Impact of COVID-19 on Healthcare Labor Market in the United States: Lower Paid Workers Experienced Higher Vulnerability and Slower Recovery

Abstract

:1. Introduction

2. Materials and Methods

- (1)

- Physician group combines emergency medicine physicians, radiologists, anesthesiologists, cardiologists, dermatologists, family medicine physicians, general internal medicine physicians, neurologists, obstetricians and gynecologists, general pediatricians, pathologist physicians, psychiatrists, and a miscellaneous category.

- (2)

- Healthcare aides include home health aides, personal care aides, nursing assistants, orderlies and psychiatric aides, occupational therapy assistants and aides, physical therapist assistants and aides, massage therapists, dental assistants, medical assistants, medical transcriptionists, pharmacy aides, veterinary assistants and laboratory animal caretakers, phlebotomists, and miscellaneous healthcare support workers.

- (3)

- Technicians include dental hygienists, cardiovascular technologists and technicians, diagnostic medical sonographers, radiologic technologists and technicians, magnetic resonance imaging technologists, nuclear medicine technologists and medical dosimetrists, emergency medical technicians, paramedics, pharmacy technicians, psychiatric technicians, surgical technologists, veterinary technologists and technicians, dietetic technicians and ophthalmic medical technicians, medical records specialists, dispensing opticians, miscellaneous health technologists and technicians, and a miscellaneous category for other healthcare practitioners and technical occupations.

- (4)

- Nurses include registered nurses, licensed practical nurses, and licensed vocational nurses.

- (5)

- Midlevel practitioners include physician assistants, nurse anesthetists, nurse practitioners, and nurse midwives.

- (6)

- “Other therapists” include chiropractors, dietitians and nutritionists, optometrists, podiatrists, audiologists, occupational therapists, physical therapists, radiation therapists, recreational therapists, respiratory therapists, speech-language pathologists, acupuncturists, a miscellaneous category for all other therapists, and a miscellaneous category for all other healthcare diagnosing or treating practitioners.

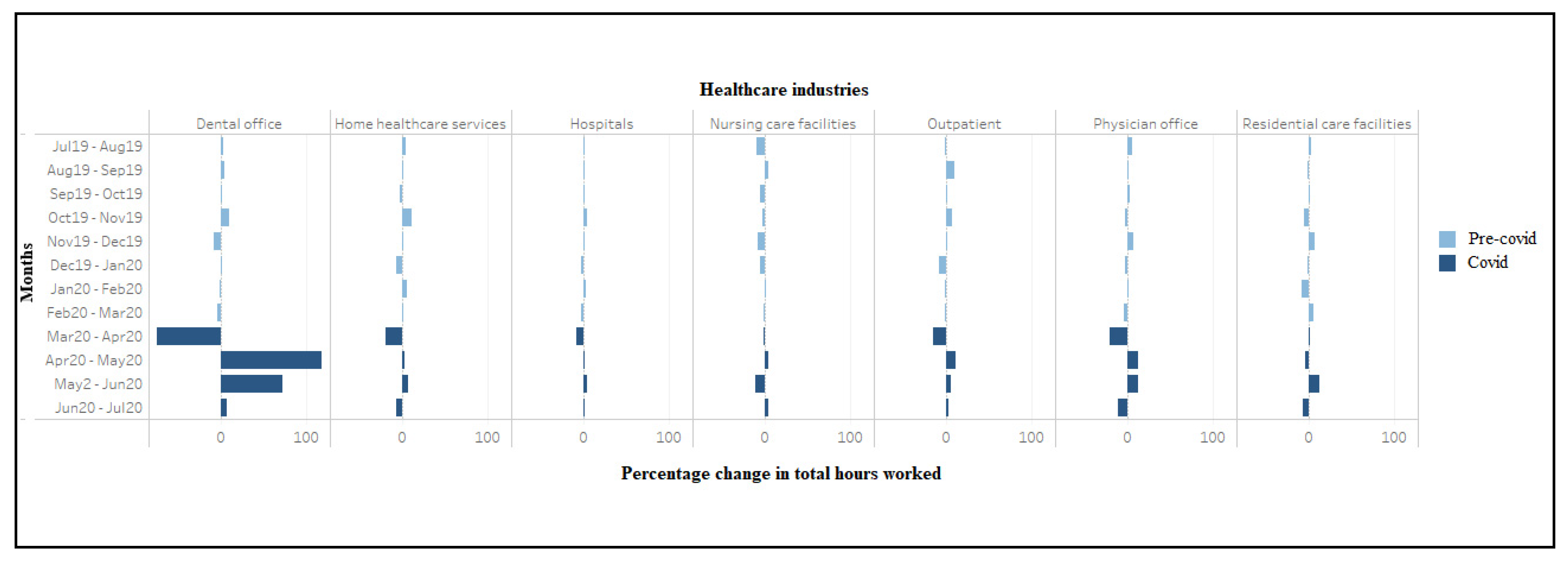

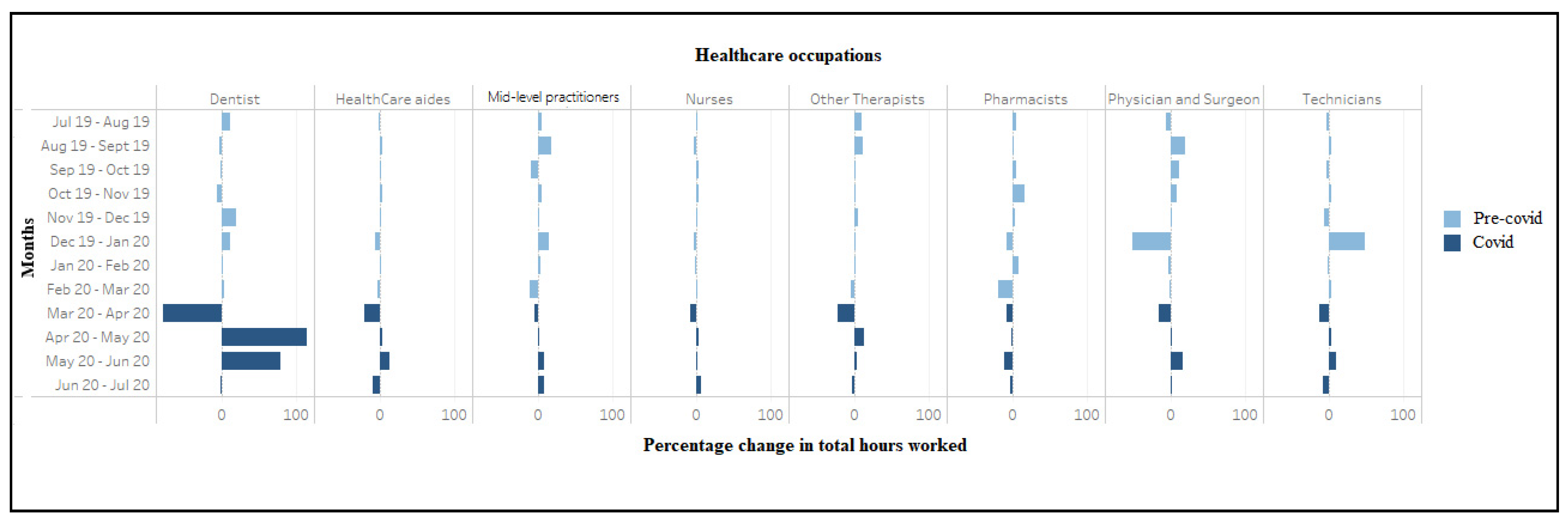

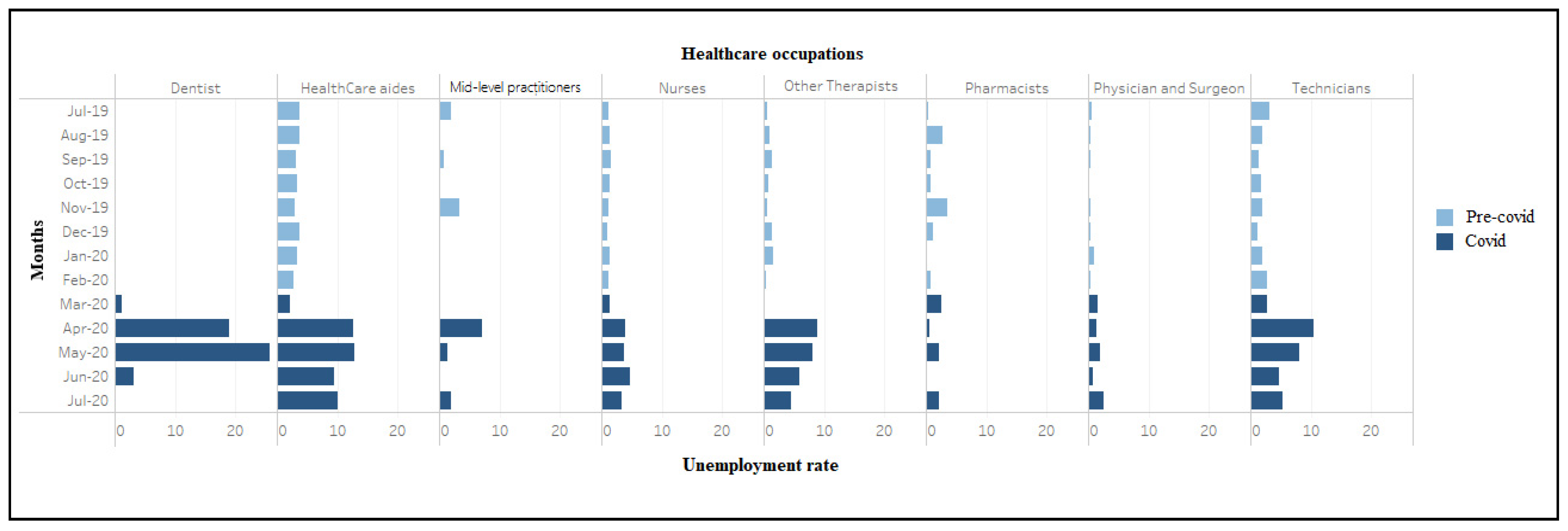

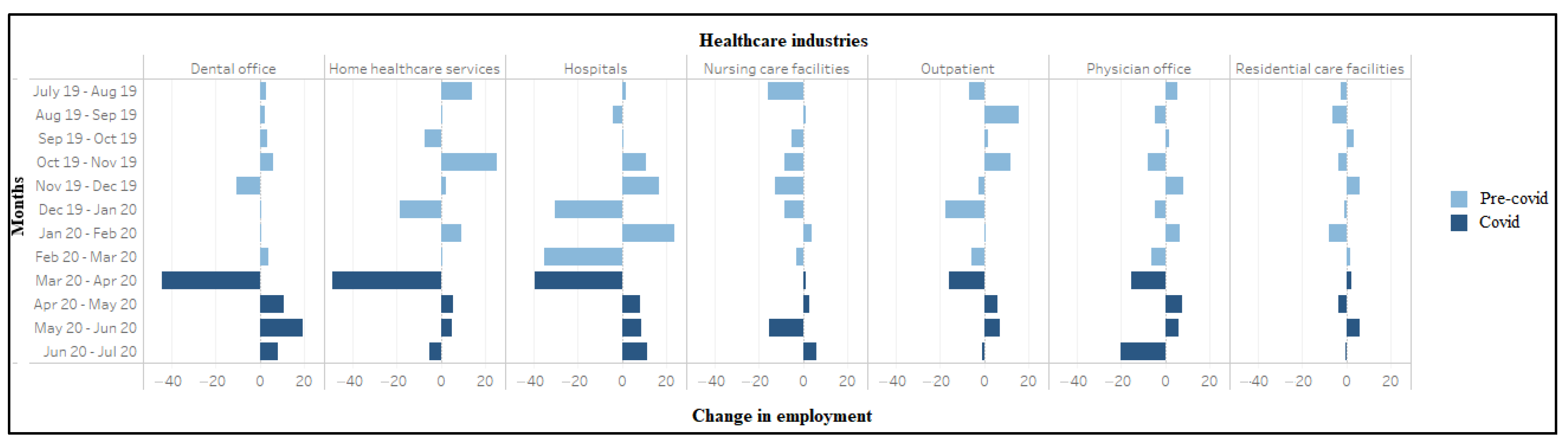

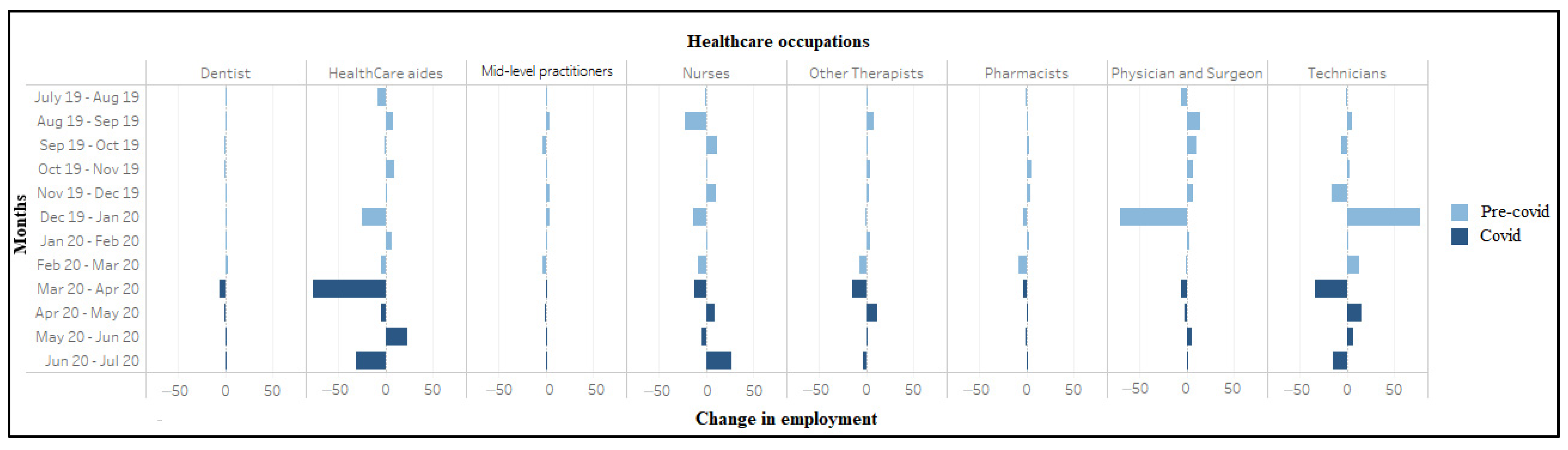

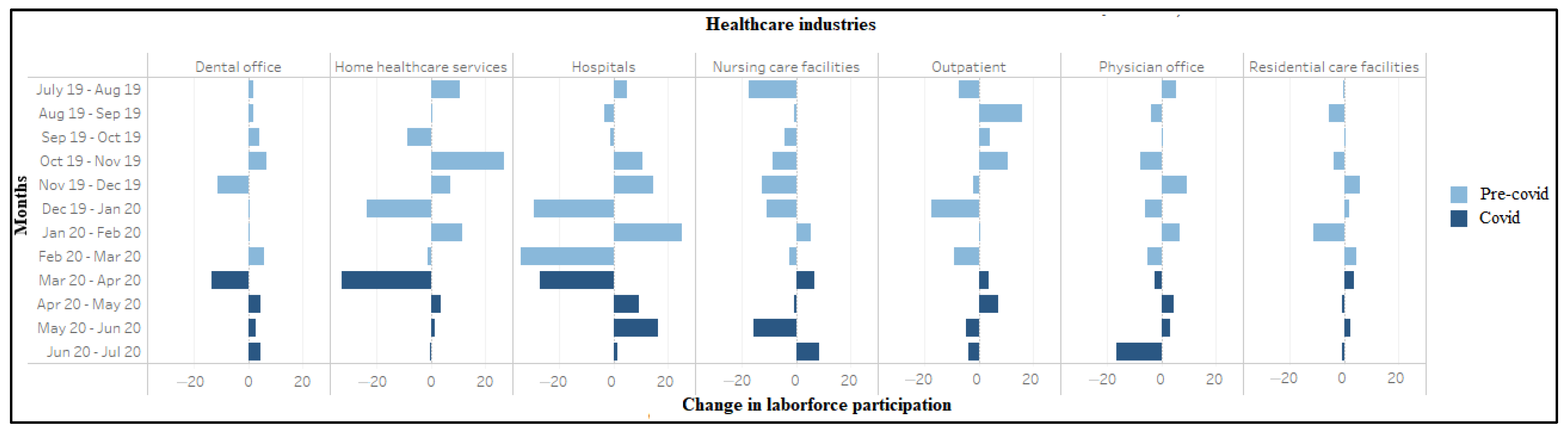

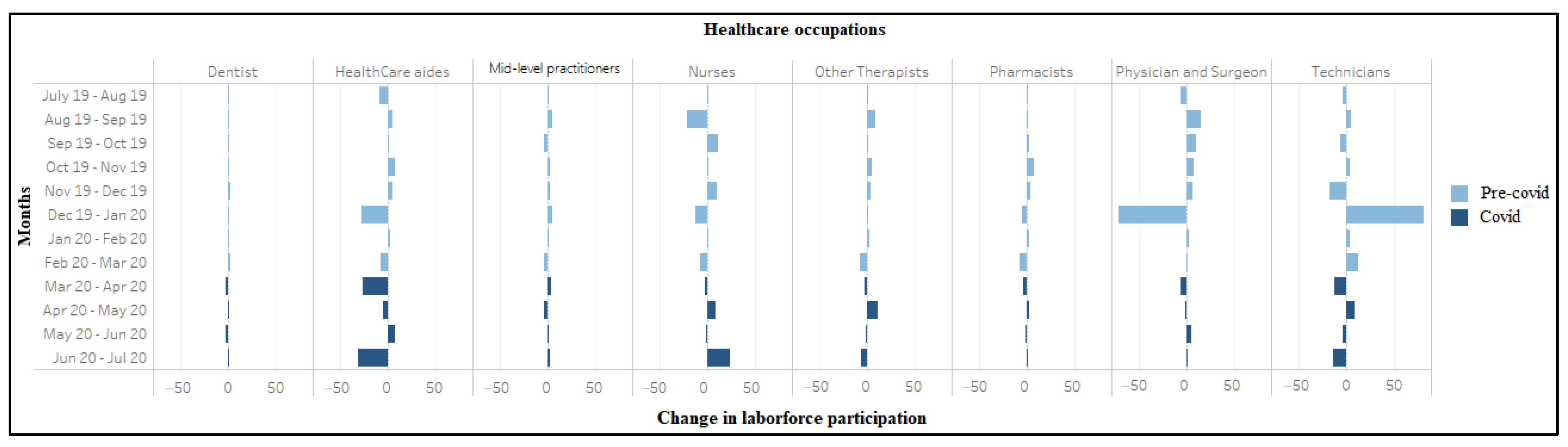

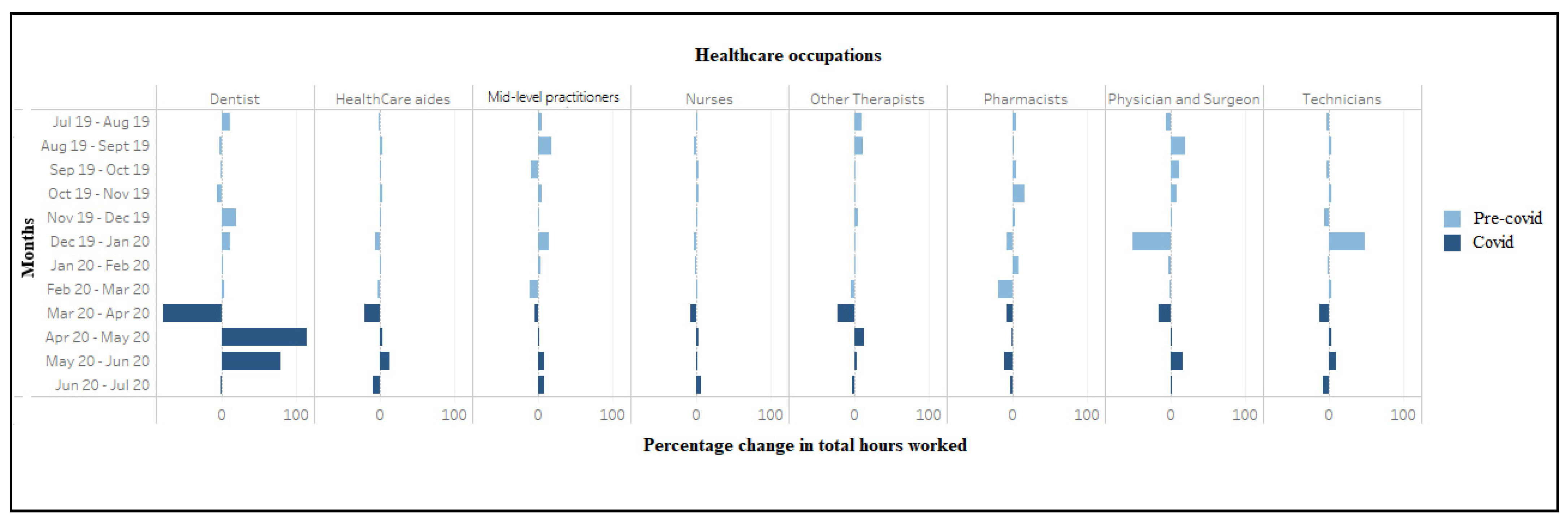

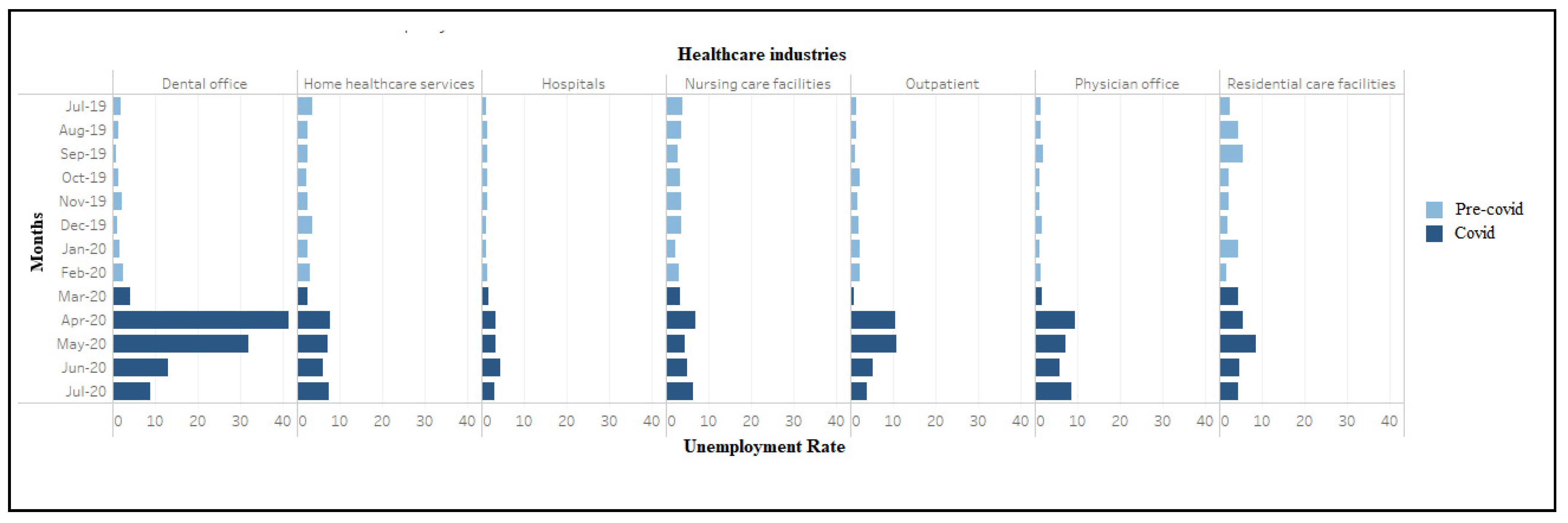

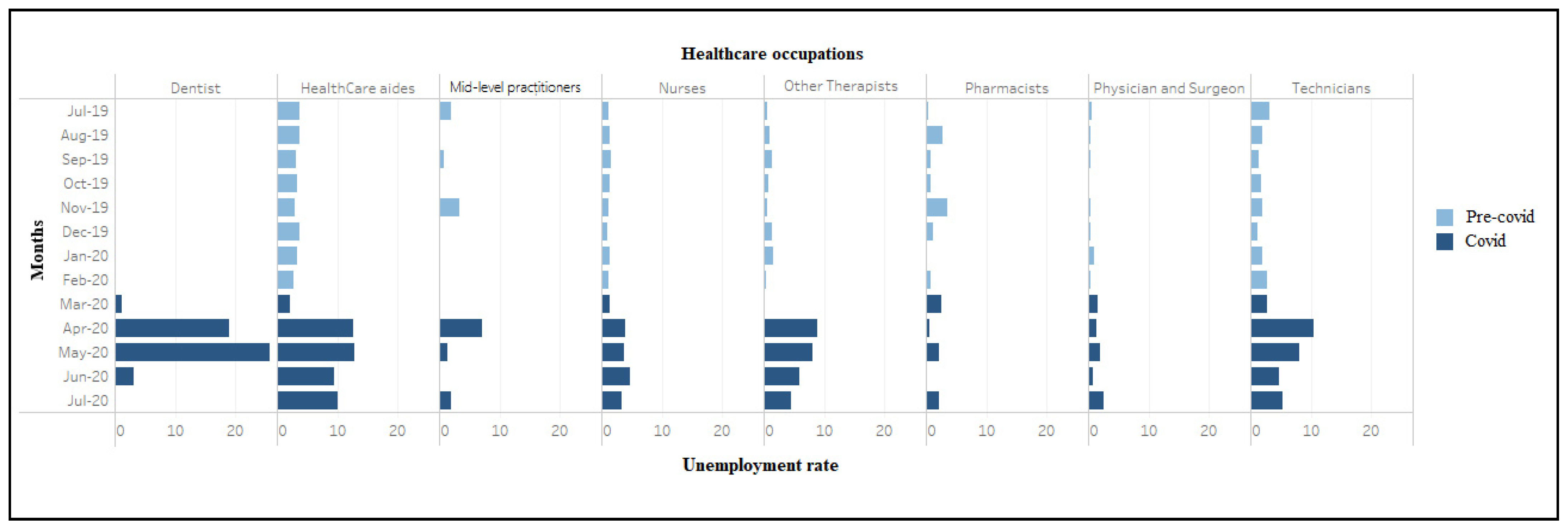

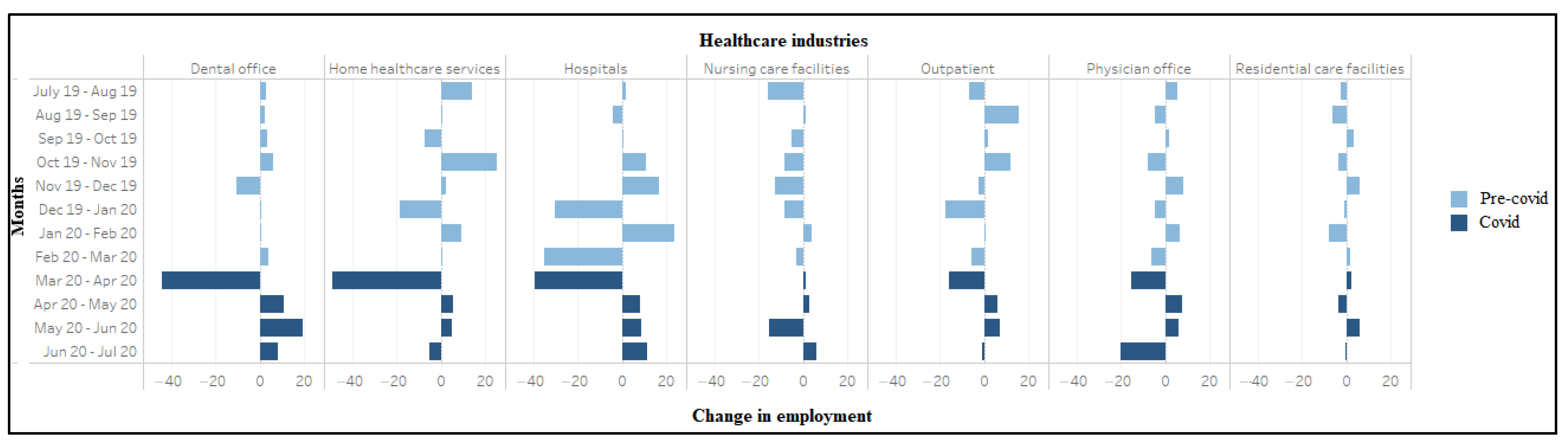

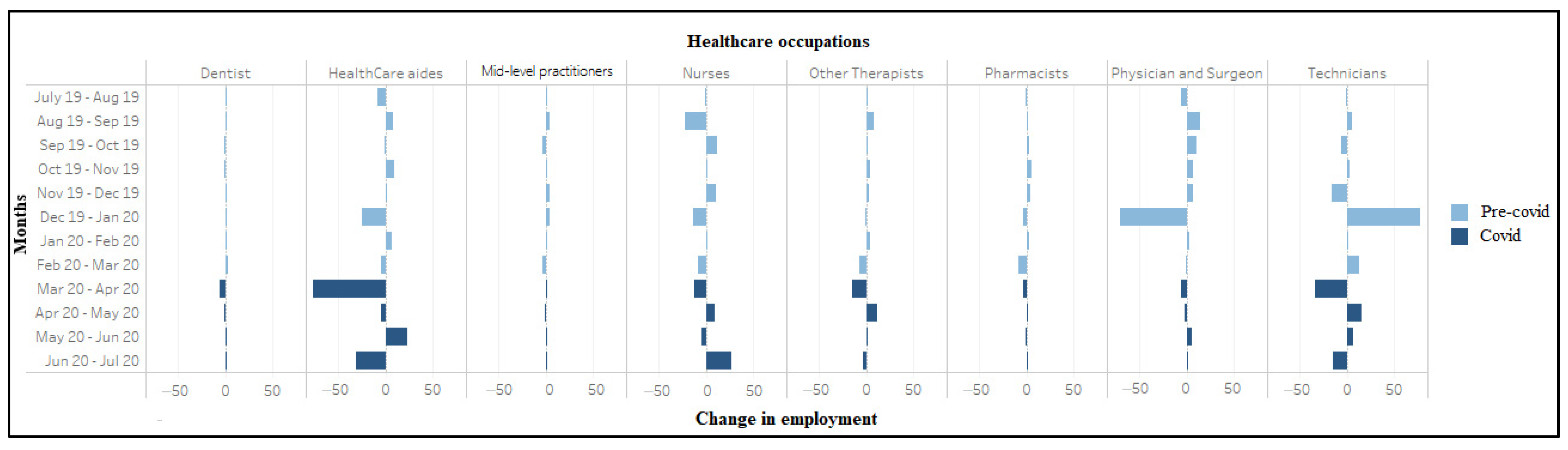

3. Results

4. Discussion

Limitations

5. Conclusions

Author Contributions

Funding

Institutional Review Board Statement

Informed Consent Statement

Data Availability Statement

Conflicts of Interest

Appendix A

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

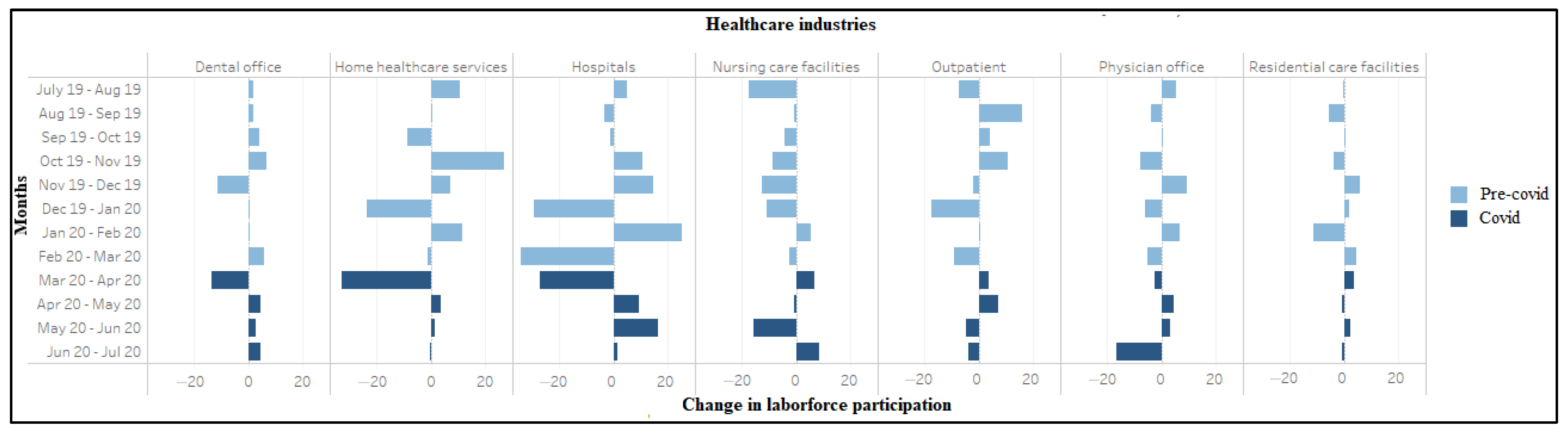

| Industry Weighted | ||||||||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| 2019 | 2020 | |||||||||||||||||

| Industry | Outcome | Mar-19 | Apr-19 | May-19 | June-19 | Jul-19 | Aug-19 | Sep-19 | Oct-19 | Nov-19 | Dec-19 | Jan-20 | Feb-20 | Mar-20 | Apr-20 | May-20 | Jun-20 | Total Weighted |

| Physician office | Umemployed | 1.8 | 2.0 | 3.7 | 3.2 | 2.5 | 2.6 | 3.3 | 1.7 | 1.8 | 2.9 | 1.7 | 2.2 | 2.9 | 15.6 | 12.3 | 9.9 | 59.48965 |

| Change in unemployement | 0.2 | 1.8 | −0.5 | −0.7 | 0.1 | 0.7 | −1.6 | 0.1 | 1.0 | −1.1 | 0.5 | 0.7 | 12.6 | −3.2 | −2.5 | |||

| Employed | 141.3 | 146.3 | 146 | 155.8 | 165.0 | 170.5 | 166.2 | 167.7 | 159.7 | 168.1 | 163.1 | 169.7 | 163.7 | 148.4 | 156.1 | 162.0 | 1960.21 | |

| Change in employement | 5.0 | −0.3 | 9.8 | 9.2 | 5.6 | −4.4 | 1.6 | −8.1 | 8.4 | −4.9 | 6.5 | −6.0 | −15.2 | 7.7 | 5.9 | |||

| Labor force | 143 | 148.3 | 149.8 | 159 | 167.5 | 173.1 | 169.5 | 169.5 | 161.5 | 170.9 | 164.9 | 171.9 | 166.6 | 164.0 | 168.5 | 171.9 | 2019.7 | |

| Change in labor force | 5.3 | 1.5 | 9.2 | 8.5 | 5.6 | −3.7 | 0.0 | −7.9 | 9.4 | −6.0 | 7.0 | −5.3 | −2.6 | 4.5 | 3.4 | |||

| Unemployement rate | 1.2 | 1.3 | 2.5 | 2.0 | 1.5 | 1.5 | 2.0 | 1.0 | 1.1 | 1.7 | 1.1 | 1.3 | 1.8 | 9.5 | 7.3 | 5.7 | ||

| Actual hours worked | 5391.5 | 5585.4 | 5502.8 | 5835.9 | 5964.5 | 6262.3 | 6232.1 | 6411.0 | 6205.9 | 6643.8 | 6380.6 | 6390.7 | 6073.3 | 4761.3 | 5357.2 | 5972.4 | ||

| Dental office | Umemployed | 1.3 | 0.5 | 1.5 | 1.3 | 1.7 | 1.2 | 0.7 | 1.5 | 2.2 | 1.1 | 1.5 | 2.2 | 4.2 | 35.1 | 28.7 | 12.1 | 92.09052 |

| Change in unemployed | −0.8 | 1.0 | −0.2 | −0.6 | −0.4 | 0.7 | 0.7 | −1.0 | 0.3 | 0.7 | 2.0 | 30.9 | −6.4 | −16.6 | ||||

| Employed | 82.5 | 91.3 | 90.7 | 93.1 | 85.6 | 88.3 | 90.7 | 94.1 | 100.1 | 89.8 | 90.1 | 90.2 | 94.0 | 49.8 | 60.6 | 80.0 | 1013.33333 | |

| Change in employement | 8.8 | −0.6 | 2.4 | −7.5 | 2.7 | 2.4 | 3.5 | 5.9 | −10.3 | 0.4 | 0.1 | 3.8 | −44.2 | 10.8 | 19.5 | |||

| Labor force | 83.8 | 91.8 | 92.1 | 94.3 | 87.4 | 89.5 | 91.4 | 95.6 | 102.2 | 90.9 | 91.6 | 92.4 | 98.2 | 84.9 | 89.3 | 92.1 | 1105.424 | |

| Change in labor force | 8.0 | 0.3 | 2.2 | −6.9 | 2.1 | 1.9 | 4.2 | 6.6 | −11.3 | 0.7 | 0.8 | 5.8 | −13.3 | 4.4 | 2.8 | |||

| Unemployement rate | 1.6 | 0.5 | 1.6 | 1.4 | 2.0 | 1.3 | 0.8 | 1.5 | 2.1 | 1.2 | 1.6 | 2.4 | 4.3 | 41.3 | 32.1 | 13.1 | ||

| Actual hours worked | 2757 | 3055 | 3079 | 3209 | 2921.7 | 2995.8 | 3107.5 | 3142.1 | 3417.9 | 3100.9 | 3100.8 | 3046.5 | 2923.1 | 717.1 | 1559.4 | 2671.8 | ||

| Hospitals | Umemployed | 11.1 | 11 | 9.4 | 10.4 | 7.4 | 10.7 | 11.5 | 9.8 | 9.7 | 8.0 | 9.1 | 10.6 | 11.7 | 23.7 | 24.8 | 32.5 | 169.475 |

| Change in unemployement | −0.1 | −1.6 | 1.0 | −3.0 | 3.3 | 0.7 | −1.7 | −0.1 | −1.7 | 1.1 | 1.4 | 1.2 | 12.0 | 1.1 | 7.7 | |||

| Employed | 731 | 744 | 733 | 712 | 743.8 | 745.5 | 741.2 | 741.7 | 752.7 | 769.2 | 738.8 | 762.6 | 727.3 | 687.9 | 696.2 | 705.0 | 8812.026 | |

| Change in employement | 13.0 | −11.0 | −21.0 | 31.8 | 1.7 | −4.3 | 0.5 | 11.0 | 16.6 | −30.4 | 23.8 | −35.3 | −39.4 | 8.3 | 8.8 | |||

| Labor force | 742 | 755 | 742 | 722 | 751.2 | 756.2 | 752.7 | 751.5 | 762.4 | 777.2 | 747.9 | 773.2 | 739.0 | 711.7 | 721.1 | 737.5 | 8981.5 | |

| Change in labor force | 13.0 | −13.0 | −20.0 | 29.2 | 5.0 | −3.5 | −1.2 | 10.9 | 14.9 | −29.3 | 25.2 | −34.2 | −27.3 | 9.4 | 16.5 | |||

| Unemployement rate | 1.5 | 1.5 | 1.3 | 1.4 | 1.0 | 1.4 | 1.5 | 1.3 | 1.3 | 1.0 | 1.2 | 1.4 | 1.6 | 3.3 | 3.4 | 4.4 | ||

| Actual hours worked | 27,349 | 27,772 | 27,232 | 26,213 | 27,304.8 | 27,226.8 | 27,642.4 | 27,793.2 | 28,675.5 | 28,966.8 | 27,827.1 | 28,334.4 | 27,258.5 | 24,831.1 | 24,954.8 | 26,028.3 | ||

| Nursing care facilities | Umemployed | 2.3 | 4.3 | 7.3 | 6.2 | 7.9 | 6.4 | 4.7 | 6.0 | 5.9 | 5.7 | 3.0 | 4.5 | 4.9 | 10.5 | 6.9 | 6.9 | 73.29763 |

| Change in unemployement | 2.0 | 3.0 | −1.1 | 1.7 | −1.5 | −1.6 | 1.2 | −0.1 | −0.2 | −2.6 | 1.4 | 0.5 | 5.5 | −3.5 | 0.0 | |||

| Employed | 156 | 164 | 173 | 189 | 188.5 | 172.6 | 173.6 | 168.2 | 159.7 | 147.1 | 138.9 | 142.9 | 140.0 | 141.4 | 144.2 | 128.7 | 1845.952 | |

| Change in employement | 8.0 | 9.0 | 16.0 | −0.5 | −15.8 | 1.0 | −5.4 | −8.5 | −12.6 | −8.2 | 4.0 | −2.9 | 1.5 | 2.7 | −15.5 | |||

| Labor force | 158.3 | 168.3 | 180.4 | 195.6 | 196.4 | 179.0 | 178.3 | 174.2 | 165.6 | 152.8 | 142.0 | 147.4 | 144.9 | 151.9 | 151.1 | 135.6 | 1919.249 | |

| Change in labor force | 10.0 | 12.1 | 15.2 | 0.8 | −17.4 | −0.6 | −4.2 | −8.5 | −12.8 | −10.8 | 5.4 | −2.5 | 7.0 | −0.8 | −15.5 | |||

| Unemployement rate | 1.5 | 2.6 | 4.0 | 3.2 | 4.0 | 3.6 | 2.7 | 3.4 | 3.6 | 3.7 | 2.1 | 3.0 | 3.4 | 6.9 | 4.6 | 5.1 | ||

| Actual hours worked | 5405 | 5777 | 6007 | 6824 | 6796.6 | 6128.5 | 6356.4 | 6004.4 | 5793.7 | 5298.6 | 4942.6 | 5013.3 | 4928.6 | 4857.7 | 5059.6 | 4460.8 | ||

| Residential care facilities | Umemployed | 1.2 | 2.2 | 1.8 | 1.3 | 2.8 | 4.7 | 5.7 | 2.1 | 2.1 | 2.0 | 4.6 | 1.6 | 4.3 | 5.7 | 8.6 | 4.9 | 49.21255 |

| Change in unemployement | 1.0 | −0.4 | −0.5 | 1.5 | 2.0 | 0.9 | −3.5 | −0.1 | −0.1 | 2.6 | −3.0 | 2.7 | 1.4 | 2.9 | −3.8 | |||

| Employed | 104 | 102 | 101 | 102 | 102.8 | 100.4 | 94.0 | 97.6 | 93.8 | 100.0 | 99.3 | 91.2 | 93.2 | 95.7 | 92.0 | 98.1 | 1158.118 | |

| Change in employement | −2.0 | −1.0 | 1.0 | 0.8 | −2.4 | −6.4 | 3.5 | −3.7 | 6.2 | −0.7 | −8.1 | 2.0 | 2.5 | −3.7 | 6.1 | |||

| Labor force | 105.2 | 104.2 | 102.5 | 103.3 | 105.5 | 105.1 | 99.7 | 99.7 | 95.9 | 102.0 | 103.9 | 92.8 | 97.5 | 101.5 | 100.6 | 103.0 | 1207.331 | |

| Change in labor force | −1.0 | −1.7 | 0.8 | 2.2 | −0.4 | −5.4 | 0.0 | −3.8 | 6.1 | 1.9 | −11.1 | 4.8 | 3.9 | −0.8 | 2.3 | |||

| Unemployement rate | 1.1 | 2.1 | 1.8 | 1.3 | 2.6 | 4.5 | 5.7 | 2.2 | 2.2 | 2.0 | 4.4 | 1.7 | 4.4 | 5.7 | 8.6 | 4.7 | ||

| Actual hours worked | 3586 | 3665 | 3671 | 3572 | 3552.1 | 3620.6 | 3531.5 | 3517.4 | 3319.1 | 3542.7 | 3495.3 | 3189.7 | 3363.5 | 3391.2 | 3231.6 | 3605.2 | ||

| Home healthcare services | Umemployed | 14.1 | 11.4 | 14 | 13.7 | 12.1 | 8.7 | 8.5 | 7.3 | 9.1 | 13.7 | 8.6 | 10.7 | 9.0 | 25.3 | 23.6 | 20.4 | 156.8995 |

| Change in unemployement | −2.7 | 2.6 | −0.3 | −1.6 | −3.5 | −0.2 | −1.2 | 1.8 | 4.6 | −5.1 | 2.1 | −1.8 | 16.3 | −1.7 | −3.3 | |||

| Employed | 354 | 325 | 344 | 348 | 322.0 | 336.1 | 336.9 | 329.5 | 354.8 | 357.3 | 339.0 | 348.4 | 348.8 | 299.8 | 305.4 | 310.3 | 3988.39 | |

| Change in employement | −29.0 | 19.0 | 4.0 | −26.0 | 14.2 | 0.7 | −7.4 | 25.3 | 2.5 | −18.4 | 9.4 | 0.4 | −49.0 | 5.6 | 5.0 | |||

| Labor force | 368.1 | 336.4 | 358 | 362.1 | 334.1 | 344.8 | 345.3 | 336.8 | 363.9 | 371.1 | 347.6 | 359.1 | 357.8 | 325.1 | 329.0 | 330.7 | 4145.29 | |

| Change in labor force | −31.7 | 21.6 | 4.1 | −28.0 | 10.7 | 0.5 | −8.5 | 27.1 | 7.1 | −23.5 | 11.6 | −1.3 | −32.7 | 3.9 | 1.7 | |||

| Unemployement rate | 3.8 | 3.4 | 3.9 | 3.8 | 3.6 | 2.5 | 2.5 | 2.2 | 2.5 | 3.7 | 2.5 | 3.0 | 2.5 | 7.8 | 7.2 | 6.2 | ||

| Actual hours worked | 12,144 | 11,475 | 12,196 | 12,223 | 11,415.6 | 11,859.8 | 12,014.7 | 11,579.3 | 12,790.9 | 12,690.5 | 11,788.7 | 12,363.8 | 12,274.2 | 9795.0 | 10,071.5 | 10,772.2 | ||

| Outpatient | Umemployed | 2.9 | 2.4 | 2.2 | 2.9 | 2.7 | 2.4 | 2.5 | 4.9 | 3.9 | 4.6 | 4.5 | 4.6 | 1.6 | 21.0 | 22.2 | 10.7 | 85.56696 |

| Change in unemployement | −0.5 | −0.2 | 0.7 | −0.2 | −0.3 | 0.1 | 2.4 | −1.0 | 0.7 | −0.1 | 0.1 | −3.0 | 19.4 | 1.3 | −11.5 | |||

| Employed | 194.6 | 201.6 | 206 | 198 | 197.2 | 190.2 | 206.1 | 207.8 | 219.5 | 217.0 | 199.4 | 199.5 | 193.6 | 177.9 | 183.9 | 190.9 | 2383.066 | |

| Change in employement | 7.0 | 4.4 | −8.0 | −0.8 | −6.9 | 15.8 | 1.7 | 11.7 | −2.5 | −17.6 | 0.1 | −5.9 | −15.6 | 6.0 | 7.0 | |||

| Labor force | 197.5 | 204 | 208 | 200.9 | 199.9 | 192.7 | 208.6 | 212.7 | 223.4 | 221.5 | 203.9 | 204.1 | 195.1 | 198.9 | 206.1 | 201.7 | 2468.633 | |

| Change in labor force | 6.5 | 4.0 | −7.1 | −1.0 | −7.2 | 15.9 | 4.1 | 10.8 | −1.9 | −17.6 | 0.2 | −9.0 | 3.8 | 7.2 | −4.5 | |||

| Unemployement rate | 1.5 | 1.2 | 1.1 | 1.4 | 1.3 | 1.3 | 1.2 | 2.3 | 1.7 | 2.1 | 2.2 | 2.2 | 0.8 | 10.5 | 10.8 | 5.3 | ||

| Actual hours worked | 6885 | 7229 | 7542 | 7106 | 6925.1 | 6793.0 | 7437.9 | 7514.1 | 7977.5 | 7975.5 | 7218.7 | 7047.7 | 6933.1 | 5855.1 | 6457.7 | 6799.4 | ||

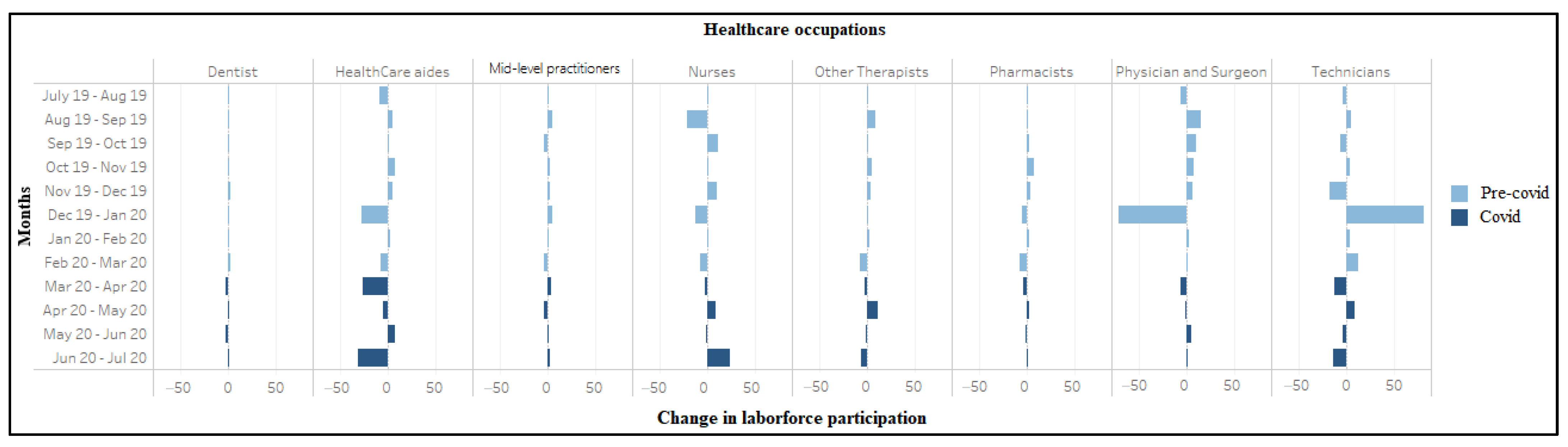

| Occupation Weighted | ||||||||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| 2019 | 2020 | |||||||||||||||||

| Industry | Outcome | Mar-19 | Apr-19 | May-19 | Jun-19 | Jul-19 | Aug-19 | Sep-19 | Oct-19 | Nov-19 | Dec-19 | Jan-20 | Feb-20 | Mar-20 | Apr-20 | May-20 | Jun-20 | Total Weighted |

| Physician and Surgeon | Umemployed | 0.7 | 0.03 | 0.07 | 0.1 | 0.5 | 0.3 | 0.3 | 0.0 | 0.5 | 0.5 | 0.6 | 0.3 | 1.0 | 0.8 | 1.0 | 0.5 | 6.421017 |

| Employed | 104 | 109 | 107 | 101 | 99.7 | 93.7 | 108.4 | 118.5 | 125.3 | 131.8 | 60.7 | 63.1 | 62.0 | 55.6 | 53.4 | 59.3 | 1031.479 | |

| Change in employment | 5.0 | −2.0 | −6.0 | −1.3 | −6.0 | 14.7 | 10.1 | 6.9 | 6.5 | −71.1 | 2.3 | −1.1 | −6.3 | −2.2 | 5.9 | |||

| Labor force | 104.7 | 109 | 107 | 101.1 | 100.2 | 94.0 | 108.8 | 118.5 | 125.8 | 132.4 | 61.4 | 63.3 | 63.0 | 56.4 | 54.4 | 59.8 | 1037.9 | |

| Change in labor force | 4.3 | −2 | −5.9 | −0.9 | −6.2 | 14.8 | 9.7 | 7.3 | 6.6 | −71.0 | 2.0 | −0.4 | −6.6 | −1.9 | 5.3 | |||

| Unemployement rate | 0.67 | 0.03 | 0.07 | 0.10 | 0.5 | 0.3 | 0.3 | 0.0 | 0.4 | 0.4 | 1.0 | 0.4 | 1.6 | 1.4 | 1.9 | 0.8 | ||

| Actual hours worked | 4929 | 5144 | 4841 | 4606 | 4470.3 | 4167.2 | 4967.4 | 5536.6 | 5969.0 | 6018.3 | 2898.2 | 2804.3 | 2736.1 | 2266.1 | 2287.0 | 2643.0 | ||

| Dentist | Umemployed | 0 | 0 | 0 | 0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.2 | 3.5 | 4.9 | 0.5 | 9.191729 |

| Employed | 16.9 | 14.5 | 17.4 | 16.3 | 15.6 | 16.0 | 15.9 | 15.5 | 15.0 | 16.9 | 17.9 | 18.6 | 20.8 | 15.1 | 14.2 | 16.3 | 197.7788 | |

| Change in employment | −2.4 | 2.9 | −1.1 | −0.67626 | 0.4 | −0.1 | −0.4 | −0.4 | 1.8 | 1.1 | 0.7 | 2.2 | −5.6 | −0.9 | 2.1 | |||

| Labor force | 17.3 | 14.5 | 17.4 | 16.3 | 15.6 | 16.0 | 15.9 | 15.5 | 15.0 | 16.9 | 17.9 | 18.6 | 21.0 | 18.7 | 19.1 | 16.8 | 206.9705 | |

| Change in labor force | −2.8 | 2.9 | −1.1 | −0.67626 | 0.4 | −0.1 | −0.4 | −0.4 | 1.8 | 1.1 | 0.7 | 2.4 | −2.3 | 0.4 | −2.3 | |||

| Unemployement rate | 0 | 0 | 0 | 0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 1.2 | 19.0 | 25.6 | 3.1 | ||

| Actual hours worked | 619 | 512.8 | 643.6 | 628.2 | 542.9 | 599.6 | 579.8 | 565.8 | 530.6 | 635.6 | 708.4 | 706.6 | 731.3 | 146.4 | 315.2 | 565.1 | ||

| Other Therapists | Umemployed | 1 | 0.4 | 0.9 | 2.7 | 0.7 | 1.1 | 1.8 | 1.0 | 0.9 | 2.1 | 2.2 | 0.6 | 0.0 | 11.9 | 11.9 | 8.4 | 42.68453 |

| Employed | 120.6 | 123.5 | 125 | 126.2 | 124.7 | 125.9 | 133.2 | 134.2 | 138.7 | 141.1 | 140.4 | 143.8 | 137.0 | 122.2 | 133.6 | 135.3 | 1610.058 | |

| Change in employment | 2.9 | 1.5 | 1.2 | −1.5 | 1.2 | 7.3 | 1.0 | 4.5 | 2.5 | −0.8 | 3.5 | −6.8 | −14.8 | 11.4 | 1.7 | |||

| Labor force | 121.6 | 123.9 | 125.9 | 128.9 | 125.4 | 127.0 | 135.0 | 135.2 | 139.5 | 143.2 | 142.6 | 144.5 | 137.0 | 134.1 | 145.5 | 143.7 | 1652.742 | |

| Change in labor force | 2.3 | 2 | 3 | −3.5291591 | 1.6 | 8.0 | 0.1 | 4.4 | 3.7 | −0.7 | 1.9 | −7.5 | −2.9 | 11.4 | −1.8 | |||

| Unemployement rate | 0.82 | 0.32 | 0.71 | 2.09 | 0.5 | 0.9 | 1.3 | 0.7 | 0.6 | 1.5 | 1.5 | 0.4 | 0.0 | 8.9 | 8.2 | 5.9 | ||

| Actual hours worked | 4270 | 4331 | 4396 | 4202 | 3753.4 | 4138.4 | 4592.5 | 4660.0 | 4714.5 | 4941.1 | 4938.7 | 4967.3 | 4696.6 | 3648.0 | 4140.2 | 4273.6 | ||

| HealthCare aides | Umemployed | 18.8 | 16.9 | 17.3 | 20.4 | 20.7 | 20.3 | 17.5 | 18.2 | 16.5 | 20.4 | 18.0 | 14.4 | 11.8 | 62.1 | 62.8 | 47.0 | 329.696 |

| Employed | 504 | 511 | 531 | 550 | 523.4 | 515.3 | 523.6 | 523.0 | 532.2 | 533.4 | 508.4 | 514.4 | 509.3 | 432.4 | 427.1 | 450.2 | 5992.788 | |

| Change in employment | 7 | 20 | 19 | −26.6 | −8.1 | 8.3 | −0.6 | 9.2 | 1.2 | −25.0 | 6.0 | −5.1 | −76.9 | −5.3 | 23.1 | |||

| Labor force | 522.8 | 527.9 | 548.3 | 570.4 | 544.1 | 535.7 | 541.0 | 541.2 | 548.7 | 553.9 | 526.4 | 528.8 | 521.1 | 494.6 | 490.0 | 497.2 | 6322.484 | |

| Change in labor force | 5.1 | 20.4 | 22.1 | −26.3 | −8.4 | 5.3 | 0.2 | 7.5 | 5.2 | −27.5 | 2.4 | −7.7 | −26.5 | −4.6 | 7.2 | |||

| Unemployement rate | 3.60 | 3.20 | 3.16 | 3.58 | 3.8 | 3.8 | 3.2 | 3.4 | 3.0 | 3.7 | 3.4 | 2.7 | 2.3 | 12.6 | 12.8 | 9.4 | ||

| Actual hours worked | 16,675 | 17,478 | 18,332 | 18,680 | 17,745.3 | 17,358.6 | 17,745.2 | 17,691.8 | 18,191.4 | 18,079.0 | 16,898.1 | 17,006.4 | 16,423.3 | 12,813.2 | 13,244.5 | 14,887.1 | ||

| Pharmacists | Umemployed | 0.2 | 0.1 | 0.6 | 0.2 | 0.1 | 0.9 | 0.2 | 0.2 | 1.4 | 0.5 | 0.03 | 0.3 | 0.8 | 0.2 | 0.7 | 0.1 | 5.38202 |

| Employed | 38.3 | 34.3 | 31.5 | 33.5 | 30.8 | 29.8 | 30.0 | 32.5 | 38.0 | 41.8 | 37.7 | 40.0 | 31.4 | 28.4 | 29.7 | 28.9 | 398.9206 | |

| Change in employment | −4 | −2.8 | 2 | −2.70935 | −1.0 | 0.2 | 2.5 | 5.5 | 3.9 | −4.2 | 2.3 | −8.5 | −3.1 | 1.3 | −0.8 | |||

| Labor force | 38.5 | 34.4 | 32.1 | 33.7 | 30.9 | 30.7 | 30.2 | 32.7 | 39.4 | 42.3 | 37.7 | 40.2 | 32.3 | 28.6 | 30.4 | 29.0 | 404.3027 | |

| Change in labor force | −4.1 | −2.3 | 1.6 | −2.8150368 | −0.2 | −0.4 | 2.5 | 6.7 | 2.9 | −4.6 | 2.5 | −8.0 | −3.7 | 1.8 | −1.4 | |||

| Unemployement rate | 0.52 | 0.29 | 1.87 | 0.59 | 0.3 | 2.8 | 0.7 | 0.7 | 3.6 | 1.1 | 0.1 | 0.7 | 2.6 | 0.7 | 2.2 | 0.3 | ||

| Actual hours worked | 1424 | 1314 | 1210 | 1232 | 1071.9 | 1129.1 | 1138.8 | 1192.2 | 1381.2 | 1416.9 | 1303.7 | 1407.8 | 1138.0 | 1044.0 | 1032.4 | 907.4 | ||

| Technicians | Umemployed | 4.9 | 5.8 | 3.5 | 5 | 7.1 | 4.2 | 3.0 | 3.6 | 4.4 | 2.5 | 5.6 | 8.0 | 8.4 | 29.8 | 23.8 | 13.7 | 114.1234 |

| Employed | 198 | 203 | 213 | 208 | 211.7 | 211.0 | 216.4 | 209.7 | 212.3 | 196.2 | 273.6 | 274.8 | 287.0 | 253.2 | 268.2 | 274.6 | 2888.717 | |

| Change in employment | 5 | 10 | −5 | 3.6704 | −0.6 | 5.3 | −6.6 | 2.5 | −16.0 | 77.4 | 1.2 | 12.3 | −33.9 | 15.0 | 6.4 | |||

| Labor force | 202.9 | 208.8 | 216.5 | 213 | 218.8 | 215.2 | 219.4 | 213.4 | 216.7 | 198.7 | 279.2 | 282.8 | 295.4 | 283.0 | 292.0 | 288.3 | 3002.84 | |

| Change in labor force | 5.9 | 7.7 | −3.5 | 5.8 | −3.5 | 4.1 | −6.0 | 3.3 | −17.9 | 80.5 | 3.6 | 12.6 | −12.4 | 9.0 | −3.6 | |||

| Unemployement rate | 2.41 | 2.78 | 1.62 | 2.35 | 3.2 | 1.9 | 1.4 | 1.7 | 2.0 | 1.3 | 2.0 | 2.8 | 2.8 | 10.5 | 8.1 | 4.8 | ||

| Actual hours worked | 7014 | 7152 | 7544 | 7415 | 7625.7 | 7396.3 | 7642.9 | 7418.2 | 7641.1 | 7095.0 | 10,554.8 | 10,370.6 | 10,627.6 | 9170.3 | 9435.6 | 10,284.1 | ||

| Nurses | Umemployed | 7 | 5.2 | 4.6 | 5.8 | 4.9 | 5.4 | 6.1 | 5.5 | 5.0 | 4.4 | 5.4 | 4.4 | 5.7 | 15.4 | 14.7 | 18.3 | 95.28553 |

| Employed | 384 | 388 | 380 | 397 | 404.2 | 403.0 | 380.9 | 392.5 | 393.6 | 404.1 | 390.9 | 392.3 | 383.4 | 371.2 | 380.7 | 376.2 | 4672.909 | |

| Change in employment | 4 | −8 | 17 | 7.2 | −1.3 | −22.1 | 11.6 | 1.1 | 10.5 | −13.2 | 1.4 | −8.9 | −12.2 | 9.6 | −4.6 | |||

| Labor force | 391 | 393.2 | 384.6 | 402.8 | 409.1 | 408.4 | 387.0 | 397.9 | 398.6 | 408.5 | 396.3 | 396.7 | 389.1 | 386.6 | 395.5 | 394.5 | 4768.195 | |

| Change in labor force | 2.2 | −8.6 | 18.2 | 6.3 | −0.7 | −21.4 | 10.9 | 0.7 | 9.9 | −12.2 | 0.4 | −7.6 | −2.5 | 8.9 | −1.0 | |||

| Unemployement rate | 1.79 | 1.32 | 1.20 | 1.44 | 1.2 | 1.3 | 1.6 | 1.4 | 1.3 | 1.1 | 1.4 | 1.1 | 1.5 | 4.0 | 3.7 | 4.6 | ||

| Actual hours worked | 13,759 | 13,898 | 13,291 | 13,565 | 13,883 | 13,980.9 | 13,463.9 | 13,905.9 | 14,242.9 | 14,514.5 | 14,058.3 | 13,872.4 | 13,864.4 | 12,769.1 | 13,057.5 | 12,941.6 | ||

| Mid level pract | Umemployed | 0 | 0 | 1.5 | 0.4 | 0.8 | 0.0 | 0.4 | 0.0 | 1.5 | 0.0 | 0.0 | 0.0 | 0.0 | 3.6 | 0.7 | 0.0 | 6.918612 |

| Employed | 37.2 | 36.2 | 39.6 | 37.7 | 40.5 | 41.6 | 45.8 | 42.0 | 42.5 | 46.1 | 50.7 | 50.7 | 46.6 | 46.8 | 45.6 | 47.2 | 546.2965 | |

| Change in employment | −1 | 3.4 | −1.9 | 2.8 | 1.1 | 4.2 | −3.8 | 0.5 | 3.5 | 4.6 | 0.0 | −4.1 | 0.2 | −1.2 | 1.6 | |||

| Labor force | 37.2 | 36.2 | 41.1 | 38.1 | 41.3 | 41.6 | 46.2 | 42.0 | 44.0 | 46.1 | 50.7 | 50.7 | 46.6 | 50.4 | 46.3 | 47.2 | 553.2151 | |

| Change in labor force | −1 | 4.9 | −3 | 3.2 | 0.3 | 4.6 | −4.2 | 2.0 | 2.1 | 4.6 | 0.0 | −4.1 | 3.8 | −4.1 | 0.9 | |||

| Unemployement rate | 0.00 | 0.00 | 3.65 | 1.05 | 1.9 | 0.0 | 0.8 | 0.0 | 3.3 | 0.0 | 0.0 | 0.0 | 0.0 | 7.1 | 1.5 | 0.0 | ||

| Actual hours worked | 1352 | 1318 | 1479 | 1469 | 1471.3 | 1529.6 | 1791.3 | 1615.1 | 1686.8 | 1671.7 | 1898.8 | 1960.9 | 1747.3 | 1655.7 | 1644.0 | 1770.1 | ||

References

- Groshen, E.L. COVID−19′s impact on the US labor market as of September. Bus. Econ. 2020, 55, 213–228. [Google Scholar] [CrossRef]

- Kaye, A.D.; Okeagu, C.N.; Pham, A.D.; Silva, R.A.; Hurley, J.J.; Arron, B.L.; Sarfraz, N.; Lee, H.N.; Ghali, G.E.; Liu, H.; et al. Economic Impact of COVID-19 Pandemic on Health Care Facilities and Systems: International Perspectives. Best Pract. Res. Clin. Anesthesiol. 2020, in press. [Google Scholar] [CrossRef]

- Radulescu, C.V.; Ladaru, G.R.; Burlacu, S.; Constantin, F.; Ioanăș, C.; Petre, I.L. Impact of the COVID-19 Pandemic on the Romanian Labor Market. Sustainability 2021, 13, 271. [Google Scholar] [CrossRef]

- Shuai, X.; Chmura, C.; Stinchcomb, J. COVID-19, labor demand, and government responses: Evidence from job posting data. Bus. Econ. 2021, 56, 29–42. [Google Scholar] [CrossRef] [PubMed]

- Dolfman, M.L.; Insco, M.; Holden, R.J. Healthcare jobs and the Great Recession. Mon. Lab. Rev. 2018, 141, 1. [Google Scholar] [CrossRef]

- Fraher, E.; Carpenter, J.; Broome, S. Health care employment and the current economic recession. N. C. Med. J. 2009, 70, 331. [Google Scholar] [PubMed]

- Cassella, M.; Roubein, R. Health Care Workforce Is Recession Proof. Is It ‘Pandemic Proof’? Available online: https://www.politico.com/news/2020/04/20/health-care-workforce-crisis-197468 (accessed on 17 October 2020).

- Teasdale, B.; Schulman, K.A. Are US Hospitals Still “Recession-proof”? N. Engl. J. Med. 2020, 383, e82. [Google Scholar] [CrossRef] [PubMed]

- Diaz, A.; Sarac, B.A.; Schoenbrunner, A.R.; Janis, J.E.; Pawlik, T.M. Elective surgery in the time of COVID-19. Am. J. Surg. 2020, 219, 900–902. [Google Scholar] [CrossRef] [PubMed]

- Gold, J. Some Hospitals Continue with Elective Surgeries Despite COVID-19 Crisis. 2020. Available online: https://khn.org/news/some-hospitals-continue-with-elective-surgeries-despite-covid-19-crisis/ (accessed on 17 October 2020).

- The Commonwealth Fund. The Impact of the COVID-19 Pandemic on Outpatient Visits: Practices Are Adapting to the New Normal. 2020. Available online: https://www.commonwealthfund.org/publications/2020/jun/impact-covid-19-pandemic-outpatient-visits-practices-adapting-new-normal (accessed on 17 October 2020).

- Sanger-Katz, M. Why 1.4 Million Health Jobs Have Been Lost during a Huge Health Crisis. 2020. Available online: https://www.nytimes.com/2020/05/08/upshot/health-jobs-plummeting-virus.html (accessed on 17 October 2020).

- McDermott, D.; Cox, C. What Impact Has the Coronavirus Pandemic Had on Healthcare Employment? 2020. Available online: https://www.healthsystemtracker.org/chart-collection/what-impact-has-the-coronavirus-pandemic-had-on-healthcare-employment/#item-start (accessed on 17 October 2020).

- Reilly, K. An Inside Look at Healthcare Hiring in the U.S. Right Now. 2020. Available online: https://business.linkedin.com/talent-solutions/blog/trends-and-research/2020/inside-look-at-healthcare-hiring (accessed on 17 October 2020).

- Keeley, C.; Jimenez, J.; Jackson, H.; Boudourakis, L.; Salway, R.J.; Cineas, N.; Villanueva, Y.; Bell, D.; Wallach, A.B.; Schwartz, D.B.; et al. Staffing Up for The Surge: Expanding The New York City Public Hospital Workforce During The COVID-19 Pandemic. Health Aff. (Millwood) 2020, 39, 1426–1430. [Google Scholar] [CrossRef] [PubMed]

- Birkmeyer, J.D.; Barnato, A.; Birkmeyer, N.; Bessler, R.; Skinner, J. The Impact of the COVID-19 Pandemic on Hospital Admissions in The United States. Health Aff. 2020, 39, 1–7. [Google Scholar] [CrossRef] [PubMed]

- DiFazio, L.T.; Curran, T.; Bilaniuk, J.W.; Adams, J.M.; Durling-Grover, R.; Kong, K.; Nemeth, Z.H. The Impact of the COVID-19 Pandemic on Hospital Admissions for Trauma and Acute Care Surgery. Am. Surg. 2020, 86, 901–903. [Google Scholar] [CrossRef] [PubMed]

- Barker, K.; Harris, A.J. ‘Playing Russian Roulette’: Nursing Homes Told to Take the Infected. 2020. Available online: https://www.nytimes.com/2020/04/24/us/nursing-homes-coronavirus.html (accessed on 17 October 2020).

- The Centers for Medicare & Medicaid Services. Coronavirus (COVID-19) Partner Toolkit (n.d.). Available online: https://www.cms.gov/outreach-education/partner-resources/coronavirus-covid-19-partner-toolkit (accessed on 17 October 2020).

- The Centers for Medicare & Medicaid Services. COVID-19 Emergency Declaration Blanket Waivers for Health Care Providers (n.d.). Available online: https://www.cms.gov/files/document/summary-covid-19-emergency-declaration-waivers.pdf (accessed on 17 October 2020).

- United States Census Bureau Basic Monthly CPS. 2019–2020. Available online: https://www.census.gov/data/datasets/time-series/demo/cps/cps-basic.html (accessed on 17 October 2020).

- Beckhusen, J. Recent Changes in the Census Industry and Occupation Classification Systems. 2020. Available online: https://www.census.gov/library/publications/2020/demo/acs-tp78.html (accessed on 17 October 2020).

- Venegas, A. Local Dental Offices Hit Hard by COVID-19 Pandemic. 2020. Available online: https://abc30.com/dentist-industry-coronavirus/6351065/ (accessed on 17 October 2020).

- Haider, M.M.; Allana, A.; Allana, R.R. Barriers to Optimizing Teledentistry during COVID-19 Pandemic. Asia Pac. J. Public Health 2020, 32, 523–524. [Google Scholar] [CrossRef] [PubMed]

- Woods, B. How this New Jersey Hospital is Fighting the Coronavirus against All Odds. 2020. Available online: https://www.cnbc.com/2020/06/06/how-this-nj-hospital-staff-is-fighting-covid-19-and-trauma.html (accessed on 20 October 2020).

- Holly, R. HHCN Survey: 92% of Home Health Agencies Have Lost Revenue Due to Coronavirus. 2020. Available online: https://homehealthcarenews.com/2020/06/hhcn-survey−92-of-home-health-agencies-have-lost-revenue-due-to-coronavirus/ (accessed on 20 October 2020).

- Murdoch, D. The Next Once-A-Century Pandemic Is Coming Sooner than you Think—But COVID-19 Can Help Us Get Ready. 2020. Available online: https://theconversation.com/the-next-once-a-century-pandemic-is-coming-sooner-than-you-think-but-covid-19-can-help-us-get-ready−139976 (accessed on 20 October 2020).

- Glied, S. Implications of the 2017 tax cuts and jobs act for public health. Am. J. Public Health 2018, 108, 734–736. [Google Scholar] [CrossRef]

- Lempel, H.; Epstein, J.M.; Hammond, R.A. Economic cost and health care workforce effects of school closures in the U.S. PLoS Curr. 2009, 1, RRN1051. [Google Scholar] [CrossRef]

- U.S. Bureau of Labor Statistics. Employment Situation News Release. 2020. Available online: https://www.bls.gov/news.release/archives/empsit_04032020.htm (accessed on 17 October 2020).

- U.S. Bureau of Labor Statistics. How the Government Measures Unemployment. 2020. Available online: https://www.bls.gov/cps/cps_htgm.htm (accessed on 17 October 2020).

- Plewes, T.J. Seasonal Adjustment of the U.S. Unemployment Rate: Introductory Remarks. J. R. Stat. Soc. Ser. D (Stat.) 1978, 27, 177–179. [Google Scholar] [CrossRef]

- Cajner, T.; Figura, A.; Price, B.M.; Ratner, D.; Weingarden, A. Reconciling Unemployment Claims with Job Losses in the First Months of the COVID-19 Crisis (July 1, 2020). FEDS Working Paper No. 2020-055. Available online: https://ssrn.com/abstract=3655846 (accessed on 20 January 2021).

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2021 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Bhandari, N.; Batra, K.; Upadhyay, S.; Cochran, C. Impact of COVID-19 on Healthcare Labor Market in the United States: Lower Paid Workers Experienced Higher Vulnerability and Slower Recovery. Int. J. Environ. Res. Public Health 2021, 18, 3894. https://doi.org/10.3390/ijerph18083894

Bhandari N, Batra K, Upadhyay S, Cochran C. Impact of COVID-19 on Healthcare Labor Market in the United States: Lower Paid Workers Experienced Higher Vulnerability and Slower Recovery. International Journal of Environmental Research and Public Health. 2021; 18(8):3894. https://doi.org/10.3390/ijerph18083894

Chicago/Turabian StyleBhandari, Neeraj, Kavita Batra, Soumya Upadhyay, and Christopher Cochran. 2021. "Impact of COVID-19 on Healthcare Labor Market in the United States: Lower Paid Workers Experienced Higher Vulnerability and Slower Recovery" International Journal of Environmental Research and Public Health 18, no. 8: 3894. https://doi.org/10.3390/ijerph18083894

APA StyleBhandari, N., Batra, K., Upadhyay, S., & Cochran, C. (2021). Impact of COVID-19 on Healthcare Labor Market in the United States: Lower Paid Workers Experienced Higher Vulnerability and Slower Recovery. International Journal of Environmental Research and Public Health, 18(8), 3894. https://doi.org/10.3390/ijerph18083894