Understanding FinTech Platform Adoption: Impacts of Perceived Value and Perceived Risk

Abstract

1. Introduction

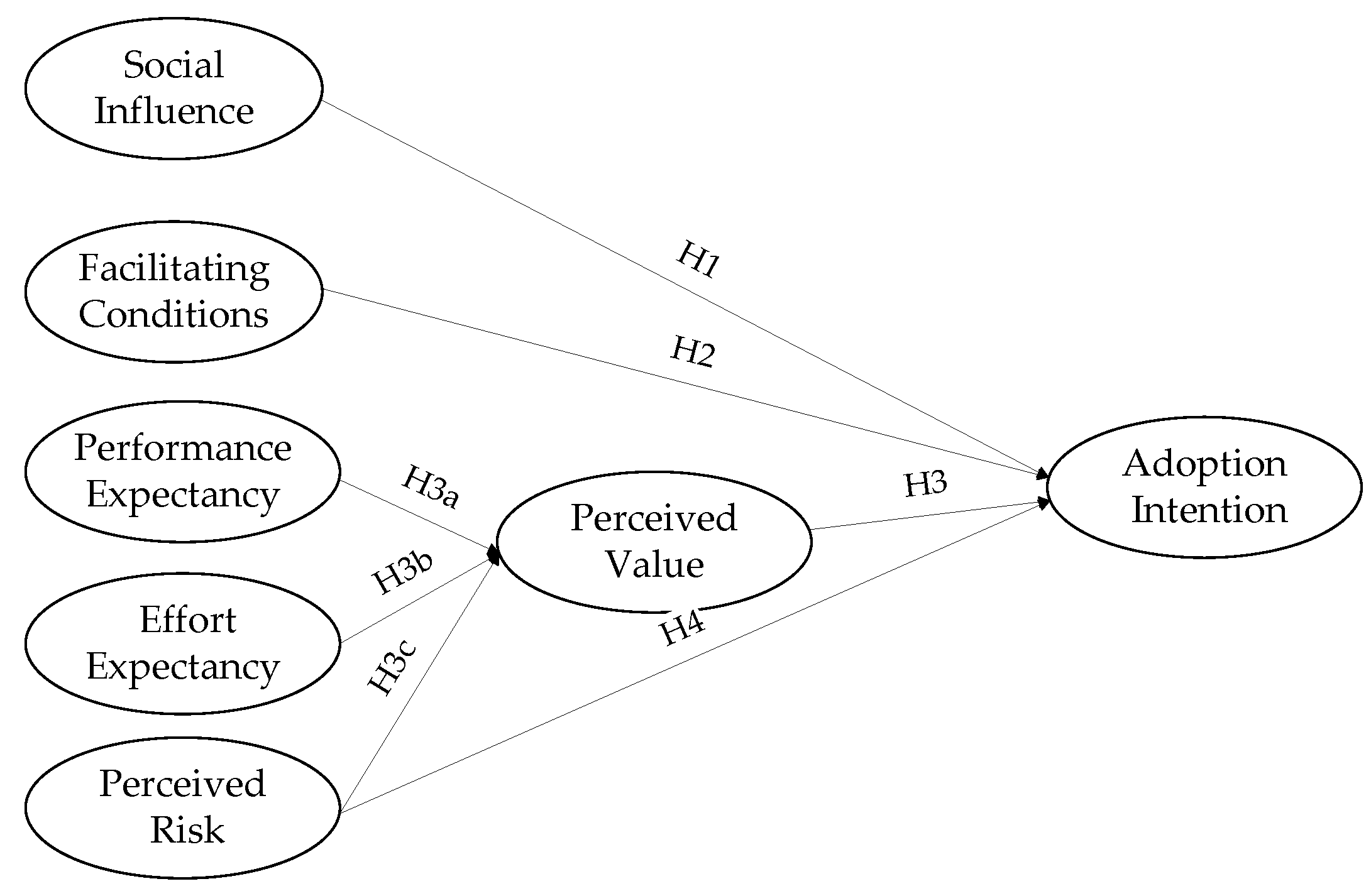

2. Theoretical Foundation and Hypotheses Development

2.1. Theoretical Foundation

2.2. Social Influence

2.3. Facilitating Conditions

2.4. Perceived Value

2.5. Performance Expectancy

2.6. Effort Expectancy

2.7. Perceived Risk

3. Methodology

3.1. Measurement

3.2. Data Collection

4. Data Analysis and Results

4.1. Measurement Model

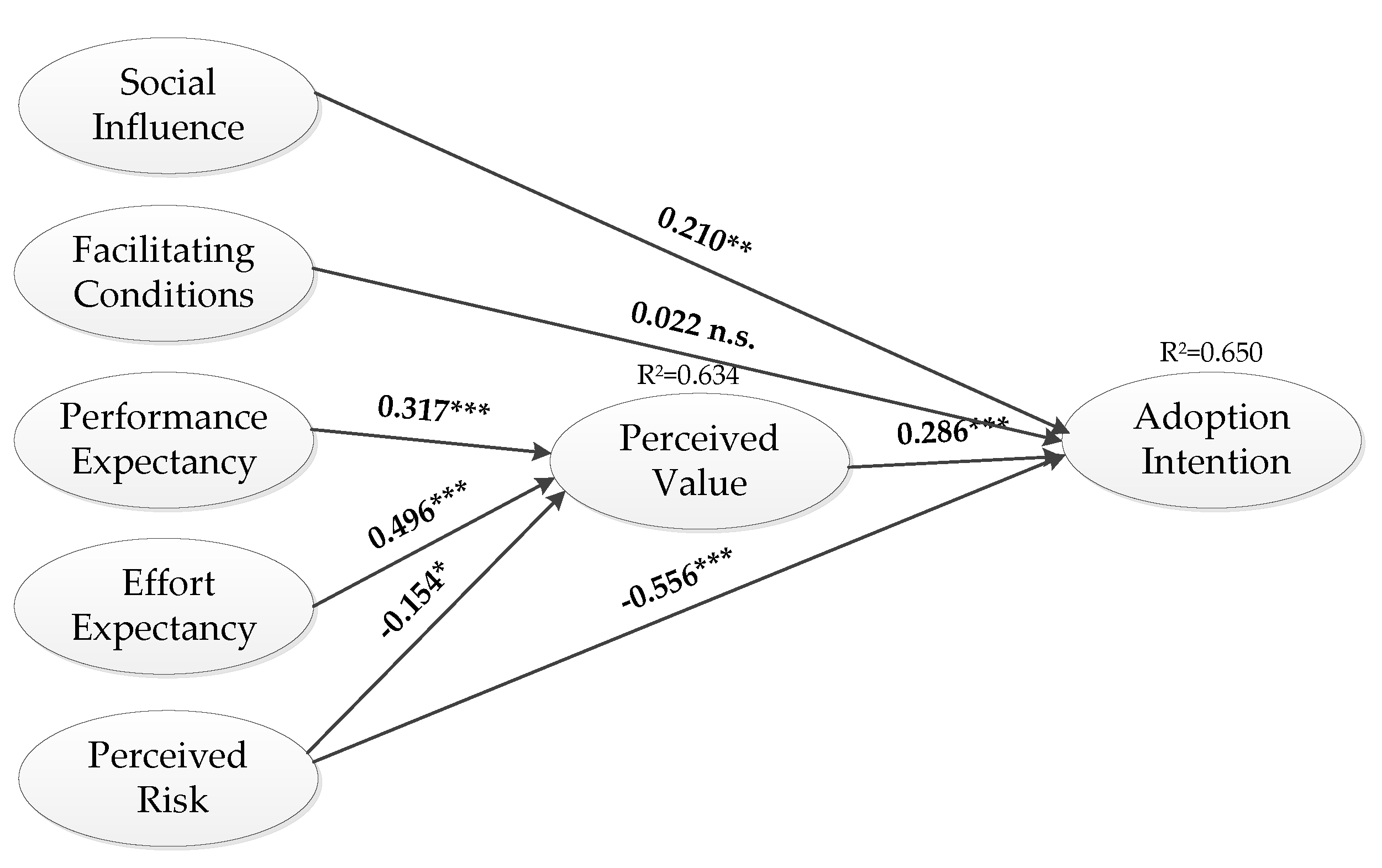

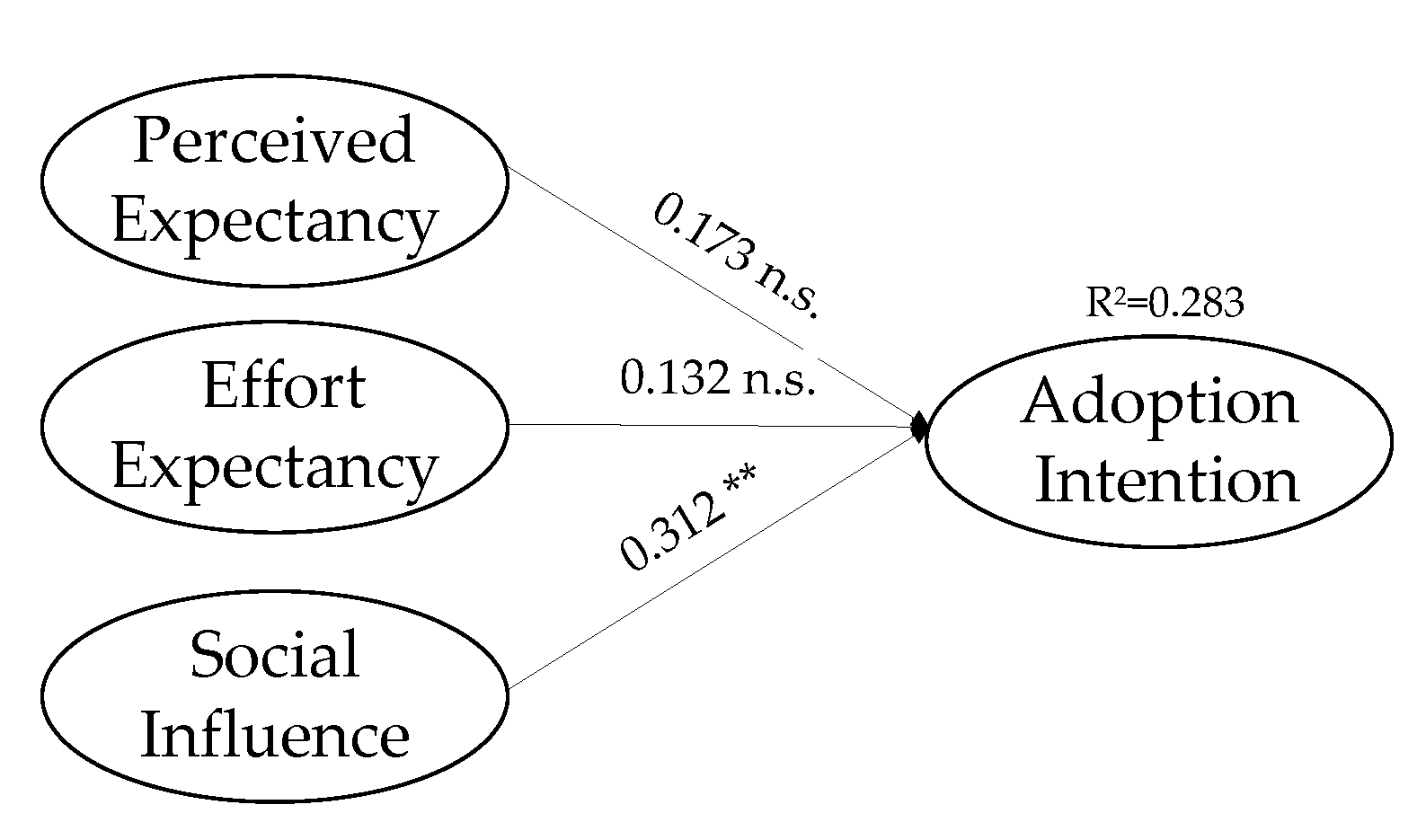

4.2. Structural Model

5. Conclusions and Discussion

6. Contributions and Limitations

6.1. Theoretical Contributions

6.2. Implications for Practice

6.3. Limitations

Author Contributions

Funding

Institutional Review Board Statement

Informed Consent Statement

Data Availability Statement

Conflicts of Interest

Appendix A

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| Construct | Measurement Items | Source |

|---|---|---|

| Performance Expectancy | PE1: I find the FinTech wealth management platform useful in my daily life. PE2: Using the FinTech wealth management platform increases my chances of capital appreciation. (dropped) PE3: Using the FinTech wealth management platform improved the utilization rate of my idle funds. PE4: Using FinTech wealth management platform increases my efficiency of finance management | Adapted from [7,50] |

| Effort Expectancy | EE1: It would be easy for me to become skillful at using the FinTech wealth management platform. EE2: I would find the platform easy to use. EE3: Learning to operate the platform is easy for me. | Adapted from [7,50] |

| Perceived Value | PV1: Compared to the effort I need to put in, the use of the FinTech wealth management platform is beneficial to me. PV2: Compared to the time I need to spend, the use of the FinTech wealth management platform is worthwhile to me. PV3: Use of the FinTech wealth management platform reducing financial management costs. PV4: Overall, the use of the FinTech wealth management platform delivers me good value. | Adapted from [28,29] |

| Social Influence | SI1: People who are important to me think that I should use the FinTech wealth management platform. SI2: People who influence my behavior think that I should use the FinTech wealth management platform. SI3: People whose opinions that I value prefer that I use the FinTech wealth management platform. (dropped) | Adapted from [7,50] |

| Perceived Risk | PR1: How would you characterize the decision to transact with the FinTech wealth management platform? (Significant risk/insignificant risk) PR2: How would you characterize the decision to transact with the FinTech wealth management platform? (Very negative/Very positive situation) PR3: How would you characterize the decision to buy a financial product from the FinTech wealth management platform? (High potential for loss/High potential for gain) PR4: How would you rate your overall perception of risk from the FinTech wealth management platform? | Adapted from [67,72] |

| Facilitating Conditions | FC1: I have the resources necessary to use the FinTech wealth management platform, such as smartphones, relative applications, and so on. FC2: I know (financial, internet usage) necessary to use the FinTech wealth management platform. FC3: I can get help from others when I have difficulties using the FinTech wealth management platform. | Adapted from [7,50] |

| Adoption Intention | AIN1: I intend to continue using the FinTech wealth management platform in the next few months. AIN2: I will always try to use the FinTech wealth management platform in my daily life. AIN3: I plan to continue to use the FinTech wealth management platform frequently. | Adapted from [7,50] |

| Adoption Behavior (for robutness test) | ABE: Please indicate your usage frequency for FinTech wealth management platforms (“never” to “many times per day”) | Adapted from [7] |

Appendix B

| Construct | 1 | 2 | 3 | 4 | 5 | 6 | 7 | |

|---|---|---|---|---|---|---|---|---|

| Performance Expectancy (PE) | PE1 | 0.775 | 0.179 | 0.219 | 0.023 | −0.109 | 0.127 | 0.157 |

| PE2 | 0.547 | 0.181 | 0.288 | 0.068 | −0.031 | 0.280 | 0.186 | |

| PE3 | 0.659 | 0.263 | 0.155 | 0.117 | −0.046 | 0.279 | 0.110 | |

| PE4 | 0.815 | 0.102 | 0.136 | 0.109 | −0.096 | 0.167 | −0.015 | |

| Effort Expectancy (EE) | EE1 | 0.337 | 0.709 | 0.050 | 0.137 | −0.059 | 0.223 | −0.001 |

| EE2 | 0.193 | 0.768 | 0.162 | 0.028 | −0.026 | 0.184 | 0.114 | |

| EE3 | 0.095 | 0.773 | 0.129 | 0.050 | −0.061 | 0.334 | 0.088 | |

| Social Influence (SI) | SI1 | 0.245 | 0.107 | 0.840 | 0.076 | −0.063 | 0.211 | 0.089 |

| SI2 | 0.230 | 0.091 | 0.804 | 0.169 | −0.025 | 0.223 | 0.188 | |

| SI3 | 0.273 | 0.306 | 0.574 | 0.147 | −0.081 | 0.272 | 0.142 | |

| Facilitating Condition (FC) | FC1 | 0.100 | 0.062 | 0.075 | 0.802 | −0.163 | 0.116 | 0.026 |

| FC2 | 0.055 | 0.129 | 0.062 | 0.845 | 0.022 | −0.017 | 0.082 | |

| FC3 | 0.067 | −0.022 | 0.111 | 0.827 | 0.076 | −0.009 | 0.003 | |

| Perceived Risk (PR) | PR1 | −0.067 | −0.062 | −0.048 | 0.025 | 0.808 | −0.092 | −0.229 |

| PR2 | −0.085 | −0.056 | −0.058 | 0.036 | 0.819 | −0.081 | −0.196 | |

| PR3 | −0.043 | −0.026 | −0.085 | −0.086 | 0.877 | −0.081 | −0.120 | |

| PR4 | −0.057 | −0.013 | 0.053 | −0.031 | 0.842 | −0.089 | −0.143 | |

| Perceived Value (PV) | PV1 | 0.225 | 0.247 | 0.184 | −0.005 | −0.104 | 0.739 | 0.218 |

| PV2 | 0.142 | 0.199 | 0.174 | 0.094 | −0.093 | 0.793 | 0.121 | |

| PV3 | 0.178 | 0.299 | 0.260 | −0.040 | −0.100 | 0.732 | 0.147 | |

| PV4 | 0.319 | 0.172 | 0.124 | 0.051 | −0.180 | 0.731 | 0.130 | |

| Adoption Intention(AIN) | AIN1 | 0.194 | 0.201 | 0.139 | 0.046 | −0.308 | 0.148 | 0.767 |

| AIN2 | 0.130 | 0.042 | 0.131 | 0.022 | −0.387 | 0.326 | 0.687 | |

| AIN3 | 0.059 | 0.024 | 0.173 | 0.097 | −0.378 | 0.175 | 0.764 | |

| Initial Eigenvalues | Extraction Sums of Squared Loadings | Rotation Sums of Squared Loadings | |||||

|---|---|---|---|---|---|---|---|

| Total | % of Variance | Total | % of Variance | Total | % of Variance | Cumulative% | |

| 1 | 7.570 | 34.411 | 7.570 | 34.411 | 3.299 | 14.995 | 14.995 |

| 2 | 3.019 | 13.723 | 3.019 | 13.723 | 2.992 | 13.600 | 28.595 |

| 3 | 2.030 | 9.229 | 2.030 | 9.229 | 2.212 | 10.056 | 38.651 |

| 4 | 1.221 | 5.552 | 1.221 | 5.552 | 2.191 | 9.959 | 48.610 |

| 5 | 1.140 | 5.182 | 1.140 | 5.182 | 2.176 | 9.892 | 58.502 |

| 6 | 0.841 | 3.821 | 0.841 | 3.821 | 2.049 | 9.315 | 67.818 |

| 7 | 0.774 | 3.518 | 0.774 | 3.518 | 1.676 | 7.617 | 75.435 |

| 8 | 0.600 | 2.729 | |||||

| 9 | 0.549 | 2.497 | |||||

| 10 | 0.505 | 2.293 | |||||

| 11 | 0.439 | 1.997 | |||||

| 12 | 0.425 | 1.930 | |||||

| 13 | 0.387 | 1.757 | |||||

| 14 | 0.353 | 1.606 | |||||

| 15 | 0.340 | 1.545 | |||||

| 16 | 0.315 | 1.430 | |||||

| 17 | 0.311 | 1.415 | |||||

| 18 | 0.282 | 1.280 | |||||

| 19 | 0.264 | 1.202 | |||||

| 20 | 0.242 | 1.101 | |||||

| 21 | 0.219 | 0.995 | |||||

| 22 | 0.173 | 0.787 | |||||

Appendix C

References

- Jiang, Y.; Ho, Y.-C.; Yan, X.; Tan, Y. Investor platform choice: Herding, platform attributes, and regulations. J. Manag. Inf. Syst. 2018, 35, 86–116. [Google Scholar] [CrossRef]

- Ernst & Young. Global FinTech Adoption Index 2019. Available online: https://go.ey.com/2CKL3vJ (accessed on 3 June 2019).

- Gomber, P.; Kauffman, R.J.; Parker, C.; Weber, B.W. On the Fintech revolution: Interpreting the forces of innovation, disruption, and transformation in financial services. J. Manag. Inf. Syst. 2018, 35, 220–265. [Google Scholar] [CrossRef]

- Gomber, P.; Kauffman, R.J.; Parker, C.; Weber, B.W. Special issue: Financial information systems and the fintech revolution. J. Manag. Inf. Syst. 2018, 35, 12–18. [Google Scholar] [CrossRef]

- Gozman, D.; Liebenau, J.; Mangan, J. The innovation mechanisms of Fintech start-ups: Insights from SWIFT’s innotribe competition. J. Manag. Inf. Syst. 2018, 35, 145–179. [Google Scholar] [CrossRef]

- Werth, O.; Schwarzbach, C.; Cardona, D.; Breitner, M.; Schulenburg, J.-M. Influencing factors for the digital transformation in the financial services sector. Z. Gesamte Versicher. 2020, 109, 1–25. [Google Scholar] [CrossRef]

- Venkatesh, V.; Thong, J.Y.L.; Xu, X. Consumer acceptance and use of information technology: Extending the unified theory of acceptance and use of technology. MIS Q. 2012, 36, 157–178. [Google Scholar] [CrossRef]

- Baptista, G.; Oliveira, T. Understanding mobile banking: The unified theory of acceptance and use of technology combined with cultural moderators. Comput. Hum. Behav. 2015, 50, 418–430. [Google Scholar] [CrossRef]

- Sharma, R.; Singh, G.; Sharma, S. Modelling internet banking adoption in Fiji: A developing country perspective. Int. J. Inf. Manag. 2020, 53, 102–116. [Google Scholar] [CrossRef]

- Maciel, Q.M.; Samuel, F.W. Blockchain adoption challenges in supply chain: An empirical investigation of the main drivers in India and the USA. Int. J. Inf. Manag. 2019, 46, 70–82. [Google Scholar] [CrossRef]

- Jansen, J.; van Schaik, P. Testing a model of precautionary online behaviour: The case of online banking. Comput. Hum. Behav. 2018, 87, 371–383. [Google Scholar] [CrossRef]

- Jia, L.; Xue, G.; Fu, Y.; Xu, L. Factors affecting consumers’ acceptance of e-commerce consumer credit service. Int. J. Inf. Manag. 2018, 40, 103–110. [Google Scholar] [CrossRef]

- Shaw, N.; Sergueeva, K. The non-monetary benefits of mobile commerce: Extending UTAUT2 with perceived value. Int. J. Inf. Manag. 2019, 45, 44–55. [Google Scholar] [CrossRef]

- Baptista, G.; Oliveira, T. Why so serious? Gamification impact in the acceptance of mobile banking services. Internet Res. 2017, 27, 118–139. [Google Scholar] [CrossRef]

- Stewart, H.; Juerjens, J. Data security and consumer trust in FinTech innovation in Germany. Inf. Comput. Secur. 2018, 26, 109–128. [Google Scholar] [CrossRef]

- Zhou, W.; Tsiga, Z.; Li, B.; Zheng, S.; Jiang, S. What influence users’ e-finance continuance intention? The moderating role of trust. Ind. Manag. Data Syst. 2018, 118, 1647–1670. [Google Scholar] [CrossRef]

- Sharma, S.K.; Sharma, M. Examining the role of trust and quality dimensions in the actual usage of mobile banking services: An empirical investigation. Int. J. Inf. Manag. 2019, 44, 65–75. [Google Scholar] [CrossRef]

- De Luna, I.R.; Liébana-Cabanillas, F.; Sánchez-Fernández, J.; Muñoz-Leiva, F. Mobile payment is not all the same: The adoption of mobile payment systems depending on the technology applied. Technol. Forecast. Soc. Chang. 2019, 146, 931–944. [Google Scholar] [CrossRef]

- Chen, X.; Hu, X.; Ben, S. How individual investors react to negative events in the FinTech era? Evidence from China’s Peer-to-Peer lending. J. Theor. Appl. Electron. Commer. Res. 2021, 16, 52–70. [Google Scholar] [CrossRef]

- Jünger, M.; Mietzner, M. Banking goes digital: The adoption of FinTech services by German households. Financ. Res. Lett. 2020, 34, 101260. [Google Scholar] [CrossRef]

- Pal Kapoor, A.; Vij, M. How to boost your App store rating? An empirical assessment of ratings for mobile banking Apps. J. Theor. Appl. Electron. Commer. Res. 2020, 15, 99–115. [Google Scholar] [CrossRef]

- Okoli, T.; Tewari, D. An empirical assessment of probability rates for financial technology adoption among African economies: A multiple logistic regression approach. Asian Econ. Financ. Rev. 2020, 10, 1342–1355. [Google Scholar] [CrossRef]

- Al Nawayseh, M.K. FinTech in COVID-19 and beyond: What factors are affecting customers’ choice of FinTech applications? J. Open Innov. Technol. Mark. Complex. 2020, 6, 153. [Google Scholar] [CrossRef]

- Kam, B.H.; Riquelme, H. An exploratory study of length and frequency of internet banking usage. J. Theor. Appl. Electron. Commer. Res. 2007, 2, 76–85. [Google Scholar] [CrossRef]

- Wei, M.-F.; Luh, Y.-H.; Huang, Y.-H.; Chang, Y.-C. Young generation’s mobile payment adoption behavior: Analysis based on an extended UTAUT model. J. Theor. Appl. Electron. Commer. Res. 2021, 16, 37. [Google Scholar] [CrossRef]

- Yeh, H. Factors in the ecosystem of mobile payment affecting its use: From the customers’ perspective in Taiwan. J. Theor. Appl. Electron. Commer. Res. 2020, 15, 13–29. [Google Scholar] [CrossRef]

- Fernando, E. Analysis of the influence of consumer behavior using FinTech services with SEM and TOPSIS. In Proceedings of the 2019 International Conference on Information Management and Technology (ICIMTech), Jakarta/Bali, Indonesia, 19–20 August 2019; pp. 93–97. [Google Scholar]

- Kim, H.-W.; Chan, H.C.; Gupta, S. Value-based adoption of mobile internet: An empirical investigation. Decis. Support Syst. 2007, 43, 111–126. [Google Scholar] [CrossRef]

- Sirdeshmukh, D.; Singh, J.; Sabol, B. Consumer trust, value, and loyalty in relational exchanges. J. Mark. 2002, 66, 15–37. [Google Scholar] [CrossRef]

- Thaler, R. Mental accounting and consumer choice. Mark. Sci. 1985, 4, 199–214. [Google Scholar] [CrossRef]

- Zeithaml, V.A. Consumer perceptions of price, quality and value: A means-end model and synthesis of evidence. J. Mark. 1988, 52, 2–22. [Google Scholar] [CrossRef]

- Gordon, R.; Dibb, S.; Magee, C.; Cooper, P.; Waitt, G. Empirically testing the concept of value-in-behavior and its relevance for social marketing. J. Bus. Res. 2018, 82, 56–67. [Google Scholar] [CrossRef]

- Chopdar, P.K.; Korfiatis, N.; Sivakumar, V.J.; Lytras, M.D. Mobile shopping apps adoption and perceived risks: A cross-country perspective utilizing the Unified Theory of Acceptance and Use of Technology. Comput. Hum. Behav. 2018, 86, 109–128. [Google Scholar] [CrossRef]

- Featherman, M.S.; Pavlou, P.A. Predicting e-services adoption: A perceived risk facets perspective. Int. J. Hum. Comput. Stud. 2003, 59, 451–474. [Google Scholar] [CrossRef]

- Kahneman, D.; Tversky, A. Prospect theory: An analysis of decision under risk. Econometrica 1979, 47, 263–292. [Google Scholar] [CrossRef]

- Thakur, R.; Srivastava, M. Adoption readiness, personal innovativeness, perceived risk and usage intention across customer groups for mobile payment services in India. Internet Res. 2014, 24, 369–392. [Google Scholar] [CrossRef]

- Antony, S.; Lin, Z.; Xu, B. Determinants of escrow service adoption in consumer-to-consumer online auction market: An experimental study. Decis. Support Syst. 2006, 42, 1889–1900. [Google Scholar] [CrossRef]

- Lee, M.-C. Factors influencing the adoption of internet banking: An integration of TAM and TPB with perceived risk and perceived benefit. Electron. Commer. Res. Appl. 2009, 8, 130–141. [Google Scholar] [CrossRef]

- Alalwan, A.A.; Dwivedi, Y.K.; Rana, N.P.; Algharabat, R. Examining factors influencing Jordanian customers’ intentions and adoption of internet banking: Extending UTAUT2 with risk. J. Retail. Consum. Serv. 2018, 40, 125–138. [Google Scholar] [CrossRef]

- Liu, Y.; Wang, M.; Huang, D.; Huang, Q.; Yang, H.; Li, Z. The impact of mobility, risk, and cost on the users’ intention to adopt mobile payments. Inf. Syst. E-Bus. Manag. 2019, 17, 319–342. [Google Scholar] [CrossRef]

- Fishbein, M.; Ajzen, I. Belief, Attitude, Intention and Behaviour: An Introduction to Theory and Research; Addison-Wesley: Boston, MA, USA, 1975. [Google Scholar]

- Davis, F.D. Perceived usefulness, perceived ease of use, and user acceptance of information technology. MIS Q. 1989, 13, 319–340. [Google Scholar] [CrossRef]

- Rogers, E.M. Diffusion of Innovations, 4th ed.; The Free Press: New York, NY, USA, 1995. [Google Scholar]

- Davis, F.D.; Bagozzi, R.P.; Warshaw, P.R. User acceptance of computer technology: A comparison of two theoretical models. Manag. Sci. 1989, 35, 982–1003. [Google Scholar] [CrossRef]

- Davis, F.D.; Bagozzi, R.P.; Warshaw, P.R. Extrinsic and Intrinsic Motivation to Use Computers in the Workplace1. J. Appl. Soc. Psychol. 1992, 22, 1111–1132. [Google Scholar] [CrossRef]

- Ajzen, I. The theory of planned behavior. Organ. Behav. Hum. Decis. Process 1991, 50, 179–211. [Google Scholar] [CrossRef]

- Taylor, S.; Todd, P. Assessing IT usage: The role of prior experience. MIS Q. 1995, 19, 561–570. [Google Scholar] [CrossRef]

- Thompson, R.L.; Higgins, C.A.; Howell, J.M. Personal computing: Toward a conceptual model of utilization. MIS Q. 1991, 15, 125–143. [Google Scholar] [CrossRef]

- Bandura, A. Social Foundations of Thought and Action: A Social Cognitive Theory; Prentice Hall: Hoboken, NJ, USA, 1986. [Google Scholar]

- Venkatesh, V.; Morris, M.G.; Davis, G.B.; Davis, F.D. User acceptance of information technology: Toward a unified view. MIS Q. 2003, 27, 425–478. [Google Scholar] [CrossRef]

- Oliveira, T.; Thomas, M.; Baptista, G.; Campos, F. Mobile payment: Understanding the determinants of customer adoption and intention to recommend the technology. Comput. Hum. Behav. 2016, 61, 404–414. [Google Scholar] [CrossRef]

- Im, I.; Hong, S.; Kang, M.S. An international comparison of technology adoption. Inf. Manag. 2011, 48, 1–8. [Google Scholar] [CrossRef]

- Yang, Q.; Pang, C.; Liu, L.; Yen, D.C.; Michael Tarn, J. Exploring consumer perceived risk and trust for online payments: An empirical study in China’s younger generation. Comput. Hum. Behav. 2015, 50, 9–24. [Google Scholar] [CrossRef]

- Venkatesh, V.; Thong, J.Y.L.; Xu, X. Unified theory of acceptance and use of technology: A synthesis and the road ahead. J. Assoc. Inf. Syst. 2016, 17, 328–376. [Google Scholar] [CrossRef]

- Yang, S.; Lu, Y.; Gupta, S.; Cao, Y.; Zhang, R. Mobile payment services adoption across time: An empirical study of the effects of behavioral beliefs, social influences, and personal traits. Comput. Hum. Behav. 2012, 28, 129–142. [Google Scholar] [CrossRef]

- Chiu, Y.-T.H.; Lee, W.-I.; Liu, C.-C.; Liu, L.-Y. Internet lottery commerce: An integrated view of online sport lottery adoption. J. Internet Commer. 2012, 11, 68–80. [Google Scholar] [CrossRef]

- Hamari, J.; Koivisto, J. “Working out for likes”: An empirical study on social influence in exercise gamification. Comput. Hum. Behav. 2015, 50, 333–347. [Google Scholar] [CrossRef]

- Rana, N.P.; Dwivedi, Y.K.; Williams, M.D.; Weerakkody, V. Adoption of online public grievance redressal system in India: Toward developing a unified view. Comput. Hum. Behav. 2016, 59, 265–282. [Google Scholar] [CrossRef]

- Oliveira, T.; Faria, M.; Thomas, M.A.; Popovič, A. Extending the understanding of mobile banking adoption: When UTAUT meets TTF and ITM. Int. J. Inf. Manag. 2014, 34, 689–703. [Google Scholar] [CrossRef]

- Beach, L.R.; Mitchell, T.R. A contingency model for the selection of decision strategies. Acad. Manag. Rev. 1978, 3, 439–449. [Google Scholar] [CrossRef]

- Payne, J.W. Contingent decision behavior. Psychol. Bull. 1982, 92, 382–402. [Google Scholar] [CrossRef]

- Sweeney, J.C.; Soutar, G.N. Consumer perceived value: The development of a multiple item scale. J. Retail. 2001, 77, 203–220. [Google Scholar] [CrossRef]

- Johnson, E.; Payne, J. Effort and accuracy in choice. Manag. Sci. 1985, 31, 395–414. [Google Scholar] [CrossRef]

- Turel, O.; Serenko, A.; Bontis, N. User acceptance of wireless short messaging services: Deconstructing perceived value. Inf. Manag. 2007, 44, 63–73. [Google Scholar] [CrossRef]

- Chiu, C.-M.; Wang, E.T.G.; Fang, Y.-H.; Huang, H.-Y. Understanding customers’ repeat purchase intentions in B2C e-commerce: The roles of utilitarian value, hedonic value and perceived risk. Inf. Syst. J. 2014, 24, 85–114. [Google Scholar] [CrossRef]

- Roy, A. Strategic social marketing. J. Int. Consum. Mark. 2016, 28, 73–74. [Google Scholar] [CrossRef]

- Kim, D.J.; Ferrin, D.L.; Rao, H.R. A trust-based consumer decision-making model in electronic commerce: The role of trust, perceived risk, and their antecedents. Decis. Support Syst. 2008, 44, 544–564. [Google Scholar] [CrossRef]

- Peter, J.P.; Ryan, M.J. An investigation of perceived risk at the brand level. J. Mark. Res. 1976, 13, 184–188. [Google Scholar] [CrossRef]

- Chong, A.Y.L. A two-staged SEM-neural network approach for understanding and predicting the determinants of m-commerce adoption. Expert Syst. Appl. 2013, 40, 1240–1247. [Google Scholar] [CrossRef]

- Slade, E.L.; Dwivedi, Y.K.; Piercy, N.C.; Williams, M.D. Modeling consumers’ adoption intentions of remote mobile payments in the United Kingdom: Extending UTAUT with innovativeness, risk, and trust. Psychol. Mark. 2015, 32, 860–873. [Google Scholar] [CrossRef]

- CNNIC. Statistical Report on Internet Development in China; China Internet Network Information Center: Beijing, China, 2019. [Google Scholar]

- Pavlou, P.A. Consumer acceptance of electronic commerce: Integrating trust and risk with the technology acceptance model. Int. J. Electron. Commer. 2003, 7, 101–134. [Google Scholar] [CrossRef]

- Brislin, R.W. Back-translation for cross-cultural research. J. Cross-Cult. Psychol. 1970, 1, 185–216. [Google Scholar] [CrossRef]

- Hair, J.F.; Black, W.C.; Babin, B.J.; Anderson, R.E. Multivariate Data Analysis, 7th ed.; Pearson Education: London, UK, 2010. [Google Scholar]

- Gefen, D.; Rigdon, E.E.; Straub, D. Editor’s Comments: An Update and Extension to SEM Guidelines for Administrative and Social Science Research. MIS Q. 2011, 35, iii–xiv. [Google Scholar] [CrossRef]

- MacKenzie, S.; Podsakoff, P.; Podsakoff, N. Construct measurement and validation procedures in MIS and behavioral research: Integrating new and existing techniques. MIS Q. 2011, 35, 293–334. [Google Scholar] [CrossRef]

- Bentler, P.M.; Bonett, D.G. Significance tests and goodness of fit in the analysis of covariance structures. Psychol. Bull. 1980, 88, 588–606. [Google Scholar] [CrossRef]

- Salisbury, W.D.; Chin, W.W.; Gopal, A.; Newsted, P.R. Research report: Better theory through measurement—Developing a scale to capture consensus on appropriation. Inf. Syst. Res. 2002, 13, 91–103. [Google Scholar] [CrossRef]

- Podsakoff, P.M.; MacKenzie, S.B.; Lee, J.Y.; Podsakoff, N.P. Common method biases in behavioral research: A critical review of the literature and recommended remedies. J. Appl. Psychol. 2003, 88, 879–903. [Google Scholar] [CrossRef] [PubMed]

- Podsakoff, P.M.; Organ, D. Self-report in organizational research: Problems and prospects. J. Manag. 1986, 12, 531–544. [Google Scholar] [CrossRef]

- Yazdanmehr, A.; Wang, J.; Yang, Z. Peers matter: The moderating role of social influence on information security policy compliance. Inf. Syst. J. 2020, 30, 791–944. [Google Scholar] [CrossRef]

- Shah, M.H.; Peikari, H.R.; Yasin, N.M. The determinants of individuals’ perceived e-security: Evidence from Malaysia. Int. J. Inf. Manag. 2014, 34, 48–57. [Google Scholar] [CrossRef]

| Measure | Items | Frequency | Percentage (%) |

|---|---|---|---|

| Gender | Female | 110 | 54.7 |

| Male | 91 | 45.3 | |

| Age | ≤20 | 15 | 7.5 |

| 21–30 | 87 | 43.3 | |

| 31–40 | 65 | 32.3 | |

| 41–50 | 25 | 12.4 | |

| >50 | 9 | 4.5 | |

| Educational background | High school and below | 27 | 13.4 |

| Some college | 73 | 36.3 | |

| Bachelor | 64 | 31.8 | |

| Master | 21 | 10.4 | |

| Doctorate | 16 | 8.0 |

| Statistic | χ2 | d.f. | χ2/d.f. | χ2 (p-Value) | CFI | TLI | RMSEA | SRMR |

|---|---|---|---|---|---|---|---|---|

| Results | 209.286 | 188 | 1.113 | 0.137 | 0.991 | 0.988 | 0.024 | 0.041 |

| Suggested Value | - | - | <5 | p > 0.05 | >0.9 | >0.9 | <0.08 | <0.1 |

| Reference | Bentler and Bonett [77]; Salisbury, et al. [78] | |||||||

| Construct | Cronbach’s α | Items | Parameters of Significant Test | Item Reliability | |||

|---|---|---|---|---|---|---|---|

| Estimate | S.E. | Est./S.E. | p | R-Square | |||

| Performance Expectancy (PE) | 0.794 | PE1 | 0.783 | 0.039 | 20.052 | *** | 0.613 |

| PE3 | 0.767 | 0.040 | 19.166 | *** | 0.588 | ||

| PE4 | 0.699 | 0.045 | 15.489 | *** | 0.488 | ||

| Effort Expectancy (EE) | 0.788 | EE1 | 0.751 | 0.042 | 18.082 | *** | 0.565 |

| EE2 | 0.711 | 0.044 | 16.040 | *** | 0.505 | ||

| EE3 | 0.771 | 0.040 | 19.210 | *** | 0.594 | ||

| Social Influence (SI) | 0.850 | SI1 | 0.834 | 0.036 | 23.064 | *** | 0.696 |

| SI2 | 0.886 | 0.034 | 25.725 | *** | 0.785 | ||

| Facilitating Condition (FC) | 0.787 | FC1 | 0.722 | 0.049 | 14.798 | *** | 0.521 |

| FC2 | 0.808 | 0.045 | 17.943 | *** | 0.653 | ||

| FC3 | 0.703 | 0.049 | 14.392 | *** | 0.494 | ||

| Perceived Risk (PR) | 0.887 | PR1 | 0.809 | 0.030 | 26.905 | *** | 0.654 |

| PR2 | 0.807 | 0.030 | 26.725 | *** | 0.651 | ||

| PR3 | 0.847 | 0.026 | 32.216 | *** | 0.718 | ||

| PR4 | 0.796 | 0.031 | 25.484 | *** | 0.634 | ||

| Perceived Value (PV) | 0.882 | PV1 | 0.839 | 0.026 | 31.744 | *** | 0.704 |

| PV2 | 0.771 | 0.033 | 23.092 | *** | 0.595 | ||

| PV3 | 0.840 | 0.026 | 31.876 | *** | 0.706 | ||

| PV4 | 0.779 | 0.033 | 23.647 | *** | 0.606 | ||

| Adoption Intention (AIN) | 0.857 | AIN1 | 0.832 | 0.030 | 28.204 | *** | 0.692 |

| AIN2 | 0.817 | 0.031 | 26.556 | *** | 0.668 | ||

| AIN3 | 0.800 | 0.032 | 24.699 | *** | 0.640 | ||

| Construct | CR | AVE | PE | EE | SI | FC | PR | PV | AIN |

|---|---|---|---|---|---|---|---|---|---|

| PE | 0.794 | 0.563 | 0.750 | ||||||

| EE | 0.789 | 0.555 | 0.666 | 0.745 | |||||

| SI | 0.851 | 0.740 | 0.633 | 0.471 | 0.860 | ||||

| PR | 0.888 | 0.664 | −0.265 | −0.198 | −0.183 | 0.815 | |||

| PV | 0.882 | 0.653 | 0.661 | 0.734 | 0.600 | −0.332 | 0.808 | ||

| FC | 0.789 | 0.556 | 0.274 | 0.249 | 0.317 | −0.083 | 0.149 | 0.746 | |

| BI | 0.857 | 0.667 | 0.456 | 0.390 | 0.484 | −0.689 | 0.597 | 0.181 | 0.817 |

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2021 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Xie, J.; Ye, L.; Huang, W.; Ye, M. Understanding FinTech Platform Adoption: Impacts of Perceived Value and Perceived Risk. J. Theor. Appl. Electron. Commer. Res. 2021, 16, 1893-1911. https://doi.org/10.3390/jtaer16050106

Xie J, Ye L, Huang W, Ye M. Understanding FinTech Platform Adoption: Impacts of Perceived Value and Perceived Risk. Journal of Theoretical and Applied Electronic Commerce Research. 2021; 16(5):1893-1911. https://doi.org/10.3390/jtaer16050106

Chicago/Turabian StyleXie, Jianli, Liying Ye, Wei Huang, and Min Ye. 2021. "Understanding FinTech Platform Adoption: Impacts of Perceived Value and Perceived Risk" Journal of Theoretical and Applied Electronic Commerce Research 16, no. 5: 1893-1911. https://doi.org/10.3390/jtaer16050106

APA StyleXie, J., Ye, L., Huang, W., & Ye, M. (2021). Understanding FinTech Platform Adoption: Impacts of Perceived Value and Perceived Risk. Journal of Theoretical and Applied Electronic Commerce Research, 16(5), 1893-1911. https://doi.org/10.3390/jtaer16050106