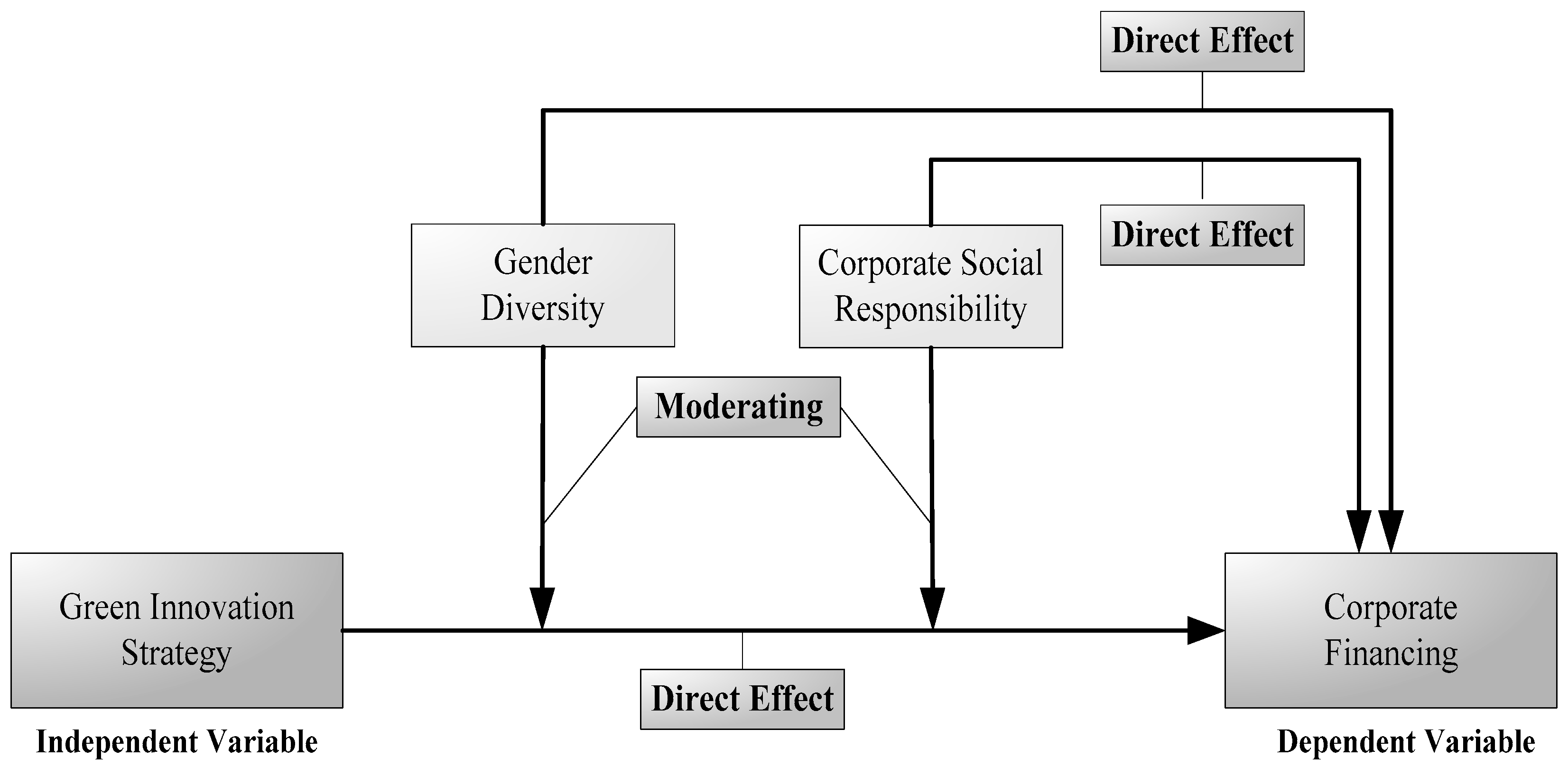

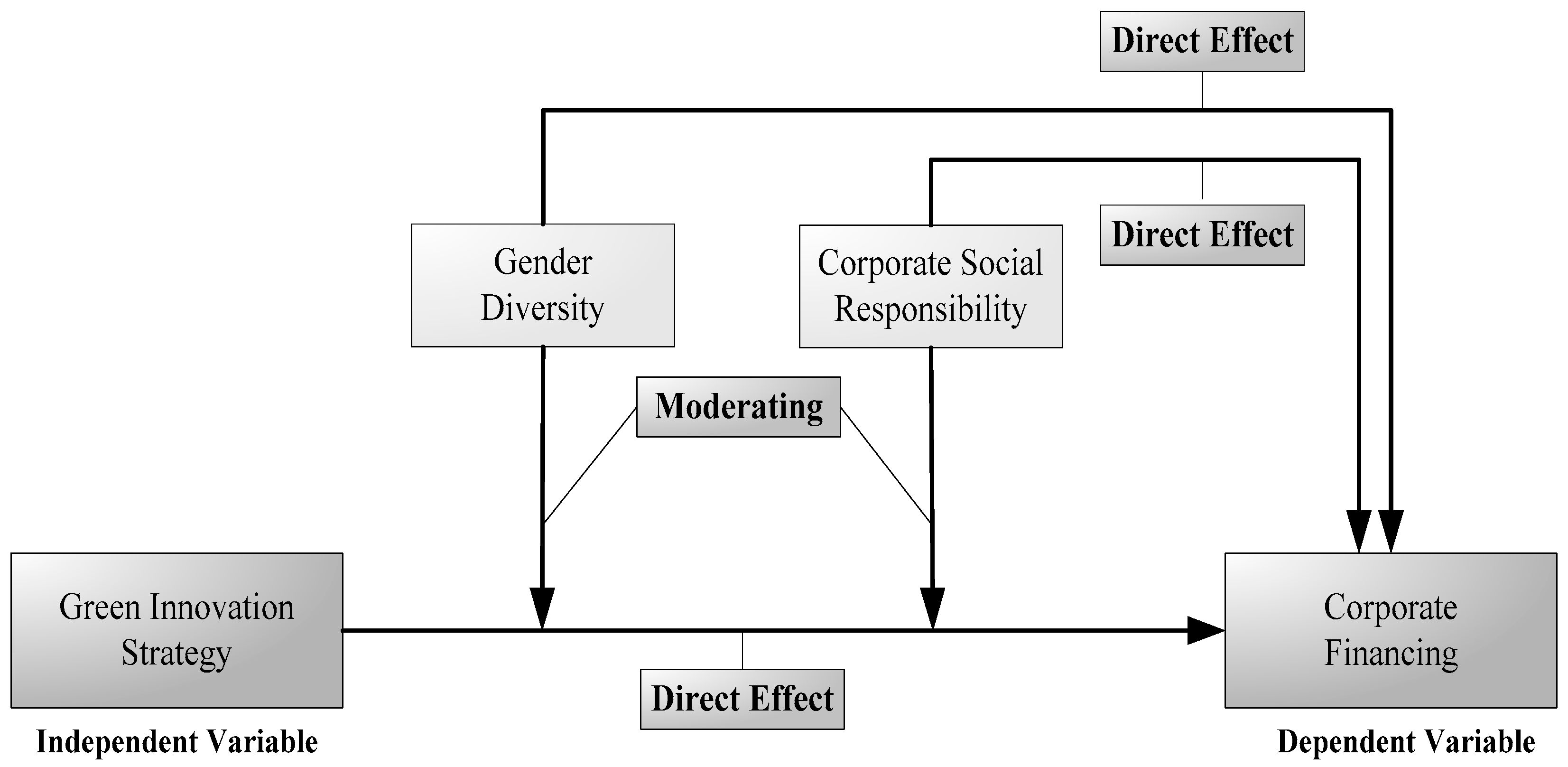

How Does Green Innovation Strategy Influence Corporate Financing? Corporate Social Responsibility and Gender Diversity Play a Moderating Role

,

,  , ,

, ,

Abstract

:1. Introduction

2. Hypothesis Construction and Theoretical Discussion

2.1. Theoretical Examination

2.2. Hypothesis Development

2.2.1. Green Innovation Strategy and Corporate Financing

2.2.2. The Role of Corporate Social Responsibility

2.2.3. The Role of Gender Diversity

3. Methodology

3.1. Selection of Data and Samples

3.2. Measurement of Variables

3.2.1. Corporate Financing

3.2.2. Green Innovation

3.2.3. Corporate Social Responsibility

3.2.4. Gender Diversity (GD)

3.2.5. Control Variables

3.3. Empirical Strategy

3.4. Fixed Effect Model

3.5. Generalized Method of Moments (GMM)

3.6. Feasible Generalized Least Square (FGLS)

3.7. Econometric Equations

4. Results and Discussion of the Investigation

4.1. Results

4.2. Additional Analysis

4.3. Discussion

5. Conclusions and Implications

5.1. Conclusions

5.2. Policy Implications

5.3. Limitation and Future Directions

Author Contributions

Funding

Institutional Review Board Statement

Informed Consent Statement

Data Availability Statement

Acknowledgments

Conflicts of Interest

References

- Nukusheva, A.; Ilyassova, G.; Rustembekova, D.; Zhamiyeva, R.; Arenova, L. Global warming problem faced by the international community: International legal aspect. Int. Environ. Agreem. Politics Law Econ. 2021, 21, 219–233. [Google Scholar] [CrossRef]

- Li, D.; Zhao, Y.; Zhang, L.; Chen, X.; Cao, C. Impact of quality management on green innovation. J. Clean. Prod. 2018, 170, 462–470. [Google Scholar] [CrossRef]

- Liao, Z. Market orientation and FIRMS’environmental innovation: The moderating role of environmental attitude. Bus. Strategy Environ. 2018, 27, 117–127. [Google Scholar] [CrossRef]

- López-Gamero, D.M.; Molina-Azorín, J.F.; Claver-Cortés, E. The potential of environmental regulation to change managerial perception, environmental management, competitiveness and financial performance. J. Clean. Prod. 2010, 18, 963–974. [Google Scholar] [CrossRef]

- Cai, W.; Lai, K.-H. Sustainability assessment of mechanical manufacturing systems in the industrial sector. Renew. Sustain. Energy Rev. 2021, 135, 110169. [Google Scholar] [CrossRef]

- Li, X.; Xu, Y.; Yao, X. Effects of industrial agglomeration on haze pollution: A Chinese city-level study. Energy Policy 2021, 148, 111928. [Google Scholar] [CrossRef]

- Javeed, S.A.; Latief, R.; Jiang, T.; San Ong, T.; Tang, Y. How environmental regulations and corporate social responsibility affect the firm innovation with the moderating role of Chief executive officer (CEO) power and ownership concentration? J. Clean. Prod. 2021, 308, 127212. [Google Scholar]

- Liu, Z.; Guan, D.; Wei, W.; Davis, S.J.; Ciais, P.; Bai, J.; Peng, S.; Zhang, Q.; Hubacek, K.; Marland, G.; et al. Reduced carbon emission estimates from fossil fuel combustion and cement production in China. Nature 2015, 524, 335–338. [Google Scholar] [CrossRef] [Green Version]

- He, L.; Zhang, L.; Zhong, Z.; Wang, D.; Wang, F. Green credit, renewable energy investment and green economy development: Empirical analysis based on 150 listed companies of China. J. Clean. Prod. 2019, 208, 363–372. [Google Scholar] [CrossRef]

- Xie, R.-H.; Yuan, Y.; Huang, J. Different types of environmental regulations and heterogeneous influence on “green” productivity: Evidence from China. Ecol. Econ. 2017, 132, 104–112. [Google Scholar]

- Rahman, A.B.; Cooper, S. The absence of corporate social responsibility reporting in Bangladesh. Crit. Perspect. Account. 2011, 22, 654–667. [Google Scholar]

- Grewatsch, S.; Kleindienst, I. When does it pay to be good? Moderators and mediators in the corporate sustainability–corporate financial performance relationship: A critical review. J. Bus. Ethics 2017, 145, 383–416. [Google Scholar] [CrossRef]

- Liao, Z. Is environmental innovation conducive to corporate financing? The moderating role of advertising expenditures. Bus. Strategy Environ. 2020, 29, 954–961. [Google Scholar] [CrossRef]

- Albort-Morant, G.; Leal-Millán, A.; Cepeda-Carrión, G. The antecedents of green innovation performance: A model of learning and capabilities. J. Bus. Res. 2016, 69, 4912–4917. [Google Scholar]

- Song, W.; Yu, H. Green innovation strategy and green innovation: The roles of green creativity and green organizational identity. Corp. Soc. Responsib. Environ. Manag. 2018, 25, 135–150. [Google Scholar] [CrossRef]

- Kunapatarawong, R.; Martínez-Ros, E. Towards green growth: How does green innovation affect employment? Res. Policy 2016, 45, 1218–1232. [Google Scholar] [CrossRef]

- Zhang, D.; Rong, Z.; Ji, Q. Green innovation and firm performance: Evidence from listed companies in China. Resour. Conserv. Recycl. 2019, 144, 48–55. [Google Scholar]

- Awan, U.; Kraslawski, A.; Huiskonen, J. Understanding the relationship between stakeholder pressure and sustainability performance in manufacturing firms in Pakistan. Procedia Manuf. 2017, 11, 768–777. [Google Scholar] [CrossRef]

- Abbas, J.; Sağsan, M. Impact of knowledge management practices on green innovation and corporate sustainable development: A structural analysis. J. Clean. Prod. 2019, 229, 611–620. [Google Scholar] [CrossRef]

- Chava, S.; Livdan, D.; Purnanandam, A. Do shareholder rights affect the cost of bank loans? Rev. Financ. Stud. 2009, 22, 2973–3004. [Google Scholar] [CrossRef]

- Friedman, R. Strategic Management: A Stakeholder Perspective; Prentice-Hall: Hoboken, NJ, USA, 1984. [Google Scholar]

- Jensen, C.M.; Meckling, W.H. Theory of the firm: Managerial behavior, agency costs and ownership structure. J. Financ. Econ. 1976, 3, 305–360. [Google Scholar] [CrossRef]

- Li, L.; Liu, Q.; Tang, D.; Xiong, J. Media reporting, carbon information disclosure, and the cost of equity financing: Evidence from China. Environ. Sci. Pollut. Res. 2017, 24, 9447–9459. [Google Scholar] [CrossRef]

- Passetti, E.; Cinquini, L.; Tenucci, A. Implementing internal environmental management and voluntary environmental disclosure: Does organisational change happen. Account. Audit. Account. J. 2018, 31, 1145–1173. [Google Scholar] [CrossRef]

- Calza, F.; Profumo, G.; Tutore, I. Corporate ownership and environmental proactivity. Bus. Strategy Environ. 2016, 25, 369–389. [Google Scholar] [CrossRef]

- Dhaliwal, D.S.; Li, O.Z.; Tsang, A.; Yang, Y.G. Voluntary nonfinancial disclosure and the cost of equity capital: The initiation of corporate social responsibility reporting. Account. Rev. 2011, 86, 59–100. [Google Scholar] [CrossRef]

- Cheng, J.C.C.; Yang, C.; Sheu, C. The link between eco-innovation and business performance: A Taiwanese industry context. J. Clean. Prod. 2014, 64, 81–90. [Google Scholar] [CrossRef] [Green Version]

- Branco, C.M.; Rodrigues, L.L. Corporate social responsibility and resource-based perspectives. J. Bus. Ethics 2006, 69, 111–132. [Google Scholar] [CrossRef]

- Bocquet, R.; Le Bas, C.; Mothe, C.; Poussing, N. Strategic CSR for innovation in SMEs: Does diversity matter? Long Range Plan. 2019, 52, 101913. [Google Scholar] [CrossRef]

- Marin, L.; Martín, P.J.; Rubio, A. Doing good and different! The mediation effect of innovation and investment on the influence of CSR on competitiveness. Corp. Soc. Responsib. Environ. Manag. 2017, 24, 159–171. [Google Scholar] [CrossRef]

- Montiel, I. Corporate social responsibility and corporate sustainability: Separate pasts, common futures. Organ. Environ. 2008, 21, 245–269. [Google Scholar] [CrossRef] [Green Version]

- Tomomi, T. Environmental management strategy for small and medium-sized enterprises: Why do SMBs practice environmental management? Asian Bus. Manag. 2010, 9, 265–280. [Google Scholar] [CrossRef]

- Al-Abdin, A.; Roy, T.; Nicholson, J.D. Researching corporate social responsibility in the Middle East: The current state and future directions. Corp. Soc. Responsib. Environ. Manag. 2018, 25, 47–65. [Google Scholar] [CrossRef]

- Madueno, J.H.; Jorge, M.L.; Conesa, I.M.; Martínez-Martínez, D. Relationship between corporate social responsibility and competitive performance in Spanish SMEs: Empirical evidence from a stakeholders’ perspective. BRQ Bus. Res. Q. 2016, 19, 55–72. [Google Scholar] [CrossRef] [Green Version]

- Albino, V.; Balice, A.; Dangelico, R.M. Environmental strategies and green product development: An overview on sustainability-driven companies. Bus. Strategy Environ. 2009, 18, 83–96. [Google Scholar] [CrossRef]

- Harjoto, A.M.; Rossi, F. Religiosity, female directors, and corporate social responsibility for Italian listed companies. J. Bus. Res. 2019, 95, 338–346. [Google Scholar] [CrossRef]

- Al-Shaer, H.; Zaman, M. Board gender diversity and sustainability reporting quality. J. Contemp. Account. Econ. 2016, 12, 210–222. [Google Scholar] [CrossRef] [Green Version]

- Hussain, N.; Rigoni, U.; Orij, R.P. Corporate governance and sustainability performance: Analysis of triple bottom line performance. J. Bus. Ethics 2018, 149, 411–432. [Google Scholar] [CrossRef]

- Carter, D.A.; D’Souza, F.; Simkins, B.J.; Simpson, W.G. The gender and ethnic diversity of US boards and board committees and firm financial performance. Corp. Gov. Int. Rev. 2010, 18, 396–414. [Google Scholar] [CrossRef]

- Qin, Y.; Harrison, J.; Chen, L. A framework for the practice of corporate environmental responsibility in China. J. Clean. Prod. 2019, 235, 426–452. [Google Scholar] [CrossRef]

- Hill, L.C.W.; Jones, T.M. Stakeholder-agency theory. J. Manag. Stud. 1992, 29, 131–154. [Google Scholar] [CrossRef]

- Dickinson-Delaporte, S.; Beverland, M.; Lindgreen, A. Building corporate reputation with stakeholders: Exploring the role of message ambiguity for social marketers. Eur. J. Mark. 2010, 44, 1856–1874. [Google Scholar] [CrossRef]

- Binz, C.; Hair, J.F., Jr.; Pieper, T.M.; Baldauf, A. Exploring the effect of distinct family firm reputation on consumers’ preferences. J. Fam. Bus. Strat. 2013, 4, 3–11. [Google Scholar] [CrossRef]

- Puncheva, P. The Role of Corporate Reputation in the Stakeholder Decision-Making Process. Bus. Soc. 2007, 47, 272–290. [Google Scholar] [CrossRef] [Green Version]

- Brower, J.; Mahajan, V. Driven to Be Good: A Stakeholder Theory Perspective on the Drivers of Corporate Social Performance. J. Bus. Ethic 2012, 117, 313–331. [Google Scholar] [CrossRef]

- Cerbioni, F.; Parbonetti, A. Exploring the Effects of Corporate Governance on Intellectual Capital Disclosure: An Analysis of European Biotechnology Companies. Eur. Account. Rev. 2007, 16, 791–826. [Google Scholar] [CrossRef]

- Bénabou, R.; Tirole, J. Individual and corporate social responsibility. Economica 2010, 77, 1–19. [Google Scholar] [CrossRef] [Green Version]

- Eccles, G.R.; Ioannou, I.; Serafeim, G. The Impact of a Corporate Culture of Sustainability on Corporate Behavior and Performance; National Bureau of Economic Research: Cambridge, MA, USA, 2012. [Google Scholar]

- Carter, A.D.; Simkins, B.J.; Simpson, W.G. Corporate governance, board diversity, and firm value. Financ. Rev. 2003, 38, 33–53. [Google Scholar] [CrossRef]

- Wei, Z.; Yuguo, J.; Jiaping, W. Greenization of venture capital and green innovation of Chinese entity industry. Ecol. Indic. 2015, 51, 31–41. [Google Scholar] [CrossRef]

- Oltra, V.; Jean, M.S. Sectoral systems of environmental innovation: An application to the French automotive industry. Technol. Forecast. Soc. Chang. 2009, 76, 567–583. [Google Scholar] [CrossRef]

- Eiadat, Y.; Kelly, A.; Roche, F.; Eyadat, H. Green and competitive? An empirical test of the mediating role of environmental innovation strategy. J. World Bus. 2008, 43, 131–145. [Google Scholar] [CrossRef]

- Ahlstrom, D.; Bruton, G.D.; Yeh, K.S. Private firms in China: Building legitimacy in an emerging economy. J. World Bus. 2008, 43, 385–399. [Google Scholar] [CrossRef]

- Babiak, K.; Trendafilova, S. CSR and environmental responsibility: Motives and pressures to adopt green management practices. Corp. Soc. Responsib. Environ. Manag. 2011, 18, 11–24. [Google Scholar] [CrossRef]

- Przychodzen, J.; Przychodzen, W. Relationships between eco-innovation and financial performance—Evidence from publicly traded companies in Poland and Hungary. J. Clean. Prod. 2015, 90, 253–263. [Google Scholar] [CrossRef]

- Chang, C.-H. The Influence of Corporate Environmental Ethics on Competitive Advantage: The Mediation Role of Green Innovation. J. Bus. Ethic 2011, 104, 361–370. [Google Scholar] [CrossRef]

- Ge, B.; Yang, Y.; Jiang, D.; Gao, Y.; Du, X.; Zhou, T. An Empirical Study on Green Innovation Strategy and Sustainable Competitive Advantages: Path and Boundary. Sustainability 2018, 10, 3631. [Google Scholar] [CrossRef] [Green Version]

- Yew, W.L.; Zhu, Z. Innovative autocrats? Environmental innovation in public participation in China and Malaysia. J. Environ. Manag. 2019, 234, 28–35. [Google Scholar] [CrossRef]

- Gotschol, A.; Giovanni, P.D.; Vinzi, V.E. Is environmental management an economically sustainable business? J. Environ. Manag. 2014, 144, 73–82. [Google Scholar] [CrossRef]

- Wong, S.K. The influence of green product competitiveness on the success of green product innovation: Empirical evidence from the Chinese electrical and electronics industry. Eur. J. Innov. Manag. 2012, 15, 468–490. [Google Scholar] [CrossRef]

- Mishra, P.; Yadav, M. Environmental capabilities, proactive environmental strategy and competitive advantage: A natural-resource-based view of firms operating in India. J. Clean. Prod. 2021, 291, 125249. [Google Scholar] [CrossRef]

- Sharfman, M.P.; Fernando, C.S. Environmental risk management and the cost of capital. Strat. Manag. J. 2008, 29, 569–592. [Google Scholar] [CrossRef]

- Zhang, Y.; Xing, C.; Wang, Y. Does green innovation mitigate financing constraints? Evidence from China’s private enterprises. J. Clean. Prod. 2020, 264, 121698. [Google Scholar] [CrossRef]

- Bae, C.S.; Chang, K.; Yi, H. The impact of corporate social responsibility activities on corporate financing: A case of bank loan covenants. Appl. Econ. Lett. 2016, 23, 1234–1237. [Google Scholar] [CrossRef]

- Cochran, P.L.; Wood, R.A. Corporate social responsibility and financial performance. Acad. Manag. J. 1984, 27, 42–56. [Google Scholar]

- Cheng, B.; Ioannou, I.; Serafeim, G. Corporate social responsibility and access to finance. Strat. Manag. J. 2013, 35, 1–23. [Google Scholar] [CrossRef]

- Hamrouni, A.; Boussaada, R.; Toumi, N.B.F. Corporate social responsibility disclosure and debt financing. J. Appl. Account. Res. 2019, 20, 394–415. [Google Scholar] [CrossRef]

- Hail, L.; Leuz, C. International Differences in the Cost of Equity Capital: Do Legal Institutions and Securities Regulation Matter? J. Account. Res. 2006, 44, 485–531. [Google Scholar] [CrossRef] [Green Version]

- Chen, W.K.C.; Chen, Z.; Wei, K.C.J. Legal protection of investors, corporate governance, and the cost of equity capital. J. Corp. Financ. 2009, 15, 273–289. [Google Scholar] [CrossRef]

- El Ghoul, S.; Guedhami, O.; Kwok, C.C.; Mishra, D.R. Does corporate social responsibility affect the cost of capital? J. Bank. Financ. 2011, 35, 2388–2406. [Google Scholar] [CrossRef]

- Lins, K.V.; Servaes, H.; Tamayo, A. Social Capital, Trust, and Firm Performance: The Value of Corporate Social Responsibility during the Financial Crisis. J. Financ. 2017, 72, 1785–1824. [Google Scholar] [CrossRef] [Green Version]

- Erragragui, E. Do creditors price firms’ environmental, social and governance risks? Res. Int. Bus. Financ. 2018, 45, 197–207. [Google Scholar] [CrossRef]

- Davis, F.G.; Whitman, M.V.N.; Zald, M.N. The responsibility paradox: Multinational firms and global corporate social responsibility. Ross Sch. Bus. Pap. 2006, 1031, 41. [Google Scholar] [CrossRef] [Green Version]

- Valmohammadi, C. Impact of corporate social responsibility practices on organizational performance: An ISO 26000 perspective. Soc. Responsib. J. 2014, 10, 455–479. [Google Scholar] [CrossRef]

- Turyakira, P.; Venter, E.; Smith, E. The impact of corporate social responsibility factors on the competitiveness of small and medium-sized enterprises. South Afr. J. Econ. Manag. Sci. 2014, 17, 157–172. [Google Scholar] [CrossRef]

- Ikram, M.; Zhou, P.; Shah SA, A.; Liu, G.Q. Do environmental management systems help improve corporate sustainable development? Evidence from manufacturing companies in Pakistan. J. Clean. Prod. 2019, 226, 628–641. [Google Scholar] [CrossRef]

- Svensson, G.; Ferro, C.; Høgevold, N.; Padin, C.; Varela JC, S.; Sarstedt, M. Framing the triple bottom line approach: Direct and mediation effects between economic, social and environmental elements. J. Clean. Prod. 2018, 197, 972–991. [Google Scholar] [CrossRef]

- Awan, U.; Khattak, A.; Kraslawski, A. Corporate social responsibility (CSR) priorities in the small and medium enterprises (SMEs) of the industrial sector of Sialkot, Pakistan. In Corporate Social Responsibility in the Manufacturing and Services Sectors; Springer: Berlin/Heidelberg, Germany, 2019; pp. 267–278. [Google Scholar]

- Wang, H.; Tong, L.; Takeuchi, R.; George, G. Corporate social responsibility: An overview and new research directions: Thematic issue on corporate social responsibility. Acad. Manag. J. 2016, 59, 534–544. [Google Scholar] [CrossRef]

- Abbas, J. Impact of total quality management on corporate green performance through the mediating role of corporate social responsibility. J. Clean. Prod. 2020, 242, 118458. [Google Scholar] [CrossRef]

- Naseem, T.; Shahzad, F.; Asim, G.A.; Rehman, I.U.; Nawaz, F. Corporate social responsibility engagement and firm performance in Asia Pacific: The role of enterprise risk management. Corp. Soc. Responsib. Environ. Manag. 2020, 27, 501–513. [Google Scholar] [CrossRef]

- Suganthi, L. Examining the relationship between corporate social responsibility, performance, employees’ pro-environmental behavior at work with green practices as mediator. J. Clean. Prod. 2019, 232, 739–750. [Google Scholar] [CrossRef]

- Answer, K.M.; Zhang, Z.; Kanwal, L. Moderating effect of innovation on corporate social responsibility and firm performance in realm of sustainable development. Corp. Soc. Responsib. Environ. Manag. 2018, 25, 799–806. [Google Scholar] [CrossRef]

- Bocquet, R.; Le Bas, C.; Mothe, C.; Poussing, N. CSR, innovation, and firm performance in sluggish growth contexts: A firm-level empirical analysis. J. Bus. Ethics 2017, 146, 241–254. [Google Scholar] [CrossRef]

- Raimi, L. Understanding theories of corporate social responsibility in the Ibero-American hospitality industry. In Corporate Social Responsibility and Corporate Governance; Emerald Publishing Limited: Bingley, UK, 2017. [Google Scholar]

- Boehe, D.M.; Cruz, L.B. Corporate Social Responsibility, Product Differentiation Strategy and Export Performance. J. Bus. Ethic 2010, 91, 325–346. [Google Scholar] [CrossRef]

- Lu, I.Y.; Kuo, T.; Lin, T.S.; Tzeng, G.H.; Huang, S.L. Multicriteria decision analysis to develop effective sustainable development strategies for enhancing competitive advantages: Case of the TFT-LCD industry in Taiwan. Sustainability 2016, 8, 646. [Google Scholar] [CrossRef] [Green Version]

- Bekmezci, M. Companies’ profitable way of fulfilling duties towards humanity and environment by sustainable innovation. Procedia Soc. Behav. Sci. 2015, 181, 228–240. [Google Scholar] [CrossRef] [Green Version]

- Farrell, K.A.; Hersch, P.L. Additions to corporate boards: The effect of gender. J. Corp. Financ. 2005, 11, 85–106. [Google Scholar] [CrossRef] [Green Version]

- Schubert, R. Analyzing and managing risks—On the importance of gender differences in risk attitudes. Manag. Financ. 2006, 32, 706–715. [Google Scholar] [CrossRef]

- Maxfield, S.; Shapiro, M.; Gupta, V.; Hass, S. Gender and risk: Women, risk taking and risk aversion. Gend. Manag. Int. J. 2010, 25, 586–604. [Google Scholar] [CrossRef]

- Schicks, J. Over-indebtedness in microfinance—An empirical analysis of related factors on the borrower level. World Dev. 2014, 54, 301–324. [Google Scholar] [CrossRef] [Green Version]

- Virtanen, A. Women on the boards of listed companies: Evidence from Finland. J. Manag. Gov. 2012, 16, 571–593. [Google Scholar] [CrossRef]

- Ruigrok, W.; Peck, S.; Tacheva, S. Nationality and Gender Diversity on Swiss Corporate Boards. Corp. Gov. Int. Rev. 2007, 15, 546–557. [Google Scholar] [CrossRef]

- Sattar, U.; Javeed, S.A.; Latief, R. How audit quality affects the firm performance with the moderating role of the product market competition: Empirical evidence from Pakistani manufacturing firms. Sustainability 2020, 12, 4153. [Google Scholar] [CrossRef]

- Nguyen, T.H.; Elmagrhi, M.H.; Ntim, C.G.; Wu, Y. Environmental performance, sustainability, governance and financial performance: Evidence from heavily polluting industries in China. Bus. Strategy Environ. 2021, 30, 2313–2331. [Google Scholar] [CrossRef]

- Zaid, A.M.A.; Abuhijleh, S.T.F.; Pucheta-Martínez, M.C. Ownership structure, stakeholder engagement, and corporate social responsibility policies: The moderating effect of board independence. Corp. Soc. Responsib. Environ. Manag. 2020, 27, 1344–1360. [Google Scholar] [CrossRef]

- Usman, M.; Farooq, M.U.; Zhang, J.; Makki, M.A.M.; Khan, M.K. Female directors and the cost of debt: Does gender diversity in the boardroom matter to lenders? Manag. Audit. J. 2019, 34, 374–392. [Google Scholar] [CrossRef]

- Elmagrhi, M.H.; Ntim, C.G.; Malagila, J.; Fosu, S.; Tunyi, A.A. Trustee board diversity, governance mechanisms, capital structure and performance in UK charities. Corp. Gov. Int. J. Bus. Soc. 2018, 18, 478–508. [Google Scholar] [CrossRef]

- Hillman, A.J.; Cannella, A.A., Jr.; Harris, I.C. Women and Racial Minorities in the Boardroom: How Do Directors Differ? J. Manag. 2002, 28, 747–763. [Google Scholar] [CrossRef]

- Coffey, B.S.; Wang, J. Board Diversity and Managerial Control as Predictors of Corporate Social Performance. J. Bus. Ethic 1998, 17, 1595–1603. [Google Scholar] [CrossRef]

- Harjoto, M.A.; Laksmana, I.; Lee, R. Board Diversity and Corporate Social Responsibility. J. Bus. Ethics 2015, 132, 641–660. [Google Scholar] [CrossRef]

- Byron, K.; Post, C. Women on Boards of Directors and Corporate Social Performance: A Meta-Analysis. Corp. Gov. Int. Rev. 2016, 24, 428–442. [Google Scholar] [CrossRef]

- Boukattaya, S.; Omri, A. Impact of Board Gender Diversity on Corporate Social Responsibility and Irresponsibility: Empirical Evidence from France. Sustainability 2021, 13, 4712. [Google Scholar] [CrossRef]

- Post, C.; Rahman, N.; Rubow, E. Green governance: Boards of directors’ composition and environmental corporate social responsibility. Bus. Soc. 2011, 50, 189–223. [Google Scholar] [CrossRef]

- Landry, E.E.; Bernardi, R.A.; Bosco, S.M. Recognition for Sustained Corporate Social Responsibility: Female Directors Make a Difference. Corp. Soc. Responsib. Environ. Manag. 2014, 23, 27–36. [Google Scholar] [CrossRef]

- Qiu, Y.; Shaukat, A.; Tharyan, R. Environmental and social disclosures: Link with corporate financial performance. Br. Account. Rev. 2016, 48, 102–116. [Google Scholar] [CrossRef] [Green Version]

- Xiang, L.; Zhang, C. Corporate governance, social responsibility information disclosure, and enterprise value in China. J. Clean. Prod. 2017, 142, 1075–1084. [Google Scholar]

- Zhang, J.; Ouyang, Y.; Ballesteros-Pérez, P.; Li, H.; Philbin, S.P.; Li, Z.; Skitmore, M. Understanding the impact of environmental regulations on green technology innovation efficiency in the construction industry. Sustain. Cities Soc. 2021, 65, 102647. [Google Scholar] [CrossRef]

- Lu, L.; Bao, J.; Huang, J.; Zhu, Q.; Mu, C.; Chu, X.; Xu, Y.; Zha, X. Recent research progress and prospects in tourism geography of China. J. Geogr. Sci. 2016, 26, 1197–1222. [Google Scholar] [CrossRef]

- Rehman, S.U.; Kraus, S.; Shah, S.A.; Khanin, D.; Mahto, R.V. Analyzing the relationship between green innovation and environmental performance in large manufacturing firms. Technol. Forecast. Soc. Chang. 2021, 163, 120481. [Google Scholar] [CrossRef]

- Haniffa, R.M.; Cooke, T.E. The impact of culture and governance on corporate social reporting. J. Account. Public Policy 2005, 24, 391–430. [Google Scholar] [CrossRef]

- Mulatu, A.; Florax, R.J.G.M.; Withagen, C.A. Environmental regulation and competitiveness: An exploratory meta-analysis. In Empirical Modeling of the Economy and the Environment; Physica: Heidelberg, Germany, 2003; pp. 23–54. [Google Scholar]

- Wang, Y.; Chui, A.C.W. Product market competition and audit fees. Audit. A J. Pract. Theory 2015, 34, 139–156. [Google Scholar] [CrossRef]

- Javeed, S.A.; Latief, R.; Lefen, L. An analysis of relationship between environmental regulations and firm performance with moderating effects of product market competition: Empirical evidence from Pakistan. J. Clean. Prod. 2020, 254, 120197. [Google Scholar] [CrossRef]

- Cai, X.; Zhu, B.; Zhang, H.; Li, L.; Xie, M. Can direct environmental regulation promote green technology innovation in heavily polluting industries? Evidence from Chinese listed companies. Sci. Total Environ. 2020, 746, 140810. [Google Scholar] [CrossRef] [PubMed]

- Lim, S.; Prakash, A. Voluntary Regulations and Innovation: The Case of ISO 14001. Public Adm. Rev. 2014, 74, 233–244. [Google Scholar] [CrossRef]

- Bansal, P.; Clelland, I. Talking trash: Legitimacy, impression management, and unsystematic risk in the context of the natural environment. Acad. Manag. J. 2004, 47, 93–103. [Google Scholar]

- Ren, S.; Wang, Y.; Hu, Y.; Yan, J. CEO hometown identity and firm green innovation. Bus. Strategy Environ. 2021, 30, 756–774. [Google Scholar] [CrossRef]

- Yang, D.; Jiang, W.; Zhao, W. Proactive environmental strategy, innovation capability, and stakeholder integration capability: A mediation analysis. Bus. Strategy Environ. 2019, 28, 1534–1547. [Google Scholar] [CrossRef]

- Feng, Y.; Chen, H.H.; Tang, J. The impacts of social responsibility and ownership structure on sustainable financial development of China’s energy industry. Sustainability 2018, 10, 301. [Google Scholar] [CrossRef] [Green Version]

- Carroll, A.B. A three-dimensional conceptual model of corporate performance. Acad. Manag. Rev. 1979, 4, 497–505. [Google Scholar] [CrossRef]

- Kansal, M.; Joshi, M.; Batra, G.S. Determinants of corporate social responsibility disclosures: Evidence from India. Adv. Account. 2014, 30, 217–229. [Google Scholar] [CrossRef]

- Gomes, M.; Marsat, S. Does CSR impact premiums in M&A transactions? Finance Res. Lett. 2018, 26, 71–80. [Google Scholar]

- Xia, B.; Olanipekun, A.; Chen, Q.; Xie, L.; Liu, Y. Conceptualising the state of the art of corporate social responsibility (CSR) in the construction industry and its nexus to sustainable development. J. Clean. Prod. 2018, 195, 340–353. [Google Scholar] [CrossRef]

- Ehsan, S.; Nazir, M.S.; Nurunnabi, M.; Raza Khan, Q.; Tahir, S.; Ahmed, I. A multimethod approach to assess and measure corporate social responsibility disclosure and practices in a developing economy. Sustainability 2018, 10, 2955. [Google Scholar] [CrossRef] [Green Version]

- Yasser, Q.R.; Al-Mamun, A.; Ahmed, I. Corporate Social Responsibility and Gender Diversity: Insights from Asia Pacific. Corp. Soc. Responsib. Environ. Manag. 2017, 24, 210–221. [Google Scholar] [CrossRef]

- Hyun, E.; Yang, D.; Jung, H.; Hong, K. Women on boards and corporate social responsibility. Sustainability 2016, 8, 300. [Google Scholar] [CrossRef] [Green Version]

- Kassinis, G.; Panayiotou, A.; Dimou, A.; Katsifaraki, G. Gender and environmental sustainability: A longitudinal analysis. Corp. Soc. Responsib. Environ. Manag. 2016, 23, 399–412. [Google Scholar] [CrossRef]

- Fang, V.W.; Noe, T.H.; Tice, S. Stock market liquidity and firm value. J. Financial Econ. 2009, 94, 150–169. [Google Scholar] [CrossRef]

- Roy, P.P.; Rao, S.; Zhu, M. Mandatory CSR expenditure and stock market liquidity. J. Corp. Financ. 2022, 72, 102158. [Google Scholar] [CrossRef]

- La Rosa, F.; Liberatore, G.; Mazzi, F.; Terzani, S. The impact of corporate social performance on the cost of debt and access to debt financing for listed European non-financial firms. Eur. Manag. J. 2018, 36, 519–529. [Google Scholar] [CrossRef]

- Sayilgan, G.; Karabacak, H.; Kucukkocaoglu, G. The firm-specific determinants of corporate capital structure: Evidence from Turkish panel data. Invest. Manag. Financ. Innov. 2006, 3, 125–139. [Google Scholar]

- Patin, J.-C.; Rahman, M.; Mustafa, M. Impact of total asset turnover ratios on equity returns: Dynamic panel data analyses. J. Account. Bus. Manag. (JABM) 2020, 27, 19–29. [Google Scholar] [CrossRef]

- Mulaessa, N.; Lin, L. How Do Proactive Environmental Strategies Affect Green Innovation? The Moderating Role of Environmental Regulations and Firm Performance. Int. J. Environ. Res. Public Health 2021, 18, 9083. [Google Scholar] [CrossRef]

- Li, H.L.; Zhu, X.H.; Chen, J.Y.; Jiang, F.T. Environmental regulations, environmental governance efficiency and the green transformation of China’s iron and steel enterprises. Ecol. Econ. 2019, 165, 106397. [Google Scholar] [CrossRef]

- Bhagat, S.; Bolton, B. Corporate governance and firm performance. J. Corp. Financ. 2008, 14, 257–273. [Google Scholar] [CrossRef]

- Dittmar, A.; Mahrt-Smith, J. Corporate governance and the value of cash holdings. J. Financ. Econ. 2007, 83, 599–634. [Google Scholar] [CrossRef]

- Li, Y.; Gong, M.; Zhang, X.Y.; Koh, L. The impact of environmental, social, and governance disclosure on firm value: The role of CEO power. Br. Account. Rev. 2018, 50, 60–75. [Google Scholar] [CrossRef] [Green Version]

- Antonakis, J.; Bendahan, S.; Jacquart, P.; Lalive, R. On making causal claims: A review and recommendations. Leadersh. Q. 2010, 21, 1086–1120. [Google Scholar] [CrossRef] [Green Version]

- Hamilton, B.H.; Nickerson, J.A. Correcting for Endogeneity in Strategic Management Research. Strat. Organ. 2003, 1, 51–78. [Google Scholar] [CrossRef]

- Wintoki, M.B.; Linck, J.S.; Netter, J.M. Endogeneity and the dynamics of internal corporate governance. J. Financ. Econ. 2012, 105, 581–606. [Google Scholar] [CrossRef]

- Schultz, E.L.; Tan, D.; Walsh, K. Endogeneity and the corporate governance—Performance relation. Aust. J. Manag. 2010, 35, 145–163. [Google Scholar] [CrossRef]

- Gujarati, N.D.; Porter, D.C.; Gunasekar, S. Basic Econometrics; Tata Mcgraw-hill Education: New York, NY, USA, 2012. [Google Scholar]

- Wooldridge, J.M. Econometric Analysis of Cross Section and Panel Data; MIT Press: Cambridge, MA, USA, 2010. [Google Scholar]

- Ullah, S.; Akhtar, P.; Zaefarian, G. Dealing with endogeneity bias: The generalized method of moments (GMM) for panel data. Ind. Mark. Manag. 2018, 71, 69–78. [Google Scholar] [CrossRef]

- Wooldridge, J.M. Introductory Econometrics: A Modern Approach; Cengage Learning: Boston, MA, USA, 2015. [Google Scholar]

- Wooldridge, J.M. Inverse probability weighted m-estimators for sample selection, attrition, and stratification. Port. Econ. J. 2002, 1, 117–139. [Google Scholar] [CrossRef]

- Aitken, A.C. IV—On least squares and linear combination of observations. Proc. R. Soc. Edinb. 1936, 55, 42–48. [Google Scholar] [CrossRef]

- Greene, W. Estimating Econometric Models with Fixed Effects; Department of Economics, Stern School of Business, New York University: New York, NY, USA, 2001. [Google Scholar]

- Baltagi, B.H. Forecasting with panel data. J. Forecast. 2008, 27, 153–173. [Google Scholar] [CrossRef]

- Mayur, M.; Saravanan, P. Performance implications of board size, composition and activity: Empirical evidence from the Indian banking sector. Corp. Gov. Int. J. Bus. Soc. 2017, 17, 466–489. [Google Scholar] [CrossRef]

- Javeed, S.A.; Lefen, L. An Analysis of Corporate Social Responsibility and Firm Performance with Moderating Effects of CEO Power and Ownership Structure: A Case Study of the Manufacturing Sector of Pakistan. Sustainability 2019, 11, 248. [Google Scholar] [CrossRef] [Green Version]

- Post, C.; Rahman, N.; McQuillen, C. From board composition to corporate environmental performance through sustainability-themed alliances. J. Bus. Ethics 2015, 130, 423–435. [Google Scholar] [CrossRef]

{kind=link}

| Variables | Mean | Standard Deviation | 1 | 2 | 3 | 4 | 5 | 6 | 7 | 8 | 9 | 10 | 11 |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| 1. CF | 0.307 | 0.386 | 1 | ||||||||||

| 2. GIS | 0.738 | 0.933 | 0.967 *** | 1 | |||||||||

| 3. CSR | 1.282 | 0.781 | 0.203 *** | 0.224 *** | 1 | ||||||||

| 4. GD | 0.253 | 0.671 | 0.001 | −0.041 ** | −0.527 *** | 1 | |||||||

| 5. GISCSR | 0.022 | 0.044 | 0.760 *** | 0.675 *** | 0.268 *** | −0.118 *** | 1 | ||||||

| 6. GISGD | 0.024 | 0.110 | 0.251 *** | 0.217 *** | −0.092 *** | 0.039 *** | 0.324 *** | 1 | |||||

| 7. EA | 0.428 | 0.434 | −0.106 *** | −0.122 *** | 0.409 *** | 0.076 *** | −0.022 *** | −0.044 *** | 1 | ||||

| 8. FS | 8.080 | 6.084 | 0.134 *** | 0.155 *** | 0.516 *** | −0.022 *** | 0.104 *** | −0.065 *** | 0.425 *** | 1 | |||

| 9. ATO | 6.363 | 5.144 | 0.233 *** | 0.255 *** | 0.135 *** | -0.243 *** | 0.196 *** | 0.067 *** | −0.243 *** | −0.049 *** | 1 | ||

| 10. PPE | 0.501 | 0.524 | 0.702 *** | 0.669 *** | 0.201 *** | 0.015 *** | 0.641 *** | 0.226 *** | 0.172 *** | 0.095 *** | 0.120 *** | 1 | |

| 11. LIQ | 0.222 | 0.391 | 0.542 *** | 0.486 *** | 0.178 *** | 0.083 *** | 0.455 *** | 0.147 *** | 0.232 *** | 0.466 *** | 0.003 *** | 0.678 *** | 1 |

| Model 1 | Model 2 | Model 3 | ||||

|---|---|---|---|---|---|---|

| Variables | Corporate Financing | Corporate Financing | Corporate Financing | |||

| Fixed Effect | GMM | Fixed Effect | GMM | Fixed Effect | GMM | |

| GIS | 0.338 *** | 0.340 *** | ||||

| CSR | 0.036 *** | 0.054 *** | ||||

| GD | 0.075 *** | 0.092 *** | ||||

| EA | −0.101 *** | −0.130 *** | −0.469 *** | −0.617 *** | −0.466 *** | −0.615 *** |

| FS | 0.106 *** | −0.119 *** | 0.091 | 0.352 *** | 0.137 | 0.447 *** |

| ATO | 0.003 *** | 0.002 *** | 0.007 *** | 0.004 *** | 0.008 *** | 0.004 *** |

| PPE | 0.118 *** | 0.115 *** | 0.548 *** | 0.579 *** | 0.547 *** | 0.578 *** |

| LIQ | −0.016 *** | −0.014 *** | 0.023 | −0.008 *** | 0.019 *** | −0.012 |

| Constant | 0.021 *** | 0.023 *** | 0.131 *** | 0.116 *** | 0.154 *** | 0.154 *** |

| R2 | 0.9711 | 0.6653 | 0.6663 | |||

| F | 20.80 *** | 12.02 *** | 12.37 | |||

| N | 3006 | 2403 | 3006 | 2403 | 3006 | 2403 |

| Hausman Test | 774.82 *** | 60.77 *** | 98.17 *** | |||

| Wald Chi2 | 89,566.40 *** | 4168.49 *** | 4167.28 *** | |||

| Model 4 | Model 5 | |||

|---|---|---|---|---|

| Variables | Corporate Financing | Corporate Financing | ||

| Fixed Effect | GMM | Fixed Effect | GMM | |

| GIS | 0.327 *** | 0.330 *** | 0.331 *** | 0.340 *** |

| CSR | -0.002 | 0.008 | ||

| GISCSR | 0.580 *** | 0.425 *** | ||

| GD | 0.018 *** | 0.022 *** | ||

| GISGD | 0.044 *** | 0.026 *** | ||

| EA | −0.093 *** | −0.121 *** | −0.101 *** | −0.128 *** |

| FS | 0.113 *** | −0.104 *** | 0.109 *** | 0.118 *** |

| ATO | 0.002 *** | 0.001 *** | 0.007 *** | 0.002 *** |

| PPE | 0.108 *** | 0.106 *** | 0.117 *** | 0.113 *** |

| LIQ | −0.015 *** | −0.013 *** | −0.016 *** | −0.014 *** |

| Constant | 0.024*** | 0.012 *** | 0.015 *** | 0.017 ** |

| R2 | 0.9743 | 0.9615 | ||

| F | 15.79 *** | 19.92 *** | ||

| N | 3006 | 2403 | 3006 | 2403 |

| Hausman Test | 564.03 *** | 433.66 *** | ||

| Wald Chi2 | 98,063.04 *** | 90,936.28 *** | ||

| Model 1 | Model 2 | Model 3 | Model 4 | Model 5 | |

|---|---|---|---|---|---|

| Variables | Corporate Financing | Corporate Financing | Corporate Financing | ||

| FGLS | FGLS | FGLS | FGLS | FGLS | |

| GIS | 0.316 *** | 0.281 *** | 0.313 *** | ||

| CSR | 0.019 *** | −0.011 *** | |||

| GISCSR | 2.279 *** | ||||

| GD | 0.018 *** | 0.014 *** | |||

| GISGD | 0.067 *** | ||||

| EA | −0.037 *** | −0.249 *** | −0.237 *** | −0.024 *** | −0.044 *** |

| FS | 0.010 | 0.624 *** | 0.689 *** | 0.070 *** | 0.027 ** |

| ATO | −0.001 *** | 0.002 *** | 0.004 *** | −0.005 *** | 0.001 ** |

| PPE | 0.159 *** | 0.586 *** | 0.582*** | 0.107 *** | 0.158 *** |

| LIQ | 0.025 *** | 0.026 ** | 0.023 *** | −0.008 ** | 0.021 *** |

| Constant | 0.003 *** | 0.014 *** | 0.013 *** | 0.015 *** | −0.001 *** |

| N | 3006 | 3006 | 3006 | 3006 | 3006 |

| Wald Chi2 | 147,243.45 *** | 22,324.66 *** | 29,497.17 *** | 248,769.99 *** | 131,969.86 *** |

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2022 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Javeed, S.A.; Teh, B.H.; Ong, T.S.; Chong, L.L.; Abd Rahim, M.F.B.; Latief, R. How Does Green Innovation Strategy Influence Corporate Financing? Corporate Social Responsibility and Gender Diversity Play a Moderating Role. Int. J. Environ. Res. Public Health 2022, 19, 8724. https://doi.org/10.3390/ijerph19148724

Javeed SA, Teh BH, Ong TS, Chong LL, Abd Rahim MFB, Latief R. How Does Green Innovation Strategy Influence Corporate Financing? Corporate Social Responsibility and Gender Diversity Play a Moderating Role. International Journal of Environmental Research and Public Health. 2022; 19(14):8724. https://doi.org/10.3390/ijerph19148724

Chicago/Turabian StyleJaveed, Sohail Ahmad, Boon Heng Teh, Tze San Ong, Lee Lee Chong, Mohd Fairuz Bin Abd Rahim, and Rashid Latief. 2022. "How Does Green Innovation Strategy Influence Corporate Financing? Corporate Social Responsibility and Gender Diversity Play a Moderating Role" International Journal of Environmental Research and Public Health 19, no. 14: 8724. https://doi.org/10.3390/ijerph19148724

APA StyleJaveed, S. A., Teh, B. H., Ong, T. S., Chong, L. L., Abd Rahim, M. F. B., & Latief, R. (2022). How Does Green Innovation Strategy Influence Corporate Financing? Corporate Social Responsibility and Gender Diversity Play a Moderating Role. International Journal of Environmental Research and Public Health, 19(14), 8724. https://doi.org/10.3390/ijerph19148724