doi.org/10.3390/jrfm15080352

Alam MK, Tabash MI, Billah M, Kumar S, Anagreh S. The Impacts of the Russia–Ukraine Invasion on Global Markets and Commodities: A Dynamic Connectedness among G7 and BRIC Markets. Journal of Risk and Financial Management. 2022; 15(8):352. https://doi.org/10.3390/jrfm15080352

Chicago/Turabian StyleAlam, Md. Kausar, Mosab I. Tabash, Mabruk Billah, Sanjeev Kumar, and Suhaib Anagreh. 2022. "The Impacts of the Russia–Ukraine Invasion on Global Markets and Commodities: A Dynamic Connectedness among G7 and BRIC Markets" Journal of Risk and Financial Management 15, no. 8: 352. https://doi.org/10.3390/jrfm15080352

APA StyleAlam, M. K., Tabash, M. I., Billah, M., Kumar, S., & Anagreh, S. (2022). The Impacts of the Russia–Ukraine Invasion on Global Markets and Commodities: A Dynamic Connectedness among G7 and BRIC Markets. Journal of Risk and Financial Management, 15(8), 352. https://doi.org/10.3390/jrfm15080352