Asymmetrical Linkages between Foreign Exchange and Stock Markets: Empirical Evidence through Linear and Non-Linear ARDL

Abstract

1. Introduction

2. Literature Review

3. The Models and Methods

3.1. Linear Auto Regressive Distributed Lag Model (ARDL)

3.2. Non-Linear Auto Regressive Distributed Lag Model (NARDL)

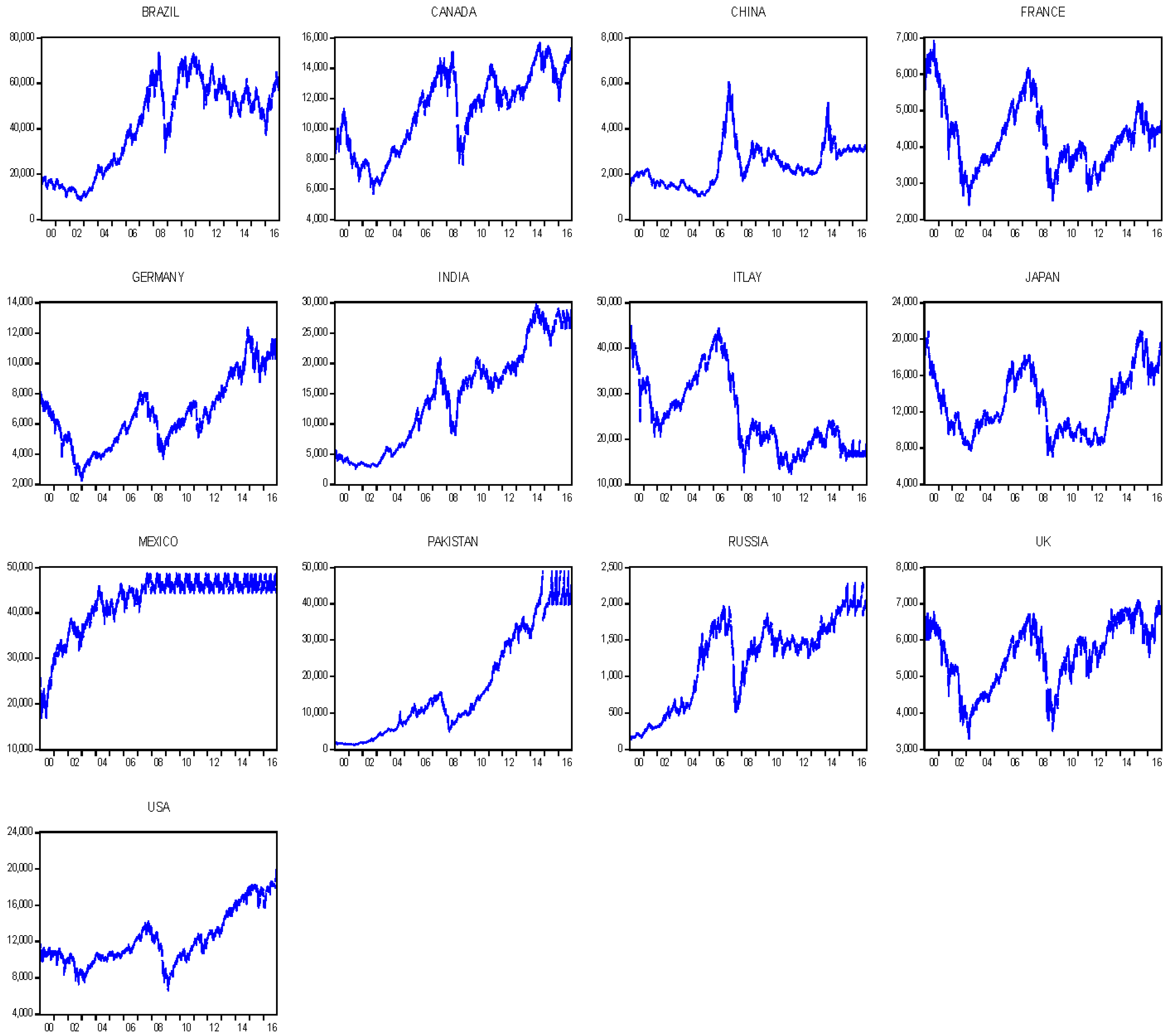

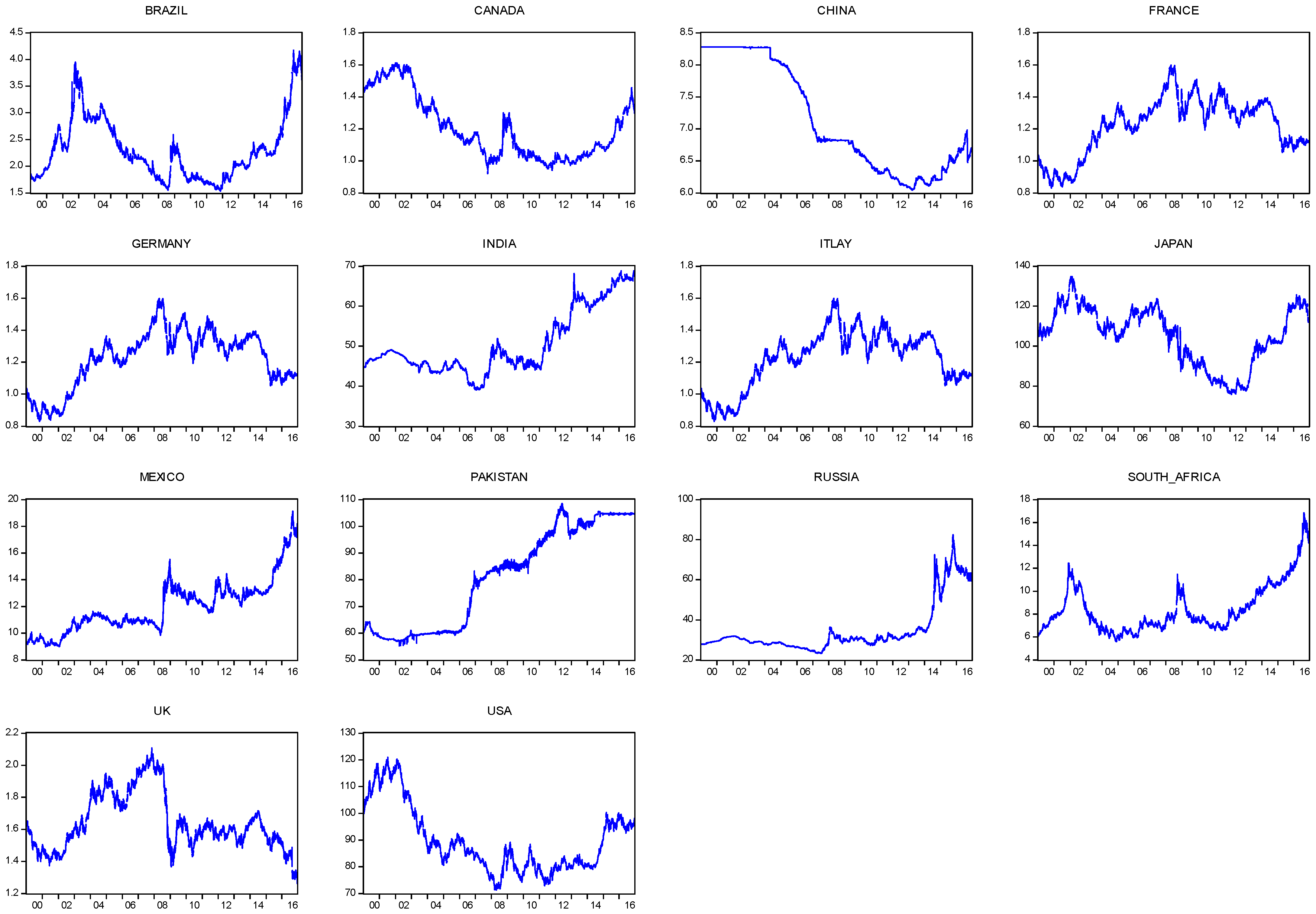

4. Empirical Results

5. Conclusions

Author Contributions

Funding

Conflicts of Interest

Appendix A

References

- Abdalla, Issam S. A., and Victor Murinde. 1997. Exchange rate and stock price interactions in emerging financial markets: Evidence on India, Korea, Pakistan and the Philippines. Applied Financial Economics 7: 25–35. [Google Scholar] [CrossRef]

- Aggarwal, R. 1981. Exchange rates and stock prices: A study of the U.S. capital markets under floating exchange rates. Akron Business and Economic Review 12: 7–12. [Google Scholar]

- Alagidede, Paul, Theodore Panagiotidis, and Xu Zhang. 2011. Causal relationship between stock prices and exchange rates. The Journal of International Trade & Economic Development 20: 67–86. [Google Scholar]

- Bahmani-Oskooee, Mohsen, and Sujata Saha. 2015. On the relation between stock prices and exchange rates: A review article. Journal of Economic Studies 42: 707–32. [Google Scholar] [CrossRef]

- Bahmani-Oskooee, Mohsen, and Sujata Saha. 2016. Do exchange rate changes have symmetric or asymmetric effects on stock prices? Global Finance Journal 31: 57–72. [Google Scholar] [CrossRef]

- Bahmani-Oskooee, Mohsen, and Sujata Saha. 2017. On the relation between exchange rates and stock prices: A non-linear ARDL approach and asymmetry analysis. Journal of Economics and Finance 42: 112–37. [Google Scholar] [CrossRef]

- Bahmani-Oskooee, Mohsen, and Ahmad Sohrabian. 1992. Stock prices and the effective exchange rate of the dollar. Applied Economics 24: 459–64. [Google Scholar] [CrossRef]

- Banerjee, Anindya, Juan Dolado, and Ricardo Mestre. 1998. Error-correction mechanism tests for cointegration in a single-equation framework. Journal of Time Series Analysis 19: 267–83. [Google Scholar] [CrossRef]

- Boonyanam, Nararuk. 2014. Relationship of stock price and monetary variables of Asian small open emerging economy: Evidence from Thailand. International Journal of Financial Research 5: 52. [Google Scholar] [CrossRef]

- Branson, William H. 1983. A Model of Exchange-Rate Determination with Policy Reaction: Evidence from Monthly Data. Cambridge: The National Bureau of Economic Research. [Google Scholar] [CrossRef]

- Buberkoku, Onder. 2013. The Relationship between Stock Prices and Exchange Rates Evidence from Developed and Developing Countries. Istanbul Stock Exchange Review 13: 1–16. [Google Scholar]

- Caporale, Guglielmo Maria, John Hunter, and Faek Menla Ali. 2014. On the linkages between stock prices and exchange rates: Evidence from the banking crisis of 2007–2010. International Review of Financial Analysis 33: 87–103. [Google Scholar] [CrossRef]

- Chortareas, Georgios, Ying Jiang, and John C. Nankervis. 2011. Forecasting exchange rate volatility using high-frequency data: Is the euro different? International Journal of Forecasting 27: 1089–107. [Google Scholar] [CrossRef]

- Dickey, David A., and Wayne A. Fuller. 1979. Distribution of the estimators for autoregressive time series with a unit root. Journal of the American Statistical Association 74: 427–31. [Google Scholar]

- Dornbusch, Rüdiger, William H. Branson, Marina V. N. Whitman, Peter Kenen, Hendrik Houthakker, Robert E. Hall, Robert Lawrence, George Perry, William Fellner, William Brainard, and et al. 1980. Exchange rate economics: Where do we stand? Brookings Papers on Economic Activity 1: 143–205. [Google Scholar] [CrossRef]

- Eita, Joel Hinaunye. 2012. Modelling macroeconomic determinants of stock market prices: Evidence from Namibia. Journal of Applied Business Research (JABR) 28: 871–84. [Google Scholar] [CrossRef]

- Engle, Robert F., and C.W.J. Granger. 1987. Co-integration and error correction: Representation, estimation, and testing. Econometrica: Journal of the Econometric Society 55: 251–76. [Google Scholar] [CrossRef]

- Frankel, Tamar. 1983. Fiduciary law. California Law Review 71: 795. [Google Scholar] [CrossRef]

- Granger, Clive W. J., Bwo-Nung Huangb, and Chin-Wei Yang. 2000. A bivariate causality between stock prices and exchange rates: Evidence from recent Asianflu. The Quarterly Review of Economics and Finance 40: 337–54. [Google Scholar] [CrossRef]

- Groenewold, Nicolaas, and James E. H. Paterson. 2013. Stock prices and exchange rates in Australia: Are commodity prices the missing link? Australian Economic Papers 52: 159–70. [Google Scholar] [CrossRef]

- Harjito, Agus D., and Carl B. McGowan. 2011. Stock price and exchange rate causality: The case of four asean countries. Southwestern Economic Review 34: 103–14. [Google Scholar]

- Inegbedion, Henry Egbezien. 2012. Macroeconomic determinants of stock price changes: Empirical evidence from Nigeria. Indian Journal of Finance 6: 19–23. [Google Scholar]

- Ismail, Mohd Tahir, and Zaidi Bin Isa. 2009. Modeling the interactions of stock price and exchange rate in Malaysia. The Singapore Economic Review 54: 605–19. [Google Scholar] [CrossRef]

- Jorion, Philippe. 1990. The exchange-rate exposure of US multinationals. Journal of Business 63: 331–45. [Google Scholar] [CrossRef]

- Khan, Faisal, Saqib Muneer, and Anuar M. Ahmad. 2013. Relationship between stock prices and economic variables: Sectoral analysis. Actual Problems of Economics 143: 544–53. [Google Scholar]

- Kollias, Christos, Nikolaos Mylonidis, and Suzanna-Maria Paleologou. 2012. The nexus between exchange rates and stock markets: Evidence from the euro-dollar rate and composite European stock indices using rolling analysis. Journal of Economics and Finance 36: 136–47. [Google Scholar] [CrossRef]

- Kutty, Gopalan. 2010. The Relationship between exchange rates and stock prices: The case of Mexico. North American Journal of Finance and Banking Research 4: 1–12. [Google Scholar]

- Lean, Hooi Hooi, Paresh Narayan, and Russell Smyth. 2011. Exchange rate and stock prices interaction in major Asian markets: Evidence for individual countries and panels allowing for structural breaks. The Singapore Economic Review 56: 255–77. [Google Scholar] [CrossRef]

- Lee, Chia-Hao, Shuh-Chyi Doong, and Pei-I. Chou. 2011. Dynamic correlation between stock prices and exchange rates. Applied Financial Economics 21: 789–800. [Google Scholar] [CrossRef]

- Lin, Chien-Hsiu. 2012. The co-movement between exchange rates and stock prices in the Asian emerging markets. International Review of Economics & Finance 22: 161–72. [Google Scholar]

- Ma, Christopher K., and G. Wenchi Kao. 1990. On exchange rate changes and stock price reactions. Journal of Business Finance & Accounting 17: 441–49. [Google Scholar]

- Mookerjee, Rajen, and Qiao Yu. 1997. Macroeconomic variables and stock prices in a small open economy: The case of Singapore. Pacific-Basin Finance Journal 5: 377–88. [Google Scholar] [CrossRef]

- Moore, Tomoe, and Ping Wang. 2014. Dynamic linkage between real exchange rates and stock prices: Evidence from developed and emerging Asian markets. International Review of Economics & Finance 29: 1–11. [Google Scholar]

- Obben, James, Andrew Pech, and Shamim Shakur. 2006. Analysis of the relationship between the share market performance and exchange rates in New Zealand: A cointegrating VAR approach. New Zealand Economic Papers 40: 147–80. [Google Scholar] [CrossRef]

- Pan, Ming-Shiun, Robert Chi-Wing Fok, and Y. Angela Liu. 2007. Dynamic linkages between exchange rates and stock prices: Evidence from East Asian markets. International Review of Economics & Finance 16: 503–20. [Google Scholar]

- Parsva, Pardis, and Hooi Hooi Lean. 2011. The analysis of relationship between stock prices and exchange rates: Evidence from six Middle Eastern financial markets. International Research Journal of Finance and Economics 66: 157–71. [Google Scholar]

- Pesaran, M. Hashem, Yongcheol Shin, and Richard J. Smith. 2001. Bounds testing approaches to the analysis of level relationships. Journal of Applied Econometrics 16: 289–326. [Google Scholar] [CrossRef]

- Phillips, Peter C. B., and Pierre Perron. 1988. Testing for a unit root in time series regression. Biometrika 75: 335–46. [Google Scholar] [CrossRef]

- Phylaktis, Kate, and Fabiola Ravazzolo. 2005. Stock prices and exchange rate dynamics. Journal of International Money and Finance 24: 1031–53. [Google Scholar] [CrossRef]

- Rahman, Md Lutfur, and Jashim Uddin. 2009. Dynamic relationship between stock prices and exchange rates: Evidence from three South Asian countries. International Business Research 2: 167. [Google Scholar] [CrossRef]

- Richards, John Simpson, and John Evans. 2009. The interaction between exchange rates and stock prices: An Australian context. International Journal of Economics and Finance 1: 3–23. [Google Scholar] [CrossRef]

- Shin, Yongcheol, Byungchul Yu, and Matthew Greenwood-Nimmo. 2014. Modelling asymmetric cointegration and dynamic multipliers in a nonlinear ARDL framework. In Festschrift in Honor of Peter Schmidt. New York: Springer, pp. 281–314. [Google Scholar]

- Smyth, Russell, and Nandha. 2003. Bivariate causality between exchange rates and stock prices in South Asia. Applied Economics Letters 10: 699–704. [Google Scholar] [CrossRef]

- Soenen, Luc A., and Elizabeth S. Hennigar. 1988. An analysis of exchange-rates and stock-prices-the united-states experience between 1980 and 1986. Akron Business and Economic Review 19: 7–16. [Google Scholar]

- Solnik, Bruno. 1987. Using financial prices to test exchange rate models: A note. The Journal of Finance 42: 141–49. [Google Scholar] [CrossRef]

- Tian, Gary Gang, and Shiguang Ma. 2010. The relationship between stock returns and the foreign exchange rate: the ARDL approach. Journal of the Asia Pacific Economy 15: 490–508. [Google Scholar] [CrossRef]

- Tsagkanos, Athanasios, and Costas Siriopoulos. 2013. A long-run relationship between stock price index and exchange rate: A structural nonparametric cointegrating regression approach. Journal of International Financial Markets, Institutions and Money 25: 106–18. [Google Scholar] [CrossRef]

- Tsai, I-Chun. 2012. The relationship between stock price index and exchange rate in Asian markets: A quantile regression approach. Journal of International Financial Markets, Institutions and Money 22: 609–21. [Google Scholar] [CrossRef]

- Tuncer, Ismail, and Tuncay Turan Turaboglu. 2014. Relationship between stock prices and economic activity in Turkish economy. Actual Problems of Economics 152: 111–21. [Google Scholar]

- Unlu, Ulas. 2013. Oil price, exchange rate and stock market in ASEAN-5 countries. The Empirical Economics Letter: A Monthly International Journal of Economics 12: 551–57. [Google Scholar]

- Wickremasinghe, Guneratne B. 2012. Stock prices and exchange rates in Sri Lanka: Some empirical evidence. Investment Management & Financial Innovations 9: 8–14. [Google Scholar]

- Yang, Zheng, Anthony H. Tu, and Yong Zeng. 2014. Dynamic linkages between Asian stock prices and exchange rates: New evidence from causality in quantiles. Applied Economics 46: 1184–201. [Google Scholar] [CrossRef]

- Yau, Hwey-Yun, and Chien-Chung Nieh. 2006. Interrelationships among stock prices of Taiwan and Japan and NTD/Yen exchange rate. Journal of Asian Economics 17: 535–52. [Google Scholar] [CrossRef]

- Yau, Hwey-Yun, and Chien-Chung Nieh. 2009. Testing for cointegration with threshold effect between stock prices and exchange rates in Japan and Taiwan. Japan and the World Economy 21: 292–300. [Google Scholar] [CrossRef]

- Zhao, Hua. 2010. Dynamic relationship between exchange rate and stock price: Evidence from China. Research in International Business and Finance 24: 103–12. [Google Scholar] [CrossRef]

{kind=link}

{kind=link}

| Brazil | China | India | Mexico | South Africa | Pakistan | Canada | |

| CONSTANT | 75,086.60 *** | 6890.091 * | −23,325.23 * | 17,128.80 * | 50,296.57 * | −38,403.95 * | 22,846.66 * |

| ER | −14,619.46 **** | −626.109 *** | 749.024 *** | 2106.868 *** | 0.362 *** | 686.057 ** | −9628.912 *** |

| Germany | Italy | Japan | UK | USA | Russia | France | |

| CONSTANT | 5033.804 * | 41,765.05 * | 2273.734 * | 5914.022 * | 15,838.97 * | 392.030 * | 6073.705 * |

| ER | 1353.288 *** | −13,608.03 *** | 101.587 *** | −177.187 *** | −40.529 *** | 24.327 *** | −1461.909 *** |

| Brazil | China | India | Mexico | South Africa | Pakistan | Canada | |

| CONSTANT | 11.980 * | 0.404 * | 5.043 * | 4.344 * | −0.096 * | 10.213 * | 1.559 * |

| ECM(-1) | −0.006 *** | −0.001 *** | −0.003 *** | −0.003 *** | −0.368 *** | −0.001 *** | −0.002 *** |

| Germany | Italy | Japan | UK | USA | Russia | France | |

| CONSTANT | 0.847 * | −5.592 * | 0.049 * | 5914.544 * | 1.931 * | 0.409 * | 0.847 * |

| ECM(-1) | −0.004 *** | −0.001 *** | −0.001 *** | −0.997 *** | −0.001 *** | −0.001 *** | −0.004 *** |

| Variables | Brazil | China | India | Mexico | South Africa | Pakistan | Canada | France | Germany | Italy | Japan | UK | USA | Russia |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| SP(-1) | 0.946 * | 1.049 * | 1.051 * | 1.182 * | 0.712 * | 0.990 * | 0.946 * | 0.959 * | 1.003 * | 0.968 * | 0.966 * | 0.961 * | 0.925 * | 1.017 * |

| SP(-2) | 0.052 * | −0.105 * | −0.066 * | −0.294 * | −0.170 * | 0.013 * | 0.052 ** | 0.005 * | −0.006 ** | 0.029 * | 0.028 * | −0.014 * | 0.042 * | −0.022 * |

| SP(-3) | −0.050 * | 0.108 * | 0.004 * | −0.002 * | 0.225 * | 0.019 * | −0.050 * | −0.013 * | 0.018 * | −0.022 * | 0.003 * | 0.045 * | −0.003 | |

| SP(-4) | 0.051 | −0.053 | 0.009 * | 0.111 | −0.241 | −0.025 * | 0.051 | 0.045 | −0.007 * | 0.025 | 0.047 | −0.0124 * | 0.006 | |

| ER | −516.217 * | 73.850 * | 9.688 | 78.586 ** | 38.878 * | −0.289 ** | −5168.217 * | 631.730 ** | 5.043 * | 15.363 ** | 0.140 ** | 575.917 ** | −19.730 ** | −0.175 * |

| ER(-1) | 548.354 ** | 2.334 ** | 19.115 ** | −122.58 ** | −11.080 *** | −0.099 ** | 5438.354 ** | −562.986 * | 53.295 * | 10.300 * | −691.94* | 20.837 * | −0.363 ** | |

| ER(-2) | −989.918 * | 4.565 ** | 28.669 ** | −71.507 * | 101.351 | 9.116 ** | −989.918 * | −134.382 ** | −51.912 * | −12.135 ** | 101.143 ** | −4.178 * | 0.968 ** | |

| ER(-3) | 440.491 ** | −85.540 | −32.728 | 100.816 * | −75.525 | −7.272 | 440.491 * | 62.125 | −168.796 | 8.275 * | −21.625 | 0.739 | 1.597 | |

| ER(-4) | 299.660 | 38.719 * | 13.831 | 18.969 * | 36.783 | 0.124 * | 299.661 | 3.873 | 171.858 * | −6.591 | 34.641 * | 2.215 | −1.981 * | |

| C | −11.972 * | 10.048 ** | −6.707 | 98.138 * | 239.51 * | −85.220 ** | −11.975 * | 7.903 * | −7.447 ** | 10.572 * | 18.742 ** | 14.433 ** | 12.212 ** | 0.640 * |

| R Square | 0.998 | 0.997 | 0.999 | 0.996 | 0.441 | 0.999 | 0.998 | 0.995 | 0.998 | 0.998 | 0.996 | 0.991 | 0.998 | 0.998 |

| F Stats | 35,3270.2 | 188.4 | 806.1 | 135.9 | 387.24 | 556.7 | 350.2 | 1164.7 | 2856.9 | 7731.8 | 162,306.3 | 95,887.73 | 27,131.6 | 320,609.2 |

| F (Prob) | 0.000 | 0.000 | 0.000 | 0.000 | 0.000 | 0.000 | 0.000 | 0.000 | 0.000 | 0.000 | 0.000 | 0.000 | 0.000 | 0.000 |

| Variables | Brazil | China | India | Mexico | South Africa | Pakistan | Canada | France | Germany | Italy | Japan | UK | USA | Russia |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| SP | * | * | * | ** | * | * | * | *** | ** | −0.000267 * | ** | |||

| SP(-1) | * | −4.2 ** | *** | *** | ** | ** | ** | ** | ||||||

| SP(-2) | * | * | 0.003 ** | |||||||||||

| SP(-3) | * | |||||||||||||

| ER(-1) | 1.075 ** | 0.927 ** | 0.962 ** | 0.943 *** | 0.966 * | 0.481 * | 0.870 * | 0.998 * | 0.990 * | 0.998 * | 0.792 * | 1.034 * | 0.999 * | 0.949 * |

| ER(-2) | −0.097 * | 0.098 * | −0.046 | 0.023 | −0.015 * | 0.154 | 0.129 * | 0.149 * | −0.041 | −0.007 * | ||||

| ER(-3) | 0.093 * | 0.073 | 0.083 * | 0.0327 * | 0.018 | 0.205 * | 0.055 | −0.022 * | 0.015 * | |||||

| ER(-4) | −0.100 * | 0.026 * | 0.158 * | 0.029 * | 0.041 | |||||||||

| C | 0.0015 * | 0.003 ** | 0.024 * | −0.001 * | 0.058 * | 0.036 * | −0.001 * | 0.002 * | 0.001 * | 0.001 * | 0.100 * | 0.002 * | 0.007 * | 0.007 * |

| R Square | 0.997 | 0.999 | 0.999 | 0.998 | 0.997 | 0.999 | 0.998 | 0.998 | 0.998 | 0.998 | 0.997 | 0.997 | 0.998 | 0.998 |

| F Stats | 361,934.6 | 6,563,187 | 729,431.2 | 562,696.6 | 413,609.4 | 123,025 | 1,010,879 | 788,714 | 1,175,828 | 117,554 | 387,782.1 | 255,209.2 | 792,247.5 | 638,360.3 |

| F (Prob) | 0.000000 | 0.000000 | 0.000000 | 0.000000 | 0.000000 | 0.000000 | 0.000000 | 0.000000 | 0.000000 | 0.000000 | 0.000000 | 0.000000 | 0.000000 | 0.000000 |

| Variables | Brazil | China | India | Mexico | South Africa | Pakistan | Canada | France | Germany | Italy | Japan | UK | USA | Russia |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| dER(-1) | −0.076 * | −0.033 * | −0.031 * | −0.530 * | −0.141 * | −0.205 * | 0.0346 * | −0.057 * | ||||||

| dER(-2) | 0.059 * | −0.088 * | −0.049 * | −0.396 * | −0.050 * | −0.058 * | ||||||||

| dER(-3) | 0.094 * | 0.024 * | −0.027 * | −0.203 * | −0.026 * | −0.043 * | ||||||||

| dER(-4) | 0.021 * | −0.090 * | −0.033 * | |||||||||||

| ER(-1) | −0.004 * | 0.002 * | −0.001 * | 0.042 * | −0.008 * | 0.087 * | 0.003 * | 0.0.47 * | −1.50 * | −0.087 * | 0.043 * | −0.079 * | −0.048 * | −0.007 * |

| ER(-2) | −0.074 * | 1.74 * | ||||||||||||

| ER(-3) | 1.58 * | |||||||||||||

| ER(-4) | 0.043 * | 0.05 * | * | |||||||||||

| POS(SP) | * | 6.987 ** | *** | ** | ** | ** | −0.005 ** | |||||||

| POS(SP-1) | * | * | 5.879 ** | ** | ** | * | * | 0.005 ** | ** | −0.004 * | * | |||

| POS(SP-2) | * | * | * | 0.087 | ||||||||||

| POS(SP-3) | * | * | ||||||||||||

| POS(SP-4) | * | −0.037 | * | |||||||||||

| NEGSP | 0.006 ** | 1.68 ** | * | * | * | |||||||||

| NEGSP(-1) | * | * | 1.12 * | * | * | * | * | * | * | * | −0.007 * | ** | ||

| NEGSP(-2) | −0.023 * | * | * | * | −0.009 * | |||||||||

| NEGSP(-3) | * | * | * | 0.070 * | 0.034 ** | |||||||||

| NEGSP(-4) | −0.069 | |||||||||||||

| C | 0.027 * | −0.002 | 0.074 * | 0.089 | −0.004 * | 0.986 | −0.4378 | * | 0.001 * | 0.364 | 0.013 | 0.123 * | 0.035 | |

| F STAT | 31.236 | 8.539 | 6.422 | 6.980 | 3.122 | 4.987 | 8.986 | 1.198 | 25.763 | 4.106 | 5.650 | 5.852 | ||

| F prob | 0.000 | 0.000 | 0.000 | 0.000 | 0.003 | 0.000 | 0.000 | 0.000 | 0.000 | 0.309 | 0.000 | 0.000 | 0.000 | 0.000 |

| Variables | Brazil | China | India | Mexico | S-Africa | Pakistan | Canada | France | Germany | Italy | Japan | UK | USA | Russia |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| SP(-1) | −0.088 *** | −0.094 ** | −0.010 ** | −0.008 ** | −0.513 ** | −0.008 ** | −0.004 ** | −0.002 ** | −0.003 ** | −0.002 ** | −0.002 ** | −0.004 ** | −0.003 ** | −0.001 ** |

| DSP(-1) | −0.074 * | 0.048 * | 0.052 * | 0.185 * | 0.205 *** | −0.037 * | −0.028 * | −0.032 * | −0.036 * | −0.072 * | ||||

| DSP(-2) | −0.050 * | −0.108 | 0.054 * | −0.032 * | −0.032 | −0.049 * | −0.033 | |||||||

| DSP(-3) | −0.046 | 0.050 * | −0.110 * | 0.265 *** | 0.027 | −0.047 * | −0.025 * | −0.048 * | ||||||

| DSP(-4) | 0.062 | 0.084 *** | −0.038 | 0.024 | 0.046 * | −0.026 | ||||||||

| POSEX | −5829.44 ** | −0.374 ** | −13.256 ** | −3.127 ** | 0.222 * | −2.50 ** | −175.88 ** | 1.356 ** | 146.684 ** | 26.767 ** | 0.464 ** | 2.149 ** | −29.03 ** | 0.038 ** |

| POSER(-1) | 342.064 | 24.412* | ||||||||||||

| POSER(-2) | 48.125 * | −558.74 | −638.07 | 263.861 | ||||||||||

| POSER(-3) | −36.301 | 452.10 * | −19.49 | |||||||||||

| POSER(-4) | 256.49 | 484.09 | 24.639 * | |||||||||||

| NEGER | −4323.8 * | −0.549 ** | −1.854 ** | 45.690 ** | 0.249 ** | −3.199 ** | 27.201 ** | 1260.120 ** | −120.65 * | 29.18 | −6.96 ** | 957.84 *** | −8.38 ** | 0.719 * |

| NEGER(-1) | 330.85 * | 128.8 *** | 20.222 | −1220.211 *** | 21.020 | |||||||||

| NEGER(-2) | −226.374 | 466.726 * | 693.448 | −15.77 * | −17.991 | |||||||||

| NEGER(-3) | −520.97 | −582.56 * | 17.227 | 24.68 | ||||||||||

| NEGER(-4) | 177.02 * | −14.371 | −18.985 | |||||||||||

| C | 62.146 * | 4.150 * | 19.039 * | 154.42 | 25,840.8 ** | 7.531 ** | 37.821 ** | 12.637 ** | 14.665 ** | 55.993 ** | 21.481 ** | 20.64 ** | 38.316 * | 1.911 ** |

| F STAT | 25.225 | 7.937 | 4.118 | 37.351 | 207.18 | 6.464 | 2.438 | 9.703 | 2.599 | 3.98 | 3.490 | 9.406 | 6.511 | 1.973 |

| F prob | 0.000 | 0.000 | 0.000 | 0.000 | 0.000 | 0.000 | 0.000 | 0.000 | 0.000 | 0.000 | 0.000 | 0.000 | 0.000 | 0.000 |

© 2018 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).

Share and Cite

Luqman, R.; Kouser, R. Asymmetrical Linkages between Foreign Exchange and Stock Markets: Empirical Evidence through Linear and Non-Linear ARDL. J. Risk Financial Manag. 2018, 11, 51. https://doi.org/10.3390/jrfm11030051

Luqman R, Kouser R. Asymmetrical Linkages between Foreign Exchange and Stock Markets: Empirical Evidence through Linear and Non-Linear ARDL. Journal of Risk and Financial Management. 2018; 11(3):51. https://doi.org/10.3390/jrfm11030051

Chicago/Turabian StyleLuqman, Rabia, and Rehana Kouser. 2018. "Asymmetrical Linkages between Foreign Exchange and Stock Markets: Empirical Evidence through Linear and Non-Linear ARDL" Journal of Risk and Financial Management 11, no. 3: 51. https://doi.org/10.3390/jrfm11030051

APA StyleLuqman, R., & Kouser, R. (2018). Asymmetrical Linkages between Foreign Exchange and Stock Markets: Empirical Evidence through Linear and Non-Linear ARDL. Journal of Risk and Financial Management, 11(3), 51. https://doi.org/10.3390/jrfm11030051