1. Introduction

There is an abundance of biomass resources in Canada. About 42% of the 910 million hectares of land is forested, of which 245 million hectares is timber productive forest [

1]. According to the World Bank, more than 7% (67.6 million hectares) of the land area is suited for agricultural purposes, of which 36.4 million hectares are used to grow crops [

1].

Expansive forests and vast amounts of arable land provided the physical resource basis of a political strategy to promote biofuel production and consumption. In early 2006, BIOCAP Canada [

2] convened a Bioenergy Challenge Dialogue group consisting of approximately 160 individuals invited from various backgrounds in the public and private sectors. After their deliberations, the group issued a communiqué stating: “[we] believe the bioenergy sector has the potential to become a significant supplier of Canadian energy and also an important and growing part of the Canadian economy [

3].” The group’s self-assigned mission was “to align and coalesce the interests of multiple bioenergy initiatives in order to form a comprehensive Canadian strategy that will stimulate the development of an environmentally, economically and socially sustainable and viable bioenergy industry; an industry that supplies 10% of Canada’s energy needs by 2012 and 20% by 2020 [

3].” This was consistent with a prevailing notion that a large scale domestic biofuel industry would convey many advantages. A report published the previous year (2005) by the Pembina Institute for Industry Canada [

4] listed several examples of the asserted benefits, including: environmental improvements, enhanced energy security, greater economic diversification, expanded employment opportunities, export market development, rural economic development, greater off-grid energy supply, improved waste management, additional value-added products and human health improvements.

Producing biofuel in Canada from agricultural and forestry feedstock, however, was neither a novel nor a new idea. The last time it had been contemplated seriously was during the energy crisis of the 1970s. In spite of high fossil fuel prices at that time and again during the early 1990s, biofuel production was not financially viable without government support [

5]. Consequently, some form of public-private coordination (where assets, risks, and rewards are shared between the government and private firms) was perceived as a prerequisite to develop the industry. The underlying idea was that private enterprises would provide greater efficiency, quantity and quality of product with government programs furnishing the additional, requisite financial resources for biofuel producers. Additional interventionist policies altering not only the incentives of final consumers but those of decision makers at each stage of biofuel production encourage the use of the increased output to satisfy energy wants. It was well established that biofuel production and consumption were highest in regions where government had taken a proactive role and forged strong ties with stakeholders in the renewable energy industry [

4].

1.1. Purpose and Objectives

In the European Union, Brazil, the United States and elsewhere, biofuels constitute an increasingly important component of national energy strategies. The general motivations of governments have been to: (1) meet national targets for the reduction of greenhouse gas emissions; (2) provide an independent, secure, diverse, sustainable and competitive energy supply; (3) stimulate the economic development of the agricultural industry and rural sector; and (4) assist renewable industries to become competitive in domestic and export markets [

6,

7]. Rather than a desire for energy security, the motivation in Canada stemmed from environmental concerns, a wish to increase rural development and infrastructure, and to improve farm incomes. Despite slightly different policy objectives in Canada, the federal and provincial governments have interceded in market processes in many ways in view of promoting biofuels.

The purpose of this study is to broaden the understanding of the motivation and economic impacts of biofuel policy in Canada. The experience in Canada provides insight that transcends geo-political boundaries regarding what was gained and what it cost. The study has two specific objectives. The first is to identify and delineate policies used to promote the production and consumption of biofuels in Canada—both federally and in the provinces. The second is to assess the implications of these policies. The assessment frames recommendations aimed at minimizing any counterproductive policy consequences.

4. Environmental and Economic Impacts

In Canada, ethanol has been promoted as a means to improve the environment through a reduction in greenhouse gas emissions, increase in farm incomes, and creation of jobs in rural areas that would contribute to revitalization of the rural economy. In this section, we evaluate how well public policies that subsidize and promote the growth of an ethanol industry in Canada meet these objectives.

4.1. Environmental Benefits

A major justification for stimulating ethanol production has been to reduce greenhouse gas emissions that result when it, rather than gasoline, is burned in internal combustion engines. Biofuel combustion releases fewer greenhouse gases into the atmosphere, notably carbon dioxide (CO

2). However, biofuel production generally requires the use (and burning) of fossil fuels. This is especially the case when cereal grains are used to produce ethanol. Modern agricultural practices involve the use of fertilizers and pesticides, both heavily dependent on the use of fossil fuels in their production. The tractors and trucks necessary to produce and transport the cereal grains to the ethanol plant require fuel. Finally, the ethanol production process itself requires some method of heating; often natural gas is used. Life cycle studies that account for all the fossil fuels used during the production of cereal-based ethanol (from well-to-wheel) reveal that the greenhouse gas reduction (over the use of gasoline in vehicles) is in the order of only 20–40 percent, depending on the agricultural practices employed, vehicle and tractor fuel economy, ethanol production process efficiency, and other factors (IEA 2004). Greenhouse gases may be reduced by 70–90 percent if cellulosic materials are used to produce ethanol (IEA 2004), mainly because fewer inputs are needed to produce the feedstock. Also, production of biodiesel from canola or soybeans reduces greenhouse gases by 40–60 percent over the use of petroleum diesel (IEA 2004). It has been found that producing ethanol from sugar cane provides a significant reduction in greenhouse gases [

34].

The Canadian public has indicated strong support for using biofuels for transportation to decrease greenhouse gas emissions [

35]. However, since corn and wheat are used as feed stocks in Canada, the federal government’s renewable fuel consumption mandate is anticipated to reduce greenhouse gas emissions by only 2.7 million tonnes per year by 2012, or roughly one percent of the Kyoto target that was in place before the federal government announced that Canada would not meet its target [

36].

The production and use of ethanol to achieve greenhouse gas reductions appears to be very costly. Henke

et al. [

37] reported on a comprehensive meta-analysis of several existing data sets from Germany to determine if the strategy to use farmland to grow the raw materials for ethanol production is a reasonable option for reducing carbon dioxide emissions. Surveying several detailed studies of ethanol feedstock production, Henke

et al. calculated net energy balances resulting from production of ethanol using sugar beets, wheat, corn, rapeseed and wood products as feedstock. The authors found that the cost of abating carbon dioxide emissions was likely to be in the range of US$300 to US$1,500 per tonne of CO

2 equivalent, depending on the assumptions used and the value of resulting by-products. This compares to estimated costs of about US$45 per tonne (or less) by using the most efficient ways of reducing greenhouse gases [

38]. Henke

et al. [

37] concluded that, from an economic perspective, there are better (less expensive) strategies for reducing greenhouse gases than using agricultural land to produce feed stocks for ethanol.

A study by Ryan

et al. [

32] examined the benefits of reducing greenhouse gases in the European Union by stimulating the use of biofuels through subsidizing the difference between the costs of biofuels and fossil fuels. The authors compared a reduction in excise taxes (a prominent strategy in Canada) or outright subsidization of the production cost of biofuels. The results of their analysis indicated the level of subsidy required to produce enough ethanol to reduce CO

2 emissions by one tonne would cost between US$269 and US$404, depending on assumptions used. They also concluded that other strategies to reduce greenhouse gases were available at much lower costs. Laan

et al. [

13] found subsidies per tonne of CO

2-equivalent avoided from corn and wheat based ethanol in Canada to be 6–100 times the market value of the offsets on the European Climate Exchange.

Although there are environmental benefits from the production and use of ethanol, there also are a number of negative environmental consequences. The rapid expansion of ethanol production in the United States has worried some that marginal quality cropland might be shifted from the Conservation Reserve Program to provide more land on which to plant corn [

11]. Farmers use more fertilizers and chemicals in their attempts to increase yields in response to the much higher prices for cereals and oilseeds. This could lead to additional leaching of nutrients into ground water and run-off into drainage systems. Increased intensity of crop production could lead to more monoculture and increased soil erosion, not to mention the greater need for fossil fuels to power the more intense farming practices.

With so little reduction in greenhouse gas emissions and the certainty of some negative environmental consequences, the wisdom of government support of ethanol expansion appears questionable if allaying environmental concerns is the only (or the main) objective. Other benefits, such as improved farm incomes, rural development and energy security are therefore needed to justify the use of government interventions to develop an ethanol industry.

4.2. Improving and Stabilizing Farm Incomes

In Canada, the production of grains and oilseeds is traditionally a low margin enterprise in which many producers struggle financially to survive [

39]. An increase in the number of ethanol plants that use cereal grains (especially corn and wheat) increases the demand and, consequently, the price, for these feed stock inputs. A report from the United States Department of Agriculture noted that the impact on primary producers in Canada could be “potentially significant with demand for (corn and wheat) expected to rise dramatically, should the ambitious 5% biofuels mandate be met” [

40].

Market analysts have partially attributed the escalation of grain and oilseed prices between spring 2006 and mid-2008 to the extra demand for corn to produce ethanol [

41]. From May 2006, when the quantity of corn to produce ethanol began to have large impacts on other competing uses of it, to June 2008 when the commodities price bubble burst, corn, soybeans, red spring wheat, oats and feed barley prices increased 193%, 149%, 92%, 125% and 124% [

42]. Spiking corn prices in mid-2012 have led many observers to suggest a reduction in ethanol production in the United States would lead to a smaller increase in food prices [

43].

It should be noted that prices of internationally traded commodities are no respecter of international boundaries. The rapid expansion of ethanol in North America has caused grain prices to increase in other countries just as surely as if the ethanol expansion had occurred there. That means that farmers around the world experience nearly the same grain and oilseed price increases regardless of whether or not ethanol production increases in their own countries.

While grain and oilseed prices increased between 2006 and 2008, this does not necessarily imply that net farm incomes increased. What is important is not gross income but net income, i.e., gross income minus total costs of production. In anticipation of higher returns from corn, land prices and rents have risen rapidly in the United States and Canada. Because of increased demand, prices also rose for all other inputs necessary for corn production, such as fertilizer, equipment and storage. While corn prices were increasing, market processes rationed the demand for inputs in corn production by way of higher prices.

Due to the competitive market structure of the grains and oilseeds sector, higher commodity prices, whether achieved through the market or through government policy actions, result in higher prices for land with little or no improvements in the net returns to agricultural labour [

44]. This already has been happening in the United States where it was reported In the 12 February 2007 issue of Agri-week that a 230-acre field in eastern Iowa sold at auction for a record for the state of US$6,010 per acre (US$1.38 million), cracking a mark that had stood for only two weeks at US$5,350. In Canada, farm land prices also have increased. The capitalization of higher farm revenues into land prices also extends to other farm assets such as equipment and buildings. Under these circumstances, higher revenues do not yield higher net farm incomes. On the contrary, they boost the demand for farm assets and increase the cost structure of the entire industry. While increased asset values improve the equity position of property owners, tenants and farm workers are likely to receive little benefit and aspiring farmers face higher entry costs.

An inevitable and undesirable result of rapidly expanding ethanol production is that livestock producers incur higher costs of their major input—feed grain. Higher feed costs for livestock have had three major effects. First, some part of the increased feed costs inevitably has been borne by producers of calves and weanling pigs. To offset higher feed costs, feedlot enterprises bid lower for feeder animals, which not only reduce the quantity of feeders offered for sale, but also provide feedlot owners with an incentive to buy heavier feeder cattle and to reduce the weight at which fed animals are sold. Second, in response to the potential decrease in supply of meat due to higher production costs, consumers face higher prices for meat products. This reduces consumption of meats both domestically and abroad. Third, higher costs are faced by canola crushers, flour millers, and other users of grains and oilseeds. Profitability in the beef feedlot business in Alberta, Canada, the largest beef producing region in the country, was devastated during the two year period when crop prices spiked upwards.

There seems to be little question that the ethanol industry has affected the costs and returns of primary agriculture throughout Canada. With the higher grain and oilseed prices, more money has come into agriculture. However, not everyone has gained, and the persistence of low net farm incomes has not been relieved.

4.3. Rural Development

Policies implemented by government commonly are evaluated in terms of how many jobs they create. Having a local ethanol plant boosts employment opportunities for nearby residents. Relatively high-paying positions at biorefineries provide incentives for young people to stay in their community. However, measuring the net economic impacts created by ethanol plants has been a problem. According to Swenson [

45], there has been a tendency among researchers and proponents of the biofuel industry to overstate, over describe, and outright double count economic activity linked to the production of ethanol.

Husky Energy’s ethanol plant at Lloydminster, Saskatchewan produces about 130 million litres of ethanol per year and employed 26 full-time workers when it opened in late 2007 [

42]. It is often stated that every new ethanol job under average rural conditions can lead, on average, to three more jobs in a rural region. However, even this modest outcome is somewhat tempered as these gains in employment are gross gains, not net gains. The difference is important.

Certainly, some local businesses and workers benefit in a region where a biofuel plant is located. It gives advantages to the landowners of the region who have an additional market for their crops and to those who have made local investments that cannot be transferred elsewhere without a diminution of their value. The benefit also spills over into surrounding regions. The totality of the benefits represents the gross gain.

However, other changes occur within a region when a business locates or expands as a result of government intervention. Ethanol plants increase the local wages of skilled and unskilled labour, which places pressure on other nearby enterprises to raise the wages they offer for skilled and unskilled labour. In response to higher wages, the other businesses have an incentive to reduce the number of hours or the quantity of labour they employ.

It is clear that increased ethanol production has caused feed grain prices to increase, which in turn has reduced the profitability and eventually the size of the livestock sector and, possibly, the livestock transportation and processing sectors. The gross benefits then are reduced by the reductions in employment and income in other sectors. For this reason, net gains generally are much smaller than the gross gains and may even be negative if the livestock industry is diminished enough (though some regions may gain while other regions suffer losses). As a result, expansion of ethanol production in Canada has led to only a small gain in rural employment and economic diversification though it undoubtedly boosted the local economies of the communities where new facilities were built.

5. Summary and Recommendations

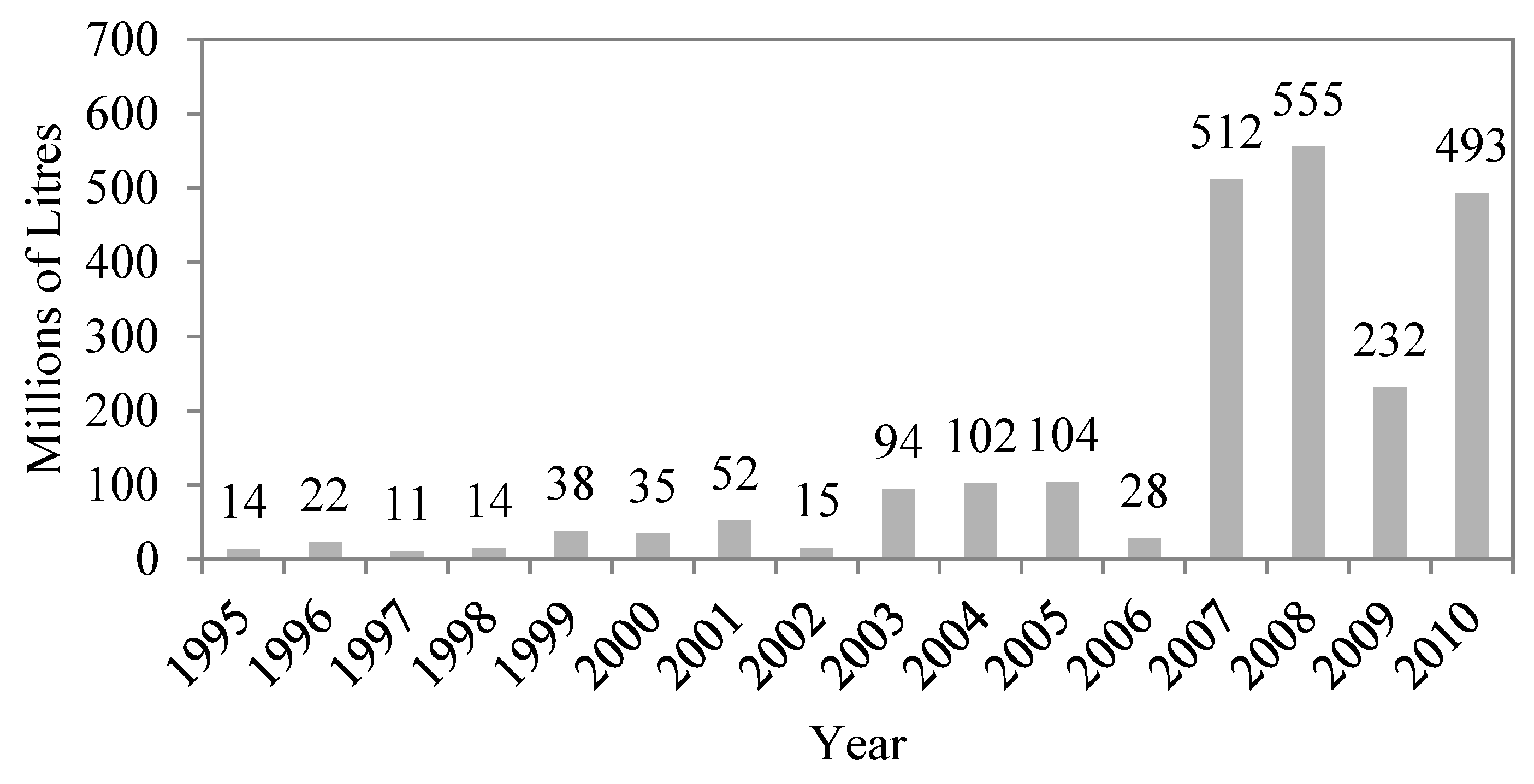

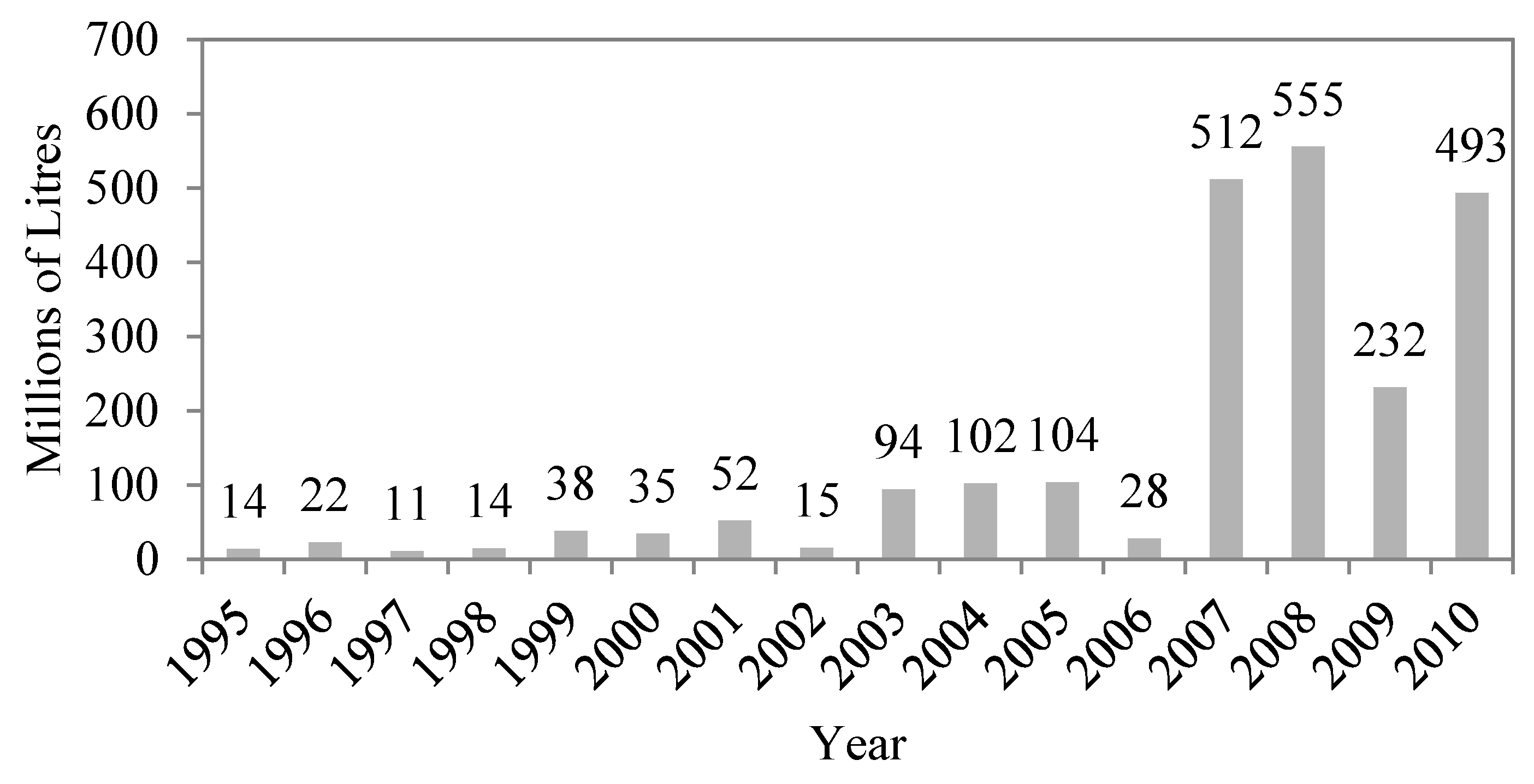

The production and use of biofuel has been increasing rapidly throughout the world, particularly since the turn of the century. In the year 2000, total world production of ethanol for fuel was less than 20 billion litres and by 2005, production had more than doubled to around 40 billion litres [

10]. This provided about 2.8% of the motor gasoline use in the world, with a slightly smaller percentage in North America [

10]. By the end of 2011, total ethanol production in the world had risen to 85 billion litres [

46] and accounts for about 5% of motor gasoline use [

10].

While the costs of producing biofuels are relatively easy to measure, the benefits are much more difficult to quantify and, therefore, the market price does not adequately reflect the benefits of biofuels [

10]. Undoubtedly, there are some clear benefits that stem from the use of biofuels in place of fossil fuels. Biofuels lower greenhouse gas emissions, reduce air pollution (though there are increases in certain pollutants, especially nitrogen oxides), and improve vehicle performance. In countries that are net energy importers (e.g., United States, western European countries, Japan, Brazil), domestic production of biofuels offer some degree of energy security even though the reduction in oil imports through this method might entail some additional costs.

The cost of producing ethanol and bio-diesel in countries where land and labour prices are relatively high (as in Canada) discourages establishment of a biofuel industry. The relatively high costs can be overcome by subsidies, of course, but large income transfers from more productive sectors of the economy might not be in the country’s best interests. Although large profits have been made in U.S. ethanol plants when ethanol prices were high and corn prices were low), it cannot be assumed that this situation will prevail into the long run. Since existing and new ethanol plants in the United States have received fairly large government transfers, it is unclear the extent to which this profitability would have inspired investment in new plants in the absence of the subsidies.

Canada is a large net exporter of energy so does not need a biofuel industry to help ensure energy security. Thus, the arguments for supporting development of a biofuel industry must rely mainly on reducing greenhouse gases and certain air pollutants, and increasing agricultural incomes and rural development. The evidence is overwhelming that there are much less expensive ways to reduce greenhouse gases than by producing ethanol from grains or bio-diesel from canola/rapeseed. Only in Brazil (and possibly some other low income countries) where the average cost of producing ethanol from sugar is much lower than in the high income countries is the cost per tonne of CO2 reduction reasonably competitive with other methods of reducing greenhouse gases. Production of ethanol from cellulosic materials (when large scale commercial production becomes possible) would substantially reduce the cost per tonne of CO2 reduction.

What about using the development of a biofuel industry as a rural development initiative? Certainly, primary grain and oilseed producers often struggle financially in Canada and much of the rural infrastructure is running down as a result. This is a complicated issue and not easy to analyze. There is some evidence that commodity prices would be increased by a small percentage if a large-scale biofuel industry could be established. However, due to the competitive market structure of the grains and oilseeds sector in Canada, it is well known that most improvements in commodity prices, whether through the market or through government transfers, result in higher prices for land with little or no improvements in the returns to agricultural labour. Of course, increases in equity (through higher valued farmland) can have some positive spin-offs for the rural economy.

Establishment of a major biofuel industry in the rural areas of Canada certainly would provide some additional jobs in the rural areas. In Brazil, for example, it has been estimated that 700,000 jobs have been created in rural areas to support the additional sugar cane and ethanol industry [

10]. However, Canada does not have the high levels of unemployment and underemployment that characterize Brazil. While some surplus labour is available in rural areas on a seasonal basis (mostly during the winter), the reality is that most permanent jobs in new ethanol production facilities could be filled only by attracting labour away from existing jobs. This would be an improvement in Canada’s welfare if the new industry was competitive and could produce profitably without government assistance. However, if substantial subsidies were required to establish the industry, then jobs created by this method would very likely lower the nation’s overall welfare rather than increase it.

Despite the extensive biomass resources that exist in Canada, it appears that Canada has a comparative disadvantage in the production of biofuels. However, if the Canadian public desires to replace some portion of its fossil fuels by ethanol and bio-diesel, every effort ought to be made to do it as inexpensively as possible. A high priority should be to encourage imports of biofuels from places where they can be produced less expensively (e.g., Brazil, India, Thailand, Philippines, etc.). If tariff and non-tariff barriers were removed, it is likely that many plants in the low income countries would be eager to supply a growing demand for these biofuels in Canada. This would also promote economic development in these low income countries by giving them a potentially lucrative market for their products.

Although it seems obvious that biofuels can be produced less expensively in developing countries, the Canadian public may still wish to establish a large-scale biofuels industry in Canada. To this end, close attention should be paid to three important economic factors to allow the industry to develop in a competitive environment.

First, every effort should be made to remove inter-provincial barriers to trade and let the industry become established in the most profitable locations. Associated with the location issue, local governments ought to refrain from offering subsidies to influence decision makers regarding the location of prospective plants.

Second, the subsidies for small plants ought to be terminated. Regulations that promote the building of small plants (as in Saskatchewan) may be suitable (and even profitable) in specific circumstances, as when an ethanol plant is associated with an adjacent feedlot. However, widespread establishment of small plants is likely to result in a much higher cost, and ultimately unsuccessful, industry.

Third, much work remains to be done to identify and remove regulations (or change certain institutions) that currently are in place to ensure adequate functioning of a supply chain for grains and oilseeds on the one hand, and to deliver gasoline and diesel fuel efficiently to consumers on the other. In the grains and oilseeds sector, plant breeding, registration of new cultivars, grain handling and storage procedures, etc. are heavily regulated and oriented to efficiently deliver high quality food and feed to consumers. Present procedures discourage (or prevent) the growing of plants that have higher yields of low quality grains (for food or feed stocks for biofuel production) and longer stemmed varieties (that would lower average costs of producing cellulosic materials). Since ethanol is hydroscopic and a solvent, it must be transported, stored and distributed in specialized containers, which rules out the use of existing pipelines to transport product. A major investment in handling infrastructure would be required to grow the industry much beyond its present size. The biofuels industry in every country including Canada is integrally related to the agricultural industry. Subsidies, price supports, tariffs and non-tariff barriers to trade bedevil the agricultural industry and make it very difficult to analyze the costs and impacts of any biofuel policies that also affect the agricultural industry. Like research in the biological and chemical areas on biofuels, research in the economic area is at least as important and at least as difficult to conduct. This does not mean that economic research should be avoided. On the contrary, the future welfare of Canadian citizens depends greatly on policy decisions taken by governments and the decision-making process can be improved if properly researched economic information is conducted and made available.

{kind=link}