Board Information Technology Governance Mechanisms and Firm Performance among Iraqi Medium-Sized Enterprises: Do IT Capabilities Matter?

Abstract

1. Introduction

- Do board IT governance mechanisms (BITGS, BITGP, and BITGR) and IT capabilities improve firm performance?

- Do board IT governance mechanisms (BITGS, BITGP, and BITGR) influence IT capabilities?

- Do IT capabilities mediate the relationship between board IT governance mechanisms (BITGS, BITGP, and BITGR) and firm performance?

2. Literature Review and Hypotheses Development

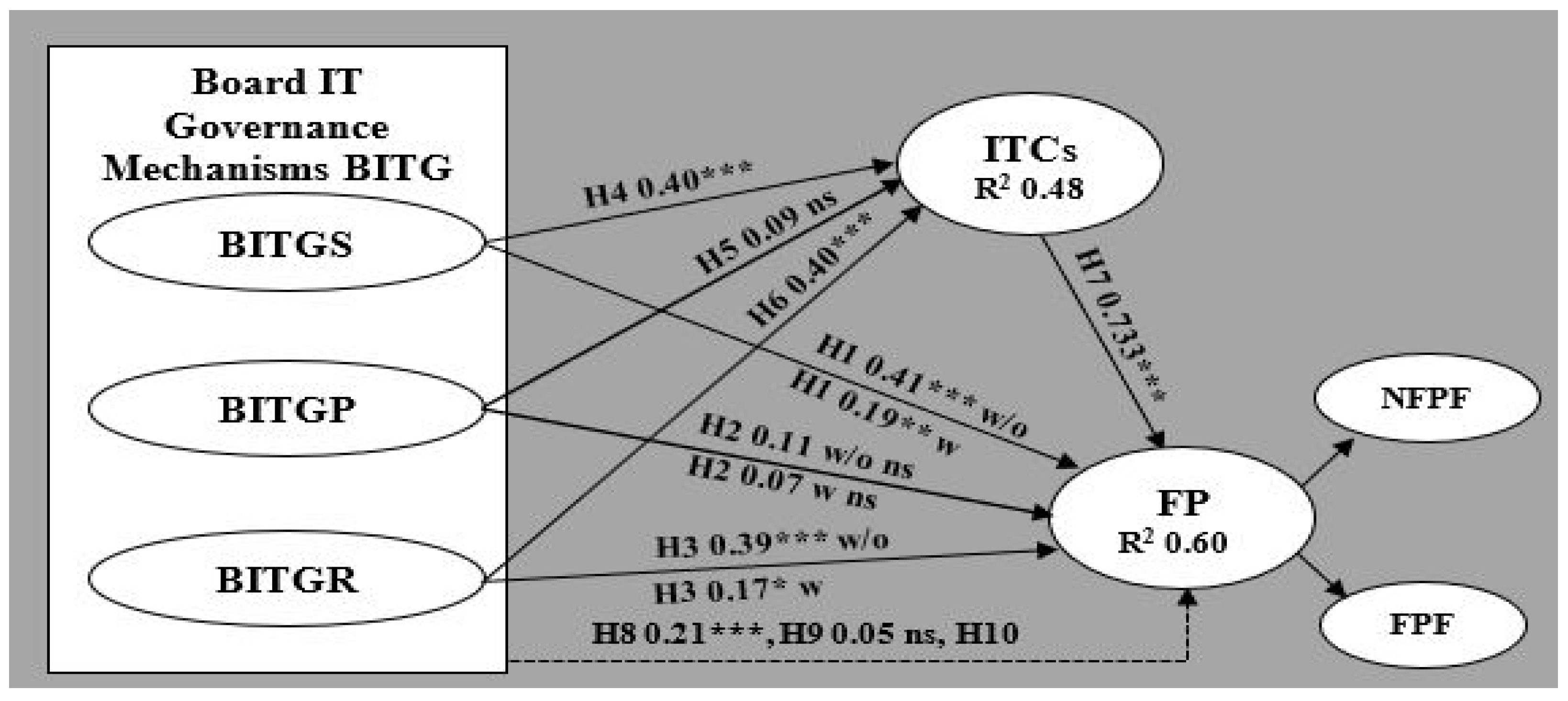

2.1. Board IT Governance Mechanisms and Firm Performance

2.2. Board IT Governance Mechanisms and IT Capabilities

2.3. IT Capabilities and Firm Performance

2.4. Board IT Governance Mechanisms, IT Capabilities, and Firm Performance

3. Materials and Methods

3.1. Measurement

3.2. Sample and Data

4. Results and Discussion

4.1. Measurement Model

4.2. Structural Model

5. Conclusions

Author Contributions

Funding

Institutional Review Board Statement

Informed Consent Statement

Data Availability Statement

Conflicts of Interest

Appendix A. Survey Questionnaire

| Latent Construct | Items | Source |

| Board IT Governance Structures (BITGS) | Directors are/have: BITGS1 resourceful in IT devices. * BITGS2 involved with overall IT budget sessions. BITGS3 connect on matters relating to IT. BITGS4 involved in providing IT policies. * BITGS5 conversant with the overall IT strategy/vision of the organisation *. BITGS6 aware of the IT risks to which the organisation is exposed. BITGS7 received formal training in IT. BITGS8 experience in the general management of IT within the organisation. BITGS9 worked directly in an IT role within the organisation. * IT strategy committee: BITGS10 ensures that IT is a regular agenda item and reporting issue for the board. BITGS11 provides strategic direction and the alignment of IT and business issues. BITGS12 provides direction for the sourcing and using IT resources, skills, and infrastructure to meet the strategic objectives. BITGS13 provides direction to management relative to IT strategy. * BITGS14 has independent members (from outside the organisation). BITGS15 addresses IT risks. | (Jewer and McKay 2012; Héroux and Fortin 2018) |

| Board IT Governance Processes (BITGP) | BITGP1 A formal planning process is used to define the IT strategy. BITGP2 A formal planning process is used to update the IT strategy. BITGP3 IT budgets are used to control and report on IT activities/investments.* BITGP4 There are IT performance measures (e.g., organisation contribution, user orientation, operational excellence, or future orientation). BITGP5 Methodologies are used to charge IT costs back to business units. BITGP6 There are formal agreements between business and IT service about IT development projects or IT operations. BITGP7 Processes are used to monitor the planned business benefits during and after implementing the IT investments/projects. BITGP8 The IT strategy and policies are defining objectives and expectations, such as accountability and responsibility. BITGP9 The IT strategy and policies are written clearly and understandably for employees affected by IT projects.* BITGP10 Provide these employees with extensive guidance regarding how to manage IT projects. * | (Héroux and Fortin 2018) |

| Board IT Governance Structures Relational mechanisms (BITGR) | BITGR1 The directors/officer in charge of IT articulate a vision for IT’s role in the organisation. BITGR2 The directors/officer in charge of IT ensure that managers clearly understand the vision for IT’s role throughout the organisation. BITGR3 There is job rotation (IT staff working in the business units and businesspeople working in IT). BITGR4 Directors and IT people are physically located close to each other. BITGR5 Directors are trained in IT, or IT people are taught about business. BITGR6 Systems such as the intranet are used to share and distribute knowledge about the IT governance framework, responsibilities, tasks, etc.* BITGR7 Business/administrative managers act as in-betweens for business and IT. BITGR8 Senior business and IT management act as “partners”. BITGR9 Senior business and IT management informally discuss the organisation’s activities and its role. * BITGR10 Internal corporate communications regularly address general IT issues. BITGR11 Campaigns are explaining the need for IT governance to business and IT people. * | (Héroux and Fortin 2018) |

| IT Capabilities (ITC) | ITC1 Our information systems are scalable. ITC2 Our information systems are adopted to share information. ITC3 Our firm transfers data with our suppliers. ITC4 Our firm connects our systems with our suppliers’ systems, which allows for the sharing of real-time information with our suppliers. ITC5 Information systems plan reflects the business plan goals. ITC6 Business plans refer to information systems plans. ITC7 Effectiveness of IT planning in our firm is better than that of other firms in our industry. ITC8 IT project management practices in our firm are better than those in other firms in our industry. | (Chen et al. 2015) |

| Financial Firm Performance (FFP) | FP1 Our organisation profit increased gradually within the last 3 years. FP2 Our organisation sales volume increased gradually within the last 3 years.* FP3 Our organisation returns on investment increased gradually within the last 3 years. FP4 Our organisation returns on assets increased gradually within the last 3 years. FP5 Our organisation market share increased gradually within the last 3 years. | (Henri 2006; Khan and Ali 2017) |

| Non-Financial Firm Performance (NFFP) | FP6 The number of new products in my organisation increased within the last 3 years. FP7 Our organisation market development increased significantly within the last 3 years. FP8 Our organisation product/services’ quality increased within the last 3 years. FP9 Our organisation employee commitment or loyalty increased within the last 3 years. FP10 Our organisation employee productivity increased within the last 3 years. FP11 Our organisation personnel development increased during the last 3 years. FP12 Our organisation employee job satisfaction increased during the last 3 years. | (Teeratansirikool et al. 2013; Khan and Ali 2017) |

| Notes: (1) * items eliminated due to low loading (less than 0.70). (2) Items are measured using a 5-point Likert scale in which 1 = strongly disagree, 2 = disagree, 3 = neutral, 4 = agree, and 5 = strongly agree. | ||

| 1 | Canadian Leaders in International Consulting submitted in 2018 a report entitled “Private Sector Development Scoping Study, Iraq” to the Netherlands Ministry of Foreign Affairs and the Netherlands Enterprise Agency regarding the investment climate in Iraq. Retrieved from: https://www.government.nl/documents/reports/2018/08/28/private-sector-development-scoping-study-iraq (accessed on 5 January 2020). |

| 2 | These firms are excluded from the population before the sample selection. |

| 3 | The number of MSEs have been extracted for the Iraqi Central Organisation for Statistics and Information Technology (http://cosit.gov.iq/en/, accessed on 15 February 2020). |

References

- Ahmed, Saad Mahmood, Mohamad Shanudin Zakaria, and Mohammed Alaa H. Altemimi. 2016. CSFS of Electronic Information Sharing in Iraqi SMEs. Journal of Engineering and Applied Sciences 11: 1846–50. [Google Scholar]

- Alaraji, Fedaa Abd Almajid Sabbar. 2017. The Role and Impact of Corporate Governance on Narrowing the Expectations Gap between the External Auditor and the Financial Community (A Practical Study of a Sample of External Audit Offices and Companies Invested in Iraq) (Case Study in Iraq). American Scientific Research Journal for Engineering, Technology, and Sciences 33: 305–27. [Google Scholar]

- Ali, Syaiful, and Peter Green. 2012. Effective Information Technology (IT) Governance Mechanisms: An IT Outsourcing Perspective. Information Systems Frontiers 14: 179–93. [Google Scholar] [CrossRef]

- Al-kafagi, Ali Mohamed Hassan. 2018. Organizing the ISIS: Emergence-Expansion-Ways Confrontation. AL-Qadisiya Journal 9: 389–54. [Google Scholar]

- Alkhaffaf, Haetham Kasem, Kamil Md Idris, Akilah Abdullah, and Al-Hasan Al-Aidaros. 2018. The Influence of Technology Readiness on Information Technology Competencies and Civil Conflict Environment. Indian-Pacific Journal of Accounting and Finance 2: 51–64. [Google Scholar] [CrossRef]

- Al-Lamy, Hayder, Mohamed Hariri Bakry, Wisam Raad, Samer Ali Al-Shami, Zaid Jabaar Alaraji, Mustafa W. Alsa-Lihi, and Hussein M. Al-Tameemi. 2018. Information Technology Infrastructure and Small Medium Enterprises in Iraq. Opcion 34: 1711–24. [Google Scholar]

- Almagtome, Akeel, Inaam Almusawi, and Karrar Aureaar. 2017. Challenges of Corporate Voluntary Disclosure Through the Annual Reports: Evidence from Iraq. World Applied Sciences Journal 35: 2093–100. [Google Scholar]

- Arora, Bharat, and Zillur Rahman. 2017. Information Technology Capability as Competitive Advantage in Emerging Markets: Evidence from India. International Journal of Emerging Markets 12: 447–63. [Google Scholar] [CrossRef]

- Aydiner, Arafat Salih, Ekrem Tatoglu, Erkan Bayraktar, and Selim Zaim. 2019. Information System Capabilities and Firm Performance: Opening the Black Box Through Decision-Making Performance and Business-Process Performance. International Journal of Information Management 47: 168–82. [Google Scholar] [CrossRef]

- Barney, Jay B., David J. Ketchen, Jr., and Mike Wright. 2011. The Future of Resource-Based Theory: Revitalization or Decline? Journal of Management 37: 1299–315. [Google Scholar] [CrossRef]

- Baron, Reuben M., and David A. Kenny. 1986. The Moderator–Mediator Variable Distinction in Social Psychological Research: Conceptual, Strategic, and Statistical Considerations. Journal of Personality and Social Psychology 51: 1173. [Google Scholar] [CrossRef] [PubMed]

- Benaroch, Michel, and Anna Chernobai. 2017. Operational IT failures, IT VALUE-Destruction, and Board-Level IT Governance Changes. MIS Quarterly. Available online: https://ssrn.com/abstract=2887773 (accessed on 10 March 2020).

- Bharadwaj, Anandhi S. 2000. A resource-based perspective on information technology capability and firm performance: An empirical investigation. MIS Quarterly 24: 169–96. [Google Scholar] [CrossRef]

- Bharadwaj, Anandhi S., Sundar G. Bharadwaj, and Benn R. Konsynski. 1999. Information Technology Effects on Firm Performance as Measured by Tobin’s Q. Management Science 45: 1008–24. [Google Scholar] [CrossRef]

- Bhatt, Ganesh, Ali Emdad, Nicholas Roberts, and Varun Grover. 2010. Building and leveraging information in dynamic environments: The role of IT infrastructure flexibility as enabler of organizational responsiveness and competitive advantage. Information & Management 47: 341–49. [Google Scholar]

- Bhatt, Ganesh, and Varun Grover. 2005. Types of Information Technology Capabilities and Their Role in Competitive Advantage: An Empirical Study. Journal of Management Information Systems 22: 253–77. [Google Scholar] [CrossRef]

- Boritz, J. Efrim, and Jee-Hae Lim. 2008. IT Control Weaknesses, IT Governance and Firm Performance. In IT Governance and Firm Performance (11 January 2008). (CAAA) 2008 Annual Conference Paper. Available online: https://ssrn.com/abstract=1082957 (accessed on 25 March 2020).

- Boudreau, Marie-Claude, David Gefen, and Detmar W. Straub. 2001. Validation in Information Systems Research: A State-Of-The-Art Assessment. MIS Quarterly 25: 1–16. [Google Scholar] [CrossRef]

- Bowen, Paul L., May-Yin Decca Cheung, and Fiona H. Rohde. 2007. Enhancing IT Governance Practices: A Model and Case Study of An Organization’s Efforts. International Journal of Accounting Information Systems 8: 191–221. [Google Scholar] [CrossRef]

- Brislin, Richard W. 1970. Back-Translation for Cross-Cultural Research. Journal of Cross-Cultural Psychology 1: 185–216. [Google Scholar] [CrossRef]

- Bureau of Economic and Business Affairs. 2015. Investment Climate Statement Iraq. U.S. Department of State. Available online: http://www.state.gov/e/eb/rls/othr/ics/2015/241599.htm (accessed on 15 September 2019).

- Byrd, Terry Anthony, and Douglas E. Turner. 2001. An Exploratory Examination of The Relationship Between Flexible IT Infrastructure and Competitive Advantage. Information & Management 39: 41–52. [Google Scholar]

- Caluwe, Laura, and Steven De Haes. 2019. Board Level IT Governance: A Scoping Review to Set the Research Agenda. Information Systems Management 36: 262–83. [Google Scholar] [CrossRef]

- Céspedes-Lorente, José J., Amalia Magán-Díaz, and Ester Martínez-Ros. 2019. Information Technologies and Downsizing: Examining Their Impact on Economic Performance. Information & Management 56: 526–35. [Google Scholar]

- Chae, Ho-Chang, Chang E. Koh, and Kwang O. Park. 2018. Information Technology Capability and Firm Performance: Role of Industry. Information & Management 55: 525–46. [Google Scholar]

- Chan, Yolande E. 2000. IT Value: The Great Divide Between Qualitative and Quantitative and Individual and Organizational Measures. Journal of Management Information Systems 16: 225–61. [Google Scholar] [CrossRef]

- Chen, Yang, Yi Wang, Saggi Nevo, Jose Benitez-Amado, and Gang Kou. 2015. IT Capabilities and Product Innovation Performance: The Roles of Corporate Entrepreneurship and Competitive Intensity. Information & Management 52: 643–57. [Google Scholar]

- Chin, Wynne W. 1998. Commentary: Issues and Opinion on Structural Equation Modeling. MIS Quarterly 22: Vii–Xvi. [Google Scholar]

- Coertze, Jacques, and Rossouw Von Solms. 2013. The Board and IT Governance: A Replicative Study. African Journal of Business Management 7: 3358–73. [Google Scholar]

- Cooper, Donald R., and Pamela S. Schindler. 2013. Business Research Methods, 12th ed. New York: McGraw-Hill. [Google Scholar]

- De Haes, Steven, and Wim Van Grembergen. 2009. An Exploratory Study into IT Governance Implementations and Its Impact on Business/IT Alignment. Information Systems Management 26: 123–37. [Google Scholar] [CrossRef]

- Dehning, Bruce, and Theophanis Stratopoulos. 2003. Determinants of A Sustainable Competitive Advantage Due to An IT-Enabled Strategy. The Journal of Strategic Information Systems 12: 7–28. [Google Scholar] [CrossRef]

- DeLone, William H. 1988. Determinants of success for computer usage in small business. MIS Quarterly, 51–61. [Google Scholar]

- Feeny, David F., and Leslie P. Willcocks. 1998. Core IS Capabilities for Exploiting Information Technology. Sloan Management Review 39: 9–21. [Google Scholar]

- Fornell, Claes, and David F. Larcker. 1981. Evaluating Structural Equation Models with Unobservable Variables and Measurement Error. Journal of Marketing Research 18: 39–50. [Google Scholar] [CrossRef]

- Grover, Varun, and Khawaja A. Saeed. 2007. The Impact of Product, Market, and Relationship Characteristics on Interorganizational System Integration in Manufacturer-Supplier Dyads. Journal of Management Information Systems 23: 185–216. [Google Scholar] [CrossRef]

- Gu, Bin, Ling Xue, and Gautam Ray. 2008. IT Governance and IT Investment Performance: An Empirical Analysis. Available online: Https://Ssrn.Com/Abstract=1145102 (accessed on 7 January 2020).

- Gupta, Sangita Dutta, Ajitava Raychaudhuri, and Sushil Kumar Haldar. 2018. Information Technology and Profitability: Evidence from Indian Banking Sector. International Journal of Emerging Markets 3: 1070–87. [Google Scholar] [CrossRef]

- Hair, Joe F., Christian M. Ringle, and Marko Sarstedt. 2011. PLS-SEM: Indeed, A Silver Bullet. Journal of Marketing Theory and Practice 19: 139–52. [Google Scholar] [CrossRef]

- Hamawandy, Nawzad Majeed, Rezan Salahaddin Azzat, and Shahla Abdulwahid Hamad. 2021. The Role of Segment Financial Reports in Rationalizing Investment Decisions in Iraq. Journal of Contemporary Issues in Business and Government 27: 3058–68. [Google Scholar]

- Hamdan, Allam, Reem Khamis, Mohammed Anasweh, Mukhtar Al-Hashimi, and Anjum Razzaque. 2019. IT Governance and Firm Performance: Empirical Study from Saudi Arabia. Sage Open 9: 2158244019843721. [Google Scholar] [CrossRef]

- Hao, Shengbin, and Michael Song. 2016. Technology-Driven Strategy and Firm Performance: Are Strategic Capabilities Missing Links? Journal of Business Research 69: 751–59. [Google Scholar] [CrossRef]

- Harash, Emad, Karim Al-Tamimi, and Suhail Al-Timimi. 2014. The Relationship Between Government Policy and Financial Performance: A Study on The SMEs in Iraq. China-USA Business Review 13: 290–95. [Google Scholar]

- Hasan, Harith. 2018. Beyond Security: Stabilization. Governance. and Socioeconomic Challenges in Iraq. Available online: https://www.atlanticcouncil.org/in-depth-research-reports/issue-brief/beyond-security-stabilization-governance-and-socioeconomic-challenges-in-iraq/ (accessed on 5 August 2019).

- Helfat, Constance E. 1997. Know-How and Asset Complementarity and Dynamic Capability Accumulation: The Case of R&D. Strategic Management Journal 18: 339–60. [Google Scholar]

- Henri, Jean-François. 2006. Management Control Systems and Strategy: A Resource-Based Perspective. Accounting, Organizations and Society 31: 529–58. [Google Scholar] [CrossRef]

- Henseler, Jörg, Christian M. Ringle, and Rudolf R. Sinkovics. 2009. The Use of Partial Least Squares Path Modeling in International Marketing. In New Challenges to International Marketing. Bingley: Emerald Group Publishing Limited, vol. 20, pp. 277–319. [Google Scholar] [CrossRef]

- Héroux, Sylvie, and Anne Fortin. 2014. Exploring IT Dependence and IT Governance. Information Systems Management 31: 143–66. [Google Scholar] [CrossRef]

- Héroux, Sylvie, and Anne Fortin. 2018. The Moderating Role of IT–business Alignment in The Relationship Between IT Governance, IT Competence, and Innovation. Information Systems Management 35: 98–123. [Google Scholar] [CrossRef]

- Higgs, Julia L., Robert E. Pinsker, Thomas J. Smith, and George R. Young. 2016. The Relationship between Board-Level Technology Committees and Reported Security Breaches. Journal of Information Systems 30: 79–98. [Google Scholar] [CrossRef]

- Hsu, Wen-Hsi Lydia, George Yungchih Wang, and Yuan-Pai Hsu. 2012. Testing mediator and moderator effects of independent director on firm performance. International Journal of Mathematical Models and Methods in Applied Sciences 5: 698–705. [Google Scholar]

- Iden, Jon, and Tom Roar Eikebrokk. 2014. Using the ITIL Process Reference Model for Realizing IT Governance: An Empirical Investigation. Information Systems Management 31: 37–58. [Google Scholar] [CrossRef][Green Version]

- Ilmudeen, Aboobucker, and Yukun Bao. 2020. IT Strategy and Business Strategy Mediate the Effect of Managing IT on Firm Performance: Empirical Analysis. Journal of Enterprise Information Management 33: 1357–78. [Google Scholar] [CrossRef]

- Ilmudeen, Aboobucker. 2019. Impact of IT Governance Mechanism on IT-Enabled Dynamic Capabilities to Shape Agility and Firm Innovative Capability: Moderating Role of Turbulent Environment. Paper presented at the 8th International Conference on Management and Economics, ICME 2019, Shanghai, China, October 19–21; Available online: http://ir.lib.seu.ac.lk/handle/123456789/4987 (accessed on 10 December 2019).

- Iraqi Ministry of Finance. 2019. Federal Budget Law, (from 2009 to 2018). Available online: http://www.mof.gov.iq/pages/ar/federalbudgetlaw.aspx (accessed on 10 December 2019).

- Jewer, Jennifer, and Kenneth N. McKay. 2012. Antecedents and Consequences of Board IT Governance: Institutional and Strategic Choice Perspectives. Journal of the Association for Information Systems 13: 1. Available online: https://aisel.aisnet.org/jais/vol13/iss7/1 (accessed on 15 June 2019).

- Jubouri, Abdul Khaleq Dubai. 2013. Iraqi Economy and the Reality of Human Development in The Light of New Transitions. Journal of The Faculty of Management and Economics for Economic Studies 314: 50–79. [Google Scholar]

- Kearns, Grover, and Albert Lederer. 2003. A resource-based view of strategic IT alignment: How knowledge sharing creates competitive advantage. Decision sciences 34: 1–29. [Google Scholar] [CrossRef]

- Kettinger, William J., Chen Zhang, and Kuo-Chung Chang. 2013. Research Note—A View from the Top: Integrated Information Delivery and Effective Information Use from the Senior Executive’s Perspective. Information Systems Research 24: 842–60. [Google Scholar] [CrossRef]

- Khan, Sajjad Nawaz, and Engku Ismail Engku Ali. 2017. The moderating role of intellectual capital between enterprise risk management and firm performance: A conceptual review. American Journal of Social Sciences and Humanities 2: 9–15. [Google Scholar] [CrossRef]

- Khan, Sajjad Nawaz, Rai Imtiaz Hussain, Muhammad Qasim Maqbool, Engku Ismail Engku Ali, and Muhammad Numan. 2019. The Mediating Role of Innovation between Corporate Governance and Organizational Performance: Moderating Role of Innovative Culture in Pakistan Textile Sector. Cogent Business & Management 6: 1–23. [Google Scholar] [CrossRef]

- Kuruzovich, Jason, Genevieve Bassellier, and V. Sambamurthy. 2012. IT Governance Processes and IT Alignment: Viewpoints from the Board of Directors. Paper presented at 2012 45th Hawaii International Conference on System Sciences, Maui, HI, USA, January 4–7; pp. 5043–52. [Google Scholar] [CrossRef]

- Lim, Jee-Hae, Theophanis C. Stratopoulos, and Tony S. Wirjanto. 2012. Role of IT Executives in The Firm’s Ability to Achieve Competitive Advantage Through IT Capability. International Journal of Accounting Information Systems 13: 21–40. [Google Scholar] [CrossRef]

- Liu, Peng, Ofir Turel, and Chris Bart. 2019. Board IT Governance in Context: Considering Governance Style and Environmental Dynamism Contingencies. Information Systems Management 36: 212–27. [Google Scholar] [CrossRef]

- Luftman, Jerry, and Tom Brier. 1999. Achieving and Sustaining Business-IT Alignment. California Management Review 42: 109–22. [Google Scholar] [CrossRef]

- Mchaal, Salim Muhammma. 2015. Legal Regulation of The Work of Foreign Workers in The Light of the Iraqi Investment Law No. 13 of 2006. Journal of the College of Law/Al-Nahrain University 17: 284–307. [Google Scholar]

- Mithas, Sunil, Narayan Ramasubbu, and Vallabh Sambamurthy. 2011. How Information Management Capability Influences Firm Performance. MIS Quarterly 35: 237–56. [Google Scholar] [CrossRef]

- Nitzl, Christian, Jose L. Roldan, and Gabriel Cepeda. 2016. Mediation Analysis in Partial Least Squares Path Modeling: Helping Researchers Discuss More Sophisticated Models. Industrial Management & Data Systems 116: 1849–64. [Google Scholar]

- Nolan, Richard, and F. Warren McFarlan. 2005. Information Technology and The Board of Directors. Harvard Business Review 83: 1–11. [Google Scholar]

- Olutoyin, Olaitan, and Stephen Flowerday. 2016. Successful IT Governance inSMES: An Application of The Technology-Organization-Environment Theory. South African Journal of Information Management 18: 1–8. [Google Scholar]

- Prasad, Acklesh, Peter Green, and Jon Heales. 2012. On IT Governance Structures and Their Effectiveness in Collaborative Organizational Structures. International Journal of Accounting Information Systems 13: 199–220. [Google Scholar] [CrossRef]

- Preacher, Kristopher J., and Andrew F. Hayes. 2008. Asymptotic and Resampling Strategies for Assessing and Comparing Indirect Effects in Multiple Mediator Models. Behavior Research Methods 40: 879–91. [Google Scholar] [CrossRef]

- Qu, Wen Guang, Wonseok Oh, and Alain Pinsonneault. 2010. The strategic value of IT insourcing: An IT-enabled business process perspective. The Journal of Strategic Information Systems 19: 96–108. [Google Scholar] [CrossRef]

- Rai, Arun, Ravi Patnayakuni, and Nainika Seth. 2006. Firm Performance Impacts of Digitally Enabled Supply Chain Integration Capabilities. MIS Quarterly 30: 225–46. [Google Scholar] [CrossRef]

- Raseed, Hasan Hantosh, and Akel Karem Zaker. 2013. Foreign investment between the law and the economy. Risalat Al-Huquq Journal 3: 6–25. [Google Scholar]

- Redha, Apostle, and Khir religion Kazim. 2009. The impact of foreign capacity in the Iraqi Investment Law No. 13 of 2006. AL-Mouhaqiq Al-Hilly Journal for Legal and Political Science 1: 128–57. [Google Scholar]

- Rivard, Suzanne, Louis Raymond, and David Verreault. 2006. Resource-Based View and Competitive Strategy: An Integrated Model of The Contribution of Information Technology to Firm Performance. The Journal of Strategic Information Systems 15: 29–50. [Google Scholar] [CrossRef]

- Santhanam, Radhika, and Edward Hartono. 2003. Issues in Linking Information Technology Capability to Firm Performance. MIS Quarterly 27: 125–53. [Google Scholar] [CrossRef]

- Sekaran, Uma, and Roger Bougie. 2016. Research Methods for Business: A Skill Building Approach. Hoboken: John Wiley & Sons. [Google Scholar]

- Slim, Ali Mechman, Omar Siti Sarah, Kadhim Ghaffar Kadhim, Bashar Jamal Ali, Ahmed Mohammed Hammood, and Bestoon Othman. 2021. The Effect of Information Technology Business Alignment Factors on Performance of SMEs. Management Science Letters 11: 833–42. [Google Scholar] [CrossRef]

- Syailendra, Gede Dion. 2019. Influence of Information Technology Governance to Company Performance with Mediation of Information Technology Capabilities in Indonesia. American Journal of Humanities and Social Sciences Research 3: 187–97. [Google Scholar]

- Tallon, Paul, Kenneth Kraemer, and Vijay Gurbaxani. 2000. Executives’ perceptions of the business value of information technology: A process-oriented approach. Journal of management information systems 16: 145–73. [Google Scholar] [CrossRef]

- Teeratansirikool, Luliya, Sununta Siengthai, Yuosre Badir, and Chotchai Charoenngam. 2013. Competitive Strategies and Firm Performance: The Mediating Role of Performance Measurement. International Journal of Productivity and Performance Management 62: 168–84. [Google Scholar] [CrossRef]

- Tema, Basem Alwan. 2013. Iraqi Investment Law No. 13 of 2006, As Amended in The Balance. Risalat Al-Huquq Journal 2: 6–61. [Google Scholar]

- Turedi, Serdar. 2020. The Interactive Effect of Board Monitoring and Chief Information Officer Presence on Information Technology Investment. Information Systems Management 37: 113–23. [Google Scholar] [CrossRef]

- Turel, Ofir, Alexander Serenko, and Paul Giles. 2011. Integrating Technology Addiction and Use: An Empirical Investigation of Online Auction Users. MIS Quarterly 35: 1043–61. [Google Scholar] [CrossRef]

- Turel, Ofir, and Chris Bart. 2014. Board-Level IT Governance and Organizational Performance. European Journal of Information Systems 23: 223–39. [Google Scholar] [CrossRef]

- Turel, Ofir, Peng Liu, and Chris Bart. 2017. Board-Level Information Technology Governance Effects on Organizational Performance: The Roles of Strategic Alignment and Authoritarian Governance Style. Information Systems Management 34: 117–36. [Google Scholar] [CrossRef]

- Turel, Ofir, Peng Liu, and Chris Bart. 2019. Is Board IT Governance A Silver Bullet? A Capability Complementarity and Shaping View. International Journal of Accounting Information Systems 33: 32–46. [Google Scholar] [CrossRef]

- Van Grembergen, Wim, and Steven De Haes. 2009. Enterprise Governance of Information Technology: Achieving Strategic Alignment and Value. New York: Springer Publishing Company, Incorporated. [Google Scholar]

- Wade, Michael, and John Hulland. 2004. The Resource-Based View and Information Systems Research: Review, Extension, and Suggestions for Future Research. MIS Quarterly 28: 107–42. [Google Scholar] [CrossRef]

- Weill, Peter. 2004. Don’t Just Lead, Govern: How Top-Performing Firms Govern IT. MIS Quarterly Executive 3: 1–17. [Google Scholar]

- Wernerfelt, Birger. 1984. A Resource-Based View of The Firm. Strategic Management Journal 5: 171–80. [Google Scholar] [CrossRef]

- Wu, Shelly Ping-Ju, Detmar W. Straub, and Ting-Peng Liang. 2015. How Information Technology Governance Mechanisms and Strategic Alignment Influence Organizational Performance. MIS Quarterly 39: 497–518. [Google Scholar] [CrossRef]

- Xu, Xiaobo, Weiyong Zhang, and Ling Li. 2016. The Impact of Technology Type and Life Cycle on IT Productivity Variance: A Contingency Theoretical Perspective. International Journal of Information Management 36: 1193–204. [Google Scholar] [CrossRef]

- Zahra, Shaker A., and John A. Pearce. 1989. Boards of Directors and Corporate Financial Performance: A Review and Integrative Model. Journal of Management 15: 291–334. [Google Scholar] [CrossRef]

- Zhang, Lu, Jinghua Huang, and Xin Xu. 2012. Impact of ERP Investment on Company Performance: Evidence from Manufacturing Firms in China. Tsinghua Science and Technology 17: 232–40. [Google Scholar] [CrossRef]

- Zhang, Man, Saonee Sarker, and Suprateek Sarker. 2008. Unpacking the Effect of IT Capability on The Performance of Export-Focused SMEs: A Report from China. Information Systems Journal 18: 357–80. [Google Scholar] [CrossRef]

- Zhang, Peiqin, Kexin Zhao, and Ram L. Kumar. 2016. Impact of IT Governance and IT Capability on Firm Performance. Information Systems Management 33: 357–73. [Google Scholar] [CrossRef]

{kind=link}

{kind=link}

| Panel A: Sample classification by sectors | ||||

| Distributed | Collected Usable | |||

| Industry | No. | % | No. | % |

| Manufacturing | 138 | 46% | 106 | 76.81% |

| Services | 66 | 22% | 50 | 75.76% |

| Agriculture | 24 | 8% | 15 | 62.50% |

| Communication | 21 | 7% | 14 | 66.67% |

| Construction | 27 | 9% | 22 | 81.48% |

| Others | 24 | 8% | 16 | 66.67% |

| Total | 300 | 100% | 223 | 74.33% |

| Panel B: Descriptive of the respondents (N 223) | ||||

| Respondents board membership | No. | % | ||

| CEOs | 57 | 25.56% | ||

| Executive members | 122 | 54.71% | ||

| Non-Executive members | 44 | 19.73% | ||

| Respondents’ education | ||||

| Bachelor’s degree | 163 | 73.09% | ||

| Master’s degree | 43 | 19.29% | ||

| Professional certificate | 17 | 7.62% | ||

| Respondents’ experience | ||||

| Less than 10 years | 56 | 25.11% | ||

| More than 10 years and less than 15 years | 67 | 30.05% | ||

| More than 15 years | 100 | 44.84% | ||

| Construct | Item | BITGS | BITGP | BITGR | ITCs | FFP | NFFP | |

|---|---|---|---|---|---|---|---|---|

| Board IT Governance Structure BITGS | BITGS2 | 0.801 | −0.056 | 0.364 | 0.464 | 0.351 | 0.419 | |

| BITGS3 | 0.831 | −0.059 | 0.378 | 0.481 | 0.364 | 0.434 | ||

| BITGS6 | 0.868 | −0.061 | 0.395 | 0.503 | 0.381 | 0.454 | ||

| BITGS7 | 0.860 | −0.061 | 0.391 | 0.498 | 0.377 | 0.450 | ||

| BITGS8 | 0.886 | −0.062 | 0.403 | 0.513 | 0.389 | 0.463 | ||

| BITGS10 | 0.807 | −0.057 | 0.367 | 0.467 | 0.354 | 0.422 | ||

| BITGS11 | 0.738 | −0.052 | 0.336 | 0.427 | 0.324 | 0.386 | ||

| BITGS12 | 0.847 | −0.060 | 0.386 | 0.491 | 0.372 | 0.443 | ||

| BITGS14 | 0.772 | −0.054 | 0.351 | 0.447 | 0.339 | 0.404 | ||

| BITGS15 | 0.716 | −0.050 | 0.326 | 0.415 | 0.314 | 0.375 | ||

| Board IT Governance Process BITGP | BITGP1 | −0.049 | 0.700 | 0.089 | 0.078 | 0.032 | 0.100 | |

| BITGP2 | −0.051 | 0.727 | 0.092 | 0.081 | 0.034 | 0.104 | ||

| BITGP4 | −0.058 | 0.816 | 0.104 | 0.091 | 0.038 | 0.117 | ||

| BITGP5 | −0.053 | 0.749 | 0.095 | 0.084 | 0.035 | 0.107 | ||

| BITGP6 | −0.060 | 0.858 | 0.109 | 0.096 | 0.040 | 0.123 | ||

| BITGP7 | −0.061 | 0.870 | 0.110 | 0.097 | 0.040 | 0.125 | ||

| BITGP8 | −0.050 | 0.712 | 0.090 | 0.079 | 0.033 | 0.102 | ||

| Board IT Governance Relational BITGR | BITGR1 | 0.411 | 0.115 | 0.902 | 0.539 | 0.378 | 0.491 | |

| BITGR2 | 0.391 | 0.109 | 0.860 | 0.514 | 0.361 | 0.469 | ||

| BITGR3 | 0.401 | 0.112 | 0.881 | 0.527 | 0.370 | 0.480 | ||

| BITGR4 | 0.388 | 0.108 | 0.853 | 0.510 | 0.358 | 0.465 | ||

| BITGR5 | 0.406 | 0.113 | 0.891 | 0.533 | 0.374 | 0.486 | ||

| BITGR7 | 0.406 | 0.113 | 0.893 | 0.534 | 0.375 | 0.487 | ||

| BITGR8 | 0.404 | 0.113 | 0.887 | 0.530 | 0.372 | 0.483 | ||

| BITGR10 | 0.338 | 0.094 | 0.743 | 0.444 | 0.312 | 0.405 | ||

| IT Capabilities ITCs | ITC1 | 0.444 | 0.085 | 0.458 | 0.766 | 0.357 | 0.546 | |

| ITC2 | 0.477 | 0.092 | 0.493 | 0.824 | 0.384 | 0.587 | ||

| ITC3 | 0.500 | 0.096 | 0.516 | 0.864 | 0.403 | 0.616 | ||

| ITC4 | 0.469 | 0.090 | 0.484 | 0.810 | 0.377 | 0.577 | ||

| ITC5 | 0.516 | 0.099 | 0.533 | 0.891 | 0.415 | 0.635 | ||

| ITC6 | 0.453 | 0.087 | 0.467 | 0.781 | 0.364 | 0.557 | ||

| ITC7 | 0.475 | 0.091 | 0.490 | 0.820 | 0.382 | 0.585 | ||

| ITC8 | 0.419 | 0.081 | 0.433 | 0.724 | 0.337 | 0.516 | ||

| Firm Performance FP | Financial Firm Performance FFP | FFP1 | 0.326 | 0.034 | 0.312 | 0.346 | 0.743 | 0.507 |

| FFP3 | 0.322 | 0.034 | 0.308 | 0.343 | 0.735 | 0.501 | ||

| FFP4 | 0.346 | 0.037 | 0.331 | 0.368 | 0.789 | 0.538 | ||

| FFP5 | 0.329 | 0.035 | 0.314 | 0.349 | 0.750 | 0.511 | ||

| Non-Financial Firm Performance NFFP | NFFP1 | 0.398 | 0.109 | 0.414 | 0.542 | 0.519 | 0.761 | |

| NFFP2 | 0.434 | 0.119 | 0.453 | 0.592 | 0.567 | 0.831 | ||

| NFFP3 | 0.384 | 0.105 | 0.400 | 0.523 | 0.500 | 0.733 | ||

| NFFP4 | 0.444 | 0.122 | 0.462 | 0.605 | 0.578 | 0.848 | ||

| NFFP5 | 0.403 | 0.110 | 0.420 | 0.549 | 0.526 | 0.771 | ||

| NFFP6 | 0.441 | 0.121 | 0.460 | 0.601 | 0.575 | 0.844 | ||

| NFFP7 | 0.407 | 0.112 | 0.424 | 0.555 | 0.531 | 0.779 | ||

| CR | AVE | BITGS | BITGP | BITGR | ITCs | FFP | NFFP | Mean | S.D. | |

|---|---|---|---|---|---|---|---|---|---|---|

| BITGS | 0.890 | 0.663 | 0.814 | 3.704 | 0.827 | |||||

| BITGP | 0.845 | 0.606 | −0.070 | 0.779 | 2.783 | 0.785 | ||||

| BITGR | 0.874 | 0.748 | 0.455 | 0.127 | 0.865 | 3.337 | 1.013 | |||

| ITCs | 0.866 | 0.659 | 0.579 | 0.112 | 0.598 | 0.812 | 3.135 | 0.827 | ||

| FFP | 0.751 | 0.569 | 0.439 | 0.046 | 0.419 | 0.466 | 0.755 | 3.420 | 0.747 | |

| NFFP | 0.848 | 0.634 | 0.523 | 0.143 | 0.545 | 0.713 | 0.682 | 0.796 | 2.864 | 0.723 |

| Structural Path | Standardised Path Coefficient | S.E. | C.R. | Label |

|---|---|---|---|---|

| BITGS --> FP | 0.412 *** | 0.062 | 5.337 | H1 Supported |

| BITGP --> FP | 0.114 | 0.051 | 1.789 | H2 Not Supported |

| BITGR --> FP | 0.391 *** | 0.039 | 5.337 | H3 Supported |

| BITGS --> ITCs | 0.401 *** | 0.073 | 5.755 | H4 Supported |

| BITGP --> ITCs | 0.088 | 0.057 | 1.589 | H5 Not Supported |

| BITGR --> ITC | 0.404 *** | 0.046 | 6.122 | H6 Supported |

| ITCs --> FP | 0.733 *** | 0.062 | 9.327 | H7 Supported |

| Hypotheses | Baron and Kenny | Bootstrapping Technique a | Sobel Test b | Observed Mediating Type | Label | ||||

|---|---|---|---|---|---|---|---|---|---|

| Effect w/o Med | Effect w/Med | Direct Effect | Indirect Effect | Total Effect | Sobel Test Statistic | Two-Tailed Probability | |||

| BITGS --> ITCs --> FP | 0.412 *** | 0.191 ** | 0.191 ** | 0.207 *** | 0.398 *** | 3.973 | 0.000 | Partial Mediation | H8 Supported |

| BITGP --> ITCs --> FP | 0.114 | 0.072 | 0.072 | 0.046 | 0.118 * | 1.726 | 0.085 | No Mediation | H9 Not Supported |

| BITGR --> ITCs --> FP | 0.391 *** | 0.174 * | 0.174 ** | 0.208 *** | 0.382 *** | 3.964 | 0.000 | Partial Mediation | H10 Supported |

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2022 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Menshawy, I.M.; Basiruddin, R.; Mohdali, R.; Qahatan, N. Board Information Technology Governance Mechanisms and Firm Performance among Iraqi Medium-Sized Enterprises: Do IT Capabilities Matter? J. Risk Financial Manag. 2022, 15, 72. https://doi.org/10.3390/jrfm15020072

Menshawy IM, Basiruddin R, Mohdali R, Qahatan N. Board Information Technology Governance Mechanisms and Firm Performance among Iraqi Medium-Sized Enterprises: Do IT Capabilities Matter? Journal of Risk and Financial Management. 2022; 15(2):72. https://doi.org/10.3390/jrfm15020072

Chicago/Turabian StyleMenshawy, Ibrahim M., Rohaida Basiruddin, Raihana Mohdali, and Nazahan Qahatan. 2022. "Board Information Technology Governance Mechanisms and Firm Performance among Iraqi Medium-Sized Enterprises: Do IT Capabilities Matter?" Journal of Risk and Financial Management 15, no. 2: 72. https://doi.org/10.3390/jrfm15020072

APA StyleMenshawy, I. M., Basiruddin, R., Mohdali, R., & Qahatan, N. (2022). Board Information Technology Governance Mechanisms and Firm Performance among Iraqi Medium-Sized Enterprises: Do IT Capabilities Matter? Journal of Risk and Financial Management, 15(2), 72. https://doi.org/10.3390/jrfm15020072