Non-Fungible Token: A Systematic Review and Research Agenda

Abstract

:1. Introduction

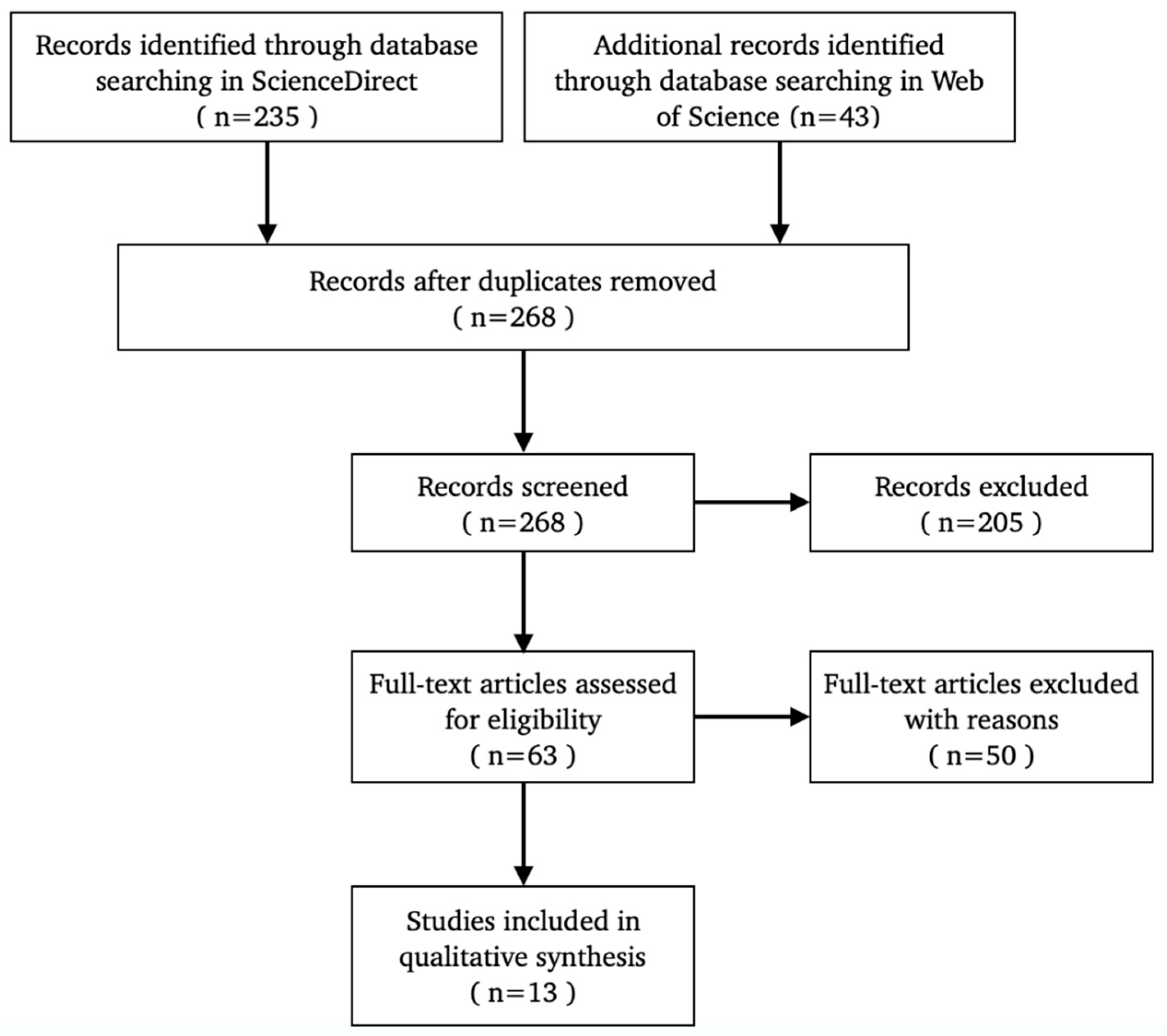

2. Method

2.1. Inclusion and Exclusion Criteria

2.2. Search Strategy and Selection Process

3. Results

3.1. Literature Distribution

3.2. Types of NFTs

3.3. Content Analysis of Empirical Studies

3.4. Content Analysis of Descriptive Research

4. Suggestions for Further Research

4.1. Asset Pricing

4.2. Tokenomics

4.3. Risk and Regulation

5. Conclusions and limitations

Author Contributions

Funding

Institutional Review Board Statement

Informed Consent Statement

Acknowledgments

Conflicts of Interest

| 1 | CryptoSlam is one of the leading NFT aggregators, collecting data from Ethereum, WAX, and FLOW blockchains. The official website is https://cryptoslam.io/ (accessed on 28 Febuary 2022). |

| 2 | AVR = Automatic Variance Ratio, AP = Automatic Portmanteau, DL = Domínguez and Lobato. |

| 3 | BSADF = Backward Sup Augmented Dickey–Fuller test. |

| 4 | TVP-VAR = Time-Varying Parameter Vector Autoregressive model. |

References

- Aharon, David Yechiam, and Ender Demir. 2021. NFTs and asset class spillovers: Lessons from the period around the COVID-19 pandemic. Finance Research Letters. in press. [Google Scholar] [CrossRef]

- Bao, Hong, and David Roubaud. 2022. Recent Development in Fintech: Non-Fungible Token. FinTech 1: 44–46. [Google Scholar] [CrossRef]

- Borri, Nicola, Yukun Liu, and Aleh Tsyvinski. 2022. The Economics of Non-Fungible Tokens. Available online: http://dx.doi.org/10.2139/ssrn.4052045 (accessed on 7 March 2022).

- Chalmers, Dominic, Christian Fisch, Russell Matthews, William Quinn, and Jan Recker. 2022. Beyond the bubble: Will NFTs and digital proof of ownership empower creative industry entrepreneurs? Journal of Business Venturing Insights 17: e00309. [Google Scholar] [CrossRef]

- Chohan, Raeesah, and Jeannette Paschen. 2021. What marketers need to know about non-fungible tokens (NFTs). Business Horizons. in press. [Google Scholar] [CrossRef]

- Chohan, Usman W. 2021. Non-Fungible Tokens: Blockchains, Scarcity, and Value. Available online: https://ssrn.com/abstract=3822743 (accessed on 24 March 2021).

- Cong, Lin William, Ye Li, and Neng Wang. 2021. Tokenomics: Dynamic adoption and valuation. The Review of Financial Studies 34: 1105–55. [Google Scholar] [CrossRef]

- Corbet, Shaen, Yang Greg Hou, Yang Hu, Charles Larkin, Brian Lucey, and Les Oxley. 2022. Cryptocurrency liquidity and volatility interrelationships during the COVID-19 pandemic. Finance Research Letters 45: 102137. [Google Scholar] [CrossRef]

- Dowling, Michael. 2022a. Fertile LAND: Pricing non-fungible tokens. Finance Research Letters 44: 102096. [Google Scholar] [CrossRef]

- Dowling, Michael. 2022b. Is non-fungible token pricing driven by cryptocurrencies? Finance Research Letters 44: 102097. [Google Scholar] [CrossRef]

- Franceschet, Massimo. 2021. HITS hits art. Blockchain: Research and Applications 2: 100038. [Google Scholar] [CrossRef]

- Gryglewicz, Sebastian, Simon Mayer, and Erwan Morellec. 2021. Optimal financing with tokens. Journal of Financial Economics 142: 1038–67. [Google Scholar] [CrossRef]

- Haaften-Schick, Lauren, and Amy Whitaker. 2022. From the artist’s contract to the blockchain ledger: New forms of artists’ funding using equity and resale royalties. Journal of Cultural Economy. Available online: https://doi.org/10.1007/s10824-022-09445-8 (accessed on 23 February 2022).

- Howell, Sabrina, Marina Niessner, and David Yermack. 2020. Initial coin offerings: Financing growth with cryptocurrency token sales. The Review of Financial Studies 33: 3925–74. [Google Scholar] [CrossRef] [Green Version]

- Karim, Sitara, Brian Lucey, Muhammad Abubakr Naeem, and Gazi Salah Uddin. 2022. Examining the interrelatedness of NFTs, DeFi tokens and cryptocurrencies. Finance Research Letters. in press. [Google Scholar] [CrossRef]

- Ko, Hyungjin, Bumho Son, Yunyoung Lee, Huisu Jang, and Jaewook Lee. 2022. The economic value of NFT: Evidence from a portfolio analysis using mean-variance framework. Finance Research Letters 47: 102784. [Google Scholar] [CrossRef]

- Liberati, Alessandro, Douglas Altman, Jennifer Tetzlaff, Cynthia Mulrow, Peter Gøtzsche, John Ioannidis, and David Moher. 2009. The PRISMA statement for reporting systematic reviews and meta-analyses of studies that evaluate healthcare interventions: Explanation and elaboration. PLoS Medicine 6: e1000100. [Google Scholar] [CrossRef] [PubMed]

- Maouchi, Youcef, Lanouar Charfeddine, and Ghassen El Montasser. 2021. Understanding digital bubbles amidst the COVID-19 pandemic: Evidence from DeFi and NFTs. Finance Research Letters. in press. [Google Scholar] [CrossRef]

- Nadini, Matthieu, Laura Alessandretti, Flavio Di Giacinto, Mauro Martino, Luca Maria Aiello, and Andrea Baronchelli. 2021. Mapping the NFT revolution: Market trends, trade networks, and visual features. Scientific Reports 11: 1–11. [Google Scholar]

- Pahlevan-Sharif, Saeed, Paolo Mura, and Sarah Wijesinghe. 2019. A systematic review of systematic reviews in tourism. Journal of Hospitality and Tourism Management 39: 158–65. [Google Scholar] [CrossRef]

- Freni, Pierluigi, Enrico Ferro, and Roberto Moncada. 2022. Tokenomics and blockchain tokens: A design-oriented morphological framework. Blockchain: Research and Applications 3: 100069. [Google Scholar] [CrossRef]

- Sarkodie, Samuel Asumadu, Maruf Yakubu Ahmed, and Phebe Asantewaa Owusu. 2022. COVID-19 pandemic improves market signals of cryptocurrencies–evidence from Bitcoin, Bitcoin Cash, Ethereum, and Litecoin. Finance Research Letters 44: 102049. [Google Scholar] [CrossRef]

- Savelyev, Alexander. 2018. Some risks of tokenization and blockchainizaition of private law. The Computer Law & Security Review 34: 863–69. [Google Scholar]

- Umar, Zaghum, Mariya Gubareva, Tamara Teplova, and Dang Tran. 2022. COVID-19 impact on NFTs and major asset classes interrelations: Insights from the wavelet coherence analysis. Finance Research Letters. in press. [Google Scholar] [CrossRef]

- Vidal-Tomás, David. 2022. The new crypto niche: NFTs, play-to-earn, and metaverse tokens. Finance Research Letters. in press. [Google Scholar]

- Wang, Qin, Rujia Li, Qi Wang, and Shiping Chen. 2021. Non-Fungible Token (NFT): Overview, Evaluation, Opportunities and Challenges. arXiv arXiv:2105.07447. [Google Scholar]

- Wilson, Kathleen Bridget, Adam Karg, and Hadi Ghaderi. 2021. Prospecting non-fungible tokens in the digital economy: Stakeholders and ecosystem, risk and opportunity. Business Horizons. [Google Scholar] [CrossRef]

- Yousaf, Imran, and Larisa Yarovaya. 2022. Static and dynamic connectedness between NFTs, Defi and other assets: Portfolio implication. Global Finance Journal 53: 100719. [Google Scholar] [CrossRef]

- Yue, Yao, Xuerong Li, Dingxuan Zhang, and Shouyang Wang. 2021. How cryptocurrency affects economy? A network analysis using bibliometric methods. International Review of Financial Analysis 77: 101869. [Google Scholar] [CrossRef]

{kind=link}

{kind=link}

| Author(s) (Year) | Journal Names (ABDC Rating) | Research Field | Methodology | Types of NFTs Analyzed |

|---|---|---|---|---|

| Chohan and Paschen (2021) | Business Horizons (B) | Business | Descriptive Research | General type |

| Wilson et al. (2021) | Business Horizons (B) | Business | Concept/Model Building | General type |

| Dowling (2022a) | Finance Research Letters (A) | Asset Pricing | Empirical Testing | Decentraland |

| Dowling (2022b) | Finance Research Letters (A) | Asset Pricing | Empirical Testing | CryptoPunk, Decentraland, and Axie Infinity |

| Vidal-Tomás (2022) | Finance Research Letters (A) | Asset Pricing | Empirical Testing | General type |

| Umar et al. (2022) | Finance Research Letters (A) | Asset Pricing | Empirical Testing | General type |

| Aharon and Demir (2021) | Finance Research Letters (A) | Asset Pricing | Empirical Testing | General type |

| Karim et al. (2022) | Finance Research Letters (A) | Financial Risks | Empirical Testing | Theta, Tezos, Enjin Coin, Decentraland and Digibyte |

| Maouchi et al. (2021) | Finance Research Letters (A) | Asset Pricing/Financial Risks | Empirical Testing | Theta, Enjin Coin, and Decentraland |

| Ko et al. (2022) | Finance Research Letters (A) | Asset Pricing | Empirical Testing | Sandbox, Decentraland, and Cryptopunks |

| Chalmers et al. (2022) | Journal of Business Venturing Insights (A) | Business | Descriptive Research | General type |

| Yousaf and Yarovaya (2022) | Global Finance Journal (A) | Asset Pricing | Empirical Testing | Theta, Tezos, Enjin Coin, DigiByte, and Decentraland |

| Haaften-Schick and Whitaker (2022) | Journal of Cultural Economics (A) | Business | Descriptive Research | General type |

| Author | Title | Method | Sample Interval |

|---|---|---|---|

| Dowling (2022a) | Fertile LAND: Pricing non-fungible tokens | AVR, AP and DL consistent test2 | March 2019 to March 2021 |

| Dowling (2022b) | Is non-fungible token pricing driven by cryptocurrencies? | Volatility spillover methodology, Wavelet coherence | March 2019 to March 2021 |

| Vidal-Tomás (2022) | The new crypto niche: NFTs, play-to-earn, and metaverse tokens | Pearson and Kendall correlations, BSADF3, Wavelet coherence | October 2017 to October 2021 |

| Umar et al. (2022) | COVID-19 impact on NFTs and major asset classes interrelations: Insights from the wavelet coherence analysis | Wavelet coherence | June 2017 to October 2021 |

| Aharon and Demir (2021) | NFTs and asset class spillovers: Lessons from the period around the COVID-19 pandemic | TVP-VAR4 | January 2018 to June 2021 |

| Karim et al. (2022) | Examining the interrelatedness of NFTs, DeFi tokens and cryptocurrencies | Quantile var, Volatility spillover methodology | March 2018 to October 2021 |

| Maouchi et al. (2021) | Understanding digital bubbles amidst the COVID-19 pandemic: Evidence from DeFi and NFTs | Logit, Probit, Tobit, and Linear regression | From the first trading day for each cryptoasset to March 2021 |

| Ko et al. (2022) | The economic value of NFT: Evidence from a portfolio analysis using mean–variance framework | Pearson correlations, Gerber Statistic, Volatility spillover methodology, TVP-VAR | December 2019 to June 2021 |

| Yousaf and Yarovaya (2022) | Static and dynamic connectedness between NFTs, Defi and other assets: Portfolio implication | TVP-VAR, BEKK-GARCH | May 2018 to July 2021 |

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2022 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Bao, H.; Roubaud, D. Non-Fungible Token: A Systematic Review and Research Agenda. J. Risk Financial Manag. 2022, 15, 215. https://doi.org/10.3390/jrfm15050215

Bao H, Roubaud D. Non-Fungible Token: A Systematic Review and Research Agenda. Journal of Risk and Financial Management. 2022; 15(5):215. https://doi.org/10.3390/jrfm15050215

Chicago/Turabian StyleBao, Hong, and David Roubaud. 2022. "Non-Fungible Token: A Systematic Review and Research Agenda" Journal of Risk and Financial Management 15, no. 5: 215. https://doi.org/10.3390/jrfm15050215

APA StyleBao, H., & Roubaud, D. (2022). Non-Fungible Token: A Systematic Review and Research Agenda. Journal of Risk and Financial Management, 15(5), 215. https://doi.org/10.3390/jrfm15050215