The Impact of COVID-19 on the Insurance Industry

,

,  , ,

, ,  , and

, and

{kind=link}

{kind=link}

{kind=link}

Abstract

1. Introduction

- (i)

- to estimate the impact of COVID-19 on the insurance industry in Ghana.

- (ii)

- to discuss insurer expectations and present solutions.

2. Materials and Methods

2.1. Sources of Data

2.2. Data Collection

3. Results

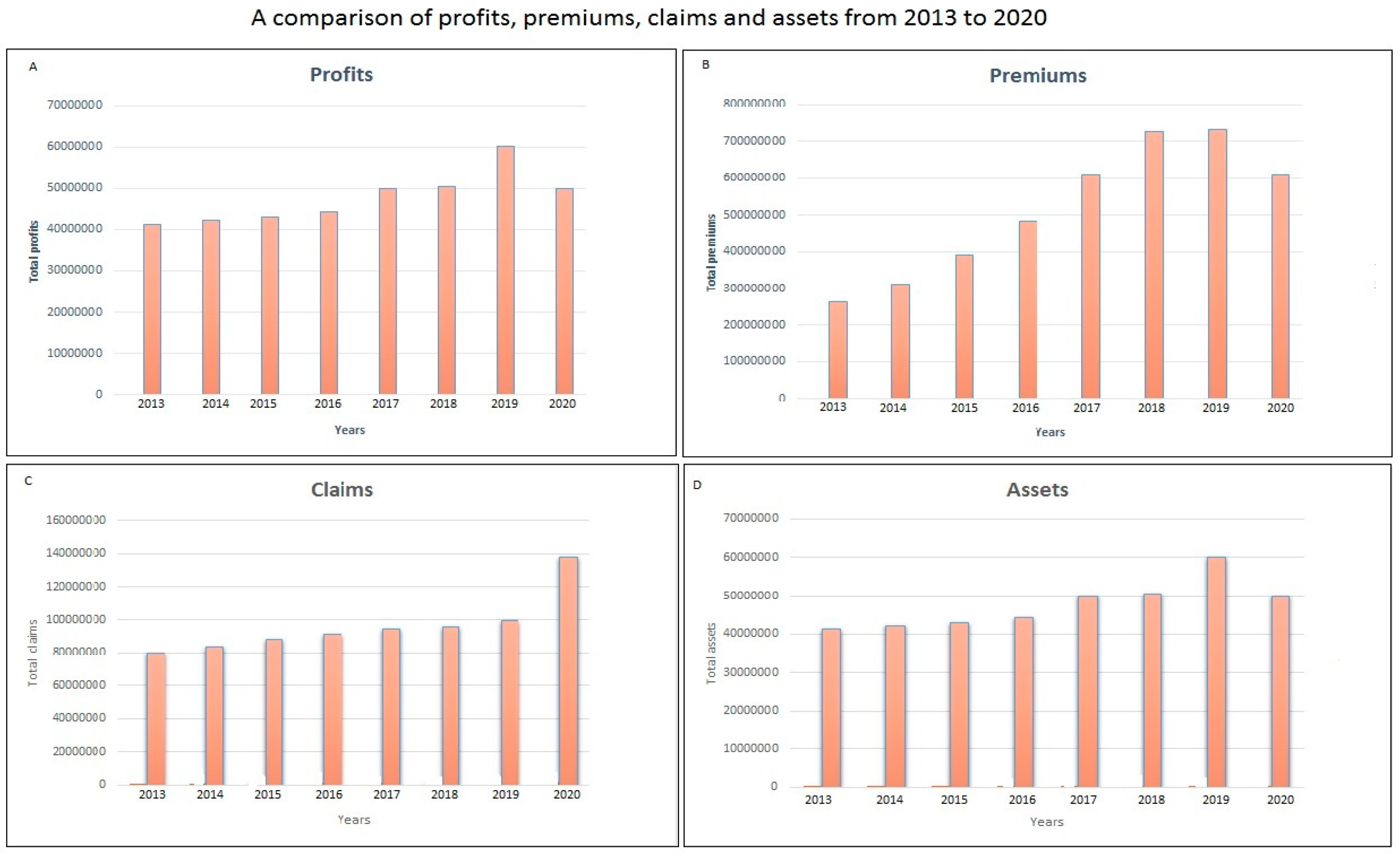

3.1. General Outlook of the Ghanaian Insurance Industry

3.2. Customer Complaints

3.3. Impact on Life and Non-Life Insurance Policies

3.4. The Impact on Health Insurance Policy: The Role of the Ghana National Health Insurance Scheme

3.5. Impact on Travel Insurance

3.6. Virtual Workforce

3.7. Level of Preparedness, Expectations and Hopes of Ghanaian Insurers

- In general, insurers were optimistic that their assets cover regulatory minimums sufficient to allow for a pandemic such as COVID-19, but 25% were doubtful whether if COVD-19 should persist beyond 12 months, they will survive insolvency.

- Most insurers have attempted to model the risk of the pandemic closely while others tried modeling their results under stress testing, but the majority have done nothing. This raises a big concern and needs to be considered by the National Health Insurance Commission. Elsewhere in the world, it is beneficial for National Health Insurance Authorities to implement readiness audits of all insurance companies to assess their finances and assets and model the impact future pandemic will have on them.

- All companies agreed that COVID-19 has had an operational economic impact on them, and they also agreed that they were not 100% prepared for the pandemic. They were however optimistic of surviving the pandemic and hopeful of a successful bounce back.

- Companies fear that existing products with guarantee rates are likely going to be unable to recoup losses as a result of COVID-19. They believe that even where rates are annually reviewable, it will probably not be feasible to recover those losses in future premiums.

- Regarding new products, little has been done to anticipate the impact COVID-19 will cause.

- All the insurers were of the view that annuity savings will protect some of their assets, but many insurance companies had little or no annuity businesses.

4. Discussion

4.1. The General Outlook

4.2. How Insurers Should Respond to the Crises

4.3. Managing and Quantifying Loss During a Pandemic

- By acting promptly: Early engagement with the client is very important to win the trust and understand the potential impacts of the pandemic.

- Understand the drivers of business specific to the insured’s business model. The insured must not be in say Accra, Kumasi or Tema (high COVID-19 case count cities in Ghana) to suffer a potential business interruption loss. Businesses operate within a long supply chain, and therefore, contingent business interruption tends to occur in the weaker part of the supply chain, which could originate from any part of the country and can lead to large losses in business.

- Keep an accurate trace of cause and effect. As losses accrue, the ability to keep an accurately documented trail to prove the direct causal link between the insured peril and financial losses is very critical.

- Keep track of worldwide activities and business trends: It is very prudent to consider the financial impact of the pandemic on other areas of the world.

- Seek early advice from professionals. Pandemics such as SARS and H1N1 have impacted insurance industries in other parts of the world, and insurance professionals have experience operating in pandemic situations. The early seeking of advice may save losses.

4.4. Other Solutions and Actions for Insurers

- Giving up-to-date and truthful information to parties: Most often, due to politics, governments and agencies try to hide the true scale of a pandemic by under-reporting on infection rates, case counts and deaths.

- Getting prepared ahead of time: There are more worries about the likelihood of a pandemic occurring today than there were 40 years ago. WHO and other partners have consistently warned the general public of the likely occurrence of a pandemic. This should, therefore, give insurers and hospitals enough reason to prepare adequately for a pandemic. The more time and resources spend preparing, the more effective a global response shall be. Vaccine development is a very important part of preparation. The government should maintain and support infectious disease control and prevention units such as the University of Ghana medical school, the Kwame Nkrumah University of Science and Technology School of Medical Sciences, the University for Development Studies School of Medical Sciences, the Noguchi Medical Research Institute, the Kumasi Centre for Collaborative Research In Tropical Medicine and some nursing training colleges such as the Jirapa Nursing and Midwifery Training College to be able to do research into virology and build the capacity of health workers. The aim is to promote research into developing vaccines that will be stocked in readiness for a pandemic. Antivirals should also be prepared in waiting for a pandemic situation.

4.5. Recovering from the Pandemic

4.6. What the World Bank Must Do to Help Client Countries

5. Conclusions

Supplementary Materials

Author Contributions

Funding

Acknowledgments

Conflicts of Interest

References

- WHO—World Health Organization. Coronavirus Disease (COVID-19) Dashboard. Available online: https://covid19.who.int/?gclid=EAIaIQobChMIm7_G7fWS6gIVlB-tBh0-jgCAEAAYASAAEgIiavD_BwE (accessed on 21 June 2020).

- NIC, Ghana-National Insurance Commission. Annual Reports and Financial Statements-2018. Available online: https://nicgh.org/wp-content/uploads/2019/02/2017_NIC_Annual-Report.pdf (accessed on 21 June 2020).

- Danquah, E.; Otto, D.M.; Nuakoh, A. Cost efficiency of insurance firms in Ghana. Manag. Decis. Econ. 2018, 39, 213–225. [Google Scholar] [CrossRef]

- Alhassan, A.L.; Biekpe, N. Efficiency, productivity and returns to scale economies in the non-life insurance market in South Africa. Geneva Pap. Risk Insur. Issues Pract. 2015, 40, 493–515. [Google Scholar] [CrossRef]

- Ansah-Adu, K.; Andoh, C.; Abor, J. Evaluating the cost efficiency of insurance companies in Ghana. J. Risk Financ. 2011, 13, 61–76. [Google Scholar] [CrossRef]

- Behravesh, C.B.; Brinson, D.; Hopkins, B.A.; Gomez, T.M. Backyard poultry flocks and salmonellosis: A recurring, yet preventable public health challenge. Clin. Infect. Dis. 2014, 58, 1432–1438. [Google Scholar] [CrossRef]

- Duncan-Jones, R.P. The impact of the Antonine plague. J. Rom. Archaeol. 1996, 9, 108–136. [Google Scholar] [CrossRef]

- DesOrmeaux, A.L. The Black Death and its Effect on Fourteenth- and Fifteenth-Century Art. Master’s Thesis, Louisiana State University, Baton Rouge, LA, USA, 2007. [Google Scholar]

- Aberth, J. The Black Death: The Great Mortality of 1348–1350. A Brief History with Documents, 1st ed.; Bedford/St. Martin’s: Boston, MA, USA; New York, NY, USA, 2005; pp. 25–101. [Google Scholar]

- Johnson, N.; Mueller, J. Updating the accounts: Global mortality of the 1918–1920 “Spanish” influenza pandemic. Bull. Hist. Med. 2002, 76, 105–115. [Google Scholar] [CrossRef]

- Reid, A.H.; Fanning, T.G.; Janczewski, T.A.; Lourens, R.M.; Taubenberger, J.K. Novel origin of the 1918 pandemic influenza virus nucleoprotein gene segment. J. Virol. 2004, 78. [Google Scholar] [CrossRef]

- Oxford, J.S.; Sefton, A.; Jackson, R.; Innes, W.; Daniels, R.S.; Johnson, N. World War I may have allowed the emergence of “Spanish” influenza. Lancet Infect. Dis. 2002, 2, 111–114. [Google Scholar] [CrossRef]

- Patterson, K.D.; Pyle, G.F. The geography and mortality of the 1918 influenza pandemic. Bull. Hist. Med. 1991, 65, 4–21. [Google Scholar]

- Basler, C.F.; Reid, A.H.; Dybing, J.K.; Janczewski, T.A.; Fanning, T.G.; Zheng, H. Sequence of the 1918 pandemic influenza virus nonstructural gene (NS) segment and characterization of recombinant viruses bearing the 1918 NS genes. Proc. Natl. Acad. Sci. USA 2001, 98, 2746–2751. [Google Scholar] [CrossRef]

- Chitnis, A.; Rawls, D.; Moore, J. Origin of HIV type 1 in colonial French Equatorial Africa? AIDS Res. Hum. Retrovir. 2000, 16, 5–8. [Google Scholar] [CrossRef] [PubMed]

- Delay, P. Gender and monitoring the response to HIV/AIDS pandemic. Emerg. Infect. Dis. 2004, 10, 256–286. [Google Scholar] [CrossRef]

- Barouch, D.H. Challenges in the development of an HIV-1 vaccine. Nature 2008, 455, 613–619. [Google Scholar] [CrossRef] [PubMed]

- Fu, W.; Sanders-Beer, B.E.; Katz, K.S.; Maglott, D.R.; Pruitt, K.D.; Ptak, R.G. Human immunodeficiency virus type 1, human protein interaction database at NCBI. Nucleic Acids Res. 2009, 37, D417–D422. [Google Scholar] [CrossRef]

- Gilbert, M.T.; Rambaut, A.; Wlasiuk, G.; Spira, T.J.; Pitchenik, A.E.; Worobey, M. The emergence of HIV/AIDS in the Americas and beyond. Proc. Natl. Acad. Sci. USA 2007, 104, 18566–18570. [Google Scholar] [CrossRef]

- Greene, W.C. A history of AIDS: Looking back to see ahead. Eur. J. Immunol. 2007, 37, S94–S102. [Google Scholar] [CrossRef] [PubMed]

- Chang, L.Y.; Shih, S.R.; Shao, P.L.; Huang, D.T.; Huang, L.M. Novel swine-origin influenza virus A (H1N1): The first pandemic of the 21st century. J. Formos. Med. Assoc. 2009, 108, 526–532. [Google Scholar] [CrossRef]

- Olsen, C.W. The emergence of novel swine influenza viruses in North America. Virus Res. 2002, 85, 199–210. [Google Scholar] [CrossRef]

- Myers, P.K.; Olsen, C.W.; Gray, C.G. Cases of swine influenza in humans: A review of the literature. Clin. Infect. Dis. 2007, 44, 1084–1088. [Google Scholar] [CrossRef]

- Newman, A.P.; Reisdorf, E.; Beinemann, J.; Uyeki, T.M.; Balish, A.; Shu, B.; Lindstrom, S.; Achenbach, J.; Smith, C.; Davis, J.P. Swine influenza A (H1N1) triple reassortant virus infection, Wisconsin. Emerg. Infect. Dis. 2008, 14, 1470–1472. [Google Scholar] [CrossRef]

- Sreta, D.; Kedkovid, R.; Tuamsang, S.; Kitikoon, P.; Thanawongnuwech, R. Pathogenesis of swine influenza virus (Thai isolates) in weanling pigs: An experimental trial. Virol. J. 2009, 6, 34–39. [Google Scholar] [CrossRef]

- LeDuc, J.W.; Barry, M.A. SARS, the first pandemic of the 21st century. Emerg. Infect. Dis. 2004, 10, 11–13. [Google Scholar] [CrossRef]

- Baas, T.; Taubenberger, J.K.; Chong, P.Y.; Chui, P.; Katze, M.G. SARS-CoV virus-host interactions and comparative etiologies of acute respiratory distress syndrome as determined by transcriptional and cytokine profiling of formalin-fixed paraffin-embedded tissues. J. Interf. Cytok. Res. 2006, 26, 309–317. [Google Scholar] [CrossRef] [PubMed]

- Baric, R.S.; Sheahan, T.; Deming, D.; Donaldson, E.; Yount, B.; Sims, B.A.C.; Roberts, R.S.; Frieman, M.; Rockx, B. SARS coronavirus vaccine development. Adv. Exp. Med. Biol. 2006, 581, 553–560. [Google Scholar] [PubMed]

- Troncoso, A. Ebola outbreak in West Africa: A neglected tropical disease. Asian Pac. J. Trop. Biomed. 2015, 5, 255–259. [Google Scholar] [CrossRef]

- Meltzer, M.I.; Atkins, C.Y.; Santibanez, S.; Knust, B.; Petersen, B.W.; Ervin, E.D.; Harmon, J.R.; Damon, I.K.; Washington, M.L. Estimating the future number of cases in the Ebola epidemic–Liberia and Sierra Leone, 2014–2015. MMWR Surveill. Summ. 2014, 63, 1–14. [Google Scholar]

- Gostin, L.O.; Lucey, D.; Phelan, A. The Ebola epidemic: A global health emergency. JAMA 2014, 312, 1095–1096. [Google Scholar] [CrossRef]

- Krech, R.; Kieny, M.P. The 2014 Ebola outbreak: Ethical use of unregistered interventions. Bull. World Health Organ. 2014, 92, 622–629. [Google Scholar] [CrossRef]

- Bowen, E.T.; Platt, G.S.; Lloyd, G.; Raymond, R.T.; Simpson, D.I. A comparative study of strains of Ebola virus isolated from southern Sudan and northern Zaire in 1976. J. Med. Virol. 1980, 6, 129–138. [Google Scholar] [CrossRef]

- Heymann, D.L.; Weisfeld, J.S.; Webb, P.A.; Johnson, K.M.; Cairns, T.; Berquist, H. Ebola hemorrhagic fever: Tandala, Zaire, 1977–1978. J. Infect. Dis. 1980, 142, 372–376. [Google Scholar] [CrossRef]

- Amblard, J.; Obiang, P.; Edzang, S.; Prehaud, C.; Bouloy, M.; Guenno, B.L. Identification of the Ebola virus in Gabon in 1994. Lancet 1997, 349, 181–182. [Google Scholar] [CrossRef]

- Lamunu, M.; Lutwama, J.J.; Kamugisha, J.; Opio, A.; Nambooze, J.; Okware, S. Containing a hemorrhagic fever epidemic: The Ebola experience in Uganda (October 2000–January 2001). Int. J. Infect. Dis. 2004, 8, 27–37. [Google Scholar] [CrossRef] [PubMed]

- Onyango, C.O.; Opoka, M.L.; Ksiazek, T.G.; Formenty, P.; Ahmed, A.; Tukei, P.M.; Sang, R.C.; Ofula, V.O.; Konongoi, S.L.; Coldren, R.L.; et al. Laboratory diagnosis of Ebola hemorrhagic fever during an outbreak in Yambio, Sudan, 2004. J. Infect. Dis. 2007, 196 (Suppl. 2), S193–S198. [Google Scholar] [CrossRef] [PubMed]

- Towner, J.S.; Sealy, T.K.; Khristova, M.L.; Albariño, C.G.; Conlan, S.; Reeder, S.A.; Quan, P.-L.; Lipkin, W.I.; Downing, R.; Tappero, J.W.; et al. Newly discovered ebola virus associated with hemorrhagic fever outbreak in Uganda. PLoS Pathog. 2008, 4, e1000212. [Google Scholar] [CrossRef]

- Leroy, E.M.; Epelboin, A.; Mondonge, V.; Pourrut, X.; Gonzalez, J.P.; Muyembe-Tamfum, J.-J.; Formenty, P. Human Ebola outbreak resulting from direct exposure to fruit bats in Luebo, Democratic Republic of Congo, 2007. Vector-Borne Zoonotic Dis. 2009, 9, 723–728. [Google Scholar] [CrossRef]

- Feldmann, H.; Geisbert, T.W. Ebola hemorrhagic fever. Lancet 2011, 377, 849–862. [Google Scholar] [CrossRef]

- Muyembe-Tamfum, J.J.; Mulangu, S.; Masumu, J.; Kayembe, J.M.; Kemp, A.; Paweska, J.T. Ebola virus outbreaks in Africa: Past and present. Onderstepoort J. Vet. Res. 2012, 79, 451. [Google Scholar] [CrossRef]

- Wamala, J.F.; Lukwago, L.; Malimbo, M.; Nguku, P.; Yoti, Z.; Musenero, M.; Amone, J.; Mbabazi, W.; Nanyunja, M.; Zaramba, S.; et al. Ebola haemorrhagic fever associated with novel virus strain, Uganda, 2007–2008. Emerg. Infect. Dis. 2010, 16, 108–117. [Google Scholar] [CrossRef]

- Peeri, N.C.; Shrestha, N.; Rahman, M.S.; Zaki, R.; Tan, Z.; Bibi, S.; Baghbanzadeh, M.; Aghamohammadi, N.; Zhang, W.; Haque, U. The SARS, MERS and novel coronavirus (COVID-19) epidemics, the newest and biggest global health threats: What lessons have we learned? Int. J. Epidemiol. 2020, 10, e0137964. [Google Scholar] [CrossRef]

- Dimitri, N. The economics of epidemic diseases. PLoS ONE 2015, 10, 9–14. [Google Scholar] [CrossRef][Green Version]

- Lagoarde-Segot, T.; Leoni, P.L. Pandemics of the poor and banking stability. J. Bank. Financ. 2013, 37, 4574–4583. [Google Scholar] [CrossRef]

- Fan, V.Y.; Jamison, D.T.; Summers, L.H. Pandemic risk: How large are the expected losses? Bull. World Health Organ. 2018, 96, 129–134. [Google Scholar] [CrossRef] [PubMed]

- Bongini, P.; Cucinelli, D.; Di Battista, M.L.; Nieri, L. Profitability shocks and recovery in time of crisis evidence from European banks. Financ. Res. Lett. 2019, 30, 233–239. [Google Scholar] [CrossRef]

- Sigala, M. Tourism and COVID-19: Impacts and implications for advancing and resetting industry and research. J. Bus. Res. 2020, 117, 312–321. [Google Scholar] [CrossRef] [PubMed]

- Barro, R.J.; Ursua, J.F.; Weng, J. The coronavirus and the great influenza pandemic: Lessons from the ‘Spanish Flu’ for the coronavirus’s potential effects on motality and economic activity. NBER 2020, 17, 26866. [Google Scholar]

- Cerra, V.; Saxena, S.C. Growth dynamics: The myth of economic recovery. Am. Econ. Rev. 2008, 98, 439–457. [Google Scholar] [CrossRef]

- Alfaro, L.; Chari, A.; Greenland, A.N.; Schott, P.K. Aggregate and firm level stock returns during pnademics in real time. NBER 2020, 12, 26950. [Google Scholar]

- Haacker, M. Financing HIV/AIDS programs in Sub-Saharan Africa. Health Aff. 2009, 28, 1606–1616. [Google Scholar] [CrossRef][Green Version]

- Bloom, D.E.; Cadarette, D.; Sevilla, J.P. Epidemics and economics: New and resurgent infectious diseases can have far-reaching economic repercussions. Financ. Dev. 2018, 55, 46–49. [Google Scholar]

- Dreyer, A.; Kritzinger, G.; Decker, J.D. Assessing the Impact of a Pandemic on the Life Insurance Industry in South Africa. In Proceedings of the 1st IAA Life Colloquium, Stockholm, Sweden, 10–13 June 2007. [Google Scholar]

© 2020 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).

Share and Cite

Babuna, P.; Yang, X.; Gyilbag, A.; Awudi, D.A.; Ngmenbelle, D.; Bian, D. The Impact of COVID-19 on the Insurance Industry. Int. J. Environ. Res. Public Health 2020, 17, 5766. https://doi.org/10.3390/ijerph17165766

Babuna P, Yang X, Gyilbag A, Awudi DA, Ngmenbelle D, Bian D. The Impact of COVID-19 on the Insurance Industry. International Journal of Environmental Research and Public Health. 2020; 17(16):5766. https://doi.org/10.3390/ijerph17165766

Chicago/Turabian StyleBabuna, Pius, Xiaohua Yang, Amatus Gyilbag, Doris Abra Awudi, David Ngmenbelle, and Dehui Bian. 2020. "The Impact of COVID-19 on the Insurance Industry" International Journal of Environmental Research and Public Health 17, no. 16: 5766. https://doi.org/10.3390/ijerph17165766

APA StyleBabuna, P., Yang, X., Gyilbag, A., Awudi, D. A., Ngmenbelle, D., & Bian, D. (2020). The Impact of COVID-19 on the Insurance Industry. International Journal of Environmental Research and Public Health, 17(16), 5766. https://doi.org/10.3390/ijerph17165766