The Internal Connection Analysis of Information Sharing and Investment Performance in the Venture Capital Network Community

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Abstract

:1. Introduction

2. Research Methods and Design

2.1. Network Community Research

2.2. Research Hypotheses and Data

2.3. Implementation of Research Model

2.4. Definition of Research Variables

3. Research Results and Analysis

3.1. Descriptive Statistics

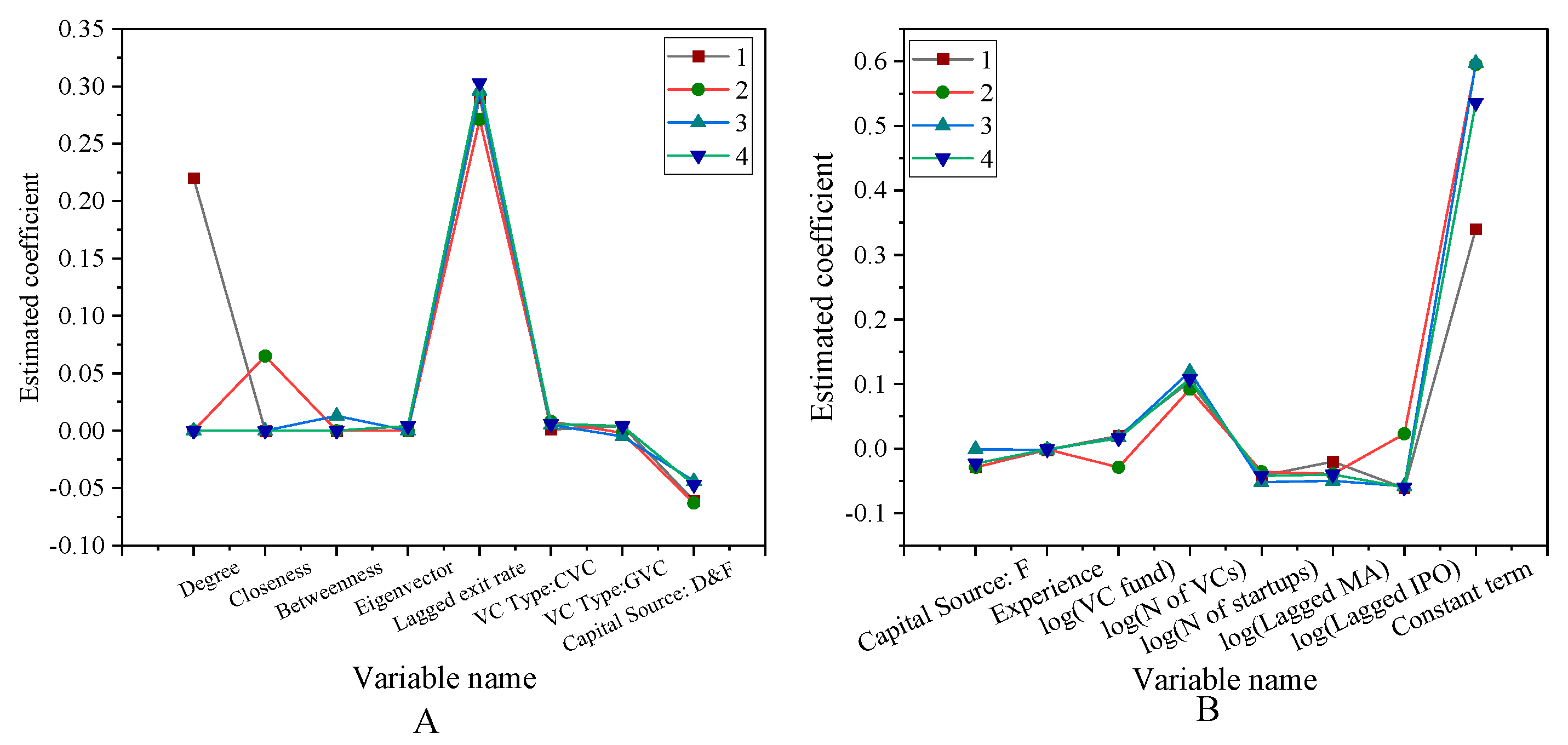

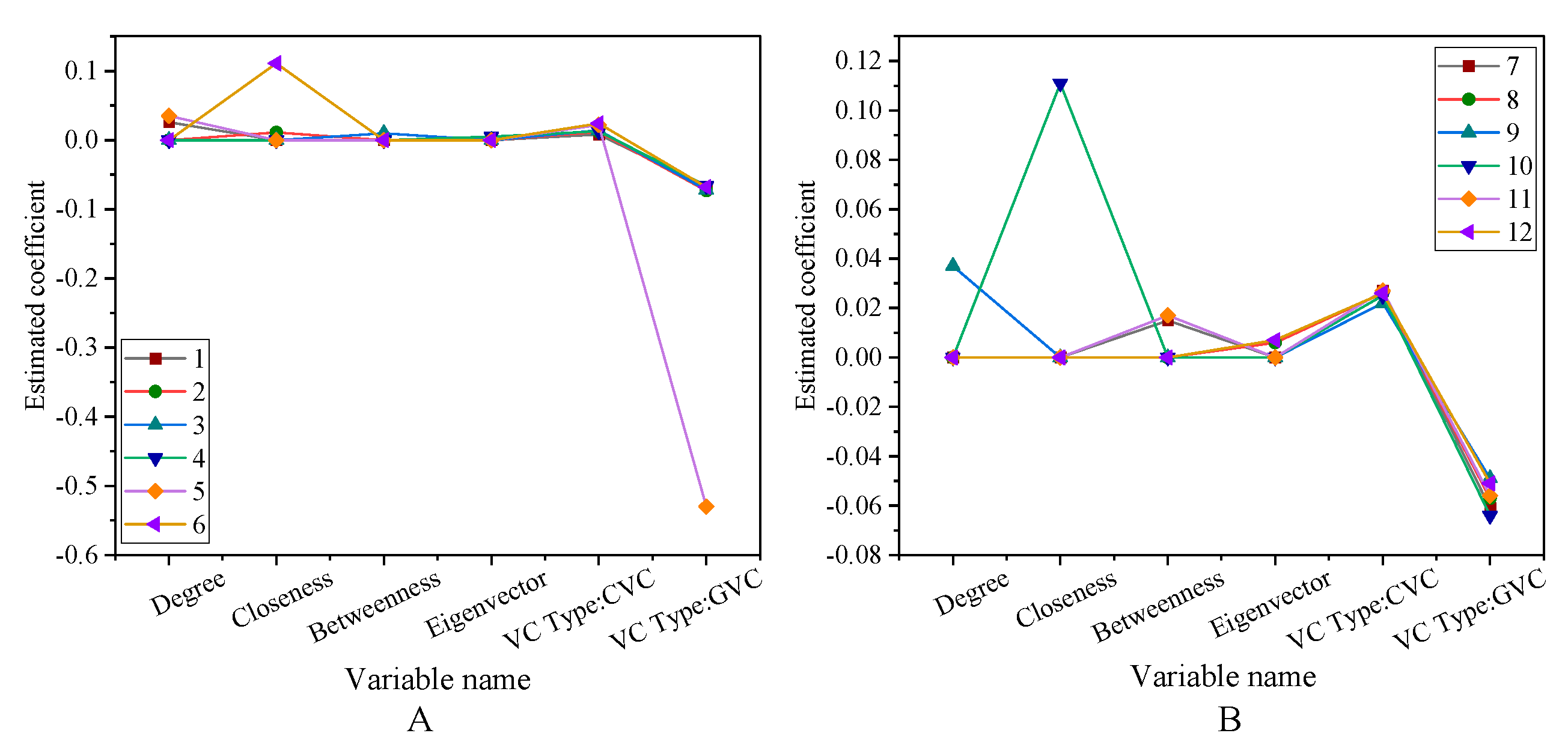

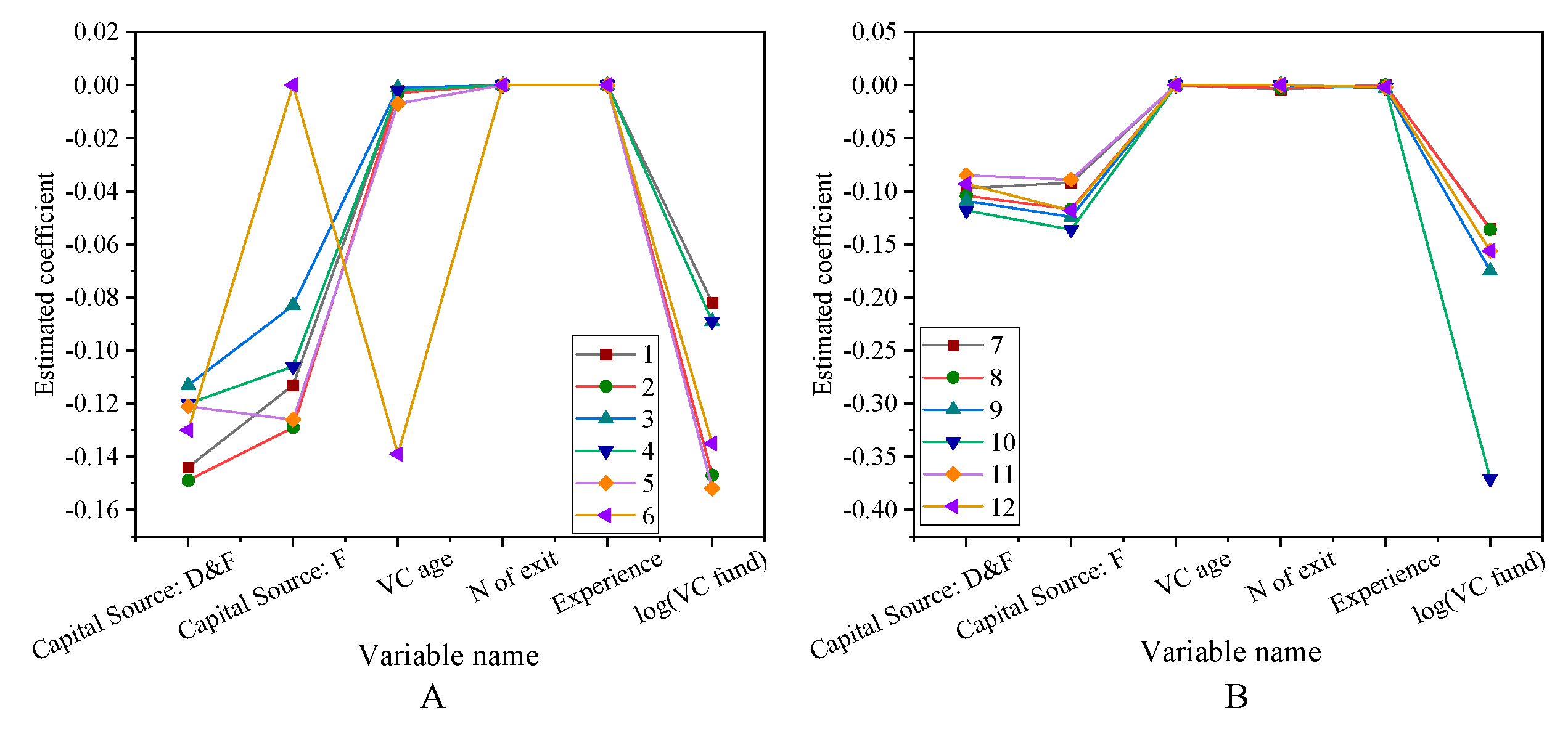

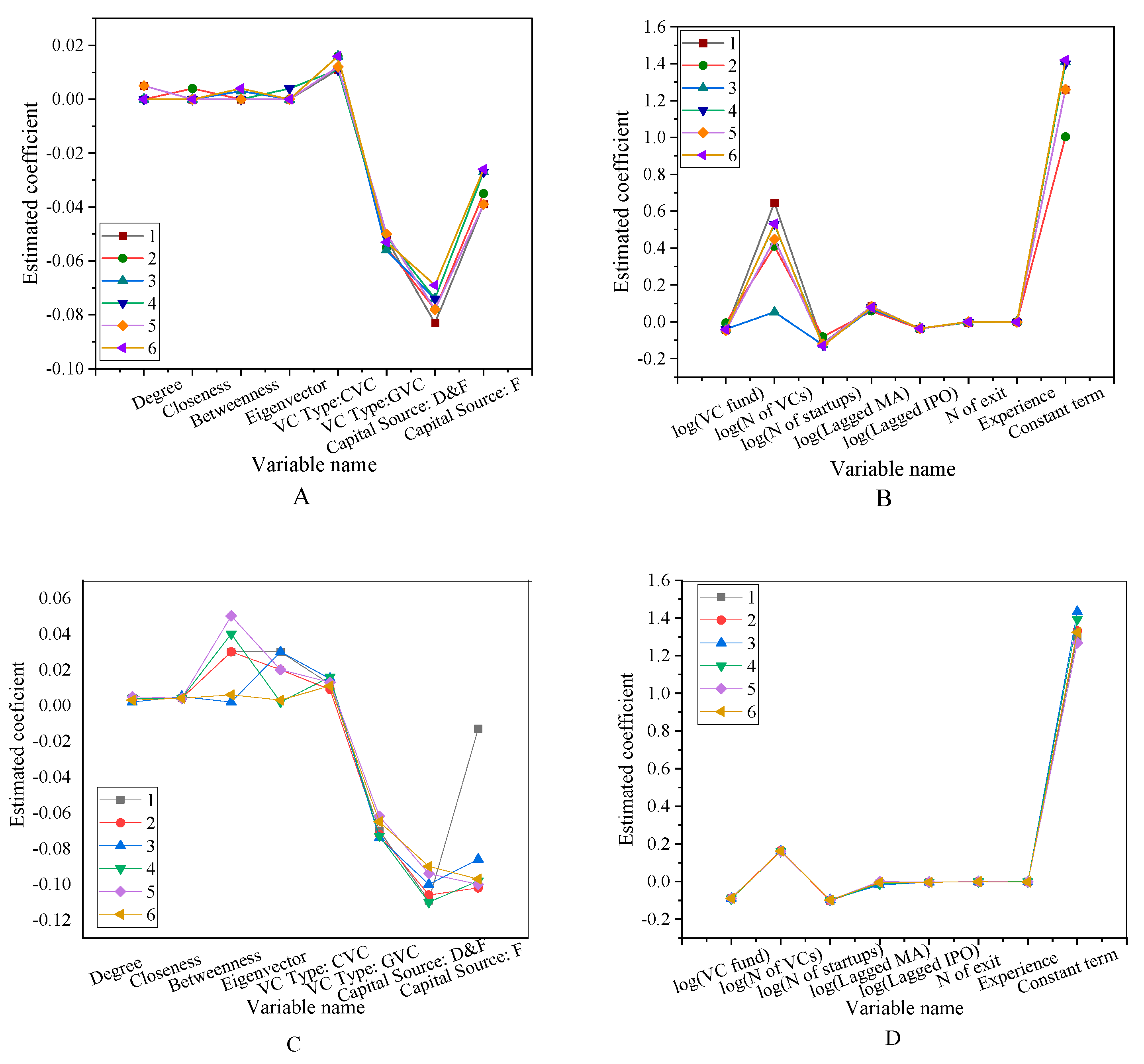

3.2. Data Analysis Results

3.3. Depth Analysis Test

3.4. Robustness Test

4. Discussion

5. Conclusions

Author Contributions

Funding

Institutional Review Board Statement

Informed Consent Statement

Data Availability Statement

Acknowledgments

Conflicts of Interest

References

- Liang, H.; Liu, G.; Yin, J.L. Venture capital reputation: A blessing or a curse for entrepreneurial firm innovation—A contingent effect of industrial distance. Front. Bus. Res. China 2019, 13, 1–25. [Google Scholar] [CrossRef]

- Pascal, G.; Axel, K.; Christophe, V. Individualism and Venture Capital: A Cross-Country Study. Manag. Int. Rev. 2019, 59, 741–777. [Google Scholar]

- Francesco, B.; Giuseppe, R.; Claudio, V. Asymmetric information and deal selection: Evidence from the Italian venture capital market. Int. Entrep. Manag. J. 2019, 15, 721–732. [Google Scholar]

- Luo, J.D.; Rong, K.; Yang, K.H.; Guo, R.; Zou, Y.Q. Syndication through social embeddedness: A comparison of foreign, private and state-owned venture capital (VC) firms. Asia Pac. J. Manag. 2019, 36, 499–527. [Google Scholar] [CrossRef]

- Moreno, B.; Valerio, C.; Pietro, P.; Silvia, L.; Lucas, L. Vito Latora. Predicting success in the worldwide start-up network. Sci. Rep. 2020, 10, 347–361. [Google Scholar]

- Bertoni, F.; Colombo, M.G.; Quas, A.; Tenca, F. The changing patterns of venture capital investments in Europe. Econ. Politica Ind. 2019, 46, 229–250. [Google Scholar] [CrossRef]

- Pierrakis, Y.; Saridakis, G. The role of venture capitalists in the regional innovation ecosystem: A comparison of networking patterns between private and publicly backed venture capital funds. J. Technol. Transf. 2019, 44, 850–873. [Google Scholar] [CrossRef]

- Bosco, D.B.; Chierici, R.; Mazzucchelli, A. Fostering entrepreneurship: An innovative business model to link innovation and new venture creation. Rev. Manag. Sci. 2019, 13, 561–574. [Google Scholar] [CrossRef]

- Amit, B.; Sanjiv, R.D.; Paul, H. The Fast and the Curious: VC Drift. J. Financ. Serv. Res. 2020, 57, 69–113. [Google Scholar]

- Jeong, J.; Kim, J.; Son, H.; Nam, D. The role of venture capital investment in startups’ sustainable growth and performance: Focusing on absorptive capacity and venture capitalists’ reputation. Sustainability 2020, 12, 3447. [Google Scholar] [CrossRef] [Green Version]

- Dhuha, A.A.; Siti, Z.M.H.; Roselina, S. Nature-inspired optimization algorithms for community detection in complex networks: A review and future trends. Telecommun. Syst. 2020, 74, 225–252. [Google Scholar]

- Parsons, S.; Kovshoff, H. Building the evidence base through school-research partnerships in autism education: The Autism Community Research Network@ Southampton [ACoRNS]. Good Autism Pract. 2019, 20, 114–121. [Google Scholar]

- Zhou, J.; Li, K.; Luo, X.; Zeng, Q.; Jiaerken, Y.; Wang, S.; Xu, X.; Liu, X.; Li, Z.; Zhang, T.; et al. Distinct impaired patterns of intrinsic functional network centrality in patients with early-and late-onset Alzheimer’s disease. Brain imaging Behav. 2021, 13, 1–10. [Google Scholar] [CrossRef]

- Naik, D.; Behera, R.K.; Ramesh, D.; Rath, S.K. Map-reduce-based centrality detection in social networks: An algorithmic approach. Arab. J. Sci. Eng. 2020, 45, 10199–10222. [Google Scholar] [CrossRef]

- Vega-Oliveros, D.A.; Gomes, P.S.; Milios, E.E.; Berton, L. A multi-centrality index for graph-based keyword extraction. Inf. Process. Manag. 2019, 56, 102063–102071. [Google Scholar] [CrossRef]

- Gurfinkel, A.J.; Rikvold, P.A. Adjustable reach in a network centrality based on current flows. Phys. Rev. E 2021, 103, 052308–052311. [Google Scholar] [CrossRef] [PubMed]

- Wang, J.B.; Yang, N.D. Dynamics of collaboration network community and exploratory innovation: The moderation of knowledge networks. Scientometrics 2019, 121, 1067–1084. [Google Scholar] [CrossRef]

- Abdulla, M.O.A.; Deniz, E.; Karagöz, M.; Gürüf, G. An experimental study on a novel defrosting method for cold room. Appl. Therm. Eng. 2021, 188, 116573–116581. [Google Scholar] [CrossRef]

- Tatiana, L.; Magdalena, C. Marketing social marketing theory to practitioners. Int. Rev. Public Nonprofit Mark. 2020, 17, 237–252. [Google Scholar]

- Jan, S.K.; Vlachopoulos, P. Social network analysis: A framework for identifying communities in higher education online learning. Technol. Knowl. Learn. 2019, 24, 621–639. [Google Scholar] [CrossRef]

- Bolivar, L.M.; Castro-Abancéns, I.; Casanueva, C.; Gallego, A. Network resource mobilisation limitations and the alliance portfolio network. Balt. J. Manag. 2021, 26, 124–134. [Google Scholar] [CrossRef]

- Hu, Z.; Hu, Y.; Jiang, Y.; Peng, Z. Pricing Constraint and the Complexity of IPO Timing in the Stock Market: A Dynamic Game Analysis. Entropy 2020, 22, 546. [Google Scholar] [CrossRef]

- Wu, J.; Luo, C.; Liu, L. A social network analysis on venture capital alliance’s exit from an emerging market. Complexity 2020, 256, 1158–1162. [Google Scholar] [CrossRef]

- Guo, X.; Li, K.; Yu, S.; Wei, B. Enterprises’ R&D Investment, Venture Capital Syndication and IPO Underpricing. Sustainability 2021, 13, 7290–7299. [Google Scholar]

- Patrick, B.; Xavier, M.; Frédéric, S. Global Public-Private Investment Partnerships: A Financing Innovation with Positive Social Impact. J. Appl. Corp. Financ. 2020, 32, 139–149. [Google Scholar]

- Liu, W.; Shao, X.; De Sisto, M.; Li, W.H. A new approach for addressing endogeneity issues in the relationship between corporate social responsibility and corporate financial performance. Financ. Res. Lett. 2021, 39, 101623–101631. [Google Scholar] [CrossRef]

- Alzoubi, H.; Yanamandra, R. Investigating the mediating role of information sharing strategy on agile supply chain. Uncertain Supply Chain. Manag. 2020, 8, 273–284. [Google Scholar] [CrossRef]

- Imbert, E.; Morone, P.; Bigi, F. Assessing the potential of social enterprises through social network analysis—Evidence from Albania. J. Evol. Econ. 2019, 29, 1211–1239. [Google Scholar] [CrossRef] [Green Version]

- Sun, W.; Zhao, Y.; Sun, L. Big data analytics for venture capital application: Towards innovation performance improvement. Int. J. Inf. Manag. 2020, 50, 557–565. [Google Scholar] [CrossRef]

- Zhang, R.; Yang, X.; Li, N.; Khan, M.A. Herd Behavior in Venture Capital Market: Evidence from China. Mathematics 2021, 9, 1509. [Google Scholar] [CrossRef]

- Glaziev, S.S. Problems and Prospects of Development of Venture Capital Institutions in Russia. Russ. Econ. J. 2021, 3, 81–103. [Google Scholar] [CrossRef]

- Hasheminejad, A.; Pishvaee, M.S. Syndicated venture capital portfolio Companies Selection: A Fuzzy Inference System—Agent based Approach. Int. J. Comput. Math. 2021, 1, 1176. [Google Scholar] [CrossRef]

- Pandher, G. The performance of venture capital investments: Failure risk, valuation uncertainty & venture characteristics. Quant. Financ. 2021, 21, 2271. [Google Scholar]

- Scarlata, M.; Alemany, L.; Zacharakis, A. A Gendered View of Risk Taking in Venture Philanthropy. J. Soc. Entrep. 2021, 15, 1–19. [Google Scholar] [CrossRef]

- Duening, T.N.; Hisrich, R.D.; Lechter, M.A. Managing the Venture: Strategy and Operations. In Technology Entrepreneurship, 3rd ed.; Academic Press: New York, NY, USA, 2021; Volume 19, pp. 291–312. [Google Scholar]

- Nahlik, C.; Fabozzi, F.J. Criteria for Successful Project Financing. World Sci. Book Chapters 2021, 43, 176–181. [Google Scholar]

- Koenig, L.; Burghof, H.P. The Investment Style Drift Puzzle and Risk-Taking in Venture Capital. SSRN Electron. J. 2021, 21, 66–74. [Google Scholar] [CrossRef]

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2021 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Feng, B.; Sun, K.; Zhong, Z.; Chen, M. The Internal Connection Analysis of Information Sharing and Investment Performance in the Venture Capital Network Community. Int. J. Environ. Res. Public Health 2021, 18, 11943. https://doi.org/10.3390/ijerph182211943

Feng B, Sun K, Zhong Z, Chen M. The Internal Connection Analysis of Information Sharing and Investment Performance in the Venture Capital Network Community. International Journal of Environmental Research and Public Health. 2021; 18(22):11943. https://doi.org/10.3390/ijerph182211943

Chicago/Turabian StyleFeng, Bing, Kaiyang Sun, Ziqi Zhong, and Min Chen. 2021. "The Internal Connection Analysis of Information Sharing and Investment Performance in the Venture Capital Network Community" International Journal of Environmental Research and Public Health 18, no. 22: 11943. https://doi.org/10.3390/ijerph182211943

APA StyleFeng, B., Sun, K., Zhong, Z., & Chen, M. (2021). The Internal Connection Analysis of Information Sharing and Investment Performance in the Venture Capital Network Community. International Journal of Environmental Research and Public Health, 18(22), 11943. https://doi.org/10.3390/ijerph182211943