Risk Capital and Emerging Technologies: Innovation and Investment Patterns Based on Artificial Intelligence Patent Data Analysis

Abstract

1. Introduction

2. Theory Development and Hypotheses

2.1. Search

2.2. Risk Capital and the Emergence of AI

2.3. Peculiarities of Patenting AI Software

2.4. Characteristics of AI Patents That Are Selected by VCs

2.5. Knowledge Coupling across Technological Boundaries

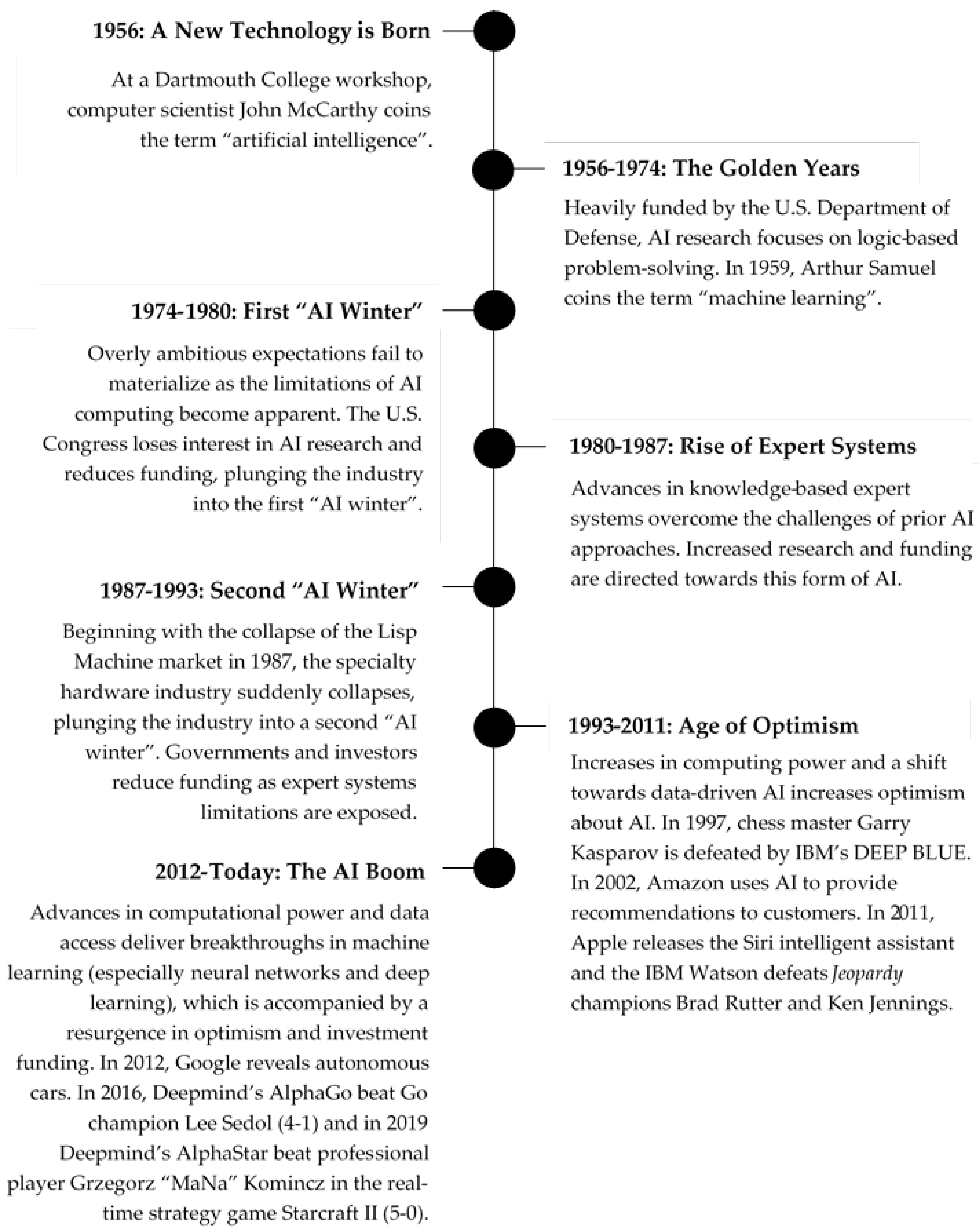

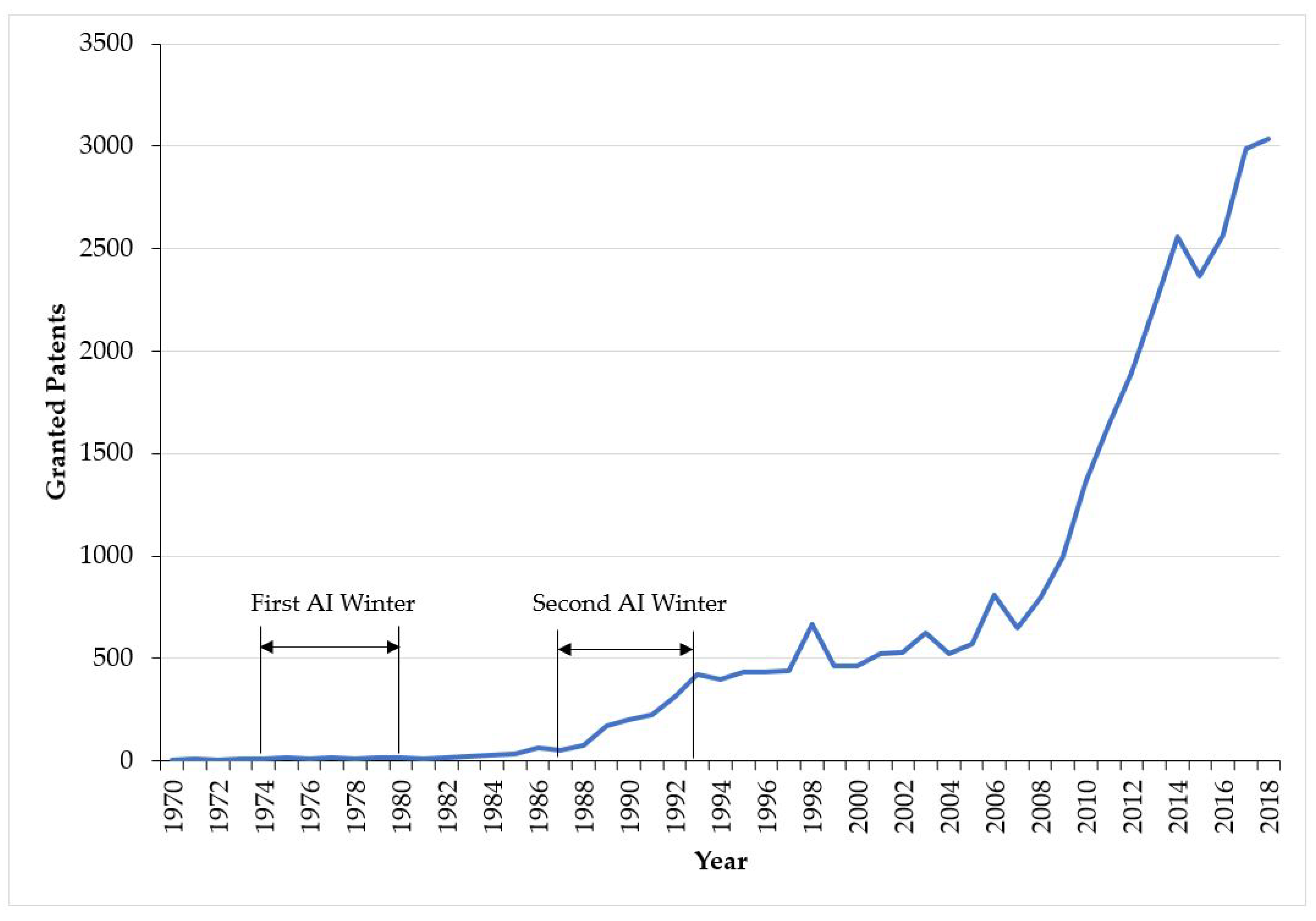

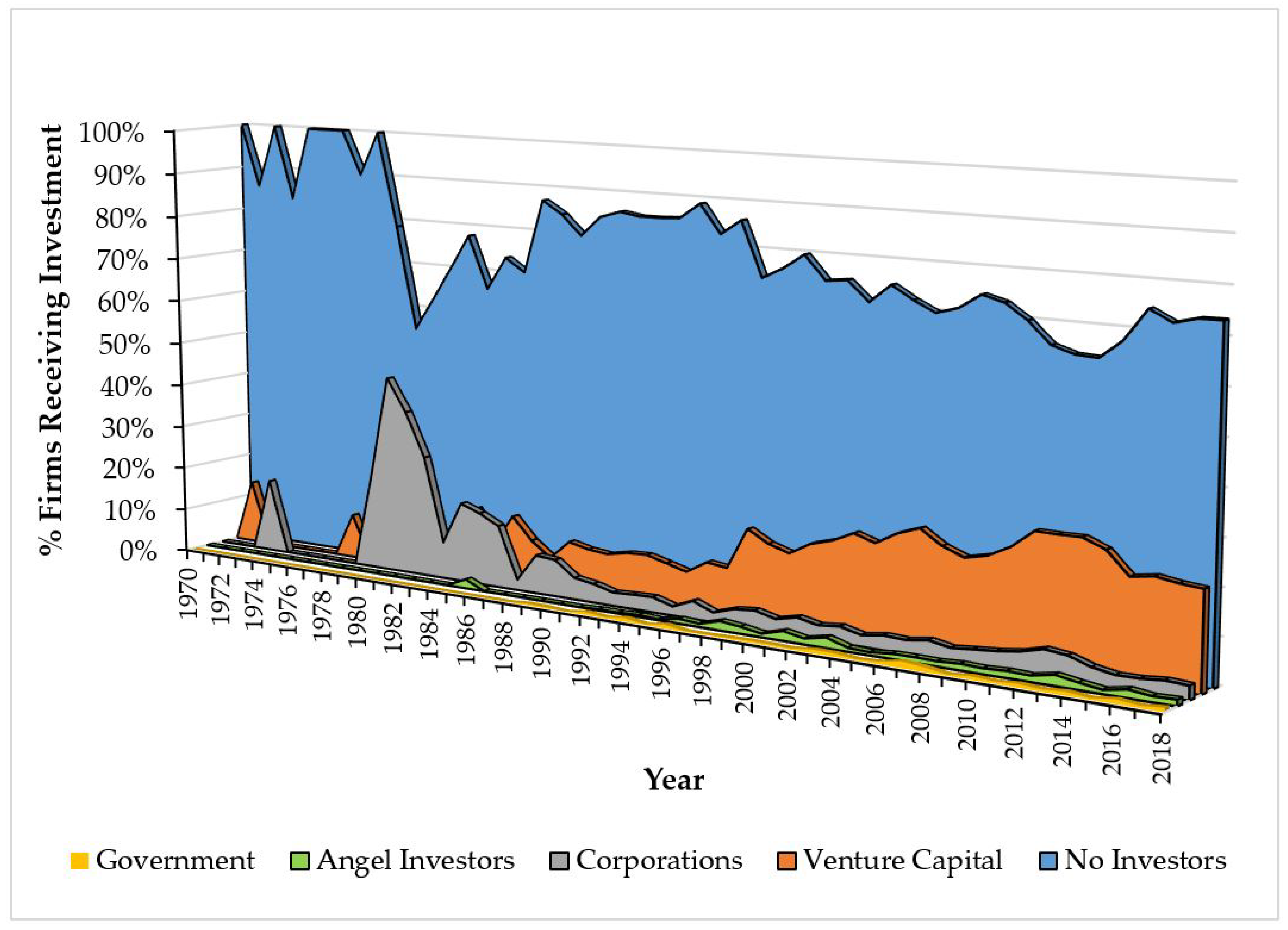

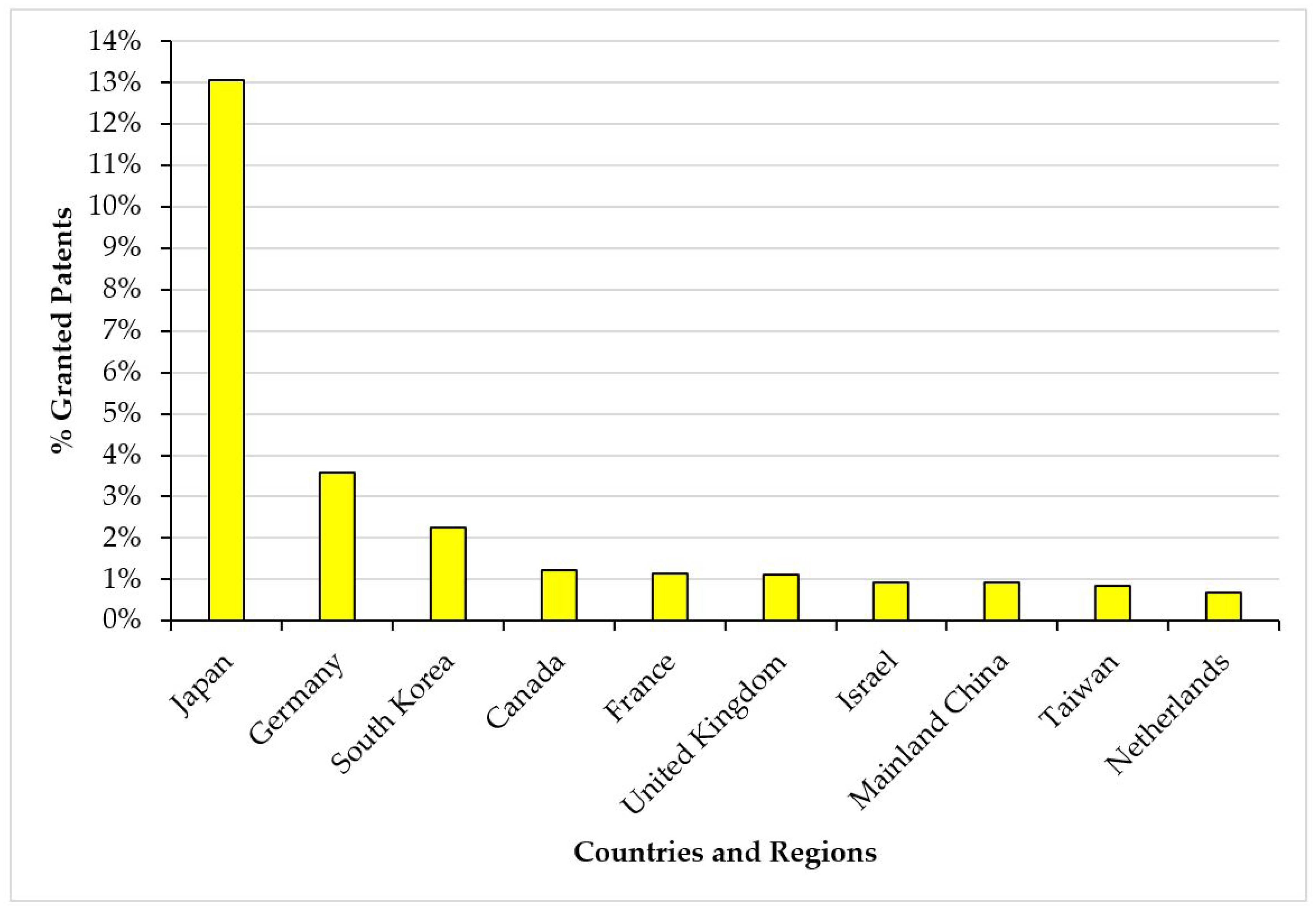

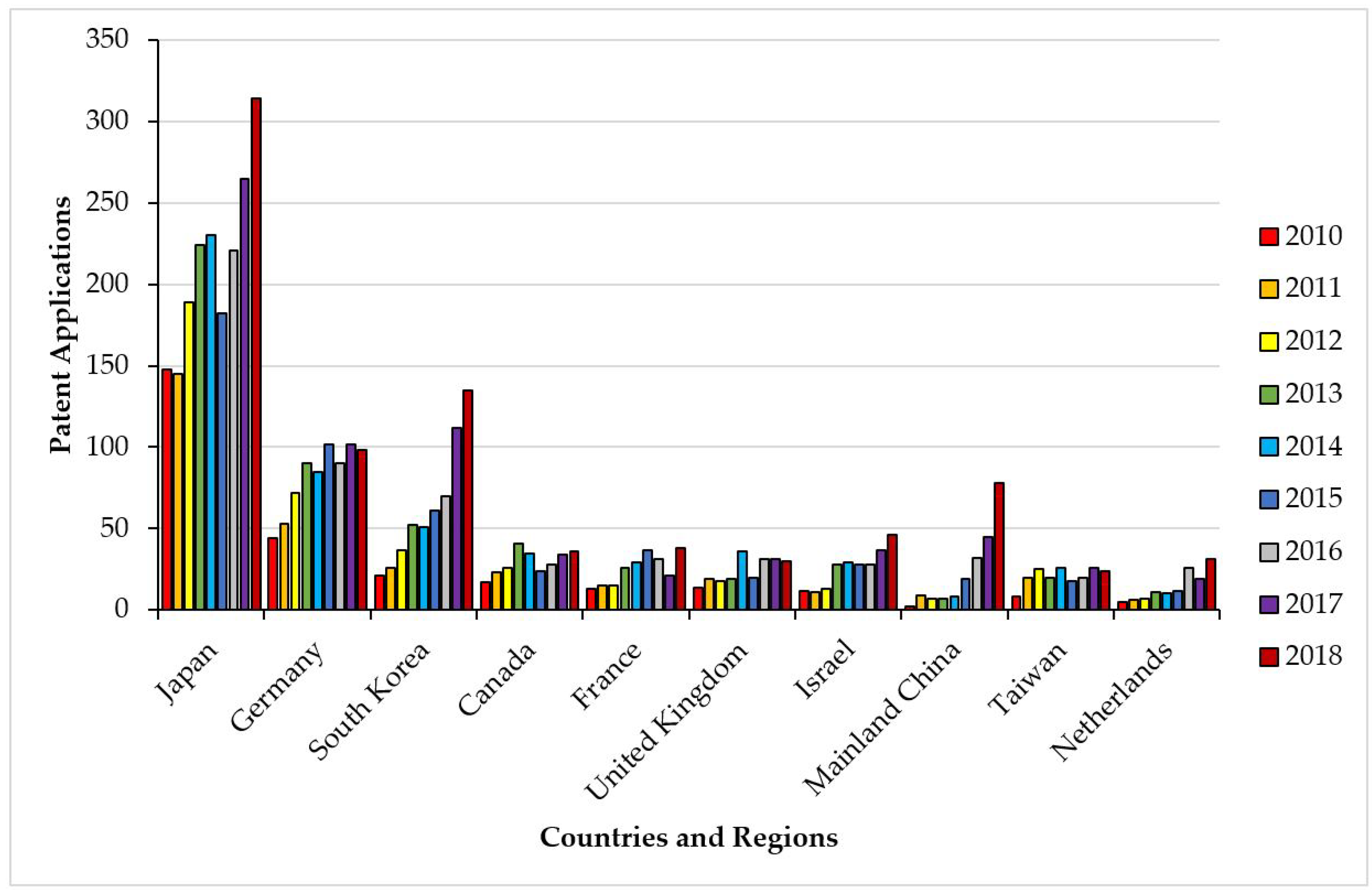

3. Sample and Technology Innovation Characteristics

Technology Innovation Characteristics

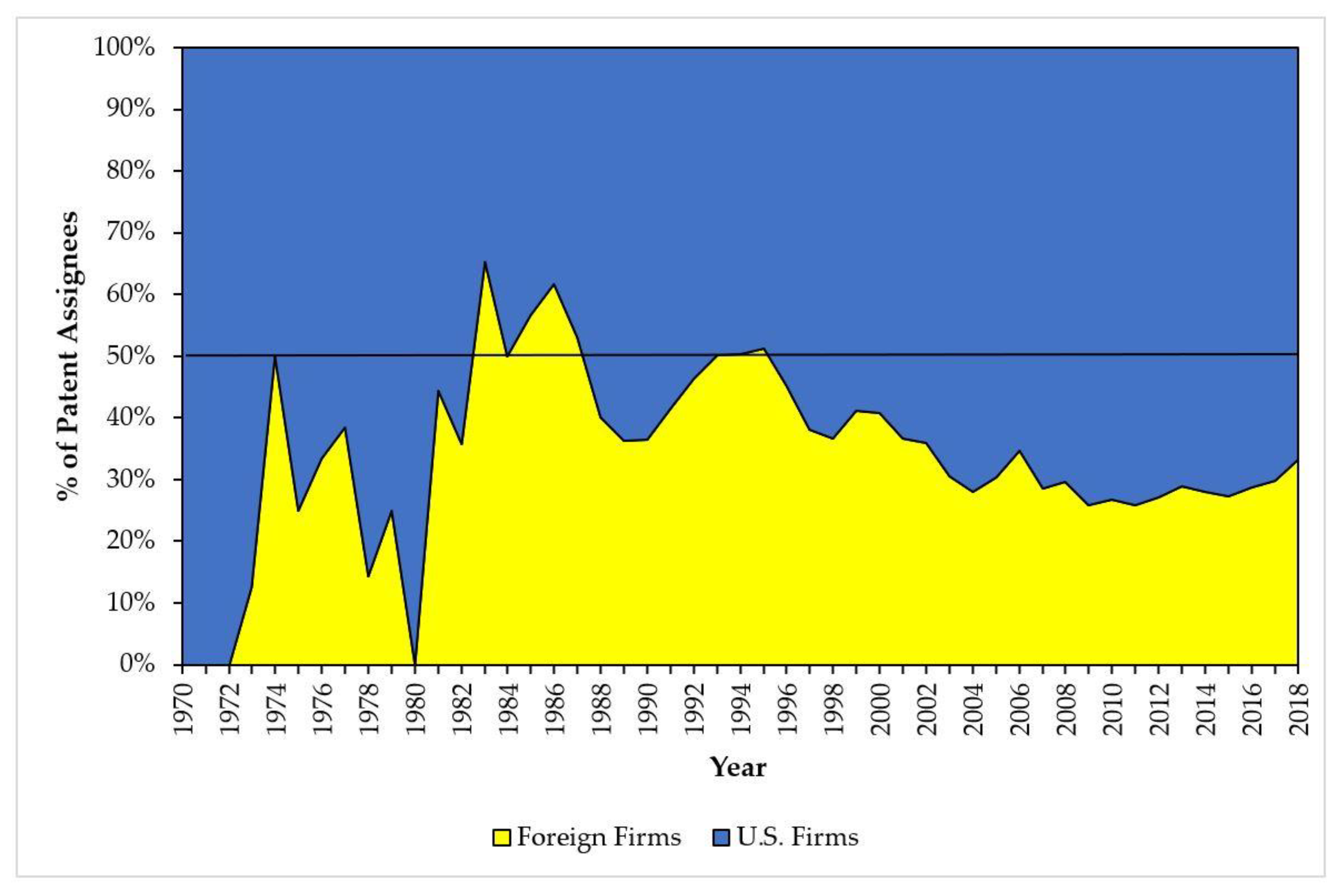

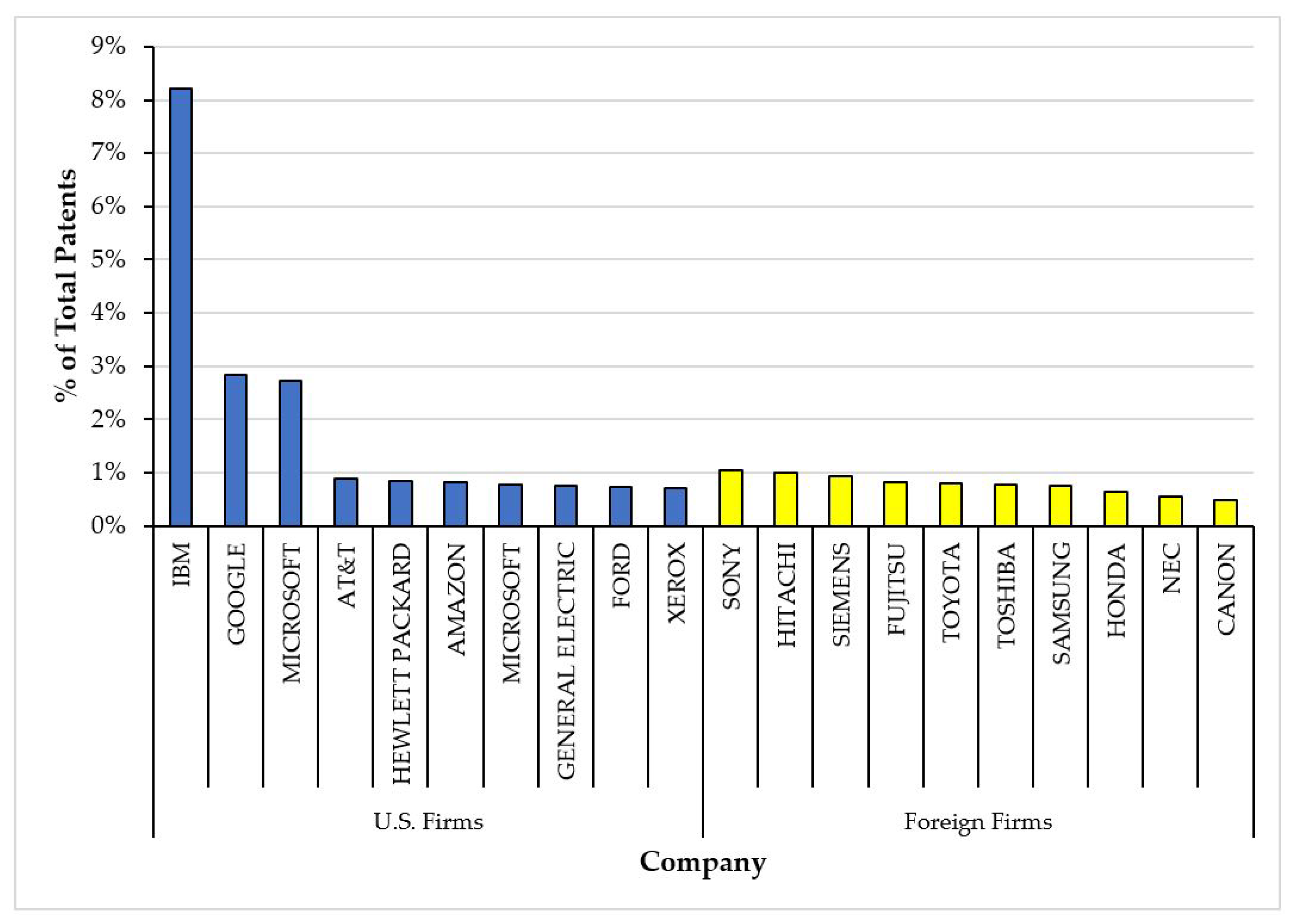

4. Globalization, Spillovers, and a Changing Game

5. Methods

5.1. Dependent Variable

5.2. Independent Variables

5.2.1. Technology Classes

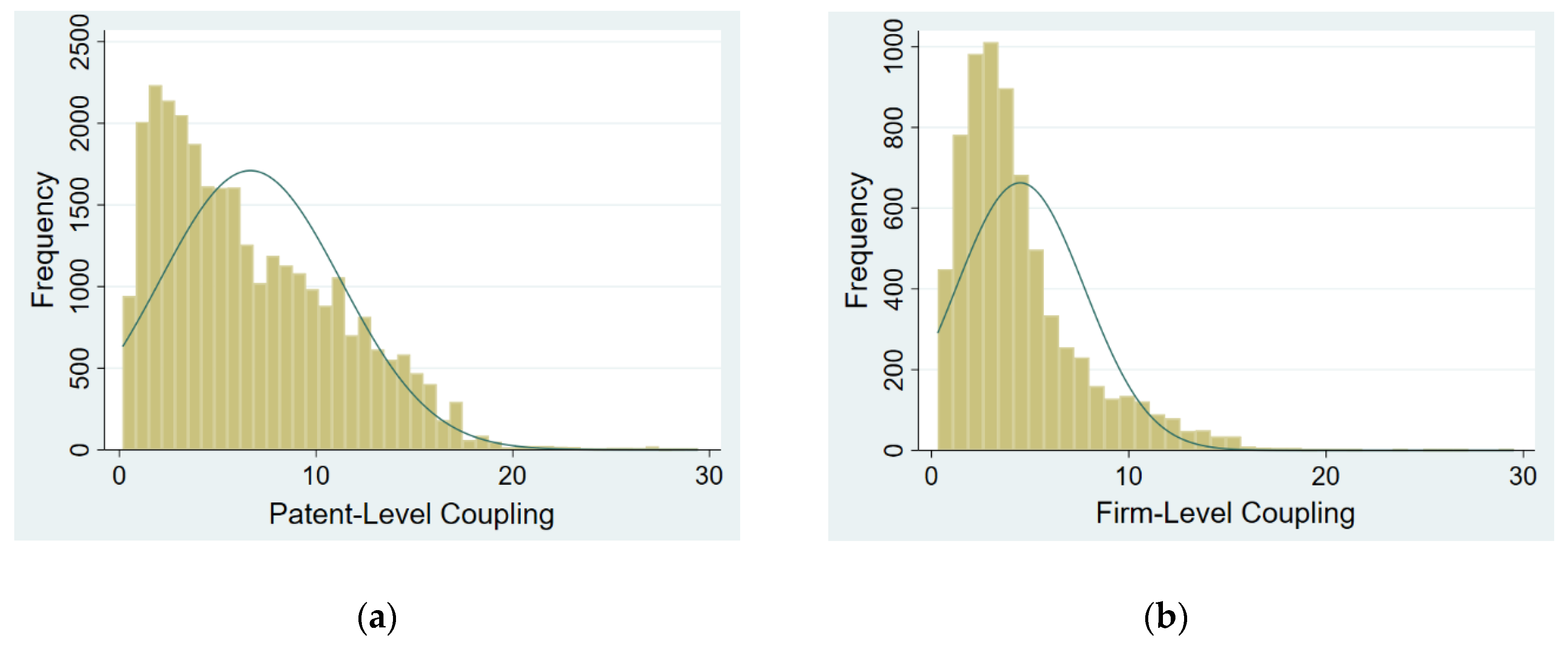

5.2.2. Coupling

- Ei is the ease of recombination of technology class i;

- Ej is the ease of recombination of patent j;

- Cx is the coupling of firm x.

5.2.3. Control Variables

5.2.4. Estimation Approach

6. Findings

7. Discussion

7.1. Contributions

7.2. Practical Implications

7.3. Limitations and Future Research

8. Conclusions

Author Contributions

Funding

Acknowledgments

Conflicts of Interest

Appendix A

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| A61B5/7264 | G01N2201/1296 | G06F17/289 | G06N5/027 | H01J2237/30427 |

| A61B5/7267 | G01N29/4481 | G06F17/30029 | G06N5/04 | H01M8/04992 |

| A63F13/67 | G01N33/0034 | G06F17/30247 | G06N5/043 | H02H1/0092 |

| B23K31/006 | G01R31/2846 | G06F17/30522 | G06N5/048 | H02P21/0014 |

| B25J9/161 | G01R31/2848 | G06F17/3053 | G06N7/005 | H02P23/0018 |

| B29C2945/76979 | G01R31/3651 | G06F17/30654 | G06N7/02 | H03H2017/0208 |

| B29C66/965 | G01S7/417 | G06F17/30663 | G06N7/046 | H03H2222/04 |

| B60G2600/1876 | G05B13/027 | G06F17/30702 | G06N7/06 | H042012/5686 |

| B60G2600/1878 | G05B13/0275 | G06F17/30705 | G06T2207/20081 | H042025/03464 |

| B60G2600/1879 | G05B13/028 | G06F17/30713 | G06T2207/20084 | H04L2025/03554 |

| B60W30/06 | G05B13/0285 | G06F17/30743 | G06T2207/30236 | H04L25/0254 |

| B60W30/10 | G05B13/029 | G06F2207/4824 | G06T2207/30248 | H04L25/03165 |

| B60W30/12 | G05B13/0295 | G06K7/1482 | G06T2207/30268 | H04L41/16 |

| B60W30/14 | G05B2219/33002 | G06K9 | G06T3/4046 | H04L45/08 |

| B60W30/17 | G05D1/00 | G06N/20 | G06T9/002 | H04N21/4662 |

| B62D15/0285 | G05D1/0088 | G06N20/00 | G08B29/186 | H04N21/4666 |

| B64G2001/247 | G06F11/1476 | G06N3 | G10H2250/151 | H04Q2213/054 |

| E21B2041/0028 | G06F11/2257 | G06N3/004 | G10H2250/311 | H04Q2213/13343 |

| F02D41/1405 | G06F11/2263 | G06N3/008 | G10K2210/3024 | H04Q2213/343 |

| F03D7/046 | G06F15/18 | G06N3/02 | G10K2210/3038 | H04R25/507 |

| F05B2270/707 | G06F17/16 | G06N3/0427 | G10L15/00 | Y10S128/924 |

| F05B2270/709 | G06F17/2282 | G06N3/0436 | G10L15/16 | Y10S128/925 |

| F05D2270/709 | G06F17/27 | G06N3/0454 | G10L17/00 | Y10S706 |

| F16H2061/0081 | G06F17/2795 | G06N3/088 | G10L25/30 | |

| F16H2061/0084 | G06F17/28 | G06N5/003 | G11B20/10518 |

Appendix B

- Consider A9.com Inc. patent US9928466 that was granted in 2018. Patent US9928466 is associated with two technological domains as indicated by CPC classes G06F16 and G06N7. Each CPC class represents a knowledge component. Prior to the firm’s use of class G06F16, within the whole set of AI-related patents, it had been recombined 3718 times with 188 other components. This results in an observed ease of recombination score of 188/3718 = 0.051 (see Equation (A1) below). Similarly, CPC class G06N7 had been recombined 1769 times with 176 other components. This results in an observed ease of recombination score of 176/1769 = 0.099 (see Equation (A2) below).

- Using the values calculated above, we can then determine the patent’s observed ease of recombination. This is calculated as the sum of the individual class recombination scores divided by the number of classes assigned to the patent. This results in a patent ease of recombination score of (0.051 + 0.099)/2 = 0.075 (see Equation (A3) below).

- Finally, we compute the firm-level measure of coupling. For example, A9.com Inc. had 9 patents granted up to 2018 and the sum of observed ease of recombination of these patents was 1.439 (following the same procedure as outlined above). Thus, the coupling of A9.com Inc. in 2018 was 9/1.439 = 6.254 (see Equation (A4) below).

References

- Acs, Zoltan J., Pontus Braunerhjelm, David B. Audretsch, and Bo Carlsson. 2009. The knowledge spillover theory of entrepreneurship. Small Business Economics 32: 15–30. [Google Scholar] [CrossRef]

- Agarwal, Rajshree, David Audretsch, and Mitra Barun Sarkar. 2010. Knowledge spillovers and strategic entrepreneurship. Strategic Entrepreneurship Journal 4: 271–83. [Google Scholar] [CrossRef]

- Alice Corp. v. CLS Bank International. 2014. 573 U.S. 208. Supreme Court. Available online: https://www.supremecourt.gov/opinions/13pdf/13-298_7lh8.pdf (accessed on 13 December 2019).

- Alphabet, Inc. 2018. Form 10-K 2018. Available online: https://www.sec.gov/Archives/edgar/data/1652044/000165204419000004/goog10-kq42018.htm#s6C1DB95EDB3C5C7998B5E96D339C677B (accessed on 13 December 2019).

- Anderson, Philip, and Michael L. Tushman. 1990. Technological discontinuities and dominant designs: A cyclical model of technological change. Administrative Science Quarterly 35: 604–33. [Google Scholar] [CrossRef]

- Anton, James J., and Dennis A. Yao. 1994. Expropriation and inventions: Appropriable rents in the absence of property rights. The American Economic Review 84: 190–209. [Google Scholar]

- Arthur, W. Brian. 2009. The Nature of Technology: What It Is and How It Evolves. New York: Simon and Schuster. [Google Scholar]

- Arthur, W. Brian. 2014. Complexity and the Economy. New York: Oxford University Press. [Google Scholar]

- Arthur, W. Brian, and Wolfgang Polak. 2006. The evolution of technology within a simple computer model. Complexity 11: 23–31. [Google Scholar] [CrossRef]

- Audretsch, David B., and Erik E. Lehmann. 2005. Does the knowledge spillover theory of entrepreneurship hold for regions? Research Policy 34: 1191–202. [Google Scholar] [CrossRef]

- Barney, Jay. 1991. Firm resources and sustained competitive advantage. Journal of Management 17: 99–120. [Google Scholar] [CrossRef]

- Burk, Dan L., and Mark A. Lemley. 2002. Is patent law technology-specific. Berkeley Technology Law Journal 17: 1155–206. [Google Scholar] [CrossRef]

- CB Insights. 2019. VCs Nearly Doubled Their Investment in This Tech Last Year. Available online: https://www.cbinsights.com/research/artificial-intelligence-funding-venture-capital-2018/ (accessed on 13 December 2019).

- Christensen, Clayton M., and Joseph L. Bower. 1996. Customer power, strategic investment, and the failure of leading firms. Strategic Management Journal 17: 197–218. [Google Scholar] [CrossRef]

- Crevier, Daniel. 1993. AI: The Tumultuous History of the Search for Artificial Intelligence. New York: Basic Books. [Google Scholar]

- Crow, Lauren. 2019. The Coming Innovation Explosion. Available online: https://worldin.economist.com/article/17389/edition2020ren-zhengfei-coming-innovation-explosion (accessed on 1 December 2019).

- Dosi, Giovanni. 1988. Sources, procedures, and microeconomic effects of innovation. Journal of Economic Literature 26: 1120–71. [Google Scholar]

- Executive Order No. 13859, 84 FR 3967. 2019. Available online: https://www.federalregister.gov/documents/2019/02/14/2019-02544/maintaining-american-leadership-in-artificial-intelligence (accessed on 13 December 2019).

- Fleming, Lee. 2001. Recombinant uncertainty in technological search. Management Science 47: 117–32. [Google Scholar] [CrossRef]

- Fleming, Lee, and Olav Sorenson. 2004. Science as a map in technological search. Strategic Management Journal 25: 909–28. [Google Scholar] [CrossRef]

- Garcia-Vega, Maria. 2006. Does technological diversification promote innovation?: An empirical analysis for European firms. Research Policy 35: 230–46. [Google Scholar] [CrossRef]

- Gaston, Robert J. 1989. Finding Private Venture Capital for Your Firm. New York: John Wiley and Sons. [Google Scholar]

- Hayek, Friedrich August. 1945. The use of knowledge in society. The American Economic Review 35: 519–30. [Google Scholar]

- Henderson, Rebecca, and Iain Cockburn. 1994. Measuring competence? Exploring firm effects in pharmaceutical research. Strategic Management Journal 15: 63–84. [Google Scholar] [CrossRef]

- Hsu, David H., and Rosemarie H. Ziedonis. 2008. Patents as quality signals for entrepreneurial ventures. Academy of Management Proceedings 2008: 1–6. [Google Scholar] [CrossRef]

- Huber, George P. 1991. Organizational learning: The contributing processes and the literatures. Organization Science 2: 88–115. [Google Scholar] [CrossRef]

- Kim, Dong-Jae, and Bruce Kogut. 1996. Technological platforms and diversification. Organization Science 7: 283–301. [Google Scholar] [CrossRef]

- King, Gary, and Langche Zeng. 2001. Explaining rare events in international relations. International Organization 55: 693–715. [Google Scholar] [CrossRef]

- Kirzner, Israel M. 1973. Competition and Entrepreneurship. Chicago: University of Chicago Press. [Google Scholar]

- Kogut, Bruce, and Udo Zander. 1992. Knowledge of the firm, combinative capabilities, and the replication of technology. Organization Science 3: 383–97. [Google Scholar] [CrossRef]

- Landström, Hans. 1993. Informal risk capital in Sweden and some international comparisons. Journal of Business Venturing 8: 525–40. [Google Scholar] [CrossRef]

- Levinthal, Daniel A., and James G. March. 1993. The myopia of learning. Strategic Management Journal 14: 95–112. [Google Scholar] [CrossRef]

- Liyanage, Yohan, and Kathy Berry. 2019. Insight: Intellectual Property Challenges during an AI Boom. Available online: https://news.bloomberglaw.com/ip-law/insight-intellectual-property-challenges-during-an-ai-boom (accessed on 29 November 2019).

- March, James G. 1991. Exploration and exploitation in organizational learning. Organization Science 2: 71–87. [Google Scholar] [CrossRef]

- Mason, Colin, Richard Harrison, and Jennifer Chaloner. 1991. Informal Risk Capital in the UK: A Study of Investor Characteristics, Investment Preferences and Investment Decision-Making. Working paper. Southampton: University of Southampton. [Google Scholar]

- Nelson, Richard R. 2003. On the uneven evolution of human know-how. Research Policy 32: 909–22. [Google Scholar] [CrossRef]

- Nelson, Richard R., and Sidney G. Winter. 1982. An Evolutionary Theory of Technical Change. Cambridge: Harvard University Press. [Google Scholar]

- Newquist, Harvey P. 1994. The Brain Makers: Genius, Ego, and Greed in the Quest for Machines That Think. New York: Macmillan/SAMS. [Google Scholar]

- O’Meara, Sarah. 2019. Will China Lead the World in AI by 2030? Available online: https://www.nature.com/articles/d41586-019-02360-7 (accessed on 27 October 2019).

- Pahnke, Emily Cox, Riitta Katila, and Kathleen M. Eisenhardt. 2015. Who takes you to the dance? How partners’ institutional logics influence innovation in young firms. Administrative Science Quarterly 60: 596–633. [Google Scholar] [CrossRef]

- Peteraf, Margaret A. 1993. The cornerstones of competitive advantage: A resource-based view. Strategic Management Journal 14: 179–91. [Google Scholar] [CrossRef]

- Petkova, Antoaneta P., Anu Wadhwa, Xin Yao, and Sanjay Jain. 2014. Reputation and decision making under ambiguity: A study of US venture capital firms’ investments in the emerging clean energy sector. Academy of Management Journal 57: 422–48. [Google Scholar] [CrossRef]

- Russell, Stuart J., and Peter Norvig. 2016. Artificial Intelligence: A Modern Approach, 3rd ed. Harlow: Pearson Education Limited. [Google Scholar]

- Schumpeter, Joseph A. 1934. Capitalism, Socialism and Democracy. New York: Harper & Row. [Google Scholar]

- Shane, Scott. 2000. Prior knowledge and the discovery of entrepreneurial opportunities. Organization Science 11: 448–69. [Google Scholar] [CrossRef]

- Shapiro, Carl. 2000. Navigating the patent thicket: Cross licenses, patent pools, and standard setting. Innovation Policy and the Economy 1: 119–50. [Google Scholar] [CrossRef]

- Su, Jeb. 2019. Venture Capital Funding for Artificial Intelligence Startups Hit Record High in 2018. Available online: https://www.forbes.com/sites/jeanbaptiste/2019/02/12/venture-capital-funding-for-artificial-intelligence-startups-hit-record-high-in-2018/#550daf8a41f7 (accessed on 13 December 2019).

- Trajtenberg, Manuel, Rebecca Henderson, and Adam Jaffe. 1997. University versus corporate patents: A window on the basicness of invention. Economics of Innovation and New Technology 5: 19–50. [Google Scholar] [CrossRef]

- Turnbull, Stuart. 2018. Capital allocation in decentralized businesses. Journal of Risk and Financial Management 11: 82. [Google Scholar] [CrossRef]

- Tushman, Michael L., and Philip Anderson. 1986. Technological discontinuities and organizational environments. Administrative Science Quarterly 31: 439–65. [Google Scholar] [CrossRef]

- Utterback, James M., and Fernando F. Suárez. 1993. Innovation, competition, and industry structure. Research Policy 22: 1–21. [Google Scholar] [CrossRef]

- World Intellectual Property Organization. 2019. WIPO Technology Trends 2019: Artificial Intelligence. Geneva: World Intellectual Property Organization. [Google Scholar]

- Yayavaram, Sai, and Gautam Ahuja. 2008. Decomposability in knowledge structures and its impact on the usefulness of inventions and knowledge-base malleability. Administrative Science Quarterly 53: 333–62. [Google Scholar] [CrossRef]

- Yayavaram, Sai, and Wei-Ru Chen. 2015. Changes in firm knowledge couplings and firm innovation performance: The moderating role of technological complexity. Strategic Management Journal 36: 377–96. [Google Scholar] [CrossRef]

- York, Jeffrey G., Timothy J. Hargrave, and Desirée F. Pacheco. 2016. Converging winds: Logic hybridization in the Colorado wind energy field. Academy of Management Journal 59: 579–610. [Google Scholar] [CrossRef]

| (a) | ||||||||||

| Variable | 1 | 2 | 3 | 4 | 5 | 6 | 7 | 8 | 9 | 10 |

| 1. Early Round Investment | 1.000 | |||||||||

| 2. Technology Classes | −0.017 * | 1.000 | ||||||||

| 3. Coupling | −0.003 | −0.140 * | 1.000 | |||||||

| 4. GDP per Capita (ln) | 0.057 * | 0.155 * | 0.006 | 1.000 | ||||||

| 5. Foreign Investor Ratio | 0.030 * | −0.003 | −0.005 | −0.081 * | 1.000 | |||||

| 6. U.S. Company | 0.129 * | 0.015 * | 0.016 * | 0.390 * | −0.149 * | 1.000 | ||||

| 7. Angel | 0.055 * | −0.003* | 0.006 | 0.032 * | 0.191 * | 0.035 * | 1.000 | |||

| 8. VC | 0.232 * | 0.034 * | 0.006 | 0.139 * | 0.217 * | 0.205 * | 0.127 * | 1.000 | ||

| 9. CVC | 0.273 * | 0.002 | −0.003 | 0.007 | 0.213 * | 0.012 * | 0.032 * | 0.154 * | 1.000 | |

| 10. GVC | 0.014 * | 0.033 * | −0.004 | 0.018 * | 0.173 * | 0.002 | 0.080 * | 0.026 * | −0.011 | 1.000 |

| Mean | 0.050 | 3.332 | 7.194 | 10.593 | 0.055 | 0.686 | 0.013 | 0.446 | 0.046 | 0.006 |

| S.D. | 0.217 | 2.465 | 11.258 | 0.417 | 0.289 | 0.464 | 0.130 | 1.039 | 0.242 | 0.079 |

| (b) | ||||||||||

| Variable | 1 | 2 | 3 | 4 | 5 | 6 | 7 | 8 | 9 | |

| 1. Early Round Investment | 1.000 | |||||||||

| 2. Coupling | 0.015 | 1.000 | ||||||||

| 3. GDP per Capita (ln) | 0.042 * | −0.017 | 1.000 | |||||||

| 4. Foreign Investor Ratio | 0.076 * | 0.022 | −0.031 * | 1.000 | ||||||

| 5. U.S. Company | 0.114 * | 0.010 | 0.335 * | −0.134 * | 1.000 | |||||

| 6. Angel | 0.091 * | 0.027 * | 0.048 * | 0.185 * | 0.055 * | 1.000 | ||||

| 7. VC | 0.310 * | 0.021 | 0.094 * | 0.268 * | 0.152 * | 0.184 * | 1.000 | |||

| 8. CVC | 0.141 * | 0.009 | 0.013 | 0.187 * | 0.031 * | 0.060 * | 0.189 * | 1.000 | ||

| 9. GVC | 0.032 * | 0.014 | 0.031 * | 0.175 * | 0.003 | 0.058 * | 0.041 * | −0.009 | 1.000 | |

| Mean | 0.048 | 4.779 | 10.515 | 0.073 | 0.658 | 0.023 | 0.390 | 0.038 | 0.009 | |

| S.D. | 0.214 | 7.507 | 0.480 | 0.350 | 0.474 | 0.175 | 1.047 | 0.220 | 0.100 | |

| Variable | Model 1 Patent-Level | Model 2 Patent-Level | Model 3 Patent-Level | Model 4 Firm-Level | Model 5 Firm-Level |

|---|---|---|---|---|---|

| Technology Classes | −0.072 | ||||

| (0.069) | |||||

| Coupling | 0.010 * | 0.020 ** | |||

| (0.005) | (0.009) | ||||

| Controls | |||||

| GDP per Capita (ln) | −1.105 *** | −1.042 *** | −1.125 *** | −0.185 | −0.086 |

| (0.290) | (0.297) | (0.289) | (0.198) | (0.372) | |

| Foreign Investor Ratio | 0.977 *** | 0.974 *** | 0.978 *** | 0.549 *** | 0.626 *** |

| (0.257) | (0.257) | (0.258) | (0.124) | (0.211) | |

| U.S. Company | 1.817 *** | 1.793 *** | 1.831 *** | 1.107 *** | 1.383 *** |

| (0.579) | (0.573) | (0.581) | (0.241) | (0.438) | |

| Angel | 1.575 *** | 1.543 *** | 1.538 *** | 0.882 *** | 1.309 *** |

| (0.390) | (0.390) | (0.388) | (0.203) | (0.304) | |

| VC | 0.760 *** | 0.766 *** | 0.761 *** | 0.469 *** | 0.332 *** |

| (0.097) | (0.098) | (0.097) | (0.041) | (0.058) | |

| CVC | 0.161 | 0.219 | 0.166 | 1.021 *** | 1.347 *** |

| (0.405) | (0.417) | (0.407) | (0.167) | (0.230) | |

| GVC | 2.356 *** | 2.366 *** | 2.333 *** | 0.603 | −0.376 |

| (0.466) | (0.462) | (0.466) | (0.399) | (0.917) | |

| Intercept | 4.686 * | 4.311 | 4.835 * | −2.551 | −3.829 |

| (2.797) | (2.860) | (2.783) | (2.044) | (3.878) | |

| N | 6042 | 6042 | 6013 | 5436 | 2284 |

| χ2 | 170.25 *** | 170.77 *** | 170.95 *** | 310.47 *** | 134.09 *** |

| Mean VIF | 1.180 | 1.170 | 1.120 | 1.140 | 1.120 |

| Condition Number | 1.935 | 1.938 | 1.648 | 1.818 | 1.792 |

© 2019 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).

Share and Cite

Santos, R.S.; Qin, L. Risk Capital and Emerging Technologies: Innovation and Investment Patterns Based on Artificial Intelligence Patent Data Analysis. J. Risk Financial Manag. 2019, 12, 189. https://doi.org/10.3390/jrfm12040189

Santos RS, Qin L. Risk Capital and Emerging Technologies: Innovation and Investment Patterns Based on Artificial Intelligence Patent Data Analysis. Journal of Risk and Financial Management. 2019; 12(4):189. https://doi.org/10.3390/jrfm12040189

Chicago/Turabian StyleSantos, Roberto S., and Lingling Qin. 2019. "Risk Capital and Emerging Technologies: Innovation and Investment Patterns Based on Artificial Intelligence Patent Data Analysis" Journal of Risk and Financial Management 12, no. 4: 189. https://doi.org/10.3390/jrfm12040189

APA StyleSantos, R. S., & Qin, L. (2019). Risk Capital and Emerging Technologies: Innovation and Investment Patterns Based on Artificial Intelligence Patent Data Analysis. Journal of Risk and Financial Management, 12(4), 189. https://doi.org/10.3390/jrfm12040189