1. Introduction

In developing countries, a huge amount of waste is not reused or properly disposed of by firms (Gunasekaran & Spalanzani, 2012) [

1]. This practice has led to the problem of hazardous waste management, and locating new landfills, as a result of depletion of raw material (Gunasekaran & Spalanzani, 2012) [

1]. Periathamby et al. (2011) state that solid waste generation and its implications for society and environment are global issues, with the complexity of waste composition and ever-increasing per capita waste generation becoming a challenge for managers, particularly in developing countries [

2]. Due to the lack of effort by authorities, the management of waste has become a persistent problem, despite that the largest part of municipal expenditure is allotted to it (Das & Bhattacharyya, 2015) [

3]. However, the collection of waste generated has not yet solved the issue of hazardous waste management; it requires disposing of waste in an environmentally safe and economically sustainable manner (Das & Bhattacharyya, 2015) [

3]. It is, therefore, noted that the issue of waste management needs serious attention.

Environmental and waste management related research in South Africa have focused more on disclosure (Fienh & Ball, 2005; Mitchell & Hill, 2011; Raufflet et al., 2014; Costantini et al., 2013; Du Toit, 2016) but none of these prior researchers has looked into the effect of waste management expenditure and waste reduction in South Africa [

4,

5,

6,

7,

8]. Researchers such as Lopez-Gamero et al. (2012), Guerrero Maas and Hogland (2013), Clor-Proell and Maines (2014), conducted studies that examine the effect of environmental practices and firm performance in other countries [

9,

10,

11]. Therefore, this study becomes necessary to address the issue of waste management among selected stakeholders within the manufacturing sector in South Africa, since they are considered substantial contributors to waste generation.

Notwithstanding, there are greater social demands on firms to reduce their environmental impact because of the related environmental problems caused by firms’ operations (Contantini et al., 2013) [

7]. Shaw (2012) states that many environmental issues have accompanied the growth in the South Africa economy [

12]. Fienh and Ball (2005) mentioned that in the past poor waste management, as one of the key environmental issue in South Africa has been uncoordinated and poorly funded [

4]. Barcena-Ruiz and Casado-Izaga (2015) reiterate that production and distribution of goods result in waste and rubbish that firms must plan to dispose of, and the disposal of waste material is expensive, as waste must be transported to collection points [

13].

A cornerstone of sustainability of any business is the establishment of an affordable, efficient, and truly sustainable waste practice at the operational level (Kulkarni et al., 2014) [

14]. However, waste management activities, like segregation, collection, treatment, and disposal, still need to be done (Shalini et al., 2012) [

15]. Implementation of appropriate waste management practices requires reliable waste statistics (Metin et al., 2013) [

16]. The data should represent a sufficiently long time frame, with relatively short measurement frequencies, to be statistically acceptable (Gow et al., 2016) [

17]. In the waste management process, segregation practice needs to be practised more strictly, and by the waste generators themselves (Shalini et al., 2012) [

15]. There may be many aspects of waste management practices as can be noted from the literature (Metin et al., 2013; Shalini et al., 2012; Kulkarni et al., 2014 and Gow et al., 2016) [

14,

16,

17]. In their study, waste management practices refer to the action taken by companies to remedy issues of the environment. Among other environmental problems, the study focuses on the waste reduction.

Society is facing several environmental challenges, due to a massive increase in production services aspects (Kulkarni et al., 2014) [

14]. Challenges, such as carbon emissions, increase negative environment impacts (Mihai & Ingrao, 2016) [

18]. These challenges are the result of bad practices, which represent a threatening factor for both the local environment and public health, and cause major losses regarding compositing recycling or energy recovery potential (Mihai & Ingrao, 2016) [

18]. According to Hornsby et al. (2016), environmental challenges surrounding the effect of the current waste management practices have received a high level of public attention, due to the continuous problems in establishment and implementation of effective waste management since the mid-1990s [

19]. Researchers such as Caspersen (2015), and Qian and Schneider (2016), found that practices had positive influences on the financial performance [

20,

21]. Therefore, firms need to consider proper waste management practices to perform well financially.

According to Gangolells et al. (2014), most commonly implemented waste management practices were found to be on the side of cleanliness and correct storage of raw materials; such practices encourage prevention of waste and waste diversion from wild dumps (Mihai & Ingrao, 2016) [

18,

22]. Bisschop (2006) and Hafeez et al. (2016) also found that a common practice to reduce the volume and to recover metals and plastics, is dumping waste in an open ground and burning of waste [

23,

24]. From the above literature, the importance of sound waste management practices cannot be ignored. Moreover, it is plausible that firms need to maintain sound financial performance through proper waste management.

This study examines whether waste management expenditure has an impact on waste reduction targets, and also considers the impact of waste reduction targets on firm’s profitability. There is relevance for this study, given the importance attached to environmental protection by the South African government. From the arguments above, there is little previous research evidence about waste reduction targets and their effect on waste management expenditure, and profitability of the manufacturing sector in South Africa.

The following section describes the theoretical framework used, and the identified literature.

4. Method

The study sampled 30 firms consistently listed on the Johannesburg Securities Exchange Socially Responsible Investment (JSE SRI) Index for a period of 10 years (2007 to 2016). The study used a combination of firms from both the mining and manufacturing sectors, because these sectors are considered to be high on waste generation, and they are consistently listed on the JSE SRI Index for the period under consideration. The use of a sample of 30 firms from more than one sector is believed to enhance the study and give robustness to the analysis. Moreover, the JSE SRI Index is a reputable source of reliable financial and non-financial information.

The causal research design was adopted because it measures the correlation between variables and the impact a specific change will have on existing assumptions. Scholars like Cohenet al. (2013); De Franco et al. (2013); Clor-Proell and Maines (2014); Heckman and Pinto (2015); and Gow et al. (2016); have used the causal research design [

11,

83,

84,

85].

Information available on the JSE SRI Index is valid and reliable. However, JSE listed firms are expected to comply with the strategic framework governing waste management in South Africa, such as the Air Quality Act (Act 39 of 2004) and the National Environmental Management (Waste Act, 2008 (59 of 2008) [

86,

87]. The study used the quantitative method to determine the correlation between two variables. The panel data method of analysis was considered appropriate for this study. The regression equation is as follows:

where:

WRTit = Waste Reduction Targets

αi = Intercept

β = Slope

WMEit1 = Waste Management Expenditure

FPit2 = Firm’s Profitability

∆TURNOVERit3 = Change in Tunrover

LEVERAGEit4 = Leverage

In this study, waste reduction targets (WRT) was used as a dependent variable, and independent variables are waste management expenditure (WME) and firm’s profitability (FP). Change in turnover and leverage are control variables since different characteristics of a firm can affect both a company’s waste management expenditure and waste reduction target in various ways. The analysis of the effect between waste management expenditure and waste reduction target alone does not justify the findings from this study. Previous researchers used to control variables in their studies to justify their findings (Galbreathe & Shum, 2012; Saeidi et al., 2015; Henri et al., 2016; Chen et al., 2016) [

62,

65,

88,

89]. The objective of using control variables is to control for factors that may influence the regression result. Therefore, this study considered leverage, and change in turnover, to be control variables. Prior studies, such as Danso and Adomako (2014), and Fosu et al. (2016), used leverage as a control variable, and the study of Chen et al. (2016) used change in turnover, among others, as a control variable, in their study of understanding the relationships between environmental management practices and financial performances of multinational construction firms [

65,

90,

91]. In line with prior studies, such as Nyirenda et al., 2013, and Panagiotidou et al. (2015), the study used two-panel data techniques, namely, fixed-effects model, and random-effects model [

79,

92]. The Hausman test is used to identify if the individual effects are random.

5. Results

This section presents and discusses the findings of the study.

Table 1 above shows 300 observations for 10 years for 7 manufacturing firms and 21 mining firms listed on JSE SRI Index. The mean of the dependent variable, waste reduction targets (WRT) was 5.4812, while those for the independent variables, waste management expenditure (WME) and firm’s profitability (FP), were 0.9763 and 2.811257, respectively. Moreover, the mean of the control variables change in turnover and leverage, were 4.36147 and 1.8838, respectively.

The standard deviation measures the dispersion of variables; for this research, it shows the standard deviation for waste reduction targets of 12.33445, waste management expenditure has a deviation of 2.587124, and firms’ profitability has a deviation of 64.54298. While on the other hand, the control variables change in turnover and leverage, have a deviation of 11.90228 and 11.52015, respectively.

As seen in

Table 1 above, the minimum and maximum for waste reduction targets are 0 and 87.34, waste management expenditure is 0 and 12.38, and for firm’s profitability, −493.51 and 815.48. However, change in turnover, as one of the control variables, has a minimum and maximum of −36 and 50. The other control variable leverage has a minimum and maximum of −32.47 and 155.65.

Table 2 presents the results of the independent

t-test of the study variables.

Table 2 shows an independent

t-test using a sample of 600 combined

obs of independent variables (IVs) (change in turnover and leverage) to determine if they influence waste reduction targets differently. This test determines whether the means of the population are equal or not. In this case, it is appropriate to test the control variables, as they are independent, and of a different population. Both IVs consists of 600 randomly-assigned observations. The results indicate that leverage had a statistically significantly lower

influence on waste reduction targets compared to the change in turnover

. Therefore, change in turnover and leverage were not statistically significant to influence waste reduction targets.

Table 3 shows the correlation between individual variables.

As seen from

Table 3 above, the correlation between dependent variable waste reduction targets and itself is a perfect 1.0000. The same applies to the independent variables, waste management expenditure and firms’ profitability, which were also 1.0000.

Table 3 also shows a positive correlation between waste reduction targets and waste management expenditure of 0.0919.

Table 4 below presents the multiple linear regression of the variables.

From

Table 4 above, the significant statistics to note is the adjusted R-squared. As the significant levels have been set to 95% confidence, the adjusted R-squared shows −0.11% level. This renders the regression as insignificant. A further analysis tested the variables for significant factors that could affect the regression, multicollinearity (see

Table 5) and auto-correlation below. The results below present the autocorrelation test.

Autocorrelation test (Durbin–Watson statistics)

Source: author’s results of Durbin–Watson test from Stata.

The Durbin–Watson test was performed to test the autocorrelation within the panel data. It is appropriate to enhance the reliability of the regression results, as the number of observations may give rise to the effect of autocorrelation, which may affect the authenticity of the panel regression. The Durbin–Watson statistic is between 0 and 2; if the results are close to 2, it means there is autocorrelation, and if the results are close to 0, it means there is no autocorrelation.

From the results in

Table 5, show the Durbin–Watson of 0.7106506, which is closer to 0. This means that there is no autocorrelation within the variables of the study.

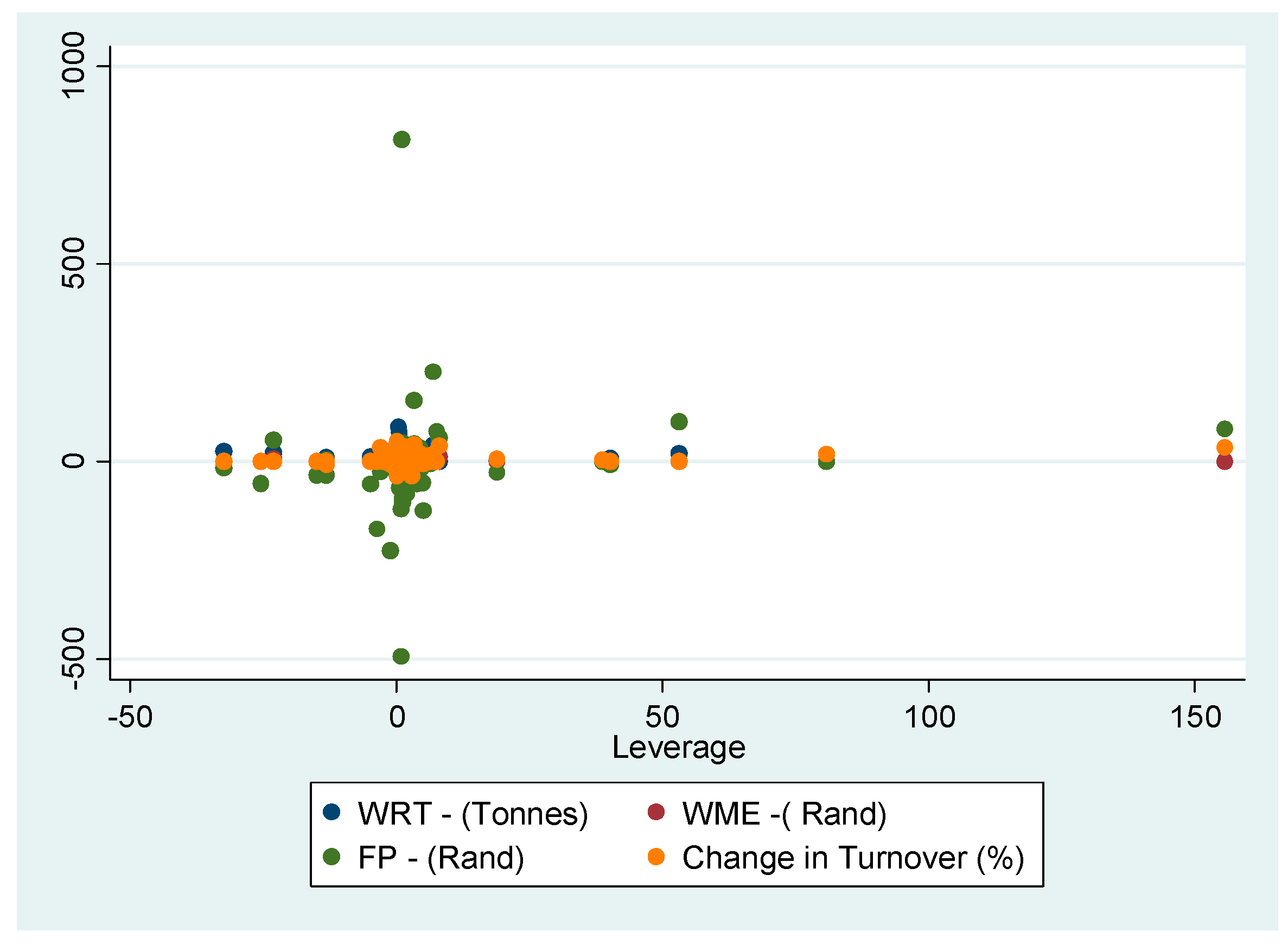

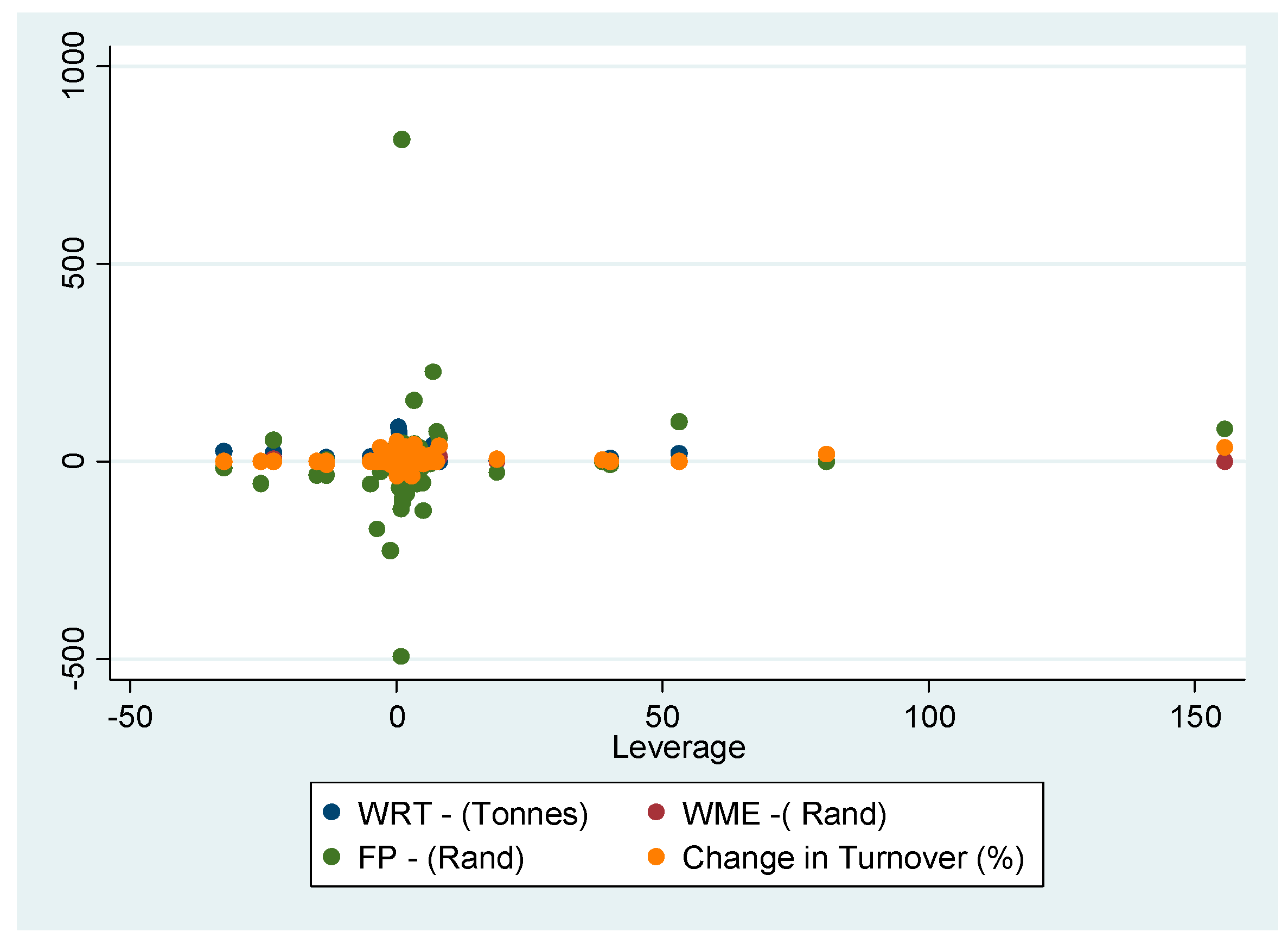

Figure 1 presents the scatter plots for the variables.

For enhancement of the regression validity, the multicollinearity test was performed. Multicollinearity can create a problem in regression, as it can lead to a situation where the independent variables are closely correlated with one another, leading to a bias in the probability values (

p-values). In testing for the presence of multicollinearity, the variance inflation factors (VIF) test was performed in Stata. This test measures how the standard errors inflate the coefficients in the regression model, leading to a bias in the

p-values. An ideal VIF should not be more than four times the square of the standard errors. Therefore, based on the mean VIF (1.03) and the individual VIF of the independent variables as shown in

Table 5, no multicollinearity is present.

The result below shows the results for heteroscedasticity test.

Breusch–Pagan/Cook–Weisberg test for heteroscedasticity

Source: Author’s results of heteroscedasticity from Stata.

According to Williams (2015), if error terms do not have constant variance, they are said to be heteroscedastic, on the other side, when the variance of the error term is constant, it is called homoscedasticity [

93]. A large chi-square would indicate heteroscedasticity (Williams, 2015) [

93]. In this study, the chi-square is 0.0186. Therefore, heteroscedasticity is not present.

Table 6 presents the correlation matrix of coefficients of regress model.

Table 6 above shows the correlations between the variables. All variables are perfectly correlated with each other (1.0000). However, the correlation between waste management expenditure and firm profitability is shown as −0.1010. Overall, results show a correlation closer to 0.000, hence no multicollinearity is present.

Table 7 and

Table 8 present the panel data results using the fixed effects model for waste reduction targets.

From

Table 8 above, the relevant results to take note of are the

p-values and the coefficient of the regressors. The significance level is set at 95% levels, with

p-values greater than 0.05 considered to be insignificant, similar to other waste management studies (Worku & Muchie, 2012; Licy et al., 2013; Kishore et al., 2014; Richter et al., 2017) [

94,

95,

96,

97]. The result above shows that there is a positive, but insignificant, relationship between waste reduction targets and waste management expenditure represented by a coefficient of 0.373839 and a

p-value of 0.207. Therefore, the result reveals that waste management expenditure has a negative and insignificant association on waste reduction targets. A positive and insignificant relationship between waste reduction targets and firms’ profitability is also reported from the results.

Moreover, the results show that there is a negative correlation between change in turnover and waste reduction targets, indicated by −0.02779 coefficient and a

p-value of 0.610. Lastly,

Table 8 also shows that there is a negative correlation between leverage and waste reduction targets, represented by a coefficient of −0.00204 and

p-value of 0.971.

Table 9 and

Table 10 below show the results for the random effects model for waste reduction targets.

From

Table 10 above, the relevant statistics to take note of are the coefficient and the

p-values. The significance level is set at 95% levels, with

p-values greater than 0.05 interpreted to be insignificant. The results show the coefficient of 0.389756 and

p-value of 0.164. The findings show that there is a positive, but insignificant, association between waste reduction targets and waste management expenditure. This indicates that any increase in waste management expenditure will lead to an increase in waste reduction targets by 38.98%.

Moreover, the results show that there is a negative correlation between change in turnover and waste reduction targets, demonstrated by the coefficient of −0.03061 and p-value of 0.565. Furthermore, the results also show that there is a negative correlation between leverage and waste reduction targets, represented by a coefficient of −0.00634 and p-value of 0.909.

In deciding between the fixed effects model and random effects model for waste reduction targets, the Hausman test is appropriate, where the null hypothesis confirms that the preferred model is the random effects model, while the alternative is the fixed effects model.

Table 11 below presents Hausman test results for waste reduction targets.

The results from

Table 11 above from the Hausman test run, indicate the use of random effects model, since prob > chi

2 = 0.9899 is greater than 0.05. Therefore, the study used the results from random effects model to establish the relationship between waste reduction targets (dependent variable) and the independent variables (waste management expenditure and firms’ profitability). The following section discusses the findings.

7. Conclusions

The overall results of this study showed that there is a significant link between waste management expenditure and waste reduction targets in the waste management systems for improved environmental performance of companies. As evidenced from existing literature, no prior studies regarding the impact of waste reduction targets on waste management expenditure and companies’ profitability have been carried out within mining and manufacturing firms in South Africa. The results, thus, are important in adding to the waste management/financial performance debate, particularly in the context of an emerging African economy, like South Africa. Three theories, namely the waste management theory, stakeholder, and legitimacy theories, provided insights into the thinking of scholars in this study area. The WMT confirms the relevance of setting waste reduction targets, which are influenced in this study by waste management. This shows that in achieving the desired waste reduction target, firms need to invest in its management. The study noted that when firms manage their waste effectively, it leads to good ethical behavior and a consideration of their stakeholders’ interest. Waste management theory indicates that moving towards waste reduction requires that the firms commit themselves to increase the proportion of non-waste leaving the process. Moreover, legitimacy theory encourages firms to take care of the waste generated, to act in the best interest considering norms and values of society; this is true because it is the legitimate thing to do. Moreover, the stakeholder confirms that by investing more in waste management, firms are responsive to the needs of its stakeholder by reducing the volume of waste that ends up in the landfill.

The study explained the adoption of quantitative methods, which helped the researcher to address the objectives of this study. The study adopted a causal research design. With the casual research design, the study was able to address the impact of waste management expenditure on waste reduction targets, and the relationship between waste reduction targets and firms’ profitability. The study used the mixed method approach. The approach was appropriate for this study because it enabled the researcher to test for possible relationships between waste management expenditure (measured in Rand) and waste reduction targets (measured in tons), and also, to examine the impact of waste reduction targets on firm’s profitability (measured in Rand).

Data was sourced from published integrated financial and sustainability reports of the selected mining and manufacturing firms. The researchers firmly believe that the adoption of the methods mentioned above is appropriate to fulfil the objective of this study.

The study used the South African mining and manufacturing sectors as the population, because it was easy to obtain valid and comparable sustainability reports and integrated annual financial statements from the JSE and the companies’ websites. The mining and manufacturing sectors were chosen, among other sectors, because firms within these sectors have the most influence on waste generation in both the environment and society.

The control variables were described. The objective of using control variables is to control for factors that may influence the result of the regression analysis. Leverage and change in turnover were used as control variables in the study. The panel data analysis was discussed.

The results revealed that there is a positive association between waste management expenditure and waste reduction targets. Moreover, results show an insignificant positive association between firm’s profitability and waste reduction targets. On the other hand, the study used legislative documents to explain the data, to ensure consistency with the results of the statistical analysis. From the explanations, the study shows an overview of South African manufacturing firms’ waste reduction strategies, compliance with mandatory legislation, and voluntary waste management guidelines and the ISO 14001 were also explained, about the practices of the firms.

South Africa has its regulations, like other countries in the world, to protect the environment, health, and well-being of those who live in it. The study found that firms in the study are fully compliant with the legislations. In doing so, the firms avoided possible penalties by protecting their reputation from the various stakeholders. Lastly, firms in this study are voluntarily engaging with their stakeholder. Results indicate that most firms are working towards reducing the amount of waste produced in their production processes with the objective of achieving a sustainable environment.

The results of this study added to the existing knowledge and literature on the waste reduction and waste management. The study has paved the way for further research in the field of waste and waste management.

This study has limitations. The paper used sustainability reports for analysis; therefore, our results cannot be generalized. The study used those mining and manufacturing firms that were consistently listed on the JSE SRI, and these were 30 in total. Other researchers may use other sectors, and they can also use a larger sample. Many firms that are operating in South Africa are not listed under the sectors mentioned above, and as a result, the findings of this study, therefore, may not be fully representative of the mining and manufacturing sectors in South Africa.

From the study, one can note that waste information and waste management are of critical environmental concerns. This study paved the way for other future researchers in the waste reduction and waste management area. Future researchers may opt for other sectors, and may use an increased number of firms.

{kind=link}