The Impact of Health Insurance Programs on Out-of-Pocket Expenditures in Indonesia: An Increase or a Decrease?

Abstract

:1. Introduction

2. Health Insurance in Indonesia—Sources of Endogeneity

{kind=link}

{kind=link}

| Characteristics | Health Insurance Schemes | ||

|---|---|---|---|

| Askes | Jamsostek | Askeskin | |

| Established | 1968 | 1992 | 2005 |

| Population coverage | 14 million (about 6% of the population) in 2007 | 4.1 million (about 2% of the population) in 2009 | 76.4 million (about 34% of the population) in 2007 |

| Participation | Mandatory | Mandatory, opt-out option for employers that could provide better benefit plans | Social insurance |

| Organization/Carrier | State-owned company (PT ASKES Indonesia) | State-owned company (PT JAMSOSTEK Indonesia) | Ministry of Health |

| Beneficiaries | Civil servants, pensioners of civil servants and armed forces | Formal private employee | Identified poor and near poor, based on individual and household targeting |

| Eligible dependents | Spouse and 2 oldest children <21 years of age (if unemployed, unmarried), or <25 years of age if a full-time student | Spouse and 3 oldest children <21 years of age | Spouse and children |

| Source of funds | Member contribution 2% of basic salary + contribution from government 2% of basic salary | Member contribution, if single: 3% of basic salary; member with dependents: 6% of basic salary | No contribution from beneficiaries because it is tax-based with calculation for premium 6,000 IDR (0.46€) per capita |

| Benefits package and provider choice | Outpatient and inpatient care at public providers only | Outpatient care at both public and private providers networks, and for inpatient care at public providers only | Outpatient and inpatient care at public providers only |

| Negative list of benefits package | Cosmetic surgery, physical check-up, alternative medicine, dental prostheses, fertility treatment, non-basic immunization | General check-up, cancer treatment, heart surgery, renal dialysis, and lifelong treatment for congenital diseases, prostheses, non-basic immunization, transplantation, fertility treatment | Cosmetic surgery, physical check-ups, alternative medicine, dental prostheses, fertility treatment |

| Copayment | Yes, if members want to upgrade class, branded drugs out of formulary, renal dialysis, transplantation, heart surgery | None, but Jamsostek does not cover high cost treatments such as cancer treatment, heart surgery, and renal dialysis | None |

| Provider payment arrangement | Primary care: capitation Secondary care: fee schedule | Primary care: capitation Secondary care: capitation and fee schedule | Primary care: capitation Secondary care: negotiated fee with limit |

3. Methodology

3.1. Data

3.2. Outcome Variable

| Variable | 1993 | 1997 | 2000 | 2007 | ||||

|---|---|---|---|---|---|---|---|---|

| N = 7,194 | N = 6,667 | N = 6,703 | N = 6,335 | |||||

| Mean | Std. Dev. | Mean | Std. Dev. | Mean | Std. Dev. | Mean | Std. Dev. | |

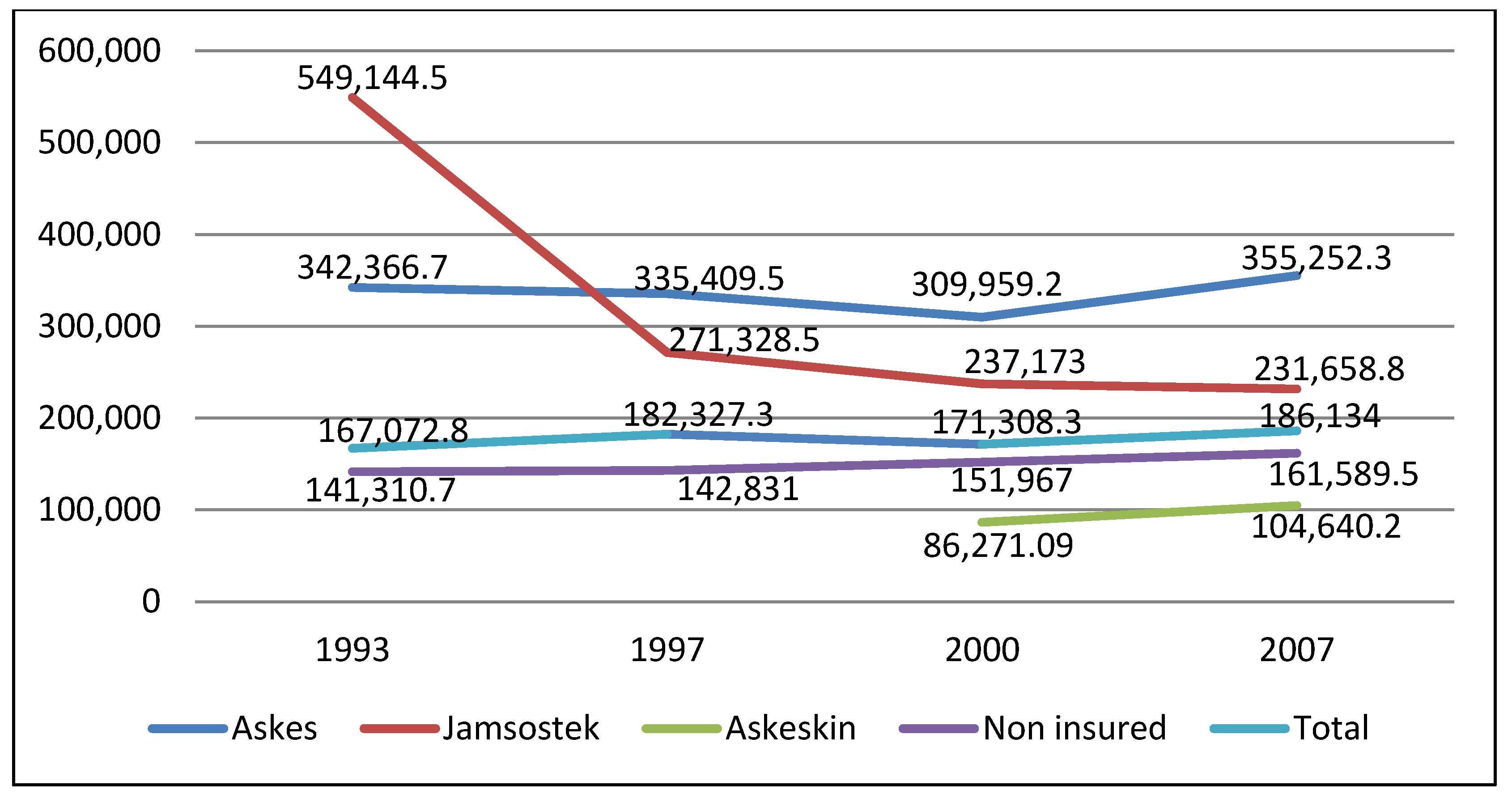

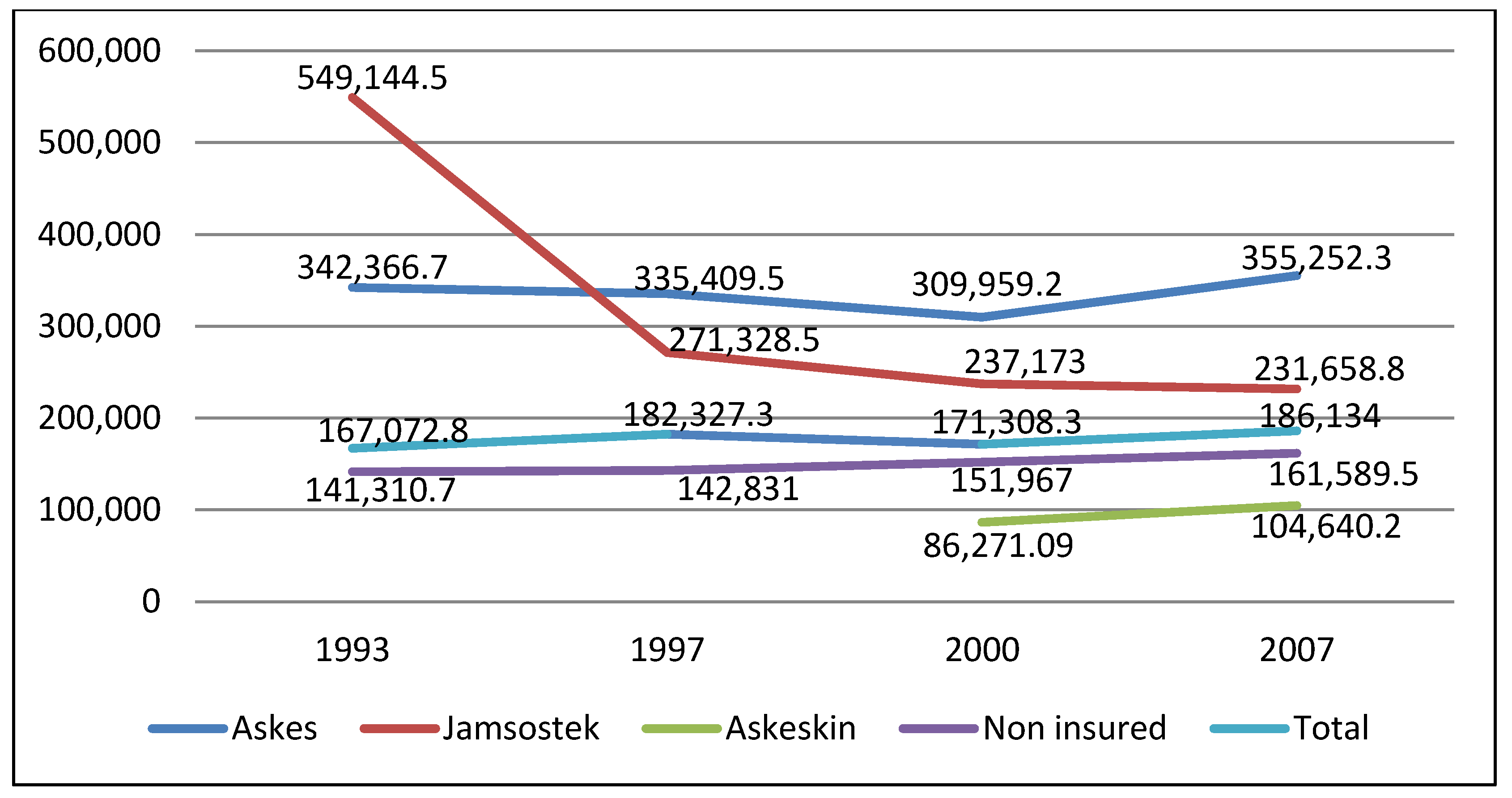

| Out-of-pocket expenditures (IDR) | 167,072.80 | 806,423.10 | 182,327.30 | 816,080.70 | 171,308.30 | 2,033,662.00 | 186,134.00 | 843,351.20 |

| Household income (IDR) | 5,310,577.00 | 5,310,577.00 | 6,999,397.00 | 1.22e+07 | 6,447,424.00 | 7,573,455.00 | 7,862,883.00 | 2.48e+07 |

| Health insurance | ||||||||

| Askes | 0.086 | 0.281 | 0.147 | 0.354 | 0.134 | 0.340 | 0.129 | 0.335 |

| Jamsostek | 0.010 | 0.097 | 0.070 | 0.255 | 0.067 | 0.251 | 0.074 | 0.262 |

| Askeskin | - | - | - | - | - | - | 0.179 | 0.383 |

| Male | 0.839 | 0.368 | 0.822 | 0.382 | 0.816 | 0.387 | 0.781 | 0.414 |

| Married | 0.368 | 0.377 | 0.815 | 0.389 | 0.805 | 0.396 | 0.765 | 0.424 |

| Education: | ||||||||

| Below junior high | 0.687 | 0.464 | 0.691 | 0.462 | 0.669 | 0.471 | 0.638 | 0.481 |

| Junior high | 0.118 | 0.322 | 0.114 | 0.318 | 0.124 | 0.329 | 0.124 | 0.328 |

| Senior high | 0.139 | 0.346 | 0.140 | 0.347 | 0.143 | 0.350 | 0.163 | 0.369 |

| University | 0.056 | 0.231 | 0.055 | 0.227 | 0.062 | 0.241 | 0.077 | 0.266 |

| Household size >4 | 0.471 | 0.499 | 0.594 | 0.491 | 0.674 | 0.469 | 0.756 | 0.429 |

| Age composition (years): | ||||||||

| 0–5 | 0.115 | 0.151 | 0.088 | 0.124 | 0.074 | 0.106 | 0.048 | 0.084 |

| 6–17 | 0.245 | 0.220 | 0.243 | 0.197 | 0.231 | 0.186 | 0.175 | 0.160 |

| 18–59 | 0.545 | 0.245 | 0.564 | 0.230 | 0.584 | 0.226 | 0.662 | 0.211 |

| 60 and above | 0.095 | 0.220 | 0.105 | 0.216 | 0.111 | 0.212 | 0.115 | 0.194 |

| Urban | 0.475 | 0.499 | 0.452 | 0.498 | 0.455 | 0.498 | 0.493 | 0.500 |

| Ethnicity (Javanese) | 0.587 | 0.492 | 0.589 | 0.492 | 0.590 | 0.492 | 0.585 | 0.493 |

| Health status | ||||||||

| GHS is “poor” | 0.200 | 0.400 | 0.270 | 0.444 | 0.325 | 0.468 | 0.356 | 0.479 |

| ADL with limitation | 0.297 | 0.457 | 0.535 | 0.499 | 0.627 | 0.484 | 0.595 | 0.491 |

3.3. Explanatory Variables

3.3.1. Income

3.3.2. Health Insurance

3.3.3. Health Status

3.3.4. Age Composition of Household

3.3.5. Other Variables

3.4. Econometric Model

4. Results

4.1. Descriptive Analysis

| Insurance status | 1993 | 1997 | 2000 | 2007 | ||||

|---|---|---|---|---|---|---|---|---|

| n | % | n | % | n | % | n | % | |

| Askes | 622 | 9.56 | 981 | 14.71 | 895 | 13.35 | 817 | 12.90 |

| Jamsostek | 69 | 0.96 | 467 | 7.00 | 451 | 6.73 | 470 | 7.42 |

| Askeskin | 0 | 0.00 | 0 | 0.00 | 0 | 0.00 | 1,133 | 17.88 |

| Uninsured | 6,503 | 90.39 | 5,219 | 78.28 | 5,357 | 79.92 | 3,915 | 61.80 |

| Total households | 7,194 | 100.00 | 6,667 | 100.00 | 6,703 | 100.00 | 6,335 | 100.00 |

4.2. Impact Estimation Results

| Variables | (1) Pooled OLS 1993–2007 | (2) Pooled OLS—comparison for (3) 1997–2007 | (3) Pooled 2SLS (IV) for Askes and Jamsostek 1997–2007 | (4) Pooled OLS—comparison for (5) 2000–2007 | (5) Pooled 2SLS (IV) for Askeskin 2000–2007 | (6) FE 1993–2007 |

|---|---|---|---|---|---|---|

| Health insurance | ||||||

| Askes | 0.015 (0.040) | −0.007 (0.045) | −0.802 (0.337) ** | - | - | 0.008 (0.068) |

| Jamsostek | 0.024 (0.051) | 0.011 (0.053) | −0.102 (0.261) | - | - | 0.017 (0.064) |

| Askeskin | −0.088 (0.055) | - | - | −0.022 (0.059) | −0.411 (0.238) * | −0.111 (0.064) * |

| Subsidized rice recipient | - | - | - | −0.146 (0.036) *** | −0.113 (0.041) *** | - |

| Male | −0.026 (0.049) | 0.015 (0.056) | 0.004 (0.057) | −0.021 (0.070) | −0.013 (0.070) | 0.002 (0.070) |

| Married | −0.049 (0.049) | −0.100 (0.056) * | −0.107 (0.057) * | −0.086 (0.070) | −0.095 (0.070) | 0.032 (0.068) |

| Education: Below junior high *) | ||||||

| Junior high | 0.167 (0.037) *** | 0.186 (0.042) *** | 0.264 (0.055) *** | 0.138 (0.051) *** | 0.132 (0.051) ** | −0.036 (0.062) |

| Senior high | 0.209 (0.037) *** | 0.237 (0.044) *** | 0.431 (0.097) *** | 0.171 (0.052) *** | 0.156 (0.053) *** | −0.069 (0.073) |

| University | 0.273 (0.056) *** | 0.273 (0.065) *** | 0.661 (0.176) *** | 0.196 (0.075) *** | 0.179 (0.076) ** | −0.201 (0.106) * |

| Household size | −0.073 (0.027) *** | −0.100 (0.032) *** | −0.058 (0.040) | −0.084 (0.041) ** | −0.086 (0.041) ** | −0.056 (0.046) |

| Age composition (years): 18–59 *) | ||||||

| 0–5 | 0.699 (0.096) *** | 0.757 (0.124) *** | 0.648 (0.134) *** | 0.864 (0.168) *** | 0.890 (0.169) *** | 0.975 (0.140) *** |

| 6–17 | −0.384 (0.067) *** | −0.395 (0.081) *** | −0.450 (0.088) *** | −0.453 (0.102) *** | −0.438 (0.102) *** | −0.124 (0.091) |

| 60 and above | 0.445 (0.068) *** | 0.427 (0.081) *** | 0.473 (0.085) *** | 0.459 (0.101) *** | 0.455 (0.101) *** | 0.413 (0.112) *** |

| Urban | 0.071 (0.025) *** | 0.055 (0.029) * | 0.078 (0.034) ** | 0.043 (0.035) | 0.052 (0.036) | 0.013 (0.068) |

| Ethnicity | 0.193 (0.024) *** | 0.246 (0.028) *** | 0.255 (0.031) *** | 0.210 (0.036) *** | 0.203 (0.036) *** | - |

| Health status | ||||||

| GHS is poor | 0.365 (0.025) *** | 0.350 (0.028) *** | 0.355 (0.028) *** | 0.342 (0.034) *** | 0.346 (0.034) *** | 0.292 (0.029) *** |

| ADL with limitation | 0.177 (0.024) *** | 0.159 (0.027) *** | 0.182 (0.029) *** | 0.145 (0.033) *** | 0.146 (0.033) *** | 0.160 (0.028) *** |

| Household income: Lowest *) | ||||||

| Lower 20% | 0.582 (0.033) *** | 0.517 (0.039) *** | 0.538 (0.040) *** | 0.471 (0.048) *** | 0.469 (0.048) *** | 0.416 (0.042) *** |

| Middle 20% | 1.009 (0.035) *** | 0.936 (0.040) *** | 0.967 (0.044) *** | 0.861 (0.048) *** | 0.856 (0.048) *** | 0.759 (0.045) *** |

| Higher 20% | 1.531 (0.036) *** | 1.448 (0.042) *** | 1.511 (0.053) *** | 1.370 (0.051) *** | 1.356 (0.052) *** | 1.206 (0.049) *** |

| Highest 20% | 2.231 (0.041) *** | 2.119 (0.048) *** | 2.230 (0.073) *** | 1.981 (0.059) *** | 1.964 (0.060) *** | 1.698 (0.057) *** |

| Year: 1993 *) | ||||||

| 1997 | 0.024 (0.029) | - | - | - | 0.026 (0.031) | |

| 2000 | −0.182 (0.029) *** | −0.204 (0.029) *** | −0.222 (0.030) *** | - | −0.146 (0.034) *** | |

| 2007 | −0.131 (0.034) *** | −0.177 (0.032) *** | −0.203 (0.035) *** | 0.070 (0.035) ** | 0.135 (0.053) ** | −0.001 (0.042) |

| Constant | 9.282 (0.050) *** | 9.388 (0.058) *** | 9.380 (0.059) *** | 9.356 (0.072) *** | 9.350 (0.072) *** | 9.595 (0.072) *** |

| F-statistic (p-value) | 237.35 ( .00) | 179.64 ( .00) | 172.48 ( .00) | 116.81 ( .00) | 116.51 ( .00) | 57.85 ( .00) |

| R2 | 0.248 | 0.233 | - | 0.219 | - | 0.095 |

| No. of observation | 20,168 | 14,475 | 14,474 | 9,140 | 9,140 | 20,168 |

| No. of clusters | 6,969 | 6,390 | 6,390 | 5,883 | 5,883 | 6,969 |

| Test | Askes and Jamsostek | Askeskin | ||

|---|---|---|---|---|

| Statistics | p-value | Statistics | p-value | |

| Durbin-Wu-Hausman chi-square test | χ2 = 6.684 | 0.035 | χ2 = 2.859 | 0.091 |

| Wu-Hausman F test | F (2,14450) = 3.337 | 0.037 | F (1,9118) = 2.859 | 0.091 |

| Test | Askes | Jamsostek | Askeskin |

|---|---|---|---|

| R2 | 0.239 | 0.100 | 0.192 |

| Adjusted R2 | 0.238 | 0.099 | 0.191 |

| Partial R2 | 0.019 | 0.045 | 0.059 |

| F-test | F (3,14451) = 69.775 *** | F (3,14451) = 77.467 *** | F (1,9119) = 227.177 *** |

| Shea’s partial R2 | 0.016 | 0.038 | 0.059 |

| Shea’s Adjusted partial R2 | 0.015 | 0.037 | 0.057 |

5. Discussion

6. Conclusions

Acknowledgments

Conflict of Interest

References

- Yip, W.; Berman, P. Targeted health insurance in a low income country and its impact on access and equity in access: Egypt’s school health insurance. Health Econ. 2001, 10, 207–220. [Google Scholar] [CrossRef]

- Devadasan, N.; Criel, B.; Van Damme, W.; Manoharan, S.; Sarma, P.S.; Van der Stuyft, P. Community health insurance in Gudalur, India, increases access to hospital care. Health Policy Plann. 2010, 25, 145–154. [Google Scholar] [CrossRef]

- Axelson, H.; Bales, S.; Minh, P.D.; Ekman, B.; Gerdtham, U.G. Health financing for the poor produces promising short-term effects on utilization and out-of-pocket expenditure: Evidence from Vietnam. Int J. Equity Health 2009, 8, 20. [Google Scholar] [CrossRef]

- Noirhomme, M.; Meessen, B.; Griffiths, F.; Ir, P.; Jacobs, B.; Thor, R.; Criel, B.; Van Damme, W. Improving access to hospital care for the poor: Comparative analysis of four health equity funds in Cambodia. Health Policy Plann. 2007, 22, 246–262. [Google Scholar] [CrossRef]

- Wagstaff, A.; Lindelow, M. Can insurance increase financial risk? The curious case of health insurance in China. J. Health Econ. 2008, 27, 990–1005. [Google Scholar] [CrossRef]

- Ghosh, S. Catastrophic Payments and Impoverishment due to Out-of-Pocket Health Spending: The Effects of Recent Health Sector Reforms in India. In Working Paper Series on Health and Demographic Change in the Asia-Pacific; Stanford University, Walter H. Shorenstein Asia-Pacific Research Center, Asia Health Policy Program: Stanford ,CA, USA, 2010. [Google Scholar]

- Ekman, B.; Liem, N.T.; Duc, H.A.; Axelson, H. Health insurance reform in Vietnam: A review of recent developments and future challenges. Health Policy Plann. 2008, 23, 252–263. [Google Scholar] [CrossRef]

- Wagstaff, A. Estimating health insurance impacts under unobserved heterogeneity: The case of Vietnam’s health care fund for the poor. Health Econ. 2010, 19, 189–208. [Google Scholar] [CrossRef]

- The World Health Report 2000—Health Systems: Improving Performance; World Health Organization: Geneva, Switzerland, 2002.

- Hidayat, B.; Thabrany, H.; Dong, H.; Sauerborn, R. The effects of mandatory health insurance on equity in access to outpatient care in Indonesia. Health Policy Plann. 2004, 19, 322–335. [Google Scholar] [CrossRef]

- Bachtiar, A.; Wibisana, W.; Pujiyanto. Laporan Akhir Hasil Asesmen Cepat Program PKPS-BBM 2005 Bidang Kesehatan; PUSKA-FKM University of Indonesia: Jakarta, Indonesia, 2006. [Google Scholar]

- Zweifel, P.; Manning, W.G. Moral Hazard and Consumer. Incentives in Health Care. In Handbook of Health Economics; Culyer, A.J., Newhouse, J.P., Eds.; Elsevier: Amsterdam, The Nertherlands, 2000; Volume 1A, pp. 409–459. [Google Scholar]

- Cutler, D.M.; Zeckhauser, R.J. The Anatomy of Health Insurance. In Handbook of Health Economics; Culyer, A.J., Newhouse, J.P., Eds.; Elsevier: Amsterdam, The Nertherlands, 2000; Volume 1A. [Google Scholar]

- McGuire, T.G. Physician Agency. In Handbook of Health Economics; Culyer, A.J., Newhouse, J.P., Eds.; Elsevier: Amsterdam, The Nertherlands, 2000; Volume 1A. [Google Scholar]

- Nguyen, C.V. The Impact of voluntary health insurance on health care utilization and out-of-pocket payments: New evidence for Vietnam. Health Econ. 2012, 21, 946–966. [Google Scholar] [CrossRef]

- Galarraga, O.; Sosa-Rubi, S.G.; Salinas-Rodriguez, A.; Sesma-Vazquez, S. Health insurance for the poor: Impact on catastrophic and out-of-pocket health expenditures in Mexico. Eur. J. Health Econ. 2010, 11, 437–447. [Google Scholar] [CrossRef]

- Luke Shaefer, H.; Grogan, C.M.; Pollack, H.A. Transitions from private to public health coverage among children: Estimating effects on out-of-pocket medical costs and health insurance premium costs. Health Serv. Res. 2011, 46, 840–858. [Google Scholar] [CrossRef]

- Sepehri, A.; Sarma, S.; Simpson, W. Does non-profit health insurance reduce financial burden? Evidence from the Vietnam living standards survey panel. Health Econ. 2006, 15, 603–616. [Google Scholar] [CrossRef]

- Statistical Yearbook of Indonesia 2012; BPS-Statistics Indonesia: Jakarta, Indonesia, 2012.

- World Bank, Investing in Indonesia’s Health: Challenges and Opportunities for Future Public Spending; The World Bank Office Jakarta: Jakarta, Indonesia, 2008.

- Rokx, C.; Schieber, G.; Harimurti, P.; Tandon, A.; Somanathan, A. Health Financing in Indonesia: A Reform Road Map; The World Bank: Washington DC, USA, 2009. [Google Scholar]

- Bender, K.; GTZ Office Jakarta. Options for Social Protection Reform in Indonesia; GTZ Office Jakarta: Jakarta, Indonesia, 2008. [Google Scholar]

- ILO, Social Security in Indonesia: Advancing the Development Agenda; International Labour Organization: Jakarta, Indonesia, 2008.

- Sparrow, R.; Suryahadi, A.; Widyanti, W. Social Health Insurance for the Poor: Targeting and Impact of Indonesia’s Askeskin Program; The SMERU Research Institute: Jakarta, Indonesia, 2010. [Google Scholar]

- Hidayat, B.; Pokhrel, S. The selection of an appropriate count data model for modelling health insurance and health care demand: case of Indonesia. Int J. Environ. Res. Public Health 2010, 7, 9–27. [Google Scholar] [CrossRef]

- Thabrany, H. Social Security for All: A continuous Challenge for Workers in Indonesia. Available online: Available online: library.fes.de/pdf-files/iez/08152.pdf (accessed on 23 October 2011).

- ADB, Preparatory Studies on National Social Security System in Indonesia; Asian Development Bank: Manila, Philippines, 2007.

- WHO, Social Health Insurance: Selected Country Case Studies from Asia and the Pacific; World Health Organization—South-East Asia Region: New Delhi, India, 2005.

- Frankenberg, E.; Thomas, D. The Indonesia Family Life Survey (IFLS): Study Design and Results from Waves 1 and 2; RAND Labor and Population Program: Santa Monica, CA, USA, 2000. [Google Scholar]

- Strauss, J.; Beegle, K.; Sikoki, B.; Dwiyanto, A.; Herawati, Y.; Witoelar, F. The Third Wave of the Indonesia Family Life Survey: Overview and Field Report; RAND Labor and Population: Santa Monica, CA, USA, 2004. [Google Scholar]

- Strauss, J.; Witoelar, F.; Sikoki, B.; Wattie, A.M. The Fourth Wave of the Indonesia Family Life Survey: Overview and Field Report; RAND Labor and Population: Santa Monica, CA, USA, 2009. [Google Scholar]

- Statistics Canada, Your Guide to the Consumer Price Index; Minister of Industry Canada: Ottawa, Canada, 1996.

- O’Donnell, O.; Doorslaer, E.V.; Wagstaff, A.; Lindelow, M. Analyzing Health Equity Using Household Survey Data: A Guide to Techniques and Their Implementation; The World Bank: Washington, DC, USA, 2008. [Google Scholar]

- Ha, N.T.; Berman, P.; Larsen, U. Household utilization and expenditure on private and public health services in Vietnam. Health Policy Plann. 2002, 17, 61–70. [Google Scholar] [CrossRef]

- Gotsadze, G. Health care—Seeking behaviour and out-of-pocket payments in Tbilisi, Georgia. Health Policy Plann. 2005, 20, 232–242. [Google Scholar] [CrossRef]

- Cameron, A.C.; Trivedi, P.K. Microeconometrics Using Stata; Stata Press: Texas, TX, USA, 2009. [Google Scholar]

- Stock, J.H.; Yogo, M. Testing for Weak Instruments in Linear IV Regression. In Technical Working Paper 284; National Bureau of Economic Research: Cambridge, MA, USA, 2002. [Google Scholar]

- Baum, C.F.; Schaffer, M.E. Instrumental variables and GMM: Estimation and testing. Stata J. 2003, 3, 1–31. [Google Scholar]

- World Bank, Jamkesmas Health Service Fee Waiver: Social Assistance Program and Public Expenditures Review 4; Jakarta Office: Jakarta, Indonesia, 2012.

- Chu, T.B.; Liu, T.C.; Chen, C.S.; Tsai, Y.W.; Chiu, W.T. Household out-of-pocket medical expenditures and National Health Insurance in Taiwan: Income and regional inequality. BMC Health Serv. Res. 2005, 5, 60. [Google Scholar] [CrossRef]

- Limwattananon, S.; Tangcharoensathien, V.; Prakongsai, P. Equity in Financing Healthcare: Impact of Universal Access to Healthcare in Thailand. In Working Paper 16; EQUITAP: Phnom Pehn, Cambodia, 2005. [Google Scholar]

- Abel-Smith, B.; Rawal, P. Can the poor afford “free” health services? A case study of Tanzania. Health Policy Plann. 1992, 7, 329–341. [Google Scholar] [CrossRef]

- Shamsun, N.; Costello, A. The hidden cost of “free” maternity care in Dhaka, Bangladesh. Health Policy Plann. 1998, 13, 417–422. [Google Scholar] [CrossRef]

© 2013 by the authors; licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution license (http://creativecommons.org/licenses/by/3.0/).

Share and Cite

Aji, B.; De Allegri, M.; Souares, A.; Sauerborn, R. The Impact of Health Insurance Programs on Out-of-Pocket Expenditures in Indonesia: An Increase or a Decrease? Int. J. Environ. Res. Public Health 2013, 10, 2995-3013. https://doi.org/10.3390/ijerph10072995

Aji B, De Allegri M, Souares A, Sauerborn R. The Impact of Health Insurance Programs on Out-of-Pocket Expenditures in Indonesia: An Increase or a Decrease? International Journal of Environmental Research and Public Health. 2013; 10(7):2995-3013. https://doi.org/10.3390/ijerph10072995

Chicago/Turabian StyleAji, Budi, Manuela De Allegri, Aurelia Souares, and Rainer Sauerborn. 2013. "The Impact of Health Insurance Programs on Out-of-Pocket Expenditures in Indonesia: An Increase or a Decrease?" International Journal of Environmental Research and Public Health 10, no. 7: 2995-3013. https://doi.org/10.3390/ijerph10072995

APA StyleAji, B., De Allegri, M., Souares, A., & Sauerborn, R. (2013). The Impact of Health Insurance Programs on Out-of-Pocket Expenditures in Indonesia: An Increase or a Decrease? International Journal of Environmental Research and Public Health, 10(7), 2995-3013. https://doi.org/10.3390/ijerph10072995