Bank Risk Capital and Its Effectiveness in Selected Euro Area Banking Sectors

Abstract

:1. Introduction

2. Literature Review

- tightening of capital requirements—strengthening the size and quality of banks’ equity,

- implementation of liquidity requirements—which did not occur in previous Basel Accords,

- determination of the maximum banks’ leverage—the leverage ratio.

- minimum capital requirement—the Pillar I,

- additional capital requirement—Pillar II,

- capital buffers.

- the new supervisory regulations and prudential norms implemented in financial institutions’ operations, spread over time (until 2019) and constantly modified (Basel Committee on Banking Supervision 2010; Jumreornvong et al. 2018; Directive 2013; Regulation 2013),

- a wide objective and subjective scope of regulations, not encountered in the financial system until the global financial crisis,

- low, close to zero and sometimes even negative interest rate policy of central banks (Pyka et al. 2019; Angrick and Nemoto 2017; Arseneau 2017; Cœuré 2014; Dong and Wen 2017; International Monetary Fund 2017; Jobst and Lin 2016; Pyka and Nocoń 2017, 2019),

- strong concentration of impact of various regulatory, economic and behavioral factors on banking activities effectiveness (Gómez-Fernández-Aguado et al. 2018; Erfani and Vasigh 2018),

- a permanent decline in efficiency of credit institutions, observed in their operating activities.

3. Materials and Methods

4. Results

5. Discussion and Conclusions

- −

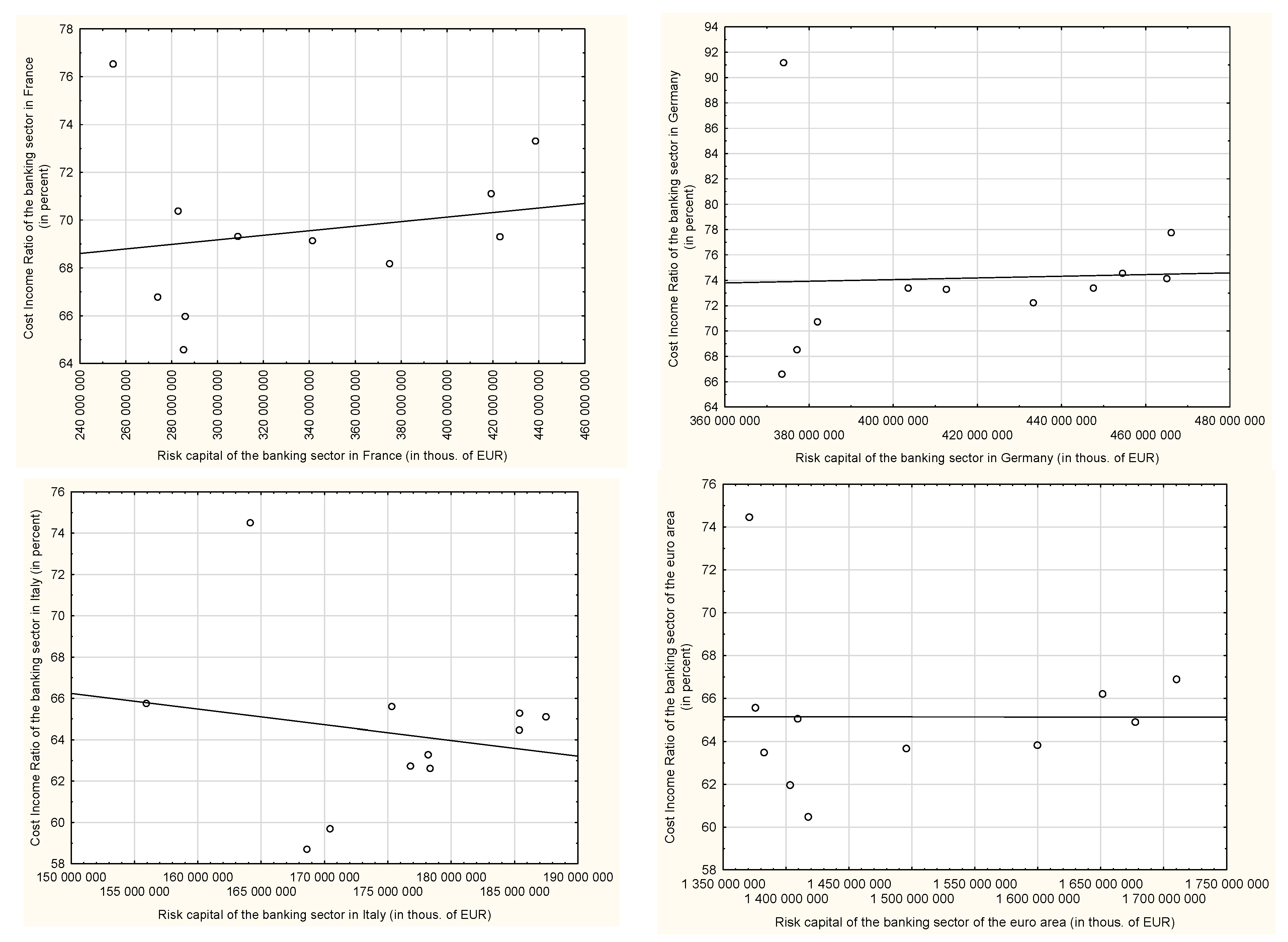

- an increase of bank risk capital was related to a growth of return on assets of banks and credit institutions in France, Germany and in the aggregated euro area banking sector; in the case of France and the whole euro area, this dependence was strong, while in the German banking sector it took the form of a moderate correlation; a lack of relation was observed for the Italian banking sector;

- −

- an increase in a level of own funds also resulted in an improvement in return on equity in the aggregated sector of the euro area (strong correlation); a moderate positive correlation was identified in France and Germany; while in the Italian banking sector there was no correlation between the examined features, and therefore return on equity was independent of the size of bank risk capital and profitability was strongly determined by macroeconomic factors;

- −

- regression analysis of the profitability, measured by the cost income ratio in relation to the size of risk capital, did not allow for unambiguous conclusions, because in all analyzed banking sectors there were almost no correlations.

- −

- the sectoral approach to the analysis of effectiveness of bank risk capital does not allow for unambiguous conclusions regarding assessment of the observed changes direction,

- −

- the analysis of effectiveness of bank risk capital in the European Union requires concentration on national banking sectors and banks, mainly systemically important financial institutions, because they often have a significant share in a total level of sectoral effectiveness of bank risk capital,

- −

- the research results indicate that in the conditions of ongoing regulatory changes in banks, diversity of risk capital effectiveness determinants may increase, which justifies extension of subjective scope of the conducted research and might be a basis for further Authors’ in-depth research.

Author Contributions

Funding

Institutional Review Board Statement

Informed Consent Statement

Data Availability Statement

Conflicts of Interest

Appendix A

| France | Germany | Italy | Euro Area | |

| Results of stage 1 | ||||

| Constant of regression () | −0.1485 | −0.9950 | −0.7043 | −1.8718 |

| Regression coefficient () | 0.000000001382 | 0.000000002510 | 0.000000003740 | 0.000000001333 |

| Correlation coefficient () | 0.7656 | 0.6660 | 0.0660 | 0.8742 |

| Coefficient of determination () | 0.5862 | 0.4435 | 0.0044 | 0.7643 |

| Standard error of estimation | 0.0827 | 0.1111 | 0.5776 | 0.1044 |

| The value of t-student statistics | tα0 = = −1.1238 | tα0 = = −2.5356 | tα0 = = −0.2131 | tα0 = = −5.039 |

| tα1 = = 3.5706 | tα1 = = 2.6784 | tα1 = = 0.1984 | tα1 = = 5.4016 | |

| The value of the F statistics | 12.749 | 7.1739 | 0.0394 | 29.1775 |

| p-value | 0.0060 < 0.05 | 0.0253 < 0.05 | 0.8471 > 0.05 | 0.0004 < 0.05 |

| Results of stage 2 | ||||

| Constant of regression () | 1.1600 | −23.3994 | −8.0010 | −28.1808 |

| Regression coefficient () | 0.00000001310 | 0.00000005707 | 0.00000003946 | 0.00000001999 |

| Correlation coefficient () | 0.5115 | 0.5112 | 0.0495 | 0.8157 |

| Coefficient of determination () | 0.2617 | 0.2614 | 0.0024 | 0.6654 |

| Standard error of estimation | 1.5683 | 3.7915 | 8.1384 | 1.9978 |

| The value of t-student statistics | tα0 = = 0.4632 | tα0 = = −1.7474 | tα0 = = −0.1718 | tα0 = = −3.9633 |

| tα1 = = 1.7859 | tα1 = = 1.7846 | tα1 = = 0.1485 | tα1 = = 4.2305 | |

| The value of the F statistics | 3.1894 | 3.1847 | 0.0221 | 17.8968 |

| p-value | 0.1078 > 0.05 | 0.1080 > 0.05 | 0.8852 > 0.05 | 0.0022 < 0.05 |

| Results of stage 3 | ||||

| Constant of regression () | 66.3200 | 71.4101 | 77.5979 | 65.1612 |

| Regression coefficient () | 0.000000009505 | 0.000000006599 | −0.00000007571 | 0.00000000002180 |

| Correlation coefficient () | 0.1908 | 0.0387 | 0.1788 | 0.0008 |

| Coefficient of determination () | 0.0364 | 0.0015 | 0.0320 | 0.0000 |

| Standard error of estimation | 3.4858 | 6.7412 | 4.2557 | 3.7982 |

| The value of t-student statistics | tα0 = = 0.0000 | tα0 = = 2.9993 | tα0 = = 0.0111 | tα0 = = 4.8201 |

| tα1 = = 0.5742 | tα1 = = 0.1161 | tα1 = = 0.5989 | tα1 = = −0.0024 | |

| The value of the F statistics | 0.3399 | 0.0135 | 0.2971 | 0.0000 |

| p-value | 0.5742 > 0.05 | 0.9102 > 0.05 | 0.5989 > 0.05 | 0.9981 > 0.05 |

| 1 | The following types of capital among own funds were identified (Czerwińska and Jajuga 2016):

|

References

- Abbas, Faisal, Omar Masood, Shoaib Ali, and Sohail Rizwan. 2021. How Do Capital Ratios Affect Bank Risk-Taking: New Evidence from the United States. SAGE Open 11: 2158244020979678. [Google Scholar] [CrossRef]

- Agénor, Pierre-Richard, Leonardo Gambacorta, Enisse Kharroubi, and Luiz A. Pereira da Silva. 2018. The effects of prudential regulation, financial development, and financial openness on economic growth. BIS Working Papers 752: 1–39. [Google Scholar]

- Ahnert, Toni, James Chapman, and Carolyn Wilkins. 2020. Should Bank Capital Regulation Be Risk Sensitive? Journal of Financial Intermediation 46: 1–31. [Google Scholar] [CrossRef]

- Altunbas, Yener, Mahir Binici, and Leonardo Gambacorta. 2017a. Macroprudential policy and bank risk. BIS Working Papers 646: 1–46. [Google Scholar] [CrossRef] [Green Version]

- Altunbas, Yener, Mahir Binici, Leonardo Gambacorta, and Andres Murcia. 2017b. New evidence on the effectiveness of macroprudential measures. CEPR Policy Portal. December 5. Available online: https://voxeu.org/article/new-evidence-effectiveness-macroprudential-measures (accessed on 12 September 2021).

- Altunbas, Yener, Santiago Carbo, Edward Gardener, and Philip Molyneux. 2007. Examining the relationship between capital, risk and efficiency in European banking. European Financial Management 13: 49–70. [Google Scholar]

- Angrick, Stefan, and Naoko Nemoto. 2017. Central banking below zero: The implementation of negative interest rates in Europe and Japan. ADBI Working Paper Series 740: 1–34. [Google Scholar] [CrossRef]

- Arseneau, David M. 2017. How Would U.S. Banks Fare in a Negative Interest Rate Environment? Finance and Economics Discussion Series 2017-030; Washington, DC: Federal Reserve Board, pp. 1–29. [CrossRef]

- Athanasoglou, Panayiotis P., Sophocles N. Brissimis, and Matthaios D. Delis. 2008. Bank-specific, industry-specific and macroeconomic determinants of bank profitability. Journal of International Financial Markets, Institutions and Money 18: 121–36. [Google Scholar] [CrossRef] [Green Version]

- Augur, Itai, and Maria Demertzis. 2012. Excessive Bank Risk Taking and Monetary Policy. Working Paper Series 1457; Frankfurt: European Central Bank. [Google Scholar]

- Baker, Malcolm, and Jeffrey Wurgler. 2015. Do stricte Capital Requirements Raise the Cost of Capital? Bank Regulation, Capital Structure, and the Low Risk Anomaly. American Economic Review 105: 315–20. [Google Scholar] [CrossRef]

- Baldwin, Richard. 2012. A new eReport: Excessive risk-taking by banks. Voxeu CEPR, March 30. [Google Scholar]

- Basel Committee on Banking Supervision. 2010. Basel III: A Global Regulatory Framework for More Resilient Banks and Banking Systems. Basel: Bank for International Settlements. [Google Scholar]

- Basel Committee on Banking Supervision. 2017. Basel III: Finalising Post-Crisis Reforms. Basel: Bank for International Settlements. [Google Scholar]

- Basel Committee on Banking Supervision. 2019. The costs and benefits of bank capital—A review of the literature. Working Paper 37: 1–29. [Google Scholar]

- Begg, David, Stanley Fischer, and Rudiger Dornusch. 1995. Ekonomia (Economics). Warsaw: Polish Economic Publisher. [Google Scholar]

- Behn, Markus, Marco Gross, and Tuomas Peltonen. 2016. Assessing the Costs and Benefits of Capital-Based Macroprudential Policy. ECB Working Paper Series 1935; Frankfurt: ECB. [Google Scholar]

- Beltrame, Federico, Roberto Cappelletto, and Gabriele Toniolo. 2014. Estimating SMEs Cost of Equity Using a Value at Risk Approach. The Capital at Risk Model. London: Palgrave Macmillan. [Google Scholar]

- Bhattacharyya, Sugato, and Amiyatosh Purnanandam. 2012. Risk-taking by Banks: What Did We Know and When Did We Know It? AFA 2012 Chicago Meetings Paper; American Finance Association. Available online: https://ssrn.com/abstract=1619472 (accessed on 30 September 2021).

- Bitar, Mohammad, Kuntara Pukthuanthong, and Thomas Walker. 2018. The effect of capital ratios on the risk, efficiency and profitability of banks: Evidence from OECD countries. Journal of International Financial Markets, Institutions and Money 53: 227–62. [Google Scholar] [CrossRef] [Green Version]

- Bitar, Mohammad, Kuntara Pukthuanthong, and Thomas Walker. 2019. Efficiency in Islamic vs. conventional banking: The role of capital and liquidity. Global Finance Journal 19: 100487. [Google Scholar] [CrossRef]

- Bojinov, Bojidar. 2016. Risk Management in the Banking Basic Principles and Approaches. SSRN Electronic Journal 3: 48–55. [Google Scholar] [CrossRef]

- Bougatef, Khemaies, and Nidhal Mgadmi. 2016. The impact of prudential regulation on bank capital and risk-taking: The case of MENA countries. The Spanish Review of Financial Economics 14: 51–56. [Google Scholar] [CrossRef]

- Buser, Stephen A., Andrew H. Chen, and Edward Kane. 1981. Federal Deposit Insurance, Regulatory Policy, and Optimal Bank Capital. Journal of Finance 36: 51–60. [Google Scholar]

- Caprio, Gerard, Jr. 2013. Financial Regulation After the Crisis: How Did We Get Here, and How Do We Get Out? LSE Financial Markets Group Special Paper Series 226: 285–319. [Google Scholar] [CrossRef] [Green Version]

- Cerutti, Eugenio, Stijn Claessens, and Luc Laeven. 2017. The use and effectiveness of macroprudential policies: New evidence. Journal of Financial Stability 28: 203–24. [Google Scholar] [CrossRef]

- Charnes, Abraham, William W. Cooper, and Edwardo L. Rhodes. 1978. Measuring the Efficiency of Decision Making Units. European Journal of Operational Research 2: 429–44. [Google Scholar] [CrossRef]

- Chockalingam, Arun, Shaunak Dabadghao, and Rene Soetekouw. 2018. Strategic risk, banks, and Basel III: Estimating economic capital requirements. Journal of Risk Finance 19: 225–46. [Google Scholar]

- Cœuré, Benoît. 2014. Life Below Zero: Learning about Negative Interest Rates. Presentation at the Annual Dinner of the ECB’s Money Market Contact Group. Frankfurt: ECB, September 9. [Google Scholar]

- Cohen, Benjamin. H., and Michela Scatigna. 2014. Banks and capital requirements: Channel of adjustment. BIS Working Papers 443: 1–26. [Google Scholar] [CrossRef]

- Colyer, T., and M. Sebag-Montefiore. 2011. The State of European Bank Funding. Oliver Wyman. Available online: https://www.oliverwyman.com/content/dam/oliver-wyman/v2/publications/2011/State_of_European_Funding_Report_2011.pdf (accessed on 4 November 2021).

- Committee on the Global Financial System. 2018. Structural changes in banking after the crisis. CGFS Papers 60: 1–119. [Google Scholar]

- Culp, Christopher L. 2002a. Contingent capital: Integrating corporate financing and risk management. Journal of Applied Corporate Finance 15: 46–56. [Google Scholar]

- Culp, Christopher L. 2002b. The Art of Risk Management, Alternative Risk Transfer, Capital Structure, and the Convergence of Insurance and Capital Markets. New York: John Wiley & Sons. [Google Scholar]

- Culp, Christopher L. 2002c. The Revolution in Corporate Risk Management: A Decade of Innovations in Process and Products. Journal of Applied Corporate Finance 14: 8–26. [Google Scholar]

- Czerwińska, Teresa, and Krzysztof Jajuga, eds. 2016. Ryzyko instytucji finansowych—Współczesne trendy i wyzwania (Risk of Financial Institutions—Modern Trends and Challenges). Warsaw: C.H. Beck. [Google Scholar]

- Czyżewski, Andrzej, and Katarzyna Smędzik. 2010. Efektywność techniczna i środowiskowa gospodarstw rolnych w Polsce według ich typów i klas wielkości w latach 2006–2008 [Technical and Environmental Efficiency of Farms in Poland in 2006–2008, According to their Types and Sizes]. Annals of Agricultural Sciences—Series G 97. Warsaw: Warsaw University of Life Sciences Publishing House, pp. 61–71. [Google Scholar]

- Dagher, Jihad, Giovanni Dell’Ariccia, Luc Laeven, Lev Ratnovski, and Hui Tonga. 2020. Bank Capital: A Seawall Approach. International Journal of Central Banking 16: 249–91. [Google Scholar]

- Danielsson, Jon, ed. 2015. Evolution of Economic Thinking as It Happened on Vox. London: Centre for Economic Policy Research. [Google Scholar]

- Deelchand, Tara, and Carol Padgett. 2009. The Relationship between Risk, Capital and Efficiency: Evidence from Japanese Cooperative Banks. December 18. Available online: https://ssrn.com/abstract=1525423 (accessed on 12 September 2021).

- Directive. 2013. Directive 2013/36/EU of the European Parliament and of the Council of 26 June 2013 on access to the activity of credit institutions and the prudential supervision of credit institutions and investment firms, amending Directive 2002/87/EC and repealing Directives 2006/48/EC and 2006/49/EC. Official Journal of the European Union L 176: 338. [Google Scholar]

- Doherty, Neil A. 2005. Risk management, risk capital, and the cost of capital. Journal of Applied Corporate Finance 17: 119–23. [Google Scholar] [CrossRef]

- Dong, Feng, and Yi Wen. 2017. Optimal Monetary Policy under Negative Interest Rate. In Working Paper Series, 2017-019A. St. Louis: Federal Reserve Bank of St. Louis, pp. 1–22. [Google Scholar]

- Dudycz, Tadeusz, and Bogumiła Brycz. 2006. Efektywność funkcjonowania polskich przedsiębiorstw w latach 1994–2004—wstępne badania empiryczne (Effectiveness of Polish enterprises in the years of 1994–2004—Preliminary empirical research), in Efektywność źródłem bogactwa narodów (Efficiency as a source of nations wealth). Working Papers of the University of Social Sciences VII: 91–106. [Google Scholar]

- Duliniec, Aleksandra. 2011. Finansowanie przedsiębiorstwa. Strategie i instrumenty (Financing the Enterprise. Strategies and Instruments). Warsaw: PWE. [Google Scholar]

- ECB. 2016. Recent developments in the composition and cost of bank funding in the euro area. Economic Bulletin 1: 26–45. [Google Scholar]

- ECB. 2019. Dlaczego banki muszą utrzymywać kapitał? [Why Do Banks Need to Maintain Capital?]. Available online: https://www.bankingsupervision.europa.eu/about/ssmexplained/html/hold_capital.pl.html (accessed on 1 September 2021).

- Elizalde, Abel, and Rafael Pepullo. 2007. Economic and regulatory capital in banking: What is the difference? International Journal of Central Banking 3: 87–117. [Google Scholar]

- Erel, Isil, Stewart C. Myers, and James A. Read Jr. 2021. Risk Capital: Theory and Applications. Journal of Applied Corporate Finance 33: 8–21. [Google Scholar]

- Erfani, G. Rod, and Bijan Vasigh. 2018. The Impact of the Global Financial Crisis on Profitability of the Banking Industry: A Comparative Analysis. Economies 6: 66. [Google Scholar] [CrossRef] [Green Version]

- Feridun, Mete, and Alper Özün. 2020. Basel IV implementation: A review of the case of the European Union. Journal of Capital Markets Studies 4: 7–24. [Google Scholar]

- Fiordelisi, Franco, David Marques-Ibanez, and Phil Molyneux. 2011. Efficiency and risk in European banking. Journal of Banking & Finance 35: 1315–26. [Google Scholar] [CrossRef] [Green Version]

- Gemar, Pablo, German Gemar, and Vanesa Guzman-Parra. 2019. Modeling the Sustainability of Bank Profitability Using Partial Least Squares. Sustainability 11: 4950. [Google Scholar] [CrossRef] [Green Version]

- Goddard, John, Philip Molyneux, and John O. S. Wilson. 2001. European Banking: Efficiency, Technology and Growth. London: Wiley. [Google Scholar]

- Gómez-Fernández-Aguado, Pilar, Purificación Parrado-Martínez, and Antonio Partal-Ureña. 2018. Risk Profile Indicators and Spanish Banks’ Probability of Default from a Regulatory Approach. Sustainability 10: 1259. [Google Scholar] [CrossRef] [Green Version]

- International Monetary Fund. 2017. Negative Interest Rate Policies—Initial experiences and assessments. IMF Policy Paper, 1–49. [Google Scholar]

- International Monetary Fund. 2018. Regulatory reform 10 Years after the Global Financial Crisis: Looking back, Looking forward. In Global Financial Stability Report—A Decade after the Global Financial Crisis: Are We Safer? Washington: IMF, pp. 55–79. [Google Scholar]

- Iqbal, Jamshed, and Sami Vähämaa. 2019. Managerial risk-taking incentives and the systemic risk of financial institutions. Review of Quantitative Finance and Accounting 53: 1229–58. [Google Scholar] [CrossRef] [Green Version]

- Ishikawa, Tatsuya, Yasuhiro Yamai, and Akira Ieda. 2003. On the Risk Capital Framework of Financial Institutions. IMES Discussion Paper Series 2003-E-7; Tokyo: Bank of Japan. [Google Scholar]

- Isnurhadi, Isnurhadi, Adam Mohamad, Sulastri Sulastri, Adriana Isni, and Muizzuddin Muizzuddin. 2021. Bank Capital, Efficiency and Risk: Evidence from Islamic Banks. Journal of Asian Finance, Economics and Business 8: 841–50. [Google Scholar] [CrossRef]

- Jobst, Andreas, and Huidan Lin. 2016. Negative Interest Rate Policy (NIRP): Implications for Monetary Transmission and Bank Profitability in the Euro Area. IMF Working Paper WP/16/172. Washington, DC: IMF, pp. 1–48. [Google Scholar]

- Jonek-Kowalska, Izabela, and Mariusz Zieliński. 2017. CSR activities in the banking sector in Poland. Paper presented at 29th International Business Information Management Association Conference, Austria, Vienna, May 3–4; Edited by Khaled S. Soliman. pp. 1294–304. [Google Scholar]

- Jumreornvong, Seksak, Chanakarn Chakreyavanich, Sirimon Treepongkaruna, and Pornsit Jiraporn. 2018. Capital Adequacy, Deposit Insurance, and the Effect of Their Interaction on Bank Risk. Journal of Risk Financial Management 11: 79. [Google Scholar] [CrossRef] [Green Version]

- Kibritcioglu, Aykut. 2002. Excessive Risk-Taking, Banking Sector Fragility, and Banking Crises. Working Paper 02-0114. Champaign: University of Illinois at Urbana-Champaign, College of Business. [Google Scholar]

- Kochaniak, Katarzyna. 2010. Efektywność finansowa banków giełdowych (Financial efficiency of listed banks). Warsaw: PWN. [Google Scholar]

- Kovner, Anna, and Peter Van Tassel. 2018. Evaluating Regulatory Reform: Banks’ Cost of Capital and Lending. Federal Reserve Bank of New York Staff Report 854. New York: Federal Reserve Bank of New York Staff. [Google Scholar]

- Kovner, Anna, Peter Van Tassel, and Brandon Zborowski. 2018. Regulatory Changes and the Cost of Capital for Banks. Liberty Street Economics. October 1. Available online: https://libertystreeteconomics.newyorkfed.org/2018/10/regulatory-changes-and-the-cost-of-capital-for-banks.html (accessed on 1 October 2021).

- Lee, Chien-Chiang, and Meng-Fen Hsieh. 2013. The impact of capital on profitability and risk in Asian banking. Journal of International Money and Finance 32: 251–81. [Google Scholar] [CrossRef]

- Lui, Alison. 2017. Financial Stability and Prudential Regulation: A Comparative Approach to the UK, US, Canada, Australia and Germany. New York: Routledge. [Google Scholar]

- Maddaloni, Angela, and Alessandro D. Scopelliti. 2019. Rules and Discretion(s) in Prudential Regulation and Supervision: Evidence from EU Banks in the Run-Up to the Crisis. ECB Working Paper Series 2284; Frankfurt: ECB. [Google Scholar]

- Marcinkowska, Monika. 2009. Standardy kapitałowe banków. Bazylejska nowa umowa kapitałowa w polskich regulacjach nadzorczych [Bank Capital Standards. New Basel Accord in Polish Supervisory Regulations]. Gdańsk: Reagen Press, p. 435. [Google Scholar]

- Matten, Chris. 2000. Managing Bank Capital: Capital Allocation and Performance Measurement, 2nd ed. Chichester: John Wiley & Sons. [Google Scholar]

- Matwiejczuk, Rafał. 2005. Efektywność—Próba interpretacji (Effectiveness—An attempt of interpretation). Przegląd Organizacji 11: 27–31. [Google Scholar]

- Mendicino, Caterina, Kalin Nikolov, Juan Rubio-Ramirez, Javier Suarez, and Dominik Supera. 2021. How much capital should banks hold? ECB Research Bulletin 80: 27. [Google Scholar]

- Merton, Robert C., and André F. Perold. 1993a. Management of risk capital in financial firms. In Financial Services: Perspectives and Challenges. Edited by Samuel L. Hayes. Boston: Harvard Business School Press, pp. 215–45. [Google Scholar]

- Merton, Robert C., and André F. Perold. 1993b. Theory of risk capital in financial firms. Journal of Applied Corporate Finance 6: 16–32. [Google Scholar] [CrossRef]

- Mingo, John J. 1975. Regulatory Influence on Bank Capital Investment. Journal of Finance 30: 1111–21. [Google Scholar] [CrossRef]

- Mughes, Joseph P., and Loretta J. Mester. 1998. Bank capitalization and cost: Evidence of scale economies in risk management and signaling. Review of Economics and Statistics 80: 314–25. [Google Scholar]

- Nocoń, Aleksandra, and Irena Pyka. 2018. Effectiveness of Risk Capital (own funds) in the Polish Banking Sector in the Years of 2002–2016. Paper presented at 10th International Scientific Conference “Business and Management 2018”, Vilnius, Lithuania, May 4; pp. 9–19. [Google Scholar]

- Nocoń, Aleksandra, and Irena Pyka. 2019. Sectoral analysis of the effectiveness of bank risk capital in the Visegrad Group countries. Journal of Business Economics and Management 20: 336–57. [Google Scholar] [CrossRef] [Green Version]

- Orgler, Yair E., and Robert A. Taggart Jr. 1983. Implications of Corporate Capital Structure Theory for Banking Institutions: Note. Journal of Money, Credit and Banking 15: 212–21. [Google Scholar] [CrossRef]

- Peltzman, Sam. 1970. Capital Investment in Commercial Banking and its Relationship to Portfolio Regulation. Journal of Political Economy 78: 1–26. [Google Scholar] [CrossRef]

- Perottia, Enrico, Lev Ratnovski, and Razvan Vlahu. 2011. Capital Regulation and Tail Risk. International Journal of Central Banking 7: 123–63. [Google Scholar]

- Posacka, Katarzyna, and Anna Szelągowska. 2006. Zastosowanie analizy regresji w ocenie konkurencyjności wybranych banków komercyjnych w Polsce w latach 1996–2004 (Application of regression analysis in evaluation of competitiveness of analyzed commercial banks in Poland from 1996 to 2004). Scientific Paper of University of Computer Sciences and Skills in Łódź, Theory and Application of Computer Science 5: 137–46. [Google Scholar]

- Pringle, John H. 1974. The Capital Decision in Commercial Banks. Journal of Finance 29: 779–95. [Google Scholar] [CrossRef]

- Pyka, Irena, and Aleksandra Nocoń. 2017. Ryzyko niskich stóp procentowych w sektorze bankowym. In Strategie stóp procentowych w bankowości. Edited by Piotr Masiukiewicz. Warsaw: The Polish Bank Association, CPBiI Publishing House. [Google Scholar]

- Pyka, Irena, Aleksandra Nocoń, and Joanna Cichorska. 2019. Nowy ład Regulacyjny w Sektorze Bankowym Unii Europejskiej. Warsaw: CeDeWu, pp. 161–71. [Google Scholar]

- Pyka, Irena, and Aleksandra Nocoń. 2019. Negative Interest Rate Risk. Atavism or Normalization of Central Banks’ Monetary Policy. Acta Universitatis Lodziensis. Folia Oeconomica 3: 89–116. [Google Scholar] [CrossRef] [Green Version]

- Redo, Magdalena. 2015. The importance of prudential regulations in the process of transmitting monetary policy to economy. Copernican Journal of Finance & Accounting 4: 145–58. [Google Scholar]

- Regulation. 2013. (EU) No 575/2013 of the European Parliament and of the Council of 26 June 2013 on prudential requirements for credit institutions and investment firms and amending Regulation (EU) No 648/2012. Official Journal of the European Union L 176/1. [Google Scholar]

- Rutkowska, Anna. 2013. Teoretyczne aspekty efektywności—Pojęcie i metody pomiaru. Journal of Management and Finance 11: 439–53. [Google Scholar]

- Saita, Francesco. 1999. Allocation of Risk Capital in Financial Institutions. Financial Management 28: 95–111. [Google Scholar] [CrossRef]

- Samuelson, Paul A., and William D. Nordhaus. 2012. Ekonomia (Economics). Poznań: REBIS Publishing House. [Google Scholar]

- Santomero, Anthony M., and Ronald D. Watson. 1977. Determining Optimal Capital Standards for the Banking Industry. Journal of Finance 32: 1267–82. [Google Scholar] [CrossRef]

- Schwarcz, Steven L., and Maziar Peihani. 2018. Addressing Excessive Risk Taking in the Financial Sector: A Corporate Governance Approach. Center for International Governance Innovation Policy Brief 139: 1–12. [Google Scholar]

- Shimpi, Prakash. 1999. Integrating Corporate Risk Management. London and New York: Swiss Re (Textere Texere LLC). [Google Scholar]

- Shimpi, Prakash. 2001. The Insurative Model. Risk Management 48: 10. [Google Scholar]

- Sironi, Andrea. 2018. The Evolution of Banking Regulation Since the Financial Crisis: A Critical Assessment. BAFFI CAREFIN Centre Research Paper 103: 1–60. [Google Scholar] [CrossRef]

- Stolz, Stéphanie. 2002. The Relationship between Bank Capital, Risk-Taking, and Capital Regulation: A Review of the Literature. Kiel Working Paper 1105. Available online: https://www.econstor.eu/handle/10419/17759 (accessed on 12 September 2021).

- Stulz, René M. 2015. Risk-Taking and Risk Management by Banks. Journal of Applied Corporate Finance 27: 8–18. [Google Scholar] [CrossRef]

- Taggart, Robert A., Jr., and Stuart I. Greenbaum. 1978. Creenbaum, Bank Capital and Public Regulation. Journal of Money, Credit and Banking 10: 158–69. [Google Scholar] [CrossRef]

- Tropeano, Domenica. 2018. Financial Regulation in the European Union after the Crisis. A Minskian Approach. London and New York: Routledge. [Google Scholar]

- Tursoy, Turgut. 2018. Risk management process in banking industry. MPRA Paper 86427: 136. [Google Scholar]

- Van Greuning, Hennie, and Sonja B. Bratanovic. 2020. Analyzing Banking Risk. A Framework for Assessing Corporate Governance and Risk Management, 4th ed. Washington, DC: World Bank. [Google Scholar]

- Viñals, José. 2016. Analysing the Effectiveness of Macroprudential Tools. BIS Papers 86b. Available online: https://ssrn.com/abstract=2844225 (accessed on 12 September 2021).

- Wieczorek-Kosmala, Monika. 2017. Kapitał Ryzyka w Przedsiębiorstwie z Perspektywy Zintegrowanego Zarządzania Ryzykiem (Risk Capital in an Enterprise from the Perspective of Integrated Risk Management). Warsaw: CeDeWu, p. 63. [Google Scholar]

- Wieczorek-Kosmala, Monika. 2019. The Concept of Risk Capital and Its Application in Non-Financial Companies: A Sustainable Dimension. Sustainability 11: 894. [Google Scholar] [CrossRef] [Green Version]

- World Bank. 2019. Bank Regulation and Supervision a Decade after the Global Financial Crisis. In Global Financial Development Report. Washington, DC: World Bank. [Google Scholar]

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| France | Germany | Italy | Euro Area |

|---|---|---|---|

| France | Germany | Italy | Euro Area |

|---|---|---|---|

| France | Germany | Italy | Euro Area |

|---|---|---|---|

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2021 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Pyka, I.; Nocoń, A. Bank Risk Capital and Its Effectiveness in Selected Euro Area Banking Sectors. J. Risk Financial Manag. 2021, 14, 555. https://doi.org/10.3390/jrfm14110555

Pyka I, Nocoń A. Bank Risk Capital and Its Effectiveness in Selected Euro Area Banking Sectors. Journal of Risk and Financial Management. 2021; 14(11):555. https://doi.org/10.3390/jrfm14110555

Chicago/Turabian StylePyka, Irena, and Aleksandra Nocoń. 2021. "Bank Risk Capital and Its Effectiveness in Selected Euro Area Banking Sectors" Journal of Risk and Financial Management 14, no. 11: 555. https://doi.org/10.3390/jrfm14110555

APA StylePyka, I., & Nocoń, A. (2021). Bank Risk Capital and Its Effectiveness in Selected Euro Area Banking Sectors. Journal of Risk and Financial Management, 14(11), 555. https://doi.org/10.3390/jrfm14110555