The Asymmetric Overnight Return Anomaly in the Chinese Stock Market

Abstract

1. Introduction

2. Literature Review

2.1. Studies on Overnight Return

2.2. Overnight Return Anomaly

2.3. Investor Attention and Overnight Return Anomaly

3. Empirical Analysis

3.1. Data

3.2. Analysis of Overnight Return in Chinese Stock Market

3.2.1. Tests for Overnight Return Anomaly

3.2.2. Analysis of the Asymmetry of the Anomaly

3.3. Analysis of the Causes of the Overnight Return Anomaly

3.3.1. Individual Investors’ Limited Attention

3.3.2. Regression Analysis of Attention of Individual Investors

3.4. Further Analysis

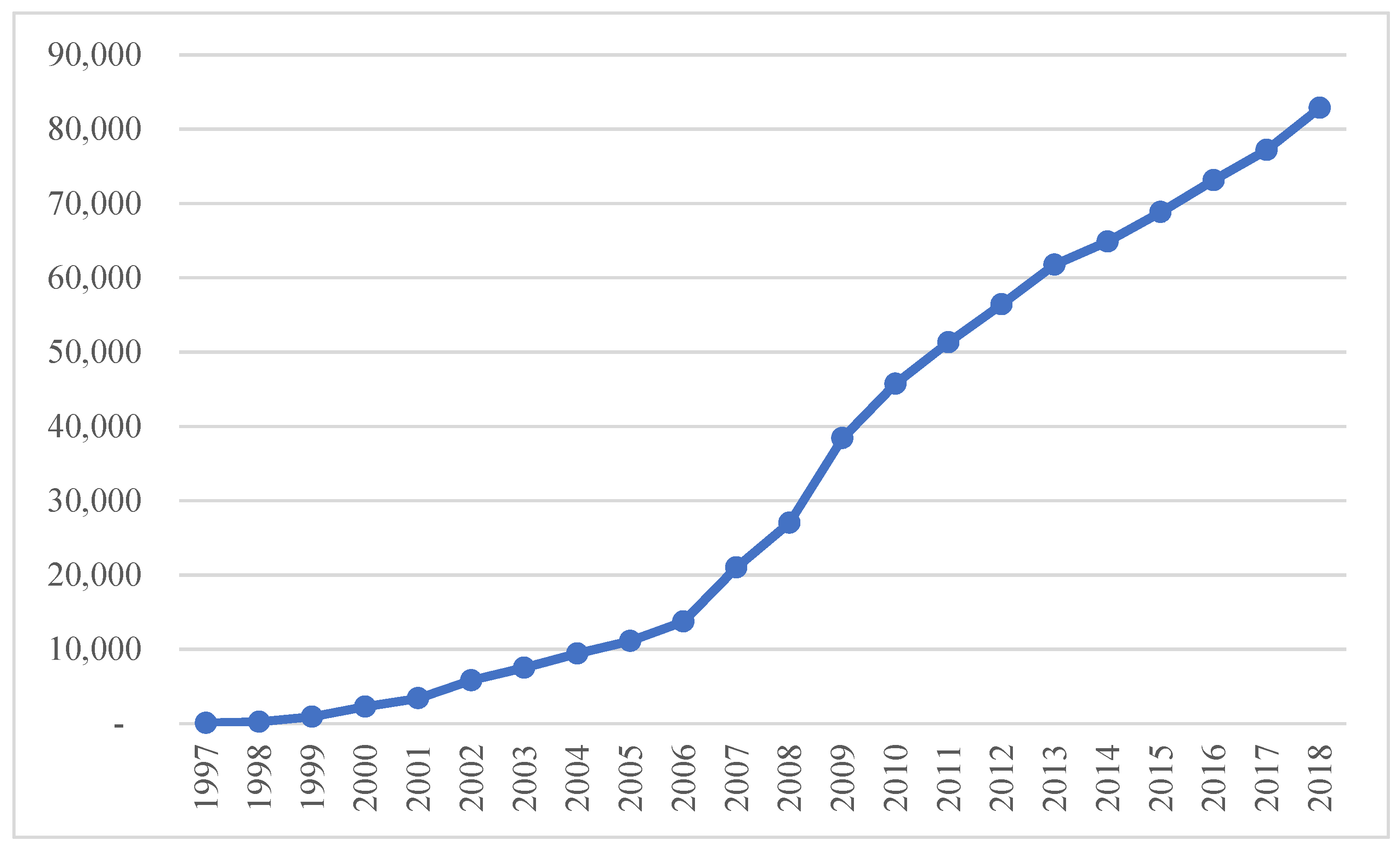

3.4.1. Effect of Widespread Internet Use on Overnight Return of Stock Indexes

3.4.2. Overnight Return by Firm Characteristics

3.4.3. Effect of Internet Development on Individual Investors

4. Conclusions

Author Contributions

Funding

Data Availability Statement

Conflicts of Interest

Appendix A

{kind=link}

| Variable | Description |

|---|---|

| opent | Opening price on day t |

| closet | Closing price on day t |

| returnt | (closet − closet−1)/closet−1 |

| return_overnightt | (opent+1− closet)/closet |

| return_overnightt−1 | (opent − closet−1)/closet−1 |

| return_overnightt−2 | (opent−1− closet−2)/closet−2 |

| return_overnightt−3 | (opent−2− closet−3)/closet−3 |

| dummyt | If returnt > 0, dummyt = 0; returnt < 0, dummyt = 1 |

| post_overnightt | Number of posts on night of trading day t |

| num_netizent | Number of Chinese internet users over the years released by the China Internet Network Information Center |

| Amihudit | Amihud illiquidity for stock i in year t |

| residual_turnoverit | Residual of regression of Amihud illiquidity on turnover |

| BMit | Ratio of book value to market value of stock i in year t |

| sizeit | Market value of stock i in year t |

| ratio_downit | Ratio of number of days with negative returns of stock i to the total number of trading days in year t |

| Code | Name | Country/Region |

|---|---|---|

| AEX | Amsterdam Exchange AEX Index | Netherlands |

| AS30 | Australian Stock Exchange All Ordinaries Index | Australia |

| ATX | Vienna Stock Exchange Austrian Traded Index | Austria |

| BEL20 | Belgium 20 Index | Belgium |

| BVSP | Sao Paulo Bovespa Index | Brazil |

| DJCI | Dow Jones Composite Average Index | USA |

| DJI | Dow Jones Industries Average Index | USA |

| DJSX50E | Dow Jones EURO STOXX 50 Index | USA |

| DWC | Dow Jones Wilshire 5000 Index | USA |

| FCHI | CAC 40 Index | France |

| FTSE | FTSE 100 Index | UK |

| GDAXI | DAX 30 Index | Germany |

| GSPC | S&P 500 Index | USA |

| GSPTSE | S&P/TSX Composite Index | Canada |

| HERMES | Egypt Hermes index | Egypt |

| HSCCI | Hang Seng China-Affiliated Corporations Index | Hong Kong |

| HSCEI | Hang Seng China Enterprises Index | Hong Kong |

| HIS | Hang Seng Index | Hong Kong |

| IBOV | Bovespa index | Brazil |

| JKSE | Indonesia Jakarta Composite Index | Indonesia |

| KLCI | FTSE Bursa Malaysia KLCI Index | Malaysia |

| KLSE | Kuala Lumpur Stock Exchange Index | Malaysia |

| KS11 | Korea Stock Exchange KOSPI Index | South Korea |

| MADX | Madrid Stock Exchange General Index | Spain |

| MCIX | Russia MICEX Stock Market Index | Russia |

| MERVAL | The Argentina Merval Index | Argentina |

| MEXBOL | S&P/BMV IPC Index | Mexico |

| N225 | Nikkei 225 Stock Index | Japan |

| NDX | NASDAQ 100 Index | USA |

| NIFTY | S&P CNX NIFTY Index | India |

| NYA | NYSE Composite Index | USA |

| NZSE50FG | S&P/NZX 50 Index | New Zealand |

| OEX | S&P 100 Index | USA |

| RAY | Russell 3000 Index | USA |

| RIY | Russell 1000 Index | USA |

| RTSI | Russia RTS Index | Russia |

| RTY | Russell 2000 Index | USA |

| SENSEX | S&P BSE SENSEX Index | India |

| SMI | Swiss Market Index | Switzerland |

| STI | FTSE Straits Times Index | Singapore |

| TA100 | The TA-125 Index | Israeli |

| TWII | Taiwan Weighted Index | Taiwan |

| Panel A Granger Causality Test on CSI 300 | |||

| Null Hypothesis: | Obs | F-Statistic | Prob. |

| CSI 300 does not Granger Cause DJI | 3646 | 1.26052 | 0.2836 |

| DJI does not Granger Cause CSI 300 | 1.55010 | 0.2124 | |

| CSI 300 does not Granger Cause GDAXI | 3646 | 4.11302 | 0.0164 |

| GDAXI does not Granger Cause CSI 300 | 1.03259 | 0.3562 | |

| CSI 300 does not Granger Cause NYA | 3646 | 1.80157 | 0.1652 |

| NYA does not Granger Cause CSI 300 | 1.45278 | 0.2341 | |

| CSI 300 does not Granger Cause RAY | 3646 | 1.04629 | 0.3513 |

| RAY does not Granger Cause CSI 300 | 1.03266 | 0.3562 | |

| CSI 300 does not Granger Cause RTY | 3646 | 0.95458 | 0.3851 |

| RTY does not Granger Cause CSI 300 | 0.91070 | 0.4023 | |

| Panel B Granger Causality Test on Shanghai Composite Index | |||

| Null Hypothesis: | Obs | F-Statistic | Prob. |

| SH does not Granger Cause DJI | 3646 | 1.46700 | 0.2308 |

| DJI does not Granger Cause SH | 2.59610 | 0.0747 | |

| SH does not Granger Cause GDAXI | 3646 | 4.52909 | 0.0109 |

| GDAXI does not Granger Cause SH | 0.82271 | 0.4393 | |

| SH does not Granger Cause NYA | 3646 | 1.95545 | 0.1416 |

| NYA does not Granger Cause SH | 2.31752 | 0.0987 | |

| SH does not Granger Cause RAY | 3646 | 1.30585 | 0.2711 |

| RAY does not Granger Cause SH | 1.68997 | 0.1847 | |

| SH does not Granger Cause RTY | 3646 | 1.36520 | 0.2555 |

| RTY does not Granger Cause SH | 1.47632 | 0.2286 | |

| Panel C Granger Causality Test on Shenzhen Composite Index | |||

| Null Hypothesis: | Obs | F-Statistic | Prob. |

| SZ does not Granger Cause DJI | 3646 | 1.27455 | 0.2797 |

| DJI does not Granger Cause SZ | 1.53380 | 0.2159 | |

| SZ does not Granger Cause GDAXI | 3646 | 3.40143 | 0.0334 |

| GDAXI does not Granger Cause SZ | 1.22990 | 0.2924 | |

| SZ does not Granger Cause NYA | 3646 | 1.66056 | 0.1902 |

| NYA does not Granger Cause SZ | 1.35785 | 0.2573 | |

| SZ does not Granger Cause RAY | 3646 | 1.06953 | 0.3433 |

| RAY does not Granger Cause SZ | 0.90384 | 0.4051 | |

| SZ does not Granger Cause RTY | 3646 | 1.27926 | 0.2784 |

| RTY does not Granger Cause SZ | 1.01274 | 0.3633 | |

| 1 | B shares market is lack of liquidity and H shares market represents companies listed in Hongkong stock market. |

| 2 | T + 1 trading rule restricts investors from buying the stocks and selling them on the same day. However, this regulation does not prohibit investors to sell the holding stocks and buy other stocks on the same day. |

| 3 | Guba platform is an online stock forum with most users in China. |

| 4 | As the database has not timely updated all the global indexes, the global indexes including the three main Chinese stock market indexes AEX, ATX, DJI, FCHI, FTSE, GDAXI, GSPTSE, HERMES, HSCCI, HSCEI, JXSE, KLSE, KS11, N225, NDX, NIFTY, NYA, RAY, RTSI, RTY, STI, TA100 and TWII are from 2007 to 2021. The rest of the global indexes are in the period from 2007 to 2017. |

| 5 | Stock illiquidity is defined as the average ratio of the daily absolute return to the trading volume on that day (Amihud 2002). |

| 6 | The number of Chinese internet users (num_netizent) is collected from the statistical reports of the China Internet Network Information Center. |

References

- Abraham, Abraham, and David L. Ikenberry. 1994. The individual investor and the weekend effect. Journal of Financial and Quantitative Analysis 29: 263–77. [Google Scholar] [CrossRef]

- Amihud, Yakov. 2002. Illiquidity and stock returns: Cross-section and time-series effects. Journal of Financial Markets 5: 31–56. [Google Scholar] [CrossRef]

- Barber, Brad M., and Terrance Odean. 2008. All that glitters: The effect of attention and news on the buying behavior of individual and institutional investors. The Review of Financial Studies 21: 785–818. [Google Scholar] [CrossRef]

- Berkman, Henk, Paul D. Koch, Laura Tuttle, and Ying Jenny Zhang. 2012. Paying attention: Overnight returns and the hidden cost of buying at the open. Journal of Financial and Quantitative Analysis 47: 715–41. [Google Scholar] [CrossRef]

- Branch, Ben S., and Aixin James Ma. 2006. The overnight return, one more anomaly. One More Anomaly. Available online: https://papers.ssrn.com/sol3/papers.cfm?abstract_id=937997 (accessed on 29 September 2022).

- Cheema, Muhammad A., Mardy Chiah, and Yimei Man. 2022. Overnight returns, daytime reversals, and future stock returns: Is China different? Pacific-Basin Finance Journal 74: 101809. [Google Scholar] [CrossRef]

- Chen, Jiaqi. 2018. Online Search Frequency, Retail Investor Overreaction, and the Cross-Section of Stock Returns: Evidence from the Chinese Stock Market. Emerging Markets Finance and Trade 54: 3189–208. [Google Scholar] [CrossRef]

- Da, Zhi, Joseph Engelberg, and Pengjie Gao. 2011. In search of attention. The Journal of Finance 66: 1461–99. [Google Scholar] [CrossRef]

- De Bondt, Werner F. M., and Richard H. Thaler. 1987. Further evidence on investor overreaction and stock market seasonality. The Journal of finance 42: 557–81. [Google Scholar] [CrossRef]

- Foster, F. Douglas, and Subramanian Viswanathan. 1993. Variations in trading volume, return volatility, and trading costs: Evidence on recent price formation models. The Journal of Finance 48: 187–211. [Google Scholar] [CrossRef]

- French, Kenneth R., and James M. Poterba. 1991. Investor diversification and international equity markets. American Economic Review 81: 222–26. [Google Scholar]

- Gao, Ya, Xing Han, Youwei Li, and Xiong Xiong. 2019. Overnight momentum, informational shocks, and late informed trading in China. International Review of Financial Analysis 66: 101394. [Google Scholar] [CrossRef]

- Granger, Clive William John, and Oskar Morgenstern. 1970. Predictability of Stock Market Prices. Lexington: Heath Lexington Books, p. 34. [Google Scholar]

- Huang, Bwo-Nung, Chin-Wei Yang, and John Wei-Shan Hu. 2000. Causality and cointegration of stock markets among the United States, Japan and the South China Growth Triangle. International Review of Financial Analysis 9: 281–97. [Google Scholar] [CrossRef]

- Ivković, Zoran, and Scott Weisbenner. 2005. Local does as local is: Information content of the geography of individual investors’ common stock investments. The Journal of Finance 60: 267–306. [Google Scholar] [CrossRef]

- Chan, Kalok, Mark Chockalingam, and Kent W.L. Lai. 2000. Overnight information and intraday trading behavior: Evidence from NYSE cross-listed stocks and their local market information. Journal of Multinational Financial Management 10: 495–509. [Google Scholar] [CrossRef]

- Kaniel, Ron, Gideon Saar, and Sheridan Titman. 2008. Individual investor trading and stock returns. The Journal of Finance 63: 273–310. [Google Scholar] [CrossRef]

- Kelly, Michael A., and Steven P. Clark. 2011. Returns in trading versus non-trading hours: The difference is day and night. Journal of Asset Management 12: 132–45. [Google Scholar] [CrossRef]

- Lee, Charles M. C., Andrei Shleifer, and Richard H. Thaler. 1991. Investor sentiment and the closed-end fund puzzle. The Journal of Finance 46: 75–109. [Google Scholar] [CrossRef]

- Liu, Qingyuan, Hongbo Guo, and Xianhua Wei. 2015. Negative overnight returns: China’s security markets. Procedia Computer Science 55: 980–89. [Google Scholar] [CrossRef]

- Lockwood, Larry J., and Thomas H. McInish. 1990. Tests of stability for variances and means of overnight/intraday returns during bull and bear markets. Journal of Banking & Finance 14: 1243–53. [Google Scholar]

- Malm, Patrick. 2018. Cointegration between the Chinese and US Stock Markets. Master’s thesis, Lund University, Lund, Sweden. Available online: https://lup.lub.lu.se/student-papers/search/publication/8948197 (accessed on 29 September 2022).

- Oldfield, George S., and Richard J. Rogalski. 1980. A theory of common stock returns over trading and non-trading periods. The Journal of Finance 35: 729–51. [Google Scholar] [CrossRef]

- Qiao, Kenan, and Lammertjan Dam. 2020. The overnight return puzzle and the “T + 1” trading rule in Chinese stock markets. Journal of Financial Markets 50: 100534. [Google Scholar] [CrossRef]

- Riedel, Christoph, and Niklas Wagner. 2015. Is risk higher during non-trading periods? The risk trade-off for intraday versus overnight market returns. Journal of International Financial Markets, Institutions and Money 39: 53–64. [Google Scholar] [CrossRef]

- Sicherman, Nachum, George Loewenstein, Duane J. Seppi, and Stephen P. Utkus. 2016. Financial attention. The Review of Financial Studies 29: 863–97. [Google Scholar] [CrossRef]

- Tsiakas, Ilias. 2008. Overnight information and stochastic volatility: A study of European and US stock exchanges. Journal of Banking & Finance 32: 251–68. [Google Scholar]

- Wang, Qin, and Jun Zhang. 2015. Individual investor trading and stock liquidity. Review of Quantitative Finance and Accounting 45: 485–508. [Google Scholar] [CrossRef]

- Yuan, Yu. 2015. Market-wide attention, trading, and stock returns. Journal of Financial Economics 116: 548–64. [Google Scholar] [CrossRef]

- Zhang, Bing. 2020. T + 1 trading mechanism causes negative overnight return. Economic Modelling 89: 55–71. [Google Scholar] [CrossRef]

- Zhou, Xuemei, Qiang Liu, and Shuxin Guo. 2021. Do overnight returns explain firm-specific investor sentiment in China? International Review of Economics & Finance 76: 451–77. [Google Scholar]

| Panel A: Individual stocks | |||

| p | Number of stocks | ||

| p = 0.01 (t < −2.58) | 2490 (67.94%) | ||

| p = 0.05 (t < −1.96) | 2719 (74.19%) | ||

| p = 0.1 (t < −1.56) | 2845 (77.63%) | ||

| Panel B: Market indexes | |||

| CSI 300 Index | Shanghai Composite Index | Shenzhen Component Index | |

| Overnight return | −0.001 *** | 0.000 | −0.000 *** |

| (−6.41) | (0.48) | (−3.29) | |

| Daytime return | 0.001 *** | 0.001 *** | 0.001 *** |

| (4.55) | (3.24) | (2.48) | |

| Panel A: Chinese market indexes | ||||||

| CSI 300 | Shanghai Composite Index | Shenzhen Component Index | ||||

| Overnight return | −0.001 *** | −0.001 *** | −0.001 *** | |||

| (−5.81) | (−7.98) | (−4.46) | ||||

| Daytime return | −0.001 *** | −0.001 *** | −0.001 ** | |||

| (−3.42) | (−4.07) | (−2.92) | ||||

| Panel B: Global market indexes | ||||||

| Group | AEX | AS30 | ATX | BEL20 | BVSP | DJCI |

| Overnight return | 0.0004 ** | 0.001 | 0.0002 | 0.025 ** | −0.006 | −0.123 |

| (2.98) | (0.28) | (0.64) | (1.99) | (−0.98) | (−0.37) | |

| Daytime return | −0.0002 | 0.016 | 0.001 | −0.006 | 0.012 | 0.034 * |

| (−1.02) | (0.94) | (0.33) | (−0.32) | (0.37) | (1.92) | |

| DJI | DJSX50E | DWC | FCHI | FTSE | GDAXI | |

| Overnight return | 0.0001 | 0.124 * | 0.087 | 0.0004 ** | −0.000001 | 0.0004 *** |

| (1.23) | (1.77) | (1.19) | (2.59) | (−0.56) | (3.10) | |

| Daytime return | 0.0002 | −0.131 *** | −0.041 ** | −0.0002 | 0.0001 | −0.00005 |

| (1.43) | (−4.35) | (−2.09) | (−1.04) | (0.61) | (−0.26) | |

| GSPC | GSPTSE | HERMES | HSCCI | HSCEI | HSI | |

| Overnight return | 0.013 *** | 0.0004 *** | −0.0001 | 0.001 *** | 0.007 *** | 0.077 *** |

| (3.69) | (3.07) | (−0.56) | (5.04) | (3.51) | (4.36) | |

| Daytime return | 0.033 * | −0.0001 | 0.0003 | −0.001 *** | −0.001 ** | −0.065 *** |

| (1.75) | (−1.20) | (1.23) | (−3.66) | (−2.83) | (−3.63) | |

| IBOV | JXSE | KLCI | KLSE | KS11 | MADX | |

| Overnight return | 0.001 | 0.0002 ** | 0.001 *** | −0.0000001 | 0.001 *** | 0.027 * |

| (0.31) | (2.59) | (2.66) | (−0.001) | (5.36) | (1.7) | |

| Daytime return | −0.003 | 0.0002 | 0.012 | 0.0001 | −0.0005 ** | −0.035 |

| (−0.10) | (1.13) | (0.53) | (1.18) | (−2.79) | (−1.30) | |

| MCIX | MERVAL | MEXBOL | N225 | NDX | NIFTY | |

| Overnight return | −0.001 | 0.053 *** | 0.006 ** | 0.0004 *** | 0.0003 ** | 0.012 *** |

| (−0.26) | (5.63) | (2.15) | (3.12) | (2.43) | (10.46) | |

| Daytime return | 0.026 | 0.07 | 0.013 | −0.0002 | 0.0004 * | −0.0001 *** |

| (0.91) | (1.6) | (0.66) | (−0.98) | (1.95) | (−4.14) | |

| NYA | NZSE50FG | OEX | RAY | RIY | RTSI | |

| Overnight return | 0.001 | 0.004 ** | 0.014 *** | 0.0001 *** | 0.007 | 0.0005 * |

| (0.91) | (2.47) | (3.6) | (2.84) | (1.11) | (1.74) | |

| Daytime return | −0.000002 | 0.050 *** | 0.031 * | −0.0002 | 0.036 | 0.0001 |

| (−0.01) | (4.11) | (1.65) | (−0.75) | (1.56) | (0.16) | |

| RTY | SENSEX | SMI | STI | TA100 | TWII | |

| Overnight return | 0.0001 ** | 0.137 *** | 0.014 | 0.0002 * | 0.001 *** | 0.001 *** |

| (2.34) | (13.47) | (1.15) | (1.65) | (4.57) | (7.45) | |

| Daytime return | −0.00003 | −0.100 *** | 0.004 | 0.0002 * | 0.0003 ** | 0.001 *** |

| (−0.13) | (−5.23) | (0.22) | (1.60) | (2.59) | (5.06) | |

| Panel A: Overnight return of individual stocks | |||

| p | Number of stocks | ||

| With positive daytime return | p = 0.01 (t < −2.33) | 682 (18.61%) | |

| p = 0.05 (t < −1.65) | 1083 (29.55%) | ||

| p = 0.1 (t < −1.29) | 1299 (35.44%) | ||

| p = 0.01 (t > 2.33) | 320 (8.73%) | ||

| p = 0.05 (t > 1.65) | 571 (15.58%) | ||

| p = 0.1 (t > 1.29) | 733 (20.00%) | ||

| With negative daytime return | p = 0.01 (t < −2.33) | 3361 (91.71%) | |

| p = 0.05 (t < −1.65) | 3573 (97.49%) | ||

| p = 0.1 (t < −1.29) | 3621 (98.80%) | ||

| Panel B: Overnight return of market index | |||

| CSI 300 | Shanghai Composite Index | Shenzhen Component Index | |

| With positive daytime return | −0.000 | 0.001 *** | 0.002 *** |

| (−0.35) | (7.28) | (5.35) | |

| With negative daytime return | −0.002 *** | −0.002 *** | −0.002 *** |

| (−8.16) | (−13.59) | (−10.11) | |

| Panel A CSI 300 | |||||

| CSI 300 | DJI | GDAXI | NYA | RAY | |

| DJI | −0.0132 | ||||

| GDAXI | −0.0139 | −0.0010 | |||

| NYA | −0.0058 | 0.9083 * | −0.0176 | ||

| RAY | −0.0057 | 0.9420 * | −0.0073 | 0.9255 * | |

| RTY | −0.0091 | 0.8327 * | 0.0034 | 0.8453 * | 0.9178 * |

| Panel B Shanghai Composite Index | |||||

| Shanghai Composite Index | DJI | GDAXI | NYA | RAY | |

| DJI | −0.0129 | ||||

| GDAXI | −0.0102 | −0.0010 | |||

| NYA | −0.0085 | 0.9083 * | −0.0176 | ||

| RAY | −0.0083 | 0.9420 * | −0.0073 | 0.9255 * | |

| RTY | −0.0129 | 0.8327 * | 0.0034 | 0.8453 * | 0.9178 * |

| Panel C Shenzhen Composite Index | |||||

| Shenzhen Composite Index | DJI | GDAXI | NYA | RAY | |

| DJI | −0.0098 | ||||

| GDAXI | −0.0194 | −0.0010 | |||

| NYA | −0.0027 | 0.9083 * | −0.0176 | ||

| RAY | −0.0018 | 0.9420 * | −0.0073 | 0.9255 * | |

| RTY | −0.0041 | 0.8327 * | 0.0034 | 0.8453 * | 0.9178 * |

| Volume | Posts | Reads | Comments |

|---|---|---|---|

| Average | 1625.129 | 2,933,245.167 | 4818.833 |

| Std. Dev | 1684.269 | 1,872,821.367 | 3087.082 |

| Group | Posts | Reads | Comments |

|---|---|---|---|

| With positive daytime return | 417.986 | 1,867,849.691 | 3173.755 |

| With negative daytime return | 745.864 | 2,481,500.738 | 4161.267 |

| Negative-Positive | 327.878 *** | 613,651.047 *** | 987.515 *** |

| (8.55) | (5.26) | (4.03) |

| Variables | Overnight × Dummy | Overnight × Dummy |

|---|---|---|

| intercept | 0.004 * | 0.041 |

| (1.80) | (0.15) | |

| post_overnightt | −0.023 *** | −0.188 *** |

| (−6.41) | (−4.53) | |

| return_overnightt−1 | −0.103 ** | |

| (−2.44) | ||

| return_overnightt−2 | −0.139 *** | |

| (−3.68) | ||

| return_overnightt−3 | 0.089 ** | |

| (2.37) | ||

| returnt | 0.067 *** | |

| (3.15) | ||

| Observations | 411 | 411 |

| Adj R-square | 0.089 | 0.151 |

| Variables | Overnight Return | Variables | Overnight Return |

|---|---|---|---|

| Regression 2 | Regression 3 | ||

| intercept | 0.003 | intercept | −0.006 ** |

| (1.00) | (−2.30) | ||

| dummyt | 0.000 | dummyt | −0.001 *** |

| (−0.85) | (−2.77) | ||

| post_overnightt | −0.246 *** | return_overnightt−1 | 0.025 |

| (−4.87) | (0.50) | ||

| return_overnightt−1 | −0.021 | return_overnightt−2 | −0.072 |

| (−0.42) | (−1.48) | ||

| return_overnightt−2 | −0.104 ** | return_overnightt−3 | 0.169 *** |

| (−2.18) | (3.47) | ||

| return_overnightt−3 | 0.131 *** | ||

| (2.72) | |||

| Observations | 411 | Observations | 411 |

| Adj. R-square | 0.096 | Adj R-square | 0.045 |

| Period | Shanghai Composite Index | Shenzhen Component Index | Dow Jones Industries Average Index |

|---|---|---|---|

| Before 2001 | 0.0016 *** | 0.0002 | −0.0001 ** |

| (3.02) | (0.70) | (−2.15) | |

| After 2001 | −0.0008 *** | −0.0006 *** | 0.00002 |

| (−7.36) | (−5.59) | (0.43) |

| Panel A: Sort by size | ||||

| Group | Mean | Standard deviation | Observations | T-statistics |

| 1 (low) | −0.0015 | 0.0028 | 288 | −8.9730 |

| 2 | −0.0013 | 0.0026 | 288 | −8.6607 |

| 3 | −0.0012 | 0.0025 | 288 | −7.8779 |

| 4 | −0.0010 | 0.0024 | 288 | −6.9647 |

| 5 (high) | −0.0008 | 0.0024 | 288 | −5.7492 |

| High-Low (5–1) | 0.0007 | 5.0526 | ||

| Panel B: Sort by Amihud illiquidity | ||||

| Group | Mean | Standard deviation | Observations | T-statistics |

| 1 (low) | −0.0013 | 0.0025 | 288 | −8.6306 |

| 2 | −0.0013 | 0.0025 | 288 | −9.0446 |

| 3 | −0.0012 | 0.0025 | 288 | −8.4675 |

| 4 | −0.0012 | 0.0025 | 288 | −8.0994 |

| 5 (high) | −0.0007 | 0.0031 | 288 | −3.8335 |

| High-Low (5–1) | 0.0006 | 5.1178 | ||

| Panel C: Sort by Turnover | ||||

| Group | Mean | Standard deviation | Observations | T-statistics |

| 1 (low) | −0.0006 | 0.0021 | 288 | −4.8041 |

| 2 | −0.0008 | 0.0023 | 288 | −6.2700 |

| 3 | −0.0011 | 0.0025 | 288 | −7.2690 |

| 4 | −0.0014 | 0.0027 | 288 | −8.6267 |

| 5 (high) | −0.0019 | 0.0032 | 288 | −10.2974 |

| High-Low (5–1) | −0.0013 | −6.9789 | ||

| Variables | Overnight Return | ||

|---|---|---|---|

| (1) | (2) | (3) | |

| intercept | −0.001 *** | 0.0002 | 0.0003 ** |

| (−45.44) | (1.54) | (1.97) | |

| num_netizent | −0.189 *** | −0.071 *** | −0.075 *** |

| (−17.44) | (−8.25) | (−9.26) | |

| Amihudit | 0.001 *** | 0.001 *** | |

| (28.37) | (29.50) | ||

| residual_turnoverit | −0.002 *** | −0.002 *** | |

| (−31.18) | (−33.37) | ||

| BMit | −0.001 *** | −0.001 *** | |

| (−12.10) | (−5.78) | ||

| sizeit | −0.036 | 0.034 | |

| (−0.78) | (0.93) | ||

| ratio_downit | −0.003 *** | −0.003 *** | |

| (−11.04) | (−12.53) | ||

| Fixed effect | Yes | Yes | No |

| Observation | 18,069 | 14,509 | 14,509 |

| Number of groups | 2105 | 1792 | 1792 |

| Adj. R-square | 0.013 | 0.089 | 0.112 |

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2022 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

An, Y.; Huang, L.; Li, Y. The Asymmetric Overnight Return Anomaly in the Chinese Stock Market. J. Risk Financial Manag. 2022, 15, 534. https://doi.org/10.3390/jrfm15110534

An Y, Huang L, Li Y. The Asymmetric Overnight Return Anomaly in the Chinese Stock Market. Journal of Risk and Financial Management. 2022; 15(11):534. https://doi.org/10.3390/jrfm15110534

Chicago/Turabian StyleAn, Yahui, Lin Huang, and Youwei Li. 2022. "The Asymmetric Overnight Return Anomaly in the Chinese Stock Market" Journal of Risk and Financial Management 15, no. 11: 534. https://doi.org/10.3390/jrfm15110534

APA StyleAn, Y., Huang, L., & Li, Y. (2022). The Asymmetric Overnight Return Anomaly in the Chinese Stock Market. Journal of Risk and Financial Management, 15(11), 534. https://doi.org/10.3390/jrfm15110534