Use of Derivatives and Market Valuation of the Banking Sector: Evidence from the European Union

Abstract

:1. Introduction

2. Theoretical Background

2.1. Derivatives, Risk Management, and Firm Value

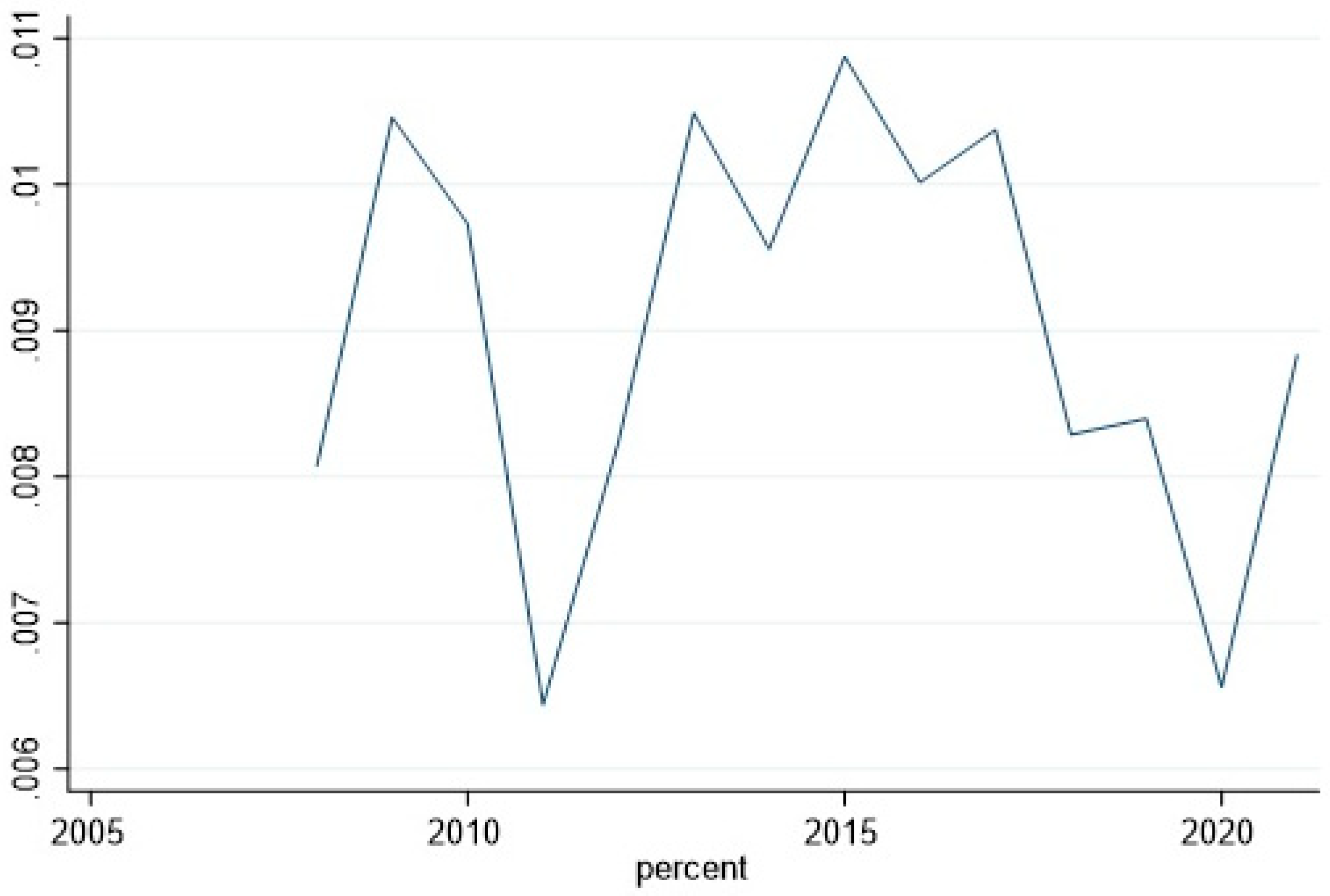

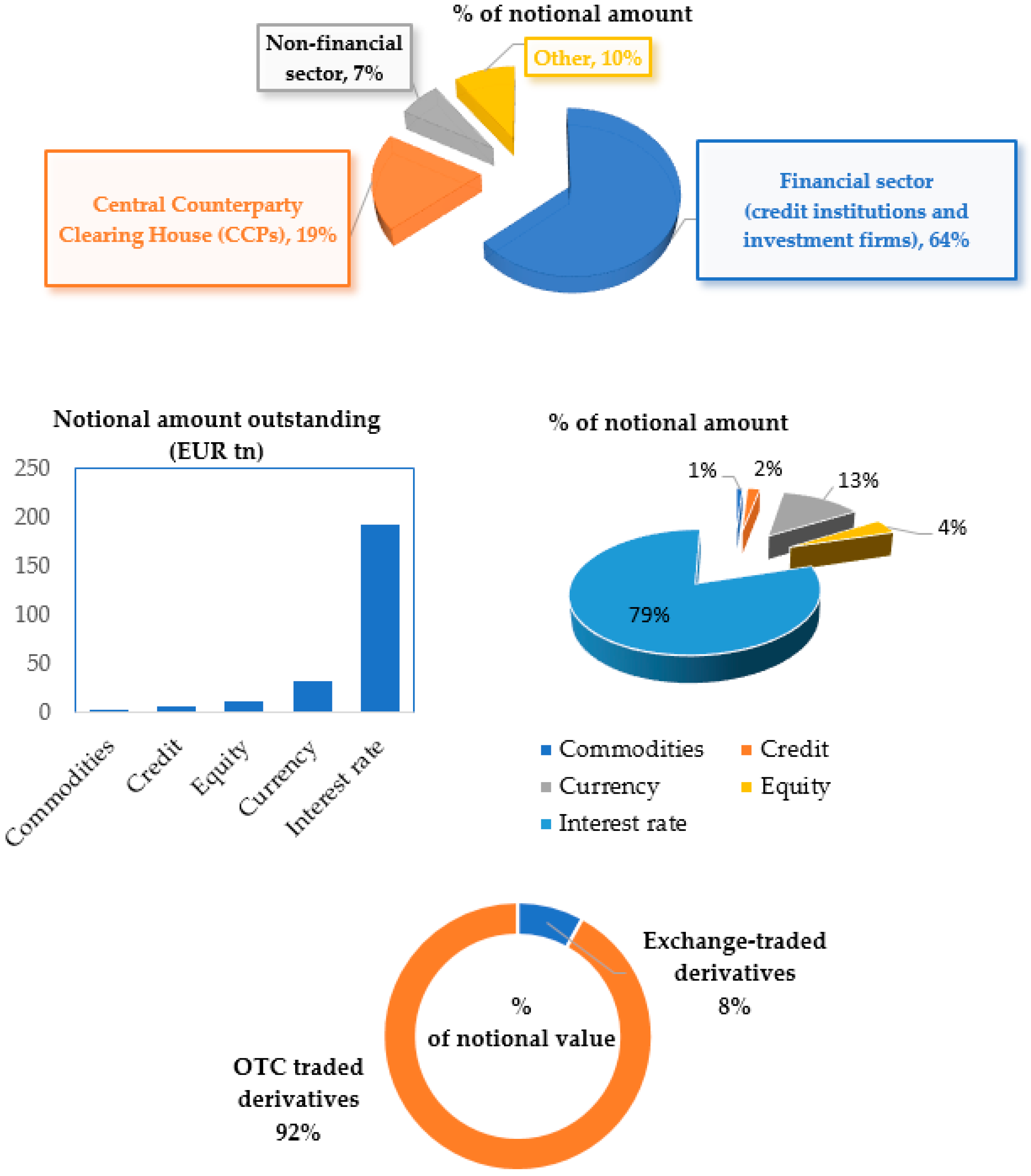

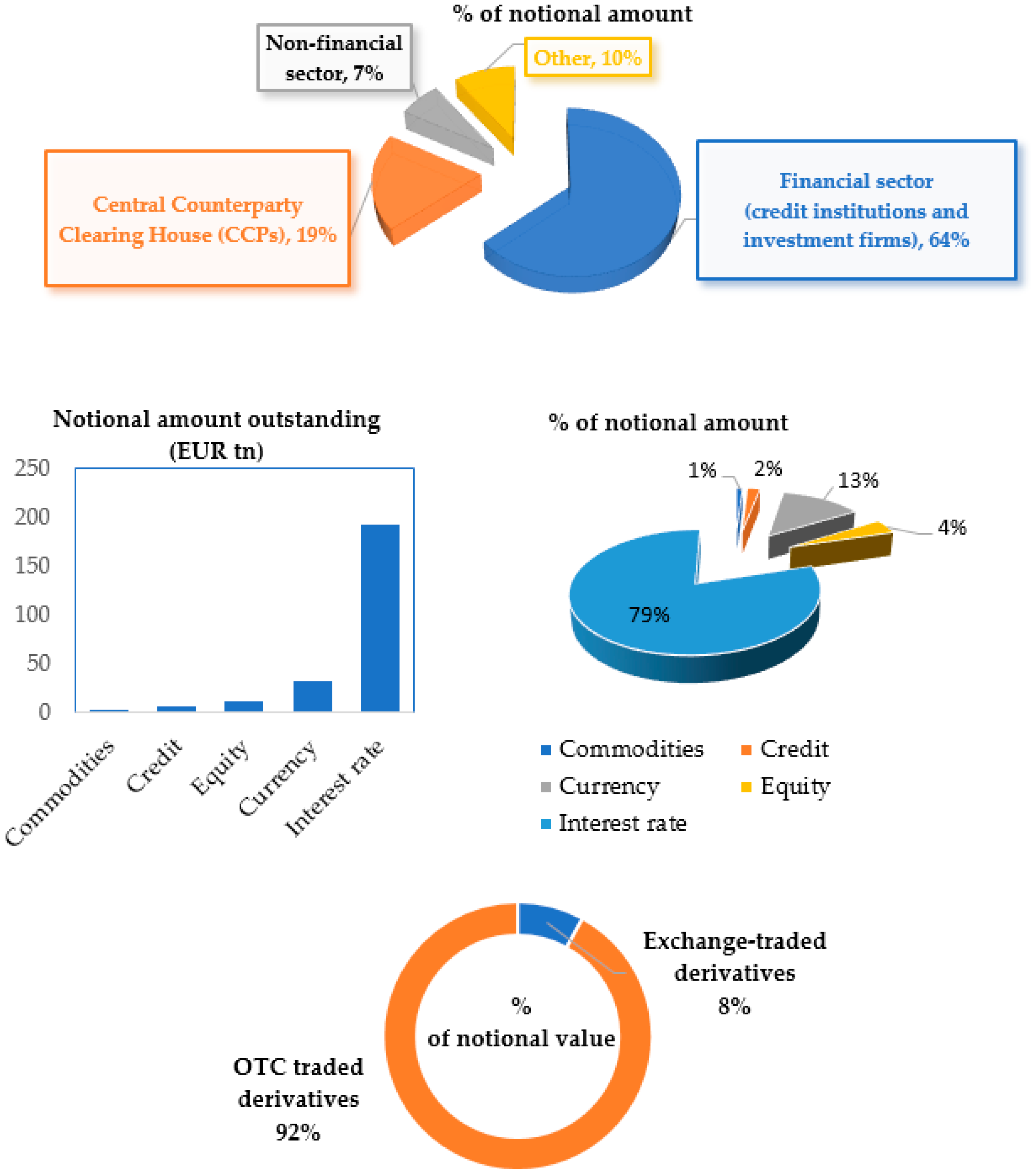

2.2. The Derivatives Market at the European Level

3. Empirical Background

3.1. Data and Variables Specification

3.2. Methodology

3.3. Results and Interpretation

4. Conclusions

Author Contributions

Funding

Institutional Review Board Statement

Informed Consent Statement

Data Availability Statement

Conflicts of Interest

Appendix A

{kind=link}

{kind=link}

| PBR | ROA | DAP | LTA | ROE | PER | NPL | NLTA | CAR | |

|---|---|---|---|---|---|---|---|---|---|

| PBR | 1 | ||||||||

| ROA | 0.5129 | 1 | |||||||

| DAP | 0.0088 | 0.0289 | 1 | ||||||

| LTA | −0.2021 | −0.3788 | −0.1016 | 1 | |||||

| ROE | 0.5644 | 0.8091 | 0.0536 | −0.204 | 1 | ||||

| PER | 0.0531 | −0.15 | −0.0036 | 0.0569 | −0.1916 | 1 | |||

| NPL | 0.0441 | 0.1298 | −0.0014 | −0.1915 | 0.0173 | 0.1398 | 1 | ||

| NLTA | −0.2014 | 0.0042 | 0.0076 | −0.2181 | −0.0843 | −0.0629 | −0.0505 | 1 | |

| CAR | 0.0498 | 0.5485 | −0.0051 | −0.5753 | 0.1317 | −0.0873 | 0.2346 | 0.1769 | 1 |

| VARIABLES | POLS | FE | RE |

|---|---|---|---|

| DAP | −0.0519 *** | −0.0541 *** | −0.0519 *** |

| (0.0159) | (0.0166) | (0.0159) | |

| LTA | −0.0980 *** | −0.164 ** | −0.0980 *** |

| (0.0299) | (0.0822) | (0.0299) | |

| ROE | 2.055 *** | 1.477 ** | 2.055 *** |

| (0.726) | (0.590) | (0.726) | |

| PER | 0.0652 | 0.0283 | 0.0652 |

| (0.0795) | (0.0594) | (0.0795) | |

| NPL | −0.557 ** | −0.821 *** | −0.557 ** |

| (0.276) | (0.296) | (0.276) | |

| NLTA | 0.00341 | 0.443 * | 0.00341 |

| (0.256) | (0.236) | (0.256) | |

| CAR | 0.147 | 0.896 | 0.147 |

| (1.064) | (1.073) | (1.064) | |

| LPBR | |||

| Constant | 2.444 *** | 3.334 ** | 2.444 *** |

| (0.667) | (1.480) | (0.667) | |

| Observations | 1151 | 1151 | 1151 |

| Number of companies | 120 | 120 | 120 |

| 0.2126 | 0.0771 | 0.2126 | |

| Hausman p-value | 0.0000 | ||

| BP LM | 0.0000 |

| VARIABLES | POLS | FE | RE |

|---|---|---|---|

| DAP | −0.0199 | −0.0228 | −0.0199 |

| (0.0203) | (0.0207) | (0.0203) | |

| GFC*DAP | −0.0875 ** | −0.0839 * | −0.0875 ** |

| (0.0418) | (0.0437) | (0.0418) | |

| GFC dummy | 0.0587 | 0.0319 | 0.0587 |

| (0.0457) | (0.0431) | (0.0457) | |

| LTA | −0.0934 *** | −0.163 * | −0.0934 *** |

| (0.0292) | (0.0825) | (0.0292) | |

| ROE | 2.070 *** | 1.499 ** | 2.070 *** |

| (0.714) | (0.575) | (0.714) | |

| PER | 0.0622 | 0.0252 | 0.0622 |

| (0.0785) | (0.0587) | (0.0785) | |

| NPLA | −0.540 * | −0.827 ** | −0.540 * |

| (0.287) | (0.318) | (0.287) | |

| NLTA | 0.00591 | 0.451 * | 0.00591 |

| (0.259) | (0.239) | (0.259) | |

| CAR | 0.0246 | 0.617 | 0.0246 |

| (1.102) | (1.114) | (1.102) | |

| LPBR | |||

| Constant | 2.363 *** | 3.327 ** | 2.363 *** |

| (0.672) | (1.511) | (0.672) | |

| Observations | 1151 | 1151 | 1151 |

| Number of companies | 120 | 120 | 120 |

| 0.2244 | 0.0818 | 0.2244 | |

| Hausman p-value | 0.0000 | ||

| BP LM | 0.0000 |

References

- Acharya, Viral V., and Matthew Richardson. 2009. Causes of the financial crisis. Critical Review. A Journal of Politics and Society 21: 195–210. [Google Scholar] [CrossRef]

- Ahmed, Rida. 2021. A Study on the Impact of Derivatives on Bank Risk and Profitability. Available online: https://papers.ssrn.com/sol3/papers.cfm?abstract_id=3799045 (accessed on 15 August 2022).

- Alayannis, George, and Eli Ofek. 2001. Exchange rate exposure, hedging, and the use of foreign currency derivatives. Journal of International Money and Finance 20: 273–96. [Google Scholar] [CrossRef] [Green Version]

- Alvarez, Javier, and Manuel Arellano. 2022. Robust likelihood estimation of dynamic panel data models. Journal of Econometrics 226: 21–61. [Google Scholar] [CrossRef]

- Ashraf, Dawood, Yener Altunbas, and John Goddard. 2007. Who transfers credit risk? Determinants of the use of credit derivatives by large US banks. The European Journal of Finance 13: 483–500. [Google Scholar] [CrossRef]

- Bachiller, Patricia, Sabri Boubaker, and Salma Mefteh-Wali. 2021. Financial derivatives and firm value. What have we learned? Finance Research Letters 39: 101573. [Google Scholar] [CrossRef]

- Bao, Yong, and Xuewen Yu. 2022. Indirect inference estimation of dynamic panel data models. Journal of Econometrics. in press. [Google Scholar] [CrossRef]

- Bartram, Söhnke M., Gregory W. Brown, and Frank R. Fehle. 2009. International evidence on financial derivatives usage. Financial Management 38: 185–206. [Google Scholar] [CrossRef]

- Bartram, Söhnke M., Gregory W. Brown, and Jennifer Conrad. 2011. The effects of derivatives on firm risk and value. The Journal of Financial and Quantitative Analysis 46: 967–99. [Google Scholar] [CrossRef] [Green Version]

- Bazih, Jad H., and Dieter Vanwalleghem. 2021. Deriving value or risk? Determinants and the impact of emerging market banks’ derivative usage. Research in International Business and Finance 56: 101379. [Google Scholar] [CrossRef]

- BIS. 2021. Statistics. Available online: https://www.bis.org/statistics/about_derivatives_stats.htm?m=2639 (accessed on 15 August 2022).

- Brewer, Elijah, William E. Jackson, and James T. Moser. 1996. Alligators in the swamp: The impact of derivatives on the financial performance of depository institutions. Journal of Money, Credit and Banking 28: 482–97. [Google Scholar]

- Brewer, Gene A., Sally Coleman Selden, and Rex L. Facer. 2000. Individual conceptions of public service motivation. Public Administration Review 60: 204–14. [Google Scholar] [CrossRef]

- Brunnermeier, Markus K., Gang N. Dong, and Darius Palia. 2020. Banks’ noninterest income and systemic risk. The Review of Corporate Finance Studies 9: 229–55. [Google Scholar] [CrossRef]

- Chang, Chuang C., Keng Y. Ho, and Yu J. Hsiao. 2018. Derivatives usage for banking industry: Evidence from the European markets. Review of Quantitative Finance and Accounting 51: 921–41. [Google Scholar] [CrossRef]

- Choi, Wonho W., Jinyong Kim, and Mingook Kim. 2016. Derivatives holdings and market values of U.S. bank holding companies. Applied Economics 48: 4747–57. [Google Scholar]

- Colquitt, Lee L., and Robert E. Hoyt. 1997. Determinants of Corporate Hedging Behavior: Evidence from the Life Insurance Industry. Journal of Risk and Insurance 64: 649–71. [Google Scholar] [CrossRef]

- Cummins, David J., Richard D. Phillips, and Stephen D. Smith. 1997. Corporate Hedging in the Insurance Industry. North American Actuarial Journal 1: 13–40. [Google Scholar] [CrossRef]

- Cyree, Ken B., Pinghsun Huang, and James T. Lindley. 2012. The economic consequences of banks’ derivatives use in good times and bad times. Journal of Financial Services Research 41: 121–44. [Google Scholar] [CrossRef]

- De Ceuster, Marc, Liam Flanagan, Allan Hodgson, and Mohammad I. Tahir. 2003. Determinants of derivative usage in the life and general insurance industry: The Australian evidence. Review of Pacific Basin Financial Markets and Policies 6: 405–31. [Google Scholar] [CrossRef]

- De Marzo, Peter, and Darrell Duffie. 1995. Corporate incentives for hedging and hedge accounting. The Review of Financial Studies 8: 743–71. [Google Scholar] [CrossRef]

- Deng, Kebin, Wenxia Ge, and Jing He. 2021. Inside debt and shadow banking. Journal of Corporate Finance 69: 102038. [Google Scholar] [CrossRef]

- Egly, Peter V., and Jun Sun. 2014. Trading income and bank charter value during the financial crisis: Does derivative dealer designation matter? The Quarterly Review of Economics and Finance 54: 355–70. [Google Scholar] [CrossRef]

- ESMA. 2021. EU Derivatives Markets. ESMA Annual Statistical Report. Available online: https://www.esma.europa.eu/sites/default/files/library/esma50-165-2001_emir_asr_derivatives_2021.pdf (accessed on 15 August 2022).

- Froot, Kenneth A., David S. Scharfstein, and Jeremy C. Stein. 1993. Risk Management: Coordinating Corporate Investment and Financing Policies. The Journal of Finance 48: 1629–58. [Google Scholar] [CrossRef]

- Fung, Hung G., Min M. Wen, and Gaiyan Zhang. 2012. How Does the Use of Credit Default Swaps Affect Firm Risk and Value? Evidence from US Life and Property/Casualty Insurance Companies. Financial Management 41: 979–1007. [Google Scholar] [CrossRef]

- Ghaeli, Reza M. 2017. Price-to-earnings ratio: A state-of-art review. Accounting 3: 131–36. [Google Scholar] [CrossRef]

- Graham, John R., and Daniel A. Rogers. 2002. Do Firms Hedge in Response to Tax Incentives? The Journal of Finance 57: 815–39. [Google Scholar] [CrossRef] [Green Version]

- Guay, Wayne R. 1999. The impact of derivatives on firm risk: An empirical examination of new derivative users. Journal of Accounting and Economics 26: 319–51. [Google Scholar] [CrossRef]

- Hentschel, Ludger, and S.P. Kothari. 2001. Are corporations reducing or taking risks with derivatives? Journal of Financial and Quantitative Analysis 36: 93–118. [Google Scholar] [CrossRef]

- Huan, Xing, and Antonio Parbonetti. 2019. Financial derivatives and bank risk: Evidence from eighteen developed markets. Accounting and Business Research 49: 847–74. [Google Scholar] [CrossRef]

- Jaffe, Dwight. 2003. The Interest Rate Risk of Fannie Mae and Freddy Mac. Journal of Financial Services Research 24: 5–29. [Google Scholar] [CrossRef]

- Khediri, Ben K. 2010. Do investors really value derivatives use? Empirical evidence from France. Journal of Risk Finance 11: 62–74. [Google Scholar] [CrossRef]

- Kim, Sung H., and Gary D. Koppenhaver. 1993. An Empirical Analysis of Bank Interest Rate Swaps. Journal of Financial Services Research 7: 57–72. [Google Scholar] [CrossRef]

- Koppenhaver, Gary D. 1985. Bank funding risks, risk aversion, and the choice of futures hedging instrument. The Journal of Finance 40: 241–55. [Google Scholar] [CrossRef]

- Koski, Jennifer L., and Jeffrey Pontiff. 1999. How are derivatives used? Evidence from the mutual fund industry. The Journal of Finance 54: 791–816. [Google Scholar] [CrossRef]

- Leland, Hayne E. 1998. Agency Costs, Risk Management, and Capital Structure. The Journal of Finance 53: 1213–43. [Google Scholar] [CrossRef]

- Li, Shaofang, and Matej Marinč. 2014. The use of financial derivatives and risks of U.S. bank holding companies. International Review of Financial Analysis 35: 46–71. [Google Scholar] [CrossRef]

- Mayordomo, Sergio, Maria Rodriguez-Moreno, and Juan Ignacio Peña. 2014. Derivatives holdings and systemic risk in the US banking sector. Journal of Banking & Finance 45: 84–104. [Google Scholar]

- Minton, Bernadette, René Stulz, and Rohan Williamson. 2009. How Much Do Banks Use Credit Derivatives to Hedge Loans? Journal of Financial Services Research 35: 1–31. [Google Scholar] [CrossRef]

- Modigliani, Franco, and Merton H. Miller. 1958. The cost of capital, corporation finance and the theory of investment. American Economic Review 48: 261–97. [Google Scholar]

- Morrison, Alan D. 2005. Credit derivatives, disintermediation, and investment decisions. The Journal of Business 78: 621–48. [Google Scholar] [CrossRef]

- Paletta, Damian, and Scott Patterson. 2010. Deal near on Derivatives. Wall Street Journal. April 26. Available online: https://www.wsj.com/articles/SB10001424052748703441404575206252252365076 (accessed on 15 August 2022).

- Purnanandam, Amiyatosh. 2007. Interest Rate Derivatives at Commercial Banks: An Empirical Investigation. Journal of Monetary Economics 54: 1769–808. [Google Scholar] [CrossRef]

- Reichert, Alan, and Yih W. Shyu. 2003. Derivative activities and the risk of international banks: A market index and VaR approach. International Review of Financial Analysis 12: 489–511. [Google Scholar] [CrossRef]

- Ross, Stephen A. 1977. The Determination of Financial Structure: The incentive-signaling approach. The Bell Journal of Economics 8: 23–40. [Google Scholar] [CrossRef] [Green Version]

- Said, Ali. 2011. Does the use of derivatives impact bank performance? A case study of relative performance during 2002–2009. Middle Eastern Finance and Economics Journal 11: 77–88. [Google Scholar]

- Schrand, Catherine, and Haluk Unal. 1998. Hedging and coordinated risk management: Evidence from thrift conversions. The Journal of Finance 53: 979–1013. [Google Scholar] [CrossRef] [Green Version]

- Shanker, Latha. 1996. Derivatives usage and interest risk of large banking firms. Journal of Futures Market 16: 459–74. [Google Scholar] [CrossRef]

- Shyu, Yih W., and Alan K. Reichert. 2002. The determinants of derivative use by U.S. and foreign banks. Research in Finance 19: 143–72. [Google Scholar]

- Sinkey, Joseph F., and David A. Carter. 2000. Evidence on the financial characteristics of banks that do and do not use derivatives. Quarterly Review of Economics and Finance 40: 431–49. [Google Scholar] [CrossRef]

- Smith, Clifford W., and René Stulz. 1985. The determinants of firms’ hedging policies. Journal of Financial and Quantitative Analysis 20: 391–405. [Google Scholar] [CrossRef]

- Whidbee, David A., and Mark Wohar. 1999. Derivatives activities and management incentives in the banking industry. Journal of Corporate Finance 5: 251–76. [Google Scholar] [CrossRef]

| Sample | Number of Companies |

|---|---|

| Sector: Financial service activities, except insurance and pension funding Location: European Union countries and the United Kingdom Status of the company: Active, publicly listed companies | 5744 |

| Companies with known values of derivative assets over the period of analysis | 155 |

| Companies with no less than five years of missing reports of derivative holdings | 120 |

| Type of Variable | Variables | Computation Description | Abbreviation |

|---|---|---|---|

| Dependent variable | Firm value | Price-to-Book (P/B) ratio | PBR |

| Interest variable | Derivatives holdings | % annual change in derivatives’ assets | DAP |

| Control variables | Size | Log (total assets) | LTA |

| Profitability | Return on equity | ROE | |

| Expectations of the market | Price-to-earnings ratio | PER | |

| Bank risk | Non-performing loans/gross loans | NPL | |

| Liquidity performance | Net loans/total assets | NLTA | |

| Financial condition | Book equity/total assets | CAR |

| Variable | Mean | Std. Dev. | Minimum | Maximum | Observations |

|---|---|---|---|---|---|

| PBR | 0.9380 | 0.9100 | −6.122 | 8.559 | 1527 |

| DAP | 0.2283 | 1.0917 | −1.0000 | 9.9091 | 1559 |

| LTA | 17.0013 | 2.0654 | 12.5901 | 21.6919 | 1696 |

| ROE | 0.0537 | 0.3039 | −9.9230 | 2.0029 | 1695 |

| PER | 0.1453 | 0.2656 | 0.0016 | 6.6178 | 1329 |

| NPL | 0.0838 | 0.1066 | 0.0000 | 0.9698 | 1511 |

| NLTA | 0.5762 | 0.1893 | 0.0001 | 0.9014 | 1616 |

| CAR | 0.1226 | 0.1372 | −0.0393 | 0.9675 | 1696 |

| VARIABLES | GMM | ||

|---|---|---|---|

| (1) | (2) | (3) | |

| DAP | −0.167 *** | −0.142 *** | −0.142 *** |

| (0.00279) | (0.00361) | (0.0381) | |

| LTA | −0.160 *** | −0.160 ** | |

| (0.0115) | (0.0779) | ||

| ROE | 3.484 *** | 3.484 ** | |

| (0.0493) | (1.443) | ||

| PER | 0.188 *** | 0.188 | |

| (0.0211) | (0.180) | ||

| NPL | 3.578 | 3.578 | |

| (0.0885) | (1.479) | ||

| NLTA | −0.966 *** | −0.966 * | |

| (0.0790) | (0.503) | ||

| CAR | −7.888 *** | −7.888 ** | |

| (0.276) | (3.933) | ||

| LPBR | 0.496 *** | 0.467 *** | 0.467 *** |

| (0.00271) | (0.00624) | (0.0500) | |

| Constant | 0.457 *** | 4.005 *** | 4.005 *** |

| (0.00511) | (0.197) | (1.407) | |

| Observations | 1072 | 1072 | 1072 |

| Number of companies | 119 | 119 | 119 |

| Hansen p-value | 0.0957 | 0.2499 | 0.2499 |

| VARIABLES | GMM | ||

|---|---|---|---|

| (1) | (2) | (3) | |

| DAP | −0.134 *** | −0.113 *** | −0.113 *** |

| (0.00281) | (0.00329) | (0.0397) | |

| GFC*DAP | −0.415 *** | −0.353 *** | −0.353 * |

| (0.0349) | (0.0614) | (0.214) | |

| GFC dummy | 0.0984 *** | 0.0835 *** | 0.0835 |

| (0.0133) | (0.0169) | (0.0657) | |

| LTA | −0.0913 *** | −0.0913 | |

| (0.00981) | (0.0746) | ||

| ROE | 3.275 *** | 3.275 ** | |

| (0.0473) | (1.460) | ||

| PER | 0.146 *** | 0.146 | |

| (0.0196) | (0.173) | ||

| NPL | 3.785 | 3.785 | |

| (0.0777) | (1.532) | ||

| NLTA | −1.407 *** | −1.407 *** | |

| (0.0509) | (0.480) | ||

| CAR | −5.001 *** | −5.001 | |

| (0.254) | (4.065) | ||

| LPBR | 0.501 *** | 0.469 *** | 0.469 *** |

| (0.00283) | (0.00829) | (0.0513) | |

| Constant | 0.437 *** | 2.801 *** | 2.801 ** |

| (0.00541) | (0.186) | (1.323) | |

| Observations | 1072 | 1072 | 1072 |

| Number of companies | 119 | 119 | 119 |

| Hansen p-value | 0.0643 | 0.1703 | 0.1703 |

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2022 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Miloș, M.C.; Miloș, L.R. Use of Derivatives and Market Valuation of the Banking Sector: Evidence from the European Union. J. Risk Financial Manag. 2022, 15, 501. https://doi.org/10.3390/jrfm15110501

Miloș MC, Miloș LR. Use of Derivatives and Market Valuation of the Banking Sector: Evidence from the European Union. Journal of Risk and Financial Management. 2022; 15(11):501. https://doi.org/10.3390/jrfm15110501

Chicago/Turabian StyleMiloș, Marius Cristian, and Laura Raisa Miloș. 2022. "Use of Derivatives and Market Valuation of the Banking Sector: Evidence from the European Union" Journal of Risk and Financial Management 15, no. 11: 501. https://doi.org/10.3390/jrfm15110501

APA StyleMiloș, M. C., & Miloș, L. R. (2022). Use of Derivatives and Market Valuation of the Banking Sector: Evidence from the European Union. Journal of Risk and Financial Management, 15(11), 501. https://doi.org/10.3390/jrfm15110501