Mobile Payment Innovation Ecosystem and Mechanism: A Case Study of Taiwan’s Servicescapes

Abstract

1. Introduction

- (1)

- What are the dynamic capabilities required for a focal firm to drive innovation ecosystems?

- (2)

- Why did the focal firm establish an overall operation mechanism in the innovation ecosystem?

- (3)

- How can participants in mobile payments participate and collaborate in an innovation ecosystem for mobile payments?

2. Literature Review

2.1. Innovation Ecosystem

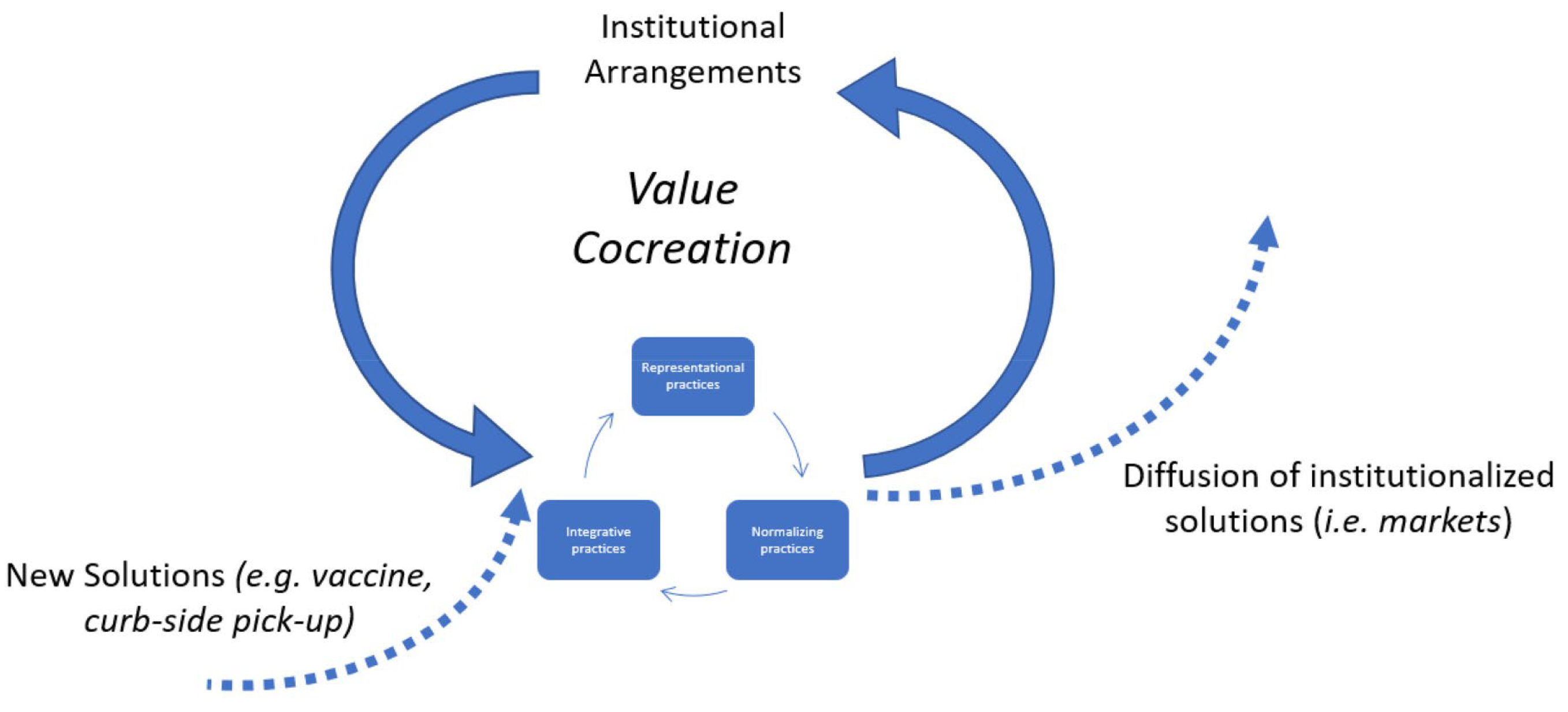

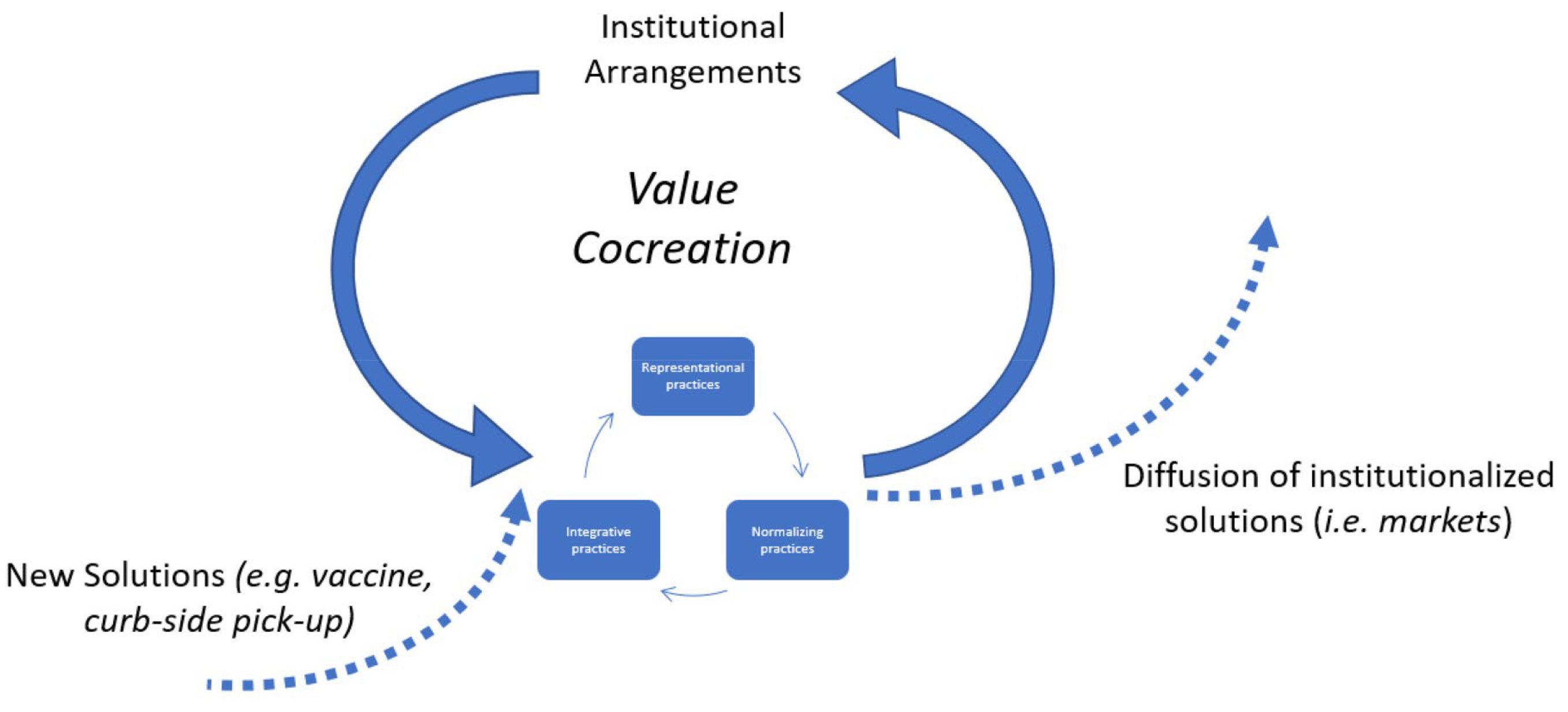

2.2. Value Co-Creation

2.3. Dynamic Capabilities

3. Methodology

3.1. Case Studies

3.2. Case Selection

3.3. Data Collection and Analysis

4. Case Briefing

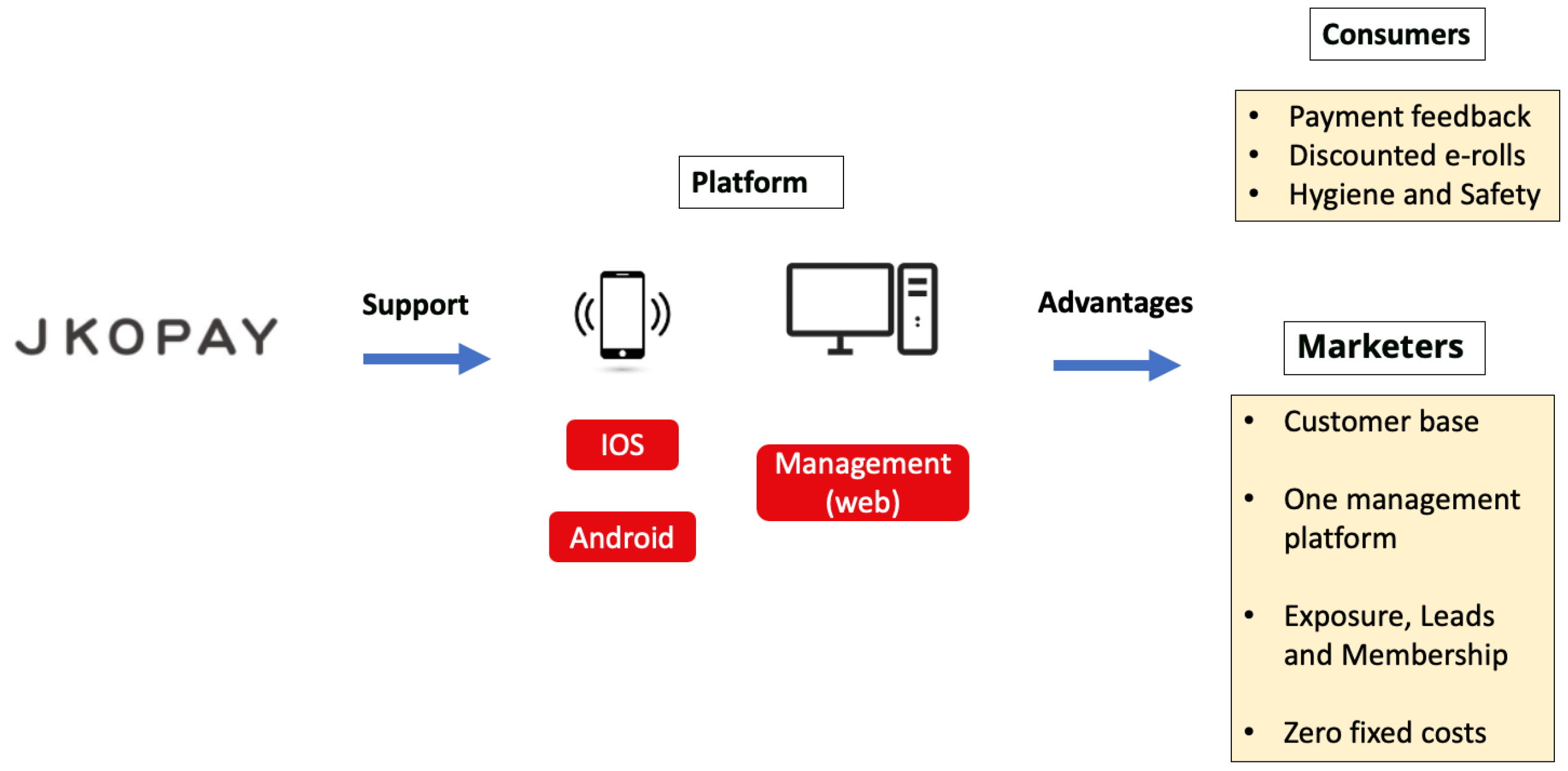

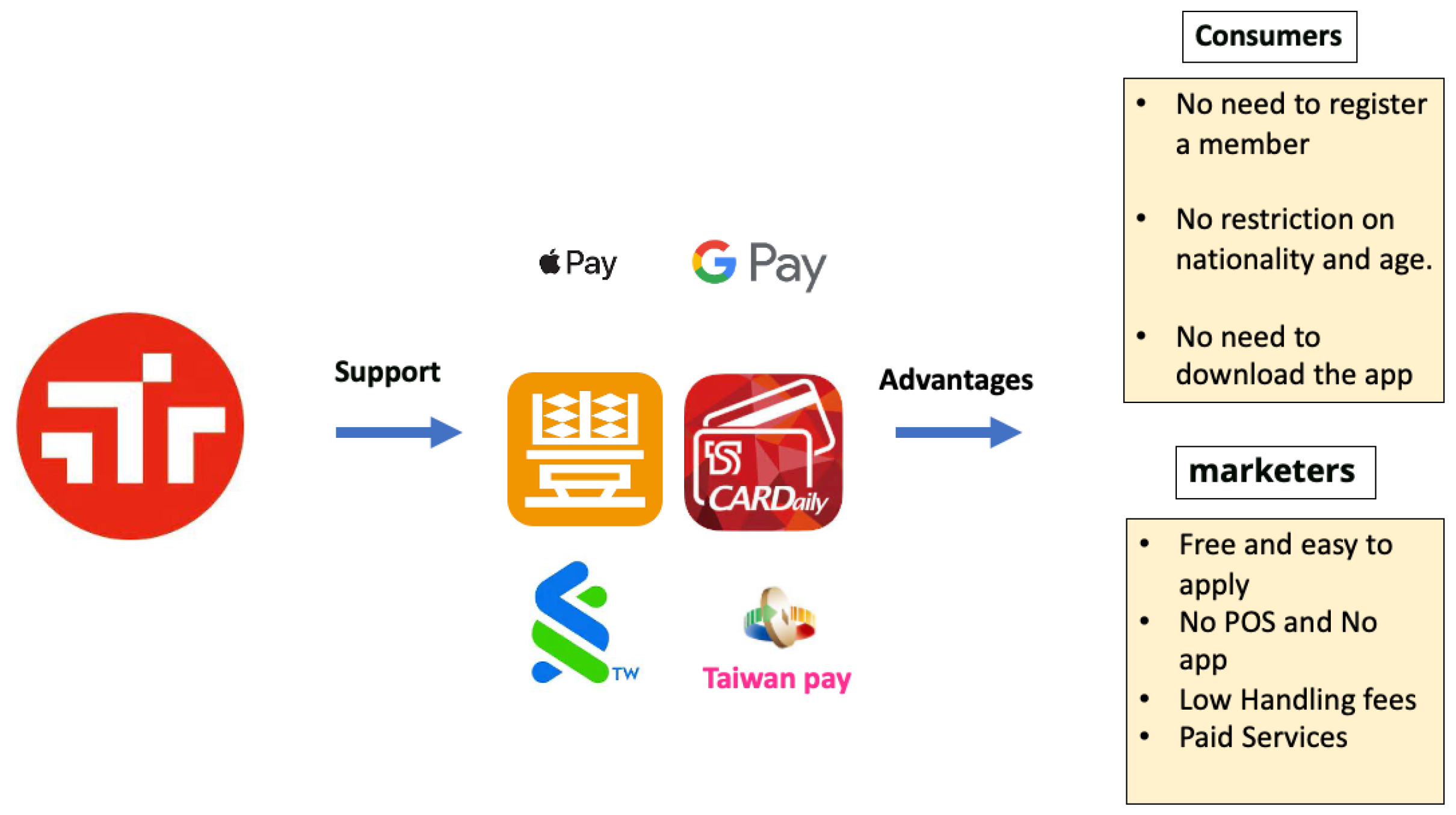

4.1. Servicescape A

4.2. Servicescape B

4.3. Servicescape C

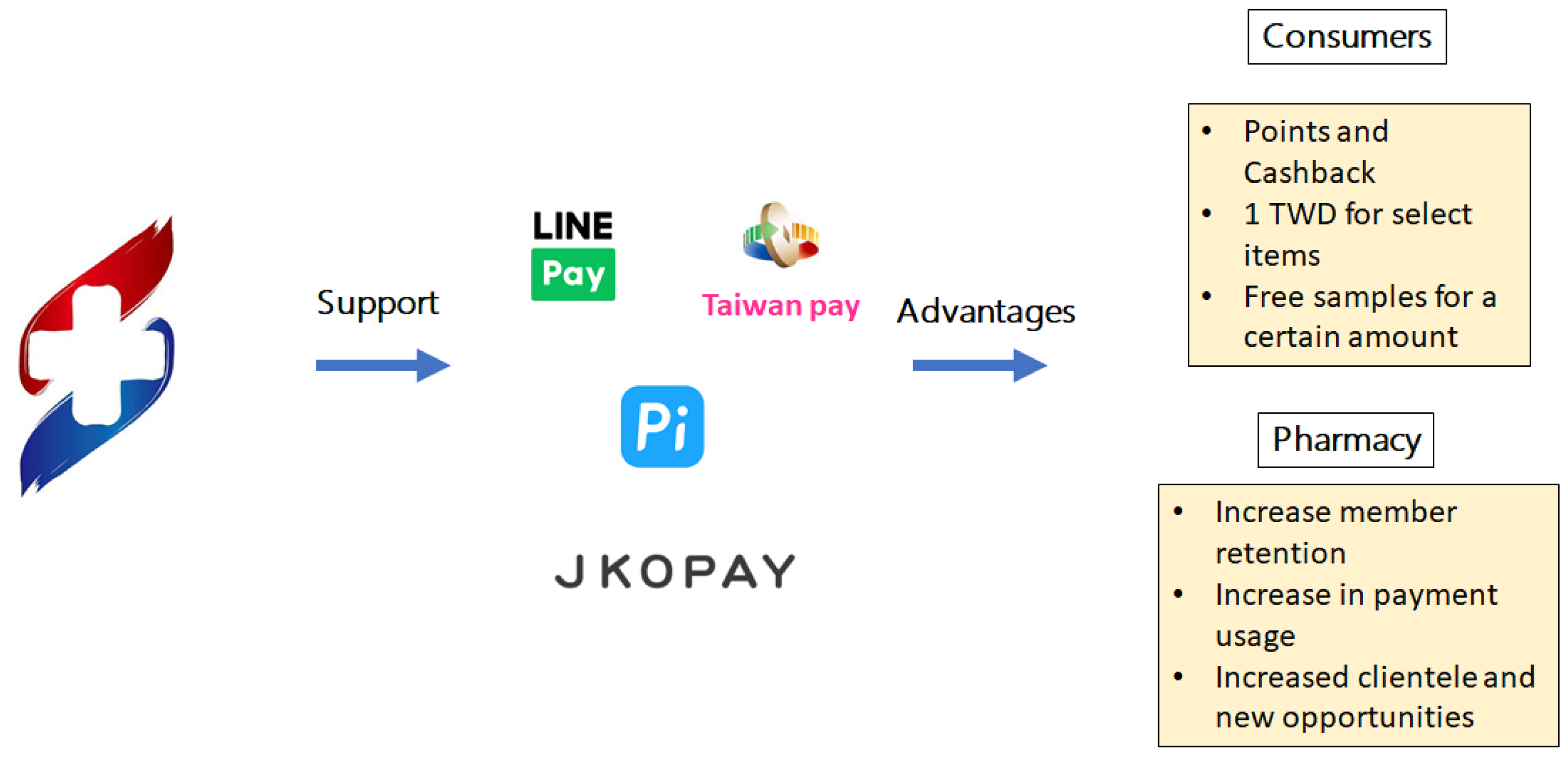

4.4. Servicescape D

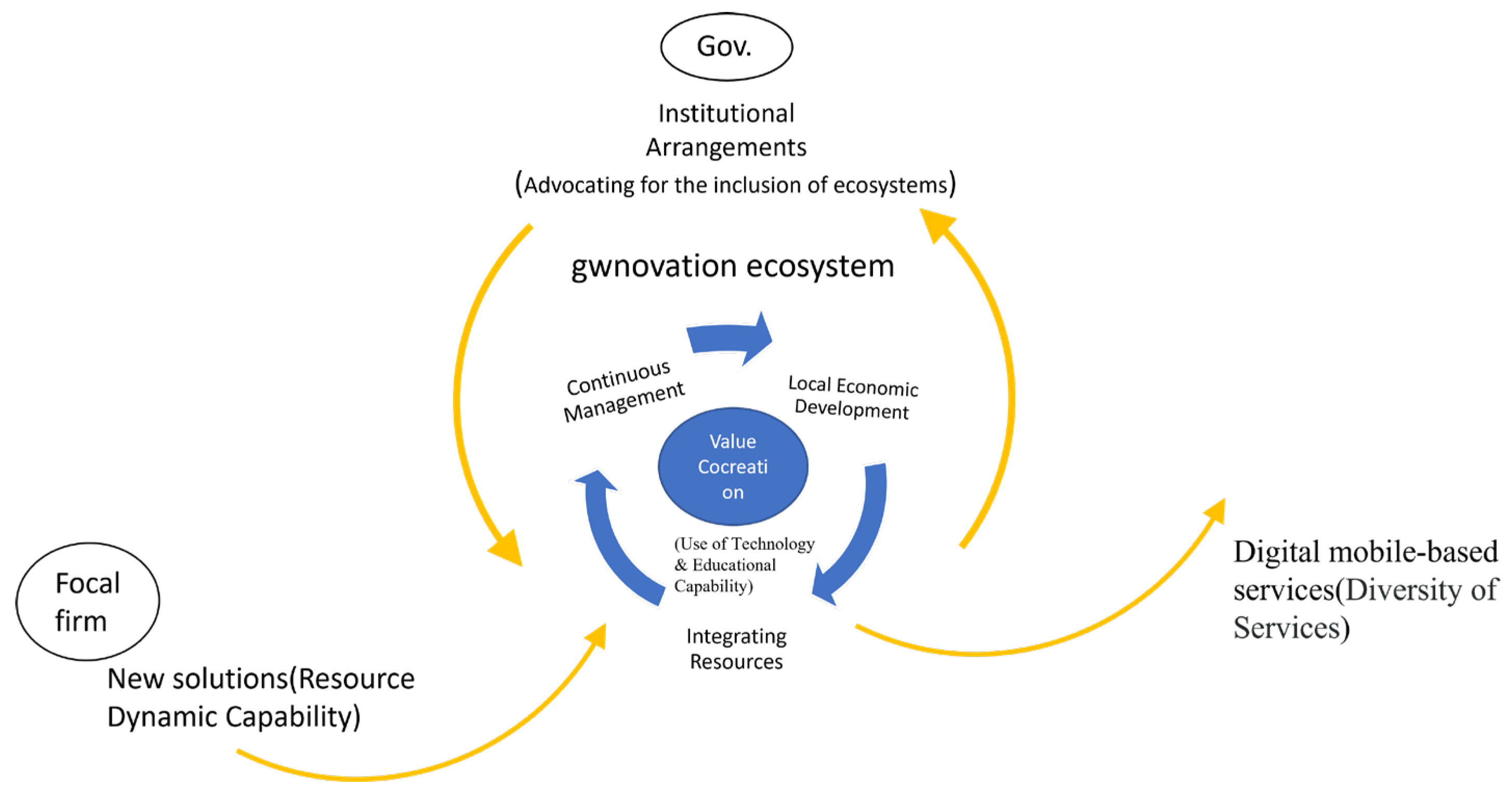

5. Findings

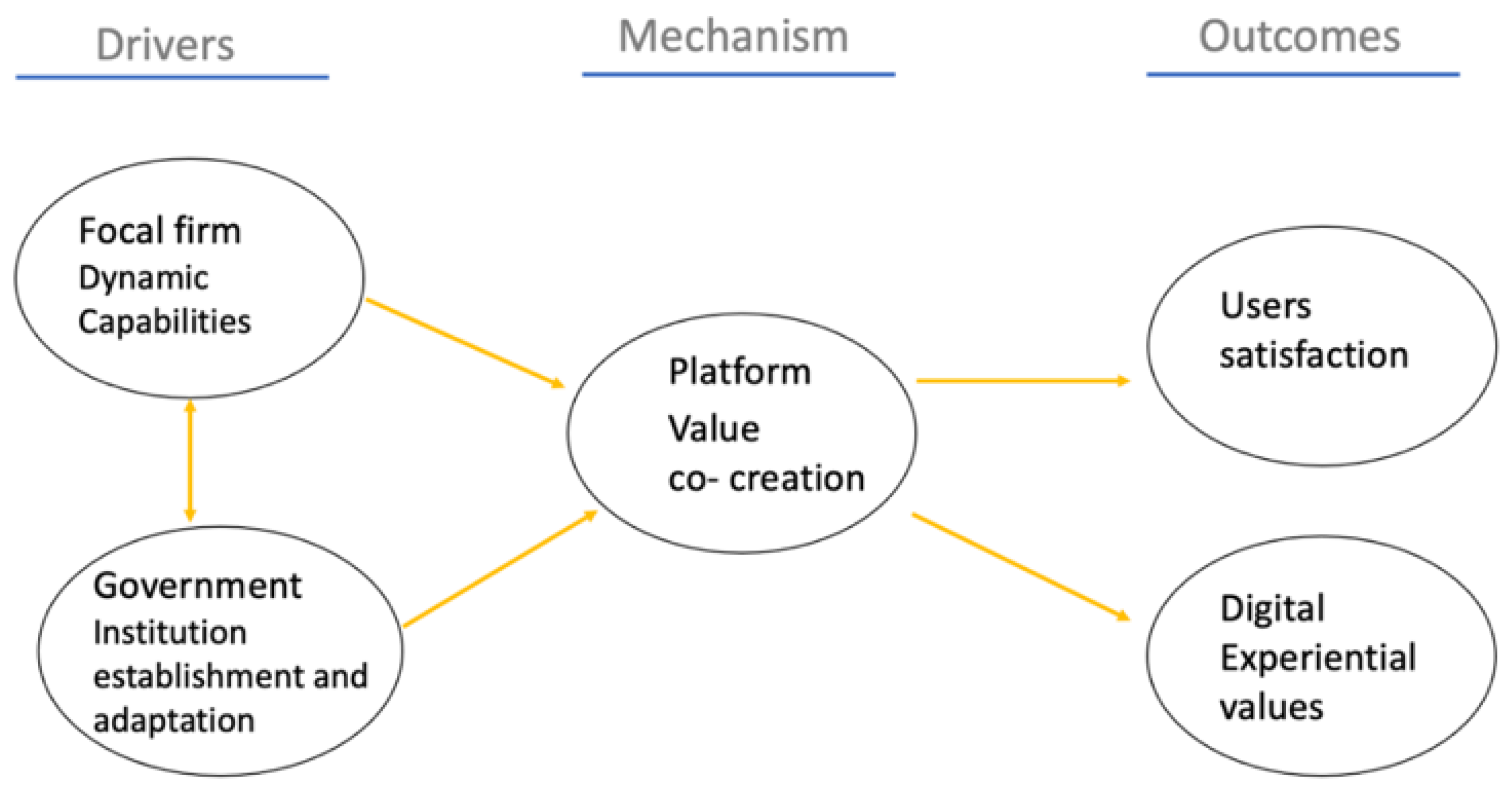

5.1. Dynamic Capabilities of Focal Firms

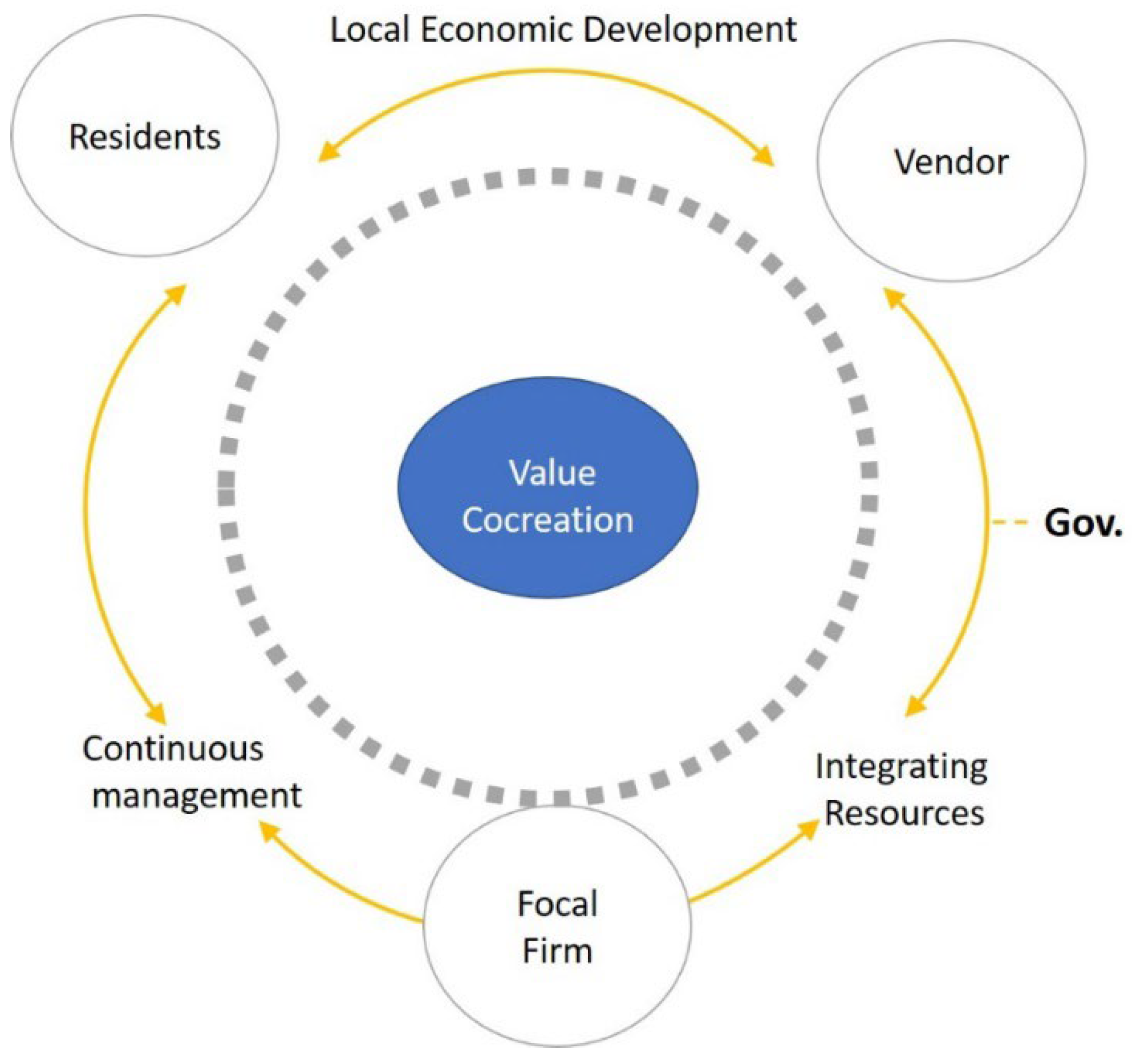

5.2. Holistic Mechanisms for Innovation Ecosystems

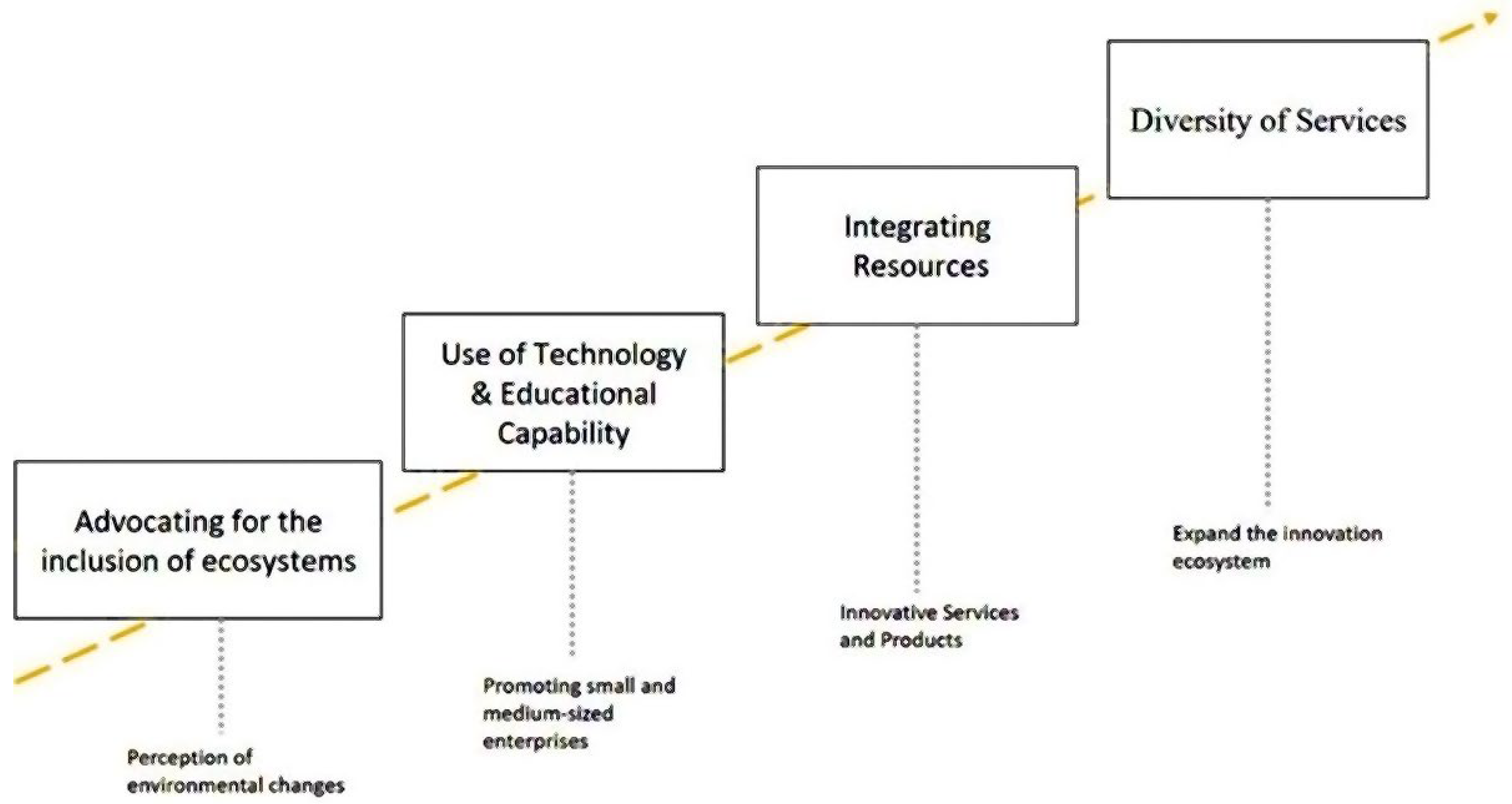

5.3. Government Involvement Helps to Achieve Urban Development Goals

6. Discussion

6.1. Focal Vendors Should Integrate Resources Effectively

6.2. Follow-Up on Management Needs to Be Supported by Technology and Digital Platform Services

6.3. Collaboration between Focal Firms and the Government Promotes Local Economic Development Effectively

7. Conclusions

7.1. Conclusions

7.2. Theoretical Contribution

7.3. Practical Implications

7.4. Research Limitations

Author Contributions

Funding

Institutional Review Board Statement

Informed Consent Statement

Data Availability Statement

Conflicts of Interest

Appendix A

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| 1. What are the specifics of the mobile payment import implementation? |

| 2. What are the business performances of corporations, the numbers of customers, and the use of multi-payment after and before the adoption of mobile payment? |

| 3. What are the products of the partner companies? |

| 4. How are consumer test scores collected? What plan was carried out? |

| 5. How are the Member Information data used after they have been collected? |

| 6. What are your thoughts on the importance of user experience in the mobile payment process? What steps have you taken to improve the user experience? |

| 1. How to extend the effect of value-added services in the future? |

| 2. How to enlist the participation of vendors around the market? |

| 3. How will the results of the marketing event be sustained in the future? |

| 4. What are the plans for co-operation with local governments? |

| 5. What are the plans for the arrival of overseas tourists after the outbreak is lifted? |

| 6. Does your mobile payment mechanism support multiple payment methods? If so, how do you achieve this diversity? |

| 1. How to connect customers’ needs beyond the payment function? |

| 2. What strategies have been adopted in the face of the onslaught of the COVID-19 pandemic? |

| 3. What promotions and services are used online? |

| 4. What are the online services and plans after the outbreak is lifted? |

| 5. What are the actors and works for management in payment adoption? |

| 6. What training plan and solution for mobile payment have been carried out? |

| 7. What strategies are used to maintain existing customers and develop new customers? |

| 8. What is the autonomy of vendor’s data? How are the backend data collected, analyzed, and applied? |

| 9. What is the plan for online and shops traffic diversion? |

| 10. When designing the mobile payment mechanism, have you considered scalability and the possibility of future expansion? What are your plans to address future changes and developments in the mobile payments market? |

| 1. How to extend the effect of value-added services in the future? |

| 2. How can more in-depth planning be carried out for night markets with different types and characteristics? |

| 3. There are different types of customers, such as local, tourist, commuter, etc. How to focus on different types as a follow-up reference? |

| 4. What are the plans for co-operation with local governments? |

| 5. What are the characteristics of night markets that are conducive to the promotion of mobile payments? |

| 6. How well are the vendors learning about mobile payments? |

| 7. What customized services are provided to vendors? |

| 8. How do we measure ongoing consumer use and satisfaction? |

| 9. What are the gains and growth of introducing mobile payments? |

| 10. What are the specific benefits for merchants using your mobile payment mechanism? How did you design the mechanism to ensure merchant satisfaction and benefits? |

References

- Yu, S.-Y.; Chen, D.C. Consumers’ Switching from Cash to Mobile Payment under the Fear of COVID-19 in Taiwan. Sustainability 2022, 14, 8489. [Google Scholar] [CrossRef]

- Cohen, M.J. Does the COVID-19 outbreak mark the onset of a sustainable consumption transition? Sustain. Sci. Pract. Policy 2020, 16, 1–3. [Google Scholar] [CrossRef]

- Buhalis, D.; Harwood, T.; Bogicevic, V.; Viglia, G.; Beldona, S.; Hofacker, C. Technological disruptions in services: Lessons from tourism and hospitality. J. Serv. Manag. 2019, 30, 484–506. [Google Scholar] [CrossRef]

- Verhoef, P.C.; Broekhuizen, T.; Bart, Y.; Bhattacharya, A.; Dong, J.Q.; Fabian, N.; Haenlein, M. Digital transformation: A multidisciplinary reflection and research agenda. J. Bus. Res. 2021, 122, 889–901. [Google Scholar] [CrossRef]

- Gomes, L.A.D.V.; Facin, A.L.F.; Salerno, M.S.; Ikenami, R.K. Unpacking the innovation ecosystem construct: Evolution, gaps and trends. Technol. Forecast. Soc. Chang. 2018, 136, 30–48. [Google Scholar] [CrossRef]

- Paasi, J.; Wiman, H.; Apilo, T.; Valkokari, K. Modeling the dynamics of innovation ecosystems. Int. J. Innov. Stud. 2023, 7, 142–158. [Google Scholar] [CrossRef]

- Cannas, R. Exploring digital transformation and dynamic capabilities in agrifood SMEs. J. Small Bus. Manag. 2021, 61, 1611–1637. [Google Scholar] [CrossRef]

- Ellström, D.; Holtström, J.; Berg, E.; Josefsson, C. Dynamic capabilities for digital transformation. J. Strategy Manag. 2022, 15, 272–286. [Google Scholar] [CrossRef]

- Cordeiro, L.F.D.S.; Cordeiro, C.F.D.S.; Ferrari, S. Cotton yield and boron dynamics affected by cover crops and boron fertilization in a tropical sandy soil. Field Crops Res. 2022, 284, 108575. [Google Scholar] [CrossRef]

- Klimas, P.; Czakon, W. Species in the wild: A typology of innovation ecosystems. Rev. Manag. Sci. 2022, 16, 249–282. [Google Scholar] [CrossRef]

- Yaghmaie, P.; Vanhaverbeke, W. Identifying and describing constituents of innovation ecosystems. EuroMed J. Bus. 2020, 15, 283–314. [Google Scholar] [CrossRef]

- Pundziene, A.; Adams, R.; Grichnik, D.; Volkmann, C. Artificiality and Sustainability in Entrepreneurship. Exploring the Unforeseen and Paving the Way to a Sustainable Future; Springer: Cham, Switzerland, 2022; pp. 3–16. [Google Scholar]

- Kubiszewski, I.; Concollato, L.; Costanza, R.; Stern, D.I. Changes in authorship, networks, and research topics in ecosystem services. Ecosyst. Serv. 2023, 59, 101501. [Google Scholar] [CrossRef]

- Jacobides, M.G.; Cennamo, C.; Gawer, A. Towards a theory of ecosystems. Strateg. Manag. J. 2018, 39, 2255–2276. [Google Scholar] [CrossRef]

- Wang, Y.; Ma, L.; Pei, J.; Li, W.; Zhou, Y.; Dou, X.; Wang, X. The level of life space mobility among community-dwelling elderly: A systematic review and meta-analysis. Arch. Gerontol. Geriatr. 2023, 117, 105278. [Google Scholar] [CrossRef]

- Ananda, A.S.; Hanny, H.; Hernández-García, Á.; Prasetya, P. Stimuli Are All Around’—The Influence of Offline and Online Servicescapes in Customer Satisfaction and Repurchase Intention. J. Theor. Appl. Electron. Commer. Res. 2023, 18, 524–547. [Google Scholar] [CrossRef]

- Moore, J. Predators and prey: A new ecology of competition. Harv. Bus. Rev. 1999, 71, 75–86. [Google Scholar]

- Darko, P.; Liang, D.; Xu, Z.; Kobina, A.; Obiora, S. A novel multi-attribute decision-making for ranking mobile payment services using online consumer reviews. Expert Syst. Appl. 2023, 213, 119262. [Google Scholar] [CrossRef] [PubMed]

- Ng, C.L.; Vargo, S.L. Service-dominant logic, service ecosystems and institutions: An editorial. J. Serv. Manag. 2018, 29, 518–520. [Google Scholar] [CrossRef]

- Vargo, S.L.; Lusch, R.F. Service-dominant logic 2025. Int. J. Res. Mark. 2017, 34, 46–67. [Google Scholar] [CrossRef]

- Kaur, P.; Dhir, A.; Singh, N.; Sahu, G.; Almotairi, M. An innovation resistance theory perspective on mobile payment solutions. J. Retail. Consum. Serv. 2020, 55, 102059. [Google Scholar] [CrossRef]

- Bolton, R.N.; McColl-Kennedy, J.R.; Cheung, L.; Gallan, A.; Orsingher, C.; Witell, L.; Zaki, M. Customer experience challenges: Bringing together digital, physical and social realms. J. Serv. Manag. 2018, 29, 776–808. [Google Scholar] [CrossRef]

- Teece, D.J. Explicating dynamic capabilities: The nature and micro-foundations of (sustainable) enterprise performance. Strateg. Manag. J. 2007, 28, 1319–1350. [Google Scholar] [CrossRef]

- Busch, G.; Spiller, A.; Kühl, S. Review: Ethical responsibilities and transformation strategies of focal companies in the meat supply chain: The implementation dilemma. Animal 2023, 17, 100915. [Google Scholar] [CrossRef] [PubMed]

- Kohtamäki, M.; Rajala, R. Theory and practice of value co-creation in b2b systems. Ind. Mark. Manag. 2016, 56, 4–13. [Google Scholar] [CrossRef]

- Marcos, J.; Nätti, S.; Palo, T.; Baumann, J. Value co-creation practices and capabilities: Sustained purposeful engagement across b2b systems. Ind. Mark. Manag. 2016, 56, 97–107. [Google Scholar] [CrossRef]

- Lusch, R.; Vargo, S.; Tanniru, M. Service, value networks and learning. J. Acad. Mark. Sci. 2009, 38, 19–31. [Google Scholar] [CrossRef]

- Vargo, S.L.; Lusch, R.F. Service-dominant logic: Continuing the evolution. J. Acad. Mark. Sci. 2007, 36, 1–10. [Google Scholar] [CrossRef]

- Akaka, M.A.; Vargo, S.L.; Lusch, R.F. The complexity of context: A service ecosystems approach for international marketing. J. Int. Mark. 2013, 21, 1–20. [Google Scholar] [CrossRef]

- Beirão, G.; Patrício, L.; Fisk, R.P. Value cocreation in service ecosystems. J. Serv. Manag. 2017, 28, 227–249. [Google Scholar] [CrossRef]

- Wassler, P.; Fan, D.X.F. A tale of four futures: Tourism academia and COVID-19. Tour. Manag. Perspect. 2021, 38, 100818. [Google Scholar] [CrossRef]

- Akaka, M.A.; Vargo, S.L.; Nariswari, A.; O’Brien, M. Micro-foundations for macro-marketing: A metatheoretical lens for bridging the micro-macro divide. J. Macro-Mark. 2021, 43, 61–75. [Google Scholar] [CrossRef]

- Petricevic, O.; Teece, D.J. The structural reshaping of globalization: Implications for strategic sectors, profiting from innovation, and the multinational enterprise. J. Int. Bus. Stud. 2019, 50, 1487–1512. [Google Scholar] [CrossRef]

- Teece, D.; Peteraf, M.; Leih, S. Dynamic capabilities and organizational agility: Risk, uncertainty, and strategy in the innovation economy. Calif. Manag. Rev. 2016, 58, 13–35. [Google Scholar] [CrossRef]

- Matarazzo, M.; Penco, L.; Profumo, G.; Quaglia, R. Digital transformation and customer value creation in made in Italy SMEs: A dynamic capabilities perspective. J. Bus. Res. 2021, 123, 642–656. [Google Scholar] [CrossRef]

- Blaschke, M.; Riss, U.; Haki, K.; Aier, S. Design principles for digital value co-creation networks: A service-dominant logic perspective. Electron. Mark. 2019, 29, 443–472. [Google Scholar] [CrossRef]

- Chen, J.-S.; Kerr, D.; Chou, C.; Ang, C. Business co-creation for service innovation in the hospitality and tourism industry. Int. J. Contemp. Hosp. Manag. 2018, 29, 1522–1540. [Google Scholar] [CrossRef]

- Plugge, A.; Bouwman, H. Tensions in global IT multi-sourcing arrangements: Examining the barriers to attaining common value creation. J. Glob. Inf. Technol. Manag. 2018, 21, 262–281. [Google Scholar]

- Chen, C.-L. Value-constellation innovation by firms participating in government-funded technology development. J. Glob. Inf. Technol. Manag. 2020, 23, 248–272. [Google Scholar] [CrossRef]

- de Luna, I.R.; Liébana-Cabanillas, F.; Sánchez-Fernández, J.; Muñoz-Leiva, F. Mobile payment is not all the same: The adoption of mobile payment systems depending on the technology applied. Technol. Forecast. Soc. Chang. 2018, 146, 931–994. [Google Scholar] [CrossRef]

- Pinho, J. Dynamic capabilities and international performance of SMEs: The interaction effect of relational social capital. In Research Handbook on Export Marketing; Edward Elgar Publishing: Cheltenham, UK, 2014; pp. 45–59. [Google Scholar]

- Gawer, A.; Cusumano, M. Industry platforms and ecosystem innovation. J. Prod. Innov. Manag. 2014, 31, 417–433. [Google Scholar] [CrossRef]

- Perry, C. Processes of a case study methodology for postgraduate research in marketing. Eur. J. Mark. 1998, 32, 785–802. [Google Scholar] [CrossRef]

- Mills, A.J.; Durepos, G.; Wiebe, E. Encyclopedia of Case Study Research; SAGE Publications, Inc.: Thousand Oaks, CA, USA, 2010. [Google Scholar]

- Eisenhardt, K.M. Better stories and better constructs: The case for rigor and comparative logic. Acad. Manag. Rev. 1991, 16, 620–627. [Google Scholar] [CrossRef]

- Benbasat, I.; Goldstein, D.K.; Mead, M. The case research strategy in studies of information systems. MIS Q. 1987, 11, 369–386. [Google Scholar] [CrossRef]

- Yin, R.K. Case Study Research: Design and Methods; Sage Publications: Thousand Oaks, CA, USA; London, UK, 2003. [Google Scholar]

- Lian, J.-W.; Li, J. The dimensions of trust: An investigation of mobile payment services in Taiwan. Technol. Soc. 2021, 67, 101753. [Google Scholar] [CrossRef]

- Shang, S.S.C.; Chiu, L.S.L. A race pathway for inventing and sustaining mobile payment innovation—A case study of a leading bank in Taiwan. Asia Pac. Manag. Rev. 2023, 28, 401–409. [Google Scholar] [CrossRef]

- Alvesson, M. Beyond neopositivists, romantics, and localists: A reflexive approach to interviews in organizational research. Acad. Manag. Rev. 2003, 28, 13–33. [Google Scholar] [CrossRef]

- Yin, R.K. Case Study Research and Applications: Design and Methods; SAGE: Los Angeles, CA, USA, 2018. [Google Scholar]

- Kasabov, E. Marketing mix. In Wiley Encyclopedia of Management; Wiley: Hoboken, NJ, USA, 2015. [Google Scholar]

- Eisenhardt, K.M. Building theories from case study research. Acad. Manag. Rev. 1989, 14, 532–550. [Google Scholar] [CrossRef]

- Karimi, J.; Walter, Z. The role of dynamic capabilities in responding to digital disruption: A factor-based study of the newspaper industry. J. Manag. Inf. Syst. 2015, 32, 39–81. [Google Scholar] [CrossRef]

- Prentice, C.; Altinay, L.; Woodside, A.G. Transformative service research and COVID-19. Serv. Ind. J. 2021, 41, 1–8. [Google Scholar] [CrossRef]

- Haki, K.; Blaschke, M.; Aier, S.; Winter, R.; Tilson, D. Dynamic capabilities for transitioning from product platform ecosystem to innovation platform ecosystem. Eur. J. Inf. Syst. 2022, 33, 181–199. [Google Scholar] [CrossRef]

- Soluk, J.; Kammerlander, N. Digital transformation in family-owned Mittelstand firms: A dynamic capabilities perspective. Eur. J. Inf. Syst. 2021, 30, 676–711. [Google Scholar] [CrossRef]

- Baiyere, A.; Salmela, H.; Tapanainen, T. Digital transformation and the new logics of business process management. Eur. J. Inf. Syst. 2020, 29, 238–259. [Google Scholar] [CrossRef]

- Nambisan, S.; Lyytinen, K.; Majchrzak, A.; Song, M. Digital innovation management. MIS Q. 2017, 41, 223–238. [Google Scholar] [CrossRef]

- Han, J.; Zhou, H.; Lowik, S.; de Weerd-Nederhof, P. Enhancing the understanding of ecosystems under innovation management context: Aggregating conceptual boundaries of ecosystems. Ind. Mark. Manag. 2022, 106, 112–138. [Google Scholar] [CrossRef]

- Kapoor, R. Ecosystems: Broadening the locus of value creation. J. Organ. Des. 2018, 7, 12. [Google Scholar] [CrossRef]

- Arli, D.; Dietrich, T. Can social media campaigns backfire? Exploring consumers’ attitudes and word-of-mouth toward four social media campaigns and its implications on consumer-campaign identification. J. Promot. Manag. 2017, 23, 1–17. [Google Scholar] [CrossRef]

- Teece, D.J. Profiting from innovation in the digital economy: Enabling technologies, standards, and licensing models in the wireless world. Res. Policy 2018, 47, 1367–1387. [Google Scholar] [CrossRef]

- Fadhil-Ondoy, M.; Vafaei-Zadeh, A.; Hanifah, H.; Ramayah, T.; Ping, T. Achieving a sustainable cashless society through mobile e-wallet: An extended technology acceptance model. Int. J. Mob. Commun. 2024, 23, 257–297. [Google Scholar]

- Dolan, P. The sustainability of sustainable consumption. J. Macromark. 2002, 22, 170–181. [Google Scholar] [CrossRef]

- Tubillejas-Andrés, B.; Cervera-Taulet, A.; García, H.C. How emotional response mediates servicescape impact on post consumption outcomes: An application to opera events. Tour. Manag. Perspect. 2020, 34, 100660. [Google Scholar] [CrossRef]

- Wong, D.T.W.; Ngai, E.W.T. Economic, organizational, and environmental capabilities for business sustainability competence: Findings from case studies in the fashion business. J. Bus. Res. 2021, 126, 440–471. [Google Scholar] [CrossRef]

- Nguyen, A.T.V.; McClelland, R.; Thuan, N.H. Exploring customer experience during channel switching in omnichannel retailing context: A qualitative assessment. J. Retail. Consum. Serv. 2022, 64, 102803. [Google Scholar] [CrossRef]

- Zhang, T.; Gerlowski, D.; Acs, Z. Working from home: Small business performance and the COVID-19 pandemic. Small Bus. Econ. 2021, 58, 611–636. [Google Scholar] [CrossRef]

- Song, Z.; Sun, Y.; Wan, J.; Huang, L.; Zhu, J. Smart e-commerce systems: Current status and research challenges. Electron. Mark. 2019, 29, 221–238. [Google Scholar] [CrossRef]

- Song, K.; Wu, P.; Zou, S. The adoption and use of mobile payment: Determinants and relationship with bank access. China Econ. Rev. 2023, 77, 101907. [Google Scholar] [CrossRef]

- Yi, J.; Kim, J.; Oh, Y.K. Uncovering the quality factors driving the success of mobile payment apps. J. Retail. Consum. Serv. 2024, 77, 103641. [Google Scholar] [CrossRef]

- Chen, C.-L. Cross-disciplinary innovations by Taiwanese manufacturing SMEs in the context of industry 4.0. J. Manuf. Technol. Manag. 2020, 31, 1145–1168. [Google Scholar] [CrossRef]

- Zhang, M.Y.; Williamson, P. The emergence of multiplatform ecosystems: Insights from China’s mobile payments system in overcoming bottlenecks to reach the mass market. Technol. Forecast. Soc. Chang. 2021, 173, 121128. [Google Scholar] [CrossRef]

- Marshall, A.; Lipp, A.; Ikeda, K.; Singh, R.R. Ecosystems boost revenues from innovation initiatives. Strategy Leadersh. 2020, 48, 17–27. [Google Scholar] [CrossRef]

| Case | Servicescape A (Cultural and Creative Park) | Servicescape B (Night Market) | Servicescape C (Market) | Servicescape D (Neighborhood Pharmacy) |

|---|---|---|---|---|

| Merchants | 60 | 84 | 144 | 40 |

| Period | 7-month | 7-month | 7-month | 7-month |

| Interviewees | Manager and deputy manager of creative development department | Project business manager of market development department | Manager and assistant manager of operations management department | Special assistant to the manager, commissioner to the manager |

| Case | Servicescape A (Cultural and Creative Park) | Servicescape B (Night Market) | Servicescape C (Market) | Servicescape D (Neighborhood Pharmacy) |

|---|---|---|---|---|

| Impact | Indoor space | Crowded | Risk of touch | Medical Facilities |

| Problem and challenge | Far away ATM/ cannot apply for POS /High mobility | cannot apply for POS/Customer Needs | cannot apply for POS/Low profit | Large-scale shops of the same type already have mobile payment |

| Aspiration | Space taken up by displaying labels/Understanding Difficulties | COVID-19 pandemic affects food and tourism industry severely | Older vendors are used to cash and hard to learn | Want to establish services other than the provision of medicines |

| Customer Types | Younger demographic Out-of-town and foreign tourists | Local residents Out-of-town and foreign tourists | Women aged 60 and above | Local residents |

| Number of multiple actors | Park Management (focal firms), Mobile Payments, Vendors, Consumers | Local organizations, vendors, mobile payments (focal firms), consumers | Mobile payments (focal firms), government, vendors, market administration office | Pharmacy (focal firms), deliveries, Mobile Payment, Manufacturers, Convenience Stores, Consumers |

| Leadership Characteristics | Link to platforms, vendors, and consumers | Provide platform and technology, guidance, and marketing | Provide platform and technology, Link to Local organizations | Link to store, member, and deliveries |

| Payment | QR Pay | Jko Pay | QR Pay | multi-payment |

| Payment | QR Pay | Jko Pay | Multi-Payment |

|---|---|---|---|

| Application/ System | Platform website | Application | Application |

| Device | QR Code stickers, stand tools | QR Code stickers, stand tools | QR Code stickers, stand tools |

| Financial Considerations | service charge | Uncertainty about the future | Service charge turnover disclosure |

| Payment Steps | Merchants apply on the platform website, customers make payments by scanning QR codes, supports two types of mobile payment modes | Merchants and customers need to register corresponding payment applications, customers make payments by scanning QR codes to enter the application, supports four types of mobile payment modes | Merchants and customers need to register corresponding payment applications, customers make payments by scanning QR codes to enter the application, supports four types of mobile payment modes |

| Customer Types | Regular customers, customers with smartphones, customers without smartphones | Customers with smartphones | Regular customers and customers with smartphones |

| Advantages | Simple and easy to use, no need to download applications, suitable for most regular customers | Provides application payment, suitable for customers with smartphones | Provides multiple payment modes, suitable for different types of customers |

| Disadvantages | Risk of data leakage through online platform operation | Only supports a single application | Requires downloading applications |

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2024 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Ng, W.-K.; Chen, S.; Chen, W.-H.; Chen, C.-L.; Jiang, J.-L. Mobile Payment Innovation Ecosystem and Mechanism: A Case Study of Taiwan’s Servicescapes. J. Theor. Appl. Electron. Commer. Res. 2024, 19, 633-653. https://doi.org/10.3390/jtaer19010034

Ng W-K, Chen S, Chen W-H, Chen C-L, Jiang J-L. Mobile Payment Innovation Ecosystem and Mechanism: A Case Study of Taiwan’s Servicescapes. Journal of Theoretical and Applied Electronic Commerce Research. 2024; 19(1):633-653. https://doi.org/10.3390/jtaer19010034

Chicago/Turabian StyleNg, Wai-Kit, Shi Chen, Wei-Hung Chen, Chun-Liang Chen, and Jhih-Ling Jiang. 2024. "Mobile Payment Innovation Ecosystem and Mechanism: A Case Study of Taiwan’s Servicescapes" Journal of Theoretical and Applied Electronic Commerce Research 19, no. 1: 633-653. https://doi.org/10.3390/jtaer19010034

APA StyleNg, W.-K., Chen, S., Chen, W.-H., Chen, C.-L., & Jiang, J.-L. (2024). Mobile Payment Innovation Ecosystem and Mechanism: A Case Study of Taiwan’s Servicescapes. Journal of Theoretical and Applied Electronic Commerce Research, 19(1), 633-653. https://doi.org/10.3390/jtaer19010034