1. Introduction

Financial security at different levels of socio-economic relationships in modern society has emerged as a separate area of research. As a component of economic security, it first and foremost attracts the attention of economists. However, economists differ in their areas of expertise and in how they view financial security in their research: as a state (

Shynkar et al. 2020), a process (

Nguyen and Nguyen 2020) or a feature of a particular economic system (

Franchuk et al. 2020).

Scientists and specialists in the fields of management and finance thoroughly and professionally study the concept of ‘financial security’ as an independent objective of enterprise management, but there are not enough studies on the methodology used to assess it (

Stashchuk et al. 2020). Recommendations for analyzing and managing financial security boil down to ‘the need to use a system of indices, indicators and methods’. At best, there is a list of indicators that exactly coincide with the economic analysis indicators used to assess an enterprise’s financial condition (

Cherep et al. 2020;

Turgaeva et al. 2020). At worst, there are only unfounded ‘recommendations’ for managing or assessing a company’s financial security.

Most scientists explore this multidimensional concept from the standpoint of ‘their’ science. For example, financiers examine it from the standpoint of finance; macroeconomists from the perspective of macroeconomics. However, financial decisions are not always made solely based on empirical evidence and financial indicators that show the state of financial security; nor are they necessarily based on information about processes that minimize the risk of losing sufficient levels of financial security.

To make objectively optimal decisions such as decisions about investing, stakeholders need to assess a large spectrum of information to evaluate an entity’s financial condition and vast amounts of data to determine its level of financial security (

Bochulia and Melnychenko 2019;

Tullio and Mario 2011). However, for firms such as banks that work with payment systems around the clock, the corresponding indicators change after each client’s transaction, almost every second, 24 hours per day. Thus, because a large part of the data becomes out of date while it is being processed, determining the state of a financial institution actually does not make sense. In addition, for other entities, if the analysis is conducted, for example, on the day of peak payables, financial stability indicators may differ significantly from those that would allow the financial security level to be evaluated as high.

Considering the need to examine an enterprise’s external environment to determine its financial security, only artificial intelligence with powerful computing capabilities (

Melnychenko 2019), which would more or less provide generalized information for decision-making, could cope with this task. However, decisions made in this case would be suboptimal. On one hand—as noted—by the time a decision must be made, the situation will change. On the other hand, the increased amount of processed information cannot clearly indicate the quality of the decisions made on its basis.

Thus, the problem raised in this study is that financial indicators and their analysis do not offer an objective reflection of a company’s level of financial security, although their consideration is important in the assessment. However, stakeholder decisions are based on the perceived level of financial security, and its indicators have only an indirect impact.

Indeed, under certain circumstances, economic analysis—assessing financial security status using a number of indicators—may indicate a low level of financial security according to different calculation methods, which, apparently, should prompt the manager to make decisions using cautious tactics and may lead to the inability to grow rapidly because of the low probability of investment in the business. However, as in the case with Apple, the perception of potential gain or loss is sometimes crucial. Founded in 1976 by two friends—without any rational grounds for evaluating it as financially secure—this company raised venture capital and, in 2018, was the first company in history to be valued at US

$ one trillion, thanks to the perceptions associated with Steve Jobs, one of the co-founders. An economic model of such success, based solely on using economic analysis data to assess financial security as a state, would be impossible, since all indicators would have shown the company had an extremely low level of financial security at its inception and thus, could not have predicted the investments made in it (

Porter 2018).

Therefore, regardless of how well a company’s financial security information is evaluated, decisions made on its basis will not lead to objectively optimal results. Thus, it is necessary to develop a concept that, first, would be able to represent a company’s real level of financial security and second, would allow evaluation of both its economic essence and the nature and complex vision of the essence. Such a concept should be premised on objective financial indicators, while considering the particularities of the individual’s decision-making based on their judgments about the company. Therefore, it should be borne in mind the contradictions associated with the basic principle of agnosticism: it is impossible to obtain certainty based solely on subjective judgments.

Thus, the significance of this study for economic science is that the proposed concept describes a universal approach to assessing the level of financial security of an enterprise. It takes into account both the indicators of objective control based on financial and management reporting, as well as the value of subjective professional judgments of stakeholders, which ultimately guide decisions about the future business, investment policy or lending. Such judgments are formed based on an understanding of all aspects of financial security, not just those reflected in economic indicators or indicators calculated on the basis of reporting data.

This study hypothesizes that the level of a company’s financial security is determined not so much by the economic indicators of its activity, but by the perceptions of individuals and other stakeholders who make decisions. At the same time, these perceptions are formed as a result of the stakeholder’s continuous participation in operations, constant monitoring of financial indicators, study of current approaches to enterprise management, changes in the environment and market conditions.

This study’s purpose is to substantiate the principles used to assess a company’s financial security based on the perceptions and professional judgment of stakeholders, which are not peculiar to artificial intelligence, which could assess the enterprise’s financial security are.

No studies have been published on the possibility of leveling the cognitive limitations of decision-makers on the enterprise’s financial security with help of artificial intelligence.

2. Materials and Methods

This study analyzes existing approaches to assessing financial security and highlights one based on behavioral economics: managers’ or other stakeholders’ perceptions of financial security formed using their personal understanding of data, information and business in general—as well as the cognitive constraints to making decisions about further development of companies, investing, and so on.

The basic categories that affect the achievement of financial security are ‘pillars of finance’ (

Thacker 2013): income, debt management, savings. It is thanks to them achieved the level of financial security, which allows to conduct business calmly, keep balance and confidently move forward for any company. Therefore, we can say that based on the assessment of these categories, decisions are made about the level of financial security of the enterprise. Further decision-making is the basis of the idea of this study. Moreover, the level of financial security depends on the effectiveness of their management. ‘Often, in practice, the occurrence of bankruptcy can be detected by human expert-based knowledge, experience and judgment. Nevertheless, human personal and affective biases cannot be eradicated, and the personal judgments tend to be significantly subjective’ (

Lahmiri and Bekiros 2019).

As

Hacker (

2011) notes in his research, for most people, maintaining a current level of income is far more important than its growth. Therefore, lower-income households may have a relatively higher level of economic security, with a lower level of financial security, than the middle-class population or those with higher material status when loss or a significant reduction in income may lead to destabilization or crisis. Wherein financial security depends mainly on the level of financial literacy and its understanding or the financial skills of decision makers. This is corroborated by considerable research showing that low levels of savings, ineffective financial portfolio allocation and poor risk diversification are associated with a lack of financial awareness (

Tavares et al. 2017;

Raczkowski 2014). However, financial security also can be enhanced by making qualitative changes in a payment system and its technical infrastructure, such as changes in supervisory rules and regulations (

Yilmaz 2007).

The aspects considered in the works of other authors also indicate that it is impossible to assess the level of financial security of an enterprise using only economic indicators. Hence, financial security as the state of businesses that allows them to balance their basic needs and unavoidable expenses, considering physiological and social needs, as well as cultural norms. In contrast, financial security, as a continuous process, requires reducing or eliminating monetary risks to ensure capital adequacy, which is adapted to the entity’s risk profile and preferences (

Miendlarzewska et al. 2019).

Indeed, an individual system’s particular state can be considered in statics, analyzing its indicators at a particular point in time as one, or they can be combatting opposites: threats that affect all system elements, with system countermeasures to overcome them. In this case, financial security as a state can and should be assessed, in particular, by economic methods, such as economic analysis tools. However, other managerial methods that are relevant to the tools of other sciences are needed to analyze the process. In this sense, a study showing that money can be used to purchase pleasure, which contributes to financial security and psychological reassurance, deserves attention (

Howell et al. 2012).

Nowadays, economics as a science is in a state where interdisciplinary relationships in the study of phenomena and processes have acquired special significance; therefore, tools from other disciplines, such as mathematical methods and models, the principles and methods of political science or those used in psychology, are widely used in research. Indeed, economic science itself does not have universal methods for predicting and comprehensively assessing states and trends. This fact was demonstrated by practice, when economists have been unable to anticipate and prevent all or, at least most, negative consequences, such as those of the global financial crisis. Researchers’ conclusions and recommendations made without a proper combination of methods from other sciences are, in fact, ‘just a mind game’ (

Belyanin 2018). Examples of properly assessing individual economic processes are embedded in behavioral economics—which incorporates the study of psychology into the analysis of the decision-making behind an economic outcome and has demonstrated to be viable—and its supporters and creators have deserved the highest recognition worldwide.

R. Thaler, the Nobel Prize winner in economics 2017, is an outstanding representative, supporter and, actually, creator of behavioral economics in its modern form, as well as a specialist and scientist whose findings have been accepted by scholars and practitioners. His work and research have demonstrated and convinced colleagues that society is not so rational that it can be clearly described by the models most economic approaches, forecasts, and policies of enterprises and states are built on. It does not consist of ‘fictional creatures that populate economic models’ (

Thaler 2015). Moreover, knowledge of people’s irrational behaviors can and should be used in defining economic policies at different levels to enhance societal well-being. When a behavioral problem becomes clear, a behavioral solution can be found for it (

Thaler 2015). Finally, this study is devoted to the following task: finding a solution to objectively assess a company’s financial security, based on the fact that its level is determined by the perceptions of decision-makers.

A deeper understanding of human behavior is as important to success as is knowledge of financial reporting and company management. After all, businesses are run by people, and their subordinates and customers are also people (

Thaler 2015). Therefore, financial security should also be considered as their perceptions of the level of security.

At the same time, people have various disadvantages that do not allow them to assess situations objectively or make decisions that would not lead merely to satisfactory or good results, but to optimal ones. This position is consistent with the assertions of scientists studying data analysis with regard to human cognitive limitations, which rightly indicate ‘the amount of data has increased and the methods for analyzing them have advanced considerably in recent years, the basic cognitive ability of human beings has not developed in the same way’. In addition, ‘developing expert-level knowledge and skills is time-consuming and we seldom acquire exceptional or even adequate skill levels in a wide range of domains’ (

Kalakoski et al. 2019). Moreover, even when using decision support systems, decisions do not become the most optimal (

Arnott 2005;

Phillips-Wren et al. 2019). As a result, our cognitive limitations lead to cognitive biases or cognitive illusions described in detail by

Pohl (

2004).

In addition, human thinking is infrequently followed in strictly rational ways; it is prone to many types of cognitive biases. For example, we tend to look for evidence that meets our expectations and rely on information that confirms what we want to see and find (confirmation bias). For example, when a term in a sentence or question is replaced by a semantically similar, but incorrect term, we have difficulty detecting the distortion (Moses illusion) (

Pohl 2004). Hence, human thinking is not the best instrument for decision-making, that why it should be search and used new instruments for more optimal decisions. Such instrument could be an artificial intelligence (AI), which can enhance a human capital performance beyond human benchmarks (

Laila and Haitham 2020).

From the field of artificial intelligence and brain modeling have developed neural networks (

Smith and Gupta 2000). K. A. Smith and J. N. D. Gupta(2000) made an overview of the different types of neural network models (Multilayered feedforward neural networks, Hopfield neural network, Self-organizing neural networks and other neural network models, most of these are extensions of the first three) which are applicable when solving business problems, especially problems related to financial security. Therefore, ‘in 1991, the banks started to use neural networks to make decisions about loan applicants and speculate about financial prediction’, ‘financial fraud detection is another important area of neural networks in business. Visa International have an operational fraud detection systems which is based upon a neural network’ (

Smith and Gupta 2000). These are the examples that are directly related to the enterprise’s financial security.

The issue of an enterprise’s financial security has been relatively well researched, with a significant number of publications on the nexus of relationships existing between failure, bankruptcy, institutional context and local characteristics on one hand and entrepreneurship, firm survival and performance on the other (

Eklund et al. 2020), about a comprehensive analysis of the financial attributes and identify those that are most relevant to bankruptcy prediction (

Zoričák et al. 2020), regarding relationships and research trends in the prediction of business failure (

Dimitras et al. 1996), regarding pillars of personal finance (

Thacker 2013), sustainable development (

Dalevska et al. 2019;

Kuzior et al. 2019;

Kwilinski et al. 2019), industry 4.0 (

Dzwigol et al.2020;

Kwilinski and Kuzior 2020), in the information economy (

Kwilinski 2018), regarding smart city systems (

Lakhno et al. 2018), virtual regionalization conditions (

Pająk et al. 2016), information technologies influence on financial security of economy (

Tkachenko et al. 2019b). Furthermore, methods for predicting financial distress of small and medium-sized enterprises using logistic regression and neural networks (

Altman et al. 2020).

Many previous studies relate to management, financial management also using artificial intelligence (

Tkachenko et al. 2019a). G. D. Sharma et al. have provided an overview of how artificial intelligence is applied in different government sectors (

Sharma et al. 2020). They found that the extant literature retrieved from Web of Science and Scopus databases is less focused on healthcare, ICT, education, social and cultural services and fashion sector. However, their research in which sphere is most superficial and related only to government sectors ignoring financial security also in these areas of government. Other scientists have surveyed financial fraud methods using machine learning and deep learning methodology under IoT environment refers to the unauthorized use of mobile transaction using mobile platform through identity theft or credit card stealing to obtain money fraudulently (

Choi and Lee 2018).

Fethi and Pasiouras (

2010) discuss applications neural networks, support vector machines and multicriteria decision aid that have also been used in recent years, in bank failure prediction studies and the assessment of bank creditworthiness and underperformance. Policy making as a strategic challenge for artificial intelligence discussed

M. Milano et al. (

2014). However, no studies have been published on the possibility of leveling the cognitive limitations of decision-makers on the enterprise’s financial security with help of artificial intelligence.

To prove the low level of economic analysis’ objectivity in assessing the enterprise’s financial security, we will use a method that allows measures the efficiency of the decision making unit is the data envelopment analysis (DEA) method. It compares indicators of the investigated object with the best in the sample to derive compared efficiency by correlating the input and output data (

Allen et al. 2013).

Scientists

Allen et al. (

2013) describe the method as follows ‘DEA measures the efficiency of the decision making unit by comparison with the best producer in the sample to derive compared efficiency’. DEA was introduced by

A. Charnes et al. (

1978) as a nonparametric linear programming approach, capable of handling multiple inputs as well as multiple outputs (

Charnes et al. 1994;

Cooper et al. 2007).

‘DEA is a mathematical programming technique for the development of production frontiers and the measurement of efficiency relative to these frontiers’ (

Fethi and Pasiouras 2010).

Using the terminology of the DEA method, incomes are essentially input data, debt and output data. To assess the enterprise’s financial security, it is advisable to take into account that the savings should be understood as all the assets that are its accumulated resources.

The research results are based mainly on qualitative data about the nature of the thing investigated—the enterprise’s financial security. Sources of data were observations used observational research and secondary data.

3. Results

To confirm the hypothesis of this study it should be analyzed the state of a company’s financial security with, ‘inter alia’, economic analysis methods. Here, explanations should be provided for an unambiguous understanding of what other static methods can be used to analyze a company’s financial security. Issues of a company’s financial security also include the state of the company’s payment infrastructure, payment instruments and client–bank systems. These components simply cannot be comprehensively evaluated using only economic analysis methods. In addition, the need for some types of enterprises to monitor their financial position every second indicates financial security analysis based on economic analysis using, for example, financial statements prepared once per reporting period, is insufficient. In addition, when presenting data in numeric or visual format, it is rarely possible to simultaneously present all information as a whole (

Kalakoski et al. 2019). That is, an important element of managing a company’s financial security is an objective and early determination of its level, which cannot be done without a comprehensive analysis of both the company’s financial and non-financial indicators. ‘Ultimately, every company can contain risks that exist outside of the balance sheet’ (

Simply Wall St. 2020)

In this case, it is necessary to determine who assesses financial security and for what purpose. For example, company management definitely perceives its level even without calculating indicators, since it constantly participates in the enterprise’s processes, understands where there are strengths and weaknesses and receives daily operational information not only in consolidated form, but also in disaggregated form from various departments and spheres, creating the overall picture of the enterprise; the reporting data only back up it with actual indicators. Nevertheless, other stakeholders, who do not always have access to operational data, can only use reporting information, which is lags behind a real situation that can change almost every second.

At the same time, it is necessary to pay tribute to the results of economic analysis and evaluation of important indices (or, as they are often called in publications on methodology for assessing financial security, indicators), since they are an objective reflection of the enterprise’s financial condition, provided the input and output data, for example, reporting, are reliable. Modern information accounting systems at enterprises allow the analysis results to be displayed at any time. In the meantime, with the proper level of automation, indicators for assessing financial condition can be displayed in real time for various groups of stakeholders with an appropriate level of access to data.

To analyze the state of a company’s financial security, it is necessary to audit the equipment involved in financial transactions, infrastructure security and software reliability, organization of cash operations and its physical protection and employee awareness of measures that will prevent possible financial losses depending on the type of enterprise.

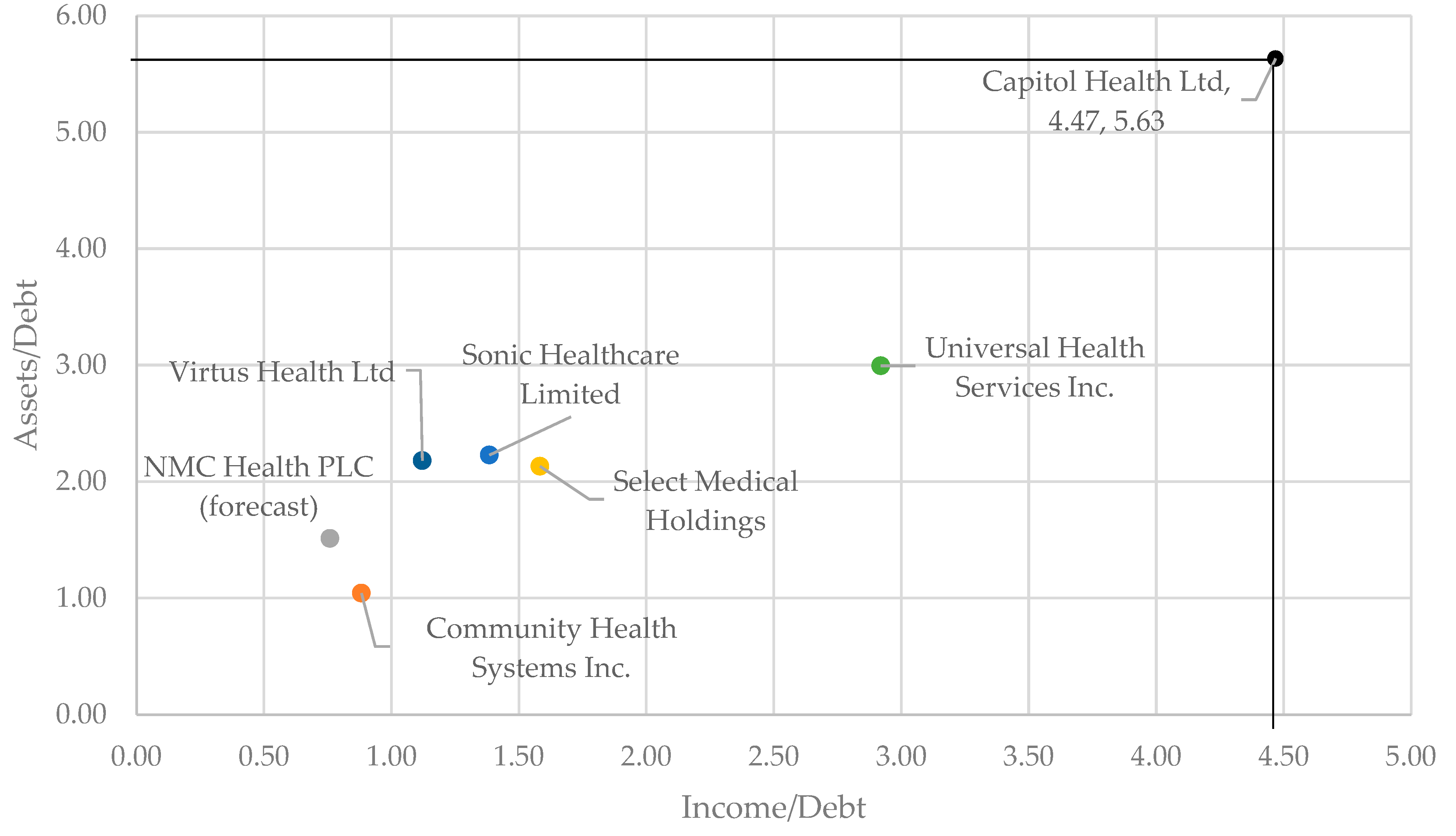

Table 1 shows the management’s effectiveness of financial pillars (income, debt and earnings) using the DEA method of medical companies, given the relevance of the issue of medical providing in conditions of the COVID-19 pandemic.

The list of companies is taken from the resource AnnualReports.com (

Hospitals Companies 2020) Americas largest annual report service.

The performance ratios of ‘debt participation in income’ and ‘debt participation in assets’ suggests that Capitol Health, Ltd. is the most efficient hospital at debt management.

The graph (

Figure 1) shows the position represented by Capitol Health, Ltd. which demonstrates a level of efficiency superior to all the other branches.

The straight lines from Capitol Health, Ltd. to the Y and X axis represent the efficiency frontier which represents a standard of best achieved performance and is a threshold against which to measure the performance of all the other hospitals.

Can such an enterprise be called financially secure? It is obvious, yes if decisions are made by the relevant persons—people who have, in addition to data, also the feeling that such debt can be repaid despite the losses of the company. It is confirmed that in 2019 the company already had a net profit of $US 27.5 million.

Could the decision to increase the debt lead to other results of Capitol Health, Ltd.? Obviously, if there were unforeseen circumstances caused by a pandemic or other unforeseen crises and measures to overcome it.

During March 2020, the value of shares of Capitol Health, Ltd. decreased by 48% (

Capitol Health Ltd. 2020). This has led, among other things, to problems with the company’s revenue, it ‘has had to make staff across the business take a combination of annual leave and leave without pay’ (

Douglas 2020). It, ‘together with other management initiatives, represent an operating expenditure saving of around 40 per cent, consistent with the trend in revenue’ (

Douglas 2020).

This means, again, that no one could have predicted a pandemic scenario.

This graph displays only the smallest part of the cost management system, more precisely, it practically does not say anything, because the data for its construction is taken from financial statements for previous periods. Since then, many parameters have changed, external and internal factors that affect the level of financial security of the company as a whole and its position on this chart in particular (

Simply Wall St. 2020).

Only a system that continuously analyzes financial indicators and the external environment can provide objective data for a particular enterprise (

Raguseo et al. 2020). Today, only artificial intelligence can be such a system, which has access both to the financial system of the company and to the Big Data, collecting, analyzing information and drawing conclusions based on it (

Kulakli and Osmanaj 2020;

Sivarajah et al. 2017), especially deep learning algorithm which has a major advantage compared to other traditional shallow machine learning algorithms (

Jing et al. 2018).

In this case—in combination with 5G technology—such an analysis can be really operational, because the information, in particular, in the Big Data change every fraction of a second. Thanks to this technology with ultra-low latency (round time of less than a microsecond) (

Morgado et al. 2018) the financial indicator’s analysis will be really objective.

Such instantaneous changes in the data require, however, the same instantaneous decisions, which, however, cannot be made by a person, much less a group of experts. Given the time needed for reflection, discussion, etc. Of course, today key financial decisions are not made too quickly, but there are a number of problems that can be solved instantly by a certain algorithm. For example, the transfer of budget funds from articles for the purchase of non-critical equipment for staff such as a new mobile phone, TV for the purchase of critical personal protective equipment, ventilators, could be accepted without delay and additional discussions.

Or keep funds in accounts to maintain the level of financial security during the coming crisis. Such decisions will not adversely affect the financial security of the enterprise.

To perform such functions, it is advisable to involve artificial intelligence, which would perform the described tasks.

Olson et al. (

2012) found decision trees are relatively more accurate compared to artificial neural networks and support vector machines. The benefits of a decision tree are also to some extent evidenced by the results of research by

Butaru et al. (

2016). It is important, however, to note that there is no ideal algorithm either, as

Königstorfer and Thalmann (

2020) notes, for assessing credit risk in particular or the financial security of an entity as a whole, because ‘the performance of different algorithms, as well as the best performing algorithm, differ depending on the dataset used in the training and testing process’ (

Butaru et al. 2016;

Königstorfer and Thalmann 2020).

Financial security, as a process, focuses on reducing or eliminating monetary risks. In this case, management methods and risk management, which is not uncertain, should be applied and vice versa: the probability of its occurrence should be evaluated, and the necessary measures taken to minimize (or maximize) the business impact, in particular, financial security. Risk should not be avoided, but foreseen to reduce or increase its level, depending on its nature.

Once again, the research framework established that financial security can be considered a state, a process and a perception.

The author contemplates separately the aspects that should be assessed in the framework of measures for analyzing the state of a company’s financial security.

The techniques involved in an enterprise’s monetary circulation depend, of course, on the types and forms of enterprise activities.

For example, a large supermarket can sell goods worth 300–500 thousand euros in one day (

Melnychenko 2015). Some payments will be in cash, while others will be cashless. For example, on holidays, in evenings or during hours with the largest volume of customers, such a store can simultaneously employ up to 30 cash desks, capable of serving up to 5000 customers a day. These statistics show that an average of about 160 customers a day or up to 3–5 thousand euros of revenue go through each cash register. In this case, there are specific figures for the risk of financial losses due to issues such as idle equipment at one or 10 cash registers. This factor directly affects a company’s financial security, as do the losses that can occur from unsold goods or spoiled food products.

There is another point to be made here: cash equipment includes a set of interrelated elements, such as the filing system, scanning, data processing (cashier’s work computer and data servers), cash storage and payment terminals. Each also influences the amount of goods and income, the loss of which may indicate a decrease in financial security, in this case, of a trading company. According to our research, 43% of customer service time at a cashier is spent on goods payment using a mixture of payments (cash and non-cash). Payment times will further increase if an outdated terminal is used, such as one without a contactless payment function or a cash-only register.

Returning to the amounts of money cashiers can process in a day, attention should be paid to the lion’s share of cash payments, which are preferred by customers for various reasons. This preference prevents supermarkets from eliminating this form of payment without considering other illegal aspects of cash use in a trading company’s circulation. If time spent on servicing payments with one cashier could be significantly reduced, it would lead to optimizing the cashiers’ staff and\or increasing revenue by increasing the number of customers served by one cashier.

The amount of cash per day can be up to 50% of revenue—or about 150–250 thousand euros in certain circumstances. This cash should be properly accounted for, verified, processed, saved and, for example, transferred to storage. Establishing the cashier’s work to avoid error or fraud that may cause the enterprise to lose money requires considerable effort and is also directly related to a company’s financial security.

In addition, the cashiers’ qualifications and responsibility should be, first, verified and second, monitored, since the conformity of financial flows and preservation of values depend on their work, actions and skills. One example is determining banknote authenticity. Bank tellers receive training on how to work with cash, detect fake banknotes, etc. Supermarket employers do not pay as much attention to teaching their cashiers how to work properly with funds, payment terminals and the like. On the contrary, it is often possible to find workers ignorant about the product line, nomenclature and assortment—or that lack understanding of the operation principles of technology.

This situation can be avoided not only by training cashiers, but also by properly organizing their work. A good example of this is the German Lidl chain of stores: with six to eight cash desks, one or two cashiers are constantly actively serving the store’s needs. At the same time, cash desks that are not currently engaged can be quickly connected to work; employees with the access rights to work at the cash desk also work with goods, process them, lay out, replace and deliver. In addition, almost every employee is constantly communicating with other store employees. The first allows cashiers to competently possess information about products, while the second provides timely responses by all personnel to requests arising from customer service at the cash register.

The bank at which the company maintains its operating activities account is an important element for ensuring a company’s financial security. This aspect is rarely considered in economically developed countries, but for developing countries it has become relevant in recent years since a number of banks were withdrawn from the market, liquidated or otherwise suspended. A significant number of entrepreneurs experienced times when, based on the conditions of usual activities and the proper level of financial security from the perspective of economic analysis, their state changed sharply from positive to extremely negative: banks blocked entrepreneurs’ funds for daily activities due to the introduction of temporary administrations and termination of financial transactions with customer accounts.

The process of reducing or eliminating monetary risks in the practical field is given considerable attention by insurance companies; one of their main goals is to insure such risks and determine a company’s financial security. All activities of an insurance company directly depend on a correct assessment.

Thus, to develop a new risk research methodology, AXA insurance company has applied a risk-level identification system based on an enterprise survey to determine respondents’ risk perceptions. At the same time, ranking increases and decreases reflect respondents’ perceptions of risk, but not actual changes in the risk assessment itself. One perceived risk may not change at all, but another may be perceived as higher or lower, thus affecting other risks (

AXA and Eurasia Group 2019).

The overall ranking of new risks depends on both the number of votes for a given risk and its risk score. Formally, for any given risk i, the assessment is as follows (

AXA and Eurasia Group 2019):

where

n is the number of respondents who share the same concern about risk

i, and point

i corresponds to the number of points assigned to the ranked risk position

i.

Ping An Insurance (Group), another well-known insurance company, uses a smart risk monitoring system, employing technology, IT systems, modeling, big data analytics and artificial intelligence; conducts comprehensive risk assessments; and implements controls to work and process management. Technology applications in areas such as counterparty monitoring of business transactions, valuation, blacklist updating and systematic risk assessment of the retail business allow it to further automate risk management tasks and support early detection and mitigation. Applying technologies based on using these innovations collectively prevented approximately 15 million frauds, preventing more than

$45 billion in losses (

Kwilinski 2019;

Melnychenko and Hartinger 2017;

Ping An Insurance (Group) Company of China 2018).

The perception of financial security by company managers plays an important role in ensuring and shaping it as a whole. The perception of its level depends on the person’s experience, intuition, knowledge and general perception, which defines and forms his/her professional judgment.

Among best practices, financial security for employees is enhanced by health insurance, bonuses, physical activity programs, health recreation, future retirement benefits and participation in professional conferences and seminars. Using economic analysis indices and indicators to increase the levels of employee financial security, in particular and that of the companies where they work, will not succeed, because financial security is already formed at the level of each person’s perception of the state and internal sense of this security. At the same time, its formation is influenced by the whole spectrum of psychological aspects, including today’s popular cognitive distortion, the obvious disadvantage of a formal logical situation, and the unreasonable transfer of stereotypes to issues that do not relate to their validity.

It was noted above that financial security depends mainly on the level of financial literacy and its understanding, as well as the fact that this term in the literature refers to a state, that is, when subjects are able to balance their basic needs and inevitable expenses, considering physiological and social needs as well as cultural norms. Therefore, the lower the needs and sense of cultural norms, the easier it is to reach such a state and a higher level of financial security.

Indeed, a person with a low level of social responsibility will not be worried about his appearance and other attributes of a ‘successful life’. On the other hand, for example, deeply religious people will also not be concerned with the issues of tomorrow: they have important feelings and opportunities ‘here and now’. However, the issue of security, including financial security, has the prospect of being able not to meet one’s needs, not only today, but also tomorrow, since the ability to cover them in the current period without the understanding and confidence that they can be financed in the future will lead to an incomplete sense of financial security. After all, the next period may be in the near future, a fact the subject will undoubtedly remember, and this will create a feeling of anxiety that cannot be assessed at current possibilities as a safe (financial) condition. Thus, the main criterion for financial security is its perception.

The foregoing discussion suggests analysis of financial indicators based on economic analysis data does not allow assessing a company’s financial security in an unambiguous and objective way and that its level is instead determined based on the perceptions of those who evaluate it, and further, that it is impossible to obtain reliability based solely on subjective judgments. Consequently, I propose use of the expert method as the most objective approach for assessing a company’s financial security. This conclusion is based on early research into the application of well-known qualitative methods based on expert opinion such as focus group (

Blackburn and Stokes 2000;

Goldman 1962;

Krueger 2015;

Robinson 2001), Delphi method (

Dalkey and Helmer 1963;

Parente et al. 1984;

Rowe and Wright 1999;

Turoff 1970).

This approach is not new or unique, because this is how almost all and especially large, businesses have worked successfully for a long time, creating collegial bodies for decision-making (boards, boards of directors, supervisory boards) (

Das et al. 2020). However, this method is characterized by shortcomings and features that are inherent in the principles of behavioral economics, which should be considered in more detail.

It is clear that experts’ perceptions of the level of this important indicator cannot be formed only on the basis of even their significant experience, but should also consider the company’s objective control data derived from its financial, management and other reporting—those indices and indicators that reflect the state of financial security for a certain (adequate) period of its functioning.

The key question is who and for what purposes the company’s financial security is being assessed. The experts’ final decisions about the level of financial security will depend on the set goals and tasks, as well as their formulations (an example of Asian disease (

Thaler 2015)). This is due to the cognitive limitations of each expert group member.

Therefore, I model a situation where the level of financial security is determined by a group of experts, which includes the business owners. The decision relates to the opportunity to invest in a new line of business, which is expected to either bring the owners more than 100% profit or not pay off. Considering the endowment effect (

Thaler 2015), there is a high probability that the experts will assess the level of financial security as not high enough to take the risk, owing to the fact that the investment may not be returned. The principle of loss aversion becomes a priority.

Such a decision by stakeholders will also be reinforced by a model of intertemporal choice—the discounted utility model—because consumption now is indeed more important than consumption later (

Thaler 2015). It looks unattractive to the average person to abandon resources now for investing and obtain (perhaps) more in the future, even if more goods. At the same time, almost every person has a heuristic way of thinking (

Thaler 2015); examples and the evidence most commonly encountered by this person and other cognitive distortions come to mind while solving certain problems.

The easiest way to solve such a problem would be to include an expert team of people who would at least not depend on the endowment effect, that is, would not have a sense of loss when making an irrational decision that could lead to losses. This approach would include involving paid consultants; not all businesses can afford this, some for financial reasons, others because of management overconfidence. It is important, however, to keep in mind the ‘inside view’ and ‘outside view’ principle introduced by

Kahneman (

2011), when experts make decisions based on two deviations: bold forecasts or timid choices. The first is when they evaluate a problem as a team member, stakeholder, owner or manager and are limited by a number of cognitive distortions and the second is from the position of an external independent expert, considering other experiences, examples and views. Using various necessary pieces of information, the competence of the expert ‘outside view’ will be more objective and his/her professional judgment will lead to more successful decisions.

Therefore, the level of a company’s financial security is ultimately determined by just two levels of ‘high enough’ and ‘not high enough’ when making concrete decisions in specific situations. This level is defined by a group of people or one person entrusted with such powers for the company. It is possible to determine the level of a company’s financial security using a certain numeric value, for example, using an integral indicator or a set of indices, coefficients and indicators based on different methods. However, although these indicators and their normative values can be thoroughly substantiated, decision-makers will only take them into account and not consider them explicitly as dogma.

Thus, the most important issue is formulating the request to decision-makers and justifying its consequences.

- -

improving the quality of data processing: considering, apart from important noticeable and significant data, also important imperceptible, secondary noticeable and imperceptible, as well as even insignificant, omissible and imperceptible data for analyzing information and identifying the truth;

- -

increasing the productivity of the analytics system by analysis of the information, associated with the enterprise, round-the-clock, without fatigue, distraction, with a stable high speed of data processing;

- -

acceleration of reaction to changes in the information space and considering all possible factors that influence or have influenced the decision-making associated with the enterprise, reduce the risk of errors caused by obsolete knowledge.

Performing these functions depends on specific tasks according to the type of control object. Thus, before setting the task to artificial intelligence, it is necessary to classify the object according to different features: volume, size, scale, level, etc. (

Melnychenko 2019;

Omoteso 2012).

For example, the control over the correctness of the calculation and payment of value added tax is appropriate to assign to artificial intelligence, in particular, in part of the comparison of information in the regulations, primary documents, agreements with counterparties, budget movement report for funds in bank accounts, tax returns, etc., when it comes to a separate enterprise. Otherwise, it is advisable to describe the level of information support when it comes to state-level control. In addition, the information from the tax authorities, data from registers of different levels, etc. should be used as well (

Issa et al. 2016;

Melnychenko 2019).

- -

analysis of complete information about the firm and its individual elements, including indirect, in particular, Big Data research;

- -

comparison of the information about object of control with the analyzed information;

- -

identify inconsistencies that lead to misstatements in the financial or other business reporting of the entity.

5. Conclusions

This study substantiates that the level of a company’s financial security depends not so much on its activity indicators, but on how it is perceived by decision-makers and other stakeholders. At the same time, this perception is formed by the stakeholder’s continuous participation in operations and constant monitoring of financial indicators, the study of current approaches to enterprise management, changes in the environment and market conditions. The role of economic analysis in assessing a company’s financial security as a state is not in its complex study, but in the economic indicators presented and the processing of quantitative data about the company’s financial security. Instead, to speak of a comprehensive and thorough study of the level of financial security solely based on economic analysis would be incorrect and unreliable. Analysis of indices and indicators that are based on financial or management reporting provide only a cursory view of the problem or may even distort the overall picture, as they are measured at a particular point in time. For example, liquidity indicators change in certain groups of businesses and a country’s economic or political environment can transform a solidly liquid company into an absolutely illiquid one in a few moments. However, considering the previous data of economic analysis without bearing in mind other aspects makes it possible to make fatal decisions for a company. Although, of course, such a scenario is impossible, since behind each enterprise there are people whose decisions and experience depend on its further development; practice shows that such people are not oriented solely to economic analysis data without context to assess the situation in a country’s economy or the world in general. Their experience and perceptions of financial security are essential in decision-making.

The same applies to artificial intelligence, which is able to process huge amounts of information about the enterprise’s activities and make certain forecasts and conclusions, but not able to think and predict that in enterprise is the most important skill of a manager.

Thus, this paper presents the argument that the expert method of assessing a company’s financial security is the most objective one; however, it has disadvantages associated with people’s cognitive limitations.

I also suggest that the expert method helps in mitigating the influence of behavioral biases, thereby improving the quality of assessment of an enterprise’s financial security. Taking into account the cognitive limitations inherent in people contributes to a sustainable and responsible evaluation regarding the level of financial security of the enterprise.

Let us focus on the possibility of using machine learning methods to identify the cognitive limitations of stakeholders who make decisions about the level of financial security of the enterprise and their leveling.

Assume that the decision to declare an enterprise financially secure or not is made by a group of experts, each of whom has his or her own opinion on the matter. In this case, decisions are made in two, as I said above, possible variations: “high enough” and “not high enough” level of financial security for a particular situation, which may relate to investment, staff expansion, sale of shares. Each of the cognitive illusions can "distort" the opinion of the expert to the contrary.

Thus, the best solution would be to create artificial intelligence, which would eliminate the cognitive limitations and illusions of experts when making decisions about the level of financial security of the enterprise.

There are 21 such illusions in the literature (

Pohl 2004), the presence of each of them does not exclude the presence of the other. Thus, in order to level them, it would first be necessary to expose them, identify them, classify them and determine their impact on the decisions made.

Each of these stages would require significant effort, time and other resources and given the need for financial decisions that are often instantaneous, this task seems unsolvable today.

Further research on the perception of a company’s financial security based on the principles of behavioral economics should focus on interviewing entrepreneurs to supplement and refine the approach of using statistical analysis methods, as well as financial security research into neurofinance.

This study is a review article, therefore, data based on financial statements and input variables are not presented in the work. However, still remains the need for a more detailed study of this topic for testing a company’s financial security on accounting data (depreciation methods, the turnover rate, etc.), which has different degrees of influence on the errors in human judgment in future research, empirical proofs that the expert method of assessing a company’s financial security is the most objective one. It is important to keep in mind the accuracy of the model in terms of artificial intelligence, machine learning and neural networks depends largely on the weights designed by the model, such as structure, hidden layers, etc. Therefore, in future research, a model of corporate financial security issues and the reduction of human errors when making decisions regarding the level of enterprise’s financial security should be developed.

To build a model of the work of artificial intelligence in assessing the enterprises’ financial security, further research should also use developments in the field of neurofinance as a defined research field that seeks to understand financial decision-making, combining psychology and neuroscience with finance theories (

Ardalan 2018;

Miendlarzewska et al. 2019;

Peterson 2010). Its apologists argue that the human brain, based on developmental processes throughout its existence, has not evolved as a creature that makes optimal financial decisions, and the issue of money is secondary to primary needs. However, the main goal of neurofinance is to further refine models of decision-making and behavior in the market by investigating how the brain processes information and makes decisions (

Miendlarzewska et al. 2019). This approach to decision-making is related not so much to psychology as to neuroscience and physiology, although psychology issues are also relevant to this area.

{kind=link}