A Generic Framework for the Evaluation of the Benefits Expected from the Smart Grid

Abstract

:1. Introduction

2. Objectives and Benefits of the Smart Grid

2.1. Targets of the Smart Grid

- (i)

- solving problems related to numerous grid operations such as demand/response (DR), automated measurement and control, grid monitoring and physical surveillance, real-time load management, power theft identification, etc.

- (ii)

- ensuring interoperability and security of power supply;

- (iii)

- integrating and managing and all kinds of distributed power generation including renewable energy sources;

- (iv)

- leveraging the electricity market by allowing demand side participation, providing new tariff schemes and facilitating the consumers participation in the free energy market [7].

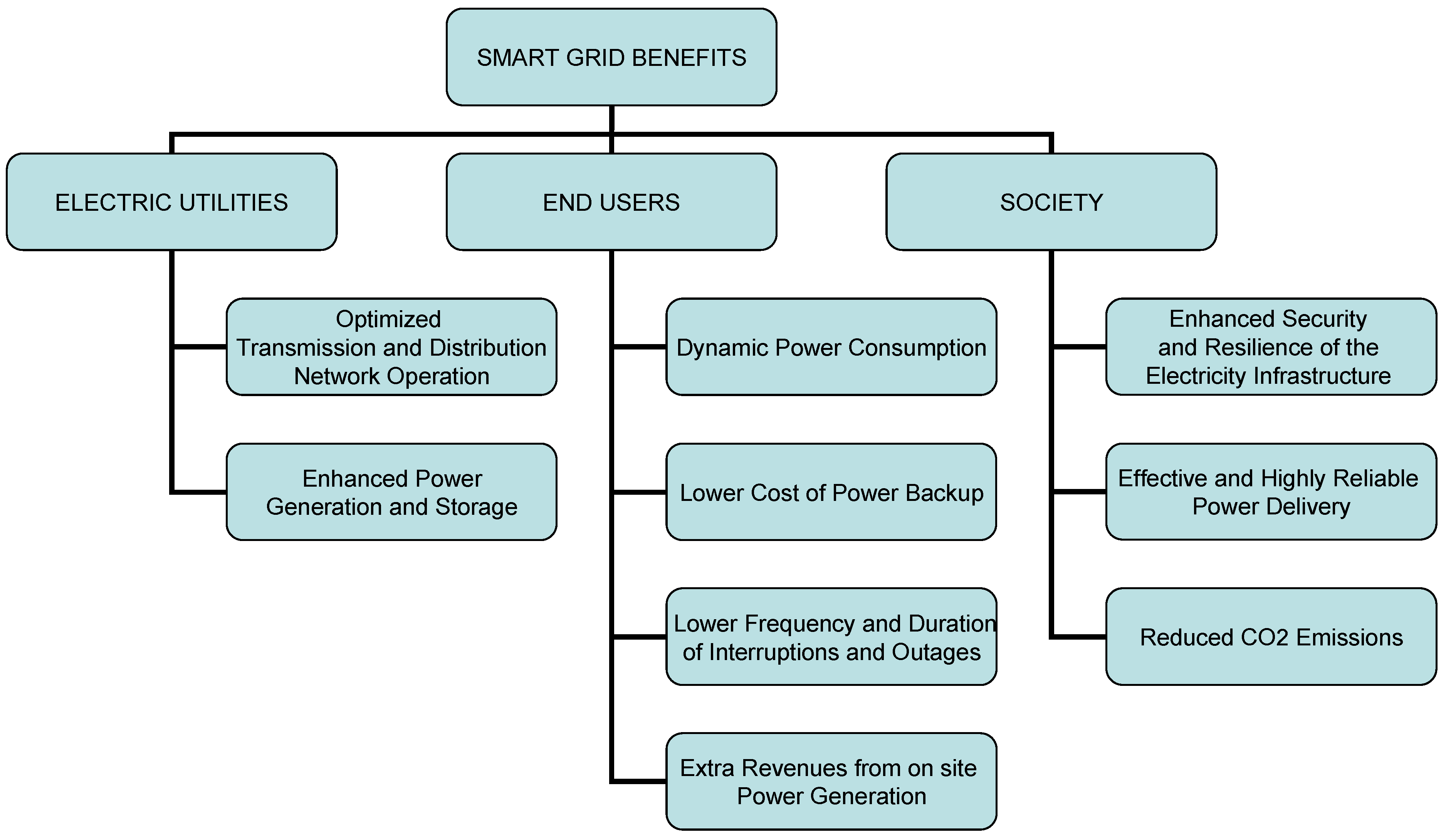

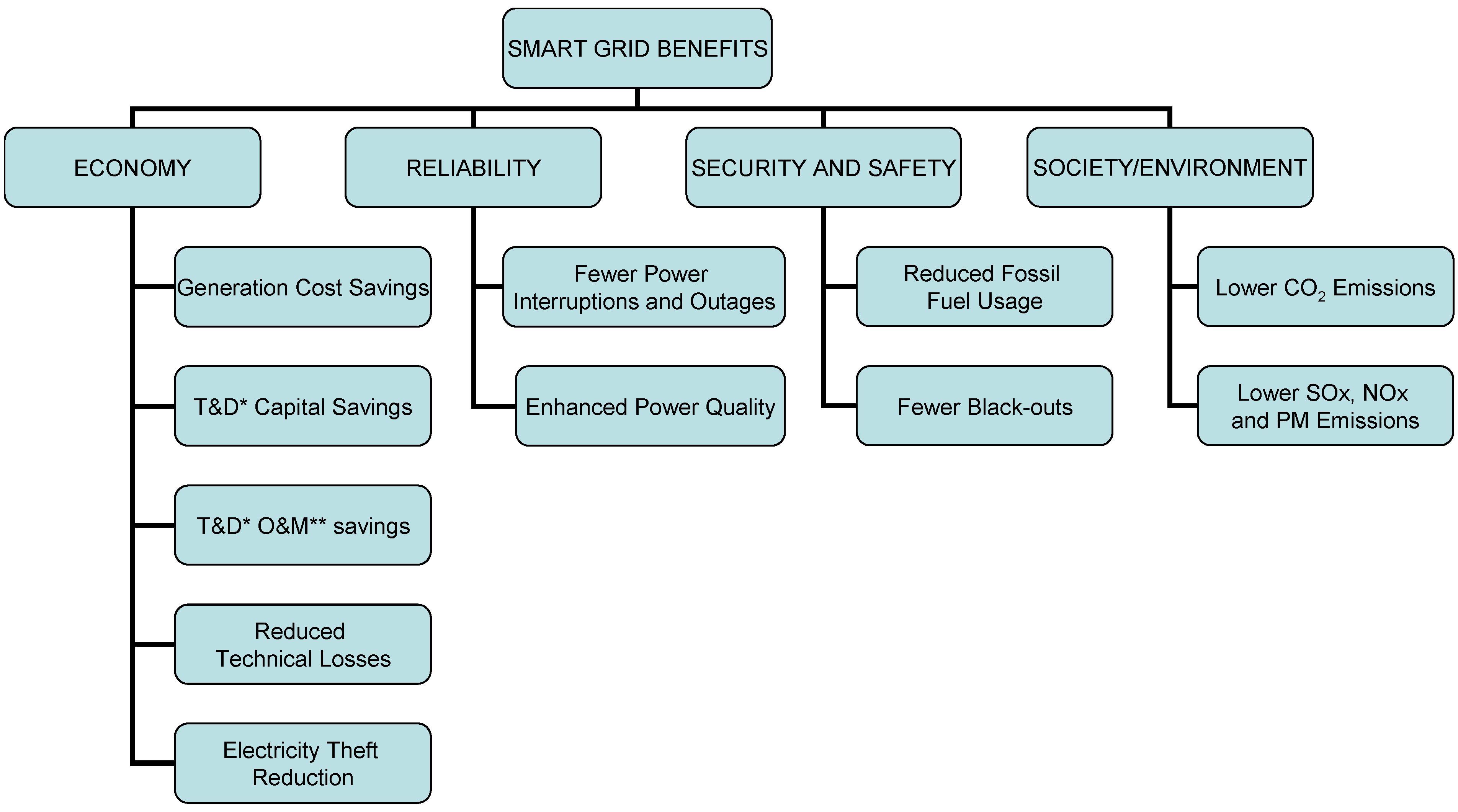

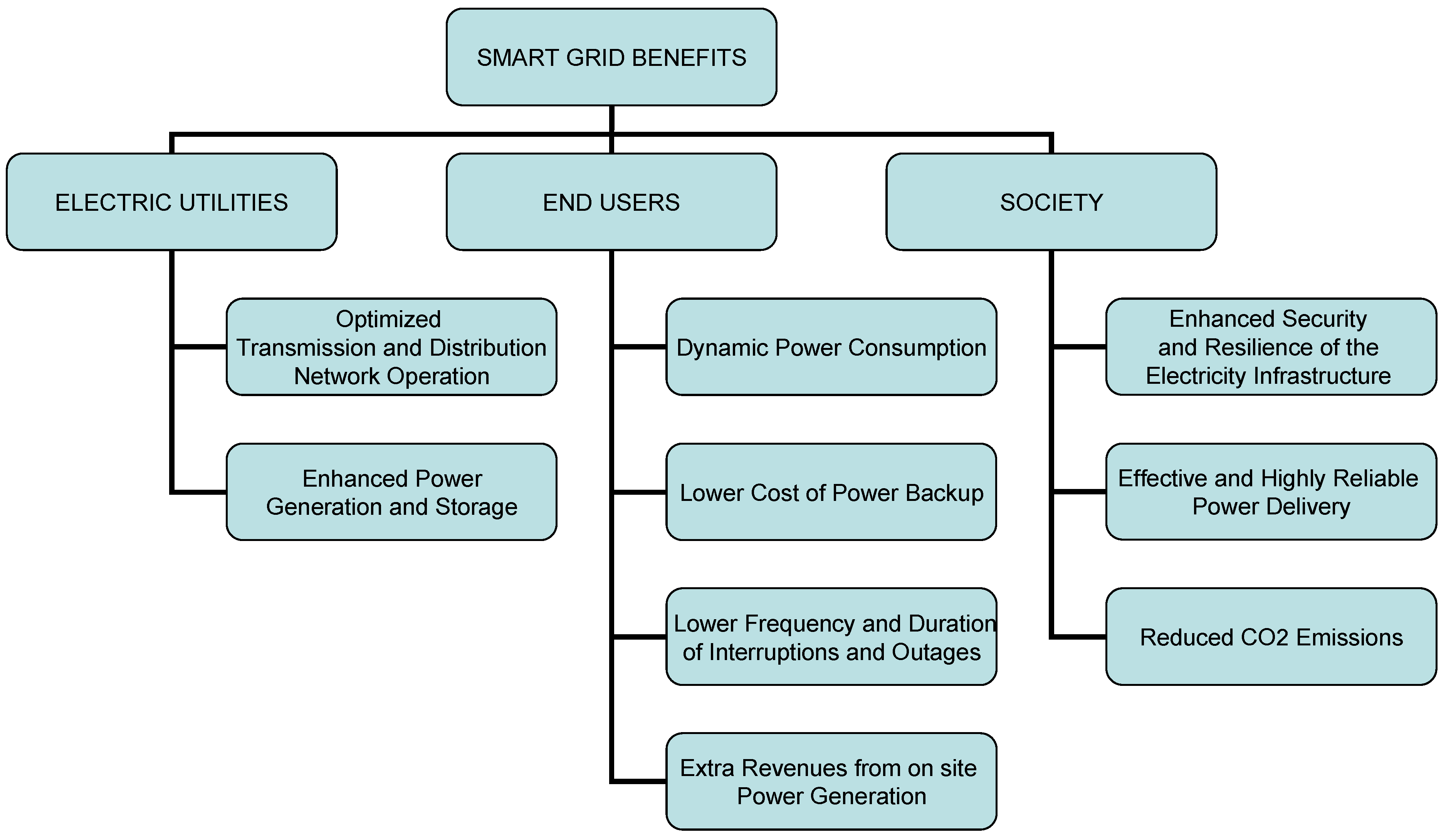

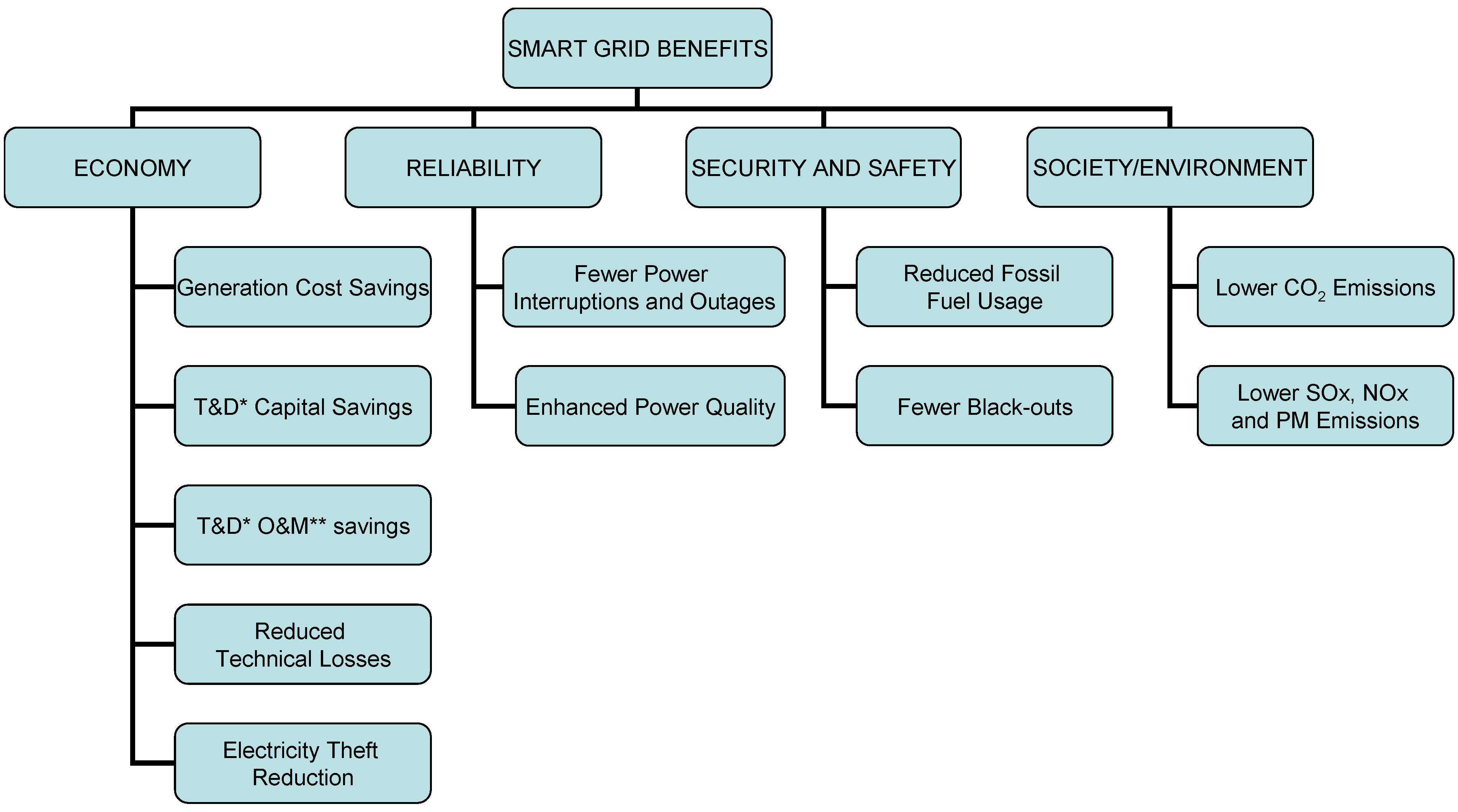

2.2. Benefits Offered to DSOs

- (i)

- Operational: The enhanced observability and manageability of the power system offered by the Smart Grid will allow DSOs to reduce the frequency and duration of power interruptions and outages, thus enhancing system reliability. Also, the preventive grid maintenance facilitated by the Smart Grid is expected to result in fewer component failures [9];

- (ii)

- Economic: DSOs will benefit from the significant reduction offered by the Smart Grid both with regard to the technical losses on the distribution grid and to the peak load. Significant economic benefits will also be offered from leveraging the business opportunities brought in by the Smart Grid due to DR, microgrid operation, etc. In addition to the improved smart metering accuracy and the significant reduction of failures and outages, electricity theft will be drastically reduced and cash flows will improve as a result of timely billing and revenue collection;

- (iii)

- Environmental/social: Lower losses on the transmission and distribution grid will come up due to network optimization. Also, the Smart Grid operation will enhance the seamless incorporation of closer-to-the-load power production from distributed renewable energy generation, thus reducing the proportion of fossil fuel based generation in the overall generation mix. This will result in fewer emissions due to the expected reduction in the use of fossil fuels. Moreover, the integration of intermittent renewable energy generators into the conventional power grid will also help the DSOs to improve their environmental profile by directing power generation towards environmentally friendly methods [10]. Also, the adaptation of power consumption to generation will be beneficial to DSOs since it is important to avoid reinforcement for the integration of photovoltaic and wind generators by reducing the feed-in peak. Through an intelligent and more efficient control of distributed energy resources, backup reserves and other ancillary services, the Smart Grid will maximize the power system capability to manage intermittent power generation [11,12];

- (iv)

- Security-specific: The enhanced monitoring and physical surveillance of the electricity network will increase its robustness and resilience both from a physical and a cyber point of view.

2.3. Benefits Offered to End Users

- (i)

- Operational: By enhancing the power system reliability, the Smart Grid will offer better QoS to the consumers. The consequent reduction in the frequency and duration of power interruptions and outages will be translated in less productivity and business losses for the consumers. Moreover, the ability to collect real-time information will give consumers the opportunity to control their consumption in practically real-time and engage themselves actively in the electricity market [8]. The significant peak load reduction expected from smart grid operation will allow the DSOs to reduce their costs and eventually the prices enjoyed by the consumers;

- (ii)

- Economic: In addition to potential bill savings for all consumers, corporate users may enjoy significant indirect economic benefits as havoc situations that lead to severe losses of productivity will be prevented;

- (iii)

- Environmental/social: Going green will be facilitated as the Smart Grid will enable the consumers to migrate to a more dynamic consumption pattern, thus indirectly leading to reduced energy consumption coming from fossil fuels. Being an essential component of the Smart Grid, smart metering will give the end-users the opportunity to control—practically in real time—the amount of energy they consume and how much they spend every month on their energy bills [13,14]. Demand-side management will enable consumers to adapt their energy consumption and, consequently, the level of the generated power. Moreover, shifting demand away from the peak will lower the peak prices [11,12];

- (iv)

3. Regulatory, Technical and Business Considerations Related to the Smart Grid

3.1. The General Regulatory Framework for DSOs

3.2. Technical Considerations Related to the Smart Grid

3.2.1. Smart Grid Communications

- (i)

- (ii)

- Wireless communication technologies, mainly for the last mile, to connect substations and provide services related to remote metering.

- The power system layer, responsible for the safety and reliability of the distribution network.

- The communications layer intended for the exchange of information between any nodes of the power grid.

3.2.2. Smart Grid ICT Services

3.2.2.1. Critical Services

- (i)

- As the sole responsible for any investment decision on the Smart Grid are the DSOs, should they engage a Telco/ICT solution provider to procure smart grid services or do it on their own?

- (ii)

- What is the most suitable among the available ICT approaches each time?

3.2.2.2. Generic Services

3.3. DSO Business Models Related to the Smart Grid

4. Relating the Smart Grid Benefits to Power System Operation and Business Needs

5. Benefits Expected from Improved Distribution Reliability due to Smart Grid Operation

5.1. A Study Case

{kind=link}

{kind=link}

{kind=link}

| Functions | Benefits |

|---|---|

| Automatic Voltage and VAR Control (F01) | It can be implemented by a DSO based on operating strategies, or in response to local or regional contingency or outage events. It also includes the ability to adjust or optimize the distribution power factor to reduce losses or achieve specific power factor targets. |

| Automatic Feeder Reconfiguration—Single-Level (F02) | Individual feeders can be reconfigured and optimized, including coordinated switching on the primary feeder or its laterals, or with an adjacent feeder. This may be in response to an outage or for peak load control. |

| Automatic Feeder Reconfiguration—Multi-Level (F03) | Multiple distribution feeders in an area may be reconfigured and optimized, including those with tie points to one or more substations. |

| Optimum Power Flow Analysis (F04) | Real-time monitoring and analysis enables distribution operators to make decisions concerning system performance, reliability, power quality, losses and asset utilization. |

| Distributed Energy Resources (DER) Monitoring (F05) | Individual DER units are monitored for status and output; this information is available to the utility staff in near real-time. |

| DER Control by Unit (F06) | Individual DER units are controlled independently by utilities in near real-time to improve distribution system efficiency and performance. |

| DER Control by Class (F07) | Individual DER units are controlled in groups or classes, either by the utilities or third-party operators, in near real-time. |

| Automatic Protection Reconfiguration (F08) | It addresses circuit loading and two-way power flow issues associated with high DER penetration. |

| Isolation of Higher Impedance Faults (F09) | It enables faster isolation of high impedance faults in order to minimize safety hazards and reduce damage to equipment and property. |

| Automatic Switching—Local (F10) | It is used to isolate faulted segments of distribution circuits to reduce the duration and scope of power outages. It can also reduce the time and effort required for crews to travel between switch positions and operate the devices manually. |

| Automatic Switching—Central (F11) | Switches will operate automatically in response to signals from a central distribution management system. |

| Automatic Condition-Based Equipment Maintenance (F12) | Distribution units equipped with sensors that monitor the grid condition and report accordingly increase the reliability and reduce the cost of maintenance. |

| Low-Impact Fault Detection (F13) | It reduces the stress on the transmission and distribution infrastructure prolonging their expected lives and reducing equipment failures. |

| Automatic Islanding and Resynchronization (F14) | It is fundamental to microgrid operation; it isolates loads within microgrids, and enhances the operating flexibility of the utilities in certain areas. |

| Real-Time Communications from the Utility to the Customer (F15) | Utilities can communicate directly with customers in real time to provide information such as price signals, network conditions, restoration times, and safety advice. |

| Automatic Phase Load Balancing (F16) | It provides real-time measurements of customer consumption and manages the load through Advanced Metering Infrastructure (AMI) supporting customers decisions. |

| Real‐Time Communications from the Customer to the Utility (F17). | As in F15 |

| Assumptions Concerning the SAIFI Improvement | Partial (%) SAIFI Improvement |

|---|---|

| Automatic Switching (F10) | |

| Percentage of SAIFI caused by mainline outages | P10,1 = 50% |

| Percentage of previously affected customers that do not experience an interruption | P10,2 = 50% |

| System percentage that employs automatic switching | P10,3 = 50% |

| Percentage of time adjacent feeder is capable of carrying transferable load | P10,4 = 75% |

| Partial SAIFI improvement due to Automatic Switching (P10 = P10,1P10,2P10,3P10,4) | P10 = 9.38% |

| Automatic Condition-Based Equipment Maintenance (F12) | |

| Percentage of SAIFI related to distribution equipment failures | P12,1 = 44% |

| Percentage of equipment failures that are reduced due to early detection | P12,2 = 75% |

| Percentage of equipment that affects SAIFI by monitoring equipment | P12,3 = 75% |

| Partial SAIFI improvement due to Automatic Condition-Based Equipment (P12 = P12,1P12,2P12,3) | P12 = 24.75% |

| Low-Impact Fault Detection (F13) | |

| Percentage of SAIFI caused by this type of equipment failure | P13,1 = 0,5% |

| Percentage of failures reduced by low-impact fault detection | P13,2 = 90% |

| Percentage of relevant equipment employing this capability | P13,3 = 100% |

| Partial SAIFI improvement due to Low-Impact Fault Detection (P13 = P13,1P13,2P13,3) | P13 = 0.45% |

| Automatic Islanding and Resynchronization (F14) | |

| Percentage of customers included in microgrids | P14,1 = 1% |

| Percentage of outages that would be avoided as a result of microgrid formation | P14,2 = 90% |

| Percentage of customers located within the microgrid that does not have lines down. | P14,3 = 50% |

| Partial SAIFI improvement due to Automatic Islanding and Resynchronization (P14 = P14,1P14,2P14,3) | P14 = 0.45% |

| Aggregate SAIFI improvement PSAIFI =P10 + P12 + P13 + P14 − (P10P12 + P10P13 + P10P14 + P12P13 + P12P14 + P13P14) + (P10P12P13 + P10P12P14 + P12P13P14) − P10P12P13P14) | PSAIFI = 32.40% |

| Current SAIFI (# outages) | 1.066 | Change in SAIFI (%) | 32.4 | New SAIFI (# outages) | 0.721 |

| Current SAIDI (min.) | 108.3 | Change in SAIDI (%) | 32.4 | New SAIDI (min.) | 73.2 |

5.2. Guidelines for the Assessment of a Smart Grid Investment

6. Conclusions

List of Abbreviations

| BN | Business Need |

| CAIDI | Customer Average Interruption Duration Index |

| CAPEX | Capital Expenditure |

| DA | Distribution and Automation |

| DG | Distributed Generation |

| DGO | Distributed Generation Operators |

| DR | Demand Response |

| DSO | Distribution System Operators |

| EBIT | Earnings before Interests and Taxes |

| ETSP | Energy Transport service Providers |

| EV | Electric Vehicle |

| ICT | Information and Communication Technologies |

| IPP | Independent Power Producer |

| LV | Low Voltage |

| MV | Medium Voltage |

| NPV | Net Present Value |

| O&M | Operation and Maintenance |

| OCF | Operating Cash Flows |

| OPEX | Operational Expenditure |

| PLC | Power Line Communications |

| QoS | Quality of Service |

| SAIDI | System Average Interruption Duration Index |

| SAIFI | System Average Interruption Frequency Index |

| SME | Small and Medium Enterprise |

| SOA | Service Oriented Architecture |

| T&D | Transmission and Distribution |

| TSO | Transmission System Operators |

| WACC | Weighted Average Cost of Capital |

References

- Kumar, R.; Ray, P.D.; Reed, C. Smart Grid: An Electricity Market Perspective. In Proceedings of ΙEEE Power and Energy Society (PES) Conference on Innovative Smart Grid Technologies (ISGT 2011), Anaheim, CA, USA, 17–19 January 2011.

- Lesourd, J.B. Electricity: The Limits of Commodity Status. Communication. In Proceedings of Conférence sur L’ouverture des Marchés de L’éléctricité, Marseille, France, 23 January 2004.

- Ruff, L.E. Competitive Electricity Markets: Why They Are Working and How to Improve Them; Report for Harvard Electricity Policy Group: Cambridge, MA, USA, 12 May 1999. [Google Scholar]

- Fang, X.; Misra, S.; Xue, G.; Yang, D. Smart Grid—The New and Improved Power Grid: A Survey. IEEE Commun. Surv. Tutor. 2012, 14, 944–980. [Google Scholar] [CrossRef]

- The Smart Grid: Opportunities for Industry and How IEEE Can Help. Available online: http://www.ieee.org/documents/ieee_smart_grid_whitepaper_sept2011.pdf (accessed on 28 January 2013).

- Sarafi, A.M.; Tsiropoulos, G.I.; Cottis, P.G. Hybrid Wireless-Broadband over Power Lines: A Promising Broadband Solution in Rural Areas. IEEE Commun. Mag. 2009, 47, 140–147. [Google Scholar] [CrossRef]

- Power Systems Engineering Research Center. U.S. Energy Infrastructure Investment: Large-Scale Integrated Smart Grid Solutions with High Penetration of Renewable Resources, Dispersed Generation, and Customer Participation. Available online: http://www.pserc.wisc.edu/documents/publications/papers/2009_general_publications/pserc_smart_grid_white_paper_march_2009_adobe7.pdf (accessed on 28 January 2013).

- European Commission; Joint Research Centre (JRC); Institute for Energy and Transport; US Department of Energy-DOE; Office of Electricity and Energy Reliability. Assessing Smart Grid Benefits and Impacts: EU and U.S. Initiatives. Joint Report. 2012. Available online: http://ses.jrc.ec.europa.eu/assessing-smart-grid-benefits-and-impacts-eu-and-us-initiatives (accessed on 28 January 2013).

- National Energy Technology Laboratory. Understanding the Benefits of the Smart Grid. 18 June 2010. Available online: http://www.netl.doe.gov/smartgrid/referenceshelf/whitepapers/06.18.2010_Understanding%20Smart%20Grid%20Benefits.pdf (accessed on 28 January 2013). [Google Scholar]

- Yu, F.R.; Zhang, P.; Xiao, W.; Choudhury, P. Communications systems for grid integration of renewable energy resources. IEEE Netw. 2011, 25, 22–29. [Google Scholar] [CrossRef]

- Kim, Y.; Thottan, M.; Kolesnikov, V.; Wonsuck, L. A Secure Decentralized Data-Centric Information Infrastructure for Smart Grid. IEEE Commun. Mag. 2010, 48, 58–65. [Google Scholar]

- Metke, A.R.; Ekl, R.L. Security technology for smart grid networks. IEEE Trans. Smart Grids 2010, 1, 99–107. [Google Scholar] [CrossRef]

- Hart, D.G. Using AMI to realize the smart grid. In Proceedings of IEEE Power and Energy Society General Meeting 2008—Conversion and Delivery of Electrical Energy in the 21st Century, Pittsburgh, PA, USA, 20–24 July 2008; pp. 1–2.

- Roozbehani, M.; Dahleh, M.; Mitter, S. Dynamic pricing and stabilization of supply and demand in modern electric power grids. IEEE Smart Grid Comm. 2010, 10, 543–548. [Google Scholar]

- Casazza, J.; Delea, F. Understanding Electric Power Systems: An Overview of the Technology and the Marketplace; John Wiley and Sons, Inc.: Hoboken, NJ, USA, 2003; ISBN 0-471-44652-1. [Google Scholar]

- Rahimi, F.; Ipakchi, A. Demand response as a market resource under the smart grid paradigm. IEEE Trans. Smart Grid 2010, 1, 82–88. [Google Scholar] [CrossRef]

- Van Werven, M.J.N.; Scheepers, M.J.J. Dispower: The Changing Role of Energy Suppliers and Distribution System Operators in the Deployment of Distributed Generation in Liberalized Electricity Markets. ECN-C-05-048. June 2005. Available online: http://www.ecn.nl/docs/library/report/2005/c05048.pdf (accessed on 28 January 2013).

- EURELECTRIC. The Role of DSOs on Smart Grids and Energy Efficiency. A EURELECTRIC position paper. January 2012. Available online: http://www.eurelectric.org/media/26860/final_the_role_of_dsos_on_sg__ee-13_january_sd-2012-030-0025-01-e.pdf (accessed on 28 January 2013).

- Nykamp, S.; Andor, M.; Hurink, J.L. Standard incentive regulation hinders the integration of renewable energy generation. Energy Policy 2012, 47, 222–237. [Google Scholar] [CrossRef]

- Bauknecht, D. Incentive Regulation and Network Innovations; EUI Working Paper RSCAS 2011/02. European University Institute, Florence, Robert Schuman Centre for Advanced Studies, Loyola de Palacio Programme on Energy Policy. Available online: http://cadmus.eui.eu/handle/1814/15481 (accessed on 28 January 2013).

- Gungor, V.C.; Lambert, F.C. A Survey on communication networks for electric system automation. Comput. Netw. 2006, 50, 877–897. [Google Scholar] [CrossRef]

- Jih, S.; Yin, M.-L. An Availability Analysis on SONET Ring Networks in Power Grid Communications. In Proceedings of Annual Reliability and Maintainability Symposium (RAMS), Reno, NV, USA, 23–26 January 2012.

- Lazaropoulos, A.G.; Cottis, P.G. Capacity of overhead medium voltage power line communication channels. IEEE Trans. Power Deliv. 2010, 25, 723–733. [Google Scholar] [CrossRef]

- Lazaropoulos, A.G.; Cottis, P.G. Broadband bia underground medium voltage power lines—Part II: Capacity. IEEE Trans. Power Deliv. 2010, 25, 2425–2434. [Google Scholar] [CrossRef]

- Gungor, V.C.; Sahin, D.; Kocak, T.; Ergüt, S.; Buccella, C.; Cecati, C.; Hancke, G.P. Smart grid technologies: Communication technologies and standards. IEEE Trans. Ind. Inf. 2011, 7, 529–539. [Google Scholar] [CrossRef]

- European Commission. Electricity Utilities and Telecom Companies. In Proceedings of 2nd EC-Utilities-Telecom Workshop, Brussels, Belgium, 5 October 2011.

- European Landscape Report 2012. Available online: http://www.smartregions.net/default.asp?SivuID=26927 (accessed on 29 January 2013).

- Blazewicz, S.; Shlatz, G.; Small, F.; Tobias, S.; Bean, J.; (Navigant Consulting Inc). The Value of Distribution Automation; California Energy Commission, PIER Energy Systems Integration Program CEC-500-2007-103. , 2008. Available online: http://www.ilgridplan.org/Shared%20Documents/CEC%20PIER%20Report%20-%20The%20Value%20of%20Distribution%20Automation.pdf (accessed on 28 January 2013).

- Sullivan, M.; Schellenberg, J. How to Assess the Economic Consequences of Smart Grid Reliability Investments; Report for Miles Keogh National Association of Regulatory Utility Commissioners; Washington, DC, USA, 29 November 2010. [Google Scholar]

- Baer, W.S.; Fulton, B.; Mahnovski, S. Estimating the Benefits of the Grid Wise Initiative; Report for the Pacific Northwest National Laboratory; Richland, WA, USA, 2004; TR-160-PNNL. [Google Scholar]

- Electric Power Research Institute (EPRI). Methodological Approach for Estimating the Benefits and Costs of Smart Grid Demonstration Projects; Final Report; U.S. Department of Energy, Electric Power Research Institute: Palo Alto, CA, USA, January 2010; Available online: http://www.smartgridnews.com/artman/uploads/1/1020342EstimateBCSmartGridDemo2010_1_.ppd (accessed on 28 January 2013).

- Electric Power Research Institute (EPRI). Estimating the Costs and Benefits of the Smart Grid: A Preliminary Estimate of the Investment Requirements and the Resultant Benefits of a Fully Functioning Smart Grid; 2011 Technical Report; U.S. Department of Energy, Electric Power Research Institute: Palo Alto, CA, USA, March 2011; Available online: http://www.sgiclearinghouse.org/node/3272 (accessed on 28 January 2013).

- Electric Power Research Institute (EPRI). The Cost of Power Disturbances to Industrial and Digital Economy Companies. Submitted to EPRI’s Consortium for Electric Infrastructure for a Digital Society, (CEIDS). 29 June 2001. Available online: http://www.onpower.com/pdf/EPRICostOfPowerProblems.pdf (accessed on 28 January 2013).

- Elmakias, D. Reliability of distribution systems. Stud. Comput. Intell. 2008, 111, 373–404. [Google Scholar]

- Elmakias, D. Basic Notions of power system reliability. Stud. Comput. Intell. 2008, 111, 1–53. [Google Scholar]

- Moslehi, K.; Kumar, R. Smart Grid—A Reliability Perspective Paper. In Proceedings of IEEE Power and Energy Society (PES) Conference on “Innovative Smart Grid Technologies”, Washington, DC, USA, 19–20 January 2010.

- McGranaghan, M.; Goodman, F. Technical and system requirements for advanced distribution automation. In Proceedings of 18th International Conference and Exhibition on Electricity Distribution, Turin, Italy, 6–9 June 2005; pp. 1–5.

- Tumilty, R.M.; Elders, I.M.; Burt, G.M.; McDonald, J.R. Coordinated protection, control & automation schemes for microgrids. Int. J. Distrib. Energy Resour. 2007, 3, 225–241. [Google Scholar]

- Allan, R.N.; Borkowska, B.; Grigg, C.H. Probabilistic analysis of power flows. Proc. Inst. Electr. Eng. 1974, 121, 1551–1556. [Google Scholar] [CrossRef]

- Dopazo, J.F.; Klitin, O.A.; Sasson, A.M. Stochastic load flows. IEEE Trans. Power Appl. Syst. 1975, 94, 299–309. [Google Scholar] [CrossRef]

- Anderson, R.N.; Boulanger, A.; Powell, W.B.; Scott, W. Adaptive stochastic control for the smart grid. Proc. IEEE 2011, 99, 1098–1115. [Google Scholar] [CrossRef]

- Bu, S.; Yu, F.R.; Liu, P.X. Stochastic unit commitment in smart grid communications. In Proceedings of IEEE 2011 International Conference on Computer Communications INFOCOM) Workshop on Green Communications and Networking, Shanghai, China, 10–15 April 2011; pp. 307–312.

- He, M.; Murugesan, S.; Zhang, J. Multiple timescale dispatch and scheduling for stochastic reliability in smart grids with wind generation integration. In Proceedings of IEEE International Conference on Computer Communications (INFOCOM) Mini-Conference, Shanghai, China, 10–15 April 2011; pp. 461–465.

- Parvania, M.; Fotuhi-Firuzabad, M. Demand response scheduling by stochastic SCUC. IEEE Trans. Smart Grid 2010, 1, 89–98. [Google Scholar] [CrossRef]

- National Energy Technology Laboratory. Building a Smart Grid Business Case; Report for the U.S. Department of Energy Office of Electricity Delivery and Energy Reliability; Palo Alto, CA, USA, August 2009. [Google Scholar]

- EURELECTRIC Comments on ERGEG Position Paper on Smart Grids. A EURELECTRIC position paper. March 2010. Available online: http://www.eurelectric.org/media/43983/eurelectric_pp_ergeg_smart_grids_final-2010-230-0001-01-e.pdf (accessed on 28 January 2013).

- LaCommare, K.H.; Eto, J.H. Cost of Power Interruptions to Electricity Consumers in the United States (U.S.); LBNLL: Berkeley, CA, USA, 2006. [Google Scholar]

- De Nooij, M.; Koopmans, C.; Bijvoet, C. The value of supply security: The costs of power interruptions: Economic input for damage reduction and investment in networks. Neth. Energy Econ. 2007, 29, 277–295. [Google Scholar] [CrossRef]

- Giordano, V.; Onyeji, I.; Fulli, G.; Jimenez, M.S.; Filiou, C. Guidelines for Conducting a Cost-Benefit Analysis of Smart Grid Projects. Report No. EUR 25246 EN. Available online: http://ec.europa.eu/energy/gas_electricity/smartgrids/doc/20120427_smartgrids_guideline.pdf (accessed on 28 January 2013).

- Bouhouras, A.S.; Labridis, D.P.; Bakirtzis, A.G. Cost/worth assessment of reliability improvement in distribution networks by means of artificial intelligence. Electr. Power Energy Syst. 2010, 32, 530–538. [Google Scholar] [CrossRef]

- Chun-Lien, S.; Jen-Ho, T. Outage costs quantification for benefit–cost analysis of distribution automation systems. Int. J. Electr. Power Energy Syst. 2007, 29, 767–774. [Google Scholar] [CrossRef]

- Bushnell, J.B.; Soft, S.E. Improving private incentives for electric grid investment. Resour. Energy Econ. 1997, 19, 85–108. [Google Scholar] [CrossRef]

- Kalagnanam, G.J.; Katz, D.; Squillante, M.; Zhang, X.; Feinberg, E. Incentive design for lowest cost aggregate energy demand reduction. In Proceedings of 2010 First IEEE International Conference on Smart Grid Communications (SmartGridComm), Yorktown Heights, NY, USA, 4–6 October 2010; pp. 519–524.

© 2013 by the authors; licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution license (http://creativecommons.org/licenses/by/3.0/).

Share and Cite

Livieratos, S.; Vogiatzaki, V.-E.; Cottis, P.G. A Generic Framework for the Evaluation of the Benefits Expected from the Smart Grid. Energies 2013, 6, 988-1008. https://doi.org/10.3390/en6020988

Livieratos S, Vogiatzaki V-E, Cottis PG. A Generic Framework for the Evaluation of the Benefits Expected from the Smart Grid. Energies. 2013; 6(2):988-1008. https://doi.org/10.3390/en6020988

Chicago/Turabian StyleLivieratos, Spiros, Vasiliki-Emmanouela Vogiatzaki, and Panayotis G. Cottis. 2013. "A Generic Framework for the Evaluation of the Benefits Expected from the Smart Grid" Energies 6, no. 2: 988-1008. https://doi.org/10.3390/en6020988