1. Introduction

The October 2018 Global Financial Stability Report by the IMF was entitled A Decade after the Global Financial Crisis: Are We Safer? The answer is Yes. Given what happened a decade ago, and its lasting economic (let alone political) costs, any other answer would be terrifying. That is in part because we are in a worse position now than then to respond to a crisis precisely because of the fiscal and monetary policy exhaustion resulting from the crisis of 2008. But, thanks to a host of policy reforms overseen at international level by the Basel Committee on Banking Supervision (BCBS) and the Financial Stability Board (FSB), the financial system is considerably safer, albeit safer than not very safe at all.

That having been said, I invite you to imagine that I have just reached the mid-point of an hour-long lecture, during the first half of which I elaborated upon the point just made. I probably spent some of that time praising the implementation in the UK of the structural separation measure known as ring-fencing that was recommended by the Independent Commission on Banking (

ICB 2011b), which I chaired. Although separation between retail and investment banking is especially important for the banking system of a country, such as the UK, that is a global financial centre, it is disappointing that structural separation measures have been rather limited internationally, despite the attempt made in the EU by the expert group chaired by

Liikanen (

2012).

But let us now turn to the question posed by Tobias Adrian in his Preface to the IMF Report: “But is the financial system safe enough?” He sounds a cautionary note. There are clouds on the horizon. Policy uncertainty has risen, there are trade tensions, and support for multi-lateralism has declined. Yet markets appear complacent about a tightening of financial conditions. Further tightening “will expose financial vulnerabilities that have built up over the years and will test the resilience of the global financial system”. The call to roll back reforms must be resisted.

All true. But did those reforms go far enough in the first place? In particular, on the core question of equity capital in the banking system, did Basel III go far enough?

I have talked about this question before, including at the BIS’s Financial Stability Institute conference last year

1, and make no apology for doing so again. How well banks and their functional equivalents are capitalised is one of the fundamental policy questions for an economic system. It is a question on which there is an astonishing gap between the mainstream “official” view and the mainstream “economist” view. They cannot both be right, but how to resolve the difference? That is the main issue that I will discuss today. A ten-years-on stage of reform fatigue is no time for silence on such a fundamental question, especially when there is a growing chorus calling for an easing of policy.

Indeed, I remember well how things felt when the ICB work began in 2010, which was exactly when the BCBS was setting the basic parameters of Basel III. Macroeconomic weakness coupled with fiscal strain and monetary policy beyond its traditional limits weighed against the major tightening of bank capital requirements. As the Eurozone crisis took hold this pressure intensified. The answer was partly to have long lead-times for the implementation of reform, and we are now just a month from the completion date for much of the reform agenda, including the deadline for the implementation of ring-fencing in the UK. One of the ironies of the reform process was the situation circa 2016 of official voices at the highest level arguing against higher equity capital requirements at a time (as now) when it would be much easier to increase them, for example by curbing dividend pay-outs, than it felt in 2010–2011.

Back then, the ICB thought that the Basel baseline CET1/RWA ratio of 7% was “clearly insufficient for systemically important banks”. This was frustrating, because Basel III was a constraint on what the ICB could responsibly recommend for the UK. For the ICB it seemed “very doubtful that any figure below [10%] can be robustly supported by the available evidence, and a case could quite easily be made for going higher”.

2 I will develop that case today, on the basis of some evidence since.

But first an anecdote from ten-and-a-bit years ago. On Monday 17 March 2008 I was at the annual conference of the Royal Economic Society listening to a lecture

3 on financial stability by Hyun Shin, then of Princeton and now at the BIS, and feeling rather pleased with myself. I had invited Hyun to give the lecture even before the collapse of Northern Rock six months earlier, and Bear Stearns had been bailed out the very day before. Perspicacious though I may have been feeling then, it barely crossed my mind that events were in train that, but for huge government rescues, would collapse the western banking system. In fact, the thought did flit across my mind, only to be dismissed, naively, as incredible.

I tell this story to illustrate that the real shock of 2008 was not the shock—of subprime, the drops in property prices, etc—but the system’s lack of resilience to the shock. Put another way, the “it” that few saw coming was not the sharp movement of asset prices, but the fragility of the system. It is a basic proposition of financial economics, and no ground for criticism of economists, that you cannot see sharp asset price movements coming. Failure to anticipate systemic fragility in the face of such shocks is an altogether different matter.

Inadequate equity capital was the basis for that fragility. Of course, there were liquidity problems too, but they were often down to (justified) perceptions of capital inadequacy, as Northern Rock itself showed. And there were problems of management conduct and incentives and corporate culture too, but their consequences for the economy are far more severe when capital falls short. Banks’ capital adequacy is a cornerstone of our economic system.

2. The Great Divide

To illustrate just how wide the gap is between Basel III and the position that leading economists hold on bank capital, I will take as my text the opinion letter published in the

Financial Times on 9 November 2010 (

Admati et al. 2010).

4 The letter made these points among others:

“Basel III is far from sufficient to protect the system from recurring crises. If a much larger fraction, at least 15 per cent, of banks’ total, non-risk-weighted, assets were funded by equity, the social benefits would be substantial. And the social costs would be minimal, if any;”

It is “a basic fallacy” to claim that more equity increases banks’ overall funding costs;

Increasing equity requirements is simpler and more effective than “contingent capital”;

The Basel system of risk weights encourages “innovations” that undermine capital regulation;

Warnings that increased equity requirements would restrict lending and impede growth are misplaced.

In sum: “Much more equity funding would permit banks to perform all their useful functions and support growth without endangering the financial system by systemic fragility. It would give banks incentives to take better account of the risks they take and reduce their incentives to game the system. And it would sharply reduce the likelihood of crises.”

The number deserves emphasis—at least 15 per cent of total assets funded by equity. Likewise, for Mervyn King, a 10 per cent equity base would be “a good start”.

These figures are enormously greater than the Basel III settlement, under which banks must maintain a leverage ratio of at least 3 per cent. Banks of global systemic importance also have an add-on of half their G-SIB capital buffer, so a bank with a 2 per cent G-SIB buffer would have to meet a 4 per cent leverage ratio in terms of Tier 1 capital. However, the Basel III requirement is in terms of Tier 1 capital—which goes wider than common equity and allows a substantial fraction of contingent capital beyond proper equity. Leverage of 33 times Tier 1 capital can be 44 times Common Equity Tier 1 (CET1).

On any reckoning, the FT letter writers are proposing four times the Basel III standard (and Mervyn King at least three times.)

By contrast, the general (albeit not universal) opinion expressed by those in the financial sector—regulators, not just banks—is that reform since 2008 has got us to about the right place. Indeed, the authorities have been “focused on

not significantly increasing overall capital requirements across the banking sector. In short, there will be no Basel IV”.

5 Gleeson (

2018, p. 50) writes that “The very mention of Basel IV is sufficient in some quarters to make strong men weep”. The general public, if they understood the jargon, might be forgiven for asking: so what?

A gulf this wide between official opinion and academic opinion on a truly fundamental economic policy question is extraordinary. Of many things that could be said about it, I will focus today on two points. The first is the serious issue of bank capital measurement, which was part of the problem a decade ago and which remains so today, especially if attention is paid to market signals. The measurement problem itself argues for substantially more bank equity capital than Basel III (plus related buffers). My other point will be that, properly understood, prominent official cost–benefit analyses of optimal bank equity capital do not justify Basel III but indicate the desirability of an approach closer to what the economists advocate.

3. Capital Measurement and Price-To-Book Ratios

The regulatory edifice—Basel III, stress tests and the rest—is built on the premise that accounting methods measure the value of bank assets in an accurate and timely way. Bank assets are inherently difficult to value because they tend not to be easily tradeable. Capital markets rather than financial intermediaries are generally the forum for more tradeable activities. Events ten years ago made plain that reliance cannot be placed on accounting methods for accurate and timely valuation. Banks that were failing in fact still met their regulatory capital ratios. Things have improved since 2008 but the basic point still holds.

The common-sense implication is to build in a substantial margin of error. If true capital might be appreciably less than measured capital, then raise the bar higher. Another implication is that policymakers would do well not to speak as if capital measurement were accurate. That is especially the case when markets are signalling a clear possibility of regulatory overvaluation of underlying asset positions. To quote from the IMF Report (

IMF 2018, p. 26) mentioned earlier:

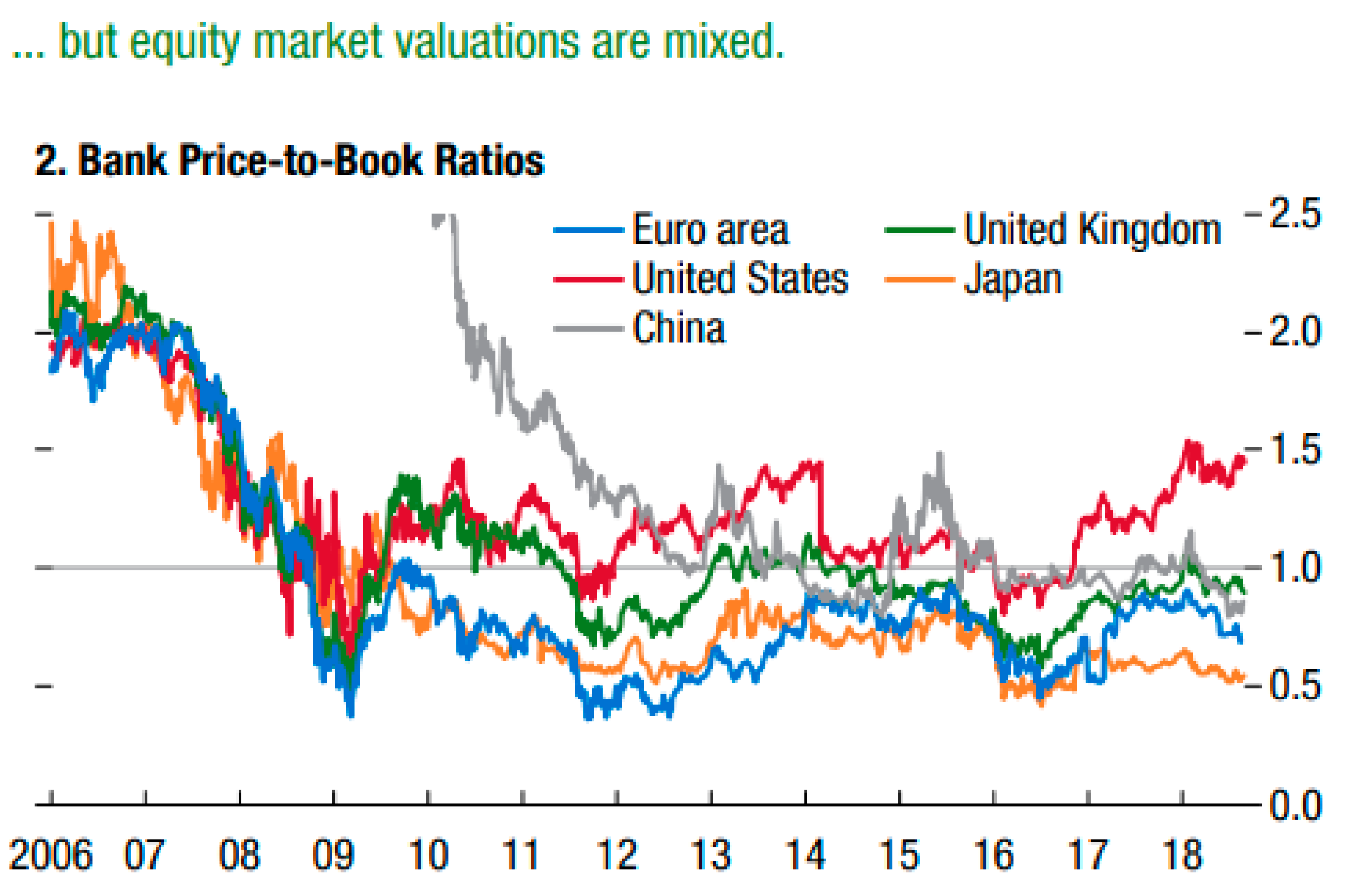

“In the Euro area, China, Japan, and the United Kingdom, bank aggregate price-to-book ratios are less than one. This means that the market value of equity is less than the amount of capital booked on bank balance sheets. If market valuations are used to calculate capital ratios—in place of the balance sheet value of capital used in the regulatory ratios—a number of banks would have a market-adjusted capitalization of less than 3 per cent, the minimum level in the Basel III framework”.

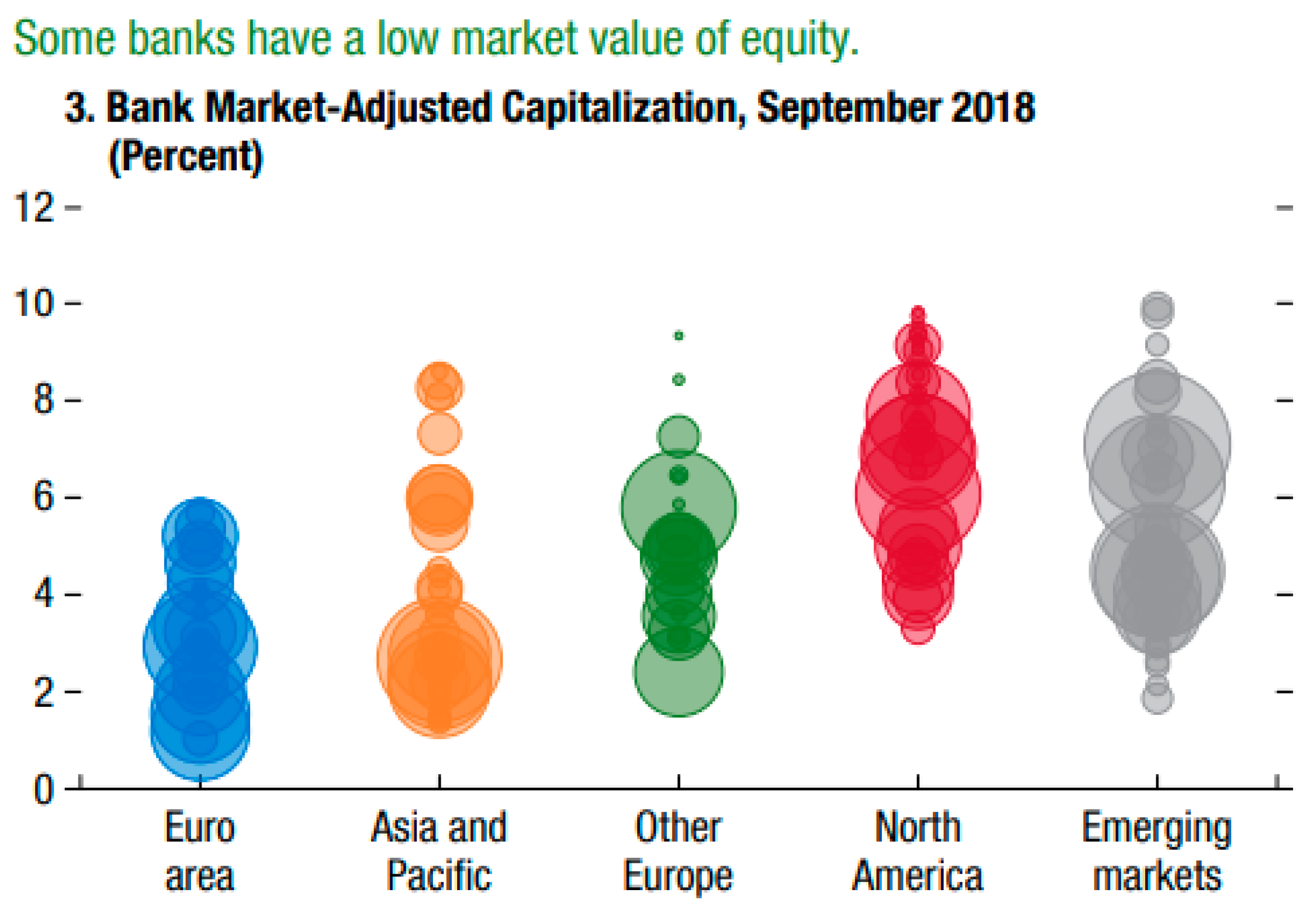

The two Figures below, both of which are panels of Figure 1.20 in

IMF (

2018), illustrate.

Figure 1 shows that average price-to-book ratios are below one in all the regions shown except the US. Pre-crisis they were about two, which shows how wrong markets can be, but markets reflected the problems emerging through 2007–2008 much more quickly than the regulatory numbers.

Figure 2 shows banks’ market-adjusted capitalisation by region. That is the price-to-book ratio (if less than one) times tangible common equity as a proportion of adjusted tangible assets. Blob size is proportional to assets, so bigger banks have bigger blobs. On a market-adjusted view, some major banks have very high leverage despite a decade of reform. The 15 per cent minimum recommended by the

FT letter writers is literally off the chart.

Where price-to-book ratios are persistently below one, there are at least serious

questions about regulatory measures of capital.

6 Price-to-book ratios should substantially

exceed one because market capitalisation reflects a view of the value of current exposures, less obligations to depositors and bondholders,

plus the franchise value of future profits in excess of the cost of capital,

plus the option value arising from shareholders’ limited liability.

Of course, the market might be taking an unduly pessimistic view, but there is a chance that it is not. It would therefore be good practice, for banks with price-to-book ratios below one, for regulators to show leverage ratios, and run stress tests, with market-implied capital values alongside those based on book values, rather as the IMF has done. For such banks, regulators should be particularly cautious about dividend pay-outs and share buy-backs.

Let me take a case in point—RBS, a bank of great systemic importance in the UK. In its Q3 results RBS reported CET1 of £32.5 bn and total assets of £720 bn, more than twenty-two times CET1. When, earlier this month RBS was removed from the FSB’s list of G-SIBs, the

Financial Times (16 November 2018) reported that the resulting cut to the bank’s capital requirements “could heighten expectations it will boost payouts next year”. RBS, it said, “has a significant pile of excess capital” and is reportedly considering a “targeted share buyback” and an “additional special dividend”.

7 RBS, however, currently has a price-to-book ratio of about 0.55. Among European banks, this is not an especially low figure, as the IMF charts show. This is hardly “excess capital” as far as the public interest is concerned.

Two years ago, when I made the parallel stress test suggestion to Bank of England, part of the response I received was that low price-to-book values can be explained by expected future cash flows being weak for reasons other than poor asset quality. But a bank’s obligations to depositors and bondholders are met, or not, by those cash flows. Their weakness is a problem whatever the cause. And if a systemic crisis hits, which is our principal concern, my ability to sell assets that might have been good quality pre-crisis might well evaporate. Anyway, if regulators have explanations to offer for low price-to-book ratios, those could be published, for public scrutiny, alongside market-based capital ratios.

In sum, the low price-to-book ratios of banks in major jurisdictions that the IMF has recently highlighted is a real concern.

4. Cost–Benefit Analyses

Major regulatory authorities, notably the

BCBS (

2010) and the Bank of England (BoE) (in the staff paper by

Brooke et al. 2015), have published cost–benefit analyses of optimal bank capital requirements. These provide a valuable framework to help gauge the relative merits of the official Basel III position and the contrasting economists’ view exemplified by the

FT letter.

The BoE analysis was an important part of the basis for the 2016 decision of its Financial Policy Committee on the systemic risk buffer for major UK retail banks. For the reasons set out in

Vickers (

2016) I believe that the buffer was set too low. The BoE staff paper is nevertheless valuable for the clarity of its approach, including transparency about how different assumptions would produce different estimates.

It notes that analyses following the crisis, notably the BCBS study, found that Tier 1 capital ratios should be “well above the agreed Basel III standard”. The paper however suggested that lower requirements could be justified on grounds that:

resolution regimes and other (TLAC) loss-absorbing capacity were coming into place, and

while much higher capital levels would be appropriate when risk was elevated, the availability of time-varying macro-prudential tools such as the counter-cyclical capital buffer means that the baseline capital level need not be so high.

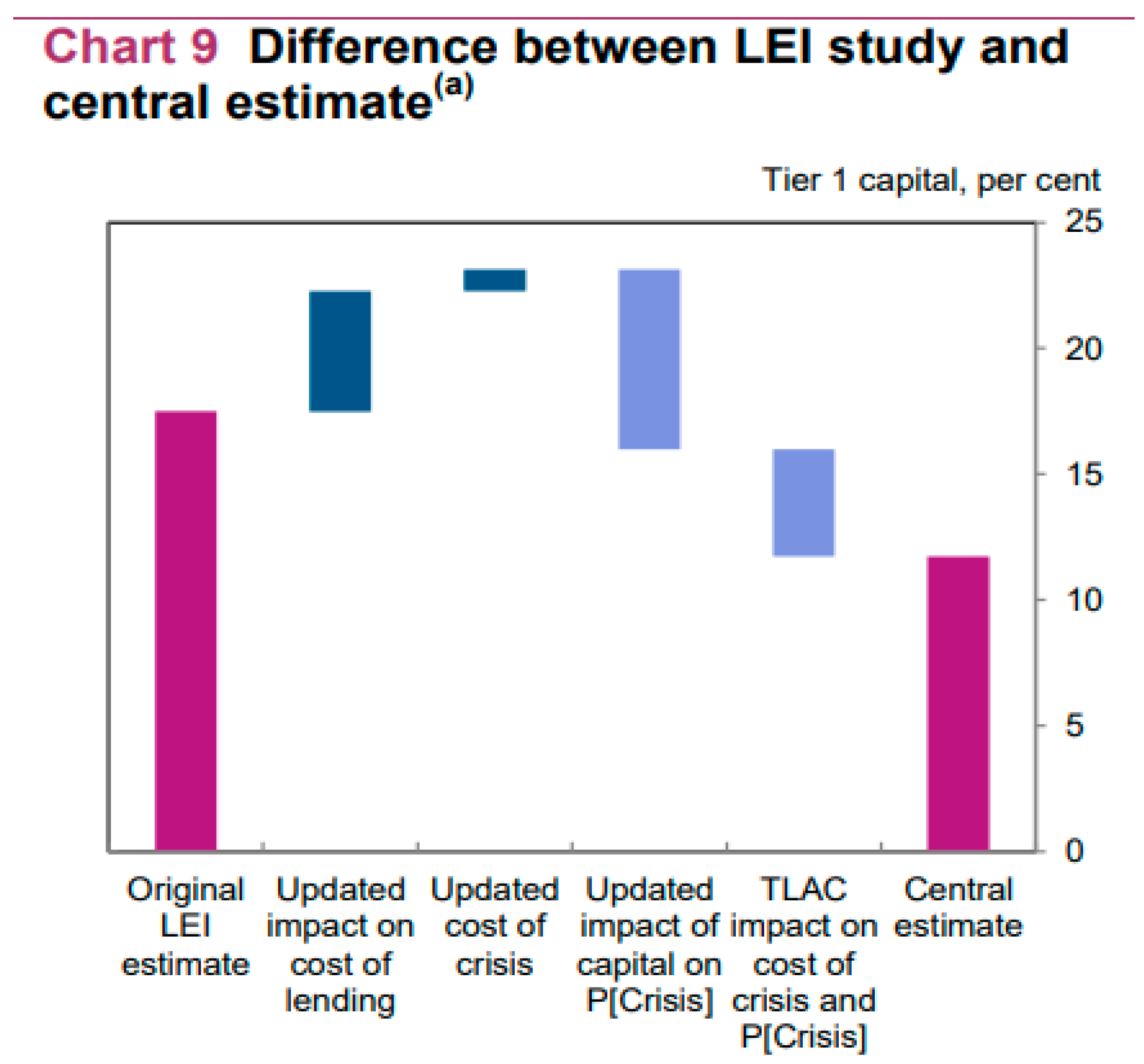

The

Figure 3 below, which is Chart 9 in the BoE study, shows the quantitative effect of these assumptions.

The left-hand bar shows the Basel Committee on Banking Supervision (BCBS) long-term economic impact (LEI) estimate of optimal Tier 1 capital requirements in terms of risk-weighted assets (RWAs). The figure is a percentage in the high teens, a long way north of Basel III. The BoE authors then adjust for the BCBS study’s over-estimate of the effect of higher capital requirements on bank funding costs—as risk declines, so should those costs. This adjustment, known as the Modigliani–Miller offset, leads to a figure above 20 per cent.

But then, as depicted in the two pale blue downward adjustments, the BoE paper introduces assumptions that reduce the probability and cost of crises, and hence the implied optimal capital requirement. One of these assumptions is that resolution regimes and TLAC reduce the probability and cost of crises. Though a supporter of bail-inable debt (as was the ICB) I do not believe that it gives good reason to lower optimal equity capital requirements. Will it work in the next systemic crisis? Nobody knows. Bail-inable debt is not a sure loss-absorber. Even if it were, and hence not implicitly subsidised by taxpayers, why not achieve the same with common equity instead? That might be less tax-efficient for banks, but that should not be a concern of prudential regulators acting in the public interest.

The assumption that the BoE study made about crisis probability deserves particular attention. Their approach estimates the optimal capital level at an average point in the risk environment, broadly equivalent to the mid-point in the credit cycle. The authors are clear that “the probability of a crisis is likely to be considerably greater at the peak of the cycle”, when higher capital ratios would be called for. Whereas the BoE study focussed on costs and benefits of bank capital for normal risk conditions, the BCBS study examined the full range of the credit cycle.

On this crucial point, surely the BCBS approach is right. Capital buffers are a safeguard for abnormal conditions, just as flood defences are built for abnormal weather conditions. The BoE paper appeals to countercyclical capital policy, but there are no grounds to suppose that such a policy could or would anticipate all elevations of risk in a timely and sufficient manner. The premise of normal risk conditions is simply the wrong basis for the analysis.

Correcting for this implausible assumption, and taking a less rosy view of the efficacy of resolution arrangements, the BoE model would deliver a very different result—optimal capital levels almost twice the BoE paper’s estimate.

I would now like to highlight two further points. The first concerns the economic costs of crises, which the BoE paper assumes to be considerably smaller than the post-2008 experience suggests. The authors’ explanation (

Brooke et al. 2015, p. 17) is that their method concerns the

marginal impact of a UK crisis, deducting the global recession element, and excluding potential spillover costs to other countries from a UK crisis, which may be large. From an international perspective, however, this is too narrow a view. The total effect, not just the marginal domestic effect, is what matters. The approach in the BoE paper therefore underestimates, by a potentially large margin, what the

global capital standard should be.

5. Economics of Risk

Finally let me draw attention to a deeper problem with cost–benefit analyses such as those of the BCBS and BoE—their treatment of risk. It is fundamental to the economics of financial asset pricing that required rates of return on equity exceed the risk-free rate precisely because investors are risk-averse. However, the cost–benefit analyses, despite incorporating equity costs that reflect risk, otherwise proceed on the assumption that society is not averse to risk. The

BCBS (

2010) study makes this point with admirable clarity:

“[A] risk-averse society would be prepared to pay a premium over the expected costs of an extreme event such as a banking crisis (probability times its cost in terms of output) in order to insure against it, i.e., pay over the actuarially fair price. This premium has not been included in the calculations and would increase the benefits.”

Likewise, the BoE study discounts future costs and benefits (at a lower rate than the BIS study did) but the rate at which future output is discounted is the same whether or not there is a crisis. The same approach was followed by

Miles et al. (

2012), who nevertheless obtained considerably higher estimates of optimal bank equity capital. It effectively assumes that there is no risk aversion on the part of society at large, despite there being substantial risk aversion on the part of equity investors in banks.

Basic economic logic suggests that this assumption gives rise to a large distortion in these estimates of optimal banks capital. As the BCBS authors noted, the inclusion of a risk premium would increase the benefits of bank capital.

One way to see the distortion is to suppose that neither bank investors nor society generally are averse to risk. That would rescue the crisis-insensitive weighting approach, but would completely undermine their estimate of the cost of equity to banks. With no risk aversion, there is no risk premium on bank equity, so there is no cost of higher bank equity, and no reason not to require much more.

Since there plainly is a risk premium on bank equity, the assumption of no risk aversion does not stand up. But then a consistent analysis must recognise that, per unit of output, averting losses in bad times is more valuable than adding to output in good times. Then the estimates of optimal bank capital from the BCBS and BoE studies are substantial under-estimates.

This is a very general point. But to see it in sharp form, consider the work of Robert Barro (following Reitz) on the effect on asset prices of the possibility of rare economic disasters—negative economic shocks that cause consumption per capita to drop sharply. Additional output is much less valuable in good states than in disaster states because of the standard economic assumption of diminishing marginal utility. This can help explain major puzzles of financial economics such as the size of the equity premium—i.e., the risk premium on shares relative to the risk-free rate on the bonds of an undoubtedly solvent government—and the low level of the risk-free rate on bonds.

Equities have low pay-outs in disaster states, when output is especially valuable, and high pay-outs in good states, but risk-free bonds pay out just as much in disasters (provided government solvency is maintained) as in good times. So, the greater the risk and magnitude of disasters, the greater is the wedge between the average return on equity and the risk-free rate.

The striking conclusion of

Barro (

2009) is that: “Calibrations indicate that society would willingly reduce GDP by around 20 per cent each year to eliminate rare disasters”. Apart from wars, banking crises are a classic example of (hopefully rare) economic disasters, though of course there are other types. Whether or not one agrees with anything like Barro’s numerical estimate, his conclusion underlines that the assumption of no risk aversion built into cost–benefit analyses of bank capital is potentially wrong by a wide margin. I do not have an estimate of how wrong to present today, but it would be a valuable public service for cost–benefit analyses by official bodies to be redone with a consistent approach to risk.

Furthermore, since the probability (and severity) of crises are related to bank capital levels, the stance of bank regulation can affect the structure of discount rates, including the risk premium itself.

Vlieghe (

2017) of the BoE’s Monetary Policy Committee, applying the same economic logic of risk, has emphasised how riskier economies have higher risk premia and lower risk-free real rates. In this regard he highlights how more debt can increase vulnerability to shocks: “Higher leverage and a larger financial intermediation sector mean that a downturn can become amplified”.

So not only do discount rates vary as between good and bad states, but the structure of those discount rates is affected by the safety and soundness, or not, of the financial system.

6. Conclusions

I have focused today on the equity capital question because it is fundamental to the systemic fragility exposed ten years ago—the real shock of 2008. On the answer to that question, the great divide between official analyses and economists’ views of optimal bank equity capital is not as wide as appears at first sight if the economics of risk is properly addressed. Adapting the BoE analysis to take account of abnormal risk conditions, a less benign view of the effectiveness of resolution regimes in a systemic crisis, an international rather than domestic perspective, and a consistent approach to risk, takes one a good distance towards the economists’ view, though differences would remain.

The economic rationale for capital levels in the region of Basel III is left looking thin. It looks thinner still when, as now, price-to-book ratios are calling regulatory capital measures into question for some important banks.

The politics of regulatory reform has resulted in a settlement that falls short of what the economics require. We are safer ten years on, but not as safe as we could and should be.

{kind=link}

{kind=link}

{kind=link}