The Impact of Vertical Theories of Harm on Investor Returns: An Event Study of US Vertical Mergers

Abstract

:1. Introduction

- Abnormal returns are lower for vertical relative to horizontal mergers, due to rivals gaining increased market power in horizontal mergers.

- Abnormal returns will be higher for targets in vertical mergers when antitrust concerns focus on exclusionary effects, such as input or customer foreclosure. In contrast, relative gains will be higher for acquirers when eliminating/forestalling competition or overall collusive effects are the primary vertical theory of harm.

2. Literature Review

2.1. Welfare Impacts of Vertical Mergers

2.2. Vertical Theory of Harm

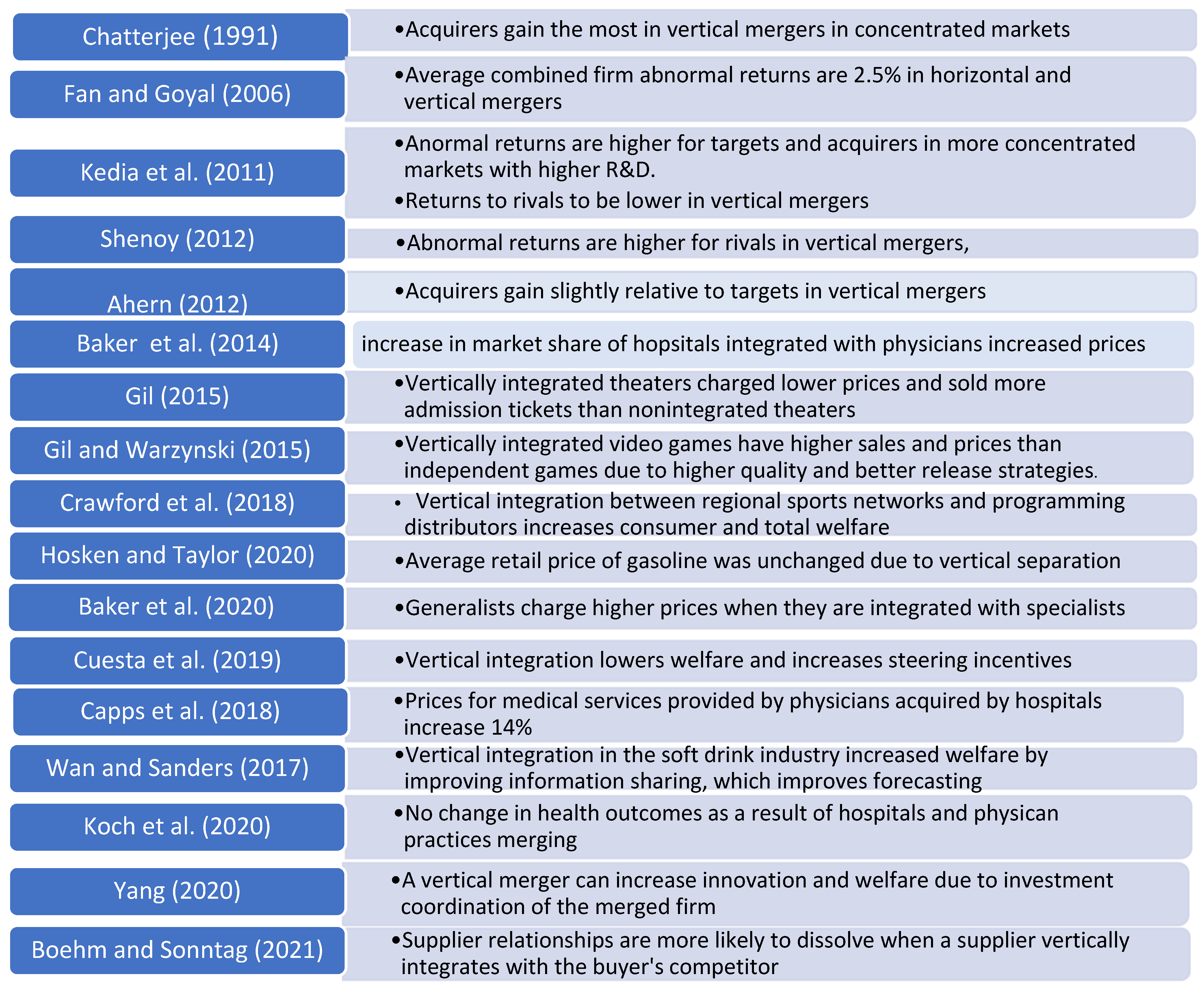

2.3. Empirical Studies Regarding Gains in Vertical Mergers

3. Materials and Methods

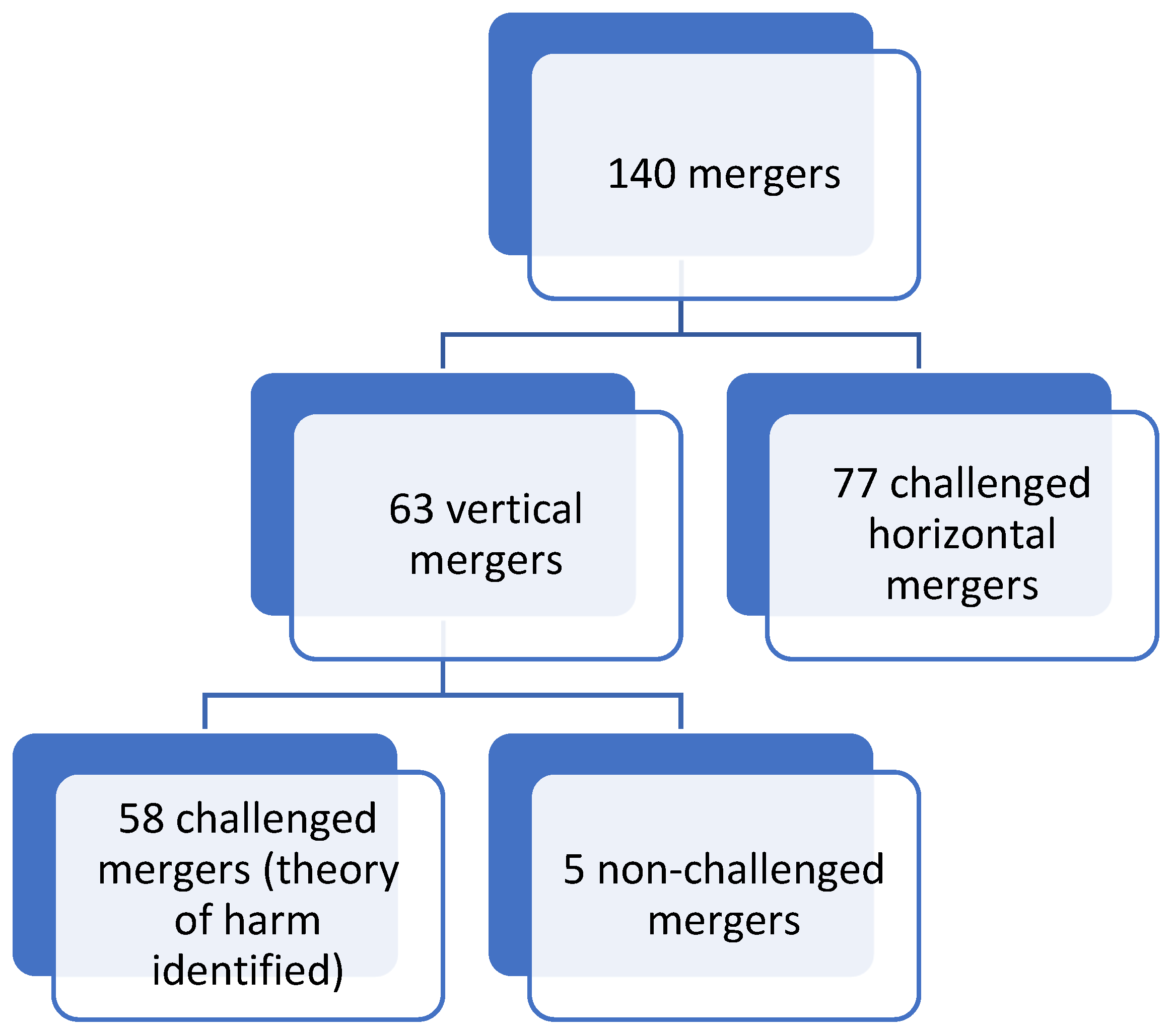

3.1. Data

3.2. Event Study Methodology

- -

- The event time corresponds to the day of the merger announcement.

- -

- The estimation window [ corresponds to the window [−150, −30], which is the period that spans from 150 days prior to the merger announcement to 30 days prior to the announcement date.

- -

- The event window is the window surrounding the event announcement date (0). We have (−1, +1) or (−2, +2) depending on the window of 1 or 2 days prior to the announcement and 1 or 2 days after the announcement.

3.3. Methodology

4. Results

4.1. Vertical Theory of Harm

4.2. Other Variables

5. Conclusions and Policy Suggestions

Author Contributions

Funding

Institutional Review Board Statement

Informed Consent Statement

Data Availability Statement

Acknowledgments

Conflicts of Interest

| 1 | See Gonzalez and Gallizo (2021), Panyagometh (2020) and Lee and Lu (2021) for event studies regarding the impact of COVID-19. |

| 2 | Industries include gasoline, healthcare, cable TV, movies, and others. |

| 3 | See Beck and Morton (2021) for numerous industry specific studies. |

| 4 | This discussion was taken from Salop and Culley (2016). |

| 5 | See note 4 above. |

| 6 | This discussion was taken from Sonenshine (2011). |

| 7 | The paper was written in 2016 with 46 vertical mergers taken from 1994–2013. The list of mergers was revised in 2018 to include an additional 12 mergers that occurred from 2014 through 2018. |

| 8 | In a number of cases multiple theories of harm were cited. |

| 9 | See Equation (4) and the discussion regarding how the weighted combined CARs were calculated. |

| 10 | |

| 11 | Figlewski et al. (2012) state that adding macroeconomic factors in their CAR model strongly increased the explanatory power of the model. The beginning of merger waves coincides with economic prosperity or economic recovery. Flannery and Protopapadakis (2002) state that inflation has a significant effect on market returns. They found a negative relationship between CPI and CARs. |

| 12 | lnRevenue refers to the acquirer revenue for the acquirer CARs and target revenue for the target CARs. We did not include both the acquirer and target or the revenue difference with the acquirer or target revenue in the regressions due to collinearity. |

| 13 | lnAsset_Intensity refers to the acquirer asset-intensity for the acquirer CARs and target asset-intensity for the target CARs. |

References

- Ahern, Kenneth. 2012. Bargaining Power and Industry Dependence in Mergers. Journal of Financial Economics 103: 530–50. [Google Scholar] [CrossRef]

- Baker, Lawrence, Kate Bundorf, and Daniel Kessler. 2014. Vertical integration: Hospital ownership of physician practices is associated with higher prices and spending. Health Affairs 33: 756–63. [Google Scholar] [CrossRef] [PubMed] [Green Version]

- Baker, Lawrence, Kate Bundorf, and Daniel Kessler. 2020. Does multispecialty practice enhance physician market power? American Journal of Health Economics 6: 324–47. [Google Scholar] [CrossRef] [Green Version]

- Beck, Marissa, and Fiona Scott Morton. 2021. Evaluating the Evidence on Vertical Mergers. Review of Industrial Organization 59: 273–302. [Google Scholar] [CrossRef]

- Boehm, Johannes, and Jan Sonntag. 2021. Vertical Integration and Foreclosure: Evidence from Production Network Data. Available online: https://jmboehm.github.io/foreclosure.pdf (accessed on 1 April 2022).

- Bork, Robert. 1978. Antitrust Paradox. New York: Basic Books. [Google Scholar]

- Capps, Cory, David Dranove, and Christopher Ody. 2018. The effect of Hopsital Acquisition Practices on Prices and Spending. Journal of Health Economics 59: 139–52. [Google Scholar] [CrossRef]

- Chandler, Alfred. 1962. The Strategy and Structure. Cambridge: MIT Press. [Google Scholar]

- Chatterjee, Sayan. 1991. Gains in vertical Acquisitions and Market Power: Theory and Evidence. Academy of Management Journal 34: 436–48. [Google Scholar]

- Chipty, Tasneen. 2001. Vertical Integration, Market Foreclosure, and Consumer Welfare in the Cable Television Industry. American Economic Review 91: 428–53. [Google Scholar] [CrossRef]

- Coase, Ronald. 1937. The Nature of the Firm. Economica 4: 386–405. [Google Scholar] [CrossRef]

- Cooper, James, Luke Froeb, Daniel O’Brien, and Michael Vita. 2005. Vertical antitrust policy as a problem of inference. International Journal of Industrial Organization 23: 639–64. [Google Scholar] [CrossRef]

- Crawford, Gregory, Robin Lee, Michael Whinston, and Ali Yurukoglu. 2018. The Welfare Effects of Vertical Integration in Multichannel Television Markets. Econometrica 86: 891–954. [Google Scholar] [CrossRef] [Green Version]

- Cuesta, Jose, Carlos Norton, and Benjamin Vatter. 2019. Vertical Integration between Hospitals and Insurers. Available online: https://drive.google.com/file/d/1_arGG1EUe0SvugLKwtDWbXu3ke87_CKH (accessed on 1 April 2022).

- Eckbo, Espen, and Peggy Wier. 1985. Antimerger policy under the Hart-Scott-Rodino Act: A reexamination of the market power hypothesis. Journal of Law and Economics 28: 119–49. [Google Scholar] [CrossRef]

- Fama, Eugene F., Lawrence Fisher, Michael C. Jensen, and Richard Roll. 1969. The Adjustment of Stock Prices to New Information. International Economic Review 10: 1–21. [Google Scholar] [CrossRef]

- Fan, Joseph, and Vidhan Goyal. 2006. On the Patterns of Wealth Effects of Vertical Mergers. Journal of Business 79: 877–902. [Google Scholar] [CrossRef] [Green Version]

- Fidrmuc, Jana, Peter Roosenboom, Richard Paap, and Tim Teunissen. 2012. One size does not fit all: Selling firms to private equity versus strategic acquirers. Journal of Corporate Finance 18: 828–48. [Google Scholar] [CrossRef]

- Figlewski, Stephen, Helena Frydman, and Weijian Liang. 2012. Modeling the effect of macroeconomic factors on corporate default and credit rating transitions. International Review of Economics and Finance 21: 87–105. [Google Scholar] [CrossRef]

- Flannery, Mark, and Aris Protopapadakis. 2002. Macroeconomic Factors do Influence Aggregate Stock Returns. The Review of Financial Studies 15: 751–82. [Google Scholar] [CrossRef]

- Gil, Ricard. 2015. Does vertical integration decrease prices? Evidence from the Paramount Antitrust case of 1948. American Economic Journal: Economic Policy 7: 162–91. [Google Scholar] [CrossRef]

- Gil, Ricard, and Frederic Warzynski. 2015. Vertical integration, exclusivity, and game sales performance in the US video game industry. The Journal of Law, Economics, and Organization 31: i143–i168. [Google Scholar]

- Gonzalez, Pedro, and Hose Luis Gallizo. 2021. Impact of COVID-19 on the Stock Market by Industrial Sector in Chile: An Adverse Overreaction. Journal of Risk Financial Management 14: 548. [Google Scholar] [CrossRef]

- Higgins, Mathew, and Daniel Rodriquez. 2006. The outsourcing of R&D through acquisitions in the pharmaceutical industry. Journal of Financial Economics 80: 351–83. [Google Scholar]

- Hosken, Daniel, and Christopher Taylor. 2020. Vertical Disintegration: The Effect of Refiner Exit from Gasoline Retailing on Retail Gasoline Pricing. Available online: https://ssrn.com/abstract=3664028 (accessed on 7 July 2022).

- Jurich, Stephen, and Mark Walker. 2019. What Drives Merger Outcomes? The North American Journal of Economics and Finance 48: 757–75. [Google Scholar] [CrossRef]

- Kedia, Simi, Abraham Ravid, and Vincent Pons. 2011. When Do Vertical Mergers Create Value? Financial Management 40: 845–77. [Google Scholar] [CrossRef]

- Koch, Thomas G., Brett W. Wendling, and Nathan E. Wilson. 2020. The effects of physician and hospital integration on Medicare beneficiaries health outcomes. Review of Economics and Statistics 103: 725–39. [Google Scholar] [CrossRef]

- Kwoka, John, and Chengyan Gu. 2015. Predicting Merger Outcomes: The Accuracy of Stock Market Event Studies, Market Structure Characteristics, and Agency Decisions. The Journal of Law & Economics 58: 519–43. [Google Scholar]

- Lafontaine, Francine, and Margaret Slade. 2007. Vertical Integration and Firm Boundaries: The Evidence. Journal of Economic Literature 45: 629–85. [Google Scholar] [CrossRef] [Green Version]

- Lee, Kuo-Jung, and Su-Lien Lu. 2021. The Impact of COVID-19 on the Stock Price of Socially Responsible Enterprises: An Empirical Study in Taiwan Stock Market. International Journal of Environmental Research Public Health 18: 1398. [Google Scholar] [CrossRef]

- Lubatkin, Michael. 1987. Merger Strategies and Stockholder Value. Strategic Management Journal 8: 39–53. [Google Scholar] [CrossRef]

- Luco, Fernando, and Guillermo Marshall. 2020. The competitive impact of vertical integration by multiproduct firms. American Economic Review 110: 2041–64. [Google Scholar] [CrossRef]

- MacKinlay, Craig. 1997. Event Studies in Economics and Finance. Journal of Economic Literature 35: 13–39. [Google Scholar]

- Masten, Scott. 1984. The organization of production: Evidence from the aerospace industry. Journal of Law and Economics 27: 403–17. [Google Scholar] [CrossRef]

- Panyagometh, Kamphol. 2020. The Effects of Pandemic Event on the Stock Exchange of Thailand. Economies 8: 90. [Google Scholar] [CrossRef]

- Perry, Martin, and Robert Groff. 1985. Resale Price Maintenance and Forward integration into a monopolistically competitive industry. Quarterly Journal of Economics 100: 1293–311. [Google Scholar] [CrossRef]

- Perry, Martin. 1989. Vertical integration. In Handbook of Industrial Organization. Edited by Richard Schmalensee and Robert Willig. Amsterdam: North Holland, pp. 185–255. [Google Scholar]

- Posner, Roger, and William Easterbrook. 1981. Antitrust. St. Paul: West Publishing. [Google Scholar]

- Riordan, Michael, and Oliver Williamson. 1985. Asset specificity and economic organization. International Journal of Industrial Organization 3: 365–78. [Google Scholar] [CrossRef]

- Salop, Steven, and Daniel Culley. 2016. Revising the Vertical Merger Guidelines: Policy Issues and an Interim Guide for Practitioners. Journal of Antitrust Enforcement 4: 1–41. [Google Scholar] [CrossRef] [Green Version]

- Shenoy, Jaideep. 2012. An Examination of the Efficiency, Foreclosure, and Collusion Rationales for Vertical Takeovers. Management Science 58: 1482–501. [Google Scholar] [CrossRef]

- Sokol, Daniel. 2018. Vertical Mergers and Entrepreneurial Exit. Florida Law Review 70: 1357. [Google Scholar]

- Sonenshine, Ralph. 2011. Effect of R&D and market concentration on merger outcomes—An event study of US horizontal mergers. International Journal of the Economics of Business 18: 419–39. [Google Scholar]

- Spiller, Pablo. 1985. On Vertical Mergers. Journal of Economics, Law, and Organization 1: 285–312. [Google Scholar]

- Walker, Gordon, and David Weber. 1987. Supplier competition, Uncertainty and make-or-buy Decisions. Academy of Management Journal 30: 589–96. [Google Scholar]

- Wan, Xiang, and Nadia Sanders. 2017. The negative impact of product variety: Forecast bias, inventory levels, and the role of vertical integration. International Journal of Production Economics 186: 123–31. [Google Scholar] [CrossRef]

- Williamson, Oliver. 1975. Markets and Hierarchies: Analysis and Antitrust Implications, A Study in the Economics of Internal Organization. New York: Free Press. [Google Scholar]

- Williamson, Oliver. 1985. The Economic Institutions of Capitalism. New York: The Free Press. [Google Scholar]

- Wong-Ervin, Koren. 2019. Antitrust Analysis of Vertical Mergers: Recent Developments and Economic Teachings. ABA Antitrust Source. Available online: https://ssrn.com/abstract=3273344 (accessed on 1 April 2022).

- Yang, Chenyu. 2020. Vertical structure and innovation: A study of the SoC and smartphone industries. The RAND Journal of Economics 51: 739–85. [Google Scholar] [CrossRef]

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| Vertical Theory of Harm | Number of Cases | Average Acquirer 3-Day CAR | Average Target 3-Day CAR | Weighted Combined 3-Day CAR9 |

|---|---|---|---|---|

| 1. Exclusionary effects | 51 | 0.9% | 10.8% | 5.3% |

| 1a. Foreclosure of inputs | 32 | 1.2% | 8.9% | 4.9% |

| 1b. Customer foreclosure | 12 | 0.01% | 12.5% | 11.1% |

| 1c. Misuse of competitors’ sensitive information | 22 | 2.1% | 12.1% | 7.5% |

| 2. Coordinated effects | 39 | 3.6% | 11.8% | 4.2% |

| 2a. Elimination of a disruptive buyer or other facilitating effects | 3 | 9.1% | 4.6% | 5.7% |

| 2b. Collusive information exchange | 39 | 3.5% | 11.8% | 4.1% |

| 3. Elimination of potential competition | 37 | 2.8% | 9.9% | 9.1% |

| 4. Unilateral effects | 115 | 3.5% | 9.9% | 3.6% |

| 5. Evasion of regulation | 2 | 4.2% | - | - |

| Average | 3.1% | 10.3% | 4.5% |

| CARs by Type | Mean Vertical | Mean Horizontal | All Mergers | T-Test |

|---|---|---|---|---|

| Target | ||||

| 3-day target CARs | 10.9% | 10.3% | 10.3% | 0.63 |

| 5-day target CARs | 11.5% | 11.7% | 11.5% | −0.04 |

| Acquirer | ||||

| 3-day acquirer CARs | 0.2% | 4.8% | 3.0% | 2.53 |

| 5-day acquirer CARs | 0.9% | 6.3% | 4.1% | 2.61 |

| Weighted combined | ||||

| 3-day combined CARs | 6.1% | 8.6% | 7.5% | 0.31 |

| 5-day combined CARs | 7.0% | 7.6% | 7.1% | 0.46 |

| Relative gains to the merger (target to total abnormal returns) | ||||

| 3-day event | 53.6% | 39.9% | 44.3% | −1.73 |

| 5-day event | 53.7% | 39.5% | 45.1% | −1.82 |

| Variable | Mean Vertical | Mean Horizontal | Total |

|---|---|---|---|

| R&D intensity | |||

| Acquirer | 4.2% | 7.0% | 6.3% |

| Target | 5.6% | 16.8% | 11.2% |

| Asset intensity | |||

| Acquirer | 50.0% | 41.6% | 23.3% |

| Target | 21.6% | 52.5% | 29.2% |

| Revenues | |||

| Acquirer | $27,732 | $22,956 | $24,880 |

| Target | $15,358 | $5477 | $9765 |

| Revenue difference | $12,541 | $17,478 | $15,150 |

| Financing | |||

| Cash | 54.2% | 48.1% | 51.1% |

| Stock | 37.6% | 45.8% | 41.9% |

| Inputfore | Custmis | Cust for | Collusive | Eliminate C | Disr Buy | Unilateral | Evasion | TargRev | ACQRev | R&Dinten | CPI | |

|---|---|---|---|---|---|---|---|---|---|---|---|---|

| Inputfore | 1.000 | |||||||||||

| Customermis | 0.272 | 1.000 | ||||||||||

| Customer_for | 0.300 | 0.244 | 1.000 | |||||||||

| Collusive | −0.243 | −0.019 | −0.117 | 1.000 | ||||||||

| EliminateC | 0.072 | 0.164 | −0.112 | 0.147 | 1.000 | |||||||

| Disr Buy | 0.018 | 0.193 | 0.121 | 0.114 | −0.082 | 1.000 | ||||||

| Unilateral E | 0.679 | −0.529 | −0.372 | 0.238 | 0.167 | −0.172 | 1.000 | |||||

| Evasion | −0.075 | −0.057 | −0.039 | −0.082 | −0.067 | 0.397 | −0.140 | 1.000 | ||||

| TargetRev | 0.248 | 0.176 | −0.037 | −0.035 | 0.004 | 0.147 | −0.182 | 0.125 | 1.000 | 1.000 | ||

| ACQrev | 0.061 | −0.051 | −0.057 | −0.023 | −0.085 | −0.034 | 0.067 | −0.051 | 0.361 | |||

| R&D-inten | 0.173 | −0.018 | 0.245 | −0.077 | −0.017 | −0.012 | −0.105 | −0.021 | −0.029 | −0.412 | 1.000 | |

| CPI | −0.074 | −0.07 | 0.031 | 0.042 | −0.012 | −0.013 | −0.012 | 0.058 | −0.284 | −0.129 | 0.120 | 1.000 |

| Variables | All Mergers (Abnormal Returns) | Vertical Mergers (Abnormal Returns) | Target to Total % Return | |||||

|---|---|---|---|---|---|---|---|---|

| Acquirer | Target | Combined | Acquirer | Target | Combined | All Mergers | Vertical | |

| Vertical theories of harm | ||||||||

| Misuse of customer sensitive information | (+) | (+) | (+) | (+) | ||||

| Eliminating a disruptive buyer | (−) | |||||||

| Eliminate competition | (+) | (−) | ||||||

| Unilateral | (−) | (−) | (−) | |||||

| Collusive effects | (−) | |||||||

| Input foreclosure | (+) | (+) | ||||||

| Evasion of regulation | (−) | |||||||

| Other variables | ||||||||

| Vertical | (−) | |||||||

| Acquirer revenue | (+) | |||||||

| Target revenue | (−) | (+) | (−) | |||||

| Revenue difference | (−) | |||||||

| R&D intensity | (+) | (+) | ||||||

| Asset intensity | (+) | (−) | ||||||

| Stock financing | (−) | (−) | ||||||

| Variables | 3-Day CAR (Acquirer) | 3-Day CAR (Target) | 3-Day CAR (Combined) | 5-Day CAR (Acquirer) | 5-Day CAR (Target) | 5-Day CAR (Combined) |

|---|---|---|---|---|---|---|

| Exclusionary | ||||||

| Input foreclosure | −0.03 | 0.00 | 0.04 | −0.03 | −0.03 | 0.08 |

| (0.02) | (0.03) | (0.11) | (0.03) | (0.03) | (0.13) | |

| Customer misuse of | 0.00 | 0.04 | 0.17 | 0.01 | 0.066 ** | 0.10 |

| information | (0.02) | (0.03) | (0.11) | (0.03) | (0.03) | (0.16) |

| Customer forclosure | 0.01 | 0.01 | 0.03 | 0.03 | 0.00 | 0.15 |

| (0.02) | (0.03) | (0.10) | (0.03) | (0.03) | (0.15) | |

| Coordinated | ||||||

| Disruptive buyer | −0.051 ** | 0.03 | −0.15 | −0.068 ** | 0.01 | 0.06 |

| (0.03) | (0.05) | (0.26) | (0.03) | (0.04) | (0.16) | |

| Collusive | 0.00 | 0.03 | −0.01 | 0.01 | 0.00 | −0.01 |

| (0.02) | (0.03) | (0.08) | (0.02) | (0.03) | (0.11) | |

| Unilateral | 0.02 | −0.05 | −0.18 | 0.00 | −0.0641 * | −0.31 * |

| (0.02) | (0.04) | (0.13) | (0.03) | (0.04) | (0.15) | |

| Eliminate compet. | −0.01 | −0.03 | 0.11 | −0.02 | −0.01 | −0.07 |

| (0.02) | (0.02) | (0.10) | (0.02) | (0.03) | (0.09) | |

| Evasion | −0.04 | −0.071 * | −0.10 | |||

| (0.03) | (0.04) | (0.12) | ||||

| Vertical | 0.00 | −0.04 | −0.09 | −0.02 | −0.04 | −0.289 ** |

| (0.03) | (0.03) | (0.14) | (0.04) | (0.04) | (0.12) | |

| lnRevenue | 0.01 ** | 0.00 | 0.02 *** | 0.00 | ||

| (0.005) | (0.01) | (0.01) | (0.01) | |||

| lnRevenue diff. | −0.03 * | −0.014 | ||||

| (0.015) | (0.013) | |||||

| lnAsset intensity | 0.004 ** | 0.00 | −0.01 | 0.004 * | 0.00 | 0.00 |

| (0.002) | (0.00) | (0.01) | (0.002) | (0.00) | (0.01) | |

| Cash | 0.02 | 0.01 | 0.09 | 0.00 | 0.01 | −0.45 * |

| (0.02) | (0.02) | (0.07) | (0.03) | (0.03) | (0.23) | |

| Stock | 0.00 | −0.004 * | 0.01 | 0.02 | −0.01 *** | −0.53 ** |

| (0.00) | (0.00) | (0.01) | (0.03) | (0.00) | (0.24) | |

| cpi | −0.70 | 2.29 | 2.37 | −1.23 | 2.55 | 1.70 |

| (1.14) | (1.91) | (4.85) | (1.33) | (2.11) | (6.63) | |

| lnR&D intensity | 0.00 | 0.01 | 0.01 | 0.006 | 0.01 | 0.00 |

| (0.00) | (0.00) | (0.01) | (0.04) | (0.00) | (0.01) | |

| Constant | 0.154 ** | 0.106 | 0.435 ** | 0.229 *** | 0.136 ** | 0.470 ** |

| (0.07) | (0.06) | (0.20) | (0.07) | (0.06) | (0.24) | |

| Observations | 132 | 126 | 119 | 132 | 127 | 128 |

| R-squared | 0.233 | 0.135 | 0.091 | 0.277 | 0.138 | 0.129 |

| Variables | 3-Day CAR (Acquirer) | 3-Day CAR (Target) | 3-Day CAR (Combined) | 5-Day CAR (Acquirer) | 5-Day CAR (Target) | 5-Day CAR (Combined) |

|---|---|---|---|---|---|---|

| Exclusionary | ||||||

| Input foreclosure | −0.01 | 0.00 | 0.02 | −0.02 | −0.02 | 0.05 |

| (0.026) | (0.031) | (0.108) | (0.030) | (0.032) | (0.137) | |

| Customer misuse of information | 0.02 | 0.06 | 0.192 * | 0.02 | 0.0836 ** | 0.13 |

| (0.027) | (0.037) | (0.117) | (0.033) | (0.036) | (0.158) | |

| Customer forclosure | 0.00 | 0.01 | 0.04 | 0.01 | 0.00 | 0.17 |

| (0.025) | (0.036) | (0.103) | (0.035) | (0.035) | (0.158) | |

| Coordinated | ||||||

| Disruptive buyer | −0.03 | 0.04 | 0.16 | −0.07 | 0.01 | 0.08 |

| (0.038) | (0.075) | (0.239) | (0.058) | (0.062) | (0.254) | |

| Collusive | −0.01 | 0.00 | −0.25 | 0.02 | −0.01 | −0.04 |

| (0.032) | (0.044) | (0.188) | (0.052) | (0.046) | (0.140) | |

| Unilateral | −0.01 | −0.05 | −0.174 * | −0.03 | −0.06 * | −0.311 ** |

| (0.023) | (0.036) | (0.108) | (0.033) | (0.03) | (0.151) | |

| Eliminate compet. | 0.02 | −0.04 | 0.355 ** | 0.00 | −0.04 | 0.184 * |

| (0.037) | (0.040) | (0.137) | (0.043) | (0.041) | (0.112) | |

| Evasion | 0.05 | −0.02 | −0.14 | |||

| (0.036) | (0.055) | (0.235) | ||||

| lnRevenue | 0.00 | −0.0148 ** | 0.00 | −0.0172 ** | ||

| (0.010) | (0.007) | (0.015) | (0.007) | |||

| lnRevenue diff. | 0.06 | 0.00 | ||||

| (0.038) | (0.039) | |||||

| lnAsset intensity | 0.00 | 0.00 | −0.0232 * | 0.00 | 0.00 | 0.00 |

| (0.002) | (0.003) | (0.012) | (0.003) | (0.003) | (0.015) | |

| Cash | 0.05 | −0.01 | −0.09 | 0.04 | 0.00 | −0.49 ** |

| (0.039) | (0.053) | (0.141) | (0.047) | (0.057) | (0.23) | |

| Stock | 0.02 | −0.03 | −0.225 * | 0.02 | −0.03 | −0.61 ** |

| (0.045) | (0.050) | (0.120) | (0.045) | (0.055) | (0.23) | |

| cpi | 0.63 | 0.84 | −9.02 | 0.67 | 0.82 | −20.81 |

| (2.188) | (4.495) | (10.890) | (2.607) | (4.134) | (15.430) | |

| lnR&D intensity | 0.00 | 0.0182 ** | 0.0602 ** | −0.01 | 0.015 | 0.03 |

| (0.005) | (0.008) | (0.022) | (0.006) | (0.008) | (0.027) | |

| Constant | −0.05 | 0.328 *** | 0.08 | −0.01 | 0.353 *** | 0.72 |

| (0.095) | (0.096) | (0.401) | (0.148) | (0.093) | (0.520) | |

| Observations | 56 | 53 | 49 | 56 | 53 | 58 |

| R-squared | 0.099 | 0.374 | 0.386 | 0.109 | 0.438 | 0.311 |

| Variables | %$CAR Full Sample (3 Days) | %$CAR Vertical (3 Days) | %$CAR Full Sample (5 Days) | %$CAR Vertical (5 Days) |

|---|---|---|---|---|

| Exclusionary | ||||

| Input foreclosure | 0.38 *** | 0.24 * | 0.052 | 0.065 |

| (0.13) | (0.12) | (0.15) | (0.14) | |

| Customer misuse ofinformation | 0.33 * | 0.22 | 0.12 | 0.14 |

| (0.19) | (0.19) | (0.19) | (0.186) | |

| Customer forclosure | −0.19 | 0.003 | −0.057 | −0.003 |

| (0.21) | (0.15) | (0.18) | (0.14) | |

| Coordinated | ||||

| Disruptive buyer | −0.002 | −0.08 | ||

| (0.2) | (0.23) | |||

| Collusive | −0.16 * | −0.45 *** | −0.19 ** | −0.32 * |

| (0.09) | (0.14) | (0.09) | (0.17) | |

| Unilateral | −0.040 | 0.016 | 0.03 | 0.12 |

| (0.17) | (0.13) | (0.19) | (0.12) | |

| Eliminate compet. | −0.096 | −0.39 *** | −0.11 | −0.47 ** |

| (0.08) | (0.11) | (0.09) | (0.16) | |

| Vertical | −0.26 | −0.002 | ||

| (0.17) | (0.18) | |||

| lnRevenue | 0.041 * | −0.059 * | 0.027 | −0.07 ** |

| (0.02) | (0.03) | (0.02) | (0.03) | |

| lnAsset target | 0.01 | −0.007 | −0.002 | −0.009 |

| (0.01) | (0.01) | (0.007) | (0.008) | |

| Cash | 0.0567 | 0.400 | −0.00791 | −0.423 |

| (0.173) | (0.558) | (0.216) | (0.428) | |

| Stock | 0.0005 | 0.11 | 0.092 | 0.05 |

| (0.01) | (0.18) | (0.10) | (0.16) | |

| lncpi | 0.018 | 0.014 | 0.022 | 0.029 |

| (0.02) | (0.03) | (0.019) | (0.03) | |

| lnR&D int. | 0.023 | 0.0042 | 0.022 | 0.01 |

| (0.02) | (0.03) | (0.02) | (0.03) | |

| Constant | 0.492 * | 1.00 *** | 0.56 * | −0.21 |

| (0.26) | (0.30) | (0.28) | (0.28) | |

| Observations | 74 | 23 | 68 | 26 |

| R-squared | 0.261 | 0.712 | 0.227 | 0.594 |

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2022 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Sonenshine, R.; Da, S. The Impact of Vertical Theories of Harm on Investor Returns: An Event Study of US Vertical Mergers. J. Risk Financial Manag. 2022, 15, 315. https://doi.org/10.3390/jrfm15070315

Sonenshine R, Da S. The Impact of Vertical Theories of Harm on Investor Returns: An Event Study of US Vertical Mergers. Journal of Risk and Financial Management. 2022; 15(7):315. https://doi.org/10.3390/jrfm15070315

Chicago/Turabian StyleSonenshine, Ralph, and Seyni Da. 2022. "The Impact of Vertical Theories of Harm on Investor Returns: An Event Study of US Vertical Mergers" Journal of Risk and Financial Management 15, no. 7: 315. https://doi.org/10.3390/jrfm15070315

APA StyleSonenshine, R., & Da, S. (2022). The Impact of Vertical Theories of Harm on Investor Returns: An Event Study of US Vertical Mergers. Journal of Risk and Financial Management, 15(7), 315. https://doi.org/10.3390/jrfm15070315