Corporate Cash Holdings and National Culture: Evidence from the Middle East and North Africa Region

Abstract

:1. Introduction

2. Literature Review and Hypotheses Development

2.1. Corporate Cash Holdings and National Culture

2.2. Hypotheses Development

3. Methodology

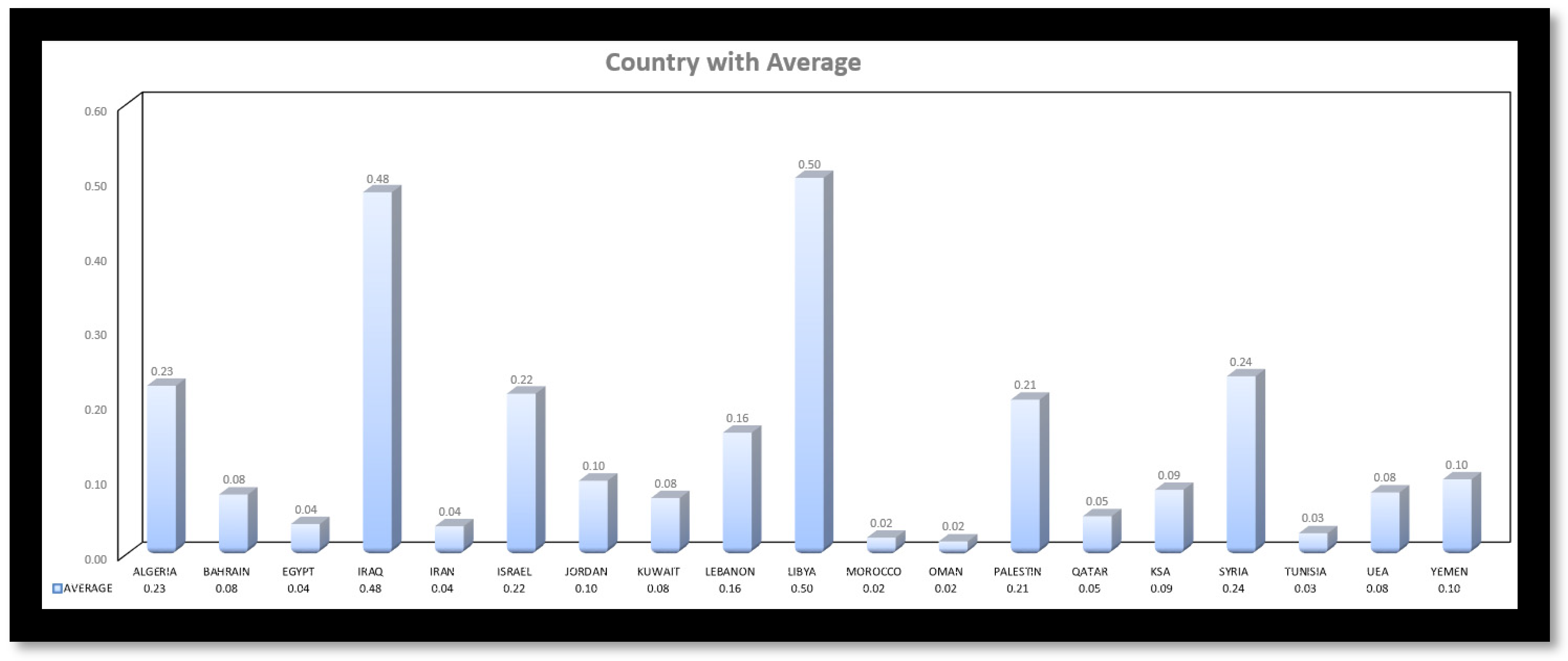

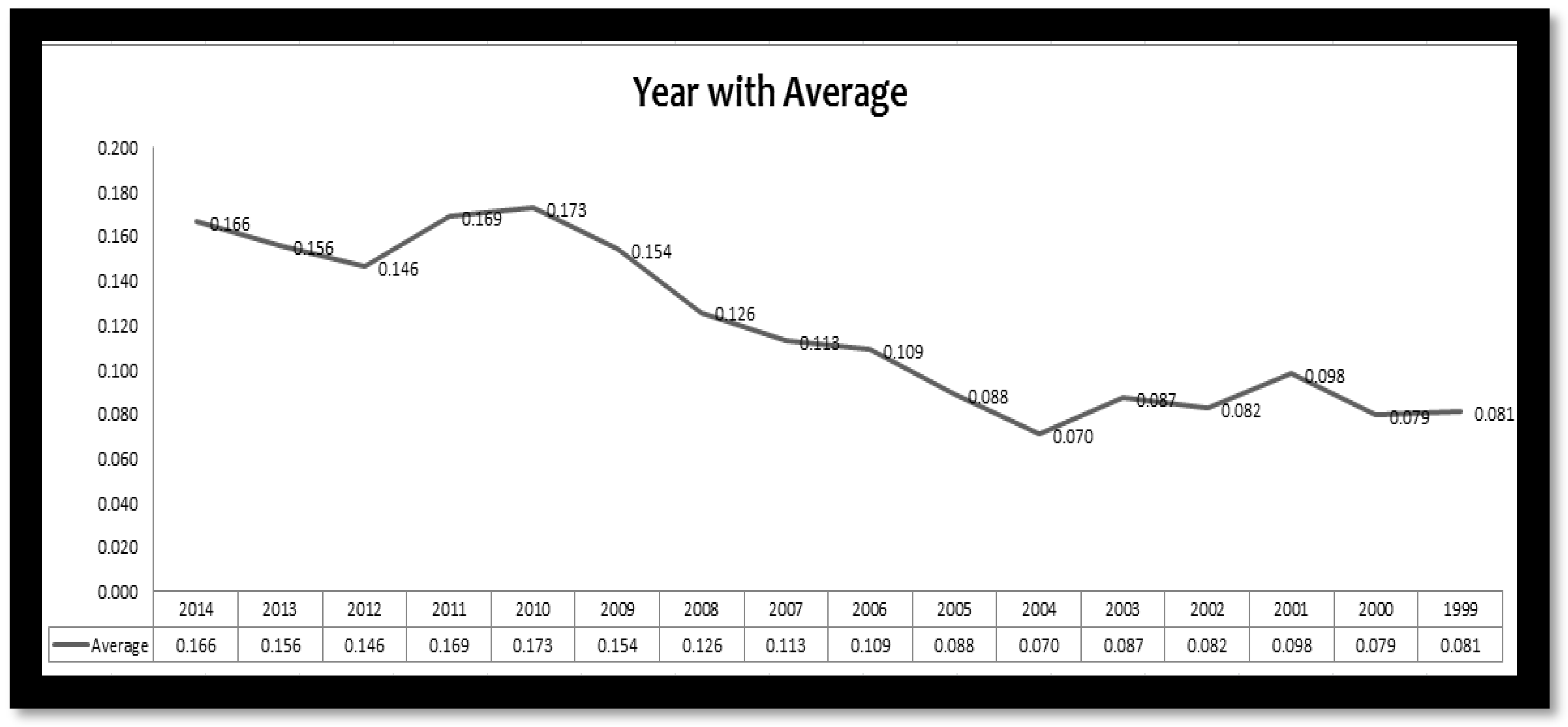

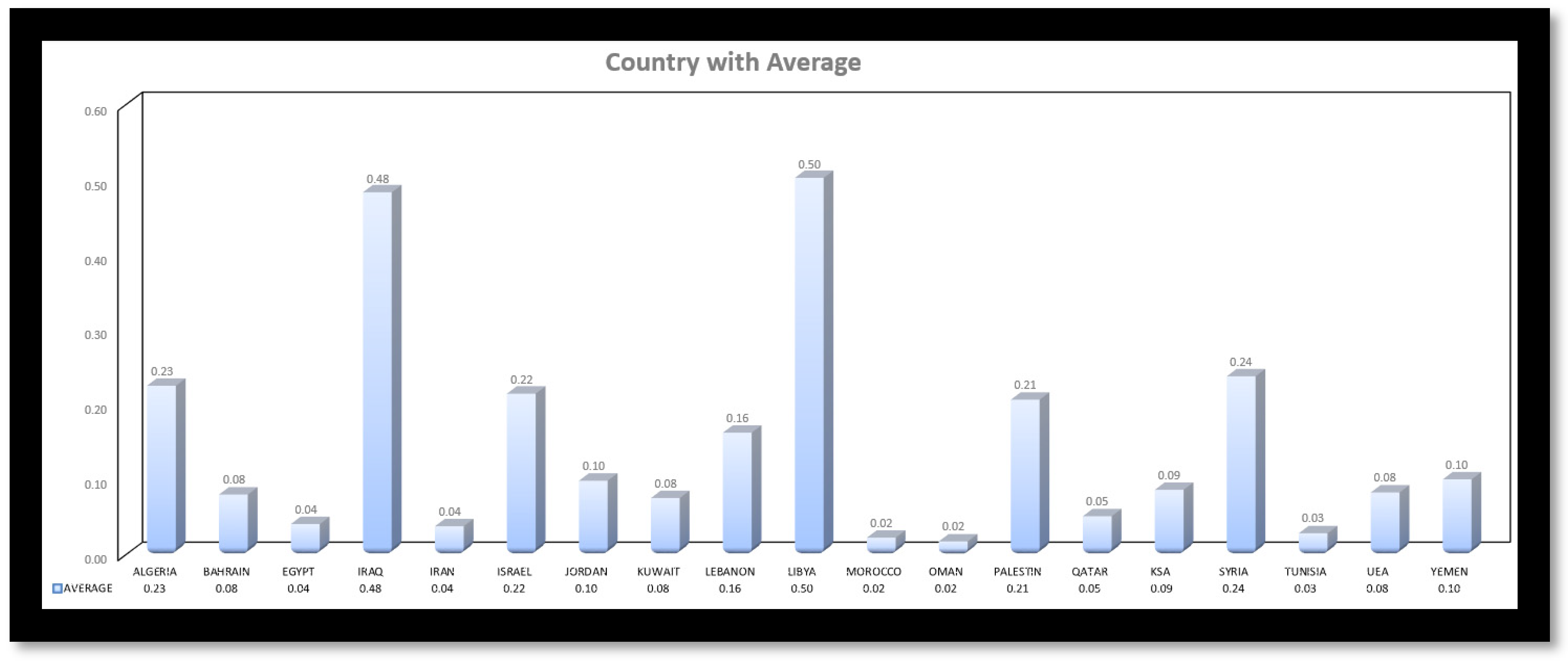

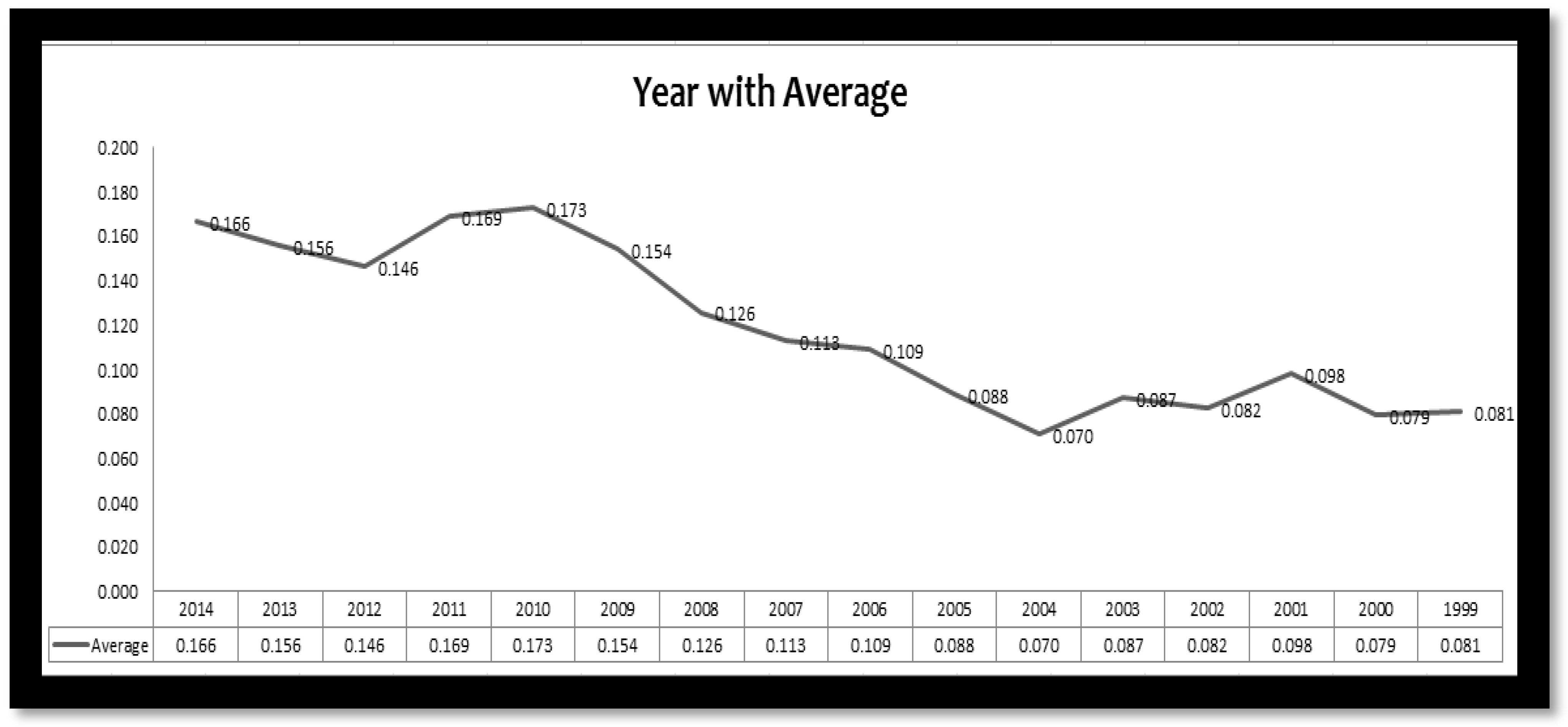

3.1. Sample and Data Collection

3.2. Variables and Research Models

4. Empirical Analysis and Discussion

4.1. Descriptive and Correlation Analysis

4.2. Regression Analysis and Discussion

4.3. Robustness Tests

5. Conclusions, Implications, and Suggestions for Further Research

5.1. Conclusions

5.2. Implications

5.2.1. Theoretical Implications

5.2.2. Practical Implications

5.3. Limitations and Future Researches

Author Contributions

Funding

Institutional Review Board Statement

Informed Consent Statement

Data Availability Statement

Acknowledgments

Conflicts of Interest

References

- Achim, Monica Violeta, Sorin Nicolae Borlea, Lucian Vasile Găban, and Alin Adrian Mihăilă. 2019. The Shadow Economy and Culture: Evidence in European Countries. Eastern European Economics 57: 352–74. [Google Scholar] [CrossRef]

- Ahern, Kenneth, Daniele Daminelli, and Cesare Fracassic. 2015. Lost in translation? The effect of cultural values on mergers around the world. Journal of Financial Economics 117: 165–89. [Google Scholar] [CrossRef]

- Ahn, Seoungpil, and Jaiho Chung. 2015. Cash holdings, corporate governance, and acquirer returns. Financial Innovation 13: 1–31. [Google Scholar] [CrossRef] [Green Version]

- Al-Najjar, Basil. 2013. The financial determinants of corporate cash holdings: Evidence from some emerging markets. International Business Review 22: 77–88. [Google Scholar] [CrossRef]

- Al-Najjar, Basil, and Yacine Belghitar. 2011. Corporate cash holdings and dividend payments: Evidence from simultaneous analysis. Managerial & Decision Economics 32: 231–41. [Google Scholar] [CrossRef]

- Al-Najjar, Basil, and Ephraim Clark. 2017. Corporate governance and cash holdings in MENA: Evidence from internal and external governance practices. Research in International Business and Finance 39: 1–12. [Google Scholar] [CrossRef] [Green Version]

- Ali, Alipour. 2021. What matters for the future? Comparing Globe’s future orientation with Hofstede’s long-term orientation. Cross Cultural & Strategic Management 28: 734–59. [Google Scholar] [CrossRef]

- Anand, Lalita, Thenmozhi Nikhil Varaiya, and Saumitra Bhadhuri. 2018. Impact of Macroeconomic Factors on Cash Holdings? A Dynamic Panel Model. Journal of Emerging Market Finance 17: S27–S52. [Google Scholar] [CrossRef]

- Arosa, Clara Maria Verduch, Nivine Richie, and Peter Schuhmann. 2014. The impact of culture on market timing in capital structure choices. Research in International Business and Finance 31: 178–92. [Google Scholar] [CrossRef]

- Bukair, Abdullah Awadh, and Azhar Abdul Rahman. 2015. Bank performance and board of directors’ attributes by Islamic banks. International Journal of Islamic and Middle Eastern Finance and Management 8: 291–309. [Google Scholar] [CrossRef]

- Bates, Thomas, Kahle Kathleen, and René Stulz. 2009. Why Do U.S. Firms Hold So Much More Cash Than They Used To? The Journal of Finance 64: 1985–2021. [Google Scholar] [CrossRef] [Green Version]

- Beugelsdijk, Sjoerd, and Bart Frijns. 2010. A cultural explanation of the foreign bias in international asset allocation. Journal of Banking & Finance 34: 2121–31. [Google Scholar] [CrossRef]

- Bitar, Mohammad, Kabir Hassan, and Wadad Saad. 2020. Culture and the capital–performance nexus in dual banking systems. Economic Modelling 87: 34–58. [Google Scholar] [CrossRef]

- Bougatef, Khemaies. 2017. Determinants of bank profitability in Tunisia: Does corruption matter? Journal of Money Laundering Control 20: 70–78. [Google Scholar] [CrossRef]

- Bui, Tat Dat, Mohd Helmi Ali, Feng Ming Tsai, Mohammad Iranmanesh, Ming-Lang Tseng, and Ming K. Lim. 2020. Challenges and Trends in Sustainable Corporate Finance: A Bibliometric Systematic Review. Journal of Risk and Financial Management 13: 264. [Google Scholar] [CrossRef]

- Breuer, Wolfgang, Bushra Ghufran, and Astrid Juliane Salzmann. 2018. National culture, managerial preferences, and takeover performance. International Business Review 27: 1270–89. [Google Scholar] [CrossRef]

- Byrne, Julie, and Thomas O’Connor. 2017. Creditor rights, culture and dividend pay-out policy. Journal of Multinational Financial Management 39: 60–77. [Google Scholar] [CrossRef] [Green Version]

- Chang, Kiyoung, and Abbas Noorbakhsh. 2006. Corporate cash holdings, foreign direct investment, and corporate governance. Global Finance Journal 16: 302–16. [Google Scholar] [CrossRef]

- Chang, Kiyoung, and Abbas Noorbakhsh. 2009. Does national culture affect international corporate cash holdings? Journal of Multinational Financial Management 19: 323–42. [Google Scholar] [CrossRef]

- Chen, Shihua, Yan Ye, Khalil Jebran, and Muhammad Ansar Majeed. 2020. Confucianism culture and corporate cash holdings. International Journal of Emerging Markets 15: 1127–59. [Google Scholar] [CrossRef]

- Chen, Yangyang, Paul Dou, Ghon Rheec, Cameron Truong, and Madhu Veeraragh. 2015. National culture and corporate cash holdings around the world. Journal of Banking & Finance 50: 1–18. [Google Scholar] [CrossRef] [Green Version]

- Chourou, Lamia, Samir Saadi, and Hui Zhub. 2018. How does national culture influence IPO underpricing? Pacific-Basin Finance Journal 51: 318–41. [Google Scholar] [CrossRef]

- Chui, Andy, and Chuck Kwok. 2008. National Culture and Life Insurance Consumption. Journal of International Business Studies 39: 88–101. [Google Scholar] [CrossRef]

- Chui, Andy C. W., Sheridan Titman, and K. C. John Wei. 2010. Individualism and momentum around the world. Journal of Finance 65: 361–92. [Google Scholar] [CrossRef]

- Deshmukh, Sanjay, Goel Anand, and Howe Keith. 2021. Do CEO beliefs affect corporate cash holdings? Journal of Corporate Finance 67: 101886. [Google Scholar] [CrossRef]

- Dittmar, Amy, Jan Mahrt-Smith, and Henri Servaes. 2003. International corporate governance and corporate cash holdings. Journal of Financial and Quantitative Analysis 38: 111–33. [Google Scholar] [CrossRef]

- Diez-Esteban, José María, Jorge Bento Farinha, and Conrado Diego García-Gómez. 2019. Are religion and culture relevant for corporate risk-taking? International evidence. Business Research Quarterly 22: 36–55. [Google Scholar] [CrossRef]

- Dittmar, Amy, and Jan Mahrt-Smith. 2007. Corporate governance and the value of cash holdings. Journal of Financial Economics 83: 599–634. [Google Scholar] [CrossRef]

- Dittmar, Amy, and Ran Duchin. 2011. Dynamics of Cash. Working Paper. Ann Arbo: University of Michigan. [Google Scholar]

- Elamer, Ahmed, Collins Ntim, Hussein Abdou, Andrew Owusu, Mohamed Elmagrhi, and Awad Ibrahim. 2020. Are Bank Risk Disclosures Informative? Evidence from Debt Markets. International Journal of Finance and Economics 26: 1270–98. [Google Scholar] [CrossRef]

- Esmaeili, Maryam, and Mehri Nasrabadi. 2020. An inventory model for single-vendor multi-retailer supply chain under inflationary conditions and trade credit. Journal of Industrial and Production Engineering 38: 75–88. [Google Scholar] [CrossRef]

- Fauver, Larry, and Michael McDonald. 2015. Culture, agency costs, and governance: International evidence on capital structure. Pacific-Basin Finance Journal 34: 1–23. [Google Scholar] [CrossRef]

- Fernandes, Nuno, and Halit Gonenc. 2016. Multinationals and cash holdings. Journal of Corporate Finance 39: 139–54. [Google Scholar] [CrossRef]

- Ferreira, Miguel, and Antonio Vilela. 2004. Why do firms hold cash? Evidence from EMU countries. European Financial Management 10: 295–319. [Google Scholar] [CrossRef]

- Foley, Fritz, Jay Hartzell, Sheridan Titman, and Garry Twite. 2007. Why do firms hold so much cash? A tax-based explanation. Journal of Financial Economics 86: 579–607. [Google Scholar] [CrossRef] [Green Version]

- Gorodnichenko, Yuriy, and Gerard Roland. 2017. Culture, Institutions, and the Wealth of Nations. Review of Economics & Statistics 99: 402–16. [Google Scholar] [CrossRef]

- Guiso, Luigi, Paola Sapienza, and Luigi Zingales. 2006. Does culture affect economic outcomes? Journal of Economic Perspectives 20: 23–48. [Google Scholar] [CrossRef] [Green Version]

- Haj-Salem, Issal, and Khaled Hussainey. 2021. Risk Disclosure and Corporate Cash Holdings. Journal of Risk and Financial Management 14: 328. [Google Scholar] [CrossRef]

- Haq, Marmiza, Daniel Hu, Robert Faff, and Shams Pathan. 2018. New evidence on national culture and bank capital structure. Pacific-Basin Finance Journal 50: 41–64. [Google Scholar] [CrossRef] [Green Version]

- Harford, Jarrad, Sattar Mansi, and William Maxwell. 2008. Corporate governance and firm cash holdings in the US. Journal of Financial Economics 87: 535–55. [Google Scholar] [CrossRef]

- Hofstede, Geert. 1980. Culture’s Consequences: International Differences in Work-Related Values. Beverly Hills: Sage. [Google Scholar]

- Hofstede, Geert. 2001. Culture’s Consequences: Comparing Values, Behaviors, Institutions, and Organizations Across Nations, 2nd ed. Newbury Park: Sage Publications. [Google Scholar]

- Hofstede, Geert. 2010. The GLOBE debate: Back to relevance. Journal of International Business Studies 41: 1339–46. [Google Scholar] [CrossRef]

- Hope, Ole-Kristian, Tony Kang, Wayne Thomas, and Yong Keun Yoo. 2008. Culture and auditor choice: A test of the secrecy hypothesis. Journal of Accounting and Public Policy 27: 357–73. [Google Scholar] [CrossRef]

- Jensen, Michael. 1986. Agency cost of free cash flow, corporate finance and takeovers. American Economic Review 76: 323–29. [Google Scholar] [CrossRef] [Green Version]

- Kanagaretnam, Kiridaran, Chee Yeow Lim, and Gerald J. Lobo. 2014. Influence of national culture on accounting conservatism and risk-taking in the banking industry. The Accounting Review 89: 1115–49. [Google Scholar] [CrossRef]

- Kariuki, Samuel, Gregory Namusonge, and George Orwa. 2015. Determinants of corporate cash holdings: Evidence from private manufacturing firms in Kenya. International Journal of Advanced Research in Management and Social Sciences 4: 15–33. [Google Scholar]

- Kashefi-Pour, Eilnaz, Shima Amini, Moshfique Uddin, and Darren Duxbury. 2020. Does Cultural Difference Affect Investment–Cash Flow Sensitivity? Evidence from OECD Countries. British Journal of Management 31: 636–58. [Google Scholar] [CrossRef]

- Keynes, Maynard. 1936. The General Theory of Employment, Interest and Money. London: Harcourt Brace. [Google Scholar]

- Kim, Jiyoung, Hyunjoon Kim, and David Woods. 2011. Determinants of corporate cash-holding levels: An empirical examination of the restaurant industry. International Journal of Hospitality Management 30: 568–74. [Google Scholar] [CrossRef]

- Kwok, Chuck, and Solomon Tadesse. 2006. National culture and financial systems. Journal of International Business Studies 37: 227–47. [Google Scholar] [CrossRef]

- Le, Duc Hoang, Phi Long Tran, Thu Phuong Ta, and Duy Minh Vu. 2018. Determinants of corporate cash holding: Evidence from UK listed firms. Business and Economic Horizons 14: 561–69. [Google Scholar] [CrossRef]

- Li, Yaoqin, Xichan Chen, Wanli Li, and Xixiong Xu. 2021. How does Buddhism affect corporate cash holdings? International Journal of Emerging Markets. ahead-of-print. [Google Scholar] [CrossRef]

- Li, Kai, Dale Griffin, Heng Yue, and Longkai Zhao. 2013. How does culture influence corporate risk-taking? Journal of Corporate Finance 23: 1–22. [Google Scholar] [CrossRef]

- Liu, Xiaoding. 2016. Corruption culture and corporate misconduct. Journal of Financial Economics 122: 307–27. [Google Scholar] [CrossRef]

- Mandal, Anindya, Brojeswar Pal, and Kripasindhu Chaudhuri. 2020. Unreliable EPQ model with variable demand under two-tier credit financing. Journal of Industrial and Production Engineering 37: 370–86. [Google Scholar] [CrossRef]

- Mittal, Rakesh, and Steven Elias. 2016. Social power and leadership in cross-cultural context. Journal of Management Development 35: 58–74. [Google Scholar] [CrossRef]

- Mondal, Amitava, and Santanu Kumar Ghosh. 2012. Intellectual capital and financial performance of Indian banks. Journal of Intellectual Capital 13: 515–30. [Google Scholar] [CrossRef]

- Myers, Stewart. 1977. Determinants of corporate borrowing. Journal of Financial Economics 5: 147–75. [Google Scholar] [CrossRef] [Green Version]

- Myers, Stewart. 1984. The capital structure puzzle. The Journal of Finance 39: 575–92. [Google Scholar] [CrossRef] [Green Version]

- Myers, Stewart, and Nicholas Majluf. 1984. Corporate financing and investment decisions when firms have information that investors do not have. Journal of Financial Economics 13: 187–221. [Google Scholar] [CrossRef] [Green Version]

- Nash, Robert, and Ajay Patel. 2019. Instrumental variables analysis and the role of national culture in corporate finance. Financial Management 48: 385–416. [Google Scholar] [CrossRef]

- Newman, Karen, and Stanley Nollen. 1996. Culture and congruence: The fit between management practices and national culture. Journal of International Business Studies 27: 753–79. [Google Scholar] [CrossRef]

- Obiols, Maria. 2018. The World’s Richest Companies 2018: Global Finance Cash. Global Finance 32: 1–24. [Google Scholar]

- Opler, Tim, Lee Pinkowitz, René M. Stulz, and Rohan Williamson. 1999. The determinants and implications of corporate cash holdings. Journal of Financial Economics 52: 3–46. [Google Scholar] [CrossRef] [Green Version]

- Ozkan, Aydin, and Neslihan Ozkan. 2004. Corporate cash holdings: An empirical investigation of UK companies. Journal of Banking & Finance 28: 2103–34. [Google Scholar] [CrossRef]

- Ozkan, Serdar, Chadi Yaacoub, Nasser El-Kanj, and VIadimir Dzenopoljac. 2021. The Effect of IFRS Adoption on Corporate Cash Holdings: Evidence from MENA Countries. Emerging Markets Finance and Trade 57: 3275–300. [Google Scholar] [CrossRef]

- Orlova, Svetlana, and Grant Harper. 2021. National culture and leverage adjustments. Review of Behavioral Finance. ahead-of-print. [Google Scholar] [CrossRef]

- Orlova, Svetlana, Ramesh Rao, and Tony Kang. 2017. National culture and the valuation of cash holdings. Journal of Business Finance and Accounting 44: 236–70. [Google Scholar] [CrossRef] [Green Version]

- Patricia, Bachiller, and Javier Garcia-Lacalle. 2018. Corporate governance in Spanish savings banks and its relationship with financial and social performance. Management Decision 56: 828–48. [Google Scholar] [CrossRef] [Green Version]

- Pinkowitz, Lee, René M. Stulz, and Rohan Williamson. 2003. Do Firms in Countries with Poor Protection of Investor Rights hold More Cash? NBER Working Papers 10188. National Bureau of Economic Research, Inc. Available online: https://ideas.repec.org/p/nbr/nberwo/10188.html (accessed on 29 August 2021).

- Prenker, Tomas, and Jens Kück. 2009. The Determinant of Corporate Cash Holdings. Master’s thesis, School of Economics and Management, Lund University, Lund, Sweden. [Google Scholar]

- Ramírez, Andrés, and Solomon Tadesse. 2009. Corporate cash holdings, uncertainty avoidance, and the multinationality of firms. International Business Review 18: 387–403. [Google Scholar] [CrossRef]

- Seifert, Bruce, and Halit Gonenc. 2016. Creditor Rights, Country Governance, and Corporate Cash Holdings. Journal of International Financial Management & Accounting 27: 65–90. [Google Scholar] [CrossRef] [Green Version]

- Seifert, Bruce, and Halit Gonenc. 2018. The effects of country and firm-level governance on cash management. Journal of International Financial Markets, Institutions and Money 52: 1–16. [Google Scholar] [CrossRef]

- Shabbir, Mohsin, Shujahat Haider Hashmi, and Ghulam Mujtaba Chaudhary. 2016. Determinants of corporate cash holdings in Pakistan. International Journal of Organizational Leadership 5: 50–62. [Google Scholar] [CrossRef]

- Tasawar, Nawaz, and Roszaini Haniffa. 2017. Determinants of financial performance of Islamic banks: An intellectual capital perspective. Journal of Islamic Accounting and Business Research 8: 130–42. [Google Scholar] [CrossRef] [Green Version]

- Tabellini, Guido. 2010. Culture and Institutions: Economic Development in the Regions of Europe. Journal of the European Economic Association 8: 677–716. [Google Scholar] [CrossRef]

- Tran, Quoc Trung. 2020. Uncertainty avoidance culture, cash holdings and financial crisis. Multinational Business Review 28: 549–66. [Google Scholar] [CrossRef]

- Tran, Ly Thi Hai, Thoa Thi Kim Tu, and Thao Thi Phuong Hoang. 2021. Managerial optimism and corporate cash holdings. International Journal of Managerial Finance 17: 214–36. [Google Scholar] [CrossRef]

- Ucar, Erdem. 2018. Creative culture, risk-taking, and corporate financial decisions. European Financial Management 25: 684–717. [Google Scholar] [CrossRef]

- Uyar, Ali, and Cemil Kuzey. 2014. Determinants of corporate cash holdings: Evidence from the emerging market of Turkey. Applied Economics 46: 1035–48. [Google Scholar] [CrossRef]

- Van Den Steen, Eric. 2004. Rational Overoptimism (and Other Biases). American Economic Review 94: 1141–51. [Google Scholar] [CrossRef] [Green Version]

- Vandello, Joseph, and Dov Cohen. 1999. Patterns of individualism and collectivism across the United States. Journal of Personality and Social Psychology 77: 279–92. [Google Scholar] [CrossRef]

- Wei, Feng, and Yu Kong. 2017. Corruption, financial development and capital structure: Evidence from China. China Finance Review International 7: 295–322. [Google Scholar] [CrossRef]

- Yong, Tan, and Christos Floros. 2012. Bank profitability and inflation: The case of China. Journal of Economic Studies 39: 675–96. [Google Scholar] [CrossRef] [Green Version]

- Zarrouk, Hajer, Khoutem Ben Jedidia, and Mouna Moualhi. 2016. Is Islamic bank profitability driven by same forces as conventional banks? International Journal of Islamic and Middle Eastern Finance and Management 9: 46–66. [Google Scholar] [CrossRef]

- Zhang, Min, Wen Zhang, and Sheng Zhang. 2016. National culture and firm investment efficiency: International evidence. Asia-Pacific Journal of Accounting & Economics 23: 1–21. [Google Scholar] [CrossRef]

- Zheng, Changjun, and Badar Nadeem Ashraf. 2014. National culture and dividend policy: International evidence from banking. Journal of Behavioural and Experimental Finance 3: 22–40. [Google Scholar] [CrossRef]

- Zheng, Xiaolan, Sadok El Ghoul, Omrane Guedhami, and Chuck C. Y. Kwok. 2012. National culture and corporate debt maturity. Journal of Banking & Finance 36: 468–88. [Google Scholar] [CrossRef]

- Zhou, Meihua, Jian Cao, and Bin Lin. 2021. CEO organizational identification and firm cash holdings. China Journal of Accounting Research 14: 183–205. [Google Scholar] [CrossRef]

- Zouari, Sarra Ben Slama, and Neila Boulila Taktak. 2014. Ownership structure and financial performance in Islamic banks: Does bank ownership matter? International Journal of Islamic and Middle Eastern Finance and Management 7: 146–60. [Google Scholar] [CrossRef]

{kind=link}

{kind=link}

| Variables | Definitions | Source |

|---|---|---|

| Dependent variable | ||

| Cash holdings ratio | Total cash and cash equivalents over total assets Logarithm of total cash and cash equivalents over total assets | Bank scope and annual reports |

| Independent variables | ||

| Power distance (PD) | The degree to which the less powerful members of a society accept and expect that power is distributed unequally. | Hofstede (1980, 2001, 2010) https://hi.hofstede-insights.com/national-culture (accessed on 20 July 2021) |

| Individualism | The preference for a loosely knit social framework in which individuals are expected to take care of only themselves and their immediate families | |

| Masculinity | It represents a preference in society for achievement, heroism, assertiveness, and material rewards for success. Society at large is more competitive | |

| Uncertainty avoidance (UA) | The degree to which the members of a society feel uncomfortable with uncertainty and ambiguity. | |

| Long Term Orientation (LTO) | Societies with a high score, take a more pragmatic approach by encourage thrift and efforts in modern education to prepare for the future. | |

| Control variables: Corporate characteristics | ||

| Size | Natural logarithm of total assets | Bank scope and annual reports |

| Listed | Dummy variable: 1 if the bank is listed in the stock market and 0 otherwise | |

| Leverage | Measured by Total liabilities (non-current + current) over total assets | |

| Financial performance | ROA: Retune on assets ROE: Return on equity | |

| Bank Type | Dummy variable: 1 if the bank is Islamic and 0 otherwise | Annual reports |

| Control variables: Country characteristics | ||

| Inflation | Inflation rate is calculated by annual growth rate of Gross domestic product implicit deflator displays the rate of price variation in economy as a whole | World bank database https://data.worldbank.org/indicator/NY.GDP.DEFL.KD.ZG.AD (accessed on 18 July 2021) |

| Control of Corruption | Corruption level is imitating views of the extent to which public power is trained for private gain, comprising petty and grand forms of corruption and capture of the state through bests and private interests | Worldwide Governance Indicators (WGI) http://info.worldbank.org/governance/wgi/ https://datacatalog.worldbank.org/dataset/worldwide-governance-indicators (accessed on 21 July 2021) |

| Foreign Exchange Rate System | Is how a nation managing its currency in the foreign exchange market. Measured as a dummy variable by giving 1 if the Foreign Exchange Rate System in the country is floating system and 0 otherwise as a fixed system | World bank database https://data.worldbank.org/indicator/PA.NUS.FCRF (accessed on 23 July 2021) |

| N | Minimum | Maximum | Mean | Std. Deviation | Skewness | Kurtosis | |

|---|---|---|---|---|---|---|---|

| CASH | 6354 | 1.4761 | 2.5631 | 0.1039 | 0.192849 | −0.096 | 21.353 |

| PD | 6354 | 13.000 | 95.00 | 7.6429 | 13.92750 | −2.024 | 6.407 |

| INDIV | 6354 | 20.000 | 59.00 | 3.6801 | 9.07610 | 0.530 | −0.109 |

| MASC | 6354 | 40.000 | 65.00 | 5.1447 | 6.24436 | 0.062 | −0.089 |

| UA | 6354 | 54.000 | 96.00 | 7.1746 | 8.75166 | 0.791 | 0.848 |

| LTO | 6354 | 0.000 | 70.00 | 2.5005 | 15.41297 | 1.109 | 1.910 |

| LIST | 6354 | 0 | 1 | 0.33 | 0.471 | 0.710 | −1.497 |

| SIZE | 5392 | 2.00 | 8.00 | 5.5027 | 0.63282 | −0.412 | 0.451 |

| LEVE | 5217 | 0.0021 | 101.166 | 1.2090 | 2.80698 | 22.997 | 745.937 |

| ROA | 5205 | −7.314 | 9.1502 | 0.0356 | 0.34821 | 12.152 | 473.423 |

| ISLAM | 6347 | 0.00 | 1.00 | 0.2469 | 0.4312 | 1.174 | −0.621 |

| INFL | 6354 | −2.53127 | 7.11480 | 6.62017 | 1.0495895 | 1.519 | 8.105 |

| CORRU | 6354 | −1.61 | 1.72 | −0.1752 | 0.72873 | 0.058 | −0.806 |

| FER | 6300 | 0 | 1 | 0.51 | 0.500 | 1.658 | −0.981 |

| CASH | PD | INDIV | MASC | UA | LTO | LIST | SIZE | LEVE | ROA | |

|---|---|---|---|---|---|---|---|---|---|---|

| CASH | 1.00 | −0.052 ** | 0.024 | −0.044 * | −0.258 ** | −0.066 ** | 0.007 | −0.056 ** | 0.067 ** | 0.045 * |

| PD | 1.00 | −0.707 ** | 0.349 ** | 0.002 | −0.040 ** | 0.004 | −0.051 ** | −0.035 | 0.001 | |

| INDIV | 1.00 | 0.075 ** | 0.094 ** | 0.199 ** | −0.141 ** | −0.098 ** | 0.064 ** | 0.005 | ||

| MASC | 1.00 | −0.151 ** | 0.333 ** | −0.291 ** | −0.169 ** | 0.039 | −0.001 | |||

| UA | 1.00 | 0.276 ** | −0.013 | 0.178 ** | −0.085 ** | −0.007 | ||||

| LTO | 1.00 | −0.035 ** | 0.005 | 0.008 | −0.010 | |||||

| LIST | 1.00 | 0.178 ** | −0.050 * | −0.002 | ||||||

| SIZE | 1.00 | −0.167 ** | −0.042 * | |||||||

| LEVE | 1.00 | 0.038 | ||||||||

| ROA | 1.00 |

| Model | Unstandardized Coefficients | Standardized Coefficients | T | Sig. | |

|---|---|---|---|---|---|

| B | Std. Error | Beta | |||

| (Constant) | 0.411 | 0.035 | 11.835 | 0.000 | |

| PD | 0.001 | 0.000 | 0.053 | 2.380 | 0.017 * |

| INDIV | 0.001 | 0.000 | 0.071 | 3.413 | 0.001 *** |

| MASC | −0.002 | 0.000 | −0.104 | −5.889 | 0.000 *** |

| UA | −0.003 | 0.000 | −0.207 | −14.793 | 0.000 *** |

| LTO | 0.000 | 0.000 | 0.033 | 2.277 | 0.023 * |

| LIST | −0.004 | 0.004 | −0.012 | −0.944 | 0.345 |

| SIZE | −0.008 | 0.004 | −0.026 | −2.057 | 0.040 |

| LEVE | 0.002 | 0.001 | 0.024 | 1.961 | 0.050 |

| ROA | 0.016 | 0.008 | 0.024 | 1.974 | 0.048 |

| Model Summary | Adjusted R square 0.40 | F 31.316 | Sig 0.000 | ||

| Variables | Unstandardized Coefficients | Standardized Coefficients | T | Sig. | |

|---|---|---|---|---|---|

| B | Std. Error | Beta | |||

| (Constant) | 0.409 | 0.035 | 11.774 | 0.000 | |

| PD | 0.001 | 0.000 | 0.054 | 2.446 | 0.014 * |

| INDIV | 0.001 | 0.000 | 0.074 | 3.593 | 0.000 *** |

| MASC | −0.002 | 0.000 | −0.105 | −5.968 | 0.000 *** |

| UA | −0.003 | 0.000 | −0.207 | −14.809 | 0.000 *** |

| LTO | 0.000 | 0.000 | 0.032 | 2.251 | 0.024 * |

| ISLAM | 0.011 | 0.004 | 0.035 | 2.819 | 0.005 |

| LIST | −0.004 | 0.004 | −0.013 | −1.004 | 0.316 |

| SIZE | −0.008 | 0.004 | −0.027 | −2.148 | 0.032 |

| LEVE | 0.002 | 0.001 | 0.024 | 1.966 | 0.049 |

| ROA | 0.016 | 0.008 | 0.023 | 1.880 | 0.060 |

| Model Summary | Adjusted R square 0.41 | F 28.109 | Sig 0.000 | ||

| Model | Unstandardized Coefficients | Standardized Coefficients | T | Sig. | |

|---|---|---|---|---|---|

| B | Std. Error | Beta | |||

| (Constant) | −1.629 | 0.134 | −12.114 | 0.000 | |

| PD | 0.002 | 0.001 | 0.061 | 2.701 | 0.007 * |

| INDIV | 0.003 | 0.001 | 0.049 | 2.323 | 0.020 * |

| MASC | −0.001 | 0.002 | −0.012 | −0.672 | 0.501 |

| UA | 0.000 | 0.001 | −0.013 | −0.940 | 0.347 |

| LTO | −0.002 | 0.000 | −0.044 | −3.038 | 0.002 * |

| LIST | 0.029 | 0.015 | 0.026 | 1.960 | 0.050 |

| SIZE | 0.027 | 0.015 | 0.024 | 1.842 | 0.066 |

| LEVE | −0.001 | 0.004 | −0.004 | −0.342 | 0.733 |

| ROA | −0.031 | 0.032 | −0.012 | −0.964 | 0.335 |

| Model Summary | Adjusted R square 0.50 | F 3.334 | Sig 0.000 | ||

| Model | Unstandardized Coefficients | Standardized Coefficients | T | Sig. | Tolerance | VIF | |

|---|---|---|---|---|---|---|---|

| B | Std. Error | Beta | |||||

| (Constant) | 0.420 | 0.039 | 10.909 | 0.000 | |||

| PD | 0.000 | 0.000 | 0.067 | 3.019 | 0.003 ** | 0.310 | 3.229 |

| INDIV | 0.000 | 0.000 | 0.030 | 1.322 | 0.186 | 0.288 | 3.476 |

| MASC | −0.002 | 0.000 | −0.098 | −5.305 | 0.000 *** | 0.446 | 2.241 |

| UA | −0.002 | 0.000 | −0.115 | −5.782 | 0.000 *** | 0.384 | 2.603 |

| LTO | 0.000 | 0.000 | 0.063 | 4.405 | 0.000 *** | 0.734 | 1.363 |

| LIST | −0.006 | 0.003 | −0.027 | −2.108 | 0.035 * | 0.918 | 1.090 |

| SIZE | 0.149 | 0.022 | 0.086 | 6.850 | 0.000 *** | 0.959 | 1.043 |

| LEVE | 0.001 | 0.001 | 0.017 | 1.353 | 0.176 | 0.961 | 1.040 |

| ROA | −0.006 | 0.003 | −0.027 | −1.898 | 0.058 * | 0.758 | 1.319 |

| Inflation | 0.000 | 0.000 | 0.068 | 5.411 | 0.000 *** | 0.958 | 1.044 |

| Corruption | −0.028 | 0.003 | −0.176 | −9.293 | 0.000 *** | 0.426 | 2.345 |

| Model Summary | Adjusted R square 0.302 | F 54.489 | Sig 0.000 | ||||

| Model | Unstandardized Coefficients | Standardized Coefficients | T | Sig. | Tolerance | VIF | |

|---|---|---|---|---|---|---|---|

| B | Std. Error | Beta | |||||

| (Constant) | 1.036 | 0.082 | 12.576 | 0.000 | |||

| PD | −0.002 | 0.000 | −0.157 | −4.839 | 0.000 *** | 0.432 | 2.315 |

| INDIV | 0.001 | 0.001 | 0.030 | 0.809 | 0.418 | 0.334 | 2.990 |

| MASC | −0.003 | 0.001 | −0.144 | −4.540 | 0.000 *** | 0.449 | 2.229 |

| UA | −0.008 | 0.001 | −0.321 | −11.873 | 0.000 *** | 0.621 | 1.610 |

| LTO | 0.000 | 0.000 | 0.018 | 0.700 | 0.484 | 0.679 | 1.472 |

| SIZE | −0.014 | 0.006 | −0.052 | −2.235 | 0.026 * | 0.834 | 1.199 |

| LEVE | −0.001 | 0.001 | −0.012 | −0.526 | 0.599 | 0.931 | 1.074 |

| ROA | 0.143 | 0.028 | 0.111 | 5.039 | 0.000 *** | 0.939 | 1.065 |

| FER System | −0.031 | 0.007 | −0.107 | −4.445 | 0.000 *** | 0.787 | 1.270 |

| Model Summary | Adjusted R square 0.175 | F 44.005 | Sig 0.000 | ||||

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2021 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

El-Halaby, S.; Abdelrasheed, H.; Hussainey, K. Corporate Cash Holdings and National Culture: Evidence from the Middle East and North Africa Region. J. Risk Financial Manag. 2021, 14, 475. https://doi.org/10.3390/jrfm14100475

El-Halaby S, Abdelrasheed H, Hussainey K. Corporate Cash Holdings and National Culture: Evidence from the Middle East and North Africa Region. Journal of Risk and Financial Management. 2021; 14(10):475. https://doi.org/10.3390/jrfm14100475

Chicago/Turabian StyleEl-Halaby, Sherif, Hosam Abdelrasheed, and Khaled Hussainey. 2021. "Corporate Cash Holdings and National Culture: Evidence from the Middle East and North Africa Region" Journal of Risk and Financial Management 14, no. 10: 475. https://doi.org/10.3390/jrfm14100475

APA StyleEl-Halaby, S., Abdelrasheed, H., & Hussainey, K. (2021). Corporate Cash Holdings and National Culture: Evidence from the Middle East and North Africa Region. Journal of Risk and Financial Management, 14(10), 475. https://doi.org/10.3390/jrfm14100475